This week’s graphic looks at the plethora of state-level mergers and acquisitions (M&A) oversight laws that are now in place, part of a recent trend that adds further scrutiny to healthcare consolidation.

Thirty-five states currently have laws that require not-for-profit healthcare entities that meet certain requirements, usually based on revenue size, to report M&A activity to state regulators. Fourteen of these states extend these requirements to for-profit healthcare entities as well.

These state laws vary in scope but generally target healthcare deals that fall below the federal reporting threshold for transaction size, updated to $119.5M in 2024.

Two states with particularly strong healthcare M&A oversight laws are Oregon and Minnesota. The Oregon Health Authority must pre-approve any healthcare transaction of at least $35M in size.

Passed in 2023, Minnesota’s healthcare antitrust law sets the deal size reporting requirements at $10M,

but the state commissioner of health and the attorney general do not have to pre-approve all healthcare mergers. Minnesota also requires merging parties to disclose extensive details on the transaction agreement, market impact, service cuts, and more to state regulators, who have broad authority to block mergers on public interest grounds.

Although some believe that these state laws will help preserve healthcare competition and access, they will increase the complexity, cost, and timeline for healthcare entities seeking to merge and could make survival for smaller providers even more difficult.

Late last week, Oregon Health & Science University (OHSU) and Legacy Health, both not-for-profit health systems based in Portland, OR, shared that they had signed a definitive agreement to merge after first announcing their intent to combine last August.

The combined system would be the largest in the Portland region, with 12 hospitals and a total annual revenue of about $6.6B. As part of the deal, OHSU has promised to invest about $1B over ten years to upgrade Legacy’s facilities.

The systems are expected to apply this summer for review by Oregon’s Health Care Market Oversight Program, which was established in 2022 and has the authority to deny or attach conditions to healthcare mergers in the state.

The Gist: If finalized, this merger would connect OHSU’s academic medical center to Legacy’s network of community hospitals and clinics, as well as secure Legacy a needed capital infusion.

Next steps include review by both federal regulatory agencies and Oregon, which is among a growing number of states to implement M&A oversight laws.

Abuses by payers are myriad, but these five areas could bear the most fruit for federal antitrust investigators.

Earlier this month, the U.S. Department of Justice announced it has haunched an investigation into “issues regarding payer-provider consolidation” along with other problems associated with mergers and acquisitions in health care. This is significant. For years Washington has trained its oversight authority on pharmaceutical manufacturers, private equity investments in health care and, more recently, pharmacy benefits managers controlled by big insurers. This has held bad actors like Martin Skhreli and Steward Healthcare accountable. But, it has also let insurers grow ever larger, under the radar.

No longer.

This task force will specifically evaluate the following, as an example: “A health insurance company buys several medical practices that compete with each other. It also prohibits its medical practices from contracting with rival health insurance companies.” The government will also dig into “anticompetitive uses of health care data,” “preventing transparency,” “price fixing,” and other areas that could drag nefarious activities of insurers into the spotlight.

I applaud the Department of Justice’s continued focus on these issues, building on the Department’s action announced in February to begin an antitrust investigation into UnitedHealth Group. (If you haven’t read the piece we published in February on UnitedHealth’s self-dealing that helped lead DOJ to open that antitrust inquiry, you can do so here.) The following are a few areas of low-hanging fruit that I hope the task force will focus on as they consider the impact insurers’ ongoing vertical integration has had on the overall health care system.

1. Insurers purchasing physician practices

Once a low-profile issue, Congress and the Biden administration alike have increasingly turned their focus to insurance companies – often referred to as payers – that now own and operate physician practices and clinics – those being paid. Even for someone without a law degree, it is easy to see the conflict this creates, particularly at scale.

There is the oft-cited statistic that UnitedHealth has said that through its Optum division, the company employs or otherwise controls about 10 percent of doctors in the U.S. – around 130,000 physicians and other practitioners in 16 states. This prompted me to take a closer look at publicly available information on the number of doctors employed by other insurers to get a better handle on how much control of physician practices payers now have.

It is difficult to put a percentage on physicians employed by each insurer, but it is clear that the others are following UnitedHealth’s lead. CVS/Aetna purchased Signify Health in 2023, adding 10,000 clinicians to its portfolio. The company says it supports “more than 40,000 physicians, pharmacists, nurses and nurse practitioners.”

Clearly taking a page out of UnitedHealth’s playbook, Elevance (formerly Anthem), which owns Blue Cross Blue Shield plans in 14 states announced last month a “strategic partnership” with 900 providers across several states. Elevance did not disclose the terms of the deal except to say it, “will primarily be through a combination of cash and our equity interest in certain care delivery and enablement assets of Carelon Health.”

