In Las Vegas this week, 10,000 healthcare entrepreneurs, investors, purchasers and industry onlookers are gathered to celebrate the business of U.S. healthcare. It follows the inaugural Nashville Healthcare Sessions last month that drew a crowd to Music City touting “the premier healthcare conference set in the most relevant, exciting, and welcoming city in the south.“

Besides their locations and exceptional marketing, three notable themes are prominent that speak volumes about where this industry is:

1- The focus is systemness—integrated, connected, data-driven and scalable. Traditional divides that separate health and social services, hospitals and insurers, biotherapeutics and companion diagnostics are obsolete and access to private capital and swift execution vitals. And embedded in systemness is an expanded role of human resources that create workforces that are right-sized, diverse, AI-enabled and productive. 2-Technologies focused on end user value are gaining traction. Solutions that enable better, quicker, more accurate and affordable transactions with consumers are prominent. While traditional providers—hospitals, physicians, long-term care providers and public health programs– see HIT and AI investments as ways to make their work more efficient and satisfying, disruptors are focused on the untapped consumer market that’s dissatisfied with the status quo. 3-Access to smart capital is key. The venture capital and private equity markets in healthcare services are weathering corrections that have deflated returns and forced many to pullback or exit. The possibility of regulatory reforms involving greater transparency, carried interest restrictions and minimum hold periods means stronger funds with experienced operating partners and stable LP funding will be advantaged. In Vegas, they’ll be working the hallways to find tuck-ins for their platform bets and courting not-for-profit hospitals needing non-operating income to fund their growth and diversification efforts.

Those attending recognize the U.S. health industry faces unprecedented challenges:

Growing employer activism against lack of price transparency and inexplicably high unit costs for hospital care, prescription drugs, insurer overhead and mal-effect of consolidation in each sector.

Medical inflation that’s persistent but disproportionately absorbed by fewer and fewer employers and individuals who lack bargaining power.

Value-based purchasing activities that have failed to achieve desired cost containment goals.

Public dissatisfaction with the “system” and growing receptivity to alternatives.

Growing hostility in media coverage about hospitals, especially large not-for-profit hospitals, deemed to be profitable and wasteful.

Increased tension between providers (hospitals, medical groups) and insurers.

Increased regulation in states and court rulings that change (or have the potential to alter) how care is defined, provided, funded and legally authorized.

HLTH and Session attendees recognize the uncertainties of the political, economic and global markets in which healthcare operates. Israel will be front of mind to all as the fast-paced HLTH proceedings continue this week.

The root causes of the system’s poor performance are understood and considered: they’re daunting. But that does not impede the willingness of private investors to make bets presuming the future of the U.S. healthcare is not a repeat of its past.

Contrary to pop culture, what happens in Vegas this week will not stay in Vegas: that’s the point. The health system is not working well. While some HLTH and Sessions attendees are no doubt focused on incremental innovations to improve the performance of their legacy organizations, others are looking beyond. And, if industries akin to healthcare like financial services and higher education are instructive, the latter are better prepared to respond than the former.

PS: Nearly 50 years to the day after the Yom Kippur War in 1973, Israel was again taken by surprise by a sudden attack. Unlike the series of clashes with Palestinian forces in Gaza over the past few years, this appears to be a full-scale conflict mounted by Hamas and its allies including Iran.

Thousands are dead, more are injured and the health systems in both will be overwhelmed by the need. Health systems matter!

The hospital workforce is critical to the care process and is most often the largest expense on a hospital or health system’s balance sheet. Even before the pandemic, labor expenses — which include costs associated with recruitment and retention, employee benefits and incentives — accounted for more than 50 percent of hospitals’ total expenses, according to the American Hospital Association.

As a result, a slight increase in labor costs can have a tremendous effect on a hospital or health system’s total expenses and operating margins. Hospitals across the country are focused on managing the premium cost of labor, while recruiting and retaining talent remains a priority, and the cost of supplies and drugs also increases due to inflation.

Here’s how 23 health systems’ labor costs are tracking based on the results of their most recent financial documents.

Note: This is not an exhaustive list. Most of the following health systems’ labor costs are for the three months ending 30, with others for the six months ending June 30 and the 12 months ending June 30 — the most recent periods for which financial data is available. The year-over-year percentage increase/decrease is also included.

21. CommonSpirit Health (Chicago) Salaries and benefits: $18.3 billion (+0.7 percent YOY) *For the 12 months ended June 30 **Merged with Broomfield, Colo. -based SCL Health in April 2022

22. Ascension (St. Louis) Salaries, wages and employee benefits: $14.3 billion (-1.3 percent YOY) *For the 12 months ended June 30

Health plan and health system CFOs point to the current economic situation when asked to identify their top concern, according to a Sept. 14 survey from Deloitte.

The consulting firm surveyed 60 finance chiefs at American health plans and health systems about their priorities and paths forward and shared their findings with Becker’s.

Inflationary pressures have created a cost-heavy operating model for many organizations, CFOs told Deloitte. Coupled with higher care delivery, labor and supply costs — and slowed revenue growth

— financial viability weighs heavily on leaders.

