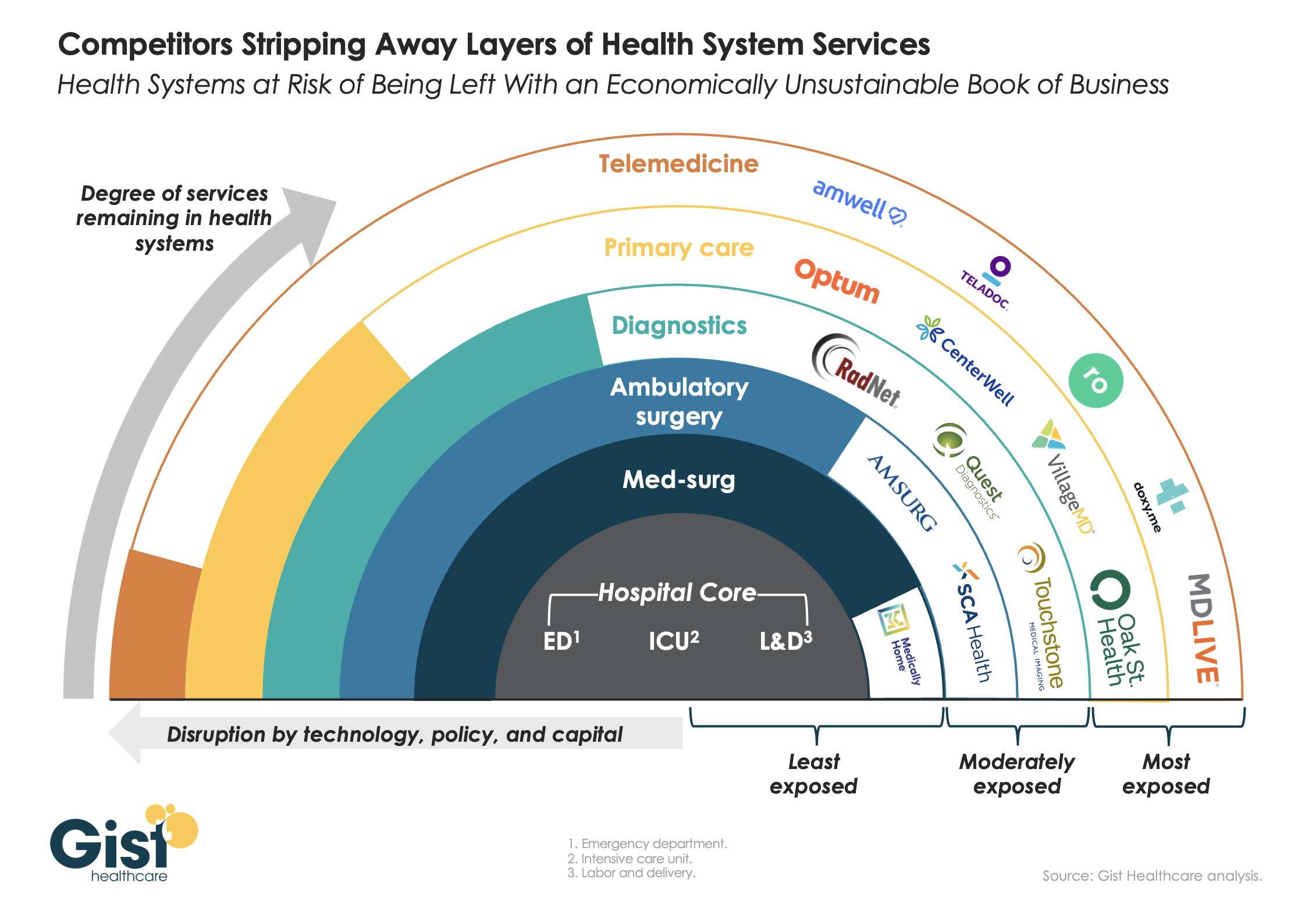

This week’s graphic features our assessment of the many emerging competitive challenges to traditional health systems.

Beyond inflation and high labor costs, health systems are struggling because competitors—ranging from vertically integrated payers to PE-backed physician groups—are effectively stripping away profitable services and moving them to lower-cost care sites. The tandem forces of technological advancement, policy changes, and capital investment have unlocked the ability of disruptors to enter market segments once considered safely within health system control.

While health systems’ most-exposed services, like telemedicine and primary care, were never key revenue sources (although they are key referral drivers), there are now more competitors than ever providing diagnostics and ambulatory surgery, which health systems have relied on to maintain their margins.

Moving forward, traditional systems run the risk of being “crammed down” into a smaller portfolio of (largely unprofitable) services: the emergency department, intensive care unit, and labor and delivery.

Health systems cannot support their operations by solely providing these core services, yet this is the future many will face if they don’temulate the strategies of disruptors by embracing the site-of-care shift, prioritizing high-margin procedures, rethinking care delivery within the hospital, and implementing lower-cost care models that enable them to compete on price.

West Reading, Pa.-based Tower Health continues to make progress on its performance improvement plan as its operating margin for the three months ended Sept. 30 rose to -4.2% from -8% during the same period in 2022. Its operating cash flow margin also increased from -0.9% to 2.3%.

During the first quarter of fiscal 2024, the three months ending Sept. 30, revenue decreased 2.9% year over year to $457.4 million. Expenses decreased 6.4% to $476.5 million.

Tower’s operating loss for the period was $19.1 million, compared with a loss of $37.6 million for the prior-year period.

As of Sept. 30, total balance sheet unrestricted cash and board-designated investment funds for capital improvements totalled $154 million — a decrease of $54 million from June 30, 2023. The main factors for the decrease were $15 million of debt service payments, physician incentive compensation payments of $9 million, capital expenditures of $6 million, negative changes in working capital of $32 million, partially offset by EBITDA of $10 million.

Total days of cash on hand for the system was 30 on Sept. 30.

After including the performance of its investment portfolio and other nonoperating items, the health system ended the three-month period with a net loss of $20.9 million, compared with a net loss of $37.6 million for the same period in 2022.

West Reading, Pa.-based Tower Health will be out of network for all Cigna Healthcare members starting Jan. 1 following a disagreement over reimbursement rates, the Reading Eagle reported Nov. 24.

The split applies to all Tower Health facilities and physicians for Cigna commercial, Medicare Advantage and behavioral health plans. Cigna said it is continuing to negotiate with Tower Health, but the health system has already begun to notify patients about the impending contract break.

“Tower Health, like other health systems, has been contending with unprecedented cost increases for personnel, supplies, equipment and medication necessary to continue providing high quality care,” a health system spokesperson told the Eagle. “Cigna has been unwilling to compensate Tower Health at reasonable payment rates.”

“We are disappointed that Tower Health is choosing to leave our network Jan. 1 unless we agree to their demands for significant rate increases that will make healthcare much more expensive for the people we serve,” a Cigna spokesperson told the Eagle. “It’s important to understand who pays the bills: any increase in cost of care is paid directly by local employers, their employees and families.”

Medicare Advantage and commercial claims denials have spiked across the country, leaving hospitals increasingly financially strapped, according to research published Nov. 17 by the American Hospital Association and Syntellis.

The report analyzed data from a national sample of 1,300 hospitals and health systems. From January 2022 to July 2023, revenue reductions related to Medicare Advantage denials increased 55.7% for the median hospital. During the same period, denial-related revenue reductions rose 20.2% for commercial plans. For denials relative to net patient service revenue for the median hospital, Medicare Advantage plans saw an increase of 63.3% and commercial plans rose 20%.

“[Hospitals] must take larger revenue reductions to account for those lost reimbursements from commercial payers and Medicare Advantage plans, which cover more than 31 million Americans and make up about half of all Medicare beneficiaries,” the report said. “The challenges will only worsen as Medicare Advantage enrollment continues to grow.”

In November 2022, an AHA survey found that half of hospitals and health systems reported having more than $100 million in unpaid claims that were more than 6 months old. As of June 2023, health systems had a median of 124 days cash on hand, down from 173 days in January 2022.

The new data coincides with recent reporting from Becker’s about hospitals across the country that have ended some or all Medicare Advantage contracts. The reasons behind contract terminations vary by system and by payer offering the plan. Some systems have cited steep losses amid excessive prior authorization denial rates and slow payments from insurers. Others have noted that most MA carriers have faced allegations of billing fraud from the federal government and are being probed by lawmakers over their high denial rates.

“It’s become a game of delay, deny and not pay,” Chris Van Gorder, president and CEO of San Diego-based Scripps Health, told Becker’s in September.

According to data shared with Becker’s by FTI Consulting, among the 64 contract disputes reported in the media this year through Sept. 30, 37 involved Medicare Advantage plans, and 10 disputes exclusively involved MA plans. In the third quarter alone, 15 disputes involved MA plans, compared to seven in the third quarter of 2022, a 115% increase year over year.

While hospitals’ overall performance declined slightly in September compared to the previous month, the median Kaufman Hall Calendar Year-To-Date Operating Margin Index reflecting actual margins was 1.4% in September. This slight increase was due to the historical variation in the performance of hospitals across 2023.

Volume decreased across the board, but data indicate improvement in the overall financial picture compared to 2022.

Does hospital ownership matter? According to a study published last week in Health Affairs Scholar, NOT MUCH. That’s a problem for not-for-profit hospitals who claim otherwise.

58% of U.S. hospitals are not-for-profit hospitals; the rest are public (19%) or investor-owned (24%). In recent months, not-for-profit systems have faced growing antagonism from regulators and critics who challenge the worthwhileness of their tax exemptions and reasonableness of the compensation paid their top executives.

The lion’s share of this negative attention is directed at large, not-for-profit hospital system operators. Case in point: last week, Banner Health (AZ) joined the ranks of high-profile operators taken to task in the Arizona Republic for their CEO’s compensation contrasting it to not-for-profit sectors in which compensation is considerably lower.

Unflattering attention to NFP hospitals, especially the big-name systems, is unlikely to subside in the near-term. U.S. healthcare has become a winner-take-all battleground increasingly dominated by large-scale, investor-owned interests in hospitals, medical groups, insurance, retail health in pursuit of a piece of the $4.6 trillion pie.

The moral high ground once the domain of not-for-profit hospitals is shaky.

The NYU study examined whether hospital ownership influenced decisions made by consumers: they found “Fewer than one-third of respondents (29.5%) indicated that hospital status had ever been relevant to them in making decisions about where to seek care…significantly more important to respondents who indicated the lowest health literacy—74.7% of whom answered the key question affirmatively—than it was for people who indicated high health literacy, of whom only 18.3% found hospital ownership status to be relevant…also considerably more relevant for people working in health care than for those who did not work in health care (61.0% vs 24.5%)…

We found little evidence that hospital nonprofit status influenced Americans’ decisions about where to seek care. Ownership status was relevant for fewer than 30% of respondents and preference was greatest overall for public hospitals. Only 30–45% of respondents could correctly identify the ownership status of nationally recognized hospitals, and fewer than 30% could identify their local hospitals.

These findings suggest that contract failure does not currently provide a justification of nonprofit hospitals’ value; further scrutiny of tax exemption for nonprofit hospitals is warranted.”

Are NFP hospitals concerned? YES. It’s reality as systems address near term operational challenges and long-term questions about their strategies.

Last weekend, I facilitated the 4th Annual Chief Strategy Officers Roundtable in Austin TX sponsored by Lumeris. The group consisted of senior-level strategists from 11 not-for-profit systems and one for-profit. In one session, each reacted to 50 future state scenarios in terms of “likelihood” and “disruptive impact” in the NEAR term (3-5 years) and LONG TERM (8-10 years) using a 1 to 10 scale with 10 HI.

From these data and the discussion that followed, there’s consensus that the U.S. healthcare market is unlikely to change dramatically long-term, their short-term conditions will be tougher and their challenges unique.

‘Near-term cost containment is a priority. Hospitals are here-to-stay, but operating them will be harder.’

‘Increased scale and growth are necessary imperatives for their systems.’

‘Hospital systems will compete in a market wherein private capital and investor ownership will play a growing role, insurers will be hostile and value will the primary focus of cost-reduction by purchasers and policymakers.’

‘Distinctions betweennot-for-profit and for-profit hospitals are significant.’

‘Conditions for hospitals will be tougher as insurers play a stronger hand in shaping the future.’

Given the NYU study findings (above) concluding NFP ownership has marginal impact on hospital choices made by consumers, it’s understandable NFPs are anxious.

My take:

The issues facing not-for-profit hospitals in the U.S. are unique and complex. Per the commentary of the CSOs, their market conditions are daunting and major changes in their structure, funding and regulation unlikely.

That means lack of public understanding of their unique role is a conundrum.

Paul

PS: Issues about CEO compensation in healthcare are touchy and often unfair.

In every major NFP system, comp is set by the Independent Board Compensation Committee with outside consultative counsel. The vast majority of these CEOs aren’t in the job for the money joining their workforce in pursuit of the unique higher calling afforded service leaders in NFP healthcare.

How should health systems spend their “community benefit” dollars?

That question was at the heart of a discussion we participated in recently at a member board meeting. To maintain their nonprofit status, all health systems are required to devote a portion of their earnings to activities that benefit the communities they serve, based on an assessment of local health needs.

The question our member’s board was grappling with, led by the system’s executive team, was how to ensure their “investment” in the community is as leveraged as possible, and generates the greatest “bang for the buck” in terms of better community health.

As the importance of addressing the social determinants of health grows, many systems are trying to target their resources toward activities that that enhance their ability to improve health status, and to reduce the barriers to better health faced by many. That requires a level of rigor and commitment to “community ROI” that goes beyond simply pointing to charity care statistics and the number of uninsured served.

What most impressed us in the discussion was the application of the same investment mindset to community benefit that the system brings to capital allocation decisions—with due attention to implementation plans, outcomes metrics, and accountability.

As the system’s COO framed it, “We don’t just want to be a ‘piggy bank’ for charitable causes, we want to make sure our investment in the community is really making a difference” in local residents’ health. At the same time, the board recognized that its role extends beyond simply contributing dollars to acting as a convener and facilitator of other community organizations working together toward a common set of goals. A worthy discussion for the board, for sure, and a priority we’re seeing leading systems begin to embrace in a serious way.

Around 400 primary and urgent care physicians, along with 150 nurse practitioners and physician assistants, employed by Minneapolis, MN-based Allina Health System have voted to unionize with the Service Employees International Union, forming the largest private-sector union of physicians in the country.

Allina, which operates 12 hospitals across Minnesota and Wisconsin, already saw over 100 inpatient physicians at its Mercy Hospital vote to unionize earlier this year. While Mercy’s physicians organized against pressure to adhere to the hospital’s new length-of-stay guidelines, this larger group of clinic-based providers say they are motivated by chronic understaffing that they claim has caused burnout and threatened patient safety. Allina Health laid off 350 workers this summer after posting a nearly $200M operating loss in 2022.

The Gist:When health systems originally recruited physicians into their newly developed employed medical groups, many pitched the arrangement as more of a partnership than traditional employment.

However, now that a majority of the nation’s physicians are employed by hospitals, some physicians are rethinking their relationships with their employers.

Only six percent of doctors were unionized in 2021, but a recent spate of unionization efforts by residents and physicians suggest that number is on the rise.

Health systems hoping to address physicians’ concerns and unionization activity should note that the motivating factors cited by organizing physicians surround working conditions, including a lack of support staff and professional autonomy, rather than personal wage demands.

Earlier this month, Governor Gavin Newsom signed a bill that puts all full- and part-time California healthcare workers, including all ancillary support staff, on a path to earning $25 per hour.

While wage increases will begin phasing in next year, the timeline for implementation depends on facility type and other factors like payer mix. Large health systems and dialysis centers have until 2026 to fully implement the new wage, while rural, independent hospitals and those with high public payer mixes, as well as other clinical facilities, have more time to comply.

The law, which replaces the $15.50 state minimum wage for all workers, is projected to impact over 469K healthcare workers in the state, potentially including 50K who already earn more than $25 per hour but are forecasted to receive wage increases to maintain their pay premiums. Strongly backed by California healthcare unions, the law ultimately received the support of the California Hospital Association on the grounds that it will “create stability and predictability for hospitals” by preempting local wage and compensation measures active in many California cities.

The Gist:On the heels of a tentatively successful labor negotiation with Kaiser Permanente—which would raise the system’s hourly minimum wage to $25—California healthcare unions have flexed their might for another win.

While this new law directly benefits healthcare workers earning less than $25 an hour, itsknock-on effects will extend to those earning above that to avoid pay compression, as well as to workers in other industries that draw from the same labor pool.

The mandated higher pay may provide California healthcare employers with a recruitment edge (and lure talent away from neighboring states), but higher costs will exacerbate the margin challenges plaguing many hospitals in the state.