As insurers have acquired physician practices, they also have created a rinse-and-repeat strategy associated with kicking physicians they don’t own out of network, and in some cases targeting those same practices for acquisition. Aetna and Humana recently told investors they will be reviewing their networks of physicians, signaling they’ll soon be further narrowing their networks. A good question for this task force: when insurers review those contracts with doctors, do they ever kick the doctors they employ out of network? (Doubtful.) This could specifically draw attention from the task force’s focus on “health care contract language and other practices that restrict competition,” such as contract provisions that require or encourage patients to seek care from doctors directly employed or closely controlled by patients’ insurers.

Additionally, UnitedHealth CEO Andrew Witty recently told analysts, “As I think you see some of the funding changes play out across the — across the next few years, I suspect that may also create new opportunities for us as different companies assess their positions.” My translation:UnitedHealth’s burdensome business practices and the way it shortchanges doctors (those “funding changes” he referenced) contribute to the financial distress that is forcing many health care providers to “assess their positions.”

As the task force continues to consider the impact of private equity in health care monopolies, transactions like this one should receive equal consideration for their lack of transparency and overall impact on market consolidation.

2. Co-mingling of middlemen

I have watched with interest for over the past year as both Democrats and Republicans in Washington increasingly trained their fire on pharmacy benefit managers. The natural next area of focus in that space, which this new task force could advance, should be around how the

three PBMs that control 80 percent of market share are all combined with health insurance companies – namely CVS/Aetna (Caremark), UnitedHealth (Optum Rx), and Cigna (Express Scripts).

An important, and politically popular, area where this consolidation has played out is in the squeeze placed on small, independent pharmacists across the country. More than 300 community pharmacies have closed in the past year alone, out of an inability to operate or push back on unfair margins pushed by these PBM-insurer monopolies. As we have written here, the fees these PBMs charge have increased more than 100,000 percent over the past decade, and are quietly contributing significantly to the profits of the largest health insurers.

We still have little insight into how these business lines interact with each other, and the ultimate impact that has on patients. Given the enormous influence just three insurance companies have over what prescriptions Americans can receive, and how much should be paid for each prescription, the task force would do well to focus on what insurers and PBMs are doing behind the scenes to maximize profits and limit patient access to prescription drugs. It’s already gaining traction on Capitol Hill, with one Congressman recently saying, “I’ll continue to bust this up … this vertical integration in health care.”

3. Prior authorization requests

CVS/Aetna shares were hammered after the company reported a significant increase in payment of Medicare Advantage claims during the first three month is of this year. Expect all insurers to notice. And as they have seen their forecasts fall short of Wall Street’s expectations – particularly because of increasing scrutiny in Washington of Medicare Advantage – these corporations will look to increase their already aggressive use of prior authorization to limit claims payments.

It is not as though insurers make seeking the care you need easy. Far from it. Prior authorization has become “medical injustice disguised as paperwork,” as the New York Times said in a recent, excellent video detailing the widespread nature of this profiteering practice.

While not a stated direct focus of this task force, the increased impact of prior authorization in care delivery is a direct outgrowth of a few large health insurers effectively controlling the marketplace. As insurers directly employ more doctors and enroll more Americans in their plans, they can use prior authorization to increasingly determine whether a patient can get care, period.

Scrutiny in this space could add momentum to increasing activity in state legislatures and Washington to rein in excessive prior authorization. As of early March, nine states and the District of Columbia had passed bills to limit how far insurers could go with prior authorization. And earlier this year, the Centers for Medicare and Medicaid released a final rule that is expected to save physicians $15 billion over the next decade by putting limits on insurer prior authorization tactics.

4. Rising out-of-pocket costs

Regular readers of this newsletter know one of my crusades is to ensure folks who pay good money for health insurance – out of their paychecks or through their tax dollars – can use it when they need it. It was a big win earlier this year for the Lower Out of Pockets Now coalition (which I lead) when President Biden called for a cap on prescription drug out-of-pocket costs of $2,000 annually for everybody, not just Medicare beneficiaries.

If there was true competition and real consumer choice in health insurance, payers wouldn’t be able to get away with increasingly shifting patients into high-deductible plans. But the fact that a few big players control the health insurance market has allowed the oligopoly of payers to do just that, with ever-rising deductibles alongside ever-rising premiums.

The task force’s focus on price fixing, collusion, and transparency in health care costs will, I hope, include some focus on how insurers use their size and clout to drive up out-of-pocket costs and premiums simultaneously – with little recourse to employers or their employees.

5. Implementing crystal clear laws and rules in health care

You know you’re a monopoly or close to it when you can pretty much do whatever you want and get away with it. Look no further than America’s health insurance companies and implementation of the No Surprises Act.

As I wrote earlier this year, Congress and CMS have been clear about how out-of-network hospital bills should be negotiated between insurers and physicians. Yet in case after case, including many that have become the basis of lawsuits, insurers are clearly flouting the Act passed by Congress and the rules promulgated by CMS. Payers are doing this, doctors have said, simply because of their size and ability to weather criticism from physicians, regulators, and the courts – while doctors struggle to pay their bills with significant payments still owed pending out-of-network negotiations with insurers.

