Given the somewhat frantic pace at which transactions are happening in healthcare these days, with insurers buying up primary care assets, private equity firms rolling up specialty practices, hospital systems looking to consolidate, and everyone circling around digital players, it’s little surprise that we’ve begun to hear some angst among health system executives about their ability to keep pace.

“Some of these disruptors are focused entirely on M&A strategies,” one CEO told us recently. “My team still has to run a complex health system at the same time. It takes us forever to get deals done.”

The concern is legitimate: for many health systems, M&A has been a one-at-a-time proposition. Evaluating and completing an acquisition takes many months, if not a year or more—and the integration of even a relatively small entity into a larger health system often takes longer.

There is a growing sentiment that the pace of single, sequential mergers and acquisitions will not allow health systems to keep pace.

One CFO shared, “We did a large merger a decade ago, and we’re just at the point of feeling like we act as a single system. We’re looking at one or two others, and we can’t delay the next opportunity because we’re still working to integrate the last.”

His strategy: systems aiming to build a super-regional organization should “rapidly build the network and integrate it once you have all the pieces”. It’s a strategy, he said, that is serving vertically integrated payers like CVS and UHG well. To keep pace in a consolidating market, health systems must maintain a pipeline of potential partners that fit with their vision. But we’re also wary of “saving” all the integration until the deals are done.

Rather, health systems looking to rapidly expand must be able to “parallel process” multiple acquisitions and integration. With smaller financial reserves compared to payer behemoths, health systems need mergers to generate value more quickly. And moreover, as providers are held to a higher standard by regulators, new partnerships will benefit from demonstrating value to consumers and communities.

