Cartoon – In Denial

https://mailchi.mp/cd392de550e2/the-weekly-gist-october-21-2022?e=d1e747d2d8

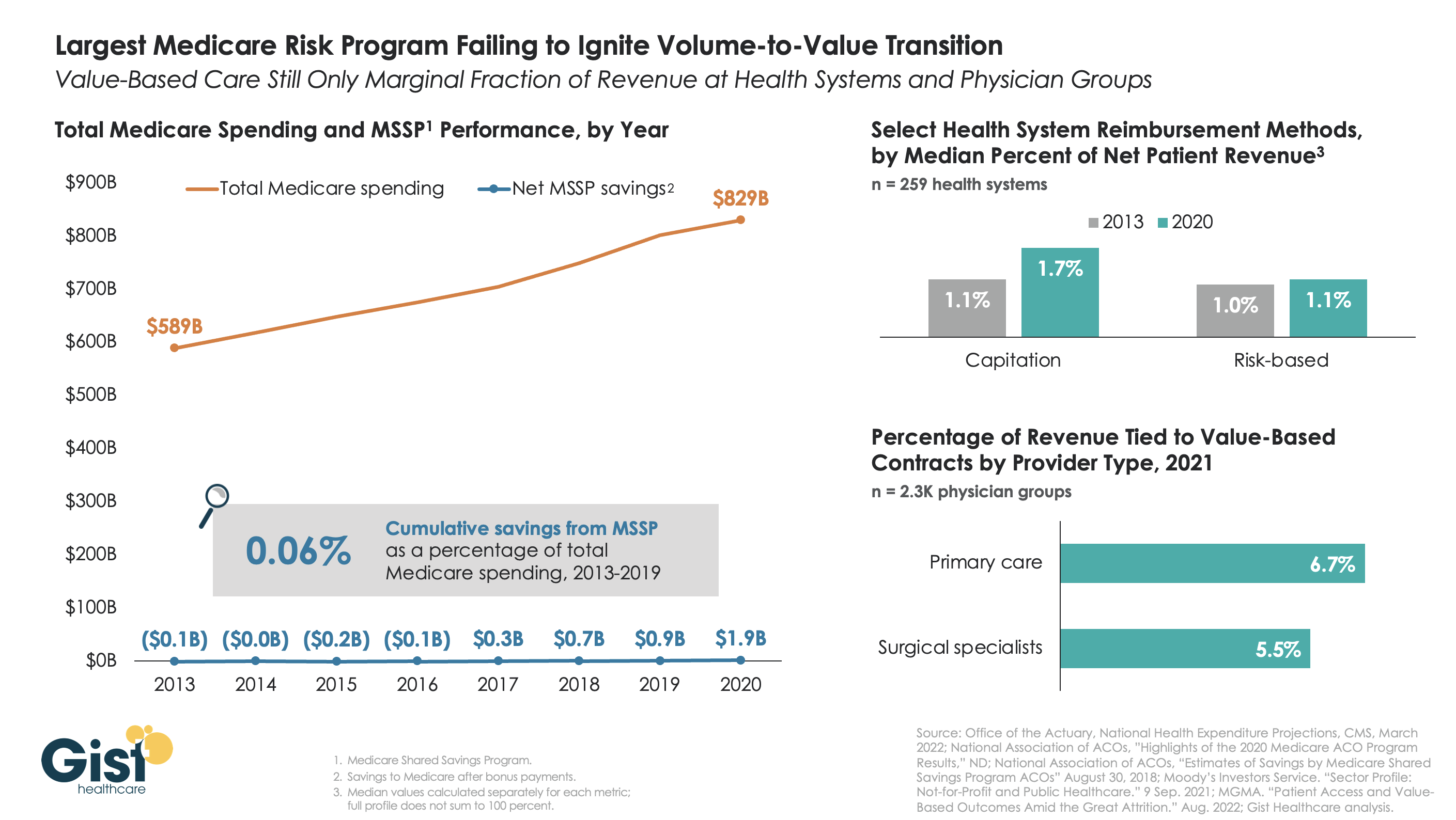

The belief that healthcare should, and would, transition from “volume to value” was a key pillar of the Affordable Care Act (ACA). However, with more than a decade of experience and data to consider, there is little indication that either Medicare or the healthcare industry at large has meaningfully shifted away from fee-for-service payment. Using data from the National Association of Accountable Care Organizations, the graphic below shows that the Medicare Shared Savings Program (MSSP)—the largest of the ACA’s payment innovations, with over 500 accountable care organizations (ACOs) reaching 11M assigned beneficiaries—has led to minimal savings for Medicare. In its first eight years, MSSP saved Medicare only $3.4B, or a paltry 0.06 percent, of the $5.6T that it spent over that time.