One would hope, at a minimum, this task force, focused on rooting out the ills of monopolies, would document how insurers are well aware of how they are supposed to implement legislation like the No Surprises Act, but flout it anyway.

Philadelphia-based Jefferson and Allentown, Pa.-based Lehigh Valley Health Network have signed a definitive agreement to merge into a 30-hospital system with more than 700 care sites.

The two shared plans to unite in December after signing a non-binding letter of intent.

Under the agreement, Jefferson and LVHN will integrate identity, clinical care and operations. The integrated system will comprise more than 65,000 employees and offer new educational opportunities to existing physicians and allow for recruitment opportunities, according to a joint May 15 news release.

The merger will also expand health plan access and improve financial stability that will allow for more investments and new technologies and improved patient outcomes.

Jefferson CEO Joseph Cacchione, MD, will maintain his existing role upon the transaction closure. LVHN president and CEO Brian Nester, DO, will serve as executive vice president and COO of Jefferson and president of the legacy LVHN. He will report to Dr. Cacchione, according to the release.

Baligh Yehia, MD, will serve as Jefferson’s executive vice president and chief transformation officer. Dr. Yehia will also serve as president of the legacy Jefferson health and report to Dr. Cacchione.

An integrated leadership team and board of trustees will comprise leaders from both health systems.

Jefferson and LVHN will operate as independent parties until the merger, the release said.

M&A Volume Up in Q1 2024 vs. Q1 2023: $10 billion Target Revenues

The number of hospital and health system M&A deals announced in the first quarter of 2024 was significantly higher than in the same period in 2023: 18 announced transactions with $10 billion in total revenues for the targets vs. 12 deals in Q1 2023 with a total of $3.4 billion in revenues for the targets. The 81 deals announced in the last 12 months is the highest it has been over the last few years, building upon the recent momentum of hospital and health system mergers, acquisitions, and divestitures across the country.

Other observations by the Cain Brothers M&A team:

Significant number of for-profit conversions to not-for-profit (e.g., divestitures by Tenet and HCA)

Significant number of divestitures by national systems to regional health systems

Accelerated closing timeline for 3 deals in CA: closed in 30-60 days — prior to new hospital merger review process going into effect April 1, 2024 in CA

Q1 2024 total volume of 18 transactions with $10 billion in revenues for targets vs. $3.4 billion for Q1 2023 This quarter saw transformative deals that may reshape how healthcare is delivered, reflecting creative partnerships that continue to form in a changing healthcare environment. Academic medical centers continue to make investments in assets of high strategic value to expand their clinical, teaching, and research capabilities. Large regional systems were quite active, with large cross regional mergers and smaller strategic acquisitions. With the Consumer Price Index (CPI) holding steady with the previous quarter, alleviation of supply cost pressures will benefit health system financials and allow them to deploy more capital.

In early January, General Catalyst’s healthcare investment subsidiary, Health Assurance Transformation Corporation (“HATCo”), announced its intent to acquire Summa Health, one of the largest integrated health delivery systems in Ohio. This announcement made waves in the healthcare industry, not just because of the size of the acquisition, but because it is the first major health system investment for newly formed HATCo. General Catalyst, a venture capital firm formed in 2000, is known for its investments in global companies including Airbnb, Warby Parker, Snap, and Kayak. General Catalyst launched HATCo in October 2023 as a vehicle to enable health systems to enhance technological health capabilities, improve financial results, and assist in meeting the shift to value based care, creating a sustainable and quality-driven healthcare model for providers and patients.

Under the terms of the deal, Summa Health will become a subsidiary of HATCo and transition from a not-for-profit to a for-profit corporation. A community foundation will be formed to continue to invest in the social determinants of health to enhance community outcomes in the Akron-Canton region. With its first acquisition, HATCo aims to become a chassis for future acquisitions and growth for General Catalyst. The deal is expected to close by the end of 2024.

Academic medical centers were active acquirers in the first quarter of 2024. On the West Coast, two University of California systems announced acquisitions from for-profit operators. In January, UCLA Health announced it is the process to acquire West Hills Hospital and Medical Center from HCA. The 260-bed hospital is located in the San Fernando Valley, north of Los Angeles, and will be UCLA’s first acute care hospital in the area. In February, UC Irvine Health signed a definitive agreement to acquire Tenet’s Pacific Coast Network, which include four hospitals in Los Angeles and Orange counties (see below for transaction multiples). The acquisition greatly expands UCI Health’s presence and inpatient bed capacity to complement their flagship UCI Medical Center in Orange. These deals come off the heels of two other University of California deals announced in 2023; UC San Diego Health’s acquisition of Alvarado Hospital from Prime Healthcare, and UCSF’s announcement to acquire two San Francisco hospitals from Dignity Health, further demonstrating the UC system’s mandate to grow and provide greater access to care in California.

