Health insurers are starting to notify states that tariffs will drive up the premiums they plan to charge individual and small group market enrollees next year.

Why it matters:

The Trump administration’s trade policy is adding another layer of uncertainty for health costs as Congress considers Medicaid cuts and is expected to sunset enhanced subsidies for Affordable Care Act coverage.

“There are sort of a perfect storm of factors that are driving prices up,” said Sabrina Corlette, research professor at Georgetown’s Center on Health Insurance Reforms.

The big picture:

Health insurers calculate monthly premiums in advance of each year based on the expected price of goods and services and projected demand for them.

Tariffs announced by President Trump are expected to drive up the cost of prescription drugs, medical devices and other medical products and services. Some of that difference ultimately would be passed down to enrollees.

Where it stands:

A handful of health insurers administering individual and small group plans have already explicitly told state regulators that tariffs are forcing plans to raise enrollee premiums more than they otherwise would next year, KFF policy analyst Matt McGough wrote in an analysis published Monday.

Independent Health Benefits Corporation told New York regulators in a filing last month that it plans to raise premiums for its individual market enrollees 38.4% next year.

About 3% of that is directly due to tariffs, based on projections of how much they’ll increase drug prices and the use of imported drugs, Frank Sava, a spokesperson for Independent Health, told Axios.

Similarly, UnitedHealthcare of Oregon said in a filing that nearly 3% of its planned 19.8% premium increase for small group enrollees next year is due to uncertainty around tariffs, particularly on how they’ll affect pharmaceutical prices.

Insurers “don’t have any historical precedent or data to project what this is going to mean for their business and health costs,” McGough said to Axios. “I think it really makes sense that they’re trying to hedge their bets.”

Insurers can’t change their premiums throughout the year. But if health plans do overshoot their premium estimates in rate filings, they have to pay enrollees back the difference in rebates.

While there may be a competitive advantage to keeping premiums lower, there isn’t really a way for insurers to make up for extra unplanned costs after the fact.

Yes, but:

Some insurers indicated that while they’re keeping a close eye on tariff-related impacts, they aren’t baking them into their premium rates yet.

“There is uncertainty around inflation and the economy due to possible tariffs however we did [not] put anything for this in this filing,” Kaiser Foundation Health Plan of the Northwest’s report to Oregon reads.

State regulators can also push back on insurers’ premium calculations before they’re finalized, McGough noted.

What we’re watching:

While some states have earlier deadlines, insurers have to submit their 2026 ACA marketplace plan rates to the federal regulators by July 16, and proposed rates will be posted by August 1.

That’s when we’ll get a better picture of how seriously tariffs are concerning health insurers.

In the Congressional Budget Office’ latest report on the status of health insurance coverage from the 2023 National Health Interview Survey released last week, a cautiously optimistic picture of coverage is presented:

“In 2023, 25.0 million people of all ages (7.6%) were uninsured at the time of interview. This was lower than, but not significantly different from 2022, when 27.6 million people of all ages (8.4%) were uninsured. Among adults ages 18 64, 10.9% were uninsured at the time of interview, 23.0% had public coverage, and 68.1% had private health insurance coverage.

The percentage of adults ages 18-64 who were uninsured in 2023 (10.9%) was lower than the percentage who were uninsured in 2022 (12.2%).

Among children ages 0–17 years, 3.9% were uninsured, 44.2% had public coverage, and 54.0% had private health insurance coverage.

The percentage of people younger than age 65 with exchange-based coverage increased from 3.7% in 2019 to 4.8% in 2023.”

That represents the highest level of coverage in modern history. Later, it adds important context: The percentage of adults ages 18–64 who were uninsured decreased between 2019 and 2023 for all family income groups shown except for adults in families with incomes greater than 400% FPL. Notably, a period in which the Covid-19 pandemic prompted federal government’s emergency funding so households and businesses could maintain their coverage.

“Among adults with incomes below 100% FPL, the percentage who were uninsured in 2023 (20.2%) was lower than, but not significantly different from, the percentage who were uninsured in 2022 (22.7%).

Among adults with incomes 100% to less than 200% FPL, the percentage who were uninsured decreased from 22.3% in 2022 to 19.1% in 2023.

Among adults with incomes 200% to 400% FPL, the percentage who were uninsured decreased from 14.2% in 2022 to 11.5% in 2023.

No significant difference was observed in the percentage of adults with incomes above 400% FPL who were uninsured between 2022 (4.1%) and 2023 (4.3%).”

In 2023, among adults ages 18–64, the percentage who were uninsured was highest among health insurance coverage of any type was higher for those with higher household income but decreased coverage in 2023 correlated to ethnicity, non-expansion of state Medicaid programs: From 2019 to 2023.”

And decreases in the ranks of the uninsured were noted across all ethnic groups:

Among Hispanic adults, from 29.7% to 24.8%

Among Black non-Hispanic adults, from 14.7% to 10.4% in 2023

Among White non-Hispanic adults, decreased from 10.5% to 6.8%

Among Asian non-Hispanic adults, from 8.8% to 4.4% in 2023.

The New York Times noted “The drops cut significantly into gaps between ethnic groups.The uninsured rate among Black Americans, for example, was almost 8% higher than for white Americans in 2010, and was only 4%higher in 2022. The data points to the broad effects of the Affordable Care Act, the landmark law President Barack Obama signed in 2010 that created new state and federal insurance marketplaces and expanded Medicaid to millions of adults. National uninsured rates have continued to drop in recent years, hitting a record low in early 2023.”

But the report also flags a reversal of the trend: “The uninsured share of the population will rise over the course of the next decade, before settling at 8.9% in 2034, largely as a result of the end of COVID-19 pandemic–related Medicaid policies, the expiration of enhanced subsidies available through the Affordable Care Act health insurance Marketplaces, and a surge in immigration that began in 2022. The largest increase in the uninsured population will be among adults ages 19–44. Employment-based coverage will be the predominant source of health insurance, and as the population ages, Medicare enrollment will grow significantly. After greater-than-expected enrollment in 2023, Marketplace enrollment is projected to reach an all-time high of twenty-three million people in 2025.”

My take:

A close reading of this report suggests its forecast might be overly optimistic. it paints a best-case picture of health insurance coverage that under-estimates the realities of household economics and marketplace trends and over-estimates the value proposition promoted by health insurers to their customers. My conclusion is based on four trends that suggest coverage might slip more than the report suggests:

The affordability of healthcare insurance is increasingly problematic to lower- and middle-income households who face inflationary prices for housing, food, energy and transportation. The CBO report verifies that household income is key to coverage and working age populations are most-at risk of losing its protections. Subsidies to fund premiums for those eligible, employer plans that expose workers to high deductibles and increased non-covered services are likely to push fewer to enroll as premiums become unaffordable to working age adults and unattractive to their employers. As outlined in a sobering KFF analysis, half of the adult population is worried about the affordability of their healthcare—and that includes 48% who have health insurance. And wages in the working age population are not keeping pace with prices for food, shelter and energy, leaving healthcare expenses including their insurance premiums and out-of-pocket obligations at greater risk.

The value proposition for health insurance coverage is eroding among employers, consumers and lawmakers. To large employers that provide employee insurance, medical costs are forcing benefits reduction or cessation altogether. Insurance has not negated their medical costs. To small employers, it’s an expensive bet to recruit and keep their workforce. To government sponsors (i.e. Medicare, Medicaid, VHA, et al), insurance is a necessary but increasingly expensive obligation with growing dependence on private insurers to administer their programs. State and federal regulators are keen to limit public spending and address disparities in their public insurance programs. All recognize that private insurers play a necessary role in the system and all recognize that confidence in health insurance protections is suspect. Thus, increased regulation of private insurers is likely though unwelcome by its members.

Public funding for government payers will be increasingly limited increasing insurer dependence on private capital for sustainability and growth. Funding for Medicare, Medicaid, Veterans and Military Health, Public Health et al are dependent on appropriations and tax collections. All are structured to invite private insurer participation: all are seeing corporate insurers seize market share from their weaker competitors. The issues are complex and controversial as evidenced by the ongoing debates about fairness in Medicare Advantage and administration of Medicaid expansion among others. And polls indicate widespread dissatisfaction with the system and lack of confidence in its insurers, hospitals, physicians or the government to fix it.

Access to private capital for private health insurers is shrinking enabling corporate insurers to play bigger roles in financing and delivering services. Private investments in healthcare services (i.e. hospitals, physicians, clinics) has slowed and momentum has shifted from sellers to buyers seeking less risk and higher returns. Capital deployment by corporate insurers i.e. UHG, HUM et al has resulted in vertically-integrated systems of health inclusive of physician services, drug distribution, ASCs and more. And funding for AI-investments that lower their admin costs and increase their contracting leverage with providers is a strategic advantage for corporate insurer that operate nationally at scale. Unless the federal government bridles their growth (which is unlikely), corporate insurers will control national coverage while others fail.

Thus, no one knows for sure what coverage will be in 2034 as presented in the CBO report. Its analysis appropriately considers medical inflation, population growth and an incremental shift to value-based purchasing in healthcare, but it fails to accommodate highly relevant changes in the capital markets, corporate insurer shareholder interests and voter sentiment.

P.S. This is an important week for healthcare: Today marks the two-year anniversary of the Supreme Court’s Dobbs decision that overturned Roe v. Wade, ending the constitutional right to an abortion that pushed reproductive rights to states.

And Thursday in Atlanta, President Joe Biden and former President Donald Trump will make history in the first presidential debate between an incumbent and a former president.

Reproductive rights will be a prominent theme along with immigration and border security as wedge issues for voters.

The economy and inflation are the issues of most consequence to most voters, so unless the campaigns directly link healthcare spending and out of pocket costs to voter angst about their household finances, not much will be said.

Notably, half of the U.S. population have unpaid medical bills and medical debt is directly related to their financial insecurity. Worth watching.

Last week, 2 important economic reports were released that provide a retrospective and prospective assessment of the U.S. health economy:

The CBO National Health Expenditure Forecast to 2032:

“Health care spending growth is expected to outpace that of the gross domestic product (GDP) during the coming decade, resulting in a health share of GDP that reaches 19.7% by 2032 (up from 17.3% in 2022). National health expenditures are projected to have grown 7.5% in 2023, when the COVID-19 public health emergency ended. This reflects broad increases in the use of health care, which is associated with an estimated 93.1% of the population being insured that year… During 2027–32, personal health care price inflation and growth in the use of health care services and goods contribute to projected health spending that grows at a faster rate than the rest of the economy.”

The Congressional Budget Office forecast that from 2024 to 2032:

National Health Expenditures will increase 52.6%: $5.048 trillion (17.6% of GDP) to $7,705 trillion (19.7% of GDP) based on average annual growth of: +5.2% in 2024 increasing to +5.6% in 2032

NHE/Capita will increase 45.6%: from $15,054 in 2024 to $21,927 in 2032

Physician services spending will increase 51.2%: from $1006.5 trillion (19.9% of NHE) to $1522.1 trillion (19.7% of total NHE)

Hospital spending will increase 51.6%: from $1559.6 trillion (30.9% of total NHE) in 2024 to $2366.3 trillion (30.7% of total NHE) in 2032.

Prescription drug spending will increase 57.1%: from 463.6 billion (9.2% of total NHE) to 728.5 billion (9.4% of total NHE)

The net cost of insurance will increase 62.9%: from 328.2 billion (6.5% of total NHE) to 534.7 billion (6.9% of total NHE).

The U.S. Population will increase 4.9%: from 334.9 million in 2024 to 351.4 million in 2032.

The Bureau of Labor Statistics CPI Report for May 2024 and Last 12 Months (May 2023-May2024):

“The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in May on a seasonally adjusted basis, after rising 0.3% in April… Over the last 12 months, the all-items index increased 3.3% before seasonal adjustment. More than offsetting a decline in gasoline, the index for shelter rose in May, up 0.4% for the fourth consecutive month. The index for food increased 0.1% in May. … The index for all items less food and energy rose 0.2% in May, after rising 0.3 % the preceding month… The all-items index rose 3.3% for the 12 months ending May, a smaller increase than the 3.4% increase for the 12 months ending April. The all items less food and energy index rose 3.4 % over the last 12 months. The energy index increased 3.7%for the 12 months ending May. The food index increased 2.1%over the last year.

Medical care services, which represents 6.5% of the overall CPI, increased 3.1%–lower than the overall CPI. Key elements included in this category reflect wide variance: hospital and OTC prices exceeded the overall CPI while insurance, prescription drugs and physician services were lower.

Physicians’ services CPI (1.8% of total impact): LTM: +1.4%

Hospital services CPI (1.0% of total impact): LTM: +7.3%

Prescription drugs (.9% of total impact) LTM +2.4%

Over the Counter Products (.4% of total impact) LTM 5.9%

Health insurance (.6% of total) LTM -7.7%

Other categories of greater impact on the overall CPI than medical services are Shelter (36.1%), Commodities (18.6%), Food (13.4%), Energy (7.0%) and Transportation (6.5%).

Three key takeaways from these reports:

The health economy is big and getting bigger. But it’s less obvious to consumers in the prices they experience than to employers, state and federal government who fund the majority of its spending. Notably, OTC products are an exception: they’re a direct OOP expense for most consumers. To consumers, especially renters and young adults hoping to purchase homes, the escalating costs of housing have considerably more impact than health prices today but directly impact on their ability to afford coverage and services. Per Redfin, mortgage rates will hover at 6-7% through next year and rents will increase 10% or more.

Proportionate to National Health Expenditure growth, spending for hospitals and physician services will remain at current levels while spending for prescription drugs and health insurance will increase. That’s certain to increase attention to price controls and heighten tension between insurers and providers.

There’s scant evidence the value agenda aka value-based purchases, alternative payment models et al has lowered spending nor considered significant in forecasts.

The health economy is expanding above the overall rates of population growth, overall inflation and the U.S. economy. GDP. Its long-term sustainability is in question unless monetary policies enable other industries to grow proportionately and/or taxpayers agree to pay more for its services. These data confirm its unit costs and prices are problematic.

As Campaign 2024 heats up with the economy as its key issue, promises to contain health spending, impose price controls, limit consolidation and increase competition will be prominent.

Public sector actions

will likely feature state initiatives to lower cost and spend taxpayer money more effectively.

Private sector actions

will center on employer and insurer initiatives to increase out of pocket payments for enrollees and reduce their choices of providers.

Thus, these reports paint a cautionary picture for the health economy going forward. Each sector will feel cost-containment pressure and each will claim it is responding appropriately. Some actually will.

PS: The issue of tax exemptions for not-for-profit hospitals reared itself again last week.

The Committee for a Responsible Federal Budget—a conservative leaning think tank—issued a report arguing the exemption needs to be ended or cut. In response,

the American Hospital Association issued a testy reply claiming the report’s math misleading and motivation ill-conceived.

This issue is not going away: it requires objective analysis, fresh thinking and new voices. For a recap, see the Hospital Section below.

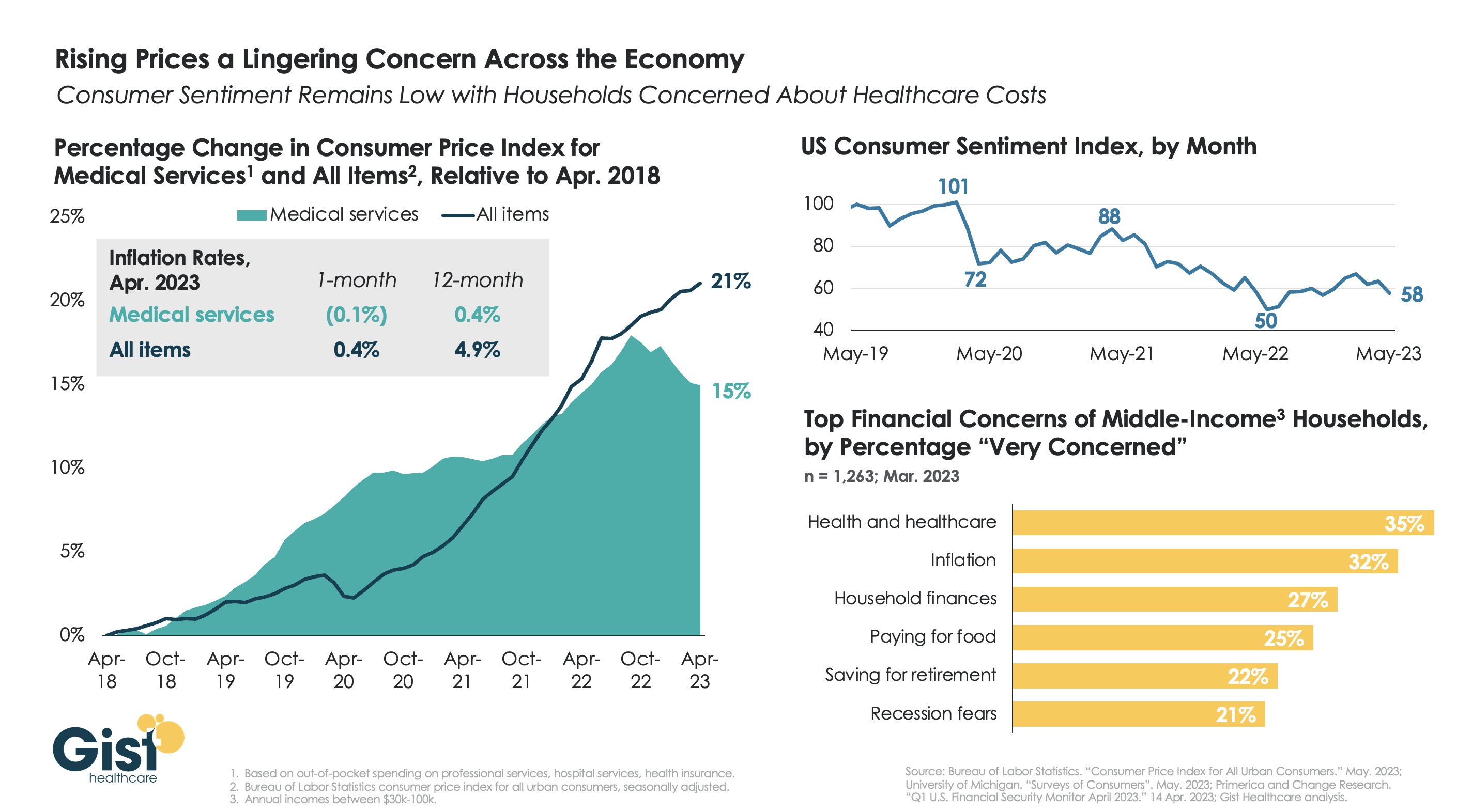

With the latest Bureau of Labor Statistics’ Consumer Price Index (CPI) report revealing the 12-month inflation rate in April 2023 rose again after hitting a recent low in March, we’re using this week’s graphic to show the cumulative picture on price and consumer sentiment changes across the last five years.

Since 2018, the CPI for all goods has risen 21 percent, while medical services have become 15 percent more expensive, in terms of consumer out-of-pocket spending. Leading into COVID, medical service prices were rising faster than general inflation, but the cumulative rise in the price of all goods caught up to medical services in early 2022.

Since December of last year, the price of medical services has actually experienced some deflation, partly due to a lagging decline in insurer profits. Reports of easing inflation had elicited a slight rebound in consumer sentiment, but last month’s 9 percent drop, the largest since June 2022, suggests this confidence is easily shaken.

Unfortunately for healthcare providers, according to a recent poll, fewer consumers worrying about elevated grocery and gas prices means that healthcare has reclaimed the top spot for household financial concerns.

Radio Advisory’s Rachel Woods sat down with Advisory Board‘s Aaron Mauck and Natalie Trebes to talk about where leaders need to focus their attention on longer-term industry challenges—like growing competition, behavioral health infrastructure, and finding success in value-based care.

Rachel Woods: So I’ve been thinking about the last conversation that we had about what executives need to know to be prepared to be successful in 2023, and I feel like my big takeaway is that the present feels aggressively urgent. The business climate today is extraordinarily tough, there are all these disruptive forces that are changing the competitive landscape, right? That’s where we focused most of our last conversation.

But we also agreed that those were still kind of near-term problems. My question is why, if things feel like they are in such a crisis, do we need to also focus our attention on longer term challenges?

Aaron Mauck: It’s pretty clear that the business environment really isn’t sustainable as it currently stands, and there’s a tendency, of course, for all businesses to focus on the urgent and important items at the expense of the non-urgent and important items. And we have a lot of non-urgent important things that are coming on the horizon that we have to address.

Obviously, you think about the aging population. We have the baby boom reaching an age where they’re going to have multiple care needs that have to be addressed that constitute pretty significant challenges. That aging population is a central concern for all of us.

Costly specialty therapeutics that are coming down the pipeline that are going to yield great results for certain patient segments, but are going to be very expensive. Unmanaged behavioral needs, disagreements around appropriate spending. So we have lots of challenges, myriad of challenges we’re going to have to address simultaneously.

Natalie Trebes: Yeah, that’s right. And I would add that all of those things are at threshold moments where they are pivoting into becoming our real big problems that are very soon going to be the near term problems. And the environment that we talked about last time, it’s competitive chaos that’s happening right now, is actually the perfect time to be making some changes because all the challenges we’re going to talk about require really significant restructuring of how we do business. That’s hard to do when things are stable.

Woods: Yes. But I still think you’re going to get some people who disagree. And let me tell you why. I think there’s two reasons why people are going to disagree. The first reason is, again, they are dealing with not just one massive fire in front of them, but what feels like countless massive fires in front of them that’s just demanding all of their strategic attention. That was the first thing you said every executive needs to know going into this year, and maybe not know, but accept, if I’m thinking about the stages of grief.

But the second reason why I think people are going to push back is the laundry list of things that Aaron just spoke of are areas where, I’m not saying the healthcare industry shouldn’t be focused on them, but we haven’t actually made meaningful progress so far.

Is 2023 actually the year where we should start chipping away at some of those huge industry challenges? That’s where I think you’re going to get disagreement. What do you say to that?

Trebes: I think that’s fair. I think it’s partly that we have to start transforming today and organizations are going to diverge from here in terms of how they are affected. So far, we’ve been really kind of sharing the pain of a lot of these challenges, it’s bits and pieces here. We’re all having to eat a little slice of this.

I think different organizations right now, if they are careful about understanding their vulnerabilities and thinking about where they’re exposed, are going to be setting themselves up to pass along some of that to other organizations. And so this is the moment to really understand how do we collectively want to address these challenges rather than continue to try to touch as little of it as we possibly can and scrape by?

Woods: That’s interesting because it’s also probably not just preparing for where you have vulnerabilities that are going to be exposed sooner rather than later, but also where might you have a first mover advantage? That gets back to what you were talking about when it comes to the kind of competitive landscape, and there’s probably people who can use these as an opportunity for the future.

Mauck: Crises are always opportunities and even for those players across the healthcare system who have really felt like they’re boxers in the later rounds covering up under a lot of blows, there’s opportunities for them to come back and devise strategies for the long term that really yield growth.

We shouldn’t treat this as a time just of contraction. There are major opportunities even for some of the traditional incumbents if they’re approaching these challenges in the right fashion. When we think about that in terms of things like labor or care delivery models, there’s huge opportunities and when I talk with C-suites from across the sector, they recognize those opportunities. They’re thinking in the long term, they need to think in the long term if they’re going to sustain themselves. It is a time of existential crisis, but also a time for existential opportunity.

Trebes: Yeah, let’s be real, there is a big risk of being a first mover, but there is a really big opportunity in being on the forefront of designing the infrastructure and setting the table of where we want to go and designing this to work for you. Because changes have to happen, you really want to be involved in that kind of decision making.

Woods: And in the vein of acceptance, we should all accept that this isn’t going to be easy. The challenges that I think we want to focus on for the rest of this conversation are challenges that up to this point have seemed unsolvable. What are the specific areas that you think should really demand executive attention in 2023?

Trebes: Well, I think they break into a few different categories. We are having real debates about how do we decide what are appropriate outcomes in healthcare? And so the concept of measuring value and paying for value. We have to make some decisions about what trade-offs we want to make there, and how do we build in health equity into our business model and do we want to make that a reality for everyone?

Another category is all of the expensive care that we have to figure out how to deliver and finance over the coming years. So we’re talking about the already inadequate behavioral health infrastructure that’s seen a huge influx in demand.

We’re talking about what Aaron mentioned, the growing senior population, especially with boomers getting older and requiring a lot more care, and the pipeline of high-cost therapies. All of this is not what we are ready as the healthcare system as it exists today to manage appropriately in a financially sustainable way. And that’s going to be really hard for purchasers who are financing all of this.

Understand the health care industry’s most urgent challenges—and greatest opportunities.

The health care industry is facing an increasingly tough business climate dominated by increasing costs and prices, tightening margins and capital, staffing upheaval, and state-level policymaking. These urgent, disruptive market forces mean that leaders must navigate an unusually high number of short-term crises.

But these near-term challenges also offer significant opportunities. The strategic choices health care leaders make now will have an outsized impact—positive or negative—on their organization’s long-term goals, as well as the equitability, sustainability, and affordability of the industry as a whole.

This briefing examines the biggest market forces to watch, the key strategic decisions that health care organizations must make to influence how the industry operates, and the emerging disruptions that will challenge the traditional structures of the entire industry.

Preview the insights below and download the full executive briefing (using the link above) now to learn the top 16 insights about the state of the health care industry today.

Preview the insights

Part 1 | Today’s market environment includes an overwhelming deluge of crises—and they all command strategic attention

Insight #1

The converging financial pressures of elevated input costs, a volatile macroeconomic climate, and the delayed impact of inflation on health care prices are exposing the entire industry to even greater scrutiny over affordability. Keep reading on pg. 6

Insight #2

The clinical workforce shortage is not temporary. It’s been building to a structural breaking point for years. Keep reading on pg. 8

Insight #3

Demand for health care services is growing more varied and complex—and pressuring the limited capacity of the health care industry when its bandwidth is most depleted. Keep reading on pg. 10

Insight #4

Insurance coverage shifted dramatically to publicly funded managed care. But Medicaid enrollment is poised to disperse unevenly after the public health emergency expires, while Medicare Advantage will grow (and consolidate). Keep reading on pg. 12

Part II | Competition for strategic assets continues at a rapid pace—influencing how and where patient care is delivered.

Insight #5

The current crisis conditions of hospital systems mask deeper vulnerabilities: rapidly eroding power to control procedural volumes and uncertainty around strategic acquisition and consolidation. Keep reading on pg. 15

Insight #6

Health care giants—especially national insurers, retailers, and big tech entrants—are building vertical ecosystems (and driving an asset-buying frenzy in the process). Keep reading on pg. 17

Insight #7

As employment options expand, physicians will determine which owners and partners benefit from their talent, clinical influence, and strategic capabilities—but only if these organizations can create an integrated physician enterprise. Keep reading on pg. 19

Insight #8

Broader, sustainable shifts to home-based care will require most care delivery organizations to focus on scaling select services. Keep reading on pg. 21

Insight #9

A flood of investment has expanded telehealth technology and changed what interactions with patients are possible. This has opened up new capabilities for coordinating care management or competing for consumer attention. Keep reading on pg. 23

Insight #10

Health care organizations are harnessing data and incentives to curate consumers choices—at both the service-specific and ecosystem-wide levels. Keep reading on pg. 25

Part III | Emerging structural disruptions require leaders to reckon with impacts to future business sustainability.

Insight #11

For value-based care to succeed outside of public programs, commercial plans and providers must coalesce around a sustainable risk-based payment approach that meets employers’ experience and cost needs. Keep reading on pg. 28

Insight #12

Industry pioneers are taking steps to integrate health equity into quality metrics. This could transform the health care business model, or it could relegate equity initiatives to just another target on a dashboard. Keep reading on pg. 30

Insight #13

Unprecedented behavioral health needs are hitting an already fragmented, marginalized care infrastructure. Leaders across all sectors will need to make difficult compromises to treat and pay for behavioral health like we do other complex, chronic conditions. Keep reading on pg. 32

Insight #14

As the population ages, the fragile patchwork of government payers, unpaid caregivers, and strained nursing homes is ill-equipped to provide sustainable, equitable senior care. This is putting pressure on Medicare Advantage plans to ultimately deliver results. Keep reading on pg. 34

Insight #15

The enