After COVID fears and shutdowns led consumers to delay care early in the pandemic, persistently high inflation over the past year has further suppressed volumes.

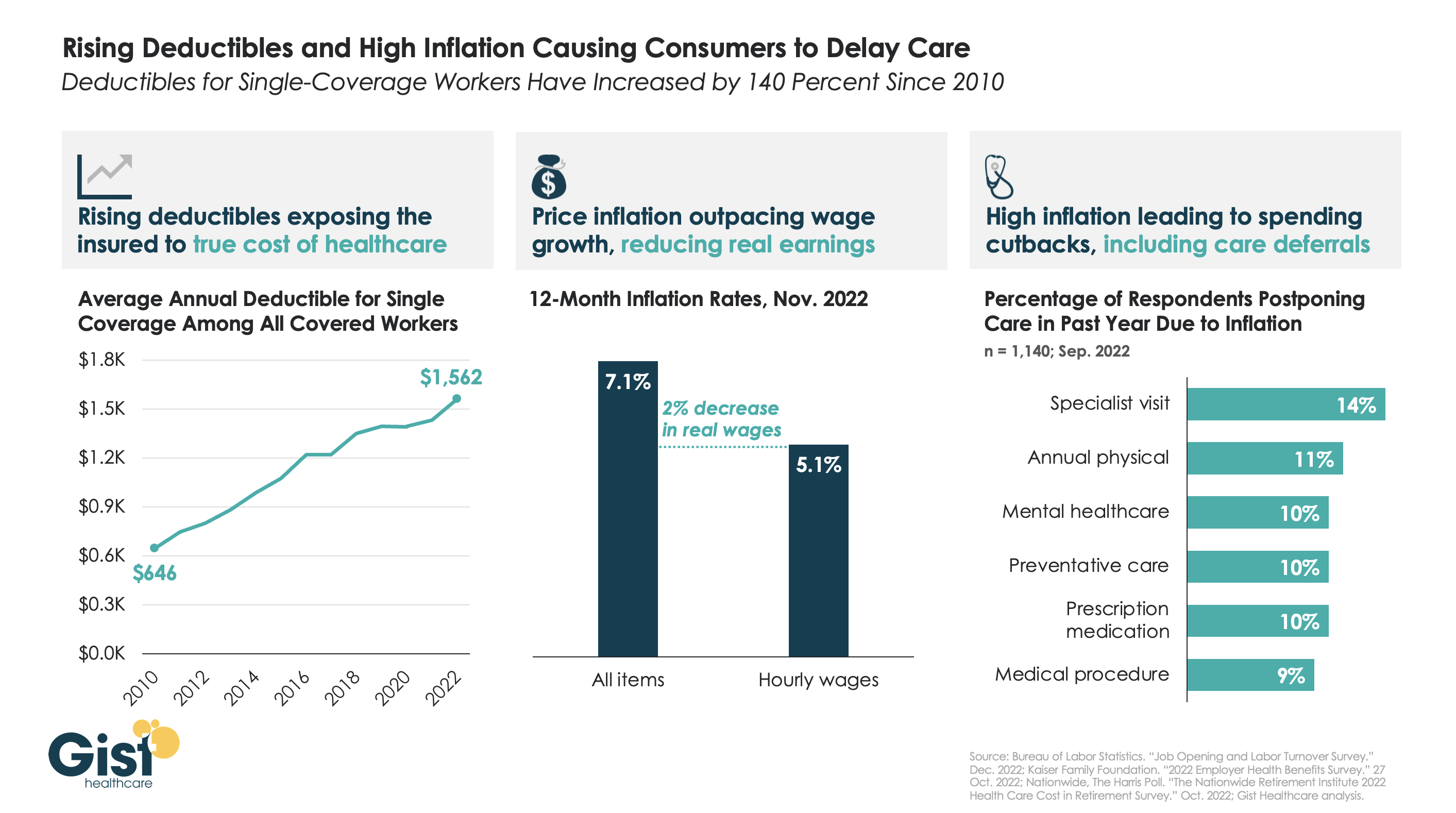

As the graphic above illustrates, the average deductible for individual coverage has grown by over 140 percent since 2010, exposing consumers to an increasing portion of healthcare costs, and prompting economists to reevaluate the adage that healthcare is “recession-proof”.

This year, that trend collided with an inflation spike that outpaced wage gains by two percent. Faced with diminished purchasing power, households are making budget tradeoffs which explicitly pit healthcare against other essential household needs.

For some, this cost-cutting impulse even extends to preventative screenings—required to be covered without cost-sharing—when consumers’ financial concerns drive them to avoid healthcare altogether.

While the latest inflation report suggests price increases are moderating, fears of a broader recession persist, making it critical for health systems and physicians to communicate with patients, encouraging them to continue to access preventive care, educating them about lower cost care options, and helping them prioritize treatment that should not be put off.

Open enrollment is upon us. While many are focused on which health insurance company has the best deal, health care sharing ministries (HCSMs) are quietly offering cheaper and less regulated alternatives to traditional coverage. Despite being an inadequate substitute, for some, they’re a welcome one.

What are HCSMs?

HCSMs are not health insurance; they are cost-sharing organizations. The idea is that members help each other directly cover medical costs. Members pay monthly contributions, similar to premiums, but can also make additional donations to cover specific bills from other members.

HCSMs are allowed to exclude pre-existing conditions from eligibility, exclude various health care services altogether, such as maternity care or contraception, and cap the lifetime financial assistance for which a member is eligible. They also do not guarantee claims will be reimbursed. (One review of HCSMs in Massachusetts found that only half of submitted claims were eligible for reimbursement.)

They are often, if not always, religiously affiliated. Members commit to a code of conduct, which may include abstaining from tobacco use and holding a traditional view of sex and marriage.

HCSMs and the Affordable Care Act

Because they are not insurance and because they are religiously affiliated, HCSMs are not regulated by the Affordable Care Act (ACA). They are not subject to minimal coverage guidelines and members are not subject to the individual mandate.

HCSMs are a notable exemption to the ACA. Supporters lobbied for the exemption based on a few reasons, including former President Obama’s promise that Americans could keep their coverage if they liked it. But the main motive was religious freedom. They argued that sharing health care costs was a “religious right and a privilege.” Congress agreed to the carveout to minimize religious opposition, and advocates lauded the decision as “Obamacare’s Silver Lining.”

The appeal of HCSMs

Some see HCSMs as a viable alternative to traditional health insurance and research suggests there may be a few reasons why.

Perhaps the most significant reason is freedom: freedom of religious expression and freedom from government oversight. The Bible encourages Christians to “bear one another’s burdens,” and HCSM members see their approach to health care costs as a fulfillment of that command. Additionally, many religious individuals oppose abortion and other medical services. As such, they may see HCSMs as a way to pay for their own health care needs without funding religiously prohibited services even indirectly.

HCSMs promote a sense of freedom beyond religion, including provider choice and less government interference. For example, members essentially pay out of pocket for health care, getting reimbursed later, so they can choose any provider that accepts self-paying patients. HCSMs also allow members to bypass “the system,” staying out of the carousel that is the heavily regulated health insurance industry.

A more tangible reason why some prefer HCSMs to traditional health insurance is thrift. Monthly contributions are typically less than monthly insurance premiums. This makes sense; HCSMs are set up to cover health care expenses after they’re accrued so upfront costs can be lower. Plus, the list of reimbursable services is often limited in exchange for even lower costs.

For healthy individuals, especially those who don’t use much health care, this kind of “low cost up front” arrangement can be enticing. But, if a member has an emergency or an extended hospital stay, or develops a chronic condition, they may be stuck with significant medical bills. Monthly contributions can also increase due to changes in health status, even common ones like weight gain.

While freedom and thrift are conscious reasons to prefer HCSMs, others may choose them due to inadequate health insurance literacy. Individuals less familiar with terms like coinsurance and deductibles may have difficulty choosing from a set of ACA-compliant health insurance plans. This difficulty likely extends to evaluating the relative costs and benefits of HCSMs.

Challenges differentiating between insurance and HCSMs may also increase when small businesses list HCSMs as a potential source of coverage for health care costs. Deceptive advertising by HCSMs and insurance brokers adds further confusion.

While HCSMs are an unregulated, risky alternative to traditional insurance coverage, some find the freedom and cost savings they provide attractive. Others don’t know of a better option and join an HCSM without understanding the potential consequences. Given that inadequate insurance coverage is associated with greater medical debt and delays in seeking necessary care, it’s important that consumers have clear, accurate information to facilitate coverage decisions.

Hospitals in some non-Medicaid expansion states are pitching expansion as a way to help solve the rural health crisis. But the industry is hardly speaking with one voice.

Driving the news: Facilities with fewer commercially insured patients that treat a large number of uninsured people see expansion as a potential lifeline in tough economic times.

In Mississippi, where up to 12 hospitals are in danger of closing, an expansion of the safety net program could generate $1 billion a year and create more than 11,000 jobs, according to one projection.

And in Texas, an expansion could reduce the $7 billion in uncompensated care hospitals there have to absorb each year, according to the state’s hospital association.

Yes, but: Republican lawmakers in the holdout states continue to oppose enlarging their Medicaid rolls, citing higher state costs of covering a bigger population.

And hospital associations in North Carolina and Florida have opposed expansion plans, either out of concern about alienating key lawmakers or because the plans could bring other changes that disrupt dollars flowing to their members.

State of play: South Dakota voters approved a Medicaid expansion ballot measure this fall, leaving 11 non-expansion states.

Democratic governors in North Carolina and Kansas think they may be wearing down Republican opposition, Politico reports, but still face uphill battles when the new legislative sessions begin.

Zoom in: Medicaid expansion can bring dollars into a state’s health care system, even if the program pays only a fraction of the actual cost of care.

Numerous studies show that Medicaid expansion can have a positive financial impact on hospitals’ operating and profit margins, particularly smaller rural facilities, Robin Rudowitz, vice president at the Kaiser Family Foundation, told Axios.

The program could provide a reprieve for hospitals that were kept afloat in part by federal pandemic aid that’s now drying up.

“We have hospitals with 12 days cash on hand. We’ve lost a nursing home this year. We have seen decreased services. We’ve lost OB services in a few places, and we’ve seen over the years the decrease in mental health,” Wyoming Hospital Association vice president Josh Hannes told state lawmakers last month, per Politico.

Expanding Medicaid in other states has also led to a significant decline in uncompensated care costs, as well as improved states’ health outcomes, including overall mortality.

Yes, but: Medicaid expansion is not necessarily a silver bullet that will rescue every struggling facility.

Some state hospital associations are seeking other types of relief, from cuts in hospital bed taxes or higher reimbursements for existing Medicaid beneficiaries.

Of note: Rural, small hospitals have the most to gain from Medicaid expansion, because they serve a smaller patient populations with a larger pool of uninsured people.

Congress sweetened the deal for non-expansion states in the American Rescue Plan Act, with a 5% increase in the federal Medicaid Assistance Percentage for the state’s current Medicaid recipients, which lasts for two years.

In Texas, whose uninsured rate is the highest in the nation, hospital leaders think Medicaid expansion could help cover many in the working class whose jobs do not offer health plans.

“If you could get those folks coverage at a Medicaid rate it would obviously help the financial situations of (rural) hospitals, and if you could get them to a medical home you could deal with more acute medical conditions going forward,” John Hawkins, president of the Texas Hospital Association, told reporters last week.

The bottom line: While rural hospitals all over are facing headwinds, those in non-expansion states are bearing the brunt of the pain. And while there is a potential lever for those states, it doesn’t appear likely their elected officials are willing to pull it.

Of these 18 million people, 3.8 million people will become completely uninsured, according to the Urban Institute’s report. The estimate is higher than HHS’ August prediction of 15 million people losing coverage after the public health emergency.

If the Covid-19 public health emergency expires in April, about 18 million people could lose Medicaid coverage, a new report concludes.

The Urban Institute, which published the report, found that of these 18 million people, 3.8 million people will become completely uninsured. About 3.2 million children will likely move from Medicaid to separate Children’s Health Insurance Programs. Additionally, about 9.5 million people will receive employer-sponsored insurance. Lastly, more than 1 million people will enroll in a plan through the nongroup market.

The Urban Institute’s estimates, published Monday, is higher than the U.S. Department of Health & Human Services’ (HHS) prediction of 15 million people losing coverage after the public health emergency ends. HHS’ report was published in August and stated that 17.4% of Medicaid and Children’s Health Insurance Program enrollees would leave the program. The Urban Institute’s report did not provide a percentage.

To conduct the study, researchers from the Urban Institute relied on the most recent administrative data on Medicaid enrollment, as well as recent household survey data on health coverage. It used a simulation model to estimate how many Americans will lose Medicaid insurance.

In 2020, Congress passed the Families First Coronavirus Response Act due to the Covid-19 pandemic. It barred states from disenrolling people during the public health emergency, and in return, states received a temporary increase in the federal Medicaid match rates. From February 2020 to June 2022, Medicaid enrollment increased by 18 million people, an unprecedented number, according to the Urban Institute.

Currently, the public health emergency is set to end in January. But since the government has to provide a 60-day notice before the expiration —and did not do so in November — it is expected to be extended to April.

Because many of the affected enrollees who will lose Medicaid coverage will be eligible for coverage through federal or state Marketplaces, the Urban Institute recommends coordination between the Marketplaces and state Medicaid agencies

Researchers called on the government to take action so Americans are prepared for the end of the public health emergency.

“State Medicaid officials and policymakers must continue to ensure that individuals currently enrolled in Medicaid are aware of the approaching end of the public health emergency, and that they have a plan to maintain or find new health coverage through their employer, the federal healthcare Marketplace, or Medicaid,” the Urban Institute said.

2022 has disproven the old trope that “healthcare is recession-proof”. With the average family deductible nearing $4,000, a significant portion of healthcare services are exposed to consumer concerns about affordability. Reflecting the impact of the recession, health systems nationwide have reported sluggish volumes, particularly for elective cases, in the second half of the year.

One COO recently shared, “We’re 15 percent off where we expected to be on elective cases…We didn’t see the usual pick-up in early fall, after summer vacation. I’m not sure if it’s related to the economy, or whether demand changed during COVID, but this decline has eroded any possibility of a positive margin for the quarter.” The recession hit just as providers mostly finished working through the backlog of cases delayed by COVID in 2020 and 2021.

To determine whether demand declines are related to the current economic environment, or signal real shifts in care patterns, health systems are looking closely to see if the usual end-of-year swell of demand for elective care materializes, as patients max out their deductibles. But even if the demand is there, some systems are worried about being able to accommodate it: “We’ve been so short-staffed for nurses and surgical techs, we’ve had to intermittently take some ORs and units offline…If we get a big December spike in elective care, I’m not sure we’ll have the staff to accommodate it.” Facing the triple threat of sky-high costs, sluggish demand, and a worsening payer environment, the ability to accommodate this demand will be critical to securing margins as providers move into 2023.

Driven by the steady progress of Medicaid expansion and pandemic-era policies to ensure access to health insurance coverage, the US uninsured rate hit an all-time low of 8 percent in early 2022. Since the Affordable Care Act passed in 2010, the US uninsured rate has been cut in half, with the largest gains coming from Medicaid expansion.

However, using data from Commonwealth Fund, the graphic below illustrates how this noteworthy achievement is undermined by widespread underinsurance, defined as coverage that fails to protect enrollees from significant healthcare cost burdens. A recent survey of working-age adults found that eleven percent of Americans experienced a coverage gap during the year, and nearly a quarter had continuous insurance, but with inadequate coverage.

High deductibles are a key driver of underinsurance, with average deductibles for employer-sponsored plans around $2,000 for individuals and $4,000 for families.

Roughly half of Americans are unable to afford a $1,000 unexpected medical bill. Americans’ healthcare affordability challenges will surely worsen once the federal COVID public health emergency ends, because between 5M and 14M Medicaid recipients could lose coverage once the federal government ends the program that has guaranteed continuous Medicaid eligibility.

The process of eligibility redeterminations is sure to be messy—while some Medicaid recipients will be able to turn to other coverage options, the ranks of uninsured and underinsured are likely to swell.

Nearly 3.4 million people have signed up for 2023 Affordable Care Act insurance coverage since the start of open enrollment on Nov. 1, a record-setting pace that is a 17% boost over last year, new federal data shows.

The signup data released Tuesday by the Centers for Medicare and Medicaid Services shows a major hike in new signups on HealthCare.gov.

“We are off to a strong start — and we will not rest until we can connect everyone possible to healthcare coverage this enrollment season,” Department of Health and Human Services Secretary Xavier Becerra said in a statement Tuesday.

The nearly 3.4 million in signups represents activity through Nov. 19 on HealthCare.gov, which is used by residents in 33 states to pick an ACA plan, and through Nov. 12 for the 16 states and District of Columbia that run their own marketplaces.

There are 655,000 people who are new to the exchanges that picked a plan already, making up 19% of the total plan signups so far. CMS added that 2.7 million people who already have 2022 coverage renewed or selected a new plan for 2023.

“These plan selection numbers represent a 17% increase in total plan selections over last year,” CMS said in a release.

There is especially major growth on HealthCare.gov, which has seen 493,216 new enrollees compared to 354,137 for the same time period last year.

“Providing quality, affordable health care options remains a top priority,” said CMS Administrator Chiquita Brooks-LaSure in a statement. “The numbers prove that our focus is in the right place.”

The new signups come as the Biden administration made new investments in expansions for marketing and outreach, including record-setting funding for the ACA navigator program. Administration officials are hoping for another robust period of signups thanks to enhanced subsidies to lower insurance costs.

“Four out of five people will be able to find a plan for $10 or less after tax credits,” CMS said.

The boosted tax credits were supposed to expire after this year but have been extended into 2025 by the Inflation Reduction Act.

The 2022 coverage year saw a record 14.5 million signups. The latest open enrollment for HealthCare.gov for 2023 coverage will run through Jan. 15.

Patients at North Carolina-based Atrium Health get what looks like an enticing pitch when they go to the nonprofit hospital system’s website: a payment plan from lender AccessOne. The plans offer “easy ways to make monthly payments” on medical bills, the website says. You don’t need good credit to get a loan. Everyone is approved. Nothing is reported to credit agencies.

In Minnesota, Allina Health encourages its patients to sign up for an account with MedCredit Financial Services to “consolidate your health expenses.” In Southern California, Chino Valley Medical Center, part of the Prime Healthcare chain, touts “promotional financing options with the CareCredit credit card to help you get the care you need, when you need it.”

As Americans are overwhelmed with medical bills, patient financing is now a multibillion-dollar business, with private equity and big banks lined up to cash in when patients and their families can’t pay for care. By one estimate from research firm IBISWorld, profit margins top 29% in the patient financing industry, seven times what is considered a solid hospital margin.

Hospitals and other providers, which historically put their patients in interest-free payment plans, have welcomed the financing, signing contracts with lenders and enrolling patients in financing plans with rosy promises about convenient bills and easy payments.

For patients, the payment plans often mean something more ominous: yet more debt.

Millions of people are paying interest on these plans, on top of what they owe for medical or dental care, an investigation by KHN and NPR shows. Even with lower rates than a traditional credit card, the interest can add hundreds, even thousands of dollars to medical bills and ratchet up financial strains when patients are most vulnerable.

Robin Milcowitz, a Florida woman who found herself enrolled in an AccessOne loan at a Tampa hospital in 2018 after having a hysterectomy for ovarian cancer, said she was appalled by the financing arrangements.

“Hospitals have found yet another way to monetize our illnesses and our need for medical help,” said Milcowitz, a graphic designer. She was charged 11.5% interest — almost three times what she paid for a separate bank loan. “It’s immoral,” she said.

MedCredit’s loans to Allina patients come with 8% interest. Patients enrolled in a CareCredit card from Synchrony, the nation’s leading medical lender, face a nearly 27% interest rate if they fail to pay off their loan during a zero-interest promotional period. The high rate hits about 1 in 5 borrowers, according to the company.

For many patients, financing arrangements can be confusing, resulting in missed payments or higher interest rates than they anticipated. The loans can also deepen inequalities. Lower-income patients without the means to make large monthly payments can face higher interest rates, while wealthier patients able to shoulder bigger monthly bills can secure lower rates.

More fundamentally, pushing people into loans that threaten their financial health runs against medical providers’ first obligation to not harm their patients, said patient advocate Mark Rukavina, program director at the nonprofit Community Catalyst.

“We’re dealing with sick people, scared people, vulnerable people,” Rukavina said. “Dangling a financial services product in front of them when they’re concerned about their care doesn’t seem appropriate.”

Debt upon debt for patients, as finance firms get a cut of payments

Nationwide, about 50 million people — or 1 in 5 adults — are on a financing plan to pay off a medical or dental bill, according to a KFF poll conducted for this project. About a quarter of those borrowers are paying interest, the poll found.

Increasingly, those interest payments are going to financing companies that promise hospitals they will collect more of their medical bills in exchange for a cut.

Hospital officials defend these arrangements, citing the need to offset the cost of offering financing options to patients. Alan Wolf, a spokesperson for the University of North Carolina’s hospital system, said that the system, which reported $5.8 billion in patient revenue last year, had a “responsibility to remain financially stable to assure we can provide care to all regardless of ability to pay.” UNC Health, as it is known, has contracted since 2019 with AccessOne, a private equity-backed company that finances loans for scores of hospital systems across the country.

This partnership has had a substantial impact on patient debt, according to a KHN analysis of billing and contracting records obtained through public records requests.

Most patients in 2019 were in no-interest payment plans

UNC Health, which as a public university system touts its commitment “to serve the people of North Carolina,” had long offered payment plans without interest. And when AccessOne took over the loans in September 2019, most patients were in no-interest plans.

That has steadily shifted as new patients enrolled in one of AccessOne’s plans, several of which have variable interest rates that now charge 13%.

In February 2020, records show, just 9% of UNC patients in an AccessOne plan were in a loan with the highest interest rate. Two years later, 46% were in such a plan. Overall, at any given time more than 100,000 UNC Health patients finance through AccessOne.

The interest can pile on debt. Someone with a $7,000 hospital bill, for example, who enrolls in a five-year financing plan at 13% interest will pay at least $2,500 more to settle that debt.

How a short-term solution ‘leads to longer-term problems’

Rukavina, the patient advocate, said adding this burden on patients makes little sense when medical debt is already creating so much hardship. “It may seem like a short-term solution, but it leads to longer-term problems,” he said. Health care debt has forced millions of Americans to cut back on food, give up their homes, and make other sacrifices, KHN found.

UNC Health disavowed responsibility for the additional debt, saying patients signed up for the higher-interest loans. “Any payment plans above zero-interest terms/conditions in place with AccessOne are in place at the request of the patient,” Wolf said in an email. UNC Health would only provide answers to written questions.

UNC Health’s patients aren’t the only ones getting routed into financing plans that require substantial interest payments.

At Atrium Health, a nonprofit system with roots as Charlotte’s public hospital that reported more than $7.5 billion in revenues last year, as many as half of patients enrolled in an AccessOne loan were in one of the company’s highest-interest plans, according to 2021 billing records analyzed by KHN.

At AU Health, Georgia’s main public university hospital system, billing records obtained by KHN show that two-thirds of patients on an AccessOne plan were paying the highest interest rate as of January.

A finance firm calls such loans ’empathetic patient financing’

AccessOne chief executive Mark Spinner, who in an interview called his firm a “compassionate, empathetic patient financing company,” said the range of interest rates gives patients and medical systems valuable options. “By offering AccessOne, you’re creating a much safer, more mission-aligned way for consumers to pay and help them stay out of medical debt,” he said. “It’s an alternative to lawsuits, legal action, and things like that.”

AccessOne, which doesn’t buy patient debt from hospitals, doesn’t run credit checks on patients to qualify them for loans. Nor will the company report patients who default to credit bureaus. The company also frequently markets the availability of zero-interest loans.

Some patients do qualify for no-interest plans, particularly if they have very low incomes. But the loans aren’t always as generous as company and hospital officials say.

AccessOne borrowers who miss payments can have their accounts returned to the hospital, which can sue them, report them to credit bureaus, or subject them to other collection actions. UNC Health refers unpaid bills to the state revenue department, which can garnish patients’ tax refunds. Atrium’s collections policy allows the hospital system to sue patients.

Because AccessOne borrowers can get low interest rates by making larger monthly payments, this financing system can also deepen inequalities. Someone who can pay $292 a month on a $7,000 hospital bill, for example, could qualify for a two-year, interest-free plan. But a patient who can pay only $159 a month would have to take a five-year plan with 13% interest, according to AccessOne.

“I see wealthier families benefiting,” said one former AccessOne employee, who asked not to be identified because she still works in the financing industry. “Lower-income families that have hardship are likely to end up with a higher overall balance due to the interest.”

Andy Talford, who oversees patient financial services at Moffitt Cancer Center in Tampa, said the hospital contracted with AccessOne to make it easier for patients to manage their medical bills. “Someone out there is helping them keep track of it,” he said.

But patients can get tripped up by the complexities of managing these plans, consumer advocates say. That’s what happened to Milcowitz, the graphic designer in Florida.

Milcowitz, 51, had set up a no-interest payment plan with Moffitt to pay off $3,000 she owed for her hysterectomy in 2017. When the medical center switched her account to AccessOne, however, she began receiving late notices, even as she kept making payments.

Only later did she figure out that AccessOne had set up two accounts, one for the cancer surgery and another for medical appointments. Her payments had been applied only to the surgery account, leaving the other past-due. She then got hit with higher interest rates. “It’s crazy,” she said.

Lenders see a growing business opportunity

While financing plans may mean more headaches and more debt for patients, they’re proving profitable for lenders.

That’s drawn the interest of private equity firms, which have bought several patient financing companies in recent years. Since 2017, AccessOne’s majority owner has been private equity investor Frontier Capital.

Synchrony, which historically marketed its CareCredit cards in patient waiting rooms, is now also inking deals with medical systems to enroll patients in loans when they go online to pay bills.

“They’re like pilot fish eating off the back of the shark,” said Jonathan Bush, a founder of Athenahealth, a health technology company that has developed electronic medical records and billing systems.

As patient bills skyrocket, hospitals face mounting pressure to collect more, which can make financing arrangements seem appealing, industry experts say. But as health systems go into business with lenders, many are reluctant to share details. Only a handful of hospitals contacted by KHN agreed to be interviewed about their contracts and what they mean for patients.

Several public systems, including Atrium and UNC Health, disclosed information only after KHN submitted public records requests. Even then, the two systems redacted key details, including how much they pay AccessOne.

AU Health, which did not redact its contract, pays AccessOne a 6% “servicing fee” on each patient loan the company administers. But like Atrium and UNC Health, AU Health refused to provide any on-the-record interviews.

Other hospital systems were even less transparent. Mercyhealth, a nonprofit with hospitals and clinics in Illinois and Wisconsin that routes its patients to CareCredit, would not discuss its lending practices. “We do not have anyone available for this,” spokesperson Therese Michels said. Allina Health and Prime Healthcare also wouldn’t talk about their patient financing deals.

Bush said there’s a reason so few hospitals want to discuss their financing deals: They’re embarrassed. “It’s like they quietly write someone’s name on a piece of paper and slide it across the table,” he said. “They don’t want to be a part of it because they have in their institutional memory that they are supposed to look after patients’ best interests.”

Some hospitals and banks still offer interest-free help

Not all hospitals expose their patients to extra costs to finance medical bills.

Lake Region Healthcare, a small nonprofit with hospitals and clinics in rural Minnesota that contracts with Missouri-based Commerce Bank, charges no interest or fees on payment plans. That’s a decision that spokesperson Katie Johnson said was made “for the benefit of our patients.”

Even some AccessOne clients such as the University of Kansas Health System shield patients from interest. But as providers look to boost their bottom lines, it’s unclear how long these protections will last. Colette Lasack, who oversees financing for the Kansas system, noted: “There’s a cost associated with that.”

Meanwhile, large national lenders such as Discover Financial Services are looking at the patient financing business.

“I’ve had to become more of a health care marketer,” said Matt Lattman, vice president for personal loans at Discover, which is pitching the loans to people with unexpected medical bills. “In a world where many people are ill prepared to cover their health care costs, the personal loan can provide an opportunity.”

The Department of Health and Human Services (HHS) appears set to extend the federal COVID PHE past its current expiration date of January 11, 2023, as HHS had promised to give stakeholders at least 60 days’ notice before ending it, and that deadline came and went on November 11th. Days later the Senate voted to end the PHE, a bill which Biden has promised to veto should it reach his desk. Measures set to expire with the PHE, or on a several month delay after it ends, include Medicare telehealth flexibilities, continuous enrollment guarantees in Medicaid, and boosted payments to hospitals treating COVID patients.

The Gist: Despite growing calls to end the PHE declaration, and even as White House COVID coordinator Dr. Ashish Jha has said another severe COVID surge this winter is unlikely, the White House is likely trying to buy time to resolve the complicated issues tied to the PHE, some of which must be dealt with legislatively.

And with a divided Congress ahead, it remains to be seen how these issues, especially Medicare telehealth flexibilities—a topic of bipartisan agreement—are sorted out. Meanwhile the continuation of the PHE prevents states from beginning Medicaid re-determinations, allowing millions of Americans to avoid being disenrolled.

While the final balance of the House and Senate are still unknown after Tuesday’s midterm elections, both chambers are expected to be narrowly divided.

Ballot initiatives on reproductive health produced more unambiguous results, with three states—California, Michigan, and Vermont—amending their constitutions to affirm reproductive rights, and two states—Kentucky and Montana—voting down proposals that would have imposed greater legal barriers to abortion access. South Dakota became the seventh, and likely final, state to expand Medicaid via ballot initiative, making an additional 28K South Dakotans eligible for coverage, and reducing the number of states that have yet to expand Medicaid to 11.

The Gist: Democrats beat expectations, bucking historical trends in which midterm voters swing strongly against the President’s party. But healthcare did not feature prominently in voters’ choices, with this being the first election in over a decade where the state of the Affordable Care Act and protecting individuals’ access to care and coverage was not a significant choice driver.

The fallout from the Supreme Court’s decision in June to overturn Roe v. Wade had a clear impact on voter turnout, with abortion tying inflation for voters’ top concern in exit polls. At the state level, South Dakota voters approved Medicaid expansion, where over 40 percent of the state’s uninsured adults could now gain access to coverage—another clear sign that voters, regardless of party affiliation, are behind the ACA’s expanded vision for the safety net program.

Moving forward, a closely divided Congress is unlikely to take on significant healthcare legislation, regardless of who ultimately holds the House and Senate.