Further east, the University of Minnesota announced in February its intent to reacquire the University of Minnesota Medical Center from Fairview Health. The University of Minnesota Regents voted to support a nonbinding letter of intent with Fairview that would provide the ability for the University’s eventual ownership of the medical center by 2027. The University of Minnesota previously sold the medical center to Fairview in 1997.

In January, Penn Medicine announced it intends to acquire Doylestown Health, a single-hospital system in Bucks County, PA. The seventh hospital for Penn Medicine, the acquisition of Doylestown Health follows a trend of expansion for Penn Medicine, with the acquisition of Chester County Hospital, Lancaster General Health, and Princeton Health all within the past 10 years. The transactions by academic health systems this quarter continue to follow the trend of AMC expansion through development of new entry points into their care network, investments in community health, and developing the ability to expand their teaching and research capabilities.

In addition to the sale of its Pacific Coast Network to UC Irvine Health, Tenet also sold Sierra Vista Regional Medical Center and Twin Cities Community Hospital to Adventist Health in California. The two hospitals, located in San Luis Obispo County in Central California, were sold to Adventist Health for approximately $550 million, implying a Revenue and EBITDA multiple of 1.6x and 14.5x, respectively. The Pacific Coast Network transaction to UCI Health announced in February came with a $975 million price tag, reflecting a 1.0x multiple of revenue and 13.7x multiple of EBITDA. These transactions follow trends of Tenet’s strategic divestitures in high value deals and reflect a broader trend of acquisitions of targets of high strategic value to health systems. It is worth noting that part of the reason for higher multiples in these California transactions is that buying is still cheaper than the high cost to build.

Regional expansion continued this quarter in the Northeast with Nuvance Health’s announcement in February that it will be joining Northwell Health. With seven hospitals in Nuvance and the largest in the State of New York with Northwell, the organizations would merge to form an integrated healthcare delivery system of 28 hospitals, 15,000 physicians, and over 1,000 care sites. In July 2023, Nuvance received a credit downgrade from Moody’s driven by weakened operating performance and reduced liquidity. As stated by both organizations, the merger also allows Northwell to expand into Connecticut while making significant investments in Nuvance’s existing clinical care footprint.

On the other hand, a number of regional mergers in recent years have been called off, including this quarter with the cancellation of the proposed merger between Essential Health and Marshfield Clinic. Previously announced in July 2023, the health systems formally ended merger discussions in January, determining that the affiliation was not the right path for the organizations. Marshfield previously paused merger discussions with Gundersen Health System in 2019.

There were also a number of single hospital acquisitions and tuck-in transactions for larger systems. Below are highlights of a few other notable transactions announced this quarter:

In February, St. Louis- based Mercy announced its plans to acquire Via Christi Hospital, its related physicians and other ancillary healthcare locations from Ascension. 152-bed Via Christi hospital will be Mercy’s third hospital in Kansas, as Mercy continues to grow westward. In 2023, Mercy acquired SoutheastHEALTH followed by its acquisition of Hermann Area District Hospital.

In January, Northern New Jersey health systems, CarePoint Health and Hudson Regional Hospital announced they are seeking to form a new combined entity that will merge the for-profit and not-for-profit hospitals together. Hudson Health System will be the new namesake of the four hospital system. Under the proposed agreement, two of the four hospitals will remain not-for-profit safety net hospitals. The unique arrangement comes after the New Jersey Department of Health confirmed that CarePoint was in financial distress and began to work with local government leaders on a solution. CarePoint executive leaders confirmed the arrangement with Hudson Regional will improve the organization’s operational and financial strength.

Also in New Jersey, Atlantic Health System announced in January its intent to merge with Saint Peter’s Healthcare. Atlantic Health, located in Morristown, NJ, is a seven-hospital health system with locations across New Jersey and Pennsylvania. Saint Peter’s Healthcare is a catholic not-forprofit system with a 478-bed flagship hospital in New Brunswick, NJ. The announcement follows a 2022 judgment by the FTC to block a proposed merger between Saint Peter’s Healthcare and RWJBarnabas Health, citing the deal would cause anti-competitive concerns with merging New Brunswick’s only two hospitals.

WellSpan Health signed a definitive agreement to acquire Evangelical Community Hospital, a 131-bed acute care hospital in Lewisburg, PA. With the pending acquisition, the hospital will become WellSpan Evangelical Hospital and will continue to serve the Central Susquehanna Valley. WellSpan is an eight-hospital system, serving six counties in Pennsylvania and two counties in Maryland. The deal is expected to close in July.

Each quarter, health system acquirers typically cite the need to grow and the desire to enchance clinical outcomes as motivating factors for deal activity. On the other hand, as we are seeing play out in real time, financial challenges area key driver of M&A for sellers.California-based Pipeline Health faces financial challenges as it retrenches its existing portfolio. In late 2023, Pipeline exited the Texas market driven by unsustainable financial losses. This example highlights the need for health systems to match mission-driven growth objectives with the reality of a harsh and volitile operating environment.