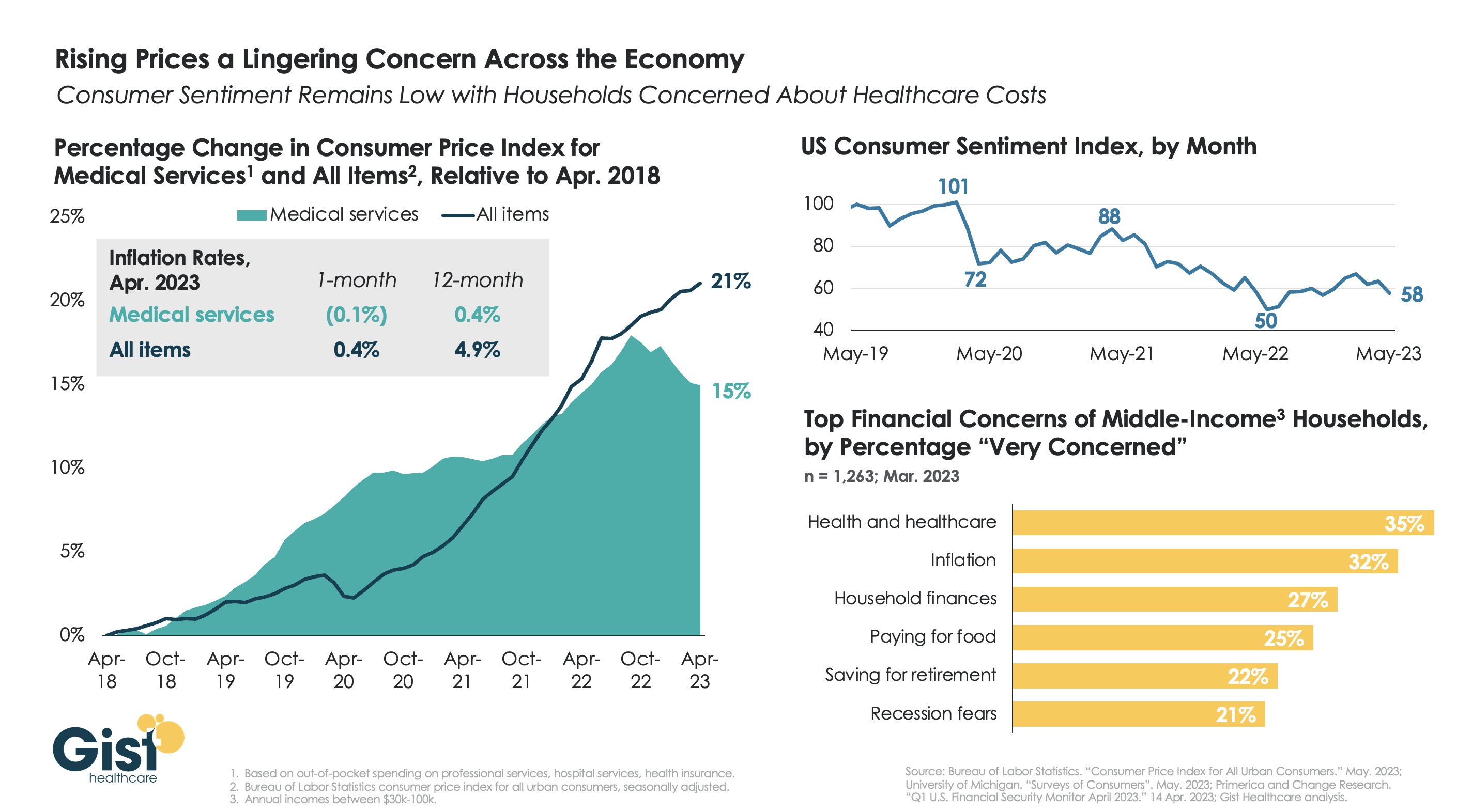

With the latest Bureau of Labor Statistics’ Consumer Price Index (CPI) report revealing the 12-month inflation rate in April 2023 rose again after hitting a recent low in March, we’re using this week’s graphic to show the cumulative picture on price and consumer sentiment changes across the last five years.

Since 2018, the CPI for all goods has risen 21 percent, while medical services have become 15 percent more expensive, in terms of consumer out-of-pocket spending. Leading into COVID, medical service prices were rising faster than general inflation, but the cumulative rise in the price of all goods caught up to medical services in early 2022.

Since December of last year, the price of medical services has actually experienced some deflation, partly due to a lagging decline in insurer profits. Reports of easing inflation had elicited a slight rebound in consumer sentiment, but last month’s 9 percent drop, the largest since June 2022, suggests this confidence is easily shaken.

Unfortunately for healthcare providers, according to a recent poll, fewer consumers worrying about elevated grocery and gas prices means that healthcare has reclaimed the top spot for household financial concerns.

Last month, Eric Jordahl, Managing Director of Kaufman Hall’s Treasury and Capital Markets practice, blogged about the dangers of nonprofit healthcare providers’ extremely conservative risk management in today’s uncertain economy.

Healthcare public debt issuance in the first quarter of 2023 was down almost 70 percent compared to the first quarter of 2022. While not the only funding channel for not-for-profit healthcare organizations,

the level of public debt issuance is a bellwether for the ambition of the sector’s capital formation strategies.

While health systems have plenty of reasons to be cautious about credit management right now, it’s important not to underrate the dangers of being too risk averse. As Jordahl puts it: “Retrenchment might be the right risk management choice in times of crisis, but once that crisis moderates that same strategy can quickly become a risk driver.”

The Gist: Given current market conditions, there are a host of good reasons why caution reigns among nonprofit health systems, but this current holding pattern for capital spending endangers their future competitiveness and potentially even their survival.

Nonprofit systems aren’t just at risk of losing a competitive edge to vertically integrated payers, whom the pandemic market treated far more kindly in financial terms, but also to for-profit national systems, like HCA and Tenet, who have been flywheeling strong quarterly results into revamped growth and expansion plans.

Health systems should be wary of becoming stuck on defense while the competition is running up the score.

Last week, California’s legislature passed a bill establishing the Distressed Hospital Loan Program, which will dole out $150M in interest-free emergency loans to struggling nonprofit hospitals in the state which meet specific eligibility criteria, including operating in an underserved area and serving a large share of Medicaid beneficiaries. A combination of state agencies will establish a specific methodology for selection, but hospitals that are part of a health system with more than two separately licensed hospital facilities will be ineligible.

Hospitals receiving loans must provide a plan for how they will use the loans to achieve financial sustainability, and must pay back the money within six years.

The Gist: With twenty percent of the state’s hospitals at risk of shuttering, California lawmakers are hoping to provide the most vulnerable hospitals an alternative to either closure or consolidation, an example other states may follow. But unlike the Paycheck Protection Program loans that shored up businesses through the pandemic’s initial disruption, the outlook for small, struggling, independent hospitals isn’t expected to improve in coming years, even if the economy recovers.

Whether these loans provide lifelines or merely serve as Band-Aids on an untenable situation will depend on whether recipient hospitals can use them to restructure their operating models to absorb increased labor costs amid stagnating volumes and commercial reimbursement.

If these loans aren’t used for transformation, they will only delay the inevitable: more closures, and more mergers to find shelter in scale.

The healthcare financings that came in the past couple of weeks generally did well. Maturities seemed to do better than put bonds, and it remains important to pay attention to couponing and how best to navigate a challenging yield curve. But these are episodic indicators rather than trends, given that the scale of issuance remains muted. Other capital markets—like real estate—are becoming more active and offer competitive funding and different credit considerations relative to debt market options. Credit management continues to be the main driver of low external capital formation, but those looking for outside funding should spend time up front considering the full array of channels and structures.

This Part of the Crisis

And now it’s official. After JPMorgan acquired First Republic Bank—with a whole lot of help from the Federal Deposit Insurance Corporation—CEO Jamie Dimon declared, “this part of the crisis is over.” Not sure regional bank shareholders would agree, but from Mr. Dimon’s perspective the biggest bank got bigger, which made it a good day.

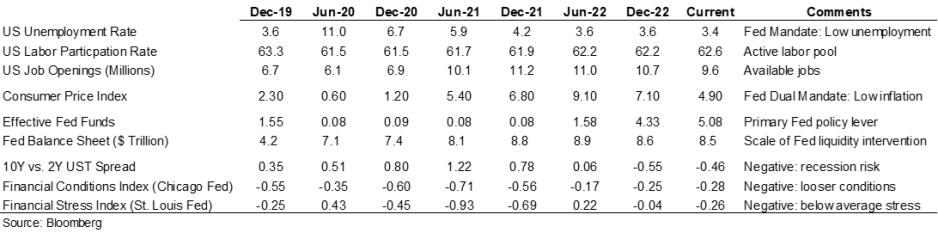

Last week the Federal Reserve raised rates another 25 basis points and the expectation (hope) seems to be that the Fed has reached the peak of its tightening cycle or will at least pause to see if constrictive forces like higher rates and regional bank balance sheet deflation slow activity enough to bring inflation back to the 2.0% Fed target. Assuming this is a pause point, it makes sense to check in on a few economic and market indicators.

Inflation is improving, although it remains well above the Fed’s 2.0% target range, and there are other indicators (like labor participation and unemployment) that have recovered some of the ground lost in 2020. But the weird part remains that this all seems quite civilized. To some, the Treasury curve spread continues to suggest a recession is looming, but in my neighborhood workers are still in short supply, restaurants are busy, and contractors are booked well into the future. Today’s ~3.36% 10-year Treasury rate is less than 100 basis points higher than the average since the start of the Fed interventionist era in 2008 and a whopping 257 basis points lower than the average since 1965. Think about how much capital has been raised in market environments much worse than now (including most of the modern-day healthcare inpatient infrastructure). Again, the main culprit in retarded capital formation is institutional credit management concerns rather than the funding environment.

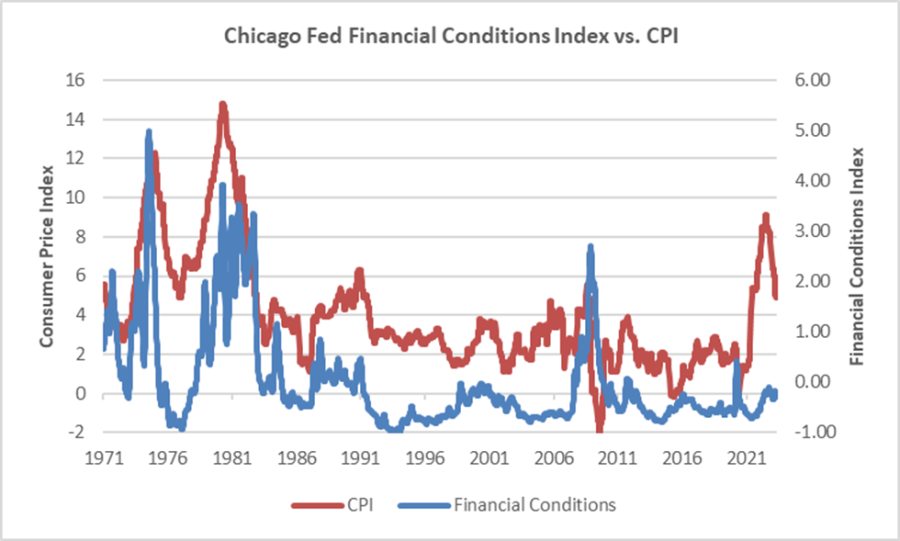

The major fallout from the Fed’s recent anti-inflation efforts seems concentrated with financial intermediaries rather than consumers (or workers), and the financial intermediary stress the Fed is relying on to help curb economic activity is grounded in their own balance sheet management decisions rather than deteriorating loan portfolios. We’ve looked at this before, but it bears repeating that in the “great inflation” of the 1970s, the Chicago Fed’s Financial Conditions Index reached its highest recorded points (higher means tighter than average conditions) and in this most recent inflationary cycle, that same index has remained consistently accommodative. Can you wring inflation out of a system while retaining relatively accommodative financial conditions? Which begs the question of whether any Fed pause is more about shifting priorities: downgrading the inflation fight in favor of moderating the financial intermediary threat? We might be living a remake of the 1970s version of stubborn inflation, which means that all the attendant issues—rolling volatility across operations, financing, and investing—might be sticking around as well.

Meanwhile, somewhere out in the Atlantic the debt ceiling storm is forming. Who knows whether it will make landfall as a storm or a hurricane, but it does remind us that the operative portion of the Jamie Dimon quote noted above is this part of the crisis is over. The next part of the long saga that is about us climbing out of a deep fiscal and monetary hole will roll in and new variations of the same central challenge will emerge for healthcare leaders.

A Healthcare Makeover

Ken Kaufman has been advancing the idea that healthcare needs a “makeover” to align with post-COVID realities. Look for a piece from him on this soon, but the thesis is that reverting to a 2019 world isn’t going to happen, which means that restructuring is the only option. The most recent National Hospital Flash Report suggests improving margins, but they remain well below historical norms and the labor part of the expense equation is structurally higher. Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.

My contribution to Ken’s argument is to reemphasize that balance sheet is the essential (only) bridge between here and a restructured sector and the journey is going to require very careful planning about how to size, position, and deploy liquidity, leverage, and investments. Of course, the central focus will be on how to reposition operations. But if organic cash generation remains anemic, the gap will be filled by either weakening the balance sheet (drawing down reserves, adding leverage, or adopting more aggressive asset allocation) or by partnering with organizations that have the necessary resources.

Organizations reach the point of greatest enterprise risk when the scale of operating challenges outstrips the scale of balance sheet resources. Missteps are manageable when the imbalance is the product of rapid growth but not when it is the result of deflating resources. If the core imperative is to remake operations, the co-equal imperative is continuously repositioning the balance sheet to carry you from here to whatever defines success.

Livonia, Mich.-based Trinity Health is restructuring leadership on the West Coast as it combines Saint Agnes Medical Center in California and Saint Alphonsus Health System in Idaho and Oregon into one regional ministry, according to a statement shared with Becker’s May 4.

Trinity Health said the combination will allow these ministries “to streamline management and decision-making, reduce administrative costs and improve overall operating performance.”

The ministries will keep their names, and the boards of directors for each ministry will remain separate, the health system said. There will also be leadership changes.

Nancy Hollingsworth, MSN, RN, will retire as president and CEO of Fresno, Calif.-based Saint Agnes, effective May 26. Odette Bolano, BSN, president and CEO of Boise, Idaho-based Saint Alphonsus, will become president and CEO of the new regional entity. Additionally, David Spivey will join Saint Agnes as interim president and market leader.

This is a natural progression, as several services have already been consolidated between Saint Agnes and Saint Alphonsus, Trinity Health said.

The health system has also merged ministries in other regions, including Michigan, Indiana, Illinois, Iowa and New York.

Trinity Health has 123,000 employees in 26 states, according to its website.

Here are 24 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global in 2023.

Note: This is not an exhaustive list. Health system names were compiled from credit rating reports.

1. Atrium Health has an ‘AA-‘ and stable outlook with S&P Global. The Charlotte, N.C.-based system’s rating reflects a robust financial profile, growing geographic diversity and expectations that management will continue to deploy capital with discipline.

2. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

3. CaroMont Health has an “AA-” rating and stable outlook with S&P Global. The Gastonia, N.C.-based system has a healthy financial profile and robust market share in a competitive region.

4. CentraCare has an “AA-” rating and stable outlook with Fitch. The St. Cloud, Minn.-based system has a leading market position, and its management’s focus on addressing workforce pressures, patient access and capacity constraints will improve operating margins over the medium term, Fitch said.

5. Children’s Minnesota has an “AA” rating and stable outlook with Fitch. The Minneapolis-based system’s broad reach within the region continues to support long-term sustainability as a market leader and preferred provider for children’s health care, Fitch said.

6. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

7. El Camino Health has an “AA-” rating and stable outlook with Fitch. The Mountain View, Calif.-based system has a history of generating double-digit operating EBITDA margins, driven by a solid market position that features strong demographics and a very healthy payer mix, Fitch said.

8. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

9. Hoag Memorial Hospital Presbyterian has an “AA” rating and stable outlook with Fitch. The Newport Beach, Calif.-based system’s rating is supported by a leading market position in its immediate area and very strong financial profile, Fitch said.

10. Inspira Health has an “AA-” rating and stable outlook with Fitch. The Mullica Hill, N.J.-based system’s rating reflects its leading market position in a stable service area and a large medical staff supported by a growing residency program, Fitch said.

11. Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The Rochester, Minn.-based system’s credit profile characterized by its excellent reputations for clinical services, research and education, Moody’s said.

12. McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The Grand Blanc, Mich.-based system has a leading market position over a broad service area covering much of Michigan and a track-record of profitability despite sector-wide market challenges in recent years, Fitch said.

13. Novant Health has an “AA-” rating and stable outlook with Fitch. The Winston-Salem, N.C.-based system has a highly competitive market share in three separate North Carolina markets, Fitch said, including a leading position in Winston-Salem (46.8 percent) and second only to Atrium Health in the Charlotte area.

14. NYC Health + Hospitals has an “AA-” rating with Fitch. The New York City system is the largest municipal health system in the country, serving more than 1 million New Yorkers annually in more than 70 patient locations across the city, including 11 hospitals, and employs more than 43,000 people.

15. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

16. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

17. Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The Cape Girardeau, Mo.-based system enjoys robust operational performance and a strong local market share as well as manageable capital plans, Fitch said.

18. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

19. Stanford Health Care has an “AA” rating and stable outlook with Fitch. The Palo Alto, Calif.-based system’s rating is supported by its extensive clinical reach in the greater San Francisco and Central Valley regions and nationwide/worldwide destination position for extremely high-acuity services, Fitch said.

20. SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system has a strong financial profile, multi-state presence and scale, with solid revenue diversity, Fitch said.

21. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

22. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

23. WellSpan Health has an “Aa3” rating and stable outlook with Moody’s. The York, Pa.-based system has a distinctly leading market position across several contiguous counties in central Pennsylvania, and management’s financial stewardship and savings initiatives will continue to support sound operating cash flow margins when compared to peers, Moody’s said.

24. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

The University of South Alabama Health Care Authority has announced plans to acquire Providence Health System from St. Louis-based Ascension. The transaction is subject to routine regulatory approval as well as customary closing conditions and is expected to close in the fall of 2023.

About the Transaction

USA Health engaged Cain Brothers, a division of KeyBanc Capital Markets, to serve as their strategic financial advisor based on its deep academic medicine and health system sector knowledge. USA Health and Providence have a longstanding relationship and the transaction will help the organizations enhance access to high quality healthcare in the Mobile community and further USA Health’s ability to fulfill its tripartite mission of education, research, and clinical care. The transaction expands USA Health’s footprint in the greater Mobile market, ensuring that the community has access to sustainable, quality healthcare long into the future.

About USA Health

USA Health is located in Mobile, AL, and stands as the only academic health system along the upper Gulf Coast. The system is comprised of nearly 30 care delivery locations, including USA Health University Hospital, the USA Health Mitchell Cancer Institute, USA Health Children’s & Women’s Hospital, a Level I trauma center, a comprehensive stroke center, and a Level III NICU. USA Health employs 3,900 clinical and nonclinical staff members, including 180 academic physicians who serve dual roles treating patients and teaching the next generation of medical doctors.

About Providence Health System

Mobile, AL-based Providence Hospital, which was founded in 1854 by the Daughters of Charity, is a full-service 349 bed hospital with 24/7 emergency care, a Level III trauma center, an outpatient diagnostic center, and a freestanding rehabilitation and wellness center. In addition to the hospital, Providence operates related sites of care throughout the greater Mobile community, including the physician practices of Ascension Medical Group. Providence became part of Ascension in 1999 when the Daughters of Charity and Sisters of St. Joseph Health System merged to form Ascension.

About Ascension

Ascension is one of the nation’s leading not-for-profit and Catholic health systems, with a mission of delivering compassionate, personalized care to all with special attention to persons living in poverty and those most vulnerable. Ascension includes approximately 37,000 aligned providers and operates more than 2,600 sites of care – including 138 hospitals in 19 states.

Twenty U.S. hospitals have received consecutive “A” safety grades from The Leapfrog Group since 2012, according to the group’s spring safety grades released May 3.

Since 2012, Leapfrog has assigned letter grades to nearly 3,000 acute-care general hospitals across the nation every fall and spring. The safety grades evaluate hospitals’ performance on up to 22 patient safety measures from CMS, the Leapfrog Hospital survey and other supplemental sources. The safety grades are the only hospital ratings program solely based on hospitals’ ability to protect patients from preventable errors, accidents, injuries and infections.

Twenty hospitals have received 23 consecutive “A” grades since the launch.

Last fall, 22 hospitals achieved consecutive “A” grades. For the spring grades, two hospitals lost their consecutive “A” streak: Sentara Williamsburg Regional Medical Center in Virginia and Sierra Vista Regional Medical Center in San Luis Obispo, Calif., both earned a “B.”

Read more about Leapfrog’s hospital safety grade methodology here.

Here are the 20 hospitals that have achieved 23 consecutive “A” grades:

Arizona

Mayo Clinic Hospital (Phoenix)

California

French Hospital Medical Center (San Luis Obispo)

Kaiser Permanente Orange County-Anaheim Medical Center

Colorado

Rose Medical Center (Denver)

Florida

AdventHealth Daytona Beach

Illinois

Elmhurst Memorial Hospital

University of Chicago Medical Center

Northwestern Medicine Central DuPage Hospital (Winfield)

Massachusetts

Beverly Hospital

Saint Anne’s Hospital (Fall River)

Michigan

University of Michigan Health (Ann Arbor)

Mississippi

Baptist Memorial Hospital Golden Triangle (Columbus)

Here are 15 major hospital and healthcare merger and acquisition-related transactions from April:

Brentwood, Tenn.-based Quorum Health is selling Waukegan, Ill.-based Vista Medical Center East to American Healthcare Systems, the Lake County News-Sun reported April 28. The hospital will change hands by May 31. American Healthcare Systems is based in Los Angeles.

West Virginia will soon likely see a combined four-hospital system as Huntington-based Mountain Health Network, Marshall Health and Marshall Universityseek to combine. The combination should be completed by the end of this year.

Yale New Haven (Conn.) Health continues to push for the acquisition of three hospitals owned by private equity-backed Prospect Medical Holdings. The system made its case to the state’s certificate of need committee as to why it is better placed to acquire the three sites.

Oakland, Calif.-based Kaiser Permanente agreed to acquire Geisinger Health in a deal that will make the Danville, Pa.-based health system the first to join Risant Health, a new nonprofit organization created by the Kaiser Foundation Hospitals. The newly formed entity, which still has to be approved by regulators, would eventually look to acquire four to six other systems.

Mobile, Ala.-based University of South Alabamaconfirmed April 19 it is buying Ascension Providence Hospital in the city in an $85 million transaction that includes the hospital’s clinics.

The Oregon Health Authority on April 13 approved Roseville, Calif.-based Adventist Health‘s acquisition of the Mid-Columbia Medical Center in The Dalles, Ore., according to the Columbia Community Connection.

Lumberton, N.C.-based UNC Health Southeastern is transitioning two of its business areas, seeking to sell a long-term care facility and transferring its current outpatient hospice program.

Salt Lake City-based Intermountain Health is partnering with two Idaho hospitals as a minority investor. The 33-hospital system is investing in Idaho Falls Community Hospital and 43-bed Mountain View Hospital, also based in Idaho Falls.

Two Wisconsin health systems — Froedtert Health and ThedaCare — signed a letter of intent to merge into a single system. Milwaukee-based Froedtert and Neenah-based ThedaCare announced the plan to combine April 11 with the goal to close the deal by the end of the year.

Franklin, Tenn.-based Community Health Systems has struck agreements to sell four hospitals across three states in 2023.

Mechanicsburg, Pa.-based Select Medical has acquiredVibra Hospital of Richmond, a 63-bed acute care facility in Richmond, Va. Terms were not disclosed. The hospital, which will take up the name Select Specialty Hospital-Richmond, will continue to provide post-ICU medical care for chronic and critically ill patients requiring long-term care, according to an April 5 release.

Carle Health has added three Peoria, Ill.-based UnityPoint Health-Central Illinois hospitals into its system. The closing, which took place April 1, integrates Methodist, Proctor and Pekin hospitals under Carle, along with 76 clinics and Methodist College, according to an April 3 news release from Carle Health. Urbana, Ill.-based Carle Health now has eight hospitals in its system following the deal’s closing.

Ann Arbor-based University of Michigan Healthacquired Lansing, Mich.-based Sparrow Health System to become a $7 billion health system with more than 200 sites of care.

Franklin, Tenn.-based Community Health Systemscompleted a $92 million sale of Oak Hill, W.Va.-based Plateau Medical Center to Charleston, W.Va.-based Vandalia Health. The healthcare giant closed on the transaction April 1.

South Arkansas Regional Hospital signed a definitive agreement to acquire El Dorado-based Medical Center of South Arkansas from subsidiaries of Community Health Systems. The deal is expected to close in the summer.