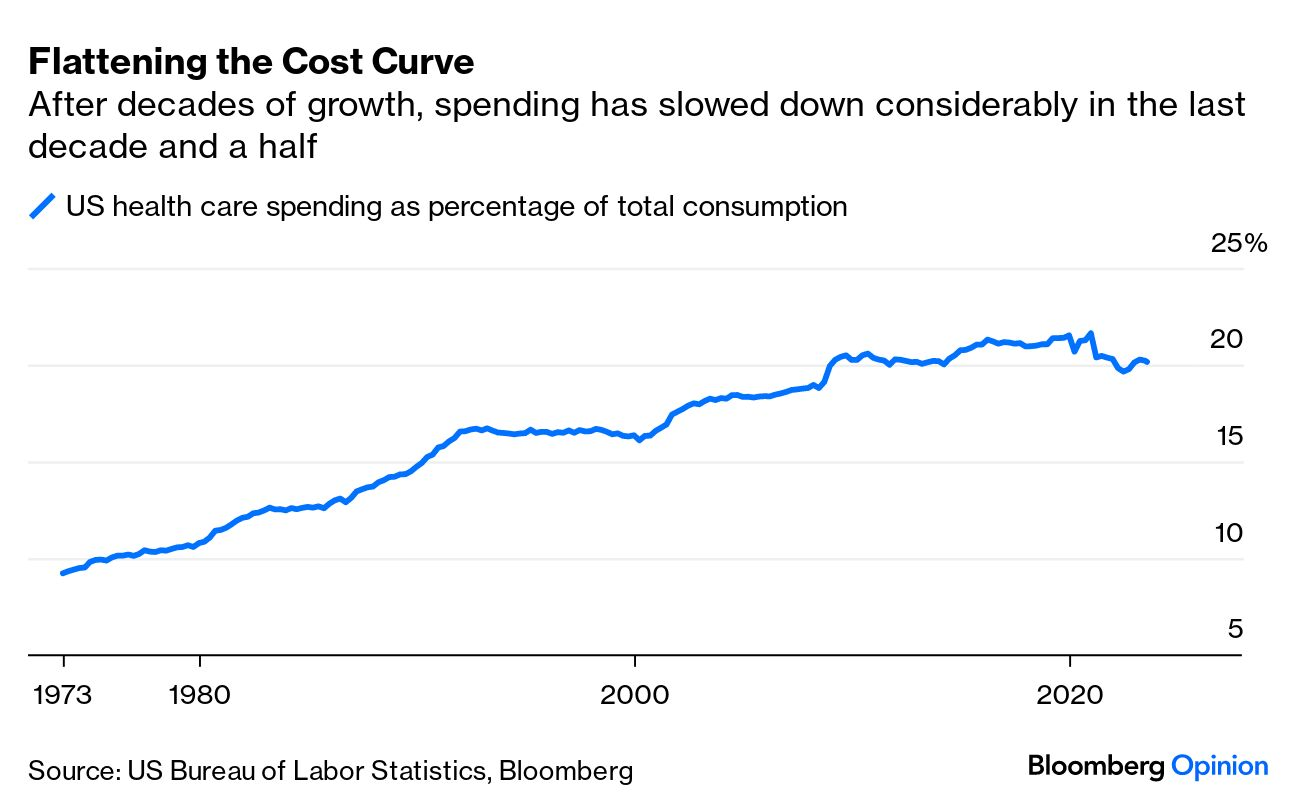

A piece published this week in the New York Times documents how Medicare spending per beneficiary has flattened since the early 2010s, coming in below projections by nearly $4T.

While the authors run through possible explanations, including changes made by the Affordable Care Act and to the Medicare Advantage program, the proliferation of effective cholesterol and blood-pressure medications, and fewer breakthroughs in new, expensive drug classes, they acknowledge that scholars have not reached a consensus on the primary drivers of this trend.

Beyond academic debate, there is also no agreement on how long the flattened spending pattern will hold—or what factors might reignite rapid cost growth.

The Gist:

Whatever the causes of this phenomenon, it has helped avert the kind of Medicare austerity measures that dominated political debates on the program in past decades.

We assume some of this flattening has to do with the fact that the average age of Medicare beneficiaries has dropped as Baby Boomers have entered the program in droves, given that younger beneficiaries are much less costly to insure.

In coming decades, the average age of Medicare beneficiaries will increase, along with their care costs, and the total number of Medicare beneficiaries will continue to rise.

By 2053, seniors will make up over 22 percent of the population and over 40 percent of the projected federal budget will be spent on programs for them.

Companies are avoiding hard layoffs but still cutting jobs by reassigning employees to different roles — a trend dubbed “quiet cutting,”The Wall Street Journal reported Aug. 27.

From August 2022 to August 2023, mentions of “reassignment” or similar phrasing during company earnings calls more than tripled, according to data from financial research platform Alphasense. Companies that have embraced large-scale reassignments include Adidas, IBM, Adobe and Salesforce. In healthcare, at least 20 health systems have announced changes to executive ranks and leadership teams this year.

“Reassigning is definitely a huge part of the dynamic right now,” Andy Challenger, senior vice president at executive coaching firm Challenger, Gray & Christmas told the Journal.

Reassignments can be a strategic way for companies to cut costs by placing top talent — that they previously spent significant amounts of money on to recruit — in new roles that are better suited to help them meet future organizational goals. In many cases, reassignments could be a way for companies to avoid letting people go. On the other hand, it could be a soft nudge to get employees to quit, executive coaches and advisers told the Journal.

“They could be putting you out to pasture,” said Roberta Matuson, executive coach and adviser on human resources matters to businesses such as General Motors and Microsoft.

For employees to gauge whether a reassignment is a genuine move to avoid letting them go or a subtle push out the door, experts said they should consider whether the reassigned role is far below the pay and experience level of their original job, and whether the reassignment requires a big move when their employer knows relocation is not a realistic option, according to the Journal.

Albert Einstein determined that time is relative. And when it comes to healthcare, five years can be both a long and a short amount of time.

In August 2018, I launched the Fixing Healthcare podcast. At the time, the medium felt like the perfect auditory companion to the books and articles I’d been writing. By bringing on world-renowned guests and engaging in difficult but meaningful discussions, I hoped the show would have a positive impact on American medicine. After five years and 100 episodes, now is an opportune time to look back and examine how healthcare has improved and in what ways American medicine has become more problematic.

Here’s a look at the good, the bad and the ugly since episode one of Fixing Healthcare:

The Good

Drug breakthroughs and government actions headline medicine’s biggest wins over the past five years.

At first, health experts expressed doubts that Pfizer, Moderna and others could create a safe and effective Covid-19 vaccine with messenger RNA (mRNA) technology. After all, no one had succeeded in more than two decades of trying.

Thanks in part to Operation Warp Speed, the government-funded springboard for research, our nation produced multiple vaccines within less than a year. Previously, the quickest vaccine took four years to develop (mumps). All others required a minimum of five years.

The vaccines were pivotal in ending the coronavirus pandemic, and their success has opened the door to other life-saving drugs, including those that might prevent or fight cancer. And, of course, our world is now better prepared for when the next viral pandemic strikes.

Weight-Loss Drugs

Originally designed to help patients manage Type 2 diabetes, drugs like Ozempic have been helping people reverse obesity—a condition closely correlated with diabetes, heart disease and cancer.

For decades, America’s $150 billion a year diet industry has failed to curb the nation’s continued weight gain. So too have calls for increased exercise and proper nutrition, including restrictions on sugary sodas and fast foods.

In contrast, these GLP-1 medications are highly effective. They help overweight and obese people lose 15 to 25 pounds on average with side effects that are manageable for nearly all users.

The biggest stumbling block to their widespread use is the drug’s exorbitant price (upwards of $16,000 for a year’s supply).

Drug-Pricing Laws

With the Inflation Reduction Act of 2022, Congress took meaningful action to lower drug prices, a move the CBO estimates would reduce the federal deficit by $237 billion over 10 years.

It’s a good start. Americans today pay twice as much for the same medications as people in Europe largely because of Congressional legislation passed in 2003.

That law, the Medicare Prescription Drug Price Negotiation Act, made it illegal for Health and Human Services (HHS) to negotiate drug prices with manufacturers—even for the individuals publicly insured through Medicare and Medicaid.

Now, under provisions of the new Inflation Reduction Act, the government will be able to negotiate the prices of 10 widely prescribed medications based on how much Medicare’s Part D program spends. The lineup is expected to include prescription treatments for arthritis, cancer, asthma and cardiovascular disease. Unfortunately, the program won’t take effect until 2026. And as of now, several legal challenges from both drug manufacturers and the U.S. Chamber of Commerce are pending.

The Bad

Spiking costs, ongoing racial inequalities and millions of Americans without health insurance make up three disappointing healthcare failures of the past five years.

Cost And Quality

The U.S. spends nearly twice as much on healthcare per citizen as other countries, yet our nation lags 10 of the wealthiest countries in medical performance and clinical outcomes. As a result, Americans die younger and experience more complications from chronic diseases than people in peer nations.

As prices climb ever-higher, at least half of Americans can’t afford to pay their out-of-pocket medical bills, which remain the leading cause of U.S. bankruptcy. And with rising insurance premiums alongside growing out-of-pocket expenses, more people are delaying their medical care and rationing their medications, including life-essential drugs like insulin. This creates a vicious cycle that will likely prolong today’s healthcare problems well into the future.

Health Disparities

Inequalities in American medicine persist along racial lines—despite action-oriented words from health officials that date back decades.

Today, patients in minority populations receive unequal and inequitable medical treatment when compared to white patients. That’s true even when adjusting for differences in geography, insurance status and socioeconomics.

Racism in medical care has been well-documented throughout history. But the early days of the Covid-19 pandemic provided several recent and deadly examples. From testing to treatment, Black and Latino patients received both poorer quality and less medical care, doubling and even tripling their chances of dying from the disease.

The problems can be observed across the medical spectrum. Studies show Black women are still less likely to be offered breast reconstruction after mastectomy than white women. Research also finds that Black patients are 40% less likely to receive pain medication after surgery. Although technology could have helped to mitigate health disparities, our nation’s unwillingness to acknowledge the severity of the problem has made the problem worse.

Uninsurance

Although there are now more than 90 million Americans enrolled in Medicaid, there are still 30 million people without any health insurance. This disturbing reality comes a full decade after the passage of the Affordable Care Act.

On Capitol Hill, there is no plan in place to reduce the number of uninsured.

Moreover, many states are looking to significantly rollback their Medicaid enrollment in the post-Covid era. Kaiser Family Foundation estimates that between 8 million and 24 million people will lose Medicaid coverage during the unwinding of the continuous enrollment provisions implemented during the pandemic. Without coverage, people have a harder time obtaining the preventive services they need and, as a result, they suffer more chronic diseases and die younger.

The Ugly

An overall decrease in longevity, along with higher maternal mortality and a worsening mental-health crisis, comprise the greatest failures of U.S. healthcare over the past five years.

Life Expectancy

Despite radical advances in medical science over the past five years, American life expectancy is back to where it was at the turn of the 20th century, according to CDC data.

Alongside environmental and social factors are a number of medical causes for the nation’s dip in longevity. Research demonstrated that many of the 1 million-plus Covid-19 deaths were preventable. So, too, was the nation’s rise in opioid deaths and teen suicides.

Regardless of exact causation, Americans are living two years less on average than when we started the Fixing Healthcare podcast five years ago.

Maternal Mortality

Compared to peer nations, the United States is the only country with a growing rate of mothers dying from childbirth. The U.S. experiences 17.4 maternal deaths per 100,000 live births. In contrast, Norway is at 1.8 and the Netherlands at 3.0.

The risk of dying during delivery or in the post-partum period is dramatically higher for Black women in the United States. Even when controlling for economic factors, Black mothers still suffer twice as many deaths from childbirth as white women.

And with growing restrictions on a woman’s right to choose, the maternal mortality rate will likely continue to rise in the United States going forward.

Mental Health

Finally, the mental health of our country is in decline with rates of anxiety, depression and suicide on the rise.

These problems were bad prior to Covid-19, but years of isolation and social distancing only aggravated the problem. Suicide is now a leading cause of death for teenagers. Now, more than 1 in every 1,000 youths take their own lives each year. The newest data show that suicides across the U.S. have reached an all-time high and now exceed homicides.

Even with the expanded use of telemedicine, mental health in our nation is likely to become worse as Americans struggle to access and afford the services they require.

The Future

In looking at the three lists, I’m reminded of a baseball slugger who can occasionally hit awe-inspiring home runs but strikes out most of the time. The crowd may love the big hitter and celebrate the long ball, but in both baseball and healthcare, failing at the basics consistently results in more losses than wins.

Over the past five years, American medicine has produced a losing record. New drugs and surgical breakthroughs have made headlines, but the deeper, more systemic failures of American healthcare have rarely penetrated the news cycle.

If our nation wants to make the next five years better and healthier than the last five, elected officials and healthcare leaders will need to make major improvements. The steps required to do so will be the focus of my next article.

Generative AI applications can already help health systems improve margins, yet only 6% have a strategy ready.

At a Glance

In the wake of their most challenging financial year since 2020, US hospitals are desperately searching for margin improvements.

Generative AI can increase productivity and cost efficiency, but only 6% of health systems currently have a strategy.

Leading providers and payers will start with highly focused, low-risk generative AI use cases, generating the funds and experience for more transformative future applications.

While Covid-19 may no longer be dominating the global news cycle, healthcare providers and payers are still feeling its reverberations. More than half of US hospitals ended 2022 with a negative margin, marking the most difficult financial year since the start of the pandemic.

CEOs and CFOs remember the challenges all too well: The Omicron surge halted nonurgent procedures in the first half of the year, government support tapered off, and labor expenses ballooned amid staffing shortages. There was also the record-high inflation that continues to intensify margin pressures today. According to a recent Bain survey of health system executives, 60% cite rising costs as their greatest concern.

Payers and providers are now on the hunt for margin improvements. In our experience, the most successful companies won’t merely reduce costs, but also ramp up productivity. When done right, modest technology investments can accomplish both.

Artificial intelligence (AI) may hold part of the answer. With the costs to train a system down 1,000-fold since 2017, AI provides an arsenal of new productivity-enhancing tools at a low investment.

Many executives recognize the growing opportunity, especially with the recent rise of generative AI, which uses sophisticated large language models (LLMs) to create original text, images, and other content. It’s inspiring an explosion of ideas around use cases, from reviewing medical records for accuracy to making diagnoses and treatment recommendations.

Our survey reveals that 75% of health system executives believe generative AI has reached a turning point in its ability to reshape the industry. However, only 6% have an established generative AI strategy.

It’s time to play offense—or be forced to play defense later. But choosing from the laundry list of generative AI applications is daunting. Companies are at high risk of overinvesting in the wrong opportunities and underinvesting in the right ones, undermining future profitability, growth, and value creation. A wait-and-see approach is a tempting prospect.

However, we believe the next generation of leading healthcare companies will start today, with highly focused, low-risk use cases that boost productivity and cost efficiency. Over the next three to nine months, these companies will improve margins and learn how to implement a generative AI strategy, building up the funds and experience needed to invest in a more transformative vision.

Endless potential—and high hurdles

The excitement around generative AI may feel akin to the hype around other recent digital and technology developments that never quite rose to their promised potential. Well-intentioned, well-informed individuals are debating how much change will truly materialize in the next few years. While developments over the past six months have been a testament to the breakneck speed of change, nobody can accurately predict what the next six months, year, or decade will look like. Will new players emerge? Will we rely on different LLMs for different use cases, or will one dominate the landscape?

Despite the uncertainty, generative AI already has the power to alleviate some of providers’ biggest woes, which include rising costs and high inflation, clinician shortages, and physician burnout. Quick relief is critical, considering that the heightened risk of a recession will only compound margin pressures, and the US could be short 40,800 to 104,900 physicians by 2030, according to the Association of American Medical Colleges.

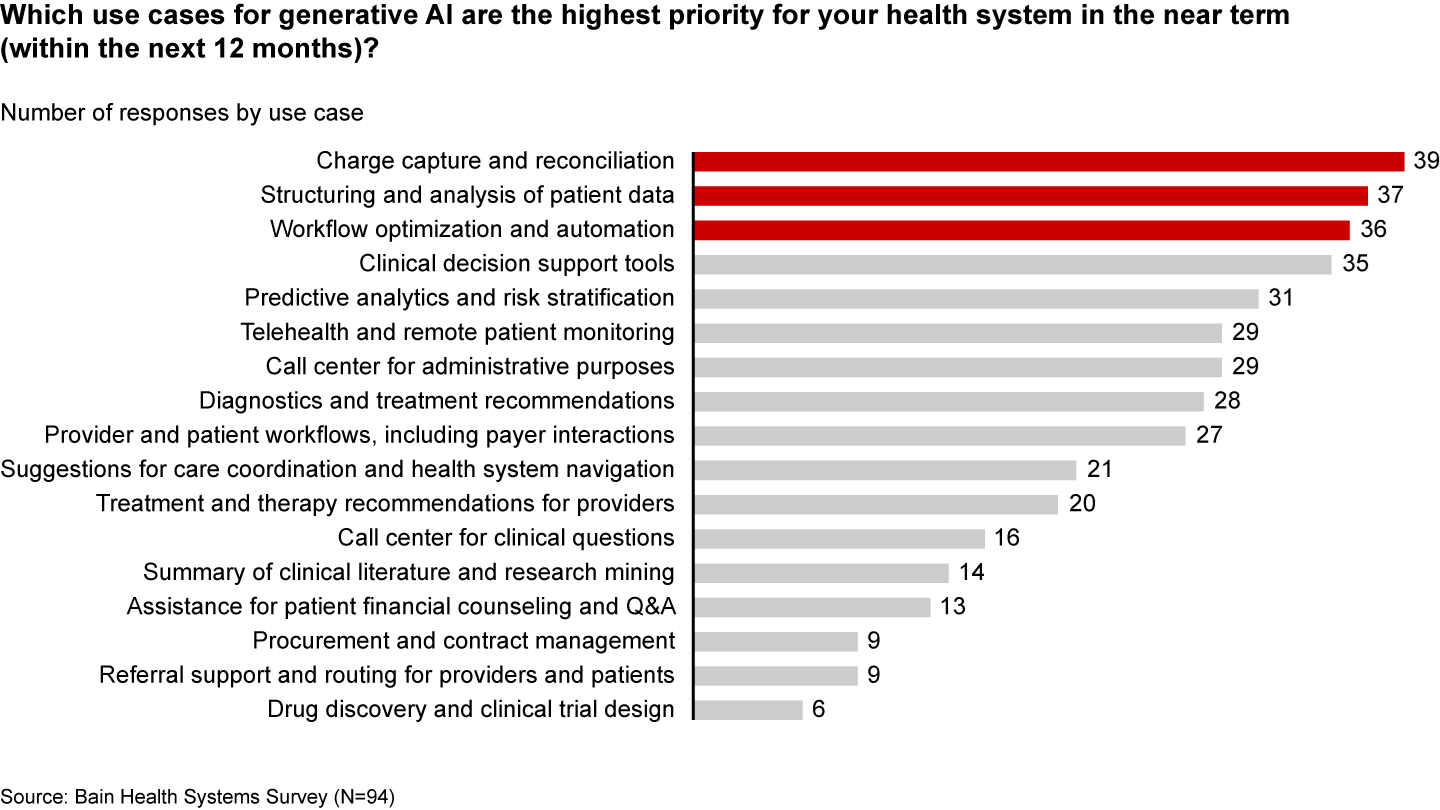

Many health systems are eyeing imminent opportunities to reduce administrative burdens and enhance operational efficiency. They rank improving clinical documentation, structuring and analyzing patient data, and optimizing workflows as their top three priorities (see Figure 1).

Figure 1

In the near term, generative AI can reduce administrative burdens and enhance efficiency

Some generative AI applications are already streamlining administrative tasks and allowing thinly stretched physicians to spend more time with patients. For instance, Doximity is rolling out a ChatGPT tool that can draft preauthorization and appeal letters. HCA Healthcare partnered with Parlance, a conversational AI-based switchboard, to improve its call center experience while reducing operators’ workload. And there are new announcements seemingly every week: Consider how healthcare software company Epic Systems is incorporating ChatGPT with electronic health records (EHRs) to draft response messages to patients, or how Google Cloud is launching an AI-enabled Claims Acceleration Suite for prior authorization processing.

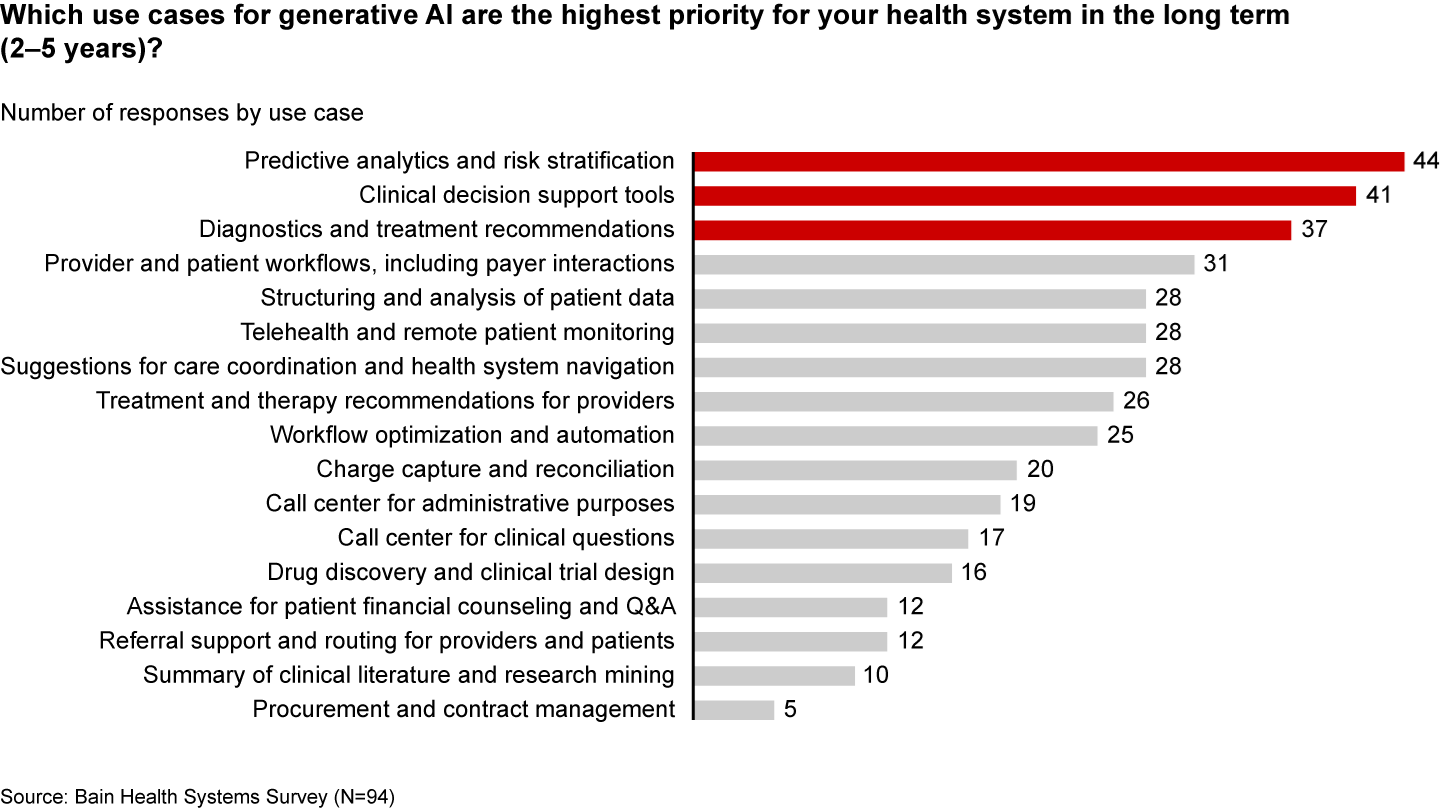

These applications only scratch the surface of potential. In the future, generative AI could profoundly transform care delivery and patient outcomes. Looking ahead two to five years, executives are most interested in predictive analytics, clinical decision support, and treatment recommendations (see Figure 2).

Figure 2

Predictive analytics, clinical decisions, and care recommendations are long-term generative AI priorities

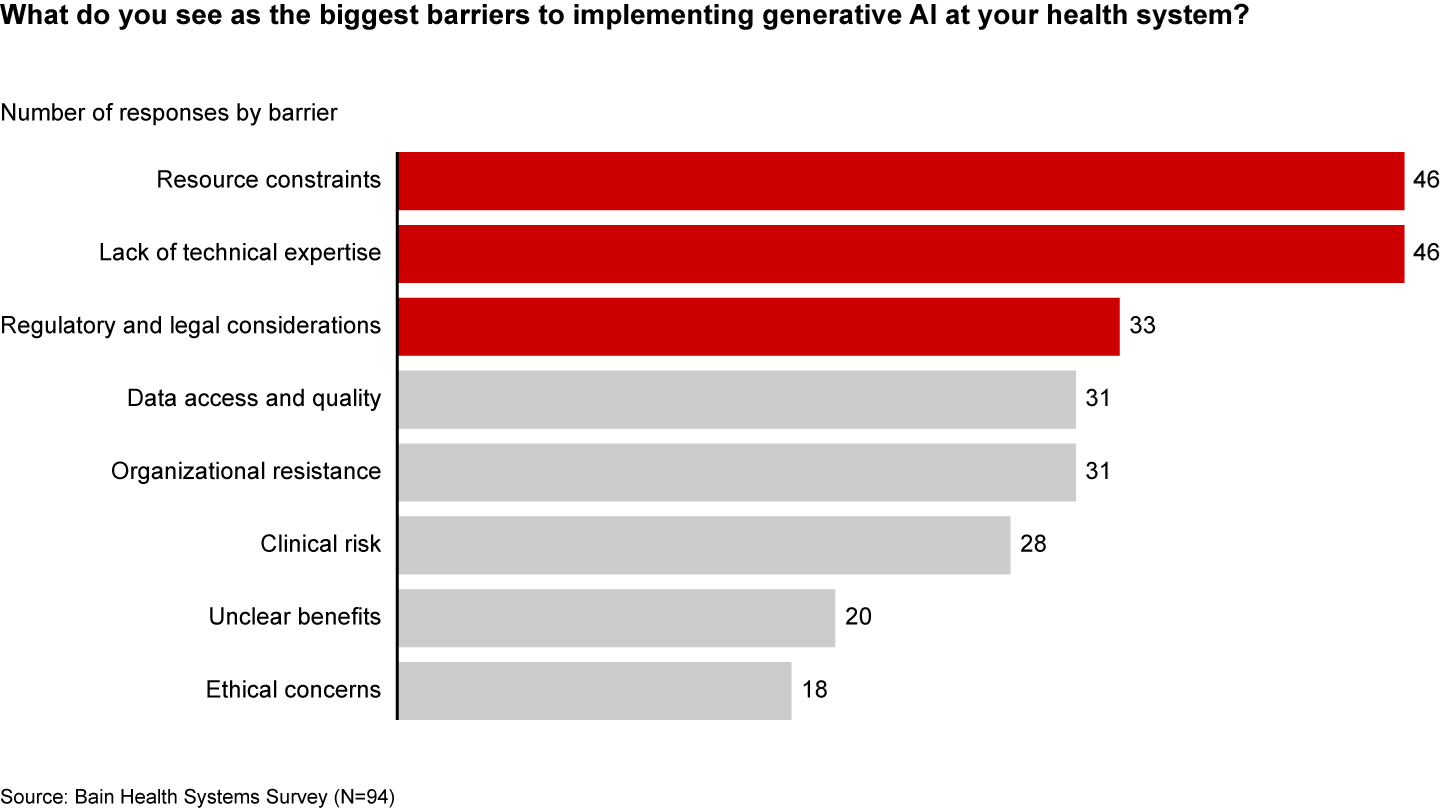

It’s hard not to catch AI “fever.” But there are real challenges ahead. Some are already tackling the biggest questions: Organizations such as Duke Health, Stanford Medicine, Google, and Microsoft have formed the Coalition for Health AI to create guidelines for responsible AI systems. Even so, solutions to the greatest hurdles aren’t yet keeping up with the rapid technology development.

Resource and cost constraints, a lack of expertise, and regulatory and legal considerations are the largest barriers to implementing generative AI, according to executives (see Figure 3).

Figure 3

A lack of resources, expertise, and regulation are the biggest barriers to generative AI in healthcare

Even when organizations can overcome these hurdles, one major challenge remains: focus and prioritization. In many boardrooms, executives are debating overwhelming lists of potential generative AI investments, only to deem them incomplete or outdated given the dizzying pace of innovation. These protracted debates are a waste of precious organizational energy—and time.

Starting small to win big

Setting the bar too high is setting up for failure. It’s easy to get caught up, betting big on what seems like the greatest opportunity in the moment. But 12 months later, leaders often find themselves frustrated that they haven’t seen results or feeling as if they’ve made a misplaced bet. Momentum and investments slow, further hindering progress.

Leading companies are forming a more pragmatic strategy that considers current capabilities, regulations, and barriers to adoption. Their CEOs and CFOs work together to enforce four guiding principles:

Pilot low-risk applications with a narrow focus first. Tomorrow’s leaders are making no-regret moves to deliver savings and productivity enhancements in short order—at a time when they need it most. Gaining experience with currently available technology, they are testing and learning their way to minimum viable products in low-risk, repeatable use cases. These quick wins are typically in areas where they already have the right data, can create tight guardrails, and see a strong potential return on investment. Some, like call center and chatbot support, can improve the patient experience. However, given the current challenges around regulation and compliance, the most successful early initiatives are likely to be internally focused, such as billing or scheduling. Most importantly, executives prioritize initiatives by potential savings, value, and cost.

Decide to buy, partner, or build. CEOs will need to think about how to invest in different use cases based on availability of third-party technology and importance of the initiative.

Funnel cost savings and experience into bigger bets. As the technology matures and the value becomes clear, companies that generate savings, accumulate experience, and build organizational buy-in today will be best positioned for the next wave of more sophisticated, transformative use cases. These include higher-risk clinical activities with a greater need for accuracy due to ethical and regulatory considerations, such as clinical decision support, as well as administrative activities that require third-party integration, such as prior authorization.

Remember generative AI isn’t a strategy unto itself. To build a true competitive advantage, top CEOs and CFOs are selective and discerning, ensuring that every generative AI initiative reinforces and enables their overarching goals.

Some health systems are already seeing powerful results from relatively small, more practical investments. For instance, recognizing that clinicians were spending an extra 130 minutes per day outside of working hours on administrative tasks, the University of Kansas Health System partnered with Abridge, a generative AI platform, to reduce documentation burden. By summarizing the most important points from provider-patient conversations, Abridge is improving the quality and consistency of documentation, getting more patients in the door, and cutting down on pervasive physician burnout.

Although it will require some upfront investment, in the long run it will be more costly to underestimate the level and speed at which generative AI will transform healthcare. The next generation of leaders will start testing, learning, and saving today, putting them on a path to eventually revolutionize their businesses.

This annual look at high-impact trends affecting healthcare in the coming year is based on evaluation of current industry research data. Healthcare Finance Trendsfor2023 (Trends) explores eight themes identified by CommerceHealthcare® ranging across four areas:

Financial. Providers enter the year contending with multiple financial stress points. They will also seek growth in technology-enabled remote care.

Patient financial experience. The need to drive not only improvement but also personalization of the financial experience is paramount. A central role will be played by patient financing programs which will see growing demand in 2023.

Trust. Building trust with all constituencies is explored as a linchpin for long-term provider success. The latest findings on cybersecurity show that this contributor to trust will continue to consume leadership attention.

Digital transformation. Pursuit of digital-first operations is accelerating, with the finance area an important focus. Emerging payment modes are finding a home in healthcare’s digital finance landscape.

This report’s consistent message is that these trends intersect in ways that compound both the challenges and the upside potential of strategies that address them.

1. Multiple Financial Stress Points Will Constrain Options

Healthcare’s financial predicament for the next 12–18 months is being described in strong terms. Citing $450 billion of EBITDA that could be in jeopardy, more than half of the industry’s project profit pool by 2027, one analyst suggests “a gathering storm.” Another perceives “broad and serious threats” as “elevated expenses” erode margins and exact “a profound financial toll.” Fitch Ratings issued a “deteriorating” outlook for nonprofit health systems.

These financial headwinds are upending healthcare’s traditional status as “recession-proof.” It is helpful to probe the multiple forces in play, the urgent workforce management challenge, and the varied solution set.

Multiple stress factors at work

Observing that margins will be down 37% in 2022 relative to pre-pandemic, a recent stark assessment concluded, “U.S. hospitals are likely to face billions of dollars in losses — which would result in the most difficult year for hospitals and health systems since the beginning of the pandemic.”

A confluence of factors is exacerbating the stress for 2023:

Rising acuity levels. Over two-thirds of surveyed C-suite executives said patient health has worsened from pandemic-induced delayed care. The upshot, stated by 27% of CFOs, is rising expenses due to higher acuity. Inpatient days are projected to increase at an 8% rate over the coming decade.

Reimbursement gaps and inflation. Commercial and government reimbursement rates are not keeping pace with rising costs. Surging inflation is widening this gap. Hospitals are also reporting substantial insurer payment delays and denials.

Investment declines. Stock and bond market declines have removed a cushion for operating weakness. Market uncertainty will complicate 2023 portfolio management.

Persistent workforce concerns remain center stage

Burnout and shortages have disrupted the clinical workforce. Nearly 60% of physician, advanced practice provider and nurse survey respondents said their teams are not adequately staffed, and 40% lack resources to operate at full potential. Many providers face extreme to moderate shortages of allied health professionals.

The problem extends beyond the clinical. A survey saw 48% of respondents experiencing severe labor deficiencies in revenue cycle management (RCM) and billing, and one in four finance leaders must fill over 20 positions to be fully staffed.

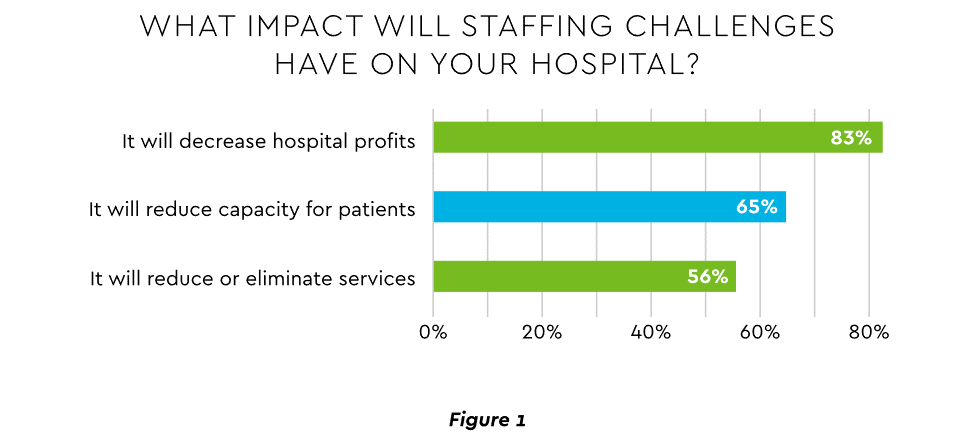

An executive outlook highlighted demonstrable impact on financial performance and growth from these workforce problems, citing reductions in profitability, capacity and service (Figure 1).1

Expenses. Hospital employee expense is expected to increase $57 billion from 2021 to 2022, with contract labor ballooning another $29 billion. Average weekly earnings are up 21.1% since early 2022. Half of medical practices budgeted higher staff cost-of-living increases in 2022. Shortages plague post-acute facilities as well. Their reduced capability to accept discharged patients is lengthening many hospitals’ patient stays.

Capacity constraint. Two-thirds of healthcare leaders identify “ability to meet demand” as their top workforce concern, suggesting a “looming capacity gap between future demand and labor supply.”

Range of measures being deployed

Health systems, hospitals and practices will vigorously pursue at least four direct actions to overcome the financial and staffing hurdles:

Cost cutting. Expense control will be paramount and “hospitals will be forced to take aggressive cost-cutting measures.” McKinsey estimates total industry administrative savings of $1 trillion through multiple aggressive changes.

Service line rationalization. Providers are rethinking how they deliver services to optimize efficiency. One path is utilizing “lower level” healthcare professionals in ways that free RNs and LPAs for more complex work suited to their top skills. Integrating remote care into the mix is another core element of the strategy.

Recruitment and retention programs. Attracting and retaining talent is crucial. Compensation is one avenue. Over two-thirds of organizations are offering signing bonuses for allied health professionals. Some are instituting value-based payments for physicians, offering salary floors to protect from drops in patient volume. CFOs and CNOs are joining forces to invest in nurse retention strategies.

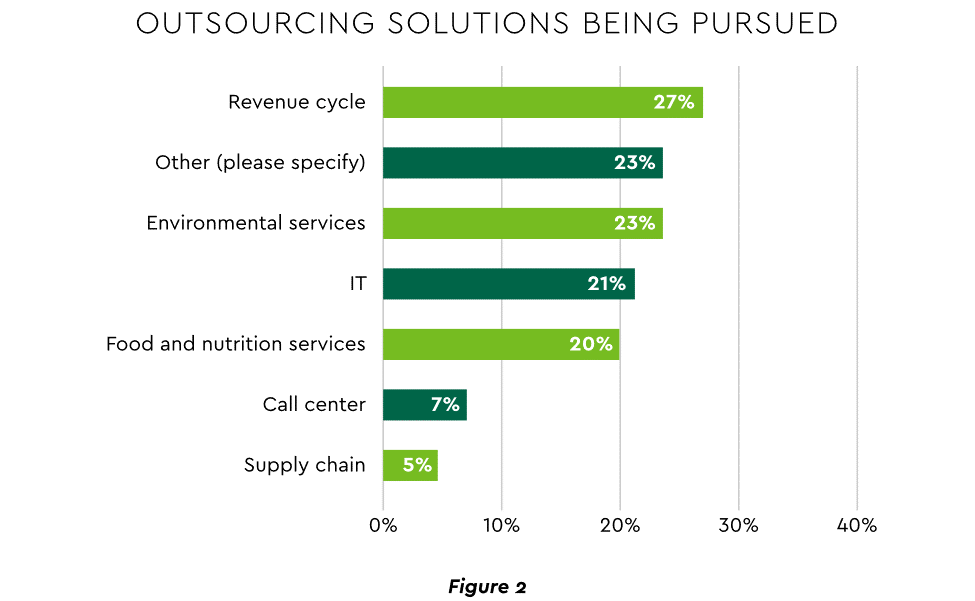

Staffing management. An increasingly popular tool to reduce labor cost and optimize staff resources is outsourcing. Figure 2 shows that RCM is leading the way among those using the solution.

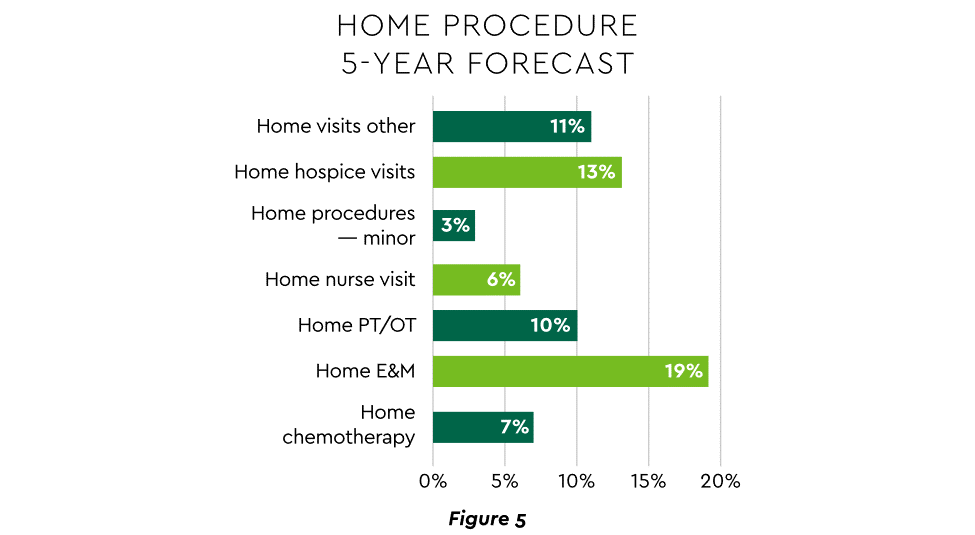

2. Growth Strategies Favor Outpatient, Virtual, Acute Home Care

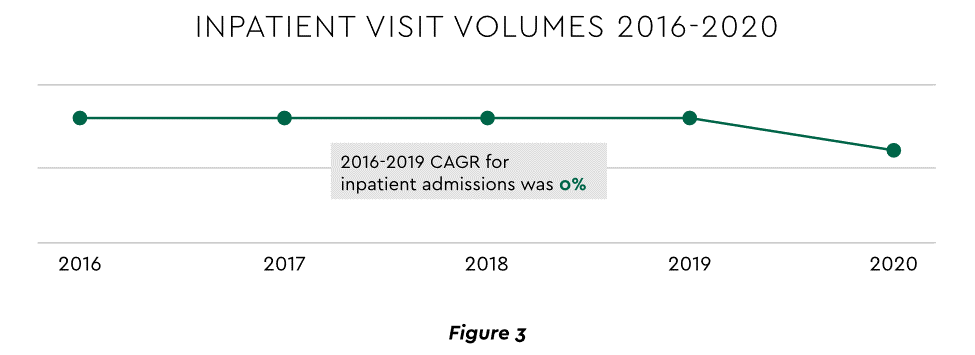

Pursuing top line growth in tandem with reining in expenses is essential. Inpatient volume growth has been tepid for several years ─ essentially flat in the 2016–20 period (Figure 3).

Leaders have been pivoting to outpatient and virtual care to diversify revenue streams. Two high-potential 2023 growth tracks in this sector merit deeper assessment.

Telehealth

Considerable evidence attests to strong commitment to telehealth and remote care. Sixty-three percent of physicians worldwide expect most consultations to be performed remotely within 10 years. Approximately 40% of health centers are using remote patient monitoring today. Consumers are also positive: 94% definitely or probably will use telehealth again, 57% prefer it for regular mental health visits and 61% use it for convenient care.

Telehealth is still in early stages of maturity. Only 4% of surveyed top executives consider their organization proficient at implementing remote care. Healthcare is also recognizing that a full telehealth ecosystem must be constructed. A physician leader explained that the industry’s early telehealth incarnations failed to build “virtual-only environments or really drive e-consults as a way of doing things.” A vital ecosystem demands alterations to current contracts, coding, collections, patient financing, staff training and other business practices.

Hospital-at-Home (HaH)

Health systems see particularly promising growth in the provision of acute care in patients’ home settings, including post-surgical and cancer treatment. The federal government has already allowed waivers to 114 systems and 256 hospitals to obtain inpatient-level reimbursement for acute care at home. However, these waivers were prompted by the pandemic and are slated to end in early 2023. The renewal uncertainty has stymied some activity and represents an overhang on the opportunity. However, enthusiasm appears strong, and 33% of hospitals in a recent poll said they would be prone to continue HaH even without renewal.

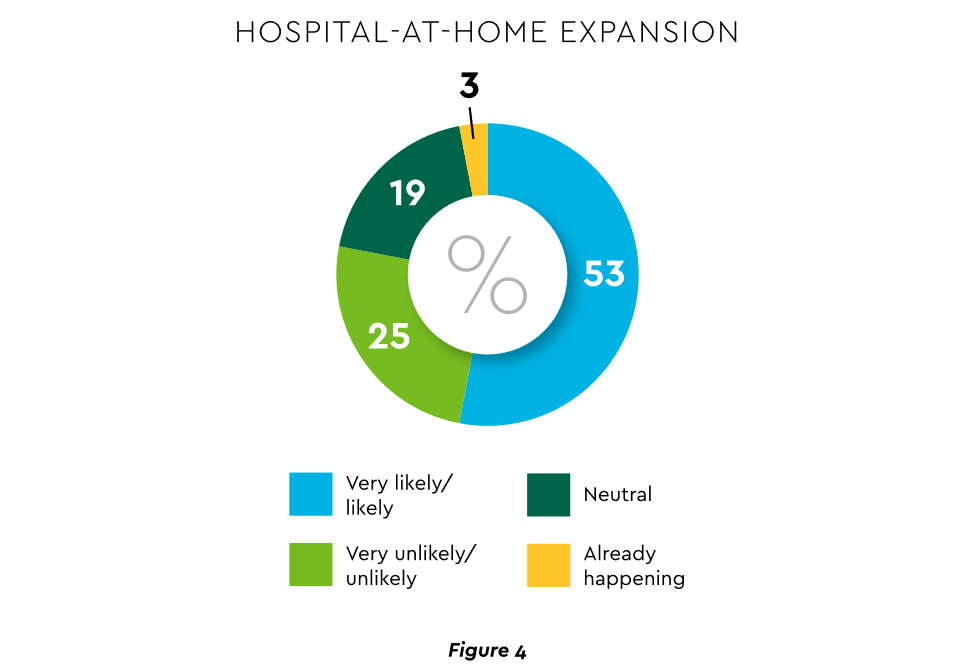

The forecasts are encouraging. Over half of hospitals believe it likely they will utilize HaH for at least half of their chronically ill patients over the next several years (Figure 4).

Harvesting the HaH potential will require implementation of current and emerging enabling technologies in remote monitoring, high-speed networks and artificial intelligence that generates algorithmic guidance for caregivers and patients alike.

3. Strong Drive to Improve and Personalize the Patient Financial Experience

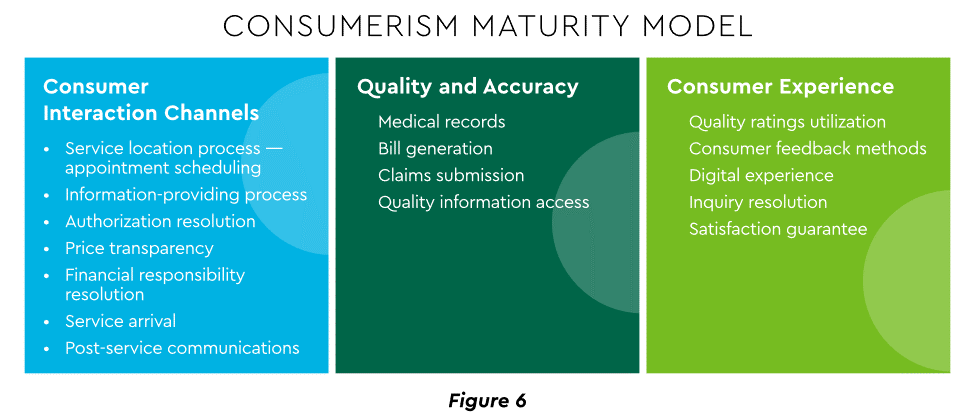

Today’s healthcare market dynamics place a premium on positive patient experiences. The goal is to deliver “an empathetic relationship between customers and brands built on what the customer wants and how they want to be treated.” It is a complex undertaking, with numerous touchpoints as captured in HFMA’s Consumerism Maturity Model (Figure 6).

An array of studies underscores the value proposition for intense provider focus on patient financial experience:

Sixty-one percent of consumers said that ease of making payments is very or somewhat important in decisions to continue seeing a doctor. Over half of patients also said text message reminders make them very or somewhat more likely to pay a bill faster than usual.

Thirty-five percent of respondents “have changed or would change healthcare providers to get a better digital patient administrative experience.”

A quality financial experience encompasses “simplified explanations, consolidated bills that match one’s health plan benefits, clear language displaying patient liability and payment options.”35

Significantly improving the financial experience requires a unified strategy, not just a collection of individual initiatives. Three threads to such a strategy will be prominent in 2023.

Using a Digital Front Door

Organizations have been moving swiftly to channel many patient financial transactions through an integrated Digital Front Door (DFD). This approach offers patients a singular online point of access and intelligent navigation to needed services. Growth is accelerating. A DFD is their patients’ first contact point for 55% of responding organizations, according to one technology survey. A leading forecaster sees 65% of patients engaging services via digital front doors by 2023.

Expanding price transparency

Mandates for full price transparency and “no surprises” billing are in effect, but estimates of compliance are mixed. An analysis of 2,000 hospitals determined that only 16% met the requirement to post an online “machine readable” file displaying clear charges for 300 “shoppable services.” Another assessment showed a more substantial 76% of hospitals had posted files, and 55% were deemed “complete.” One provision of interest to practices is the “good faith estimate” of expected charges required to be given to uninsured and self-pay individuals when they schedule visits. CommerceHealthcare® has worked with clients to enhance the patient financial experience by complementing their website pricing data with clear information on patient financing options and enrollment access. Bill pay information can also be added for one-stop guidance.

Personalizing the experience

Beyond choice and convenience, the deeper objective is truly personalized experiences throughout the care journey. The words of leading analysts best define the drive to personalize:

“Tomorrow’s healthcare experience will be built by patients tailoring their own experience.”

“By 2024, 30% of chronic care patients will truly own and openly leverage their personal health information to advocate for, secure, and realize better personalized care.”

Opportunities abound to personalize the patient financial experience. Automating manual processes establishes a foundation. Patient financing with no- or low-interest credit lines and flexible terms can produce monthly payment schedules tailored to each patient’s needs. Refunds can be made through multiple payment modes to meet varying patient preferences.

4. Evidence Underscores Growing Demand for Patient Financing

Emphasizing patient financing as part of the overall experience is powerful. Patients continue to struggle paying for care. Recent granular data details three related forces at work.

Meeting care costs difficult for many patients

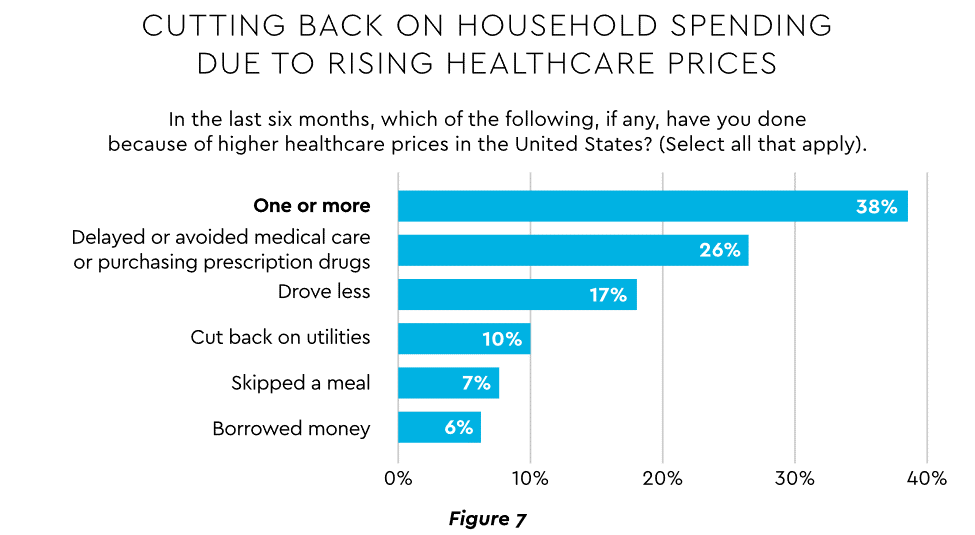

Commonwealth Fund found that 42% of individuals had problems paying medical bills or were paying off medical debt during the past year, while 49% were unable to pay an unexpected $1,000 medical bill.42 Health costs trigger reduction in a range of personal expenditures, led by deferring or avoiding care and drugs (Figure 7).

Twenty-eight percent of Americans now describe themselves as less prepared than last year to pay for routine or unanticipated care.

Patient obligation for care costs still rising

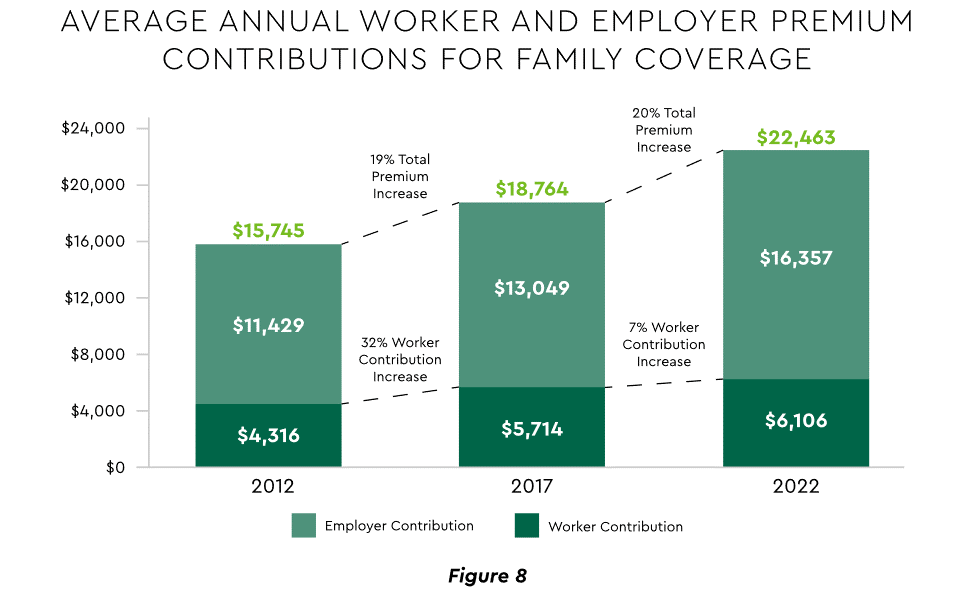

Patient obligation continues its upward march. Insurance premiums have climbed steadily for both the insured and their employers, and employees now pay over $6,000 annually on average for family coverage (Figure 8).45

High deductible health plans (HDHP) also place substantial burden on the patient. Through 2021, 28% of workers were enrolled in an HDHP with an average family deductible of $4,705. Employer satisfaction with these plans is high, auguring further expansion.

Providers feeling the financial effects

Patient payment difficulties are clearly impacting provider financials. A recent in-depth analysis uncovered substantial self-pay issues:

Self-pay accounts represented 60% of 2021 patient bad debt, up from 11% in 2018.

Nearly 18% of patient balances were over $7,500 and 17% over $14,000. Collections were noticeably lower at these balances.

Multiple chronic conditions add to the problem. A recent extensive analysis concluded: “Among individuals with medical debt in collections, the estimated amount increased with the number of chronic conditions ($784 for individuals with no conditions to $1,252 for individuals with 7–13).”

For their part, providers will be encouraged to broaden patient financing programs. Patients are certainly interested. When asked, 62% of consumers indicated they would use financing options or creative payment plans if available for large bill amounts. Many health systems, hospitals and practices will turn to outside help to satisfy the demand. A recent analysis recommended that health systems “consider keeping shorter-term payment plans in-house and extended term plans through external partnerships.”

Organizations will also need to step up their communications. A survey revealed that 64% of patients were unaware that their doctors and hospitals offered payment plans or financial help.

5. Building Trust Becoming a Critical Success Factor

Trust has emerged as a paramount issue today for most organizations as they encounter an “imperative to build trust and transparency among different stakeholder groups — employees, customers, suppliers, regulators and the communities in which they operate.” Healthcare is no exception, and the trust issue is growing in both complexity and urgency.

Healthcare’s trust gap

Trust in healthcare took a hit from the COVID-19 experience. A spring 2022 HFMA survey recorded 44% of finance leaders saying they perceived decreased patient trust. Between April 2020 and December 2021, the percentage of Americans who trusted information from doctors “a great deal” declined by 23%, from hospitals 21%, and from nurses 16%. The patient financial experience also faces “drivers of mistrust,” according to surveyed leaders who cited general payment confusion (58%), surprise billing (39%), high prices of commodity items (28%) and lack of price transparency (26%). Building trust reaps dividends. People who trust their providers are five times more likely to stay with them than those who are neutral or distrustful.

Strategies for building trust

Industry experts promote several approaches to galvanize trust among all constituencies:

Commitment. Embedding trust deeply in the organization requires full support from senior leadership.

Data transparency and governance. IDC predicts that “by end of 2023, 20% of expenses on care integration solutions will be centered around ‘trust’ to protect data, workflows and transactions.”

Reliance on fewer business partners. Many health systems, hospitals and practices are reducing their number of vendors in order to focus on a set of trusted long-term partners. For example, almost two-thirds of surveyed providers said they were seeking to streamline the number of software solutions over the next year.

The bank partner advantage

A provider’s banking relationship can yield valuable collaboration in the trust-building endeavor. Banks enjoy solid trust among consumers. As an example, 53.4% of consumers rated banks as most trusted to provide payment “super apps” and financial digital front doors ─ exceeding the next closest source by 10 points.

6. Cybersecurity in 2023: No Rest for the Weary

Cybersecurity is part of the trust calculus and has become an evergreen topic in healthcare. Compromised data and ransomware attacks are ongoing and leaders must continually refine their understanding in at least three areas: the overall security landscape, particular financially related considerations and contemporary security defenses.

The current landscape

The latest statistics quantify the cyber assault on healthcare:

Incidence. 89% of organizations suffered at least one attack in the past 12 months with the average number at 43.

Cost. A provider’s most serious attack costs an average of $4.4 million. IBM calculated healthcare’s average total cost of a breach at $10.1 million, up 42% since 2020.

Attack Characteristics. Healthcare data types most commonly compromised are personal (58%), medical (46%), and credentials (29%). Organizations have an exposure to an average of over 26,000 network-connected devices. A disturbing finding is that those healthcare institutions that paid ransom got back only 65% of their data in 2021.

Specific financial considerations

Finance leaders will also need awareness of the following:

Cyberattacks could affect credit ratings and are often a component of Environmental, Social and Governance assessments.

Financial outsourcing requires monitoring. A recent news story chronicled an accounts receivable firm’s breach that exposed individual information, account balances and payments.

Cyber insurance premiums are likely to increase substantially.

Responses/tools

Beyond a host of management and monitoring tools being deployed, a strategic philosophy is rapidly gaining ground. The “zero trust” model sounds counter to the trust-building mindset described earlier, but it has become essential. It “denies access to applications and data by default,” and 58% of hospitals and health systems have a zero trust initiative in place. Another 37% intend to implement one within 12–18 months.

Cybersecurity investment will challenge CFOs in 2023, especially in areas such as talent. Cybersecurity worker availability is estimated to satisfy only 68% of open positions. Banking partners will also be expected to play an important role. Over the years, major banks have become “leaders in enhancing cyber strategy and investing in cyber defenses, processes and talent.”

7. Digital Transformation of Finance In Focus

Digital transformation is fundamental to healthcare’s business and care delivery model changes. IBM’s website succinctly captures the goal, “Digital transformation means adopting digital-first customer, business partner, and employee experiences.” A leading forecaster believes 70% of healthcare organizations will rely on digital-first strategies by 2027.

Transformation efforts need to accelerate. One study showed that “digital, technology and analytics strategies exist for nearly all organizations, yet only 30% have begun to execute on those plans.”

One functional segment ramping up digital transformation is finance. According to a recent survey, 94% of CFOs and senior leaders stated that such efforts will be at the forefront of financial operations and strategy for 2023–2024, and 79% described it as an “absolute need” for “commercial stabilization and long-term survival of their healthcare organization.”

Advanced technology is gaining traction. Many see optimization in combining robotic process automation (RPA), artificial intelligence and machine learning to create “intelligent automation.” Together, these technologies create algorithms to automate decisions that guide “robotic” software to perform financial actions and thereby reduce manual labor.

Getting to digital-first in finance and across the enterprise has several critical success factors. These include sustained commitment, a platform-centric mindset and effective governance.

Commitment

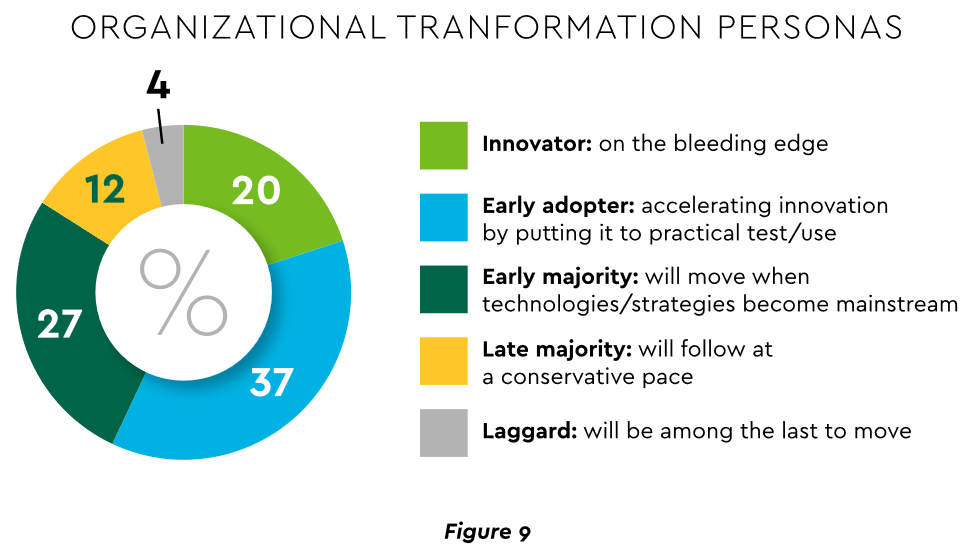

Some assert that few healthcare executives have “created digital strategies that look far enough into the future.” Speed of change is also important. Health systems, hospitals and practices exhibit varying risk appetites and change rates. When asked to self-identify “transformation personas,” a little over half regarded themselves as being on the innovative “early mover” end of the spectrum, while the remainder will adapt as technologies prove themselves (Figure 9). Slower organizations will likely need to increase the pace.

Implementing enterprise platforms rather than proliferating “point solutions” is obligatory. Organizations must be “prepared to compete in the platform economy as platform-based business models have changed the way we live, work and receive care.”

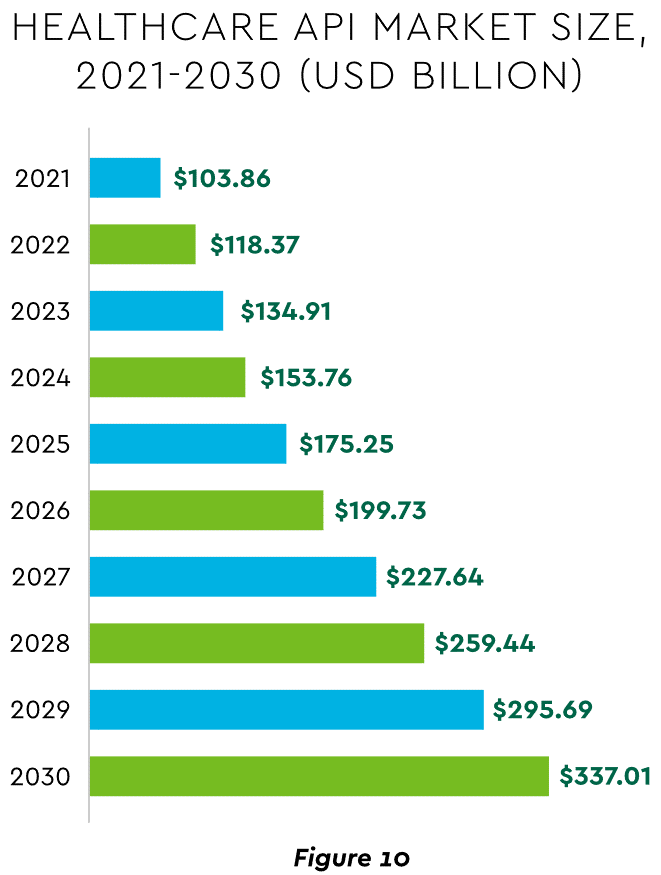

There are still too many tools and applications. A survey of top decision-makers at health systems found that 60% use over 50 software solutions just in operations (24% have over 150). System integration is one answer. Use of application programming interfaces (API) helps this effort substantially. API-first is fast becoming the norm among solution providers, with global API investment expected to nearly triple by 2030 (Figure 10)

Effective governance is vital to constructing a platform-based transformative model and to ensuring wide user adoption. Healthcare has seen the rise of new senior roles such as Chief Digital Officer and Chief Transformation Officer, positions focusing on initiatives like ownership of technology success at the department level and devising user incentives.

8. Digital Payments on the Horizon for Healthcare

A variety of emerging digital payment modes will further the transformation of finance. These payments are expected to grow almost 23% annually in healthcare. ACH payments have been on a strong upward trajectory in healthcare for several years, especially for business transactions. In 2021, ACH tallied a yearly increase of 18% in volume and 5% in dollars.

Notable technologies and payment rails to watch for expected crossover from consumer markets to healthcare include:

Mobile payments. The market for mobile payment technologies has been growing at a 16% compound annual clip and should reach $90 billion in 2023, powered by wide smartphone use, 5G networks and convenience. This category encompasses technologies such as e-wallets, forecasted to grow 23% annually worldwide through 2030.

Real-time payments (RTP). These digital transactions are settled nearly instantaneously through platforms such as The Clearing House. One forecast sees 30.4% compound RTP growth in the U.S. from 2022 to 2030.

Buy Now Pay Later (BNPL). This growing mode offers consumers short-term financing to stretch payments over several installments. A recent survey established that 23% of American adult respondents have used a BNPL service. BNPL is just entering healthcare and is currently regarded as an option for certain elective or cosmetic procedures or for specific individual credit scenarios.

Earned Wage Access (EWA). Using an RTP approach, employers are beginning to offer on-demand pay which enables “instant access to earned wages right after the work is performed, at the end of the shift, or upon completion of a project.” It is not a loan or advance pay. A 2021 poll conducted by Harris found that 83% of U.S. workers feel they should be able to access earned wages at the end of each day. Millennials were particularly interested: 80% would like daily automatic pay streaming to their bank accounts, and 78% said free EWA would boost loyalty to their employer. Given its pressing workforce concerns, healthcare is likely to find EWA a tool to promote retention.

Seeking the right use cases for these payment technologies offers many potential provider benefits.

Conclusion

The connected forces discussed and quantified here create major challenges to address in 2023. The strategic agenda calls for balancing tight cost control with investment in growth opportunities, significantly enhancing patient financial experience by meeting growing patient financial need, shoring up trusted relationships and cybersecurity, and accelerating the digital transformation of finance.

Of all the pandemic’s impacts still felt today, disruptions to the healthcare workforce and rising labor costs may be most impactful to current health system operations.

Over the next three editions of the Weekly Gist, we’ll be exploring the lingering effects of this workforce crisis, with a focus on nurse staffing and recruitment.

While wage increases helped reduce hospital registered nurse (RN) turnover rates from 27 percent in 2021 to 23 percent in 2022, nurses—along with hospital employees in general—are still changing jobs at higher rates than before the pandemic.

Over half of all hospitals still face nurse vacancy rates above 15 percent, a slight improvement from 2022 but still far more than before the pandemic.

While the worst of nursing turnover appears to have passed, the “rebasing” of wages (for nursing, 27 percent higher compared to 2019) will provide ongoing pressure to strained hospital margins.