Portfolio rationalization,AMCs with the capital to make big bets, and inter-regional consolidations are major trends that will continue into 2024. With an election looming and an uncertain healthcare and regulatory landscape, affiliation opportunities will need to be thoughtful and metric driven.

On Monday, national supermarket giant Kroger announced that it had reached a definitive agreement to sell its specialty pharmacy business to insurer Elevance Health, which plans to fold the business into its CarelonRx pharmacy benefit manager (PBM) division. Kroger’s in-store retail pharmacies and walk-in clinics are not included in the deal, which could close in the second half of 2024. Kroger’s specialty pharmacy is the sixth largest by revenue, serving two percent of the US market. The planned sale comes as Kroger pursues a merger with rival supermarket chain Albertsons, which also operates a specialty pharmacy, although the Federal Trade Commission (FTC) recently announced that it’s challenging that merger.

The Gist: With total pharmacy spend up 25 percent since 2019, including a 34 percent growth for specialty drugs, Elevance is capitalizing on a booming market by pushing into pharmacy services, following last year’s acquisition of BioPlus, another specialty pharmacy.

Administering high-cost drugs to patients with rare or complex diseases, specialty pharmacies now account for more than half of all prescription drug spending despite making up only around two percent of total prescription volumes.

Of late, private equity investors in healthcare services have faced intense criticism that their business practices have compromised patient safety and raised costs for consumers. March 5, the FTC, DOJ and HHS announced the launch of an investigation into the inner workings of PE in healthcare. It comes on the heels of U.S. Senate investigations in their Finance, HELP and Budget Committees to explore legislative levers they might pull to address their growing concerns about affordability, competition and accountability in the industry.

PE funds don’t welcome the spotlight.

Their business model lends to misinformation and disinformation: company takeovers by new owners are rarely treated as good news unless the circumstance under prior ownership was dire. Even then, attention shifts quickly to the fairness of the PE business model playbook: acquire the asset on favorable terms, replace management, reduce operating costs, grow and the sell in 5-7 years at a profit using debt to finance the deal along the way. In exchange, the PE fund’s General Partner gets an annual management fee of 2% plus 20% of the value they create when they sell the company or take it public, and favorable tax treatment (carried interest) on their gain.

Concern about PE in healthcare services comes at a particularly delicate time: hospitals. nursing homes, outpatient care, medical practices, clinics et al) are still feeling the after-effects of the pandemic, proposed reimbursement bumps by Medicare for hospitals and physicians do not offset medical inflation and the Change Healthcare cybersecurity breach February 21 has created cash flow issues for all.

Concern about PE ownership was high already.

Innovations funded through PE-backed organizations have been drowned out by the steady drip of peer reviewed and industry-sponsored studies a causal relationship between PE ownership decreased quality and patient safety and increased prices and worker discontent. Nonetheless, PE-owns 4% of hospitals (among 36% that are investor-owned, 13% of medical practices and 6% of nursing homes today and they’re increasing in all cohorts of health services.

Here are the facts:

Private equity enjoys significant influence in public policy including healthcare. Direct lobbying activity by PE funds in Congress and state legislatures is well-funded and effective, especially by the It is increasingly 20 global fund sponsors that control 46% of assets under management. Cash on hand and fund-raising by PE are strong and healthcare remains an important but non-exclusive target of PE investing.

2023 was a down year for PE, 2024 will be strong: the IPO market and sponsor- to sponsor transactions dipped, and deal values shrank. Even with interest rates remaining high, returns exceeded overall growth in the stock market for deals consummated. At the same time, PE raised $1.2 trillion last year and has $2.6 trillion of dry powder to invest. Healthcare services will be a target as PE deal activity increases in 2024.

In U.S. healthcare, PE investments are significant and increasing. Technology-enabled services that lower unit costs and AI-based solutions that enable standardization and workforce efficiency will garner higher valuations and greater PE interest than traditional services. Valuations will recover from record 2023 lows and dry powder will be deployed for roll-ups despite antitrust concerns and government investigations. Congress will investigate the impact on PE on patient safety, prices and competition and, in tandem with FTC and DOJ issue guidance: compliance will be mandated and financial penalties added. But displacement of PE in health services is unlikely.

Some notable data:

Private equity funds have $2.49 trillion of cash on hand to invest—up 7% from 2022. They raised $1.2 trillion globally in 2023. 26% of its global dry powder is more than 4 years old—undeployed.

Private equity groups globally are sitting on a record 28,000 unsold companies worth more than $3tn. 40% of the companies waiting to be sold are at least four years old. Last year, the combined value of companies that the industry sold privately or on public markets fell 44% and the value of companies sold to other buyout groups fell 47%.

Private equity investments in almost every sector in healthcare are significant, and until lately, increasing. Last year, deals were down 16.2% (from 940 to 788) cutting across every sector. In some sectors, like physician services, PE deals were tuck-in’s to their previous platform investments increasing from 75 deals in 2012 to 484 deals in 2021.

