Cartoon – Leadership Skills

As hospital leaders convene in Seattle this weekend for the American Hospital Association Leadership Summit, their future is uncertain.

Last week’s court decision in favor of hospitals shortchanged by the 340B drug program and 1st half 2023 improvement in operating margins notwithstanding, the deck is stacked against hospitals—some more than others. And they’re not alone: nursing homes and physician practices face the same storm clouds:

Most hospitals soldier on: they’re aware of these and responding as best they can. But most are necessarily focused only on the near-term: bed needs, workforce recruitment and staffing, procurement costs for drugs and supplies and so on. Some operate in markets less problematic than others, but the trends hold true directionally in every one of America’s 290 HRR markets.

Planning for the long-term is paralyzed by the tyranny of the urgent:

survival and sustainability in 2023 and making guarded bets about 2024 dominate today’s plans. That’s reality. Though the healthcare pie is forecast to get bigger, it’s being carved up by upstarts pursuing profitable niches and mega-players with deep pockets and a take-no-prisoners approach to their growth strategies. The result is an industry nearing meltdown.

Each traditional sector thinks it’s moral virtue more honorable than others. Each blames the other for avoidable waste and inaction in weeding out its bad actors. Each is pays lip service to “value-based care” and “system transformation” while doubling-down on making sure changes are incremental and painless for the near-term. And each believes the long-term destination of the system will be different than the past but no two agree on what that is.

Hospitals control 31% of the spend directly and as much as 43% with their employed physicians included. So, they’re a logical focus of attention from outsiders. Whether not for profit, public or investor owned, all are thought to be expensive and non-transparent and increasingly many are seen as ‘Big Business’ with excessive profits. Complaints about heavy-handed insurer reimbursement and price-gauging by drug companies fall on death ears in most communities. That’s why most are focused on near-term survival and few have the luxury or tools to plan for the future.

As a start, answers to the questions below in the 3-5 (mid-term) and 8–10-year (long-term) time frames is imperative for every hospital leadership team and Board:

For hospital leaders gathering in Seattle this week, and in local board meetings nationwide, necessary attention is being given the near-term issues all face. But longer-term issues lurk: the future does not appear a modernized version of the past for anyone in U.S. healthcare, especially hospitals. And among hospitals, fundamental precepts—like tax exemptions for “not-for-profit” hospitals, community benefits and charity care in exchange for tax exemption, EMTALA et al. regulations that require access without pre-condition are among many that will re-surface as the long-term view of the health system is re-considered.

To that end, the questions above deserve urgent discussion in every hospital board room and C suite. Trade-offs aren’t clear, potential future state hospital scenarios are not discreet and winners and losers unknown. But a fact-driven process recognizing a widening array of players with deep pockets and fresh approaches is necessary.

America’s hospitals have a $104 billion problem.

That’s the amount you arrive at if you multiply the number of physicians employed by hospitals and health systems (approximately 341,200 as of January 2022, according to data from the Physicians Advocacy Institute and Avalere) by the median $306,362 subsidy—or loss—reported in our Q1 2023 Physician Flash Report.

Subsidizing physician employment has been around for a long time and such subsidies were historically justified as a loss leader for improved clinical services, the potential for increased market share, and the strengthening of traditionally profitable services.

But I am pretty sure the industry did not have $104 billion in losses in mind when the physician employment model first became a key strategic element in the hospital operating model. However, the upward reset in expenses brought on by the pandemic and post-pandemic inflation has made many downstream hospital services that historically operated at a profit now operate at breakeven or even at a loss. The loss leader physician employment model obviously no longer works when it mostly leads to more losses.

This model is clearly broken and in demand of a near-term fix. Perhaps the critical question then is how to begin? How to reconsider physician employment within the hospital operating plan?

Out of the box, rethink the physician productivity model. Our most recent Physician Flash Report data shows that for surgical specialties, there was a median $77 net patient revenue per provider wRVU. For the same specialties, there was a median $80 provider paid compensation per provider wRVU. In other words, before any other expenses are factored in, these specialties are losing $3 per wRVU on paid compensation alone. Getting providers to produce more wRVUs only makes the loss bigger.

It’s the classic business school 101 problem.

If a factory is losing $5 on every widget it produces, the answer is not to produce more widgets. Rather, expenses need to come down, whether that is through a readjustment of compensation, new compensation models that reward efficiency, or the more effective use of advanced practice providers.

Second, a number of hospital CEOs have suggested to me that the current employed physician model is quite past its prime. That model was built for a system of care that included generally higher revenues, more inpatient care, and a greater proportion of surgical vs. medical admissions. But overall, these trends were changing and then were accelerated by the Covid pandemic. Inpatient revenue has been flat to down. More clinical work continues to shift to the outpatient setting and, at least for the time being, medical admissions have been more prominent than before the pandemic.

