Using data from Kaufman Hall’s latest National Hospital Flash Report and publicly available investor reports for some of the nation’s largest health systems, the graphic below takes stock of the state of health system margins.

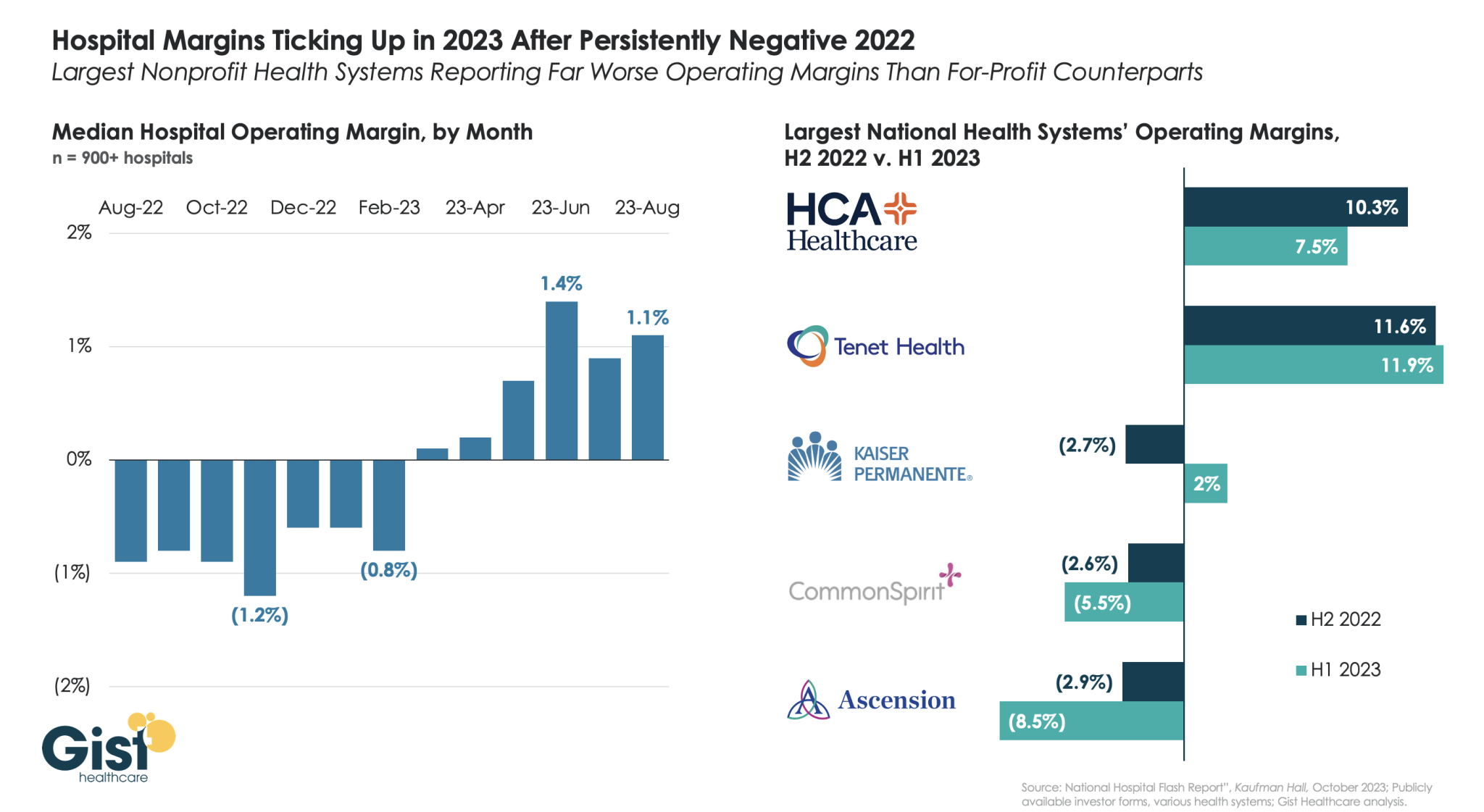

After the median hospital delivered negative operating margins for twelve-straight months, 2023 has made for a positive but slim year so far, with margins hovering around one percent. Amid this breakeven environment, fortunes have diverged between nonprofit and for-profit health systems.

