In chaos theory, there’s a concept known as the butterfly effect—the idea that a seemingly small action, occurring at just the right moment, can trigger ripple effects that grow across time and space. A butterfly flaps its wings in Brazil, the saying goes, and a tornado forms weeks later in Texas.

Presidential decisions can carry the same weight, especially those made in the first 100 days of a new administration. Time and again, these early choices unleash far-reaching consequences that reshape a nation.

As Donald Trump wraps up the opening stretch of his second term, his healthcare-focused executive actions underscore the consequentiality of this early window. And when compared with Barack Obama’s approach in 2009 (the last time a president pursued major healthcare reforms right out of the gate), the contrast becomes even more striking.

Two presidents. Two defining moments. And one fundamental question that both men had to answer in the first 100 days: Where should healthcare reform begin — by expanding coverage, improving quality or cutting costs?

Crisis, Control And A Key Healthcare Choice

The idea that a president’s first 100 days matter dates back to Franklin D. Roosevelt. In 1933, during the depths of the Great Depression, FDR passed a wave of New Deal reforms that redefined the role of government in American life.

Ever since, the opening months of a new presidency have served as both proving ground and preview. They reveal how a president intends to govern and what he values most.

For both presidents Obama and Trump, their answer to the healthcare question — where to begin? — would shape what followed. Obama chose to expand coverage. Trump has chosen to cut costs. Those decisions set them on opposing paths. And with every subsequent policy decision, the gap between their contrasting approaches only grows.

’09 Obama: Health Coverage And Congressional Action

In the quiet calculus of early governance, President Obama concluded that without health insurance coverage, access to high-quality medical care would remain out of reach for tens of millions of Americans.

Confronting a system that left 60 million uninsured, he believed that expanding access to coverage was a vital first step — not only to improve individual health outcomes, but to create a healthier nation that ultimately would require less medical care (and spending) overall.

That belief was grounded in lived experience: his mother’s battle with cancer and the insurance disputes that followed, as well as his years as a community organizer working with families who couldn’t afford medical care.

He also understood that only Congressional legislation — rather than executive action — would make those gains durable. So, in his first 100 days, he pursued a strategy grounded in consensus-building. He convened healthcare stakeholders, hosted public healthcare summits, expanded the Children’s Health Insurance Program (CHIP) and proposed a federal budget that included a $634 billion “down payment” on healthcare reform.

’25 Trump: Cost Cutting And Executive Control

Donald Trump didn’t ease into his second term. He charged in, pen in hand. His priorities for the country were clear: cut taxes, impose tariffs and reduce federal spending.

For Trump, speed was of the essence. So, he bypassed Congress in favor of executive orders, downsizing healthcare agencies and dismantling regulatory oversight wherever possible.

At the center of Trump’s domestic agenda is an ambitious income tax overhaul, dubbed the “big beautiful bill.” But passing it will require support from fiscal conservatives in his own party. To offset the steep drop in tax revenue, Trump has signaled a willingness to slash federal spending, starting with healthcare programs.

What Comes Next: Mapping Health Policy Consequences

Presidents make thousands of decisions over the course of a four-year term, but those made in the first few months typically matter most. Both Obama and Trump had to decide whether to prioritize expanding coverage or cutting costs, and that choice would shape the steps that follow.

For Obama, the consequences of his choice were sweeping. His early focus on increasing health insurance coverage laid the foundation for the Affordable Care Act, the most ambitious healthcare reform since Medicare and Medicaid in the 1960s. The ACA provided affordable insurance to more than 30 million Americans, offered subsidies to low- and middle-income families, cut the uninsured rate in half and guaranteed protections for those with preexisting conditions. The law survived political opposition, legal challenges and subsequent presidencies.

Trump’s early decisions are reshaping healthcare, too, but in ways that reflect a very different set of priorities and a sharply contrasting vision for the federal government’s role.

1. Cost-Driven Actions: Reducing Government Healthcare Spending

Guided by a business-oriented focus on cost containment, Trump has sought to reduce the federal government’s role in healthcare through sweeping budget and staffing changes. Among the most significant:

Agency layoffs: The Department of Health and Human Services has initiated mass layoffs across the CDC, NIH and FDA, reducing staff capacity by 20,000 and cutting critical programs, including HIV research grants and initiatives targeting autism, chronic disease, teen pregnancy and substance abuse.

ACA support rollbacks: The administration slashed funding for ACA navigators and rescinded extended enrollment periods, making it more difficult for individuals (especially low-income Americans) to obtain coverage.

Planned Parenthood and family planning cuts: Freezing Title X funds has reduced access to reproductive healthcare in multiple states.

Medicaid at risk: A proposed $880 billion reduction over 10 years could eliminate expanded Medicaid coverage in many states. Additional moves (like work requirements or application hurdles) would likely reduce enrollment further.

2. Cultural And Executive Power Moves: Redefining Government’s Role In Health

While cutting costs has been the central goal, many of Trump’s actions reflect a broader ideological stance. He’s using executive authority to reshape the values, norms and institutions that have defined American healthcare. These include:

Withdrawal from the World Health Organization (WHO): The administration formally ended U.S. participation, citing concerns about funding and governance.

Restructuring USAID’s health portfolio: Multiple contracts and programs related to maternal health, infectious disease prevention and international public health have been ended or scaled back.

Policy changes on federal language and research topics: Executive directives have modified how agencies are allowed to address topics related to gender and sexuality, leading to the removal of LGBTQ+ content from health resources and websites.

Reorganization of DEI programs: Diversity, equity and inclusion initiatives have been rolled back or eliminated across several federal departments.

The Likely Consequences Of Trump’s First 100 Days

President Trump’s early actions reveal two defining trends: cutting government healthcare spending and reshaping federal priorities through executive authority. Both are already changing how care is accessed, funded and delivered. And both are likely to produce lasting consequences.

The most immediate impact will come from efforts to reduce healthcare spending. Cuts to Medicaid, ACA enrollment support and family planning programs are expected to lower insurance enrollment, particularly among low-income families, young adults and people with chronic illness.

As coverage declines, care becomes harder to access and more expensive when it’s needed. The results: delayed diagnoses, avoidable complications and rising levels of uncompensated care.

His second set of actions — including reduced investment in federal science agencies — will slow drug development and weaken the infrastructure needed to respond to future public health threats.

Meanwhile, a more constrained and domestically focused healthcare agenda is likely to diminish trust in federal health agencies, limit access to culturally competent care and produce a loss of global leadership in health innovation.

The U.S. Constitution gives presidents broad power to chart the nation’s course. And the decisions made in their first 100 days shape the trajectory of an entire presidency.

One president decided to prioritize coverage, while a second chose cost-cutting. And like the flap of a butterfly’s wings, these early actions generate ripples — expanding in size over time and radically altering American healthcare, for better or worse.

Most Americans believe their healthcare is private, and the majority prefers it that way. Gallup polling shows more Americans favor a system based on private insurance rather than government-run healthcare.

But here’s a surprising reality: 91% of Americans receive government-subsidized healthcare.

Unless you’re among the uninsured or the few who receive no subsidies, government dollars are helping pay your medical bills — whether your insurance comes from an employer, a privately managed care organization or the online marketplace.

Now, as lawmakers face mounting budget pressures, those subsidies (and your coverage) could be at risk. If the government scales back its healthcare spending, your medical costs could skyrocket.

Here’s a closer look at the five ways the U.S. government funds healthcare. If you have health insurance, you’re almost certainly benefiting from one of them:

Medicare, the government-run healthcare program for those 65 and older, covers 67 million Americans at a cost of more than $1 trillion annually. Approximately half of enrollees are covered through the traditional fee-for-service plan and the other half in privately managed Medicare Advantage plans.

Medicaid and CHIP provide health coverage for around 80 million low-income and disabled Americans, including tens of millions of children. Even though 41 states have turned over their Medicaid programs over to privately managed care organizations, the cost remains public. Total Medicaid spending is $900 billion annually — the federal government pays 70% with states footing the rest.

