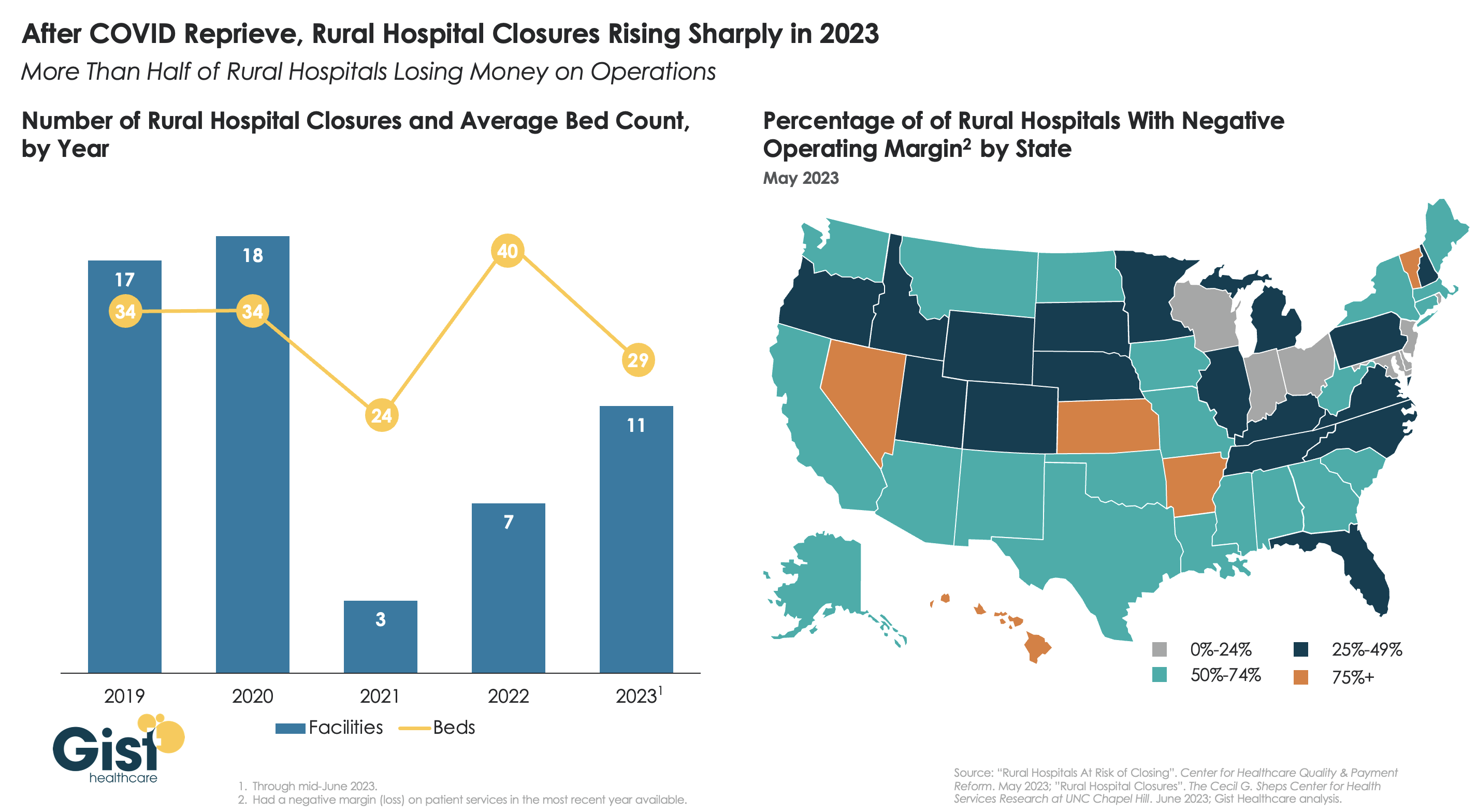

After a brief reprieve thanks to COVID relief funds, rural hospital closures are once again on the rise, with 11 facilities already closing in the first half of this year.

More rural facilities have already closed in 2023 than the previous two years combined, and this year is on pace to be the second-highest number of rural hospital beds lost since 2005.

And the majority of rural hospitals that haven’t closed are experiencing negative operating margins, with almost one in three at immediate or high risk of closure due to declining volumes, shifting payer mix, and increased labor and supply costs.

Leaders at rural hospitals now face difficult decisions including drastically cutting services, merging with a larger system, or closing their doors altogether. The Centers for Medicare and Medicaid Services (CMS) launched the Rural Emergency Hospital Program recently, designed to financially support small rural hospitals that convert to providing emergency services only, but so far program uptake has been limited.

While efforts to prop up hospitals will help to sustain access to care in the near term, rural communities ultimately need a new model for care, with reimagined facilities, supported by enhanced virtual connections to specialists and higher-acuity services.

Here are 45 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

Note: This is not an exhaustive list. Health system names were compiled from credit rating reports.

1. AdventHealth has an “AA” rating and stable outlook with Fitch. The rating reflects the Altamonte Springs, Fla.-based system’s strong financial profile, characterized by still-adequate liquidity and moderate leverage, typically strong and highly predictable profitability, Fitch said.

2. AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has maintained strong performance through the COVID-19 pandemic and current labor market pressures, Fitch said.

3. Atrium Health has an “AA-” and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

4. Banner Health has an “AA-” and stable outlook with Fitch. The Phoenix-based system’s rating highlights the strength of its core hospital delivery system and growth of its insurance division, Fitch said.

5. BayCare Health System has an “AA” rating and stable outlook with Fitch. The Tampa, Fla.-based system’s rating reflects its excellent financial profile supported by its leading market position in a four-county area and the ability to sustain a solid operating outlook in the face of inflationary sector headwinds, Fitch said.

6. Beacon Health System has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of the South Bend, Ind.-based system’s balance sheet, the rating agency said.

7. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

8. Cape Cod Healthcare has an “AA-” and stable outlook with Fitch. The Hyannis, Mass.-based system’s rating reflects a dominant market position in its service area and historically solid operating results, the rating agency said.

9. Carle Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Urbana, Ill.-based system’s distinctly leading market position over a broad service area, Fitch said.

10.CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

11. CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

12. Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

13. Concord (N.H.) Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the strength of Concord’s leverage and liquidity assessment and Fitch’s assessment that two recently acquired hospitals will be strategically and financially accretive.

14. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

15. Cottage Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Santa Barbara, Calif.-based system’s leading market position and broad reach in a service area that exhibits modest population growth but consistently high demand for acute care services, Fitch said.

16. El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

17. Froedtert Health has an “AA” rating and stable outlook with Fitch. The rating reflects the Milwaukee-based system’s maintenance of a strong, albeit compressed, operating performance and a robust liquidity position, Fitch said.

18. Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based system’s rating is supported by its strong presence in its large and demographically favorable market, Fitch said.

19. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

20. Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

21. IU Health has an “AA” rating and stable outlook with Fitch. The Indianapolis-based system has a long track record of strong operating margins and an overall credit profile that is supported by a strong balance sheet, the rating agency said.

22. Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

23. Lucile Packard Children’s Hospital has an “AA-” rating and stable outlook with Fitch. The rating reflects the Palo Alto, Calif.-based hospital’s role as a nationally known, leading children’s hospital, Fitch said. It also benefits from resilient clinical volumes and a solid market position, as well as its relationship with Stanford University and Stanford Health Care.

24. Kaiser Permanente has an “AA-” and stable outlook with Fitch. The Oakland, Calif.-based system’s rating is driven by a strong financial profile, which is maintained despite a challenging operating environment in fiscal year 2022.

25. Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

26. McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

27. MemorialCare has an “AA-” rating and stable outlook with Fitch. The rating reflects the Fountain Valley, Calif.-based system’s strong financial profile and excellent leverage metrics despite its weaker operating performance, Fitch said.

28. Memorial Sloan-Kettering Cancer Center has an “AA” rating and stable outlook with Fitch. The rating reflects Fitch’s expectation that the New York City-based system’s national and international reputation as a premier cancer hospital will continue to support growth in its leading and increasing market share for its specialty services.

29. Midland (Texas) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects Midland’s exceptional market position and limited competition for acute-care services and growing outpatient services, Fitch said.

30. Munson Healthcare has an “AA” rating and stable outlook with Fitch. The rating reflects the strength of the Traverse City, Mich.-based system’s market position and its leverage and liquidity profiles.

31. North Mississippi Health Services has an “AA” rating and stable outlook with Fitch. The Tupelo-based system’s rating reflects its very strong cash position and strong market position, Fitch said.

32. Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

33. NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

34. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

35. The Queen’s Health System has an “AA” rating and stable outlook with Fitch. The Honolulu-based system’s rating reflects its leading state-wide market position, historically strong operating performance and diverse revenue streams, the rating agency said.

36. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

37. Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

38. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

39. Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

40. SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

41. St. Clair Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Pittsburgh-based system’s strong financial profile assessment, solid market position and historically strong operating performance, the rating agency said.

42. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

43. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

44. WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

45. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

On October 1, 1908, Ford produced the first Model T automobile. More than 60 years later, this affordable, mass produced, gasoline-powered car was still the top-selling automobile of all time. The Model T was geared to the broadest possible market, produced with the most efficient methods, and used the most modern technology—core elements of Ford’s business strategy and corporate DNA.

On April 25, 2018, almost 100 years later, Ford announced that it would stop making all U.S. internal-combustion sedans except the Mustang.

The world had changed. The Taurus, Fusion, and Fiesta were hardly exciting the imaginations of car-buyers. Ford no longer produced its U.S. cars efficiently enough to return a suitable profit. And the internal combustion technology was far from modern, with electronic vehicles widely seen as the future of automobiles.

Ford’s core strategy, and many of its accompanying products, had aged out. But not all was doom and gloom; Ford was doing big and profitable business in its line of pickups, SUVs, and -utility vehicles, led by the popular F-150.

It’s hard to imagine the level of strategic soul-searching and cultural angst that went into making the decision to stop producing the cars that had been the basis of Ford’s history. Yet, change was necessary for survival. At the time, Ford’s then-CEO Jim Hackett said, “We’re going to feed the healthy parts of our business and deal decisively with the areas that destroy value.”

So Ford took several bold steps designed to update—and in many ways upend—its strategy. The company got rid of large chunks of the portfolio that would not be relevant going forward, particularly internal combustion sedans. Ford also reorganized the company into separate divisions for electric and internal combustion vehicles. And Ford pivoted to the future by electrifying its fleet.

Ford did not fully abandon its existing strategies. Rather, it took what was relevant and successful, and added that to the future-focused pivot, placing the F-150 as the lead vehicle in its new electric fleet.

This need for strategic change happens to all large organizations. All organizations, including America’s hospitals and health systems, need to confront the fact that no strategic plan lasts forever.

Over the past 25-30 years, America’s hospitals and health systems based their strategies on the provision of a high-quality clinical care, largely in inpatient settings. Over time, physicians and clinics were brought into the fold to strengthen referral channels, but the strategic focus remained on driving volume to higher-acuity services.

More recently, the longstanding traditional patient-physician-referral relationship began to change. A smarter, internet-savvy, and self-interested patient population was looking for different aspects of service in different situations. In some cases, patients’ priority was convenience. In other cases, their priority was affordability. In other cases, patients began going to great lengths to find the best doctors for high-end care regardless of geographic location. In other cases, patients wanted care as close as their phone.

Around the country, hospitals and health systems have seen these environmental changes and adjusted their strategies, but for the most part only incrementally. The strategic focus remains centered on clinical quality delivered on campus, while convenience, access, value, affordability, efficiency, and many virtual innovations remain on the strategic periphery.

Health system leaders need to ask themselves whether their long-time, traditional strategy is beginning to age out. And if so, what is the “Ford strategy” for America’s health systems?

The questions asked and answered by Ford in the past five years are highly relevant to health system strategic planning at a time of changing demand, economic and clinical uncertainty, and rapid innovation. For example, as you view your organization in its entirety, what must be preserved from the existing structure and operations, and what operations, costs, and strategies must leave? And which competencies and capabilities must be woven into a going-forward structure?

America’s hospitals and health systems have an extremely long history—in some cases, longer than Ford’s. With that history comes a natural tendency to stick with deeply entrenched strategies. Now is the time for health systems to ask themselves, what is our Ford F150? And how do we “electrify” our strategic plan going forward?

A couple of months ago, I got a call from a CEO of a regional health system—a long-time client and one of the smartest and most committed executives I know. This health system lost tens of millions of dollars in fiscal year 2022 and the CEO told me that he had come to the conclusion that he could not solve a problem of this magnitude with the usual and traditional solutions. Pushing the pre-Covid managerial buttons was just not getting the job done.

This organization is fiercely independent. It has been very successful in almost every respect for many years. It has had an effective and stable board and management team over the past 30 to 40 years.

But when the CEO looked at the current situation—economic, social, financial, operational, clinical—he saw that everything has changed and he knew that his healthcare organization needed to change as well. The system would not be able to return to profitability just by doing the same things it would have done five years or 10 years ago. Instead of looking at a small number of factors and making incremental improvements, he wanted to look across the total enterprise all at once. And to look at all aspects of the enterprise with an eye toward organizational renovation.

I said, “So, you want a makeover.”

The CEO is right. In an environment unlike anything any of us have experienced, and in an industry of complex interdependencies, the only way to get back to financial equilibrium is to take a comprehensive, holistic view of our organizations and environments, and to be open to an outcome in which we do things very differently.

In other words, a makeover.

Consider just a few areas that the hospital makeover could and should address:

There’s the REVENUE SIDE: Getting paid for what you are doing and the severity of the patient you are treating—which requires a focus on clinical documentation improvement and core revenue cycle delivery—and looking for any material revenue diversification opportunities.

There is the relationship with payers: Involving a mix of growth, disruption, and optimization strategies to increase payments, grow share of wallet, or develop new revenue streams.

There’s the EXPENSE SIDE: Optimizing workforce performance, focusing on care management and patient throughput, rethinking the shared services infrastructure, and realizing opportunities for savings in administrative services, purchased services, and the supply chain. While these have been historic areas of focus, organizations must move from an episodic to a constant, ongoing approach.

There’s the BALANCE SHEET: Establishing a parallel balance sheet strategy that will create the bridge across the operational makeover by reconfiguring invested assets and capital structure, repositioning the real estate portfolio, and optimizing liquidity management and treasury operations.

There is NETWORK REDESIGN: Ensuring that the services offered across the network are delivered efficiently and that each market and asset is optimized; reducing redundancy, increasing quality, and improving financial performance.

There is a whole concept around PORTFOLIO OPTIMIZATION: Developing a deep understanding of how the various components of your business perform, and how to optimize, scale back, or partner to drive further value and operational performance.

Incrementalism is a long-held business approach in healthcare, and for good reason. Any prominent change has the potential to affect the health of communities and those changes must be considered carefully to ensure that any outcome of those changes is a positive one. Any ill-considered action could have unintended consequences for any of a hospital’s many constituencies.

But today, incrementalism is both unrealistic and insufficient.

Just for starters, healthcare executive teams must recognize that back-office expenses are having a significant and negative impact on the ability of hospitals to make a sufficient operating margin. And also, healthcare executive teams must further realize that the old concept of “all things to all people” is literally bringing parts of the hospital industry toward bankruptcy.

As I described in a previous blog post, healthcare comprises some of the most wicked problems in our society—problems that are complex, that have no clear solution, and for which a solution intended to fix one aspect of a problem may well make other aspects worse.

The very nature of wicked problems argues for the kind of comprehensive approach that the CEO of this organization is taking—not tackling one issue at a time in linear fashion but making a sophisticated assessment of multiple solutions and studying their potential interdependencies, interactions, and intertwined effects.

My colleague Eric Jordahl has noted that “reverting to a 2019 world is not going to happen, which means that restructuring is the only option. . . . Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.”

The very nature of the socioeconomic environment makes doing nothing or taking an incremental approach untenable. It is clearly beyond time for the hospital industry makeover.

The median year-to-date operating margin index for hospitals improved slightly in April to 0 percent. While recent reports show signs of improving margins, they remain far below historical norms, and inflation and workforce expenses continue to challenge hospitals’ bottom lines.

“Hospital and health system leaders must figure out how to navigate the new financial reality and begin to take action,” Erik Swanson, senior vice president of data and analytics with Kaufman Hall, said in a May 31 report. “In the face of operating margins that may never fully recover and inflated expenses, developing and executing a strategic path forward to a future that is financially sustainable is crucial.”

Here are 29 health systems ranked by their operating margins in the first quarter:

Correction: An earlier version incorrectly referenced a Texas deal between Houston Methodist and Baylor Scott and White. News about deals is sensitive and unnecessarily disruptive to reputable organizations like these. I sourced this news from a reputable deal advisor: it was inaccurate. My apology!

Congressional Republicans and the White House spared Main Street USA the pain of defaulting on the national debt last week. No surprise.

Also not surprising: another not-for-profit-mega deal was announced:

St. Louis, MO-based BJC HealthCare and Kansas City, MO-based Saint Luke’s Health System announced their plan to form a $9.5B revenue, 28-hospital system with facilities in Missouri, Kansas, and Illinois.

This follows recent announcements by four other NFP systems seeking the benefits of larger scale:

Gundersen Health System & Bellin Health (Nov 2022): 11 hospitals, combined ’22 revenue of $2.425B

Froedtert Health & ThedaCare (Apr 2023 LOI): 18 hospitals, combined ’22 revenues of $4.6B

And all these moves are happening in an increasingly dicey environment for large, not-for-profit hospital system operators:

Increased negative media attention to not-for-profit business practices that, to critics, appear inconsistent with a “NFP” organization’s mission and an inadequate trade for tax exemptions each receives.

Decreased demand for inpatient services—the core business for most NFP hospital operations. Though respected sources (Strata, Kaufman Hall, Deloitte, IBIS et al) disagree somewhat on the magnitude and pace of the decline, all forecast decreased demand for traditional hospital inpatient services even after accounting for an increasingly aging population, a declining birthrate, higher acuity in certain inpatient populations (i.e. behavioral health, ortho-neuro et al) and hospital-at-home services.

Increased hostility between national insurers and hospitals over price transparency and operating costs.

Increased employer, regulator and consumer concern about the inadequacy of hospital responsiveness to affordability in healthcare.

And heightened antitrust scrutiny by the FTC which has targeted hospital consolidation as a root cause of higher health costs and fewer choices for consumers. This view is shared by the majorities of both parties in the House of Representatives.

In response, Boards and management in these organizations assert…

Health Insurers—especially investor-owned national plans—enjoy unfettered access to capital to fund opportunistic encroachment into the delivery of care vis a vis employment of physicians, expansion of outpatient services and more.

Private equity funds enjoy unfettered opportunities to invest for short-term profits for their limited partners while planning exits from local communities in 6 years or less.

The payment system for hospitals is fundamentally flawed: it allows for underpayments by Medicaid and Medicare to be offset by secret deals between health insurers and hospitals. It perpetuates firewalls between social services and care delivery systems, physical and behavioral health and others despite evidence of value otherwise. It requires hospitals to be the social safety net in every community regardless of local, state or federal funding to offset these costs.

These reactions are understandable. But self-reflection is also necessary. To those outside the hospital world, lack of hospital price transparency is an excuse. Every hospital bill is a surprise medical bill. Supporting the community safety net is an insignificant but manageable obligation for those with tax exemption status. Advocacy efforts to protect against 340B cuts and site-neutral payment policies are about grabbing/keeping extra revenue for the hospital. What is means to be a “not-for-profit” anything in healthcare is misleading since moneyball is what all seem to play. And short of government-run hospitals, many think price controls might be the answer.

My take:

The headwinds facing large not-for-profit hospitals systems are strong. They cannot be countered by contrarian messaging alone.

What’s next for most is a new wave of operating cost reductions even as pre-pandemic volumes are restored because the future is not a repeat of the past. Being bigger without operating smarter and differently is a recipe for failure.

What’s necessary is a reset for the entire US health system in which not-for-profit systems play a vital role. That discussion should be led by leaders of the largest NFP systems with the full endorsements of their boards and support of large employers, physicians and public health leaders in their communities.

Everything must be on the table: funding, community benefits, tax exemption, executive compensation, governance, administrative costs, affordability, social services, coverage et al. And mechanisms for inaction and delays disallowed.

It’s a unique opportunity for not-for-profit hospitals. It can’t wait.

Despite a reasonably solid third quarter, Trinity Health is still operating at a loss in its 2023 fiscal year, according to a new filing.

The health system’s fiscal year began July 1, 2022, with the latest figures covering the first nine months. Its latest operating loss shrank to $263.1 million from the prior six months’ $298 million loss. Fiscal year 2023 operating revenue currently stands at $15.9 billion, up from the same period last year.

The nonprofit health system attributed its operating revenue growth to several acquisitions (MercyOne, North Ottawa Community Health System, Genesis Health System), which collectively added $1 billion of operating revenue. Net income for the last nine months was $856.3 million, compared to $43 million in the same period the prior year.

Though inpatient volumes are stabilizing to “a new normal,” management wrote in the latest filing, most of Trinity’s revenue comes from outpatient and other non-patient revenue. Operating expenses rose $1.1 billion compared to the same period in fiscal year 2022, mostly driven by the acquisitions.

Nonoperating income was $1.2 billion during the first nine months of fiscal year 2023, up from $264.6 million in the first six months. This hike was driven partly by a $629.3 million increase in investment returns.

The health system’s operating margin was 1.6%, per the latest filing, compared to 0.1% during the same period a year ago. Margins were affected by expenses outpacing revenue, primarily driven by premium labor rates and inflation impacting supplies as well as a $137 million reduction in CARES Act grant funding.

Trinity reports $10.2 billion in unrestricted cash and investments, including 180 days cash on hand compared to 211 days in fiscal year 2022, in its latest filing.

Trinity is focused on diversifying its business by shifting to ambulatory, home health, PACE, urgent care, specialty pharmacy and telehealth. The filing also noted the recent launch of a new care delivery model dubbed TogetherTeam, involving on-site and virtual nurses, that is expected to be implemented systemwide by the end of its 2024 fiscal year.

Salaries, wages and employee benefit costs rose 2.2%, offset by a reduction of $54.6 million in executive compensation and $39.7 million more pharmacy rebates than in the same period in fiscal year 2022. Same-facility contract labor costs decreased more than 40% to $193.9 million, reflecting “unprecedented” pandemic-related costs during the third quarter in 2022.

Trinity “continues to use strong cost controls over contract labor and other operational spending as colleague investment and utilization of its FirstChoice internal staffing agency promotes labor stabilization,” management wrote.

Trinity Health spans 88 acute care hospitals and hundreds of other care locations in 26 states and purports to have the second-largest Medicare PACE (Program of All-inclusive Care for the Elderly) program in the country. It provided services to 1.3 million people and reported a community benefit and charity of $1.4 billion in fiscal year 2022.

A decline in COVID-19 funding and sustained expenses issues helped lead St. Louis-based Ascension to a $1.8 billion operating loss in the nine months ending March 31.

The nine-month loss was on revenue of $21.3 billion. In the quarter ending March 31, the 140-hospital system reported an operating loss of $1.4 billion on $6.9 billion in revenue.

Such losses compared with $640 million and $671 million deficits in the nine-month and three-month periods, respectively, ending March 31, 2022.