The largest for-profit systems, HCA Healthcare and Tenet Healthcare, posted operating margins of around 10 percent between July 2022 and June 2023, while the three largest nonprofit systems, Kaiser Permanente, CommonSpirit Health, and Ascension, suffered net losses.

Although Kaiser Permanente’s margin bounced back in the first half of this year, CommonSpirit and Ascension’s margins continued to decline, more than doubling the operating losses of the prior six months.

One key to the recent success of the largest for-profit systems is their diversification away from inpatient care.

Case in point: almost half of Tenet’s profits in 2023 have come from its ambulatory division, driven by its United Surgical Partners International (USPI) ambulatory surgery center network, which has posted 40 percent margins over the past several quarters.

Health systems are ramping up investments in ambulatory surgery centers and forming joint ventures with outpatient partners to accelerate the development of new centers. The trend is picking up steam as complex procedures increasingly move to ASCs, which are steadily growing as the preferred site of service for physicians, patients and payers.

Tenet Healthcare, one of the largest for-profit health systems in the country, has been paying close attention to outpatient migration for years and has cemented itself as the leader in the ASC space. It now operates more than 445 ASCs — the most of any health system — and 24 surgical hospitals, according to its first-quarter earnings report.

United Surgical Partners International, Tenet’s ASC company, strengthened its footing in the ASC market after its $1.2 billion acquisition of Towson, Md.-based SurgCenter Development and its more than 90 ASCs in December 2021. Over the next several years, USPI will inject more than $250 million into ASC mergers and acquisitions and work with SurgCenter to develop at least 50 more ASCs, according to terms of the transaction.

The SurgCenter acquisition was completed shortly after Tenet sold five Florida hospitals to Dallas-based Steward Health Care for $1.1 billion. In 2022, Tenet also acquired Dallas-based Baylor Scott & White Health’s 5 percent equity position in USPI to own 100 percent of the company’s voting shares and paid $78 million to acquire ownership of eight Compass Surgical Partners ASCs.

These ASC investments and hospital sales make it clear that CEO Saum Sutaria, MD, sees surgery centers to become Tenet’s main growth driver in the coming years. Dr. Sutaria has described USPI as the company’s “gem for the future,” and aims to have 575 to 600 ASCs by the end of 2025.

While Tenet continues to increase its ASC market share, its closest competitor is Deerfield, Ill.-based SCA Health, which UnitedHealth Group’s Optum acquired for $2.3 billion several years ago.

SCA has more than 320 ASCs, but has expanded its focus on value-based care under Optum and is doubling down on supporting physicians across the specialty care continuum rather than operating as an ASC company “singularly focused on partnering with surgeons in their ASCs,” SCA CEO Caitlin Zulla told Becker’s.

While Tenet may operate the most ASCs among health systems, it lags behind Optum in terms of the number of physicians it employs. Optum is now affiliated with more than 70,000 physicians, making it the largest employer of physicians in the country, and is continuing to add to that through mergers and acquisitions.

Nashville, Tenn.-based HCA Healthcare, another for-profit system, employs or is affiliated with more than 47,000 physicians, but is also ramping up its surgery center portfolio. HCA comprises 2,300 ambulatory care facilities, including more than 150 ASCs, freestanding emergency rooms, urgent care centers and physician clinics, according to its first-quarter earnings report.

Like Tenet and Optum, HCA is heavily focused on expanding its outpatient portfolio. The company ended 2021 with 125 ASCs, four more than it had at the end of 2020, and added more than 25 ASCs last year. It is focused on both developing and acquiring surgery centers in the coming years.

The other big ASC operators include Nashville, Tenn.-based AmSurg, with more than 250 surgery centers, and Brentwood, Tenn.-based Surgery Partners, with more than 120 centers. Surgery Partners spent about $250 million on ASCs acquisitions last year and recently signed collaboration agreements with two large health systems —- Salt Lake City-based Intermountain Health and Columbus-based OhioHealth.

Oakland, Calif.-based Kaiser Permanente has 62 freestanding ASCs and outpatient surgery departments on its hospital campuses, a spokesperson for the health system told Becker’s.

On Wednesday, CVS revealed plans to phase out its clinical trials unit by December 2024. The company launched the business line in 2021, building off its successful participation engaging CVS patrons in COVID vaccine and treatment studies.

With 40 percent of Americans living near a CVS pharmacy, the company had hoped to facilitate the decentralization of the clinical trials business, recruiting patients who lived in markets without academic medical centers, with goals to engage 10M patients across 150 research sites. However, to date it has only enrolled 33K participants, just over 10 percent of its COVID vaccine volunteer patient cohort.

The Gist: While CVS appears to be focusing on its faster-growing Medicare Advantage and provider businesses, following its expensive acquisitions of Oak Street Health and Signify Health, the promise for decentralized clinical research remains.

Traditional clinical trials often suffer from low participation; recruiting from more diverse populations would improve enrollment and could enhance the quality of research conducted.

Decentralization is also a win for patients, providing access to clinical trials for lower-income patients who may have difficulty regularly traveling to academic centers. Other players, ranging from startups to retail giants like Walmart and Walgreens, remain active in this space. While we hope they may bring new models to market, they will likely evaluate their programs against similar business decisions and profit objectives.

As care continues to shift to lower cost ambulatory surgery centers (ASCs), the graphic above looks at recent growth and consolidation in the ASC market.

From 2012 to 2022, the five largest operators increased their collective ownership of ASC facilities from 17 to 21 percent, and were responsible for over 50 percent of total facility growth in that period.

While physicians still fully own over half of the nation’s ASCs, the national chains tend to run larger, multispecialty facilities responsible for an outsized proportion of procedures and revenue.

The likes of Tenet, Optum, and HCA are betting big on ASCs, banking on projections that the market will grow by over 60 percent in the next seven years.

(Though AmSurg’s parent company, Envision Healthcare, filed for bankruptcy, AmSurg is buying Envision’s remaining ASCs to retain its significant foothold in the market.)

While many high-revenue specialties, notably orthopedics and gastroenterology, have already seen a significant shift to ASCs, cardiology is one of the most promising service lines for ASC growth, with some predicting that a third of cardiology procedures will be performed in ambulatory settings in the next few years.

The shift of surgeries from hospitals to ASCs is daunting for health systems, who stand to lose half or more of the revenue from each case—if they’re able keep the procedure within the system.

In the meantime, low-cost ASC operators will continue to add new facilities that deliver high margins to fuel their growth.

Last week, 35,000 gathered in Chicago to hear about the future of health information technologies at the HIMSS Global Health Conference & Exhibition where generative AI, smart devices and cybersecurity were prominent themes.

Yesterday, the Annual Meeting of the American Hospital Association convened. Its line-up includes some big names in federal health policy and politics along with some surprising notaries like Chris Wray, Head of the FBI and others. In tandem, a new TV ad campaign launched yesterday by the Coalition to Protect America’s Health Care, of which the AHA is a founding member to pressure Congress to avoid budget cuts to hospitals to “protect care for seniors”.

These events bracket what has been a whip-lash week for the U.S. healthcare industry…

Throughout the week, the fate of medication-abortion mifepristone was in suspense ending with a Supreme Court emergency-stay decision late Friday night that defers prohibitions against its use until court challenges are resolved.

At HIMSS last Monday, EHR juggernaut EPIC and Microsoft announced they are expanding their partnership and integrating Microsoft’s Azure Open AI Service into Epic’s EHR software. Epic’s EHR system will be able to run generative AI solutions through Microsoft’s Open AI Azure Service. Microsoft uses Open Ai’s language model GPT-4 capabilities in its Azure cloud solution.

Thursday HHS posted data online showing who owns 6,000 hospices and 11,000 home health agencies that are reimbursed by Medicare.

Bell-weather companies HCA (investor-owned hospitals), Johnson and Johnson (prescription drugs) and Elevance (health insurers) reported strong 1Q profits and raised their guidance to shareholders for year-end performance.

And Monday, House Speaker Kevin McCarthy told an audience at the New York Stock Exchange that Republicans will agree to increase the $31.4 trillion debt-limit if it is accompanied by spending cuts i.e. a requirement that all “able bodied Americans without children” work to receive benefits like Medicaid, re-setting federal spending to 2022 levels and others.

Each of these is newsworthy. The partisan brinksmanship about the debt ceiling is perhaps the most immediately consequential for healthcare because it will draw attention to 2 themes:

Healthcare is profitable for some. Big companies and others with access to capital are advantaged in the current environment. Healthcare is fast-becoming a land of giants: it’s almost there in health insurance (the Big 7 in the US), prescription drugs (36 major players globally), retail drugstores (the Big 5), PBMs (the Big 4) and even the accountancies who monitor their results (the Big 4).

By contrast, the hospital and long-term care sectors sectors remain fragmented though investor-owned systems now own a quarter of operations in both.

Physicians and other clinical service provider sectors (physical therapy, dentistry, et al) are transitioning toward two options—corporatization via private equity roll-ups or hospital employment.

The 1Q earnings reported by HCA, J&J and Elevance last week give credence to beliefs among budget hawks that healthcare is a business that can be lucrative for some and expensive for all. That view aka “Survival of the Fittest” will figure prominently into the debt ceiling debate.

The regulatory environment in which U.S. healthcare operates is hostile because the public thinks it needs more scrutiny. 82% of U.S. adults think the health system puts its profits above all else. The public’s antipathy toward the system feeds regulatory activism toward healthcare.

At a federal level, the debt ceiling debate in Congress will be intense and healthcare cuts a likely by-product of negotiations between hawks and doves.

In addition, government accountants and lawmakers will increase penalties for fraud and compliance suspecting healthcare’s ripe for ill-gotten gain and/or excess. Federal advocacy in each sector will be strained by increasingly significant structural fault-lines between non-profit and for profits, and public health programs that operate on shoestrings below the radar. Two committees of the House (Ways and Means and Energy and Commerce) and two Senate Committee’s) will hold public hearings on issues including not-for-profit hospitals consolidation, price transparency and others with unprecedented Bipartisan support for changes likely “uncomfortable” for industry insiders.

At a state level, matters are even more complicated: states are the gatekeeper for the healthcare system’s future. States will increasingly control the supply and performance criteria for providers and payers. Ballot referenda will address issues reflective of the state’s cultural and political values—abortion rights, public health funding, gun control, provider and prescription drug price controls, and many more.

My take

The upcoming debt ceiling debate comes at a pivotal time for healthcare because it does not enjoy the good will it has in decades past. The pandemic, dysfunctional political system and the struggling economy have taken a toll on public confidence. Long-term planning for the system’s future is subordinated to the near term imperative to control costs in the context of the debt ceiling debate.

The federal debt will hit its ceiling in June. Speaker McCarthy’s ‘Limit, Save, Grow Act’ would return the government’s discretionary spending to fiscal year 2022 levels, cap annual spending growth at 1% for a decade and raise the debt ceiling until March 31, 2024, or until the national debt increases by $1.5 trillion, whichever comes first.

That means healthcare program cuts. That’s why this debt ceiling expansion is more than perfunctory: it’s an important barometer about the system’s future in the U.S. and how it MIGHT evolve:

In 8-10 years, it MIGHT be dominated by fewer players with heightened regulatory constraints.

It MIGHT be funded by higher taxes in exchange for better performance.

It MIGHT be restructured with acute services as a public utility. It might be a B2C industry in which employers play a lesser role and a national platform powered by generative AI and GPT4 enables self-care and interoperability.

It MIGHT be an industry wherein public health and social services programs are seamlessly integrated with non-profit health systems.

It MIGHT be built on the convergence of financing and delivery into regional systems of health.

It MIGHT bifurcate into two systems—one public for the majority and one private for some who can afford it.

It MIGHT replace the trade-off between community benefits and tax exemption.

It MIGHT re-define distinctions between non-profit hospitals and plans with their predicate investor-owned operators, and so on.

No one knows for sure, but everyone accepts the future will NOT be a repeat of the past. And the resolution of the debt ceiling in the next 60 days will set the stage for healthcare for the next decade.

Franklin, Tenn.-based CHS, which reported a net loss of $20 million in the first quarter on revenues of $3.1 billion, is on the hunt for new acquisitions just as it is also in discussions to sell off more assets.

“We are considering further opportunities to expand our portfolio,” CEO Tim Hingtgen said in a webcast discussing first-quarter results.

Selling off certain assets would also help balance the system and further reduce some of its debt, President and CFO Kevin Hammons confirmed on the call.

“Moreover, we may give consideration to divesting certain additional hospitals and non-hospital businesses,” CHS said in an SEC filing. “Generally, these hospitals and non-hospital businesses are not in one of our strategically beneficial services areas, are less complementary to our business strategy and/or have lower operating margins. In addition, we continue to receive interest from potential acquirers for certain of our hospitals and non-hospital businesses.”

The health system, which operates 79 hospitals in 15 states, has agreed to sell four more hospitals effective Jan. 1, the filing stated.

CHS recently completed the $92 million sale of Oak Hill, W.Va.-base Plateau Medical Center to Charleston, W.Va.-based Vandalia Health. It also finalized on Jan. 3 an $85 million sale of its former 122-bed facility in Ronceverte, W.Va, also to Vandalia Health.

CHS shares were trading at $6.24 before its results were released. It is currently trading at approximately $3.70.

Franklin, Tenn.-based Community Health Systems, one of the largest for-profit health systems in the country,reported $179 million net income in 2022, a 51.4 percent drop from the $368 million net income reported the prior year.

The drop was driven by a decline in net operating revenues, fewer inpatient admissions and what CHS termed “unfavorable changes” in payer mix.

Total operating costs and expenses for the year ended Dec. 31 were $11.4 billion, up from $11 billion in 2021. Net operating revenues were $12.2 billion in 2022, down slightly from $12.4 billion the prior year.

Net income in the final three months of the year totaled $446 million compared with $223 million in the same period in 2021.

“We were pleased with our progress during the final quarter of the year, including solid volume growth in admissions, adjusted admissions and surgeries,” CEO Tim Hingtgen said in a statement. “We also significantly reduced contract labor from its peak in early 2022 while improving overall employee recruitment and retention levels.”

CHS, which owns or leases 79 affiliated hospitals with approximately 13,000 beds and operates more than 1,000 sites of care, also released guidance for 2023, predicting annual revenues of between $12.2 billion and $12.6 billion. Such figures compare with $12.2 billion in 2022.

The system, which is also predicting a net loss in 2023 between 0.05 and 0.65 a share, recorded long-term debt of $11.6 billion as of Dec. 31 compared with $12.1 billion at the same time in 2021.

Recent conversations with executive teams about physician issues have made us feel like we’ve time-travelled back to 2006. Both health systems and large independent physician groups report having difficulties hiring physicians willing to take call, even among specialties where it has long been part of the job expectations.

“We stopped paying for call fifteen years ago,” one CMO shared. “But now, even though we’ve started paying again, it’s hard to get takers.” While procedural specialties seem to be the hardest to cover, with orthopedics, urology, and GI cited most frequently, we’re also hearing challenges with medical specialty coverage. One hospital CEO (who lamented that call coverage had once again risen to a CEO-level problem) shared that cardiologist candidates were looking for positions without call obligations.

The knee-jerk reaction of older executives is to blame a younger generation of doctors seeking more work-life balance. Surely this contributes, but as one astute medical group CEO pointed out, the only way doctors can draw this line in the sand with health systems is if there are alternatives that don’t require call.

He referenced the growing number of investor-backed specialty practices focused squarely on outpatient growth and even offering doctors no-call positions straight out of training. In his market, he felt these doctors were discouraged from taking call: “When 80 percent of the procedures are done in a surgery center, an orthopod doesn’t need referrals from call to fill his schedule with new patients. And the patients they encounter in our ED are more likely to be uninsured or government pay, so they don’t want them anyway.”

Beyond simply paying for call, a few other solutions are gaining traction. Some hospitals are expanding the number of in-house, hospitalist-like positions for other specialties. Others are deploying virtual consult services with some success, even in procedural specialties. As one orthopedic surgeon told us, the virtual call coverage does a decent job with triage and can often save the doctor from having to come in overnight.

Ultimately, as the number of investor-owned specialty groups expands, health systems must develop collaborative relationships to solve care delivery challenges across the continuum.

Radio Advisory’s Rachel Woods sat down with Optum EVP Dr. Jim Bonnette to discuss the sustainability of modern-day hospitals and why scaling down might be the best strategy for a stable future.

Rachel Woods:When I talk about hospitals of the future, I think it’s very easy for folks to think about something that feels very futuristic, the Jetsons, Star Trek, pick your example here. But you have a very different take when it comes to the hospital, the future, and it’s one that’s perhaps a lot more streamlined than even the hospitals that we have today. Why is that your take?

Jim Bonnette: My concern about hospital future is that when people think about the technology side of it, they forget that there’s no technology that I can name that has lowered health care costs that’s been implemented in a hospital. Everything I can think of has increased costs and I don’t think that’s sustainable for the future.

And so looking at how hospitals have to function, I think the things that hospitals do that should no longer be in the hospital need to move out and they need to move out now. I think that there are a large number of procedures that could safely and easily be done in a lower cost setting, in an ASC for example, that is still done in hospitals because we still pay for them that way. I’m not sure that’s going to continue.

Woods: And to be honest, we’ve talked about that shift, I think about the outpatient shift. We’ve been talking about that for several years but you just said the change needs to happen now. Why is the impetus for this change very different today than maybe it was two, three, four, five years ago? Why is this change going to be frankly forced upon hospitals in the very near future, if not already?

Bonnette: Part of the explanation is regarding the issues that have been pushed regarding price transparency. So if employers can see the difference between the charges for an ASC and an HOPD department, which are often quite dramatic, they’re going to be looking to say to their brokers, “Well, what’s the network that involves ASCs and not hospitals?” And that data hasn’t been so easily available in the past, and I think economic times are different now.

We’re not in a hyper growth phase, we’re not where the economy’s performing super at the moment and if interest rates keep going up, things are going to slow down more. So I think employers are going to become more sensitized to prices that they haven’t been in the past. Regardless of the requirements under the Consolidated Appropriations Act, which require employers to know the costs, which they didn’t have to know before. They’re just going to more sensitive to price.

Woods: I completely agree with you by the way, that employers are a key catalyst here and we’ve certainly seen a few very active employers and some that are very passive and I too am interested to see what role they play or do they all take much more of an active role.

And I think some people would be surprised that it’s not necessarily consumers themselves that are the big catalyst for change on where they’re going to get care, how they want to receive care. It’s the employers that are going to be making those decisions as purchasers themselves.

Bonnette: I agree and they’re the ultimate payers. For most commercial insurance employers are the ultimate payers, not the insurance companies. And it’s a cost of care share for patients, but the majority of the money comes from the employers. So it’s basically cutting into their profits.

Woods: We are on the same page, but I’m going to be honest, I’m not sure that all of our listeners are right. We’re talking about why these changes could happen soon, but when I have conversations with folks, they still think about a future of a more consolidated hospital, a more outpatient focused practice is something that is coming but is still far enough in the future that there’s some time to prepare for.

I guess my question is what do you say to that pushback? And are there any inflection points that you’re watching for that would really need to hit for this kind of change to hit all hospitals, to be something that we see across the industry?

Bonnette: So when I look at hospitals in general, I don’t see them as much different than they were 20 years ago. We have talked about this movement for a long time, but hospitals are dragging their feet and realistically it’s because they still get paid the same way until we start thinking about how we pay differently or refuse to pay for certain kinds of things in a hospital setting, the inertia is such that they’re going to keep doing it.

Again, I think the push from employers and most likely the brokers are going to force this change sooner rather than later, but that’s still probably between three and five years because there’s so much inertia in health care.

On the other hand, we are hitting sort of an unsustainable phase of cost. The other thing that people don’t talk about very much that I think is important is there’s only so many dollars that are going to health care.

And if you look at the last 10 years, the growth in pharmaceutical spend has to eat into the dollars available for everybody else. So a pharmaceutical spend is growing much faster than anything else, the dollars are going to come out of somebody’s hide and then next logical target is the hospital.

Woods: And we talked last week about how slim hospital margins are, how many of them are actually negative. And what we didn’t mention that is top of mind for me after we just come out of this election is that there’s actually not a lot of appetite for the government to step in and shore up hospitals.

There’s a lot of feeling that they’ve done their due diligence, they stepped in when they needed to at the beginning of the Covid crisis and they shouldn’t need to again. That kind of savior is probably not their outside of very specific circumstances.

Bonnette: I agree. I think it’s highly unlikely that the government is going to step in to rescue hospitals. And part of that comes from the perception about pricing, which I’m sure Congress gets lots of complaints about the prices from hospitals.

And in addition, you’ll notice that the for-profit hospitals don’t have negative margins. They may not be quite as good as they were before, but they’re not negative, which tells me there’s an operational inefficiency in the not for-profit hospitals that doesn’t exist in the for-profits.

Woods: This is where I wanted to go next. So let’s say that a hospital, a health system decides the new path forward is to become smaller, to become cheaper, to become more streamlined, and to decide what specifically needs to happen in the hospital versus elsewhere in our organization.

Maybe I know where you’re going next, but do you have an example of an organization who has had this success already that we can learn from?

Bonnette: Not in the not-for-profit section, no. In the for-profits, yes, because they have already started moving into ambulatory surgery centers. So Tenet has a huge practice of ambulatory surgery centers. It generates high margins.

So, I used to run ambulatory surgery centers in a for-profit system. And so think about ASCs get paid half as much as a hospital for a procedure, and my margin on that business in those ASCs was 40% to 50%. Whereas in the hospital the margin was about 7% and so even though the total dollars were less, my margin was higher because it’s so much more efficient. And the for-profits already recognize this.

Woods: And I’m guessing you’re going to tell me you want to see not-for-profit hospitals make these moves too? Or is there a different move that they should be making?

Bonnette: No, I think they have to. I think there are things beyond just ASCs though, for example, medical patients who can be treated at home should not be in the hospital. Most not-for-profits lose money on every medical admission.

Now, when I worked for a for-profit, I didn’t lose money on every Medicare patient that was a medical patient. We had a 7% margin so it’s doable. Again, it’s efficiency of care delivery and it’s attention to detail, which sometimes in a not-for-profit friends, that just doesn’t happen.

Recent reports have raised concerns about the financial stability of hospitals amidst disruptions caused by the COVID-19 pandemic and the looming prospect of an economic recession.

Large amounts of government relief helped prop up hospital margins in 2020 and 2021. However, industry reports suggest that the outlook for hospitals and health systems has deteriorated in 2022 due to the ongoing effects of the pandemic (such as labor shortages), decreases in government relief, and broader economic trends that have led to rising prices and investment losses. According to at least one account, 2022 may be the worst financial year for hospitals in decades. These challenges could force hospitals to take steps to increase efficiency but may also result in price increases or cost-cutting measures that impair patient access or care quality. Against this backdrop,industrystakeholders have asked Congress to provide additional fiscal relief to hospitals and to stop scheduled Medicare payment reductions.

To provide context for these policy discussions, we evaluated the financial performance of the three largest for-profit health systems in the country—HCA Healthcare (“HCA”), Tenet Healthcare Corporation (“Tenet”), and Community Health Systems (CHS)—which collectively accounted for about 8 percent of community hospital beds in the US in 2020.1 These three systems are publicly traded, meaning that we were able to acquire timely financial data about these systems through their reports to the Securities and Exchange Commission (SEC), as well as data on their stock prices (see Methods for additional details).

Operating margins among all three large health systems were positive and exceeded pre-pandemic levels for the majority of the pandemic, including most recently in the third quarter of 2022.

Operating margins reflect the profit margins earned on patient care and other operations of a given health system—such as from gift shops, parking, and cafeterias—and incorporate government COVID-19 relief funds.2 Our definition of operating margins excludes income taxes and nonrecurring revenues and expenses, such as from the sale of facilities. HCA and Tenet had positive operating margins throughout the pandemic, and CHS had positive operating margins in all but two quarters of the pandemic (with one of those quarters being at the very beginning of the pandemic). HCA has had operating margins of at least 10 percent during the majority of the pandemic (9 out of 11 quarters). In other words, HCA’s revenue from patient care and other operations exceeded operating expenses by at least 10 percent for most of the pandemic. Tenet has had operating margins of at least 5 percent for the majority of the pandemic (9 out of 11 quarters), while CHS’s operating margins have been lower (less than 5% for 9 out of 11 quarters). CHS had lower margins than the other systems before the pandemic as well.

For all three systems, operating margins have exceeded pre-pandemic (2019) levels for most of the pandemic (9 out of 11 quarters), including the last quarter of our analysis (the third quarter of 2022), despite recent decreases in operating margins. HCA and Tenet dipped below their 2019 operating margins during two quarters of 2020, and CHS fell below their 2019 operating margins during the first quarter of 2020 and the second quarter of 2022 before increasing again. As of the third quarter of 2022, operating margins were 11.4 percent for HCA, 8.4 percent for Tenet, and 1.2 percent for CHS.

Stock prices increased and then decreased during the pandemic; HCA and Tenet stock prices have increased overall since January 2020 while CHS stock prices have decreased.

Stock prices generally reflect investors’ evaluation of the future earnings potential of a given company. Stock prices increased dramatically during the first 1.5 to 2 years of the pandemic. At their heights, HCA stock prices had increased by 87.9 percent, Tenet stock prices had increased by 153.8 percent, and CHS stock prices had increased by 383.1 percent relative to January 2020.

Stock prices have also decreased substantially in 2022—in line with broader economic trends—and especially so among Tenet and CHS. As of November 8, 2022, HCA and Tenet stock prices have increased overall relative to January 2020 (by 44.6% and 12.6%, respectively).3 CHS stock prices have decreased by 11.5% since January 2020, though CHS has also experienced longstanding financial challenges thatpredate the pandemic. For purposes of comparison, HCA stock prices increased by a much greater amount than the S&P 500 during this period (44.6% versus 16.8%), while the S&P 500 slightly outperformed Tenet stock (16.8% versus 12.6%) and significantly outperformed CHS stock (16.8% versus -11.5%).

As of December 2, 2022, the majority of market analysts followed by MarketWatch were bullish on HCA and Tenet stock (with 18 buy, 3 overweight, and 5 hold recommendations for HCA stock and 14 buy, 2 overweight, and 4 hold recommendations for Tenet stock) and neutral about CHS stock (with 8 hold and 4 buy recommendations); none of the analysts rated these stocks as “sell” or “underweight.”

Discussion

Industry reports have suggested that hospitals had high margins in 2020 and 2021 but have faced significant financial challenges in 2022. Our analysis adds nuance to this discussion. So far this year, operating margins among the three largest for-profit health systems in the country have met or exceeded pre-pandemic levels. HCA and Tenet in particular have had high operating margins. CHS had negative operating margins in the second quarter of 2022, and its stock prices decreased overall from January 2020 to November 2022, but its financial challenges precede the pandemic. While some hospitals are struggling in the current environment—with high inflation and the ongoing burdens posed by COVID-19, flu, and respiratory syncytial virus (RSV)—our results indicate that the largest for-profit systems have had operating margins that exceed pre-pandemic levels.