The online healthcare marketplace is for Americans whose employer doesn’t provide medical coverage or who are self-employed. This Affordable Care Act program offers federal subsidies to 92% of its 23 million enrollees, which help lower the cost of premiums and, for many, subsidize their out-of-pocket expenses. The Congressional Budget Office projects that a permanent extension of these subsidies, which are scheduled to end this year, would cost $383 billion over the next 10 years.

Veterans and military families also benefit from government healthcare through TRICARE and VA Care, programs covering roughly 16 million individuals at a combined cost of $148 billion for the federal government annually.

Employer-sponsored health insurance comes with a significant, yet often overlooked, government subsidy. For nearly 165 million American workers and their families, U.S. companies pay the majority of their health insurance premiums. However, those dollars are excluded from employees’ taxable income. This tax break, which originated during World War II and was formally codified in the 1950s, subsidizes workers at an annual government cost of approximately $300 billion. For a typical family of four, this translates into approximately $8,000 per year of added take-home pay.

With 91% of Americans receiving some form of government healthcare assistance, the idea that U.S. healthcare is predominantly “private” is an illusion.

Now, as the new administration searches for ways to rein in the growing federal deficit, all five of these programs (collectively funding healthcare for 9 in 10 Americans) will be in the crosshairs.

Twelve percent of the federal budget already goes toward debt interest payments, and this share is expected to rise sharply. Many of the bonds used to finance existing debt were issued back when interest rates were much lower. As those bonds mature and are refinanced at today’s higher rates, federal interest payments are projected to double within the next decade, according to the Congressional Budget Office.

With deficits mounting and borrowing costs soaring, most economists agree this trajectory is unsustainable. Lawmakers will eventually need to rein in spending, and healthcare subsidies will almost certainly be among the first targets. Policy experts predict Medicaid, which the House has already proposed cutting by $880 billion over the next decade, and ACA subsidies for out-of-pocket costs will likely be the first on the chopping block. But given the CBO’s projections, these cuts won’t be the last.

A Better Way: Three Solutions To Lower Healthcare Costs Without Cuts

Cutting some or all of these healthcare subsidies may seem like the simplest way to reduce the deficit. In reality, it merely shifts costs elsewhere, making medical care more expensive for everyone and increasing future government spending. Here’s why:

Eliminating subsidies doesn’t eliminate the need for care. Under the Emergency Medical Treatment and Labor Act (EMTALA), hospitals must treat emergency patients regardless of their ability to pay. When millions lose insurance, more turn to ERs for medical care they can’t afford. The cost of that uncompensated care doesn’t vanish. It gets passed on to state governments, hospitals and privately insured patients through higher taxes, inflated hospital bills and rising insurance premiums.

Delaying care drives up long-term costs. People who can’t afford doctor visits skip preventive care, screenings and early treatments. Manageable conditions like high blood pressure and diabetes then spiral into costly, life-threatening complications including heart attacks, strokes and kidney failures, which ultimately increase government spending.

The solution isn’t cutting coverage. It’s fixing the root causes of high healthcare costs. Here are three ways to achieve this:

1. Address The Obesity Epidemic

Obesity is a leading driver of diabetes, heart disease, stroke and breast cancer, which kill millions of Americans and cost the U.S. healthcare system hundreds of billions annually. Congress can take two immediate steps to reverse this crisis:

Tax high-calorie, highly processed foods and use the revenue to subsidize healthier options, making nutritious food more affordable for all Americans.

2. Enhance Chronic Disease Management With Technology

In every other industry, broad adoption of generative AI technology is already increasing quality while reducing costs. Healthcare could do the same by applying generative AI to more effectively manage chronic disease. According to the Centers for Disease Control and Prevention, improved control of these lifelong conditions could cut the frequency of heart attacks, strokes, kidney failures and cancers by up to 50%.

With swift and reasonable Food and Drug Administration approval, generative AI and wearable monitors would revolutionize how these conditions are managed, providing real-time updates on patient health and identifying when medications need adjustment. Instead of waiting months for their next in-office visit, patients with chronic diseases would receive continuous monitoring, preventing costly and life-threatening complications. Rather than restricting AI’s role in healthcare, Congress can streamline the FDA’s approval process and allocate National Institutes of Health funding to accelerate these advancements.

3. Reform Healthcare Payment Models

Under today’s fee-for-service system, doctors and hospitals are paid based on the how often they see patients for the same problem and the number of procedures performed. This approach rewards the volume of care, not the best and most effective treatments. A better alternative is a pay-for-value model like capitation, in which providers do best financially when they help keep patients healthy. To encourage participation, Congress should fund pilot programs and create financial incentives for insurers, doctors and hospitals willing to transition to this system. By aligning financial incentives with long-term health, this model would encourage doctors to prioritize prevention and effective chronic disease control, ultimately lowering medical costs by improving overall health.

The Time For Change Is Now

If Congress slashes healthcare subsidies this year, restoring them will be nearly impossible. Once the cuts take effect, the financial and political pressures driving them will only intensify, making reversal unlikely.

The voices shaping this debate can’t come solely from industry lobbyists. Elected officials need to hear from the 91% of Americans who rely on government healthcare assistance for some or all of their medical coverage. Now is the time to speak up.

The massive Republicanbudget bill working its way through Congress has mostly drawn attention for its tax cuts and Medicaid changes.

But it would also take steps to significantly roll back coverage under the Affordable Care Act, with echoes of the 2017 repeal-replace debate.

Why it matters:

The bill that passed the House before Memorial Day includes an overhaul of ACA marketplaces that would result in coverage losses for millions of Americans and savings to help cover the cost of extending President Trump’s tax cuts, Peter Sullivan wrote first on Pro.

It comes after a growth spurt that saw ACA marketplace enrollment reach new highs, with more than 24 million people enrolling for 2025, according to KFF. The House’s changes would likely reverse that trend, unless the Senate goes in a different direction when it picks up the bill next week.

Driving the news:

The changes are not as sweeping as the 2017 effort at repealing the law, but many of them erect barriers to enrollment that supporters say are aimed at fighting fraud.

Brian Blase, president of Paragon Health Institute and a health official in Trump’s first administration, said Republicans are focusing on rolling back Biden-era expansions “that have led to massive fraud and inefficiency.”

The Congressional Budget Office estimates the ACA marketplace-related provisions would lead to about 3 million more people becoming uninsured.

Cynthia Cox, a vice president at KFF, said while the changes “sound very technical” in nature, taken together “the implications are that it will be much harder for people to sign up for ACA marketplace plans.”

What’s inside:

The bill would end automatic reenrollment in ACA plans for people getting subsidies, instead requiring them to proactively reenroll and resubmit information about their incomes for verification.

It would also prevent enrollees from provisionally receiving ACA subsidies in instances where extra eligibility checks are needed, which can take months.

If people wound up making more income than they had estimated for a given year, the bill removes the cap on the amount of ACA subsidies they would have to repay to the government.

Some legal immigrants would also be cut off from ACA subsidies, including people granted asylum and those in their five-year waiting period to be eligible for Medicaid.

What they’re saying:

In a letter to Congress, patient groups pointed to the various barriers as “unprecedented and onerous requirements to access health coverage” that would have “a devastating impact on people’s ability to access and afford private insurance coverage.”

The letter was signed by groups including the American Cancer Society Cancer Action Network, American Diabetes Association and American Lung Association.

Between the lines:

A last-minute addition to the bill would also make a technical but important change that increases government payments to insurers in ACA marketplaces.

That would have the effect of reducing the subsidies that help people afford premiums and save the government money, by reducing the benchmark silver premiums that are used to set the subsidy amounts.

Democrats are concerned that if Congress also allows enhanced ACA subsidies to expire at the end of this year, the combined effect would be even higher premium increases for enrollees next year.

Insurers that already are planning their premium rates for next year say the Republican funding changesare throwing uncertainty into the mix.

“Disruption in the individual market could also result in much higher premiums,” the trade group AHIP warned in a statement on the bill.

The big picture:

Blase said changes like ending automatic reenrollment are needed to increase checks that ensure people are not claiming higher subsidies than they’re entitled to.