PE investments in US healthcare exceeded $1 trillion in the last 10 years. Investments in healthcare services i.e. acute, long-term, ambulatory and physician services– have been less profitable to investors than PE investments in technology, devices and therapeutics (based on the ratio of Enterprise Value to EBITDA) but exceed equity-market returns overall.

Peer reviewed studies have shown causal relationships between private equity ownership of hospitals, nursing homes and medical practices with lower operating costs, higher staff turnover, high prices and higher profits.

My take:

Like it or not, private equity investment in healthcare is here to stay. The likelihood of higher taxes paid by employers and individuals to fund the health system is nil. The majority (69%) of the public think it wasteful and inefficient (See Polling below). The majority believe it puts its profits above all else. The majority think it needs major change. That’s not new, but it’s felt more intensely and more widely than ever.

That means accommodation for private capital, including private equity, is not a major concern to voters: the prices they pay matters more than who owns the organization.

Tighter regulation of private equity, including more rights given to the Limited Partners who invest in the PE funds and limitations on public officials who become fund advisors, are likely. Bad actors will be vilified by regulators and elected officials. Media scrutiny of specific PE funds and their GPs will intensify as PE public reporting regulations commence. And investments made by not-for-profit multi-hospital systems and independent hospitals will be critical elements in upcoming Congressional and regulatory policy setting about their community benefit accountability and tax exemptions.

The public’s major concern about its healthcare industry is affordability. To the extent PE-backed solutions offer lower-cost, higher-value alternatives on a playing field that’s level with respect to equitable access and demand-management, they will be at the table.

To the extent PE-backed solutions cherry-pick the system’s low-hanging fruit at the expense of patient safety and affordability sans any regulatory restriction, they’ll breed public discontent from those they choose to ignore.

So, the reality is this: PE’s focus is generating profits for its GP and their LPs. Doing business in a socially responsible way is a fund’s prerogative. Some do it better than others.

PE is part of healthcare’s solution to its poorly structured, perpetually inadequate and mal-distributed funding. But creating a level playing field through meaningful regulatory reform is necessary first.

PS Among the stickier issues facing hospitals is site-neutral payments. Hospitals oppose the proposal reasoning the overhead structure for their outpatient services (HOPD) include indirect & direct costs for services provided those unable to pay i.e. emergency services. Proponents of the change argue that what’s done is the key, not where it’s done, and uniform pricing is common sense. Leavitt Partners has advanced a compromise: a Unified Ambulatory Payment System for HOPDs, ASCs and physician clinics that would be applied to 66 services starting

Two newly published investigative reports, by the intrepid reporters at STAT News and The American Prospect, pull the curtains back a little more on the astonishing number of recent acquisitions UnitedHealth has made as it moves deeper and deeper into health care delivery, enabling it to grab ever-increasing chunks of our premium and tax dollars to reward its shareholders.

That’s a strategic move that allows the company to steer more seniors to facilities it owns, boosting revenues it gets from the government and padding its bottom line.

The bigger a company gets, the less it has to disclose about the acquisitions it makes in any easily obtainable way. That’s because publicly-traded companies are only required to immediately inform investors of individual deals that are “material to earnings.”

A material amount, as Investopedia explains, “can signify any sum or figure worth mentioning, as in account balances, financial statements, shareholder reports, or conference calls. If something is not a material amount, it is considered too insignificant or trivial to mention.”

UnitedHealth’s long string of acquisitions in recent years has catapulted the company to the #5 spot on the Fortune 500 list of American companies, based on revenue. Only Walmart, Exxon Mobile, Amazon and Apple are bigger.

That rapid growth means that fewer and fewer of UnitedHealth’s acquisitions reach the threshold of requiring prominent disclosure to shareholders.

It was only through a close review of UnitedHealth’s latest annual report to investors and other financial documents that STAT was able to see what the company hides from most of us. As Herman noted:

UnitedHealth Group is so big that it doesn’t have to publicly announce a vast majority of its acquisitions. But a STAT analysis of company financial documents shows the health care conglomerate quietly acquired dozens of outpatient facilities in 2023, with a particular focus on surgery centers.

And it’s not adding random surgery centers, either. There seems to be an explicit strategy: Many of UnitedHealth’s new centers sit in geographic areas where the company is the biggest Medicare Advantage player, based on the latest insurance market share data. That overlap reinforces how UnitedHealth is looking to funnel more of its insurance members toward providers that it owns, with the overarching goal of capturing more profit.

As an example, STAT said it stumbled upon an entry–”buried within UnitedHealth’s annual report”–that revealed the company’s previously undisclosed December acquisition of National Cardiovascular Partners, which operates 21 cardiac cath and vascular labs. Not coincidentally, NCP’s facilities are “in places like Phoenix and large metro areas in Texas where UnitedHealth has the biggest MA market share.”

