If Trump and RFK Jr. want to crack down on deceptive health care ads, they should start with the avalanche of misleading Medicare Advantage commercials blanketing seniors every fall.

The Trump administration announced last week it plans to crack down on prescription drug advertising. In reporting on the news, the New York Times quoted former Food and Drug Administrator David Kessler as saying that what the administration is proposing “would in essence remove direct-to-consumer advertising from television.”

In a press release, Health and Human Services Secretary Robert F. Kennedy Jr. said the intent is to “shut down that pipeline of deception and require drug companies to disclose all critical safety facts in their advertising.”

You’ll get no argument from me that companies of any kind, especially those that make money in health care, should not be allowed to deceive the public by withholding critical facts.

What I do argue – and hope this administration and Democrats in Congress will agree on – is that this crackdown should also include so-called Medicare Advantage ads.

As we get close to “open enrollment” season, the period of time every fall when seniors and people with qualifying disabilities can choose between Traditional Medicare and one of many private health insurance plans, we already are beginning to see deceptive ads by Big Insurance to once again lure Medicare beneficiaries into their often deadly money machine.

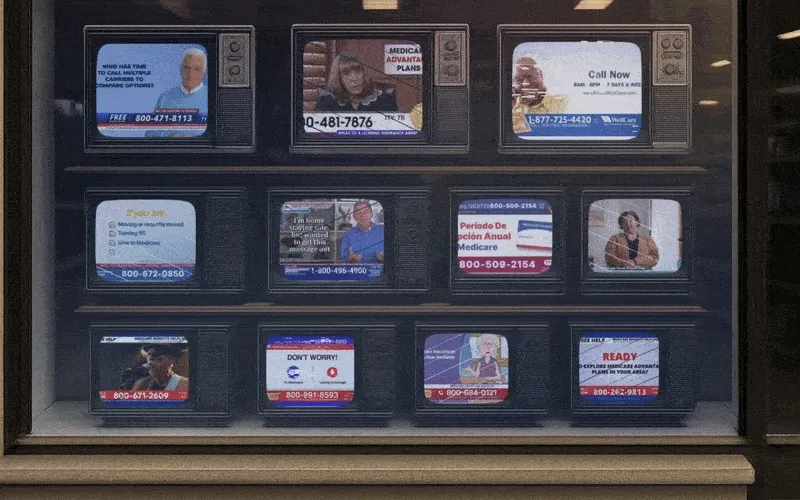

You’ve seen the ads: happy, smiling seniors playing tennis or pickleball and gabbing about “free” groceries and dental benefits they presumably get because of the generosity of their MA plans. Nowhere – ever – have you seen or heard anything in any of those ads about the potentially lethal side effect of signing up for those plans. But the terrifying truth is that an untold number of MA enrollees have gone to early graves because their insurers delayed or outright denied a test, treatment or medication their doctors said they needed. Or because they couldn’t even find a high-quality doctor, hospital or skilled nursing facility close to their home – or even far away for that matter. Many centers of excellence – hospitals and clinics that are renowned for things like cancer and cardiac care – are not in many MA plans’ “networks.”

Seniors need to be told how limited MA networks can be – and that Traditional Medicare, by contrast, doesn’t even have networks. Traditional Medicare doesn’t restrict you to certain providers. That’s because almost all doctors, labs, clinics and hospitals participate in Traditional Medicare.

And seniors need to be told explicitly in ads what prior-authorization is and how it can affect them. And they need to be told about how much money they’ll have to pay out of their own pockets if they knowingly or unknowingly get care from an out-of-network provider. They also need to be told that their MA plans can and do drop doctors and hospitals from their networks during the course of a given year and that more and more physician practices and hospitals – including world-class facilities like Johns Hopkins and M.D. Anderson and the Cleveland Clinic – have dropped out of many MA networks. And they need to be told that their MA plan could very well dump them next year by “exiting” the community they live in, as Humana, Aetna, UnitedHealth and other plans did this year and plan to do next year.

Why, Mr. Trump and Mr. Kennedy, are MA insurers not held to the same standards as pharmaceutical companies? And how fast can you put standards in place to assure us that MA ads don’t omit “critical facts?” You know as well as anyone that between October 15 and December 7 (the open enrollment period) you won’t be able to turn on your TV or scroll through your social media feeds without seeing multiple MA ads that blatantly lie by omission.

Researchers at the nonpartisan KFF found TV ads hawking MA plans ran 650,000 times during the 2022 open enrollment period. You can expect that number will be surpassed this year because Medicare Advantage has become such a cash cow for Big Insurance. As just one example, UnitedHealthcare, a division of the biggest health care conglomerate in the world, got more than 75% of its revenue last year from Medicare and other taxpayer-supported programs. Now you know why those deceptive ads are so ubiquitous, and why private insurers lie with impunity.

Speaking of UnitedHealthcare, it co-brands its MA plans with AARP, which gives that corporation a kind of good seal of approval. AARP has received billions of dollars from UnitedHealthcare over the years as part of the relationship. To its credit, AARP called attention to that KFF study on its website just before the 2023 open enrollment season started. That’s notable, but AARP needs to do much more. So I am hereby calling on AARP to join us in demanding that both the Trump administration and Congress take immediate action to make sure MA ads cannot leave out essential information. Truthful MA ads are just as important as drug company ads. Maybe even more so when you consider all the potential harms MA plans inflict on seniors and people with disabilities every single year.