Cox said another way to address fraud would be to target shady insurance brokers, rather than enrollees themselves. She estimated that marketplace enrollment could fall by roughly one-third from all the changes together.

“The justification for many of these provisions is to address fraud,” she said. “The question is, how many people who are legitimately signed up are going to get lost in that process?”

This week, the House Energy and Commerce and Ways and Means Committees begins work on the reconciliation bill they hope to complete by Memorial Day. Healthcare cuts are expected to figure prominently in the committee’s work.

And in San Diego, America’s Physician Groups (APG) will host its spring meeting “Kickstarting Accountable Care: Innovations for an Urgent Future” featuring Presidential historian Dorris Kearns Goodwin and new CMS Innovation Center Director Abe Sutton. Its focus will be the immediate future of value-based programs in Trump Healthcare 2.0, especially accountable care organizations (ACOs) and alternative payment models (APMs).

Central to both efforts is the administration’s mandate to reduce federal spending which it deems achievable, in part, by replacing fee for services with value-based payments to providers from the government’s Medicare and Medicaid programs.

The CMS Center for Medicare and Medicaid Innovation (CMMI) is the government’s primary vehicle to test and implement alternative payment programs that reduce federal spending and improve the quality and effectiveness of services simultaneously.

Pledges to replace fee-for-service payments with value-based incentives are not new to Medicare. Twenty-five years ago, they were called “pay for performance” programs and, in 2010, included in the Affordable Care as alternative payment models overseen by CMMI.

But the effectiveness of APMs has been modest at best: of 50+ models attempted, only 6 proved effective in reducing Medicare spending while spending $5.4 billion on the programs. Few were adopted in Medicaid and only a handful by commercial payers and large self-insured employers. Critics argue the APMs were poorly structured, more costly to implement than potential shared savings payments and sometimes more focused on equity and DEI aims than actual savings.

The question is how the Mehmet Oz-Abe Sutten version of CMMI will approach its version of value-based care, given modest APM results historically and the administration’s focus on cost-cutting.

Context is key:

Recent efforts by the Trump Healthcare 2.0 team and its leadership appointments in CMS and CMMI point to a value-agenda will change significantly. Alternative payment models will be fewer and participation by provider groups will be mandated for several. Measures of quality and savings will be fewer, more easily measured and and standardized across more episodes of care. Financial risks and shared savings will be higher and regulatory compliance will be simplified in tandem with restructuring in HHS, CMS and CMMI to improve responsiveness and consistency across federal agencies and programs.

Sutton’s experience as the point for CMMI is significant. Like Adam Boehler, Brad Smith and other top Trump Healthcare 2.0 leaders, he brings prior experience in federal health agencies and operating insight from private equity-backed ventures (Honest Health, Privia, Evergreen Nephrology funded through Nashville-based Rubicon Founders). Sutton’s deals have focused on physician-driven risk-bearing arrangements with Medicare with funding from private investors.

The Trump Healthcare 2.0 team share a view that the healthcare system is unnecessarily expensive and wasteful, overly-regulated and under-performing. They see big hospitals and drug companies as complicit—more concerned about self-protection than consumer engagement and affordability.

They see flawed incentives as a root cause, and believe previous efforts by CMS and CMMI veered inappropriately toward DEI and equity rather than reducing health costs.

And they think physicians organized into risk bearing structures with shared incentives, point of care technologies and dependable data will reduce unnecessary utilization (spending) and improve care for patients (including access and affordability).

There’s will be a more aggressive approach to spending reduction and value-creation with Medicare as the focus: stronger alternative payment models and expansion of Medicare Advantage will book-end their collective efforts as Trump Healthcare 2.0 seeks cost-reduction in Medicare.

What’s ahead?

Trump Healthcare 2.0 value-based care is a take-no prisoners strategy in which private insurers in Medicare Advantage have a seat at their table alongside hospitals that sponsor ACOs and distribute the majority of shared savings to the practicing physicians. But the agenda will be set, and re-set by the administration and link-minded physician organizations like America’s Physician Groups and others that welcome financial risk-sharing with Medicare and beyond.

The results of the Trump Healthcare 2.0 value agenda will be unknown to voters in the November 2026 mid-term but apparent by the Presidential campaign in 2028. In the interim, surrogate measures for performance—like physician participation and projected savings–will be used to show progress and the administration will claim success. It will also spark criticism especially from providers who believe access to needed specialty care will be restricted, public and rural health advocates whose funding is threatened, teaching and clinical research organizations who facing DOGE cuts and regulatory uncertainty, patient’s right advocacy groups fearing lack of attention and private payers lacking scalable experience in Medicare Advantage and risk-based relationships with physicians.

Last week, the American Medical Association named Dr. John Whyte its next President replacing widely-respected 12-year CEO/EVP Jim Madara. When he assumes this office in July, he’ll inherit an association that has historically steered clear of major policy issues but the administration’s value-based care agenda will quickly require his attention.

Physicians including AMA members are restless:

At last fall’s House of Delegates (HOD), members passed a resolution calling for constraints on not-for-profit hospital’ tax exemptions due to misleading community benefits reporting and more consistency in charity care reporting by all hospitals.

The majority of practicing physicians are burned-out due to loss of clinical autonomy and income pressures—especially the 75% who are employees of hospitals and private-equity backed groups. And last week, the American College of Physicians went on record favoring “collective action” to remedy physician grievances. All impact the execution of the administration’s value-based agenda.

Arguably, the most important key to success for the Trump Healthcare 2.0 is its value agenda and physician support—especially the primary care physicians on whom the consumer engagement and appropriate utilization is based. It’s a tall order.

The Trump Healthcare 2.0 value agenda is focused on near-term spending reductions in Medicare. Savings in federal spending for Medicaid will come thru reconciliation efforts in Congress that will likely include work-requirements for enrollees, elimination of subsidies for low-income adults and drug formulary restrictions among others. And, at least for the time being, attention to those with private insurance will be on the back burner, though the administration favors insurance reforms adding flexible options for individuals and small groups.

The Trump Healthcare 2.0 value-agenda is disruptive, aggressive and opportunistic for physician organizations and their partners who embrace performance risk as a permanent replacement for fee for service healthcare. It’s a threat to those that don’t.

In what’s becoming an all-too-familiar pattern, CVS Health announced it will pull Aetna out of the Affordable Care Act (ACA) marketplace in 2026, leaving about a million people across 17 states searching for new health coverage — and in some cases, fighting to afford any at all.

This marks yet another retreat by a major for-profit insurer from a program designed to provide affordable health coverage to Americans who don’t get it through work. CVS made the announcement while simultaneously celebrating a 60% increase in quarterly profit and revealing a new deal to boost sales of the pricey weight-loss drug Wegovy through its pharmacy and pharmacy benefit manager (PBM) arms.

Let me repeat that: Aetna is exiting the ACA because it claims it can’t make enough money on people enrolled in those plans, on the same day its parent company posted nearly $1.8 billion in profits in just the first three months of this year.

This is the same company, by the way, that dumped hundreds of thousands of seniors and disabled people at the end of 2024 because some of them were using more medical care than Wall Street found acceptable. If this doesn’t tell you everything you need to know about who the health insurance industry is really working for, I don’t know what will.

From “Commitment” to Abandonment

Aetna first bailed on the ACA exchanges in 2018, then re-entered in 2022 when insurers could see more clearly how they could make significant profits on that book of business. Now, after just a few years of moderate participation, it’s heading for the exits again. CVS Health executives blamed “regulatory uncertainty” and “highly variable economic factors,” according to a statement to The Columbus Dispatch.

But make no mistake—this was a cold business calculation. Uncertainties and economic variabilities are constants in the insurance game.

CVS’ CEO David Joyner told investors:

“We are disappointed by the continued underperformance from our individual exchange products … this is not a decision we made lightly.”

That’s corporate-speak for “our Wall Street friends weren’t impressed.”

Aetna’s ACA exchange business, covering roughly 1 million people, is just a sliver of CVS’ overall medical membership of 27.1 million. But even though the profits weren’t massive, the people depending on this coverage — many of them self-employed, working multiple part-time jobs, or recently uninsured — will now be thrown into chaos.