Taking all this into account suggests that in many places the employed physician organizational and operating model is entirely out of balance. One would offer the calculated guess that there are too many coaches on the team and not enough players on the field. This administrative overhead was seemingly justified in a different loss leader environment but now it is a major contributor to that $104 billion industry-wide loss previously calculated.

Finally, perhaps the very idea of physician employment needs to be rethought.

My colleagues Matthew Bates and John Anderson have commented that the “owner” model is more appealing to physicians who remain independent then the “renter” model. The current employment model offers physicians stability of practice and income but appears to come at the cost of both a loss of enthusiasm and lost entrepreneurship. The massive losses currently experienced strongly suggest that new models are essential to reclaim physician interest and establish physician incentives that result in lower practice expenses, higher practice revenues, and steadily reduced overall subsidies.

Please see this blog as an extension of my last blog, “America’s Hospitals Need a Makeover.” It should be obvious that by analogy we are not talking about a coat of paint here or even new appliances in the kitchen.

The financial performance of America’s hospitals has exposed real structural flaws in the healthcare house. A makeover of this magnitude is going to require a few prerequisites:

The basic rule of home renovation applies here as well: the longer the fix to this problem is delayed the harder and more expensive the project becomes. The losses set out here certainly suggest that physician employment is a significant contributing factor to hospitals’ current financial problems overall. It would be an understatement to say that the time to get after all of this is right now.

https://mailchi.mp/7f59f737680b/the-weekly-gist-june-30-2023?e=d1e747d2d8

The New York Times Magazine published an encouraging piece about the impressive series of recent medical breakthroughs, many of which have been in the works for decades.

Challenging the conventional wisdom that disruptive scientific breakthroughs have slowed over time, the article points out that the last five years of medicine have featured the rollout of mRNA vaccines, the first instance of a person receiving CRISPR gene therapy, and development of next-generation cancer treatment and weight-loss drugs.

The Gist: The expanding innovation pipeline not only brings excitement and optimism for patients and physicians, but also has the potential to dramatically impact long-established care delivery pathways.

Case in point: used at scale, new weight loss drugs could curb obesity-related chronic diseases and joint replacements—while possibly increasing the incidence of Alzheimer’s disease and cancer as more people live longer lives.

Providers planning for facility and other long-term investments must think through scenarios about how these early, but very promising, innovations could alter demand and shift care delivery needs over coming decades.

https://mailchi.mp/7f59f737680b/the-weekly-gist-june-30-2023?e=d1e747d2d8

At a recent board meeting, the discussion turned to what Millennial consumers want from healthcare. The system COO put the administrative coordinator, the sole Millennial in the room, on the spot to speak for the preferences of an entire generation.

Nearly every health system we work with is debating how to engage Millennial consumers or understand Millennial (and now Gen Z) employees—perhaps an even more pressing need, given that Millennials now outnumber Baby Boomers in the healthcare workforce. But having a real, live Millennial participating in a health system board meeting is a rarity.

Most often we rely on secondhand information, either from studies analyzing their behavior, or Boomer board members’ personal experiences as the parents of Millennials. When we suggested that systems are at a disadvantage in not having Millennial board members, the system CEO agreed, and said they had tried—and failed—to recruit younger members.

It was largely a question of availability. Family commitments were one challenge, but the greatest obstacle was committing to days away from work. Younger executives and community leaders are in the “high-growth” stage of their careers, and rarely in control of their own schedules, making the commitment to a (typically unpaid) board seat difficult.

As boards push for more diversity among members, recruiting younger directors is a critical component. Even if systems aren’t ready to reshape the director role for Millennials, they must find a way to directly engage younger leaders and integrate them into decision-making at all levels of the organization.

https://mailchi.mp/7f59f737680b/the-weekly-gist-june-30-2023?e=d1e747d2d8

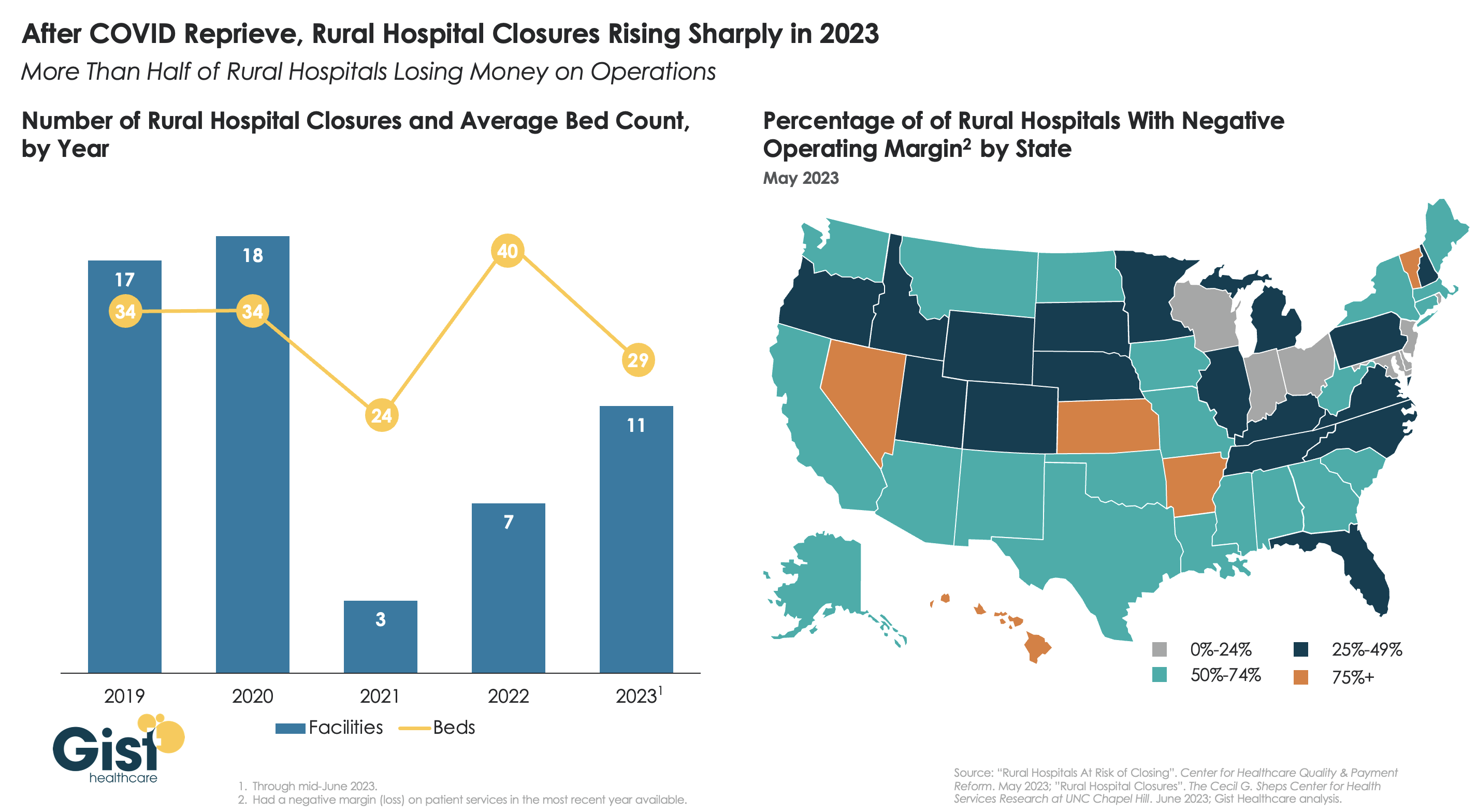

After a brief reprieve thanks to COVID relief funds, rural hospital closures are once again on the rise, with 11 facilities already closing in the first half of this year.

More rural facilities have already closed in 2023 than the previous two years combined, and this year is on pace to be the second-highest number of rural hospital beds lost since 2005.

And the majority of rural hospitals that haven’t closed are experiencing negative operating margins, with almost one in three at immediate or high risk of closure due to declining volumes, shifting payer mix, and increased labor and supply costs.

Leaders at rural hospitals now face difficult decisions including drastically cutting services, merging with a larger system, or closing their doors altogether. The Centers for Medicare and Medicaid Services (CMS) launched the Rural Emergency Hospital Program recently, designed to financially support small rural hospitals that convert to providing emergency services only, but so far program uptake has been limited.

While efforts to prop up hospitals will help to sustain access to care in the near term, rural communities ultimately need a new model for care, with reimagined facilities, supported by enhanced virtual connections to specialists and higher-acuity services.

https://mailchi.mp/7f59f737680b/the-weekly-gist-june-30-2023?e=d1e747d2d8

On July 1st, Georgia will launch its Pathways to Coverage program, which partially expands its Medicaid program to enroll individuals with incomes up to 100 percent of the federal poverty line (FPL), but only if they demonstrate at least 80 hours a month of work, education, job training, or community service.

This expansion is only projected to extend Medicaid coverage to an additional 50K state residents, far short of the 400K that full Medicaid expansion (without work requirements, to individuals earning up to138 percent of the FPL) would have covered. Georgia’s plan was approved by the Trump administration in 2020, but the Biden administration rescinded its waiver prior to implementation. Georgia then sued the Biden administration, and a Federal District Court sided with the state, allowing the partial expansion with work requirements to proceed. The Biden administration chose not to appeal.

The Gist: Though Georgia’s implementation is more limited in scope compared with other states which are currently pursuing Medicaid work requirements, Georgia sets a precedent to motivate those states that are looking to pursue similar strategies.

Research has shown that most adults on Medicaid who do not face barriers to work are already working, and that the cost of systems to monitor beneficiary work status likely offsets any savings in reduced Medicaid spending.

The burden of having to report work status is onerous for potential Medicaid enrollees, discouraging some from seeking coverage altogether.