Tkacik wrote that last Thursday, UnitedHealthcare applied for an emergency exemption that would fast-track its takeover of a medical practice in Corvallis, Oregon, which is facing the prospect of closing its doors because of the financial crunch caused by the hack. As Tkacik explained, the hack interrupted the flow of information from Change Healthcare’s claims processing systems that enables physicians, hospitals, and other health care providers to get paid.

Perversely, UnitedHealth is telling Oregon regulators that the best solution is to allow the company’s proposed acquisition of the medical practice to go forward.

Tkacik reported that:

Although the specific reason for the exemption request is redacted from the publicly posted version of the application, a clinic insider says the “emergency” is the same one that has plunged thousands of other health providers across the nation into a terrifying cash crunch…

The situation underscores the perverse state of affairs in which UnitedHealth, which comprises some 2,642 separate companies that collectively raked in $371.6 billion last year, has arguably profited from the desperation that the hacking of its Change computer systems in late February has inflicted upon the health care system.

An estimated half of all health care transactions are processed or somehow otherwise touched by Change, a rollup of dozens of health care technology firms that provide 137 software applications that have been affected by the outage.

Tkacid added that “Every dollar in revenue that has disappeared from hospitals, medical practices, and pharmacies in the aftermath of the outage corresponds to an extra dollar sitting in the coffers of the nation’s health insurers, so UnitedHealth, which pays out roughly $662 million in medical claims each day, is presumably sitting on a mountain of unexpected cash.”

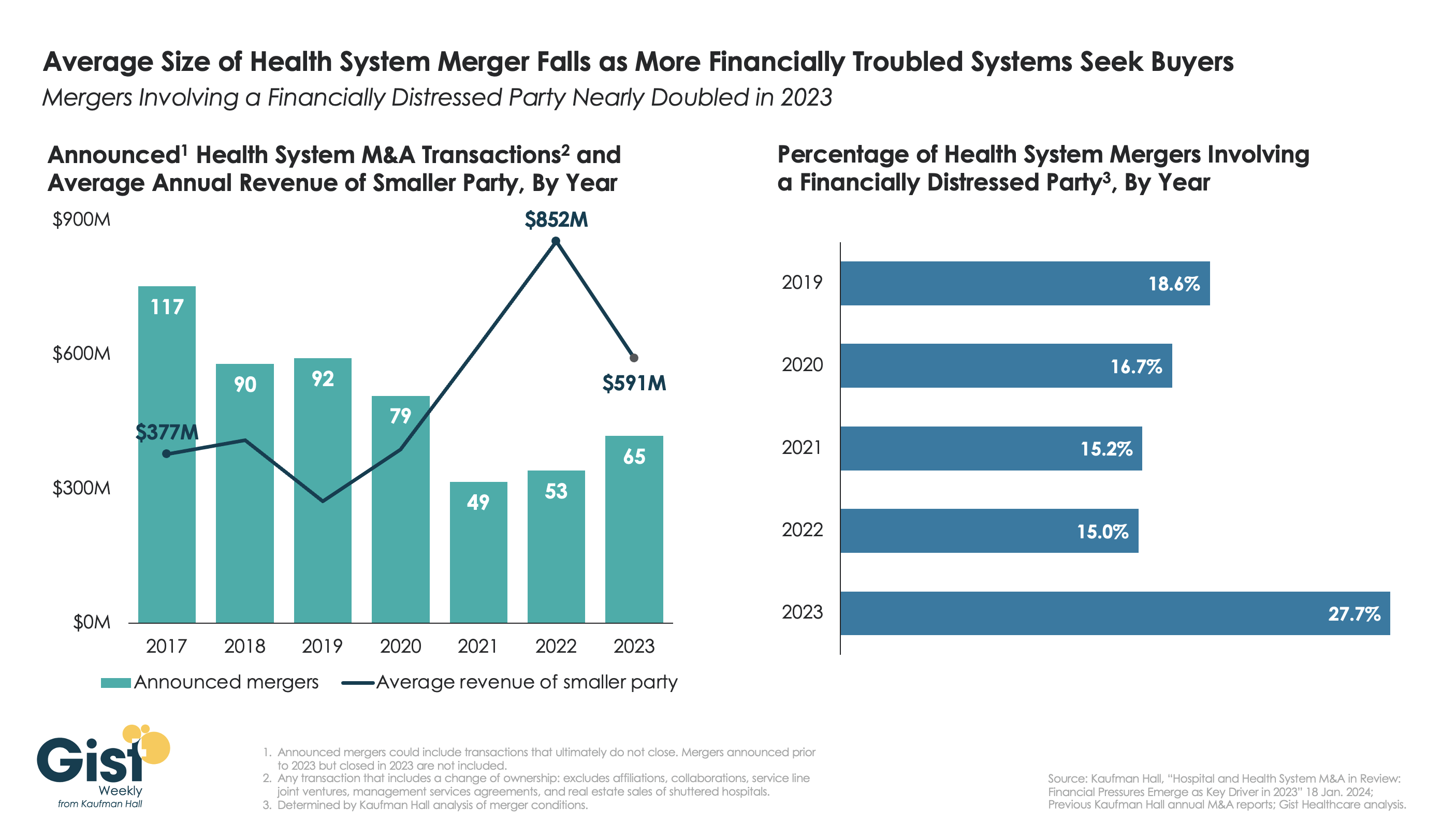

This week’s graphic highlights data from Kaufman Hall’s recently released 2023 Hospital and Health System M&A Report on the current dynamics in health system mergers and acquisitions (M&A) activity.