And it’s happening at a time when health insurance for many Americans hangs by a thread. Unless Congress acts in the coming months, the ACA’s enhanced tax subsidies—first implemented under the American Rescue Plan—are set to expire at the end of this year.Without them, premiums could spike by 50% to 100% depending on income and geography.

The Congressional Budget Office projects that the lapse in subsidies could leave 3.8 million more Americans uninsured— and now, 1 million more will be forced to find new plans as CVS/Aetna walks away.

Same Song: Prioritizing Profit, Not Patients

Let’s be clear about what CVS is doing here: It’s ditching an essential safety net for millions in order to chase higher profits elsewhere—most notably, in the exploding market for GLP-1 drugs like Wegovy. On the same day it abandoned the ACA, CVS announced a new deal to give Wegovy preferred placement on its PBM formulary, displacing Eli Lilly’s Zepbound. This will help CVS dominate the obesity drug market—and rake in profits through its Caremark PBM and nearly 9,000 retail pharmacies.

It’s a powerful example of vertical integration in action.

CVS owns the insurer (Aetna), the PBM (Caremark), and the pharmacy (CVS retail stores). When it walks away from lower-margin business like ACA plans and doubles down on high-dollar drug deals, we see its true priorities: selling expensive drugs, saddling individuals, families and employers with the costs, and keeping Wall Street happy.

Even worse, the decision is taking place against a troubling political backdrop. The Trump administration has already taken steps to undermine ACA infrastructure and expressed skepticism toward core public health programs. Cuts to navigator funding, changes to vaccine guidelines, and looming uncertainty around tax credits are all part of a slow-motion sabotage of the ACA. This is not to say that the ACA doesn’t have its flaws that need to be addressed.

But instead of penalizing hard-working Americans and their families, lawmakers and the Trump administration should focus instead on lowering the ridiculously high out-of-pocket maximum that the ACA established (and that keeps going up every year) and fixing the medical loss ratio provision that has fueled the vertical integration in the insurance industry.

Hi, everybody. I’m Elizabeth Wilkins, president and CEO of the Roosevelt Institute, and I am delighted to be here today with some big news and a very special guest. I am thrilled to announce that Nobel Prize–winning economist Paul Krugman will be joining the Roosevelt Institute as a senior fellow. Paul is one of the world’s most cited economists and widely read commentators, and for good reason. His longtime New YorkTimes column and his Substack now prove that he is not just a bold thinker, he is one of the clearest and most dynamic communicators in the field—skills that come in handy when you want to break through the noise of this moment and get people thinking about what the future of our economy and democracy might look like. And, of course, this is what Roosevelt is all about: understanding where we are in the moment and where we need to go.

So, Paul, I’m so excited to talk with you today. I started at Roosevelt in February, so we’re both new kids on the block here, and I will start with a question that I am getting a lot recently: Why your interest in affiliating with Roosevelt, and why now?

Paul Krugman:

Well, now I think because partly having retired from the New York Times, I’m free to pursue other affiliations. The Times is kind of a jealous organization. But now that I’m no longer there, I can do this. Roosevelt has been a tremendous reservoir of progressive thinking and progressive economics. I was heavily reliant on Roosevelt research particularly during the aftermath of the 2008 financial crisis—I’ve been around for a while here. [There’s] still novel stuff going on, and this seemed like a good affiliation to have in these times, to join the ranks of people with Roosevelt affiliations who have been providing really urgent commentary.

Elizabeth:

Thank you for the kind words. We appreciate it. One of the things that made your Times column such a hit for decades was the unique voice that you bring to economics: your ability to break down orthodoxy and cut to the core of what’s happening in plain terms. It almost goes without saying that there is a lot to cut through right now. We’ve seen attacks on government programs and on whole government agencies. And as you have noted and I have noted, the fate of Social Security and our social compact hangs in the balance right now. So, can you talk—with a little bit of your perspective on economic history—about what you think makes this moment unique? And through all this noise, what people should be paying attention to, and why?

Paul:

We are in a moment where we’ve lived, really since the New Deal in—whatever you want to call it—the Keynesian consensus. We’ve lived in a world where, we by no means went to socialism, but we had capitalism with some of the rough edges sanded off. Not as many of the rough edges that I would like, but we have Social Security, we’ve had Medicare since the 60s. We have Medicaid. We have the Affordable Care Act. We have a whole bunch of social insurance programs. We have government efforts to at least somewhat regulate the excesses and harms of markets. And now we are at a moment where there’s a real possibility that we may really lose that. We’re talking about possible retrogression, and the possibility of moving forward after this current moment has passed. But we really are at a point where the certainties of the underlying continuity of a fairly decent social compact is at risk. And so this is really new.

Elizabeth:

I really like that phrase, this “capitalism with the rough edges sanded off.” And what I’m hearing you say is basically the idea of the social compact is that, yes, we have capitalism, but we also have a commitment to providing a measure of security for people, and that’s the deal we have struck. You write a ton about the New Deal and FDR [Franklin D. Roosevelt]. Can you just expand a little bit about how to think about that trade-off, how long that consensus has held, and if there are any other moments in our economic history where there have been similar threats to that compact that we can learn from?

Paul:

I like to think about—it’s 1933, and the world economy has collapsed. There are a lot of reasonable people [who] have concluded that capitalism is irredeemable and can’t be saved, and that on the other hand, you have a lot of forces of repression out there. And along comes several countries—with the US in some ways leading the New Deal order, which says, no, we’re not actually going to go socialist. We’re not going to seize the commanding heights of production, but we are going to try to make sure that extreme hardship is vanished, as far as we can manage. We’re going to try to make sure that workers feel that they are a part of, and that they have rights and claims to, the system. There was very much this moment when we reached a kind of—I don’t know if it’s a compromise or a synthesis—but the idea of a basic standard of decency, the Four Freedoms. While at the same time saying that it’s not evil to make profits. It’s not evil to be personally ambitious. But we are going to try to make it so that everyone shares in the gains from economic activity.

And that really held. I mean, there was the moment when the Reagan administration came in, which represented, in many ways, a turn away from that New Deal consensus. But not to the extent that we have now. In moments of economic stress, people tend to say, well, maybe this thing doesn’t work anymore. The 1970s with stagflation, the aftermath of the 2008 financial crisis. That has basically been the case during attempts to turn away from the basic structure (which in the US context have always been a turn to the right, but in principle, you could imagine a turn to the left, but that hasn’t ever really happened in this country). And until right now, it has always seemed that the public wouldn’t stand for it. When push came to shove, when George W. Bush tried to privatize Social Security, it was a sort of resounding, “no, you don’t. We love Social Security.” But the possibility that we will have either explicitly or de facto undermining of those institutions seems much higher right now just because we live in such—well, we’re not gonna talk about the politics particularly, but there’s a possibility that we’ll lose it, that it will go away. And the one thing that I would say is that there’s this political action by itself, but there’s also the importance of getting the facts clear, getting the way the world works clear. No, there are not 10 million dead people receiving Social Security benefits. No, tax cuts and deregulation are not the only way to achieve economic growth. These are really critical things. Facts matter, analysis matters.

Elizabeth:

I’m just gonna pick up on that last thing you said about facts matter, analysis matters, and maybe go a little bit toward your true economist side. It’s not just Social Security we’re talking about. As you know and just mentioned, we’re in the middle of a tax and budget fight where we are very much looking at a situation where tax cuts for the wealthy might be traded for cuts to the programs that are specifically for our most vulnerable, like Medicaid and SNAP. This obviously has both political economy and democratic implications. It also has economic implications. Can you talk a little bit about this idea of what it means—this kind of wealth transfer, frankly, from the poorest to the richest, both in terms of hard facts, economics, and growth? And in terms of the social compacts that we’ve been talking about.

Paul:

It’s become increasingly clear that taking care of the most vulnerable members of society—it’s something you should do. It’s a moral obligation. But it’s also good economics, especially by the way of children. If you ask, a dollar spent on ensuring adequate health care and nutrition for children clearly pays off with multiple dollars of economic performance, because those children grow up to be more productive adults.

One way to say this is that conservative economic doctrine is all about punishing, it’s all about incentives: Poverty should be painful and wealth should be glorious. And what that all misses is the importance of just plain resources. That if low-income families cannot devote the resources to their children that you need to make those children fully productive adults—some will manage despite that, but just plain making sure that everybody in the country has the resources to make the most of themselves and their children is an enormously practical thing. It’s not just soft-hearted liberal talk, though I am a soft-hearted liberal, but it’s also just what you need to do if you want to make the most of your country’s potential.

Elizabeth:

I’m going to take another policy area, one actually that you know a lot about. It’s the area of focus that won you your Nobel Prize. You, in recent months, have been saying that one of the biggest risks of the Trump administration’s economic agenda is their chaotic tariff policy. We are currently recording the day after Liberation Day. And last year you predicted that the cronyism of those tariffs might be the biggest story in the long run, in addition to the chaos. So can you walk us through those risks, the chaos and the cronyism, and to what degree you’re seeing that play out for American workers and consumers? And, you know, why—I mean, there’s a lot of reasons why—but why are these tariffs different than the years that we’ve seen them in the past?

Paul:

There’s a standard economics case against tariffs, which is that it basically leads your economy to turn away from the things it’s really good at and start doing the things that it’s not especially good at. So for example, in New York, there’s lots of memories of the garment industry, but we really don’t wanna bring the garment industry back. Those were pretty bad jobs, and it happens to be stuff that can be done—where they can do it reasonably well—in Bangladesh, which desperately needs that industry, and we should be doing the things that we’re really good at instead. So that’s the classic case. What we’re discovering is that the rise of this hostility toward trade has additional costs. And the most immediate one is just plain that we don’t know what it’s gonna be.

As you said, we’re recording this the day after Liberation Day, which—nobody knows. I have to say that the actual tariff announcement shocked a lot of people, because it was both much bigger and much more arbitrary than people expected. I wouldn’t have been really shocked if there was a 15 percent across-the-board tariff, because that had been foreshadowed. But instead, there’s different tariffs for every country and this wasn’t really on anybody’s playbook. And nobody knows whether it [will] persist.

Think of yourself as being a business person trying to make decisions. You’re going to make an investment in your business—or are you? I mean, should you be spending money and making commitments on the basis that, okay, we’re gonna have 20 percent tariffs on all goods from Europe, or should you make it on the proposition that, “look, that’s crazy, those won’t last”? And both of those are defensible propositions. Anything you do, if you invest on the assumption that the tariffs are here to stay, then you’ll have made a terrible decision if they don’t. And so there’s a lot of paralysis that comes from the chaos. I’ve always been skeptical of people who invoke uncertainty as a reason that policy is holding the economy back, but because it’s often used as an argument against progressive policies: Oh, you know, your universal health care goals, that creates uncertainty. But in this case, this really is a major harmful issue.

We have not yet seen the cronyism, but it’s clearly potential. The whole root of—the reason why trade is where the dramatic stuff is happening [is because] US law creates a lot of discretion for the executive branch in tariff setting. Tariffs were only supposed to be applied as remedies for specific kinds of shocks or specific kinds of threats, but the decision about whether those conditions apply lies with the executive branch. So a president who wants to can do whatever they want on trade. And in the past, that’s always been held back by concern about: How will other countries react? What about the system? We built this global trading system. So it’s always been assumed that the president would have a wider view.

But if you take that away, then it’s not just arbitrary in terms of what are the overall levels of tariffs, it’s who gets a tariff break. And in fact, every time we do impose tariffs, there tend to be some exemptions. There are good reasons why sometimes you might want to exempt somebody from a tariff. But if it’s all arbitrary, the exemption might come because you go golfing with the president. And so that creates a lot of problematic incentives. We actually saw that in 2017, 2018, when the US was putting on tariffs—which looked trivial compared to what’s now on the plate—but it was very clear that industries and companies that were politically tied to the administration in power were much more likely to get exemptions than those that weren’t. So we actually saw this. We live in amazing times, and I mean that in the worst way. But everything that happened in the first go-around of what we called the trade war, it was really nothing—it was a skirmish compared with what’s happening now. But now, the possibilities are huge.

There’s a whole field of economic research on what the field calls rent-seeking. Economies where the way to succeed in business is not to be good at business, but to be good at cultivating political connections. And much of that actually was about tariffs and import quotas, but typically in developing countries. So there was a large concern that in places like Brazil or India, they were actually sacrificing a lot of potential gainful economic activity because businesses were focused instead on currying political favor. Well, could that happen here? Yes, it could. Very much down the road. I mean, I have to say that the speed and scale of the stuff that’s going on makes me think that we may have a global trade war and massive disruption before we even get around to the cronyism. But it’s down there, it’s in there. It’s in the mix.

Elizabeth:

We have seen, before yesterday, a real stop-start, put-on put-off, someone complains and we delay for a month. So I think we’ll really have to see, post-yesterday, where this goes. And this is a helpful roadmap for what to look for.

Paul:

And we should bear in mind also that the rest of the world has agency too. And part of the issue here is that the chaotic nature of the rollout is—again, the rest of the world has agency. And if you want to avoid getting into a lot of tit-for-tat, you probably want to at least explain what you’re doing and not be offending other countries unnecessarily. But, of course, we are doing that. I mean, to make Canada turn anti-American really takes—I didn’t think that—that wasn’t on my dance card for my career.

Elizabeth:

Roosevelt has argued for a long time for the strategic and targeted use of tariffs alongside industrial policy. And also, of course, alongside a strong sense of what rules and regulations you have to use to control unproductive uses of corporate and market power in that context, to make sure that the incentive structure that you’re creating actually targets the gains that you’re trying to make. But we’ve also argued for a way to transition into those things that takes account of some of the concerns that you’ve raised in terms of creating a stable business environment for investment, creating predictability, explaining things to mitigate the risk of fallout. And we’ve heard members of the administration say, “hey, yes.” [They] admit that this is going to be a little bit painful for a while, but it’ll be beneficial in the end.

You started to say this, but can you just pick apart for us when we hear someone say, “there might be a little bit of turmoil for a while,” what are the real costs of what that kind of turmoil might be for businesses, workers, consumers?

Paul:

I actually don’t buy—I mean, yes, there’s short-term pain, but it’s not short-term pain in exchange for a long-run gain, by any economic model I can think of applying. It’s actually short-term pain in return for probably even bigger long-term pain. The story about how this gets better is really not there.

I’m not a purist free trader. I’m not a laissez-faire guy. I mean, there’s a kind of idealized version of the post–New Deal consensus, which is, leave economic activity up to the markets, and then we’ll have a social safety net. But that has never been enough. We always need some additional stuff. We always need some industrial policy. And I think we need it more than we have actually had. But the reality is that you still want to have a lot of [trade]. International trade has, for the most part, been a plus for the US economy. There were distributional issues, but even there, it’s probably been a net-plus for the great majority of workers. And you’d want to mitigate the parts that aren’t. So the idea that shutting it down is going to produce a better outcome 5, 10 years down the pike, there’s really no clear argument to that effect. What is true is that we have this additional overlay, which is that nobody knows what the world is gonna look like next year. And so this is a tremendous inhibiting force.

Normally, when people say that, well, protectionism causes recessions, my answer has been no. There are lots of reasons not to like protectionism, but there’s no story about how it causes recessions. But protectionism where nobody knows what it’s gonna be, where nobody knows what the tariff rates are gonna be next year, that could cause a recession. So we may have the first real tariff-induced recession that I’m aware of in history, like, now.

Elizabeth:

That will give us something to keep an eye on over the next year and more.

I’m gonna change topics a little bit. We started, a little bit, to talk about power in the economy. Who has it? Who doesn’t? It’s something that you’ve explored. In your book Conscience of a Liberal, you wrote something that I really like: “The New Deal did more than create a middle-class society. It also brought America closer to its democratic ideals by giving working Americans real political power and ending the dominant position of the wealthy elite.”