Expenses for the nine-month period increased 3.7 percent on the previous year to total $22.3 billion.

“The reduction in COVID-19 funding negatively impacted revenue in the current year,” Ascension management said in the filing. “Additionally, challenges to expenses continue to persist resulting from the inflationary environment.”

The operating losses were offset by improved non-operating income in the first three months of 2023 but not over the nine-month period, which saw a net deficit of $1.9 billion.

Ascension, which operates 2,600 sites of care across 19 states and Washington, D.C., had 219 days of cash on hand as of March 31 compared with 259 at the same time last year.

Pittsburgh-based UPMC’s operating income hit $100.4 million in the first quarter — up from $50.4 million in the prior year period — due to increased patient volumes, the growth of its insurance division and equity earnings in its investment in CarepathRx.

UPMC said quarterly results were partially offset by reduced pandemic-related funding and increased labor costs. First-quarter revenue increased 12 percent year over year to $6.9 billion and expenses rose 11 percent to $6.8 billion.

Year over year, UPMC’s admissions and observations increased 6 percent, while its health plan grew by almost 500,000 members to 4.5 million. UPMC attributed the 12 percent jump to the expansion of its behavioral health and Medicaid programs in eastern Pennsylvania.

“While meeting strong patient preference for care to be provided more conveniently in ambulatory settings closer to home, UPMC’s outpatient revenue increased 9 percent compared to a year ago,” CFO Edward Karlovich said in a May 25 news release. “Our patient volumes continue to shift from inpatient to outpatient settings.”

After including the performance of its investment portfolio and other nonoperating items, the 40-hospital system reported an overall gain of $187.3 million, compared with a loss of $226.2 million in the first quarter of 2022.

Fitch Ratings Senior Director Kevin Holloran dubbed 2022 the worst operating year ever and most nonprofit health systems reported large losses. However, the losses are shrinking and some systems have even reported gains during 2023 so far.

Cleveland Clinic reported $335.5 million net income for the first quarter of the year, compared with a $282.5 million loss over the same period in 2022. The health system reported revenue of $3.5 billion for the quarter. Cleveland Clinic has 321 days cash on hand, which puts it in a strong position for the future.

Boston-based Mass General Brighamreported $361 million gain for the second quarter ending March 31, which is up from a $867 million loss in the same period last year. The health system reported quarterly revenue jumped 11 percent year over year to $4.5 billion. The system’s quarterly loss on operations was down significantly this year, hitting $8 million, compared to $183 million last year.

Renton, Wash.-based Providence reported first quarter revenues were up 5.1 percent in 2023 to $7.1 billion, and operating loss is also moving in the right direction. The system reported $345 million operating loss in the first quarter of 2023, down from $510 million last year.

All three systems cited ongoing labor shortages and labor costs as a challenge, but are working on initiatives to reduce expenses. Cleveland Clinic and Mass General Brigham reported operating margin improvement to nearly positive numbers.

Kaiser Permanente, based in Oakland, Calif., also reported operating income at $233 million for the first quarter of the year, an increase from $72 million operating loss over the same period last year. The system is focused on advancing value-based care for the remainder of the year and its health plan grew more than 120,000 members year over year.

Even more regional systems are stemming their losses. SSM Health, based in St. Louis, went from a $57.4 million loss for the first quarter of 2022 to $16.5 million quarterly loss this year. Revenue increased 13.3 percent to $2.5 billion for the quarter, with increased labor expenses and inflation on supply costs continuing to weigh on the system.

UCHealth in Aurora, Colo., also reported a first quarter income of $61.8 million and revenue of more than $5 billion.

Not every system is seeing losses decline. Chicago-based CommonSpirit Health, which reported larger operating losses in the first quarter year over year, hitting $658 million and $1.1 billion for the nine-month’s end March 31. The system was able to reduce contract labor costs, but still finds hiring a challenge and spent time last year recovering from a cybersecurity incident.

Hospitals face a long road to financial recovery from the pandemic as inflation persists and labor shortages become the norm, but movement in the right direction is welcome.