More than 40 percent of health system CFOs believe their health systems may need more than two years to reach the profit levels they generated before the COVID-19 pandemic.

Seventy percent of CFOs identified the current economic situation as a greater concern than it was last year. Meanwhile, 57 percent pointed to new regulatory requirements as a growing concern, and 51 percent said the same of the current operating model and structure.

The latest Altarum Health Sector Economic Indicators show that health spending as a percent of GDP has stabilized near 17.5%, health care price growth and economywide inflation recently converged, and the health sector added over 60,000 jobs in July. See the highlights below.

Health spending as a percent of GDP has stabilized at 17.5%

In June 2023, national health spending grew by 5.0%, year over year, and now represents 17.5% of GDP, equal to the average percent of GDP for the previous 12 months.

Nominal GDP in June 2023 was 5.8% higher than in June 2022, and grew 0.8 percentage points faster than health spending.

Neglecting government subsidies, spending on personal health care in June increased by 8.1%, year over year, and by 7.3% when subsidies are included, exceeding the GDP growth rate for the fifth consecutive month.

Neglecting government subsidies, year-over-year spending on home health care (12.2%) and nursing home care (12.0%) grew fastest in June, while physician and clinical services spending increased the least (6.9%) among major categories.

Personal health care growth (neglecting government subsidies), which continues to be dominated by growth in utilization rather than price increases, has slowed somewhat in the past 4 months.

Health care price growth and economywide inflation finally converge

The overall Health Care Price Index (HCPI) increased by 2.7% year over year in July, slowing 0.1 percentage points from the slightly revised rate in June (2.8%).

For the first time in over two years, health care price growth exceeded overall inflation as economywide price growth (measured by the GDP Deflator) fell to 2.6% in June, its lowest growth rate since March 2021.

In new data for July, overall year-over-year CPI growth actually increased slightly to 3.2%, the first increase in its growth rate since June 2022, driven primarily by changes in commodities price growth.

Among the major health care categories, prices for nursing home care (5.5%) and dental care (5.1%) grew fastest, while physician and clinical services (0.7%) price growth was the slowest in July.

Year-over-year growth in hospital prices paid by private payers fell nearly 2.5 percentage points over the past two months (from 6.1% in May to 3.7% in July), beginning to converge with public payer price growth. In July, growth in Medicare and Medicaid hospital prices reached 2.6% and 2.3% growth respectively.

Our implicit measure of health care utilization growth declined in June, up 4.5% year over year, and down somewhat from slightly revised data (4.9% growth) a month prior.

Health care adds 63,000 jobs in July, the largest increase since July 2022

Health care added 63,000 jobs in July 2023, exceeding the average of 43,700 jobs added per month for the first 6 months of the year and the largest monthly increase in the past year.

July’s health sector job growth was led by growth in ambulatory care settings, which added 35,400 jobs, followed by hospitals, which added 16,100 jobs.

Nursing and residential care facilities added 11,500 jobs in July, with growth occurring in both nursing homes (6,300 jobs) and other nursing and residential care settings (5,200 jobs).

The economy added 187,000 jobs in July, somewhat below the 12-month average of 280,200 jobs. The unemployment rate, at 3.5%, changed little in July.

Health care wage growth in June 2023 was 3.7% year over year, somewhat below the total private sector wage growth of 4.4%.

Wage growth in health care settings is now highest in nursing and residential care, at 4.8% year over year in June 2023. Wage growth in hospitals was 4.3%, while wage growth in ambulatory care settings was 3.0% in June.

In January 2023, the Rockefeller Institute published a three-part blog series on trends to watch in healthcare in 2023. The series covered broad issues related to the healthcare workforce, economy, and health policy, and highlighted internal industry changes and trends in service delivery, quality, and equity.

Here, we provide a recap and mid-year update on those trends.

The Public Health Emergency:

In January, we anticipated the COVID-19 federal public health emergency (PHE) would end at some point during the year and its ending would impact the industry by rolling back flexibilities and programs that were temporarily put in place to combat the pandemic. The end of the PHE, while not a “trend” per se, held significant potential to alter the trajectory of trends in healthcare coverage, access, and care delivery that were occurring during the pandemic.

Mid-year Update: As predicted, the PHE was not renewed and ended on May 11, 2023. The most notable impact of the non-renewal of the PHE was the end of continuous Medicaid public health insurance coverage. The Kaiser Family Foundation’s Medicaid Enrollment Tracker shows that, as of July 5, 2023, 1,652,000 Medicaid enrollees were disenrolled by the District of Columbia and 28 states reporting data. For context, this means that 39% of people with a completed renewal were disenrolled in reporting states, though disenrollment rates varied significantly across those states from 16 percent in Virginia to 75 percent in South Carolina. The eligibility redetermination process that can lead to a potential disenrollment is being conducted differently in each state with some states moving quickly to make redeterminations and others doing the process more deliberately over the course of the year with a clear intent to avoid shedding people from the Medicaid program because of an inability to submit administrative paperwork.

The process for eligibility renewals will continue to play out over the course of the next year since states have until mid-2024 to update all Medicaid enrollees’ eligibility status. Also notable are some changes made under the purview of the PHE that persist despite the emergency’s conclusion. For example, access to COVID-19 vaccinations and certain COVID-19 treatments generally have not been affected. Some telehealth flexibilities that were allowed under the PHE are also staying in effect, at least until the end of 2024.

Healthcare Workforce Shortages:

Prior to the pandemic, larger demographic trends in society were already impacting the supply of the healthcare workforce. The number of people aging and needing healthcare services was growing while the number of people available to provide care was not keeping pace thus creating a long-term healthcare workforce shortage.

Mid-year Update:The workforce shortage continues. As outlined in a May 23rd Becker’s Hospital Review article, several sources point to a continued shortage. They include a report that says the US could see a deficit of 200,000 to 450,000 registered nurses by 2025. Within the next five years, another report also projects a shortage of more than 3.2 million lower-wage healthcare workers, such as medical assistants, home health aides, and nursing assistants. As a result, some healthcare providers are becoming more creative in their efforts to counteract the workforce shortage: creating alumni networks from which to recruit or providing other benefits to their workforce, such as housing or educational assistance. Policymakers can help counteract the negative impacts of the workforce shortage through a variety of strategies. With the shortage expected to continue, it will be important to enact additional policies that bolster the workforce.

Price Inflation:

As we noted, price inflation was significant in 2022 but was not unique to the health sector.Inflation was particularly exacerbated by the re-opening of the economy after the pandemic, the continued war in Ukraine, and supply chain challenges.

Mid-year Update: Prices for many consumer goods and services increased faster than usual, with overall inflation reaching a four-decade high in mid-2022. The Bureau of Labor Statistics (BLS) reported inflation rates have slowed, with overall prices growing by 6 percent in February 2023 compared to the previous year. Interestingly, prices for medical care increased only 2.3 percent. Similarly, BLS reported that the average price of health care in the United States increased by 0.7 percent in the 12 months ending May 2023, following a previous increase of 1.1 percent. The slower price growth in healthcare compared to other sectors of the economy is highly unusual,[i] and while inflation is not easily influenced by state-level policymakers’ actions alone, the trend is still worth monitoring to better understand the impacts on healthcare access and quality. As of early July, the latest predictions from PwC are that healthcare costs will rise 7% in 2024.

Declining Margins at Hospitals:

Previous analysis by the consulting firm Kaufman Hall predicted that more than half of all hospitals would have negative margins at the end of 2022. As we noted, this was due to such factors as higher-than-normal expenses for staff, supplies, and pharmaceuticals and lower revenues.

Mid-year Update: The latest report from Kaufman Hall offers data that shows a reversal in this trend for the first part of 2023. May was the third consecutive month in which hospital margins were positive after operating in the red for most of 2022. The return to normal is largely driven by revenues that are more in line with pre-pandemic levels. With revenues returning to more normal levels, expenses will be particularly important to watch for the remainder of 2023. If hospital expenses continue to outweigh revenues, policymakers may need to evaluate the financial health of providers and the potential impact that may have on access to services for patients.

Private Equity in Healthcare:

We predicted that private equity (PE) would continue to grow in healthcare, pointing to a PwC consulting report that indicated that PE companies still had plenty of “dry powder,” or money, to invest in 2023.

Mid-year Update:There has been a slowdown in private equity deals over the last year. But it is notable that there were still 200 private equity deals in healthcare in the first quarter of 2023, according to PitchBook’s healthcare services report released in May 2023. While lower than the year before, this is still considered active when compared to pre-pandemic PE dealmaking. Because of the waning of the pandemic and stability returning to the healthcare sector, it is more likely that PE deals stabilize in 2023. And some industry predictions indicate that dealmaking will bounce back further in the second half of 2023. As noted in our previous blog, it will be important to monitor the proliferation of PE in healthcare and determine its impact on healthcare markets, care delivery, innovation, and quality.

Consolidations:

Like many other industries, consolidations of all sorts have been happening in healthcare. The consolidations are both vertical—combining two or more stages of production normally operated by separate companies into one company, such as when hospitals or insurers employ physicians and/or acquire physician practices or other entities like pharmacies—and horizontal—combining organizations that provide the same or similar services, such as hospitals acquiring hospitals.

Mid-year Update: Consolidations of all sorts of healthcare entities continued in 2023 with some of the biggest potential consolidations yet. Those include the proposed merger of two major bi-coastal health system providers: Geisinger, based in Pennsylvania, and Kaiser, based in California. Although the deal must still go through regulatory approval, if completed, the two systems will create a nonprofit that will look to add five or six more systems nationally over the next five years. Other notable consolidations include the finalization of tech-giant Amazon’s purchase of One Medical, a primary care network. And Optum, one of the largest conglomerates that is a subsidiary of United Health Group, increased its net revenue growth by 25% to $54.1 billion in the first quarter of 2023, primarily due to more patients visiting OptumHealth clinics and growth in OptumRx pharmacy scripts processed. Optum’s growth is likely to continue in 2023 as they expect to add another 10,000 physicians. Case in point, in February of this year, Optum paid an undisclosed sum for Crystal Run Healthcare, a network of nearly 400 providers in New York. A goal of consolidation has been better coordination of patient care for improved outcomes and value. Results have been mixed and it is therefore an important trend for policymakers and researchers to monitor and to ensure the impacts are positive.

Alternate Payment Models:

Alternate payment models (APMs) in healthcare have been expanding especially since enactment of the Patient Protection and Affordable Care Act in 2010. They are primarily being developed by the Center for Medicare and Medicaid Innovation (CMMI) which has driven payment policy (including APMs) in the two big government healthcare programs: Medicaid and Medicare. There have been several iterations of APMs—over 50 models—but the one common theme is that all of them generally seek to reward better care.

Mid-year Update: Since the start of 2023, the most notable expansion of the trend toward more alternate payment models was CMMI’s introduction of a new primary care-focused APM called Making Care Primary. In addition to this model, it is expected that the Centers for Medicaid and Medicare Services (CMS), which oversees the operation of these two large public health insurance programs, will introduce more new payment models in 2023, including one that allows states to manage the total cost of care in a given region. This may take various forms, including something akin to Maryland’s global budget, which is used statewide. Since the total cost of care model has yet to be officially revealed, this trend and the emergence of any new developments is worth watching in the second half of 2023. Policymakers can learn from these various payment models and use them to inform the plans implemented in their own state or region in order to improve healthcare.

Attention to Health Equity:

A notable aspect of the pandemic was the disparate impact it had on people of color and other marginalized groups. In response, policymakers and providers began paying more attention to the underlying cause of these disparities. In 2021, President Joe Biden signed an executive order to focus federal resources and attention on reducing health disparities.

Mid-year Update: Increased attention to health equity in healthcare has continued. Ernst and Young, an international consulting group, released its first-ever report on the state of health equity in the United States, which involved a survey of over 500 providers to begin tracking their methods for, and progress in, addressing health disparities. More recently, in June 2023, The Joint Commission on the Accreditation of Healthcare Organizations (JCAHO) announced that it will be adding a certification program for healthcare organizations specifically targeted towards improving health equity. While attention to equity has grown, what will be interesting to watch in the second half of 2023 is the degree to which such efforts are having an impact on actually reducing disparities. Understanding the impacts of various interventions can help policymakers expand efforts that are effective.

Digital TeleHealth Delivery Expansion:

The use of digital health expanded dramatically from 2020 to 2022 as social distancing practices were adopted and telehealth options became more widely available. As noted in our blog series, digital health “includes mobile health (mHealth), health information technology (IT), wearable devices, telehealth and telemedicine, and personalized medicine.” It also includes, “mobile medical apps and software that support the clinical decisions doctors make every day to do artificial intelligence and machine learning.”

Mid-year Update: At the end of 2022 and the start of 2023, the ability to infuse capital to drive the expansion of digital health seemed tenuous, in part due to the collapse of Silicon Valley Bank (SVB). As noted by the publication Pitchbook and CB Insights, venture capital funding in the digital health space totaled $7.5 billion in 2022, a 57 percent year-over-year drop. Although the fast pace of investment in digital health may have slowed since its explosion during the pandemic, the expansion of digital health continues. Our January blog suggested that areas such as behavioral health, care at home, and maternal health were areas to watch. In 2023, digital access is expanding in other areas, such as in-home urgent primary care to allow for the treatment of complex injuries and illnesses with the goal of reducing emergency department visits. And other important digital health deals are still occurring: health tech startup Florence picked up Zipnosis from Bright Health to expand its virtual care capabilities. And with the launch of consumer-facing tech products, such as Chat GPT and Apple Vision Pro in the first half of 2023, additional opportunities for applying such technologies in healthcare may fuel further expansion of digital health. Policies that are developed in the future may want to support the growth of such innovation, while also being mindful to monitor the potential impacts on care.

Expansion of Non-Traditional Providers:

In January, we noted an emergence of companies in healthcare whose genesis was something other than healthcare. The blog pointed to examples of how companies such as Walgreens, CVS, and Amazon were expanding their offerings in healthcare.

Mid-year Update:Non-traditional entities continue to expand in the healthcare space. Notable examples include the recent acquisitions and expansions made by CVS. One of these expansions is being done through its affiliation with the insurance company, Aetna. Through Aetna, CVS has entered the insurance exchange market in four more states in 2023, in addition to the 12 states in which it already operates. CVS also closed a deal in the first half of 2023 to acquire Oak Street Health for over $10 billion. And, in March 2023, CVS announced it had officially acquired Signify Health, a digital telehealth company that enables more care to occur in-home. As noted earlier, Amazon officially completed its deal to acquire OneMedical and United Health Group is working on expanding its use of value-based care through a partnership with Walmart. Monitoring the impact of these emerging companies in healthcare will be important for policymakers that have historically only focused on more traditional providers, such as hospitals. These non-traditional entrants, in many cases, are large organizations with substantial resources and their impact may be just as significant if not greater than traditional providers.

Conclusion

These trends merit close attention in the second half of 2023. As healthcare takes on new shapes, the implications for those in the sector and all who depend on it will be huge. In addition, there are important implications for state and federal policymakers who will need to consider how these trends impact access, affordability, and quality of health care, so they can determine whether and how government might help to accelerate beneficial innovations, invest in promising trends, prevent or reverse harmful trends, and monitor the impacts on consumers.

The latest CPI was a crowd-pleaser: Inflation has plunged from its peak, helping provide relief for consumers.

Beyond the headline, an underlying measure closely watched by economists and the Fed finally began to cool.

Why it matters:

The worst of the inflation crisis looks to be firmly behind us. Price gains appear to be on a path to returning to normal, but there is huge uncertainty around how long that will take, with plenty of hurdles still ahead.

What they’re saying:

“After a punishing stretch of high inflation that eroded consumer’s purchasing power, the fever is breaking,” Bill Adams, chief economist at Comerica Bank, wrote in a note.

While the Fed appears to be on track to tighten by a quarter percentage point two weeks from today, the promising news lowers the odds of further hikes this year.

Details:

Headline CPI rose 3% (or 2.97%, unrounded) in the 12 months through June, the smallest increase since March 2021. That reflects milder price gains for a slew of goods, including food — and outright deflation for other items consumers buy, like airline fares, which fell 8% in June.

The intrigue:

At the same time last year, headline prices skyrocketed by 9%. Now we’re lapping that period, which makes the comparison much more favorable.

Then, commodity prices soared on disruptions from Russia’s invasion of Ukraine. Those prices are sharply lower now, helping the headline figure cool rapidly. Gasoline, for instance, is down nearly 27%.

Those favorable effects will fade in the year-on-year numbers, so don’t be surprised if the headline CPI figure rebounds some in the coming months.

The most encouraging aspect was the core figure, which strips out volatile food and energy costs and is closely followed by policymakers. That rose by just 0.2% in June, the slowest monthly pace since February 2021.

In the past three months, core inflation has risen at a 4.1% annualized pace — down almost a full percentage point from May.

Under the hood, there was notable disinflation across a key sector of the economy monitored by the Fed: core services, excluding shelter. Prices in that category were flat last month, compared to a 0.2% rise in May.

That cooling is happening alongside a still-healthy labor market and solid wage gains (more on this below), which officials worried could stoke inflation in this category.

The Biden administration is eager to tout the progress. “The economy is defying predictions that inflation would not fall absent significant job destruction,” top White House economic adviser Lael Brainard is expected to say this afternoon at the Economic Club of New York, according to prepared remarks.

“Annual inflation has now declined every month for 12 months in a row,” she will say, “and inflation in the United States is now the lowest among G-7 nations … even as our economic recovery from the pandemic has been the strongest.”

The bottom line:

We have been head-faked before by what appeared to be remarkable progress on inflation, notably in the summer of 2001.

With expected cooling in other areas (including shelter, which makes up a big chunk of the index), there is reason to be hopeful this progress could be here to stay.

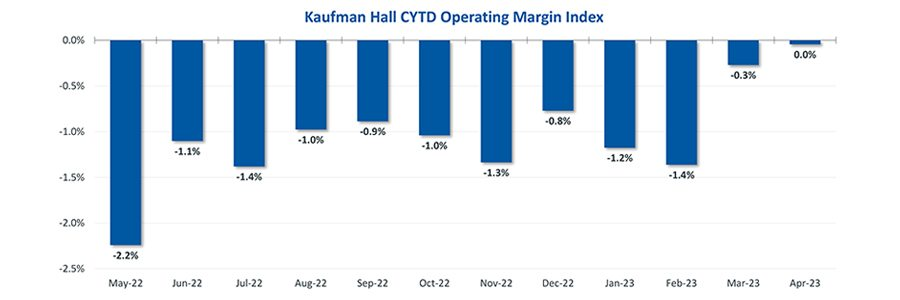

Hospital finances showed signs of stabilizing in May amid slightly improving operating margins, declining expenses and notable increases in outpatient visits.

The median Kaufman Hall Year-To-Date Operating Margin Index reflecting actual margins was 0.3% in May.

The National Hospital Flash Report uses both actual and budget data over the last three years, sampled from more than 900 hospitals on a recurring monthly basis from Syntellis Performance Solutions.

The sample of hospitals for this report is representative of all hospitals in the United States both geographically and by bed size. Additionally, hospitals of all types are represented, from large academic to small critical access. Advanced statistical techniques are used to standardize data, identify and handle outliers, and ensure statistical soundness prior to inclusion in the report.

While this report presents data in the aggregate, Syntellis Performance Solutions also has real-time data down to individual department, jobcode, paytype, and account levels, which can be customized into peer groups for unparalleled comparisons to drive operational decisions and performance improvement initiatives.

Key Takeaways

Hospitals broke even in April. The median operating margin for hospitals was 0% in April, leaving most hospitals with little to no financial wiggle room.

Volumes dropped while lengths of stay increased. Hospital volumes dropped across the board—including inpatient and outpatient. Emergency department volumes were the least affected.

Effects of Medicaid disenrollment could be materializing. Hospitals experienced increases in bad debt and charity care in April. Combined with anemic patient volumes, experts note this data could illustrate the effects of the start of widespread disenrollment from Medicaid following the end of the COVID-19 public health emergency.

Inflation continued to throttle hospital finances. Labor costs jumped in April and the costs of goods and services continued to be well above pre-pandemic levels. Though expenses generally fell in April, revenues declined at a faster rate.

National Non-Operating Results

Key Observations

At their May meeting, the Federal Open Market Committee (FOMC) raised the benchmark borrowing rate another 25 basis points, setting the range to 5.00-5.25% and marking the 10th consecutive hike in the cycle as well as a 16-year high

Fed officials acknowledged discussion of a potential pause in tightening while leaving wiggle room, saying “rates are going to come down” over a long period of time while also warning inflation “continues to run high” and the Fed will be taking a “data-dependent approach”

The consumer price index (CPI) rose 0.4% in April, a 4.9% increase year-over-year, an annual pace of inflation below 5% for the first time in two years

The labor market continued to show resilience in April as U.S. nonfarm payrolls grew by 253,000 and unemployment fell back to a 53-year low of 3.4%

Strong inflation, a robust labor market, continued banking sector woes, and a debt ceiling standoff further complicates credit conditions and may challenge the Fed to stabilize financial markets

Equities in April, as measured by the S&P 500, were up 1.5% in April and 8.6% YTD despite downbeat economic data, reoccurring banking sector fears, and mixed earnings

Two important reports released last Wednesday point to a disconnect in how policymakers are managing the U.S. economy and how the health economy fits.

Report One: The Federal Reserve Open Market Meeting

At its meeting last week, the Governors of the Federal Open Market Committee (FOMC) voted unanimously to keep the target range for the federal funds rate at 5% to 5.25%–the first time since last March that the Fed has concluded a policy meeting without raising interest rates.

In its statement by Chairman Powell, the central bank left open the possibility of additional rate hikes this year which means interest rates could hit 5.6% before trending slightly lower in 2024.

In conjunction with the (FOMC) meeting, meeting participants submitted projections of the most likely outcomes for each year from 2023 to 2025 and over the longer run:

Median

2023

2024

2025

Longer Run

Longer Run Range

% Change in GDP

1.1

1.1

1.8

1.8

1.6-2.5

Unemployment rate &

4.1

4.5

4.5

4.0

3.6-4.4

PCE Inflation rate

3.2

2.5

2.1

2.0

2.0

Core PCE Inflation

3.9

2.6

2.2

*

*

*Longer-run projections for core PCE inflation are not collected.

Notes re: the Fed’s projections based on these indicators:

The GDP (a measure of economic growth) is expected to increase 1% more this year than anticipated in its March 2023 analysis while estimates for 2024 were lowered just slightly by 0.1%. Economic growth will continue but at a slower pace.

The unemployment rate is expected to increase to 4.1% by the end of 2023, a smaller rise in joblessness than the previous estimate of 4.5%. (As of May, the unemployment rate was 3.7%). Unemployment is returning to normalcy impacting the labor supply and wages.

inflation: as measured by the Personal Consumption Expenditures index, will be 3.2% at the end of 2023 vs. 3.3% they previously projected. By the end of 2024, it expects inflation will be 2.5% reaching 2.1% at the end of 2025. Its 2.0% target is within reach on or after 2025 barring unforeseen circumstances.

Core inflation projections, which excludes energy and food prices, increased: the Fed now anticipates 3.9% by the end of 2023–0.3% above the March estimate. Price concerns will continue among consumers.

Based on these projections, two conclusions about nation’s monetary policy may be deduced the Fed’s report and discussion:

The Fed is cautiously optimistic about the U.S. economy in for the near term (through 2025) while acknowledging uncertainty exists.

Interest rates will continue to increase but at a slower rate than 2022 making borrowing and operating costs higher and creditworthiness might also be under more pressure.

Report Two: CMS

On the same day as the Fed meeting, the actuaries at the Centers for Medicare and Medicaid Services (CMS) released their projections for overall U.S. national healthcare spending for the next several years:

“CMS projects that over 2022-2031, average annual growth in NHE (5.4%) will outpace average annual growth in gross domestic product (GDP) (4.6%), resulting in an increase in the health spending share of GDP from 18.3% in 2021 to 19.6% in 2031. The insured percentage of the population is projected to have reached a historic high of 92.3% in 2022 (due to high Medicaid enrollment and gains in Marketplace coverage). It is expected to remain at that rate through 2023. Given the expiration of the Medicaid continuous enrollment condition on March 31, 2023 and the resumption of Medicaid redeterminations, Medicaid enrollment is projected to fall over 2023-2025, most notably in 2024, with an expected net loss in enrollment of 8 million beneficiaries. If current law provisions in the Affordable Care Act are allowed to expire at the end of 2025, the insured share of the population is projected to be 91.2%. In 2031, the insured share of the population is projected to be 90.5%, similar to pre-pandemic levels.”

The report includes CMS’ assumptions for 4 major payer categories:

Medicare Part D: Several provisions from the Inflation Reduction Act (IRA) are expected to result in out-of-pocket savings for individuals enrolled in Medicare Part D. These provisions have notable effects on the growth rates for total out-of-pocket spending for prescription drugs, which are projected to decline by 5.9% in 2024, 4.2% in 2025, and 0.2% in 2026.

Medicare: Average annual expenditure growth of 7.5% is projected for Medicare over 2022-2031. In 2022, the combination of fee-for-service beneficiaries utilizing emergent hospital care at lower rates and the reinstatement of payment rate cuts associated with the Medicare Sequester Relief Act of 2022 resulted in slower Medicare spending growth of 4.8% (down from 8.4% in 2021).

Medicaid: On average, over 2022-2031, Medicaid expenditures are projected to grow by 5.0%. With the end of the continuous enrollment condition in 2023, Medicaid enrollment is projected to decline over 2023-2025, with most of the net loss in enrollment (8 million) occurring in 2024 as states resume annual Medicaid redeterminations. Medicaid enrollment is expected to increase and average less than 1% through 2031, with average expenditure growth of 5.6% over 2025-2031.

Private Health Insurance: Over 2022-2031, private health insurance spending growth is projected to average 5.4%. Despite faster growth in private health insurance enrollment in 2022 (led by increases in Marketplace enrollment related to the American Rescue Plan Act’s subsidies), private health insurance expenditures are expected to have risen 3.0% (compared to 5.8% in 2021) due to lower utilization growth, especially for hospital services.

And for the 3 major recipient/payee categories:

Hospitals: Over 2022-2031, hospital spending growth is expected to average 5.8% annually. In 2023, faster growth in hospital utilization rates and accelerating growth in hospital prices (related to economy wide inflation and rising labor costs) are expected to lead to faster hospital spending growth of 9.3%. For 2025-2031, hospital spending trends are expected to normalize (with projected average annual growth of 6.1%) as there is a transition away from pandemic public health emergency funding impacts on spending.

Physicians and Clinical Services: Growth in physician and clinical services spending is projected to average 5.3% over 2022-2031. An expected deceleration in growth in 2022, to 2.4% from 5.6% in 2021, reflects slowing growth in the use of services following the pandemic-driven rebound in use in 2021. For 2025-2031, average spending growth for physician and clinical services is projected to be 5.7%, with an expectation that average Medicare spending growth (8.1%) for these services will exceed that of average Private Health Insurance growth (4.6%) partly as a result of comparatively faster growth in Medicare enrollment.

Prescription Drugs: Total expenditures for retail prescription drugs are projected to grow at an average annual rate of 4.6% over 2022-2031. For 2025-2031, total spending growth on prescription drugs is projected to average 4.8%, reflecting the net effects of key IRA provisions: Part D benefit enhancements (putting upward pressure on Medicare spending growth) and price negotiations/inflation rebates (putting downward pressure on Medicare and out-of-pocket spending growth).

Thus, CMS Actuaries believe spending for healthcare will be considerably higher than the growth of the overall economy (GDP) and inflation and become 19.6% of the total US economy in 2031. And it also projects that the economy will absorb annual spending increases for hospitals (5.8%) physician and clinical services (5.3%) and prescription drugs (4.6%).

My take:

Side-by-side, these reports present a curious projection for the U.S. economy through 2031: the overall economy will return to a slightly lower-level pre-pandemic normalcy and the healthcare industry will play a bigger role despite pushback from budget hawks preferring lower government spending and employers and consumers frustrated by high health prices today.

They also point to two obvious near-term problems:

1-The Federal Reserve pays inadequate attention to the healthcare economy. In Chairman Powell’s press conference following release of the FOMC report, there was no comment relating healthcare demand or spending to the broader economy nor a question from any of the 20 press corps relating healthcare to the overall economy. In his opening statement (below), Chairman Powell reiterated the Fed’s focus on prices and called out food, housing and transportation specifically but no mention of healthcare prices and costs which are equivalent or more stressful to household financial security:

“Good afternoon. My colleagues and I remain squarely focused on our dual mandate to promote maximum employment and stable prices for the American people…My colleagues and I are acutely aware that high inflation imposes hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are highly attentive to the risks that high inflation poses to both sides of our mandate, and we are strongly committed to returning inflation to our 2% objective.”

2-Congress is reticent to make substantive changes in Medicare and other healthcare programs despite its significance in the U.S. economy. It’s politically risky. In the June 2 Congressional standoff to lift the $31.4 debt ceiling, cuts to Medicare and Social Security were specifically EXCLUDED. Medicare is 12% of mandated spending in the 2022 federal budget and is expected to grow from a rate of 4.8% in 2022 to 8% in 2023—good news for investors in Medicare Advantage but concerning to consumers and employers facing higher prices as a result.

Even simplifying the Medicare program to replace its complicated Parts A, B, C, and D programs or addressing over-payments to Medicare Advantage plans (in 2022, $25 billion per MedPAC and $75 billion per USC) is politically tricky. It’s safer for elected officials to support price transparency (hospitals, drugs & insurers) and espouse replacing fee for service payments with “value” than step back and address the bigger issue: how should the health system be structured and financed to achieve lower costs and better health…not just for seniors or other groups but everyone.

These two realities contribute to the disconnect between the Fed and CMS. Looking back 20 years across 4 Presidencies, two economic downturns and the pandemic, it’s also clear the health economy’s emergence did not occur overnight as the Fed navigated its monetary policy. Consider:

National health expenditures were $1.366 trillion (13.3% of GDP) in 2000 and $4.255 billion in 2021 (18.3% of the GDP). This represents 210% increase in nominal spending and a 37.5% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 334 million while per capita healthcare spending increased 166% from $4,845 to $12,914. This disproportionate disconnect between population and health spending growth is attributed by economists to escalating unit costs increases for the pills, facilities, technologies and specialty-provider services we use—their underlying cost escalation notably higher than other industries.

There were notable changes in where dollars were spent: hospitals were unchanged (from $415 billion/30.4% of total spending to $1.323 trillion/31.4% of total spending), physician services shrank (from $288.2 billion/21.1% of total spending to 664.6 billion/15.6% pf total spending), prescription drugs were unchanged (from $122.3 billion/8.95% to $378 billion/8.88% of total spending) and public health increased slightly (from $43 billion/$3.2% of total spending to $187.6 billion/4.4% of total spending).

And striking differences in sources of funding: out of pocket spending shrank from $193.6/14.2% of payments to $433 billion/10.2% % of payments; private insurance shrank from $441 billion/32.3% of payments to $1.21 trillion/28.4% of total payments; Medicare grew from $224.8 billion/16.5% of payments to $900.8 billion/21.2% of payments; Medicaid + CHIP grew from $203.4 billion/14.9% to $756.2 billion/17.8% of payments; and Veterans Health grew from $19.1 billion/1.4% of payments to $106.0 billion/2.5% of payments.

Thus, if these trends continue…

Aggregate payments to providers from government programs will play a bigger role and payments from privately insured individuals and companies will play a lesser role.

Hospital price increases will exceed price increases for physician services and prescription drugs.

Spending for healthcare will (continue to) exceed overall economic growth requiring additional funding from taxpayers, employers and consumers AND/OR increased dependence on private investments that require shareholder return AND/OR a massive restructure of the entire system to address its structure and financing.

What’s clear from these reports is the enormity of the health economy today and tomorrow, the lack of adequate attention and Congressional Action to address its sustainability and the range of unintended, negative consequences on households and every other industry if left unattended. It’s illustrative of the disconnect between the Fed and CMS: one assumes it controls the money supply while delegating to the other spending and policies independent of broader societal issues and concerns.

The health economy needs fresh attention from inside and outside the industry. Its impact includes not only the wellbeing of its workforce and services provided its users. It includes its direct impact on household financial security, community health and the economic potential of other industries who get less because healthcare gets more.

Securing the long-term sustainability of the U.S. economy and its role in world affairs cannot be appropriately addressed unless its health economy is more directly integrated and scrutinized. That might be uncomfortable for insiders but necessary for the greater good. Recognition of the disconnect between the Fed and CMS is a start!

Physicians at the American Medical Association Annual Meeting called for an overhaul of the Medicare payment system, arguing that it is outdated and threatens the survival of independent practices and patients’ access to care.

“This cannot wait; we are past the breaking point. Congress must urgently address physician concerns about Medicare to account for inflation and the post-pandemic economic reality facing practices nationwide,” AMA President Jack Resneck Jr., MD, said in a June 12 news release. “Our patients are counting on us to deliver the message that access to health care is jeopardized by Medicare’s payment system. Being mad isn’t enough. We will develop a campaign — targeted and grass roots — that will drive home our message.”

Inflation, the pandemic, declining reimbursements and rising cost are making it more challenging for independent physicians to maintain their autonomy and are jeopardizing access to care, according to the AMA, which argues that CMS physician payments have declined 26 percent from 2001 to 2023 after accounting for inflation.

In January, the Medicare Payment Advisory Commission called for a physician payment update tied to the Medicare Economic Index for the first time, and, in April, a group of House members introduced a bill that would provide annual inflation updates to the Medicare fee schedule based on the index.

“Duct-taping the widening cracks of a dilapidated payment system has put us in this precarious situation,” Dr. Resneck said. “Physicians are united in our determination to build a solid foundation rather than further jury-rigging the system.”