Particularly in the environment we’re in today, what do you think policymakers should be thinking about in terms of what we can do to bring that New Deal power lens both to this moment and to a moment where we would have the ability to set the rules to put our country on a better course?

Paul:

There are two ends to that. One is just giving ordinary working- or middle-class people effective vehicles to exert political influence. And of course, we have the vote. (There may be that there’s no “of course” about that, but in principle, at least we have votes.) But I don’t think we really realized how much a strong union movement contributed toward making democracy work better. You can say, well, why isn’t the individual right to vote enough? And the answer is, look, there’s collective action problems. Politics is completely pervasive of things that would be good if everybody did them, but maybe [there’s] no individual incentives. So organizing politically is always hard, and unions are a big force in that—or were. And to some extent, still are, but much less than they used to be. And that’s really important. We are a less democratic country in practice because we don’t have workers organized. That’s one end of it, and there may be other ways, although I have to admit that I’m not all that creative. I think the success of unions in really making America more American in the postwar generation is something that we have never managed to find other routes to do.

Then on the other hand, there’s the question of the influence of malefactors of great wealth. The influence of vast wealth. And you don’t have to get too much into current events to say, well, we can really see that. I have to say, going back now, it looks like the plutocrats of the Gilded Age, by contemporary standards, were remarkable in their restraint and discretion. They didn’t try to buy influence as openly as the plutocrats today do. So now there are things you can do. It’s funny that our great grandfathers were much more open than we are in saying that one of the purposes of progressive taxation is to actually limit extreme wealth. And not simply because it’s more money to serve the common people, but because extreme wealth distorts democracy. Woodrow Wilson was much more willing to say things that would be regarded as extremely radical leftism now.

So really to reclaim who we are as a nation, [who we] are supposed to be, we need to work on both those ends. We need to try to empower basically working Americans, ordinary workers to have a role. And maybe there are other things besides unions, but that’s the obvious route.

And then you also need to try both with rules about money and politics, but also perhaps, if we can eventually, [through] constraining policy that limits the accumulation of enormous fortunes. That also limits that distortion because we really are in a situation now where it’s—all of the warnings about, as FDR would have said, the powers of organized money seem far more acute now than they ever did in the past.

Elizabeth:

You mentioned ideas that once were acceptable to say in polite company that seem more radical now. This is sort of the business of Roosevelt, to think big about how we can solve these questions of the maldistribution of power in the economy and do them at a structural level. And how to make ideas about that part of the common sense. You’ve talked about how that is part of what happened with the New Deal—that New Deal institutions that were at first considered novel and radical, by the Eisenhower presidency had become [a] normal part of American life. How did that happen in your view, that change in the common sense? And what made them so enduring and what lessons can we find for today about how to reorient what seems impossible and what seems a normal part of life?

Paul:

One of the things that strikes me when I look at history, both of economic institutions and of economic ideas, is that lots of things seem radical and scary until people have had a chance to experience them. So there’s the famous Nancy Pelosi quote—often out of context—where she said that for people to really understand the Affordable Care Act, we have to pass it. And it wasn’t like we were going to pull one over on people. It was that, as long as it was merely a theoretical thing, as long as it was something in prospect, it was possible to tell scare stories about death panels and just say, what will this do? But then after a few years, it becomes part of the fabric of life. And then, by the time we actually came fairly close to losing it, people were outraged because even imperfect as it is, Obamacare is a terrifically important safety net for many people.

You see that on a much larger scale [with] the New Deal changes. So if you go back to when FDR did his really stem-winding address in 1936 about the “I welcome their hatred” thing. The thing that was really the flash point—[that] was widely portrayed on one side of the political spectrum as an outrageous step that would destroy the market economy—was actually not Social Security, but unemployment insurance. It was like, “oh my god. You’re gonna actually pay people when they don’t have jobs.” And it turned out that hey, that’s okay. In fact—unemployment insurance was the most important thing that got us through COVID with minimal hardship. And now there are people, there’s always people who want to do away with these safety net programs. But things that can be made to sound ominous and radical when no one has actually experienced them can, after a few years, become part of the landscape.

The New Deal first got us through the Great Depression, then got us through the war. And by the time the war was over, we had become a very different country—and I would say a much better country—in which people accepted that, yeah, we have a kind of public responsibility to limit extreme inequality, to limit extreme hardship.

Elizabeth:

I want to close this out with a note that you struck in your final New York Timescolumn last December. It was a tough one. You wrote, “optimism has been replaced by anger and resentment,” and that “the public no longer has faith that the people running things know what they’re doing, or that we can assume that they’re being honest.”

I think that applies to government. It also applies to a lot of institutions across the board. So here is my question for you: What do you think it will take to rebuild trust in public institutions? And also, on a more personal level, how do you find the hope that we can make it there from here?

Paul:

Well, there’s nothing like actually doing good to build trust. If we can find our way past the current turmoil, I think that there’s an underlying reservoir of optimism still in America. And if we can get our way past this, all of these things that led us to this rather scary moment, then a few years of good governance can actually do wonders. I mean, I’m older than you are, and certainly older than a lot of the people I deal with, but I remember the 1990s. And although there are many imperfections and lots of things, it’s hard to remember just how positive people were feeling about America by the end of that decade. And that was thrown away through a variety of bad decisions. But still, it’s not that distant. It’s not that inconceivable.

And so I would think that the way forward is to get people in power who really do try to use it for good, get good programs, get good policy, get decent people. And there’s a lot of strengths in America. And this atmosphere of distrust and feeling that everyone is out to get you is self-serving. That will go away fairly quickly if it’s demonstrably not true.

Now personally, I’m terrified. I’m not giving up, but you can see a lot of the things that we read about in the history books about how societies go wrong are no longer abstract. We can see those emotions, we can see those forces out there. But the truth is that a better environment is actually—people become more generous, more positive when things are going okay. And we really don’t want to have a situation where [this] zero-sum, “I’ve got mine, I don’t want anybody else to get it” thinking is validated by experience. So, try to make things work is how we go from here.

Elizabeth:

I can tell you one of the things that gives me hope, Paul, is that in a moment where we are watching some institutions capitulate and fold in a way that is really disheartening, we also have some voices that are getting louder, not softer, and I think one of them is yours. So I wanna say how appreciative I know I am personally and how excited I know the [Roosevelt] Institute is generally to have you on as a senior fellow, in part because I really do think you are a voice out there that’s making sense of what’s happening. That’s helping us put into a context that we can understand the flood of news that we are experiencing. And, again, to demonstrate what it looks like to be a consistent voice with good analysis and moral clarity about what’s happening now, and also who we have been in the past and who we could be again. So we really appreciate your work, and we really appreciate you taking the time to chat today.

Last week, I made my once a decade trek to a dealership to buy a new car. I did my research in advance (and even negotiated the price) so I was hoping for a stress-free experience.

It was – up until the point where I got locked in the finance manager’s office for “the talk”. You know, the one where you are made to feel like a neglectful parent unless you pony up for all the fixin’s – everything from nitrogen filled tires to paint protection (just in case I encounter a flock of migratory geese on the drive home). I shook my head no about ten times before we got to the pre-paid maintenance plan options. I decided to be polite and listen (plus I was curious since I was purchasing a car from a manufacturer notorious for costly repairs). As compelling as it was to pay nearly $5,000 to what ultimately would amount to a few tire rotations for my electric vehicle, I held firm. The finance manager angrily handed me my signed documents and whisked me out of his office.

I guess I can’t blame car dealers for applying massive mark-ups for services that are inexpensive to provide. Except similar financial chicanery is currently playing out in our health insurance system. If you swap out the finance manager for a health insurer and replace me with the average everyday consumer, the dealer’s tactics are analogous to how insurers game medical loss ratio (MLR) requirements (except as a health care consumer, you can’t say “no”).

A bit of background is in order to understand why I thought about health insurance and car dealers in the same breath.

Insurance companies are required to spend a certain percentage of money they get from premiums on medical costs and quality improvement (QI); this is known as the medical loss ratio (MLR). If companies do not meet this ratio (usually 80-85%, depending on the product), they must refund the difference in the form of a rebate, or reduction in future premiums, to consumers.