After a slowdown during the pandemic, 2023 saw an uptick in M&A activity with 65 announced transactions, the most since 2020. Continuing the trend of the past two years, the number of announced “mega mergers,” in which the smaller party had at least $1B in annual revenue, represented more than a tenth of total announced transactions.

However, the average size of mergers fell in 2023, as financial distress emerged as a key driver of M&A activity. The percent of mergers involving a financially distressed party spiked to nearly 28 percent in 2023, almost double the level seen in prior years.

CARES Act funding had buoyed some health systems’ balance sheets through the pandemic, but with the end of federal aid, more systems needed to seek shelter through scale.

With the median hospital operating margin still barely hitting two percent, we anticipate this heightened level M&A activity to continue in 2024 as health systems search for stronger partners that can help them stabilize financially.

In mid-January, General Catalyst (GC) and Summa Health announced the signing of a non-binding LOI for GC to acquire Summa, which, if consummated, would be a groundbreaking transaction. Summa Health is a vertically integrated not-for-profit health system located in Akron, Ohio that operates acute care hospitals, a network of health care services, a physician group practice, and a health plan. Like much of the health system sector, Summa has found the operating environment for the past couple of years to be challenging.

GC is a venture capital firm that had approximately $25B in assets under management at the end of 2022, across a dozen fund families and a number of sectors, including its Health Assurance funds, that have a stated mission of “creating a more proactive, affordable & equitable system of care.”

Health Assurance has investments in more than 150 digital health companies worldwide and has implemented working relationships with more than a dozen of the country’s most noteworthy health systems and hospital operators.

In October, GC announced the formation of a new venture called the Health Assurance Transformation Corporation (HATCo), for the purpose of providing financial and operational advisory assistance to health systems, including using GC’s suite of digital health companies. At that time, HATCo announced plans to buy a health system in order to drive transformation in the delivery of care by leveraging technology, updating workforce/staffing models, and becoming more proactive in creating revenue streams for health systems.

Their plans included an intent to streamline operations and find efficiencies using technology, as well as implementing value-based payment models, including fully capitated risk contracts to incentivize better utilization management, an initiative that requires significant data analytics.

GC had been looking for a system with market relevance and a sweet spot in terms of size – big enough to have a full complement of services, but nimble enough to accept significant change. In Summa, it has also found a system that maintains its own health plan, which GC can use to help accelerate the shift to capitated models.

The transaction that Summa and GC are contemplating is a new and innovative attempt at addressing the underlying problems that plague the acute care industry.

In particular, 1) a continued reliance on fee-for-service revenue when reimbursement has been pressured from every angle and rate increases have failed to keep pace with the rising cost of providing care, 2) capital to fund a growing list of competing needs, and 3) the challenges of staffing for quality in a tight market for clinical labor. Summa appears to be banking on the idea that GC and the data- and technology driven solutions that reside within their portfolio companies can ease those pressures.

HATCo’s proposed purchase of Summa requires a conversion of the health system to for profit. The purchase price of the health system will contribute to the corpus for a large foundation that will address social determinants of health in the Akron community, and the operating entities would become subsidiaries of HATCo.

HATCo has stated publicly that it will continue Summa’s existing charity care commitment, that Summa’s existing management team will stay in place, and the health system Board will continue to have local community representation. HATCo has also emphasized that it plans to hold Summa for an extended period and have it serve as a digital innovation testing ground and incubation site for new healthcare IT, where it believes that aligning incentives will drive financial improvement and better care.

Innovative approaches to meaningful problems should be applauded but there is skepticism.

Will bottom line pressures affect the quality of care?

Will the typical investment horizon of venture capital align with the time frames needed to prove these solutions are taking hold?

Health system evolution has traditionally been measured in decades, rather than the 5-7 year hold periods that private capital prefers. There are also perceived conflicts to consider as Summa will be paying the GC-owned companies for their services. Acute care hospitals are central elements of their communities and their constituents are broader than most companies, often including large workforces, union leadership, politicians, government regulators, and of course patients and their families.

This transaction will receive significant scrutiny with any number of constituents taking issue with a health system’s purchase by a venture capital firm. One hurdle is the conversion process itself, which requires review and approval by the Ohio Attorney General and regulators may want to impose restrictions on GCs ability to operate that are incompatible with its plans. The hurdles to closing are daunting, but the challenges facing health systems are equally daunting.

And while this proposed combination may not come to fruition, the need for innovative solutions remains.