Policymakers had hoped that a Medicare-led move to value would prompt commercial payers to follow suit, but that also hasn’t happened. The proportion of payment to health systems in capitated or other risk-based arrangements barely budged from 2013 to 2020—remaining negligible for most organizations, and rarely amounting to enough to influence strategy. The proportion of risk-based payment for doctors is slightly higher, but still far below what is needed to enable wholesale change in care across a practice.

While Medicare has other options if it wants to increase value-based payment, like making ACOs mandatory, it’s harder to see how the trend in commercial payment will improve, as large payers, who are buying up scores of care delivery assets themselves, seem to have little motivation to deal providers in on risk.

While financial upside of moving to risk hasn’t been significant enough to move the market to date, we aren’t suggesting health systems throw out their population management playbook—to meet mounting cost labor pressures, systems must deliver lower cost care, in lower cost settings, with lower cost staff, just to maintain economic viability moving forward.

https://www.advisory.com/daily-briefing/2022/10/19/cash-pay-hospitals

Amid new price transparency laws and growing consumer demand, more hospitals are adding cash pay options for certain health care services instead of just accepting insurance, Nora Tepper writes for Modern Healthcare—and some hospital officials say these offerings are “only going to go up” in the future.

Providers advertising cash pay rates for their services used to be considered an “anomaly,” Tepper writes. Now, the No Surprises Act, the federal price transparency law, and changing consumer expectations may make cash-only payments for health care services more common.

“The market is going there,” said Larry Van Horn, associate professor of management, law, and health policy and executive director of health affairs at Vanderbilt University. “You’ve got direct primary care, you’ve got physicians going and moving into cash pay. You’re gonna have to sit there at some point and say, ‘Wait a minute, they’re taking my business.'”

Although some hospitals and health systems that serve certain populations—such as Pomerene Hospital in Ohio with Amish and Anabaptist patients and the University of Texas MD Anderson Cancer Center with medical tourists—have long had cash-pay systems, it is still a relatively new concept for most providers in the United States.

According to data from Medscape, which surveyed more than 17,000 clinicians, just 17% of clinicians used cash-only, concierge, or direct-pay primary care models in 2020. Primary care providers (PCPs) made up the largest proportion of providers accepting cash pay, with 10% of practices charging patients a flat monthly fee for unlimited services.

“[S]ome providers embracing the cash pay revolution say their bottom line benefits from faster reimbursement, lower administration costs and higher patient retention,” Tepper writes.

In a 2020 report from the Society of Actuaries, almost all PCPs who operated under self-pay models reported “better or much better” personal and professional satisfaction compared to those under a traditional fee-for-service system. In addition, 34% of respondents reported “better or much better” earnings under a direct payment model.

According to Tepper, hospitals generally offer self-paying patients, who have typically been uninsured individuals or those with high-deductible health plans, lower rates for services compared to commercial insurers since they don’t have to handle administrative work or collections.

In a 2021 study published in JAMA Network Open, researchers analyzed rates for “shoppable” services at 922 hospitals and found that the proportion of hospitals that had lower cash prices than their median commercial negotiated rate ranged from 38.4% for liver tests to 68.5% for C-sections.

During the pandemic, more insured patients began to inquire about what services they could pay cash for, leading some health systems to create new payment models for certain procedures.

For example, Deaconess Health System launched an in-house bundled payment program, which includes cardiology, radiology, and urgent care services, in July 2020. The first year, the health system sold 130 bundled services, which increased to 351 in 2021, and 489 as of August 2022.

For any services not covered by the program, Deaconess offers a 50% discount on cash payments compared to its insurer rate. However, self-paying patients are required to pay the full cost of a procedure upfront.

“The patient has decided to take a bet on themselves,” said Steve Russell, VP and chief revenue cycle officer at Deaconess. “They have a high deductible, they don’t think they’re going to reach that threshold and their thought is, ‘If I don’t use my insurance, what kind of discount can you give me?'”