Like any for-profit corporation in America today, a health insurer wants to avoid giving money back to consumers. Therefore, insurers have become adept at manipulating their MLRs through various accounting and financial engineering techniques. This manipulation optimizes their ability to meet MLR thresholds and avoid paying rebates, which runs afoul of its intended purpose: to ensure that patients receive the appropriate level of care.

So how do insurers game the system, and what evidence exists for this activity?

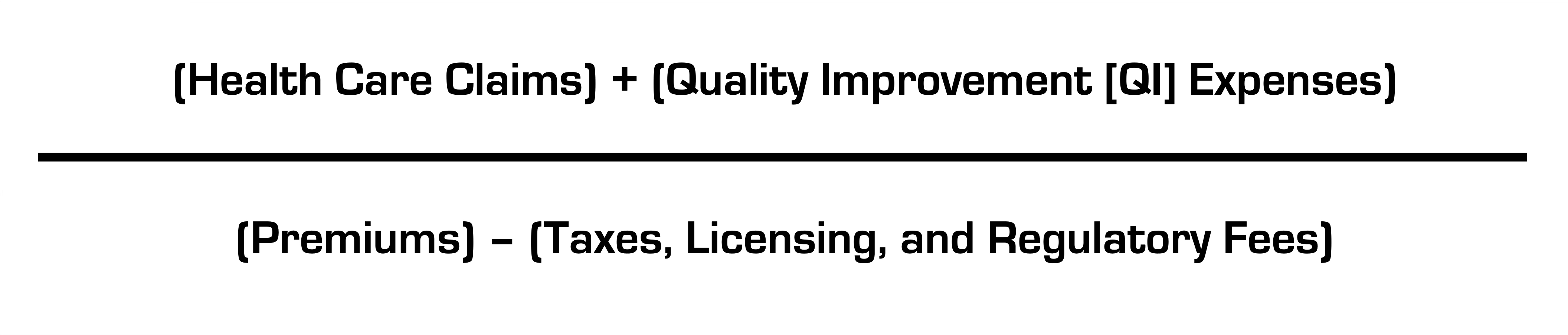

The current MLR formula is:

Health insurers do not control taxes and fees, but they can easily engineer the other variables. Below, I’ll explain how.

Step 1: Quality Improvement (QI) Expenses

The definition of allowable QI expenses is broad and includes activities to improve outcomes, patient safety, and reduce mortality (mom and apple pie stuff). Insurers played a big role in writing the MLR regulations after Congress enacted legislation and made sure they’d have wide latitude in what expenses are classified as QI (akin to the car dealer “option” list) and what product segments they assign them to.

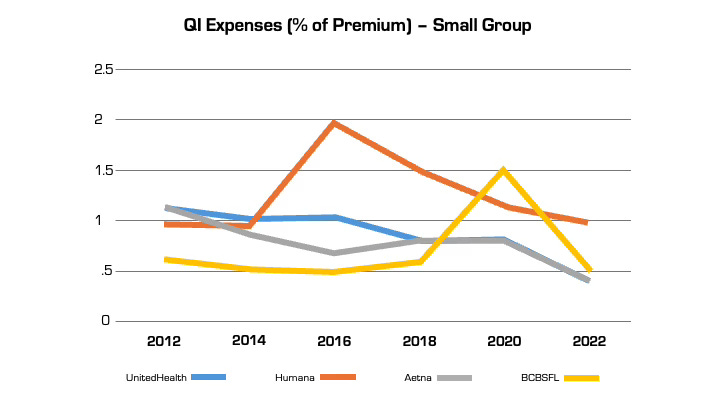

Looking at reported QI expenses sheds light on this practice. QI expenses vary between insurers. But they also vary widely for the same insurer from year to year (even after controlling for geography and product segment). In large part, this is attributable to financial engineering. QI costs can be effectively “transferred” on the income statement from one product segment to another, by adjusting the pro rata weightings). This enables them to optimize MLR performance across their insurance portfolio (i.e. by taking from a bucket with excess medical costs and putting it in another with insufficient costs) in a way that maximizes benefit to the insurer and is camouflaged from regulators and consumers. This is language from a recent UnitedHealth Group filing with the Securities and Exchange Commission: “Assets and liabilities jointly used are assigned to each reportable segment using estimates of pro-rata usage.”

Annual QI expenses across four insurers in Florida in the small group market.

Although these QI percentages are small, the associated dollar amounts are large. In 2022, UnitedHealth, Humana, and Aetna reported $494 million, $550 million, and $395 million respectively in allowable QI expenses for their national plans. While there is some legitimate QI activity at insurers (e.g., pharmacists who identify high risk medications in the elderly), the reality is that much of the QI work is already heavily resourced within provider organizations, where it is more effective. Insurers also can (and do) count “wellness and health promotion activities” despite limited evidence these programs improve health outcomes and are more often used by insurers as marketing tools.

Step 2. Health Care Claims

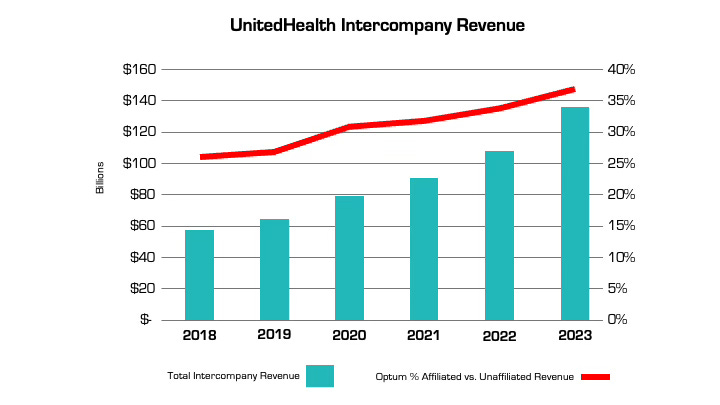

The other variable that insurers can manipulate is claims costs. The more an insurer is vertically integrated, the easier it is. The prime example is UnitedHealth, which has an insurance arm (UnitedHealthcare) and a big division that encompasses medical services, among many other things (Optum), as well as various other subsidiaries. Optum Health and Optum Rx receive a significant portion of their revenue from UnitedHealthcare for providing services like care and pharmacy benefit management to people enrolled in its health plans. In fact, the amount of UnitedHealth’s corporate “eliminations,” (meaning inter-company revenue that is reported on their consolidated financial statement) has more than doubled over the past five years (from $58.5 billion to $136.4 billion). The proportion of revenue Optum derives from UnitedHealthcare versus unaffiliated entities has increased by nearly 50% over the same period. A similar trend is playing out at every major insurer.

Take the example of the insurance company Aetna, the PBM CVS Caremark, and CVS Pharmacy, which are all vertically integrated and owned by CVS Health. If a patient goes to a CVS store to fill a prescription for Imatinib, a generic chemotherapy drug, the total cost the patient and insurance company pay is $17,710.21 for a 30-day supply. The same drug is sold by Cost Plus Drugs for $72.20 (the cost is calculated by adding the wholesale price and a 15% fee). When the patient fills the prescription at a CVS retail pharmacy, CVS Health can record that the patient paid a medical claim cost of $17,710.21 (even though the cost to acquire the drug is $70) and the remaining $17,640 can be retained as profits disguised as medical costs.

Insurers’ extensive acquisition of physician practices also facilitates gamification of the MLR via its ability to pay capitation (a set amount per person) to a risk-bearing provider organization (RBO) it owns, such as a medical group. This enables the insurer to lock in a set amount of premium as “medical expense” (usually around 85%) with the downstream provider group “managing” those costs. There’s a loophole, however. While the insurer has technically met its MLR requirement, the downstream RBO is subject to far fewer regulations on how it spends the money, which makes it easier to generate profits by skimping on care.

The regulations on RBOs vary by state. In many cases, while RBOs need to meet minimum capital requirements, they are not subject to the same MLR provisions as insurers. For a vertically integrated insurer that gets a huge amount of revenue from taxpayer-supported programs like Medicare Advantage and Medicaid, this essentially means that (1) the Center for Medicare and Medicaid Services puts the money into the insurer’s right pocket, (2) the insurer moves it to the left pocket, and (3) CMS checks the right pocket – and just the right pocket – at the end of the year to make sure it’s mostly empty (without regard to the fact that the left one may be busting at the seams).

The good news is there are ways to address these issues, both through updating the MLR provisions in the Affordable Care Act (which are long in the tooth) and more rigorous and comprehensive reporting requirements and regulation of vertically integrated insurers.

Just like I don’t want car dealers pushing unnecessary add-ons to increase their profit margins, consumers deserve that the required portion of their hard spent premium dollar actually goes toward their health care instead of further enriching huge corporations, executives, and Wall Street shareholders.

Health systems are rightly concerned about Republican plans to cut Medicaid spending, end ACA subsidies and enact site neutral payments, says consultant Michael Abrams, managing partner of Numerof, a consulting firm.

“Health systems have reason to worry,” Abrams said shortly after President Donald Trump was inaugurated on Monday.

While Trump mentioned little about healthcare in his inauguration speech, the GOP trifecta means spending cuts outlined in a one-page document released by Politico and another 50-pager could get a majority vote for passage.

Of the insurers, pharmaceutical manufacturers and health systems that Abrams consults with, healthcare systems are the ones that are most concerned, Abrams said.

At the top of the Republican list targeting $4 trillion in healthcare spending is eliminating an estimated $2.5 billion from Medicaid.

“There’s no question Republicans will find savings in Medicaid,” Abrams said.

Medicaid has doubled its enrollment in the last couple of years due to extended benefits made possible by the Affordable Care Act, despite disenrolling 25 million people during the redetermination process at the end of the public health emergency, according to Abrams.

Upward of 44 million people, or 16.4% of the non-elderly U.S. population are covered by an Affordable Care Act initiative, including a record high of 24 million people in ACA health plans and another 21.3 million in Medicaid expansion enrollment, according to a KFF report.Medicaid expansion enrollment is 41% higher than in 2020.

The enhanced subsidies that expanded eligibility for Medicaid and doubled the number of enrollees are set to expire at the end of 2025 and Republicans are likely to let that happen, Abrams said. Eliminating enhanced federal payments to states that expanded Medicaid under the ACA are estimated to cut the program by $561 billion.

If enhanced subsidies end, the Congressional Budget Office has estimated that the number of people who will become uninsured will increase by 3.8 million each year between 2026 and 2034.

The enhanced tax subsidies for the ACA are set to expire at the end of 2025. This could result in another 2.2 million people losing coverage in 2026, and 3.7 million in 2027, according to the CBO.

WHY THIS MATTERS

For hospitals, loss of health insurance coverage means an increase in sicker, uninsured patients visiting the emergency department and more uncompensated care.

“Health systems are nervous about people coming to them who are uninsured,” Abrams said. “There will be people disenrolled.”

The federal government allowed more people to be added to the Medicaid rolls during the public health emergency to help those who lost their jobs during the COVID-19 pandemic, Numerof said. Medicaid became an open-ended liability which the government wants to end now that the unemployment rate is around 4.2% and jobs are available.

An idea floating around Congress is the idea of converting Medicaid to a per capita cap and providing these funds to the states as a block grant, Abrams said. The cost of those programs would be borne 70% by the federal government and 30% by states.

This fixed amount based on a per person amount would save money over the current system of letting states report what they spent.

Another potential change under the new administration includes site neutral Medicare payments to hospitals for outpatient services.

The HFMA reported the site neutral policy as a concern in a list it published Monday of preliminary federal program cuts totaling more than $5 trillion over 10 years. The 50-page federal list is essentially a menu of options, the HFMA said, not an indication that programs will actually be targeted leading up to the March 14 deadline to pass legislation before federal funding expires.

Other financial concerns for hospitals based on that list include: the elimination of the tax exemption for nonprofit hospitals, bringing in up to $260 billion in estimated 10-year savings; and phasing out Medicare payments for bad debt, resulting in savings of up to $42 billion over a decade.

Healthcare systems are the ones most concerned over GOP spending cuts, according to Abrams. Pharmacy benefit managers and pharmaceutical manufacturers also remain on edge as to what might be coming at them next.

THE LARGER TREND

President Donald Trump mentioned little about healthcare during his inauguration speech on Monday.

Trump said the public health system does not deliver in times of disaster, referring to the hurricanes in North Carolina and other areas and to the fires in Los Angeles.

Trump also mentioned giving back pay to service members who objected to getting the COVID-19 vaccine.

He also talked about ending the chronic disease epidemic, without giving specifics.

“He didn’t really talk about healthcare even in the campaign,” Abrams said.

However, in his consulting work, Abrams said, “The common thread is the environment is changing quickly,” and that healthcare organizations need to do the same “in order to survive.”

Liberal advocacy groups are ramping up efforts to protect the Medicaid program from potential cuts by Republican lawmakers and the new Trump administration.

The Democratic group Protect Our Care launched Tuesday an eight-figure “Hands off Medicaid” ad campaign targeting key Republicans in the House and Senate, warning of health care being “ripped away” from vulnerable Americans.

The lawmakers include GOP Sens. Bill Cassidy (La.), Chuck Grassley (Iowa), Lisa Murkowski (Alaska) and Susan Collins (Maine), as well as Reps. David Schweikert (Ariz.), Mike Lawler (N.Y.) and David Valadao (Calif.).

The campaign will also include digital advertising across platforms targeting the Medicaid population in areas around nursing homes and rural hospitals, ads on streaming platforms as well as billboards and bus stop wraps.

Medicaid covers 1 in 5 Americans, and the group wants to highlight that includes “kids, moms, seniors, people of color, rural Americans, and people with disabilities.”

“The American people didn’t vote in November to have their grandparents kicked out of nursing homes or health care ripped away from kids with disabilities or expectant moms in order to give Elon Musk another tax cut,” Protect Our Care chair Leslie Dach said in a statement.

House Republicans have expressed openness to making some drastic changes in the Medicaid program to pay for extending President Trump’s signature tax cuts, including instituting work requirements and capping how much federal money is spent per person. The ideas have been conservative mainstays since they were included as part of the 2017 Obamacare repeal effort.

Separately, advocacy group Families USA led a letter with more than 425 national, state and local organizations calling on Trump to protect Medicaid.

The groups noted that if the Trump administration wants to trim health costs, “there are many well-vetted, commonsense and bipartisan proposals” that don’t involve slashing Medicaid.

“In 2017, millions upon millions of Americans rose up against proposed cuts and caps and made clear how much they valued Medicaid as a critical health and economic lifeline for themselves, their families, and their communities. The American people are watching once again, and we urge you to take this opportunity to choose a different path,” they wrote.

To understand the fatal attack on UnitedHealthcare CEO Brian Thompson and the unexpected reaction on social media, you have to go back to the 1990s when managed care was in its infancy. As a consumer representative, I attended meetings of a group associated with the health care system–doctors, academics, hospital executives, business leaders who bought insurance, and a few consumer representatives like me.

It was the dawn of the age of managed care with its promise to lower the cost and improve the quality of care, at least for those who were insured.

New perils came with that new age of health coverage.

In the quest to save money while ostensibly improving quality, there was always a chance that the managed care entities and the doctors they employed or contracted with – by then called managed care providers – could clamp down too hard and refuse to pay for treatments, leaving some people to suffer medically. Groups associated with the health care industry tried to set standards to guard against that, but as the industry consolidated and competition among the big players in the new managed care system consolidated, such worries grew.

Over the years the squeeze on care got tighter and tighter as the giants like UnitedHealthcare–which grew initially by buying other insurance companies such as Travelers and Golden Rule–and Elevance, which gobbled up previously nonprofit Blue Cross plans in the 1990s, starting with Blue Cross of California, needed to please the gods of the bottom line. Shareholders became all important. Paying less for care meant more profits and return to investors, so it is no wonder that the alleged killer of the UnitedHealthcare chief executive reportedly left the chilling message: