Cartoon – Importance of Customer Service

https://www.kaufmanhall.com/insights/thoughts-ken-kaufman/physician-employment-model-continued

From time to time the blogging process stimulates a conversation between the author and the audience. This type of conversation occurred after the publication of my recent blog, “The Hospital Makeover—Part 2.” This blog focused entirely on the current problems, financial and otherwise, of the hospital physician employment model. I received responses from CEOs and other C-suite executives and those responses are very much worth adding to the physician employment conversation. Hospital executives have obviously given the physician employment strategy considerable thought.

One CEO noted that, looking back from a business perspective, physician employment was not actually a doctor retention strategy but, in the long run, more of a customer acquisition and customer loyalty strategy.

The tactic was to employ the physician and draw his or her patients into the hospital ecosystem. And by extension, if the patient was loyal to the doctor, then the patient would also be loyal to the hospital. Perhaps this approach was once legitimate but new access models, consumerism, and the healthcare preferences of at least two generations of patients have challenged the strategic validity of this tactic.

The struggle now—and the financial numbers validate that struggle—is that the physician employment model has become extraordinarily expensive and, from observation, does not scale.

Therefore, the relevant business question becomes what are the most efficient and durable customer acquisition and loyalty models now available to hospitals and health systems?

A few more physician employment observations worth sharing:

All in all, the four very smart observations detailed above continue the hospital physician employment conversation. Please feel free to add your thoughts on this or on other topics of hospital management which may be of interest to you. Thanks for reading.

https://mailchi.mp/8e26a23da845/the-weekly-gist-june-17th-2022?e=d1e747d2d8

Health systems are on edge after two quarters of shaky financial performance, with skyrocketing labor and supply costs compressing margins. But in addition to cost challenges, many are also reporting a softening of demand, with profitable surgeries and other procedures and diagnostics being hit hard. Some report seeing a drop in elective services (as one COO told us, “We may have finally worked our way through the backlog of delayed procedures from 2020 and 2021”), but in many cases, hospitals are missing the staff necessary to open up much-needed surgical capacity.

One system reported having to shut down operating rooms due to a lack of surgical techs. Even more pressing is a shortage in anesthesia capacity, with systems across the country having trouble staffing anesthesiologists and nurse anesthetists. Some practitioners have been rolled up into large, investor-owned groups, which then have taken providers out-of-network for key insurers.

But regardless of ownership structure, a shortage of providers has led to “shoestring staffing” with little ability to cover absences or departures, leading to last-minute cancellations of procedures. Pediatric hospitals have been particularly hard-hit. Most rely on subspecialty-trained anesthesiologists, and as one physician leader pointed out, children’s hospitals use anesthesia not just for surgeries, but also for diagnostics, radiation therapy and other treatments where sedation isn’t required for adults.

All in, the shortage of anesthesiologists is leading to critical treatment delays and exacerbating revenue concerns. Moreover, systems are facing frustrated consumers, who care little about the complexities of the healthcare workforce shortage and supply chain challenges that led to an abrupt cancellation of their care.

https://mailchi.mp/d73a73774303/the-weekly-gist-may-27-2022?e=d1e747d2d8

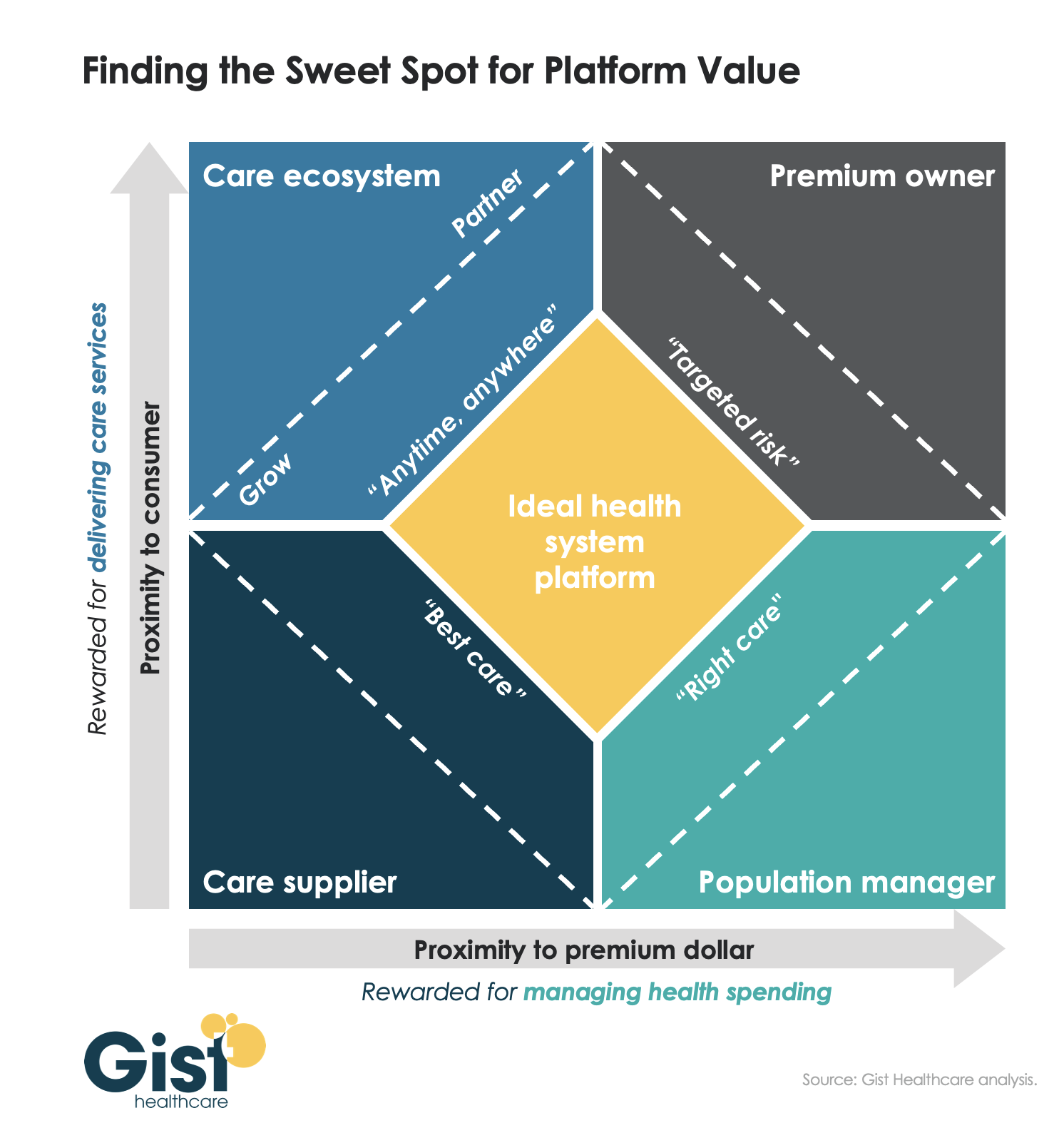

As we’ve been discussing over the past few years, several environmental forces—shifting consumer behavior, evolving demographics, new technology, and a flood of new market entrants—are pushing health systems to adopt a more consumer-centric business model. Systems must develop the capabilities needed to create an omnichannel consumer loyalty and population management platform. This platform will be the foundation for connecting consumers, curating providers, and coordinating care.

To achieve this vision, health systems must deliver value across two dimensions: increasing their proximity to the consumer (our y-axis) and their proximity to the premium dollar (our x-axis), as shown in the graphic above. Traditionally, health systems have operated primarily in the lower-left quadrant, as “care suppliers.” Some have spent considerable time and resources across the last decade, pushing closer to the premium dollar, to become “population managers.” But, importantly, managing population health is neither patient-facing, nor something consumers demand and seek.

To build deeper consumer loyalty, health systems must also move up the y-axis, creating a “care ecosystem” that provides “anywhere, anytime” care through multiple channels, including virtual and home-based solutions. And for certain populations, like Medicare Advantage, it will make sense for many systems to also explore becoming the “premium owner”, owning the full care budget and ensuring the incentives to design a consumer-centric offering.

The ideal health system platform should combine all four of these identities, tailored to the local market situation.