Separately, CommonSpirit Health‘s Catholic Health Initiatives (CHI) launched its own bundled cash price program in 2018 after noticing that many patients with high-deductible plans would defer care due to affordability concerns. The health system also advertises and sells its services on MDsave, an online marketplace that allows consumers to shop for health care procedures.

“With the No Surprises Act and the price transparency regulations, this has to be something that we offer,” said Jeanette Wojtalewicz, SVP and CFO at CHI Health’s Midwest division. “You’ll see more of this coming.”

According to Aaron Miri, SVP and chief digital and information officer at Baptist Health South Florida, although few patients are currently paying directly for health care services, the industry is heading towards that direction, which means health systems need to be prepared to meet the demand.

“When you look at the directionality of demand, this is only going to go up,” Miri said. “Patients are going to start seeing their total estimated bill and say, ‘I want to spend my $500 at a health system that was really transparent with me, and made me feel comfortable, versus the health system down the road that I’ve always gone to, but that simply can’t tell me what my actual amount due is.”

To make it easier for patients to directly pay for procedures, some health systems, including Baptist Health, have updated their payment options by adding Apple Pay, Google Pay, or other online payment systems instead of just accepting payment in-person or by phone.

However, even as direct payment models become more common, some insurers are “using their leverage to slow adoption of cash pay,” Tepper writes.

Kimberly Scaccia, VP of revenue management at MercyHealth, said some of the health system’s contracts with insurers prohibit it from offering cash discounts to insured patients.

“Some of the smaller payers, they’re fine with removing [cash pay restrictions],” Scaccia said. “Some of the very, very large payers, they simply will not allow it.”

In addition, Matthew Fiedler, a senior fellow of economic studies at the USC-Brookings Schaeffer Initiative for Health Policy, said clinicians may also be concerned about insurers asking to pay the lower cash rate during contract renewals or jeopardizing a provider’s network position.

“An insurer could say, ‘We’re gonna put this provider out-of-network, but we’re gonna put them in a preferred out-of-network position in our benefit design, where the cost-sharing is not that onerous, because we know they have this really good cash price,'” Fiedler said.

https://mailchi.mp/4587dc321337/the-weekly-gist-october-14-2022?e=d1e747d2d8

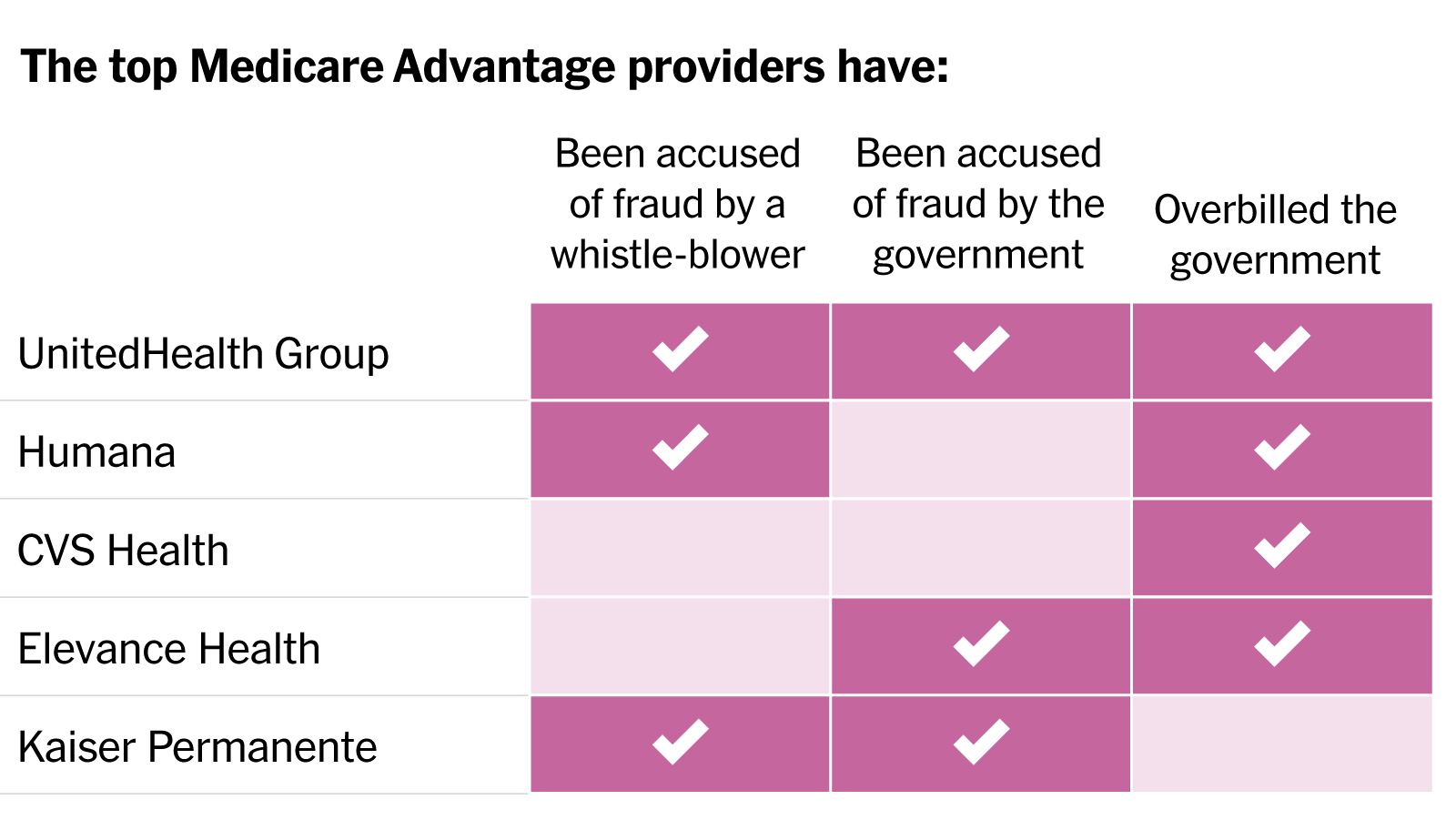

In a blistering article published in the New York Times, reporters Reed Abelson and Margot Sanger-Katz detail widespread fraud allegations involving the nation’s largest MA insurers. Nine of the ten largest plans have been accused by the government of fraud or overbilling, generally for upcoding practices that exaggerate the disease burden among their beneficiaries, without providing them more care. Insurers have disputed most allegations, and regulators have been slow to punish known infractions. As a growing steam of seniors continue the enter the program, aggressive risk adjustment has significantly increased the government’s costs. The Centers for Medicare and Medicaid Services has yet to reduce payments in response to overbilling, despite having the power to do so.

The Gist: While these practices were well known to many in the healthcare industry, MA’s growth—set to overtake traditional Medicare enrollment next year—has added a spotlight worthy of national attention. While many beneficiaries report being satisfied with their MA benefits, the program was also intended to improve the cost efficiency of senior care.

With payers gaming the system to garner record profits, the government has seen higher per-enrollee spending in MA compared to traditional Medicare. There are some signs that the strings are starting to tighten for insurers, as many of the largest are losing Medicare star bonuses in 2023, impacting both plan revenue and ability to market throughout the year. However, reduced quality bonuses change nothing about the underlying MA payment structure, and could even drive insurers to more profit-seeking behavior.

https://mailchi.mp/e60a8f8b8fee/the-weekly-gist-september-23-2022?e=d1e747d2d8

On Monday, a federal judge denied the Department of Justice (DOJ)’s attempt to block UHG’s $13B purchase of Change Healthcare, a technology firm specializing in claims processing and data analytics.

The DOJ sought to block the purchase on antitrust grounds, arguing that UHG would have access to technologies that its rivals use to compete, but the judge, writing in a sealed ruling, found the DOJ’s case inadequate. It is unclear at this point whether the DOJ will appeal.

Change will now join UHG’s OptumInsight division, though in response to anticompetitive concerns, the ruling ordered UHG to sell part of Change’s claims payment and editing business, as it had already planned to do.

The Gist: Antitrust regulators have had much greater success at challenging horizontal healthcare mergers but have struggled to find solid footing to fight vertical deals.

The UHG-Change case was closely watched in part because of the precedent it would have set in terms of holding “platform” aggregators in check. As UHG and other healthcare titans continue to acquire assets up and down the value chain (physician practices, ambulatory surgery centers, clinics, telehealth capabilities, risk products), it’s increasingly clear that the government will face an uphill climb to question the competitive effects of these vertical M&A activities.

https://mailchi.mp/6a3812741768/the-weekly-gist-september-9-2022?e=d1e747d2d8

The nation’s largest retailer and its largest insurer announced a 10-year partnership to bring together the collective expertise of both companies to provide affordable healthcare to potentially millions of Americans. Set to start next year with 15 Walmart Health locations in Georgia and Florida, the collaboration will initially focus on seniors and Medicare Advantage (MA) beneficiaries, and will include a co-branded MA plan in Georgia. Walmart Health Virtual Care will also be in-network for some UnitedHealthcare beneficiaries. Plans for future years involve expanding the collaboration across commercial and Medicaid plans, as well as including pharmacy, dental, and vision services.

The Gist: We have long wondered if this powerhouse pairing was in the works, as this kind of partnership makes a lot of sense for both parties. While Walmart has reportedly been considering an insurance company acquisition for years, and more recently been dabbling in its own insurance efforts, partnering with UHG provides the retailer with a share of the upside potential of getting into the insurance market without having to fully commit to entering that complex business. And given that 90 percent of Americans live within 10 miles of a Walmart store, and more than half of Americans visit a store every week, Walmart provides UHG with low-cost healthcare access points all over the country, especially important in markets where United’s own Optum physician network is not (yet) present.

Radio Advisory’s Rachel Woods sat down with Advisory Board’s Sarah Hostetter and Vidal Seegobin to discuss the good and bad elements of private equity and what leaders can do to make it a valuable partner to their practices.

Private equity (PE) tends to get a bad rap when it comes to health care. Some see it as a disruptive force that prioritizes profits over the patient experience, and that it’s hurting the industry by creating a more consolidated marketplace. Others, however, see it as an opportunity for innovation, growth, and more movement towards value-based care.

Radio Advisory’s Rachel Woods sat down with Advisory Board‘s Sarah Hostetter and Vidal Seegobin to discuss the good and bad elements of PE and what leaders can do to make it be a valuable partner to their practices.

Read a lightly edited excerpt from the interview below and download the episode for the full conversation. https://player.fireside.fm/v2/HO0EUJAe+KzkqmeWH?theme=dark

Rachel Woods: Clearly there are a lot of feelings about private equity. I’m frankly not that surprised, because the more we see PE get involved in the health care space, we hear more negative feelings about what that means for health care.

Frankly, this bad guy persona is even seen in mainstream media. I can think of several cable medical dramas that have made private equity, or maybe it’s specific investors, as the literal enemy, right? The enemy of the docs that are the saviors of their hospital or ER or medical practice. Is that the right way we should be thinking about private equity? Are they the bad guy?

Sarah Hostetter: The short answer is no. I think private equity is a scapegoat for a lot of the other problems we’re seeing in the industry. So the influx of money and where it’s going and the influence that that has on health care. I think private equity is a prime example of that.

I also think the horror stories all get lumped together. So we don’t think about who the PE firm is or what is being invested in. We put together physician practices and health systems and SNPs, and we lump every story all together, as opposed to considering those on their individual merits.

Woods: And feeds to this bad guy kind of persona that’s out there.

Hostetter: Yeah. And like you said, the media doesn’t help, right? If the average consumer is watching and seeing different portrayals or lumped portrayals, it’s not helping.

Vidal Seegobin: Private equity, as all actors in our complex ecosystem, is not a monolith, and no one has the monopoly on great decisions in health care, nor do they have a monopoly on the bad decisions in health care. And so if you attribute a bad case to private equity, then you also have to attribute the positive returns done from a private equity investment as well.

Hostetter: Agree with what Vidal’s saying, but bottom line is that every stakeholder is not going to have the same outcomes or ripple effects from a private equity deal. It really depends on the deal itself, the market, and the vantage points that you take.

Woods: I want to actually play out a scenario with the two of you and I want you to talk about the positive and the potentially negative consequences for different sectors or different stakeholders.

So let’s take the newest manifestation that Sarah, you talked to us through. Let’s say that there is a PE packed multi-specialty practice heavily in value-based care. That practice starts to get bigger. They acquire other practices, including maybe even some big practices in a market and they start employing all of the unaffiliated or loosely affiliated practices in the market.

I am guessing that every health system leader listening to this episode is already starting to sweat. What does this mean for the incumbent health system?

Seegobin: So I think one thing that’s going to be pretty clear is that size does confer clear advantages and health care is part and parcel that kind of benefit. What I think is challenging is when we’re entering into a moment where access to capital is challenging for health systems in particular and we’re going to need to scale up investments, health systems could see themselves falling further and further behind as private equity makes smart investments into these practices to both capture and retain volume. And as a consequence of that, reduces the amount of inpatient demand or the demand to their bread and butter services.

Hostetter: And I think it’s really important that you phrase the question, Rae, as health system. Because we so often equate health system and hospital.

But a health system includes lots of hospitals, it includes ambulatory facilities, a range of services. And so I think for systems to equate health system and hospital, it’s really hard when any type of super practice or large backed practice comes into the market.

Whether we are talking about a plan backed practice, a PE backed practice, or just a really large independent group. There are pressures on health systems who think of their job or their primary service as the hospital. And there is a moment where the power dynamics can shift in markets away from the health system, if they aren’t able to pivot their strategy beyond just the hospital.

Woods: Which is exactly why health systems see this scenario as, let’s just say it, threatening. Sarah, then how do the physicians feel? Do they have the opposite feelings as the incumbent health systems?

Hostetter: There’s a huge range. Private equity is incredibly polarizing in the physician practice world, the same way that it is in other parts of the industry. So I think there is a hope from some practices that private equity is a type of investor that is aligned with them.

Physicians who go into private practice historically tend to be more entrepreneurial. They are shareholders in their own practice, so there are some natural synergies between private equity, business minded folks, and these physicians.

Also, even though I go into a small business, it takes a lot to run a small business, so there are potentially welcome synergies and help that you can get from a PE firm. On the flip side of that, there are groups who would never in a million years consider taking a private equity investment and are unwilling to have these conversations.

Woods: There is a tendency, especially in the conversation that we’re having, for folks to think about private equity as being something that primarily impacts the provider space, at least when it comes to health care. But I’m not sure that that’s actually true. So what consequences, good or bad, might the payers feel? Might the life sciences companies feel?

Seegobin: So one common refrain when talking about private equity and their acquisition or partnering with traditional health care businesses like physician practices is that they are immediately focused on cutting costs. So they are going to consolidate all of the purchasing contracts, they are going to make pretty aggressive decisions about real estate, all the types of cost components that run the business.

Now, if you are a kind of life sciences or a diagnostic business for whom you would depend on being an incumbent in those contracting decisions, you’re worried that the private equity is either going to direct you to a lower cost provider, or in many cases, another business that the private equity firm owns as well, right?

They would love to keep synergies within the portfolio of businesses that they’ve acquired and they partner. So if you were relying on incumbent or historical purchasing practices with these physician practices, it can be disrupted, depending on the arrangement.

Hostetter: And then I think there’s a range of potential implications for payers. So you have some payers who themselves are aggregating independent practices, and they’re targeting the same type of practices that the PE firms that are betting on value-based care are targeting. They are targeting primary care groups who are big in Medicare Advantage. So there’s some inherent competition potentially for the physician practice landscape there.

Woods: Well, and I think they’re trying to offer the same thing, right? They’re trying to offer capital. They’re trying to do that with the promise of autonomy. And they’re coming up against a competitive partner that is saying, “I can do both of those things and I can do it better and faster.”

Hostetter: Yeah. And both of them are saying we can do it better and faster than hospitals. That’s the other thing, right?

Woods: Which, that part is probably true.

Hostetter: Yeah. Their goals are aligned and they believe they can get there different ways. And I think autonomy is a big sticking point here for me or a big bellwether for me, because I think whoever can get to value-based care while preserving autonomy is going to win. You have to have some level of standardization to do value-based care well. You can’t just let everyone do whatever they want. You need high quality results for lower cost. That inherently requires standardization. So who can thread the needle of getting that standardization while preserving a degree of autonomy?

It’s fascinating, as we’ve had this call, it was suggested multiple times that payers actually might be the end of the line for some of these PE deals. That there’s a lot of alignment between what payers are trying to do with their aggregation and what PE firms who are investing in primary care do, and hey, payers have a lot of money too. So could we actually see some of these PE deals end with a payer acquisition? Because they’re trying to achieve similar things, just differently.

https://mailchi.mp/11f2d4aad100/the-weekly-gist-august-12-2022?e=d1e747d2d8

According to a Wall Street Journal report, CVS is expected to submit a bid to purchase Dallas-based Signify Health, which supports physicians, payers, and health systems with tools and technology to provide in-home care. Signify acquired accountable care organization manager Caravan Health earlier this year. Last week, the Journal reported that Signify, valued at more than $4B, was looking for buyers. While CVS is said to be interested, so are private equity firms and other managed care companies.

The Gist: CVS CEO Karen Lynch told investors during last week’s earnings call that the company plans to grow its primary care and home health offerings through mergers and acquisitions. The Signify bid, along with reports that CVS considered acquiring concierge primary care company One Medical, suggests that the retail pharmacy and insurance giant is charging ahead with its strategy of creating a vertically-integrated healthcare company.

As several newly public digital health and value-based care companies have seen share prices plummet and capital dry up in a cooling economy, they are becoming targets for large insurers and tech companies who have seen their own fortunes grow during the pandemic. Watch for more announcements from these “platform assemblers” in the months to come.

All but two of the seven largest insurers saw profits climb in the second quarter as hospital operators continued to struggle with weak volumes and higher labor costs.

The nation’s top health insurers again raised financial targets for the year as revenues climbed on increased membership, while some signs indicated demand for medical services was tepid.

All but two of the seven largest insurers saw profits climb in the second quarter compared with the prior-year period, as many saw a key metric for medical spending decrease.

Industry observers have been closely watching for signals of pent-up demand as many patients delayed care amid the varying spikes in COVID-19 cases.

That didn’t seem to materialize in the second quarter as insurance executives didn’t report a surge in care. Almost all insurers saw their medical loss ratios either decline or remain the same from the second quarter last year.

Executives at Cigna, one of the nation’s largest insurers with nearly 18 million members, said there were fewer surgeries, fewer emergency room visits and fewer people admitted to the hospital in the second quarter compared to the prior-year period.

Direct COVID-19 costs were also better-than-expected, Cigna executives told investors on the second-quarter earnings call. As fewer Cigna patients sought medical care, net income climbed 6% to $1.6 billion.

Cigna wasn’t alone in reporting lighter patient volumes.

UnitedHealthcare, the insurer arm of UnitedHealth Group with more than 51 million members, reported a lower level of COVID-19 patient care and said usage of some medical services still fell below pre-pandemic levels, including pediatrics and the emergency department. UnitedHealth’s net income increased to $5.1 billion.

Humana also noticed a dip in members utilizing medical services, noting fewer Medicare members were admitted to the hospital in the quarter. Humana’s net income also climbed 18% to $696 million.

Q2 performances led insurers to raise their financial expectations for the full year.

“The lower utilization trends and lack of COVID-19 headwinds seen to date, give us confidence in raising our full year adjusted [earnings per share] guide,” Humana CFO Susan Diamond said on a call with investors.

On the other hand, the nation’s for-profit hospital chains reported fewer admissions and a dip in profits as they continued to deal with labor and other expenses amid record high inflation.

“U.S. hospitals and health systems are now halfway through an extremely challenging year,” Kaufman Hall said in a recent report that showed six consecutive months of negative operating margins.

Fitch Ratings revised its ratings outlook to negative from stable for Community Health Systems following the hospital chain’s second-quarter results.

Fitch said the revision reflects “significant increases in labor costs and weakness in volume” throughout the first half of the year.

Nonprofit hospital operators have also faced challenges in the first half of the year.

Both Kaiser Permanente and Sutter Health reported net losses in the second quarter of the calendar year as expenses grew and investment income declined.

https://mailchi.mp/efa24453feeb/the-weekly-gist-july-22-2022?e=d1e747d2d8

After a few years of relatively unchanged monthly premiums, a Kaiser Family Foundation analysis of 72 rate filings for 2023 finds a median 10 percent increase. Insurers say the biggest driver is rising medical costs, driven by higher rates for provider services and pharmaceuticals, as well as a return to pre-pandemic utilization levels. Insurers aren’t expecting COVID-19 or federal policy changes—including a potential extension of enhanced subsidies—to have much of an impact on rates.

The Gist: High inflation and the growing wage-price spiral have left providers with much higher costs, which is sure to drive up the overall cost of healthcare. Where provider systems have the leverage to demand higher rates from insurers, this will inevitably drive up premiums—an effect that is already starting to show up in the individual insurance market.

If Congressional Democrats are able to extend ACA subsidies, most ACA enrollees won’t actually feel these premium increases, but as contracts in the group market come up for renewal, we’d expect inflation in employer-sponsored premiums as well. Given the cost-sharing now built into most benefit plans, individual consumers will likely see healthcare join gas, food, and housing as household costs that are experiencing unsustainable inflationary increases.