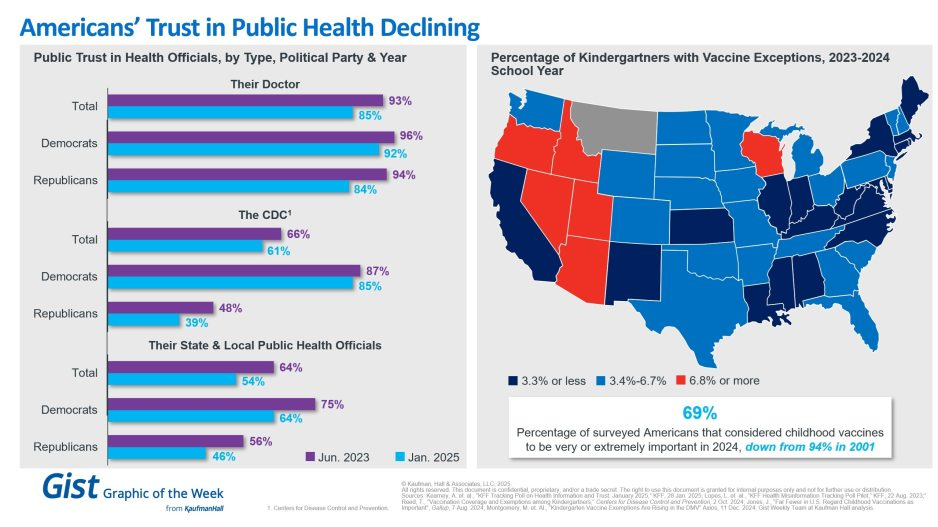

In light of the recent confirmation of Secretary Kennedy to lead HHS and new survey data on trust in public health, this graphic highlights Americans’ declining positive perception of public health officials. Among respondents’ personal doctors, the CDC and their state and local public health officials, trust in all three, regardless of political identification, has decreased from June 2023 to January 2025.

Respondents trusted their doctors more than public health officials, and there is less difference by political identification. In 2025, only 61% of surveyed Americans reported that they trusted the CDC. That prevalence drops to 39% among Republicans and increases to 85% among Democrats.

Another important public health indicator, the percentage of kindergarteners with vaccine exemptions, also illustrates the challenging place in which public health officials find themselves. During the 2023-2024 school year, about 3.3% of kindergartners received an exemption, an increase from 2022-2023 that still does not provide a complete picture. Exemption rates vary widely by state, with 6 states having exemption rates more than double the median. These differences are a reflection of how easy it is to receive an exemption in some states rather than a clear trend.

The shift also underscores how easily an outbreak could occur in some states. Alarmingly, the perceived importance of vaccines has dramatically decreased, from 94% in 2001 to 69% in 2024.

We will have to wait and see what Kennedy, long considered a vaccine skeptic, does regarding vaccines, but amid immense distrust in the healthcare system, providers’ role of giving thorough, honest information to their patients is more important than ever.

On January 17, 2025, a list of potential cost reductions to the federal budget was released by Republicans on the House Budget Committee. The list is long and covers the federal budget waterfront, but it spends considerable time focusing on reductions to healthcare spending. This laundry list of cost reductions is important because the highest priority of the Trump administration is a further reduction in federal taxes. A reduction in taxes would, of course, reduce federal revenue; if federal expenses are not proportionately reduced then the federal deficit will increase. When the deficit increases then the federal debt must increase and at that point the overall impact on the American economy becomes concerning and possibly damaging. There has already been much public speculation as to how the Federal Reserve might react to such a scenario.

It is not possible right now to highlight and describe all of the House budget proposals, but one proposal absolutely stands out: The suggestion to eliminate the tax-exempt status for interest payments on all municipal bonds, or potentially in a more targeted manner, for private activity bonds, including those issued by not-for-profit hospitals. Siebert Williams Shank, an investment banking firm, described the elimination of tax exemption for municipal bonds as “the most alarming of the proposed reforms impacting non-profit and municipal issuers.”[1] This is certainly true for hospitals, since over the past 60 years the growth and capability of America’s hospitals has been substantially constructed on the foundation of flexible and relatively inexpensive tax-exempt debt. Given all of this, it is not too early to begin speculating on the impact of the elimination of tax-exempt debt on hospital finances and strategy.

We should also point out that a separate topic is under discussion, related to the potential loss of not-for-profit status for hospitals and health systems. Such a maneuver could potentially expose hospitals to income taxes, property taxes, and higher funding costs. For now, that is beyond the scope of this blog but may be something we write about in future posts.

Below is a series of important questions related to the elimination of tax-exempt financing and some speculations on the overall impact:

What immediately happens if 501(c)(3) hospitals lose the ability to issue tax-exempt bonds? Let’s treat fixed rate debt first. Assume for now that only newly issued debt would be affected and that all currently outstanding tax-exempt fixed rate debt would remain tax-exempt. We could see an effort to apply any changes retroactively to existing bonds, but we view that as unlikely. Therefore, our current expectation is that outstanding fixed-rate debt would not see a change in interest expense.

However, it is possible that outstanding floating rate debt would immediately begin to trade based on the taxable equivalent. Historically the tax-exempt floating rate index trades at about 65% of the taxable index. The difference between the tax-exempt and taxable floating rate indices in the current market is 175 basis points. For every $100 million of debt, this would increase interest expense by $1.75m annually.

How would new hospital debt be issued? New debt would be issued in the municipal market on a taxable basis or in the corporate taxable market. The taxable municipal market would need to adapt and expand to accommodate a significant level of new issuance. The concern in the corporate taxable market is greater. Currently, the corporate market requires issuance of significant dollar size and generally the issuer brings significant name recognition to the market. Many hospitals may have difficulty meeting the issuance size of the corporate debt market and/or the necessary market recognition. As such, smaller and less frequent issuers would expect to pay a penalty of 25-50 basis points for issuing in the corporate market.

If tax-exempt debt goes away will certain hospitals be advantaged and others disadvantaged? Larger hospitals with national or regional name recognition that issue bonds with sufficiently large transaction size and frequency will likely borrow at better terms and lower rates. Smaller- to medium-sized hospitals may find borrowing much more difficult, and borrowing may come with more problematic terms and/or amortization schedules and likely higher interest rates.

Will borrowing costs go up? The cost of funds for new borrowings would increase for all hospital borrowers. For a typical A-rated hospital, annual interest expense would increase by approximately 30%. For example, in the current market, on $100 million of new debt, average annual interest expense would increase by $815,000 annually.

Will debt capacity go down? All other things being equal, interest rates will go up and hospital debt capacity will go down. Also, if the taxable market shortens amortization schedules, then that will decrease overall debt capacity as well.

What would the impact of the elimination of tax-exempt debt be on synthetic fixed rate structures? Hospitals have long employed derivative structures to hedge interest rate risk on outstanding variable rate bonds and loans. The loss of tax-exemption for outstanding variable rate bonds and loans would precipitate an adjustment to taxable rates, but corresponding swap cash flows are not designed to adjust. Interest rate risk is hedged, but tax reform risk is not. The net effect to borrowers would be an increase in cost similar to the cost contemplated above for variable rate bonds.

What are the rating implications of the elimination of the tax-exempt market? Rating implications will be varied. Hospitals with strong financial performance and liquidity are likely to absorb the increased interest expense of a taxable borrowing with little to no rating impact. In fact, over the past decade, many larger health systems in the AA rating categories have successfully issued debt in the taxable market without rating implications despite a higher borrowing rate. Even amid the pandemic chaos of 2021, numerous AA and A rated systems issued sizable, taxable debt offerings to bolster liquidity as proceeds were for general corporate purposes and not restricted by a third-party, such as a bond trustee.

Lower-rated hospitals with modest performance and below-average liquidity will be at greater risk for a downgrade. These hospitals may not be able to absorb the increased interest expense and maintain their ratings. While interest expense is typically a small percentage of a hospital’s total expenses, it is a use of cash flow.

We do not anticipate the rating agencies will take wholesale downgrade action on the rated portfolio as there would likely be a phase-in period before the elimination occurs. Rather, we expect the rating agencies will take a measured approach with a case-by-case evaluation of each rated organization through the normal course of surveillance, as they did during the pandemic and liquidity crisis in 2008. A dialogue on capital budgets and funding sources, typically held at the end of a rating meeting, would be moved to the top of the agenda, as it will have a direct impact on long-term viability.

How would the loss of the tax-exempt market impact the pace of consolidation in the hospital industry? If a hospital cannot afford the taxable market, then large capital projects would need to be funded through cash and operations. This inevitably will limit organizational liquidity, which will lead to downward rating pressure. Some hospitals, in such a situation, will be unable to both fund capital and adequately serve their local community and, therefore, will need to find a partner who can. We anticipate that the loss of the tax-exempt bond market will lead to further consolidation in the industry.

Let’s indulge in one last bit of speculation. What is the probability that Congress will pass legislation that eliminates tax-exempt financing? Sources in Washington tell us that it is premature to wager on any of the items put forth by the Budget Committee. And it should be noted that over the years the elimination of tax-exempt financing has been proposed on several occasions and never advanced in Congress. However, one well-informed source noted that as the tax and related legislation moves forward, there is likely to be significant horse-trading (especially in the House) to secure the necessary votes to pass the entire package. What happens during that horse-trading process is anybody’s guess. So the best advice to our hospital readership right now is to not take anything for granted. But be absolutely assured that the maintenance of tax-exempt financing is an essential strategic component for the successful future of America’s hospitals.

For the past six years, Kaufman Hall has been publishing its monthly National Hospital Flash Report, which is designed to provide a pulse on the health of the healthcare industry and to highlight meaningful and pertinent trends for hospital and health system leaders. The data that powers the report is taken from over 1,300 hospitals, which are reflective of all geographic locations, hospital sizes and types. To ensure the content is digestible and understandable, Kaufman Hall aggregates the data into larger cohorts and measures a select set of key metrics that are most important for understanding the health of the industry. Industry groups and system leaders use these reports both for peer review purposes but also to paint an overall story for their boards and communities.

Through a detailed review of the Flash Report data, each month Kaufman Hall develops findings that healthcare leaders may find instructive as they determine how to adjust to changing market conditions. In 2024 it was reasonably obvious that there was a widening divide between the highest performing hospitals and the lowest performers.While a significant cadre of hospitals and health systems have recovered to pre-Covid financial success, 37% of American hospitals continue to lose money.

We are often asked what the successful hospitals are doing—and importantly—what the data tell us about those that are less successful. Using 2024 data, we have drawn two important conclusions around the role of leading management teams and what separates their organizations from others.

These teams have:

A sophisticated and balanced approach to the management of departmental performance: and

An understanding of the management of shared service costs.

A sophisticated and balanced approach to the management of departmental performance

It turns out that current data demonstrate that the management of departmental performance is critical to overall hospital financial performance but in a more nuanced manner than expected.

Our analysis was conducted as follows:

First, we looked at data across hospitals nationwide to understand the difference in departmental performance between top and bottom performing hospitals.

Second, we ranked each department in a hospital from 0 to 100, with 100 representing the best performance based on expense per unit of service.

Third, we then grouped all hospitals based on their bottom-line operating margin into three cohorts: those hospitals that fell into the bottom quartile of financial performance, those between the bottom and top quartile, and those in the top quartile.

Finally, we created a histogram of the average composition of departmental performance across each of the three margin cohorts.

The findings demonstrate that organizations with top financial performance have departmental results that look like a normal curve around the median. Said more simply, in top-performing hospitals the number of lower-performing departments is roughly equal to the number of higher-performing departments, with most departments operating near the national departmental medians. In contrast, hospitals with the lowest financial performance show a much greater number of departments operating with high cost per units of service and a few departments that operate extremely efficiently.

It appears that poorer performing hospitals focus on the management of the largest clinical and nursing areas. These are the departments that tend to be the “easiest” to manage because they are the “easiest” to benchmark. But the data show that these same hospitals tend to have poor performance over the remainder of the departments, which leads to poor financial results for the total hospital.

Hospitals with top quartile financial performance tend to manage all departments as close to the benchmark median as possible. Such a result means spending more managerial time on the harder to manage departments, especially those departments that are more “unique” and where overall performance is harder to characterize and benchmark.

The observations that can be drawn here are important and as follows:

First, oversight and management of individual departments is critical to the financial success of the entire hospital or system.

Second, the overall organizational structure of departmental administration is critical as well. The more complicated your departmental structure and the more individual departments you maintain and administer, the more difficult it will be to manage a majority of departments to “median” results.

The data suggest a perhaps unexpected operational conclusion. The achievement of median national departmental benchmarks is leading to overall positive hospital financial operating margins. This outcome offers significant budgeting advice and over the course of a fiscal year should prove to be a remarkably useful administrative lesson.

Understanding the management of shared service costs

Given the growing costs of shared services and related overhead, Kaufman Hall wanted a closer look at how well hospital organizations were scaling shared service costs related to the organization’s size. Unexpectedly, shared service costs were not highly correlated to the size of the hospital or hospital system. This suggests that the management of shared service costs on a per unit basis is difficult and that this aspect of expense management requires diligent focus to enact and sustain cost change. Our data often indicates a wide variation of cost performance among shared services of similar types within different large organizations. This suggests that standardization of such services is not well developed and that there may be a certain level of wishful thinking that increases in organizational size will automatically correlate to lower per unit costs.

The data did indicate, however, that larger organizations can achieve higher performance over smaller organizations relative to shared service expenses. This is an indication that size can be leveraged for superior performance but that such results are not automatic. The takeaway here is that the total spend for shared service functions is very substantial and growing. In that regard, it is most important to proactively address expenses in these areas, build appropriate management plans, and understand how to focus on the right buttons and levers. To the extent that organizations are assuming that growth (both organic and inorganic) will create economies of scale with the overall shared service apparatus, the data demonstrate that such an outcome is possible but only with strong planning and execution.

Operating hospitals in 2025 is flat-out hard and likely to get harder over the year. Hospital executives right now should use every managerial advantage available. A close look at the National Hospital Flash Report data identifies important relationships that provide for a more nuanced and sophisticated operation of both individual departments and the bundle of shared services. The data clearly demonstrate that better results in both these areas will lead to improved financial performance within the hospital overall. The data also indicate key managerial strategies that will lead to such improvement.

Tonight at midnight, thousands of federal workers face the possibility their jobs will be eliminated as part of the Department of Government Efficiency (DOGE) federal cost reduction initiative under Elon Musk’ leadership. Already, thousands who serve in federal healthcare roles at the NIH, CDC and USAID have been terminated and personnel in agencies including CMS, HHS and the FDA are likely to follow.

The federal healthcare workforce is large exceeding more than 2.5 million who serve agencies and programs as providers, clerks, administrators, scientists, analysts, counselors and more. More than half work on an hourly basis, and 95% work outside DC in field offices and clinics. For the vast majority, their work goes unnoticed except when “government waste” efforts like DOGE spring up. In those times, they’re relegated to “expendables” status and their numbers are cut.

The same can be said for the larger private U.S. healthcare workforce. Per the U.S. Bureau of Labor Statistics, industry employment was 21.4 million, or 12.8% of total U.S. employment in 2023 and is expected to reach 24 million by 2030. It’s the largest private employer in the U.S. economy and includes many roles considered “expendable” in their organizations.

Facts about the U.S. healthcare workforce:

More than 70% of the healthcare workforce work in provider settings including 7.4 million who work in hospitals.

More than half work in non-clinical roles.

Home health aides is the highest growth cohort and hospitals employ the biggest number (7.4 million).

29% of physicians and 15% of nurses are foreign born, almost three-fourths of the workforce are women, two-thirds are non-Hispanic whites, and the majority are older than 50.

Its licensed professions enjoy public trust ranking among Gallup’s highest rated though all have declined:

% 2023

‘19-‘23

’23 Rank

% 2023

‘19-‘23

’23 Rank

Nurses

78

-7

1

Pharmacists

55

-9

6

Dentists

59

-2

Psychiatrists

36

-7

9

Medical doctors

56

-9

5

Chiropractors

33

-8

10

The Perfect storm

The healthcare workforce is unsteady: while stress and burnout are associated with doctors and nurses primarily, they cut across every workgroup and setting.

Consumers are worried about their costs of living: it hits home hardest among young, low-income households including dual eligible seniors for whom gas, food and transportation are increasing faster than their incomes, and rents exceed 50% of their income. The healthcare workforce takes a direct hit: one in five we employ cannot pay their own medical bills.

Slowdown in consolidation:

The Federal Trade Commission’s new pre-merger notification mandate that went in effect today essentially requires greater pre-merger/acquisition disclosures and a likely slowdown in deals. Organizations anticipating deals might default to layoffs to strengthen margins while the regulatory consolidation dust settles. Expendables will take a hit.

Uncertainty about Medicaid cuts:

In the House’ budget reconciliation plan, Medicaid cuts of up to $880 billion/10 years are contemplated. A cut of that magnitude will accelerate closure of more than 400 rural hospitals already at risk and throw the entire Medicaid program into chaos for the 79 million it serves—among them 3 million low-hourly wage earners in the healthcare workforce and at least 2 million in-home unpaid caregivers who can’t afford paid assistance. The impact of Medicaid cuts on the healthcare workforce is potentially catastrophic for their jobs and their health.

Heightened attention to tax exemptions for not-for-profit hospitals:

Large employers sent this recommendation to Congressional leaders last week as spending cuts were being considered: “Nonprofit hospitals, despite their tax-exempt status, frequently prioritize profits over patient care. Many have deeply questionable arrangements with for-profit entities such as management companies or collections agencies, while others have “joint ventures” with Wall Street hedge funds or other for-profit provider or staffing companies. Nonprofit hospitals often shift the burden of their costs onto taxpayers and the communities they serve by overcharging for health care services, or abusing programs intended to provide access to low-cost care and prescription drugs for low-income patients. By eliminating nonprofit hospital status, resources could be more evenly distributed across the healthcare system, ensuring that hospitals are held accountable for their charitable care both to their communities and the tax laws that govern them.” Pressures on NFP hospitals to lower costs and operate more transparently are gaining momentum in state legislatures and non-healthcare corporate boardrooms. Belt tightening is likely. Layoffs are underway.

Heightened attention to executive compensation in healthcare organizations:

Executive compensation, especially packages for CEO’s, is a growing focus of shareholder dissent, Congressional investigation, media coverage and employee disgruntlement. Compensation committee deliberations and fair market comparison data will be more publicly accessible to communities, rank and file employees, media, regulators and payers intensifying disparities between “labor” and “management”.

Increased tension between providers and insurers:

Health insurers are now recovering from 2 years of higher utilization and lower profits; hospitals did the same in 2022 and 2023. Neither is out of the woods and both are migrating to tribal warfare based on ownership (not-for-profit vs. investor owned vs. government owned), scale and ambition. Bigger, better-capitalized organizations in their ranks are faring better while many struggle. The workforce is caught in the crossfire.

Increased pressure on private equity-backed employers to exit:

The private equity market for healthcare services has experienced a slow recovery after 2 disappointing years peppered by follow-on offerings in down rounds. Exit strategies are front and center to PE sponsors; workforce stability and retention is a means to an end to consummate the deal—that’s it.

The AI Yellow Brick Road:

Last and potentially the most disruptive is the role artificial intelligence will play in redefining healthcare tasks and reorganizing the system’s processes based on large-language models and massive investments in technology. Job insecurity across the entire healthcare workforce is more dependent on geeks and less on licensed pro’s going forward.

These eight combine to make life miserable most days in health human resource management. DOGE will complicate matters more. It’s a concern in every sector of healthcare, and particularly serious in hospitals, medical practices, long-term and home care settings.

‘Modernizing the healthcare workforce’ sounds appealing, but for now, navigating these issues requires full attention. They require Board understanding and creative problem-solving by managers. And they merit a dignified and respectful approach to interactions with workers displaced by these circumstances: they’re not expendables, they’re individuals like you and me.

In May 2024 a set of articles were published in the journal Science that focused on the intersection of misinformation and social media. The results, while preliminary in the grand scheme of things, were really interesting (and maybe a little alarming).

Last week, I made my once a decade trek to a dealership to buy a new car. I did my research in advance (and even negotiated the price) so I was hoping for a stress-free experience.

It was – up until the point where I got locked in the finance manager’s office for “the talk”. You know, the one where you are made to feel like a neglectful parent unless you pony up for all the fixin’s – everything from nitrogen filled tires to paint protection (just in case I encounter a flock of migratory geese on the drive home). I shook my head no about ten times before we got to the pre-paid maintenance plan options. I decided to be polite and listen (plus I was curious since I was purchasing a car from a manufacturer notorious for costly repairs). As compelling as it was to pay nearly $5,000 to what ultimately would amount to a few tire rotations for my electric vehicle, I held firm. The finance manager angrily handed me my signed documents and whisked me out of his office.

I guess I can’t blame car dealers for applying massive mark-ups for services that are inexpensive to provide. Except similar financial chicanery is currently playing out in our health insurance system. If you swap out the finance manager for a health insurer and replace me with the average everyday consumer, the dealer’s tactics are analogous to how insurers game medical loss ratio (MLR) requirements (except as a health care consumer, you can’t say “no”).

A bit of background is in order to understand why I thought about health insurance and car dealers in the same breath.

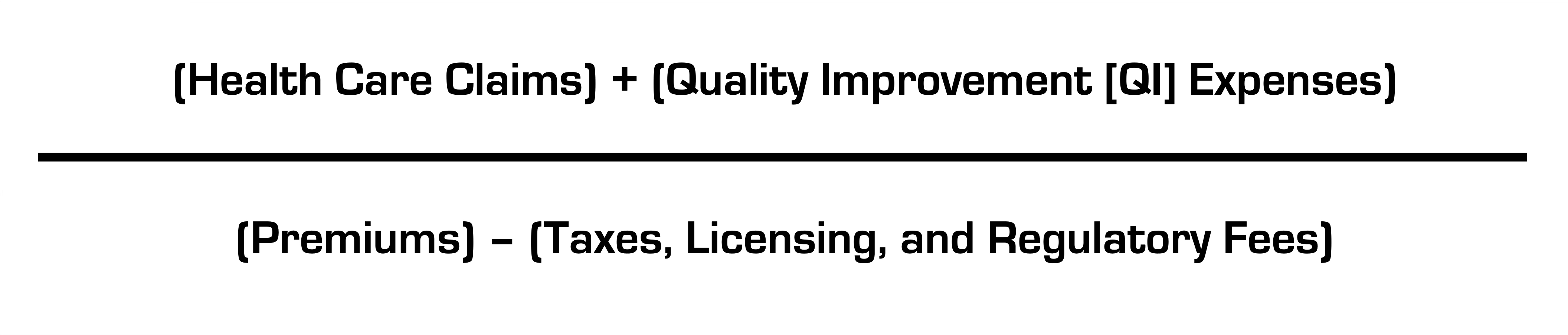

Insurance companies are required to spend a certain percentage of money they get from premiums on medical costs and quality improvement (QI); this is known as the medical loss ratio (MLR). If companies do not meet this ratio (usually 80-85%, depending on the product), they must refund the difference in the form of a rebate, or reduction in future premiums, to consumers.

Like any for-profit corporation in America today, a health insurer wants to avoid giving money back to consumers. Therefore, insurers have become adept at manipulating their MLRs through various accounting and financial engineering techniques. This manipulation optimizes their ability to meet MLR thresholds and avoid paying rebates, which runs afoul of its intended purpose: to ensure that patients receive the appropriate level of care.

So how do insurers game the system, and what evidence exists for this activity?

The current MLR formula is:

Health insurers do not control taxes and fees, but they can easily engineer the other variables. Below, I’ll explain how.

Step 1: Quality Improvement (QI) Expenses

The definition of allowable QI expenses is broad and includes activities to improve outcomes, patient safety, and reduce mortality (mom and apple pie stuff). Insurers played a big role in writing the MLR regulations after Congress enacted legislation and made sure they’d have wide latitude in what expenses are classified as QI (akin to the car dealer “option” list) and what product segments they assign them to.

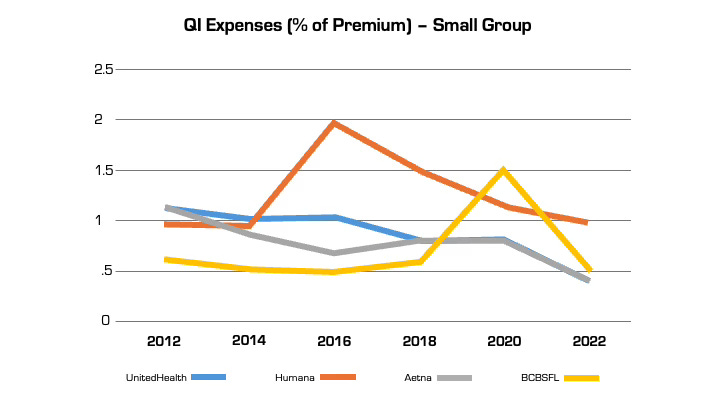

Looking at reported QI expenses sheds light on this practice. QI expenses vary between insurers. But they also vary widely for the same insurer from year to year (even after controlling for geography and product segment). In large part, this is attributable to financial engineering. QI costs can be effectively “transferred” on the income statement from one product segment to another, by adjusting the pro rata weightings). This enables them to optimize MLR performance across their insurance portfolio (i.e. by taking from a bucket with excess medical costs and putting it in another with insufficient costs) in a way that maximizes benefit to the insurer and is camouflaged from regulators and consumers. This is language from a recent UnitedHealth Group filing with the Securities and Exchange Commission: “Assets and liabilities jointly used are assigned to each reportable segment using estimates of pro-rata usage.”

Annual QI expenses across four insurers in Florida in the small group market.

Although these QI percentages are small, the associated dollar amounts are large. In 2022, UnitedHealth, Humana, and Aetna reported $494 million, $550 million, and $395 million respectively in allowable QI expenses for their national plans. While there is some legitimate QI activity at insurers (e.g., pharmacists who identify high risk medications in the elderly), the reality is that much of the QI work is already heavily resourced within provider organizations, where it is more effective. Insurers also can (and do) count “wellness and health promotion activities” despite limited evidence these programs improve health outcomes and are more often used by insurers as marketing tools.

Step 2. Health Care Claims

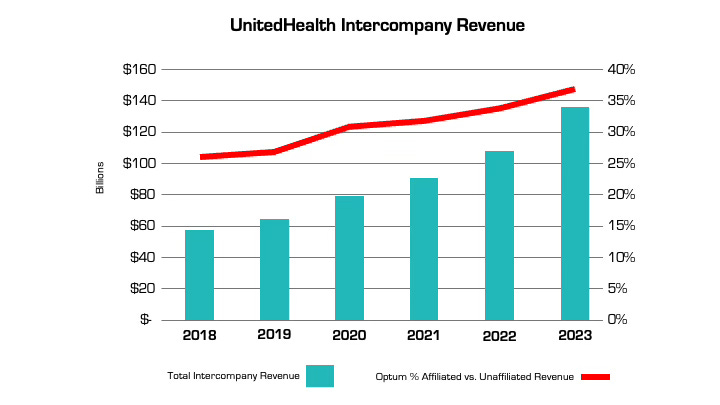

The other variable that insurers can manipulate is claims costs. The more an insurer is vertically integrated, the easier it is. The prime example is UnitedHealth, which has an insurance arm (UnitedHealthcare) and a big division that encompasses medical services, among many other things (Optum), as well as various other subsidiaries. Optum Health and Optum Rx receive a significant portion of their revenue from UnitedHealthcare for providing services like care and pharmacy benefit management to people enrolled in its health plans. In fact, the amount of UnitedHealth’s corporate “eliminations,” (meaning inter-company revenue that is reported on their consolidated financial statement) has more than doubled over the past five years (from $58.5 billion to $136.4 billion). The proportion of revenue Optum derives from UnitedHealthcare versus unaffiliated entities has increased by nearly 50% over the same period. A similar trend is playing out at every major insurer.

Take the example of the insurance company Aetna, the PBM CVS Caremark, and CVS Pharmacy, which are all vertically integrated and owned by CVS Health. If a patient goes to a CVS store to fill a prescription for Imatinib, a generic chemotherapy drug, the total cost the patient and insurance company pay is $17,710.21 for a 30-day supply. The same drug is sold by Cost Plus Drugs for $72.20 (the cost is calculated by adding the wholesale price and a 15% fee). When the patient fills the prescription at a CVS retail pharmacy, CVS Health can record that the patient paid a medical claim cost of $17,710.21 (even though the cost to acquire the drug is $70) and the remaining $17,640 can be retained as profits disguised as medical costs.

Insurers’ extensive acquisition of physician practices also facilitates gamification of the MLR via its ability to pay capitation (a set amount per person) to a risk-bearing provider organization (RBO) it owns, such as a medical group. This enables the insurer to lock in a set amount of premium as “medical expense” (usually around 85%) with the downstream provider group “managing” those costs. There’s a loophole, however. While the insurer has technically met its MLR requirement, the downstream RBO is subject to far fewer regulations on how it spends the money, which makes it easier to generate profits by skimping on care.

The regulations on RBOs vary by state. In many cases, while RBOs need to meet minimum capital requirements, they are not subject to the same MLR provisions as insurers. For a vertically integrated insurer that gets a huge amount of revenue from taxpayer-supported programs like Medicare Advantage and Medicaid, this essentially means that (1) the Center for Medicare and Medicaid Services puts the money into the insurer’s right pocket, (2) the insurer moves it to the left pocket, and (3) CMS checks the right pocket – and just the right pocket – at the end of the year to make sure it’s mostly empty (without regard to the fact that the left one may be busting at the seams).

The good news is there are ways to address these issues, both through updating the MLR provisions in the Affordable Care Act (which are long in the tooth) and more rigorous and comprehensive reporting requirements and regulation of vertically integrated insurers.

Just like I don’t want car dealers pushing unnecessary add-ons to increase their profit margins, consumers deserve that the required portion of their hard spent premium dollar actually goes toward their health care instead of further enriching huge corporations, executives, and Wall Street shareholders.

Health systems are rightly concerned about Republican plans to cut Medicaid spending, end ACA subsidies and enact site neutral payments, says consultant Michael Abrams, managing partner of Numerof, a consulting firm.

“Health systems have reason to worry,” Abrams said shortly after President Donald Trump was inaugurated on Monday.

While Trump mentioned little about healthcare in his inauguration speech, the GOP trifecta means spending cuts outlined in a one-page document released by Politico and another 50-pager could get a majority vote for passage.

Of the insurers, pharmaceutical manufacturers and health systems that Abrams consults with, healthcare systems are the ones that are most concerned, Abrams said.

At the top of the Republican list targeting $4 trillion in healthcare spending is eliminating an estimated $2.5 billion from Medicaid.

“There’s no question Republicans will find savings in Medicaid,” Abrams said.

Medicaid has doubled its enrollment in the last couple of years due to extended benefits made possible by the Affordable Care Act, despite disenrolling 25 million people during the redetermination process at the end of the public health emergency, according to Abrams.

Upward of 44 million people, or 16.4% of the non-elderly U.S. population are covered by an Affordable Care Act initiative, including a record high of 24 million people in ACA health plans and another 21.3 million in Medicaid expansion enrollment, according to a KFF report.Medicaid expansion enrollment is 41% higher than in 2020.

The enhanced subsidies that expanded eligibility for Medicaid and doubled the number of enrollees are set to expire at the end of 2025 and Republicans are likely to let that happen, Abrams said. Eliminating enhanced federal payments to states that expanded Medicaid under the ACA are estimated to cut the program by $561 billion.

If enhanced subsidies end, the Congressional Budget Office has estimated that the number of people who will become uninsured will increase by 3.8 million each year between 2026 and 2034.

The enhanced tax subsidies for the ACA are set to expire at the end of 2025. This could result in another 2.2 million people losing coverage in 2026, and 3.7 million in 2027, according to the CBO.

WHY THIS MATTERS

For hospitals, loss of health insurance coverage means an increase in sicker, uninsured patients visiting the emergency department and more uncompensated care.

“Health systems are nervous about people coming to them who are uninsured,” Abrams said. “There will be people disenrolled.”

The federal government allowed more people to be added to the Medicaid rolls during the public health emergency to help those who lost their jobs during the COVID-19 pandemic, Numerof said. Medicaid became an open-ended liability which the government wants to end now that the unemployment rate is around 4.2% and jobs are available.

An idea floating around Congress is the idea of converting Medicaid to a per capita cap and providing these funds to the states as a block grant, Abrams said. The cost of those programs would be borne 70% by the federal government and 30% by states.

This fixed amount based on a per person amount would save money over the current system of letting states report what they spent.

Another potential change under the new administration includes site neutral Medicare payments to hospitals for outpatient services.

The HFMA reported the site neutral policy as a concern in a list it published Monday of preliminary federal program cuts totaling more than $5 trillion over 10 years. The 50-page federal list is essentially a menu of options, the HFMA said, not an indication that programs will actually be targeted leading up to the March 14 deadline to pass legislation before federal funding expires.

Other financial concerns for hospitals based on that list include: the elimination of the tax exemption for nonprofit hospitals, bringing in up to $260 billion in estimated 10-year savings; and phasing out Medicare payments for bad debt, resulting in savings of up to $42 billion over a decade.

Healthcare systems are the ones most concerned over GOP spending cuts, according to Abrams. Pharmacy benefit managers and pharmaceutical manufacturers also remain on edge as to what might be coming at them next.

THE LARGER TREND

President Donald Trump mentioned little about healthcare during his inauguration speech on Monday.

Trump said the public health system does not deliver in times of disaster, referring to the hurricanes in North Carolina and other areas and to the fires in Los Angeles.

Trump also mentioned giving back pay to service members who objected to getting the COVID-19 vaccine.

He also talked about ending the chronic disease epidemic, without giving specifics.

“He didn’t really talk about healthcare even in the campaign,” Abrams said.

However, in his consulting work, Abrams said, “The common thread is the environment is changing quickly,” and that healthcare organizations need to do the same “in order to survive.”

Liberal advocacy groups are ramping up efforts to protect the Medicaid program from potential cuts by Republican lawmakers and the new Trump administration.

The Democratic group Protect Our Care launched Tuesday an eight-figure “Hands off Medicaid” ad campaign targeting key Republicans in the House and Senate, warning of health care being “ripped away” from vulnerable Americans.

The lawmakers include GOP Sens. Bill Cassidy (La.), Chuck Grassley (Iowa), Lisa Murkowski (Alaska) and Susan Collins (Maine), as well as Reps. David Schweikert (Ariz.), Mike Lawler (N.Y.) and David Valadao (Calif.).

The campaign will also include digital advertising across platforms targeting the Medicaid population in areas around nursing homes and rural hospitals, ads on streaming platforms as well as billboards and bus stop wraps.

Medicaid covers 1 in 5 Americans, and the group wants to highlight that includes “kids, moms, seniors, people of color, rural Americans, and people with disabilities.”

“The American people didn’t vote in November to have their grandparents kicked out of nursing homes or health care ripped away from kids with disabilities or expectant moms in order to give Elon Musk another tax cut,” Protect Our Care chair Leslie Dach said in a statement.

House Republicans have expressed openness to making some drastic changes in the Medicaid program to pay for extending President Trump’s signature tax cuts, including instituting work requirements and capping how much federal money is spent per person. The ideas have been conservative mainstays since they were included as part of the 2017 Obamacare repeal effort.

Separately, advocacy group Families USA led a letter with more than 425 national, state and local organizations calling on Trump to protect Medicaid.

The groups noted that if the Trump administration wants to trim health costs, “there are many well-vetted, commonsense and bipartisan proposals” that don’t involve slashing Medicaid.

“In 2017, millions upon millions of Americans rose up against proposed cuts and caps and made clear how much they valued Medicaid as a critical health and economic lifeline for themselves, their families, and their communities. The American people are watching once again, and we urge you to take this opportunity to choose a different path,” they wrote.

Downgrades continued to outpace upgrades in 2024 although at a lower rate than in 2023. When combining the rating actions of the three rating agencies, the number of downgrades (95) declined while the number of upgrades (37) increased, compared to 116 and 33, respectively, in 2023. Many of the downgrades reflected ongoing expense pressure that exceeded revenue growth, even as volumes headed back to pre-pandemic levels and the use of contract labor declined. Other downgrades reflected outsized increases in debt to fund pivotal growth strategies. Most of the upgrades reflected mergers of lower-rated hospitals into higher-rated systems. Rating affirmations remained the majority rating action in 2024, as in prior years.

Key takeaways include:

The ratio of downgrades to upgrades narrowed at Moody’s (2.0-to-1 in 2024 from 3.2-to-1 in 2023) and Fitch (1.5-to-1 from 3.5-to-1). S&P saw a wider spread in the ratio: 4.5-to-1 in 2024 from 3.8-to-1 in 2023.

Downgrades reflected a wide swath of hospitals, from small independent providers to large regional systems. Large academic medical centers and children’s hospitals saw downgrades, even with exclusive tertiary services that provided differentiation with payers. Shared, recurring downgrade factors included weaker financial performance, payer mix shifts to more governmental and less commercial, and thinner reserves. Many of the downgrades were concentrated along the two coasts: California and the Pacific Northwest and New York and Pennsylvania. Many of the ratings were already in low or below investment grade categories.

Multi-notch downgrades continued in 2024, ranging from two to four notch movements in one rating action. One of the hospitals that experienced a four-notch downgrade subsequently defaulted on an interest payment (Jackson Hospital & Clinics, AL). Multi-notch upgrades reflected mergers into higher-rated systems, the largest being a seven-notch upgrade of a small, single-site hospital into a 19-hospital system in the Midwest.

Five hospitals experienced multiple rating actions in 2024, with rating committees convening not once but two and three times during the year. These were distressed credits whose financial performance and reserve levels dropped materially from quarter to quarter, a characteristic of high-yield or speculative rated borrowers.

While some of the upgrades followed mergers, other upgrades reflected improved financial performance and stable or growing liquidity. Likewise, some of the upgraded hospitals began receiving new supplemental funds known as Direct Payment Programs (DPPs). Unlike other supplemental funds, DPPs are subject to annual federal and state approval, making their long-term reliability uncertain. Numerous types of providers saw upgrades—including academic medical centers, independent hospitals and regional health systems—and were located across the U.S. Most of the upgraded hospitals (excluding those involved in mergers) were already investment grade.

As in past years, rating affirmations represented the overwhelming majority of rating actions in 2024. This is welcome news for the industry as many hospitals and health systems will turn to the bond market to borrow for their capital projects. Investors’ view of the industry should be bolstered by the change in industry outlooks. S&P moved to Stable from Negative and Fitch moved to Neutral from Deteriorating in December 2024, joining Moody’s revision to Stable from Negative in 2023.

We expect rating affirmations will again be the majority rating action in 2025. However, even with the stability viewed by the agencies, we expect downgrades to outpace upgrades given a growing reliance on government payers, labor challenges and a competitive environment. Policy and funding changes will also cast uncertainty into the mix in 2025 and may cause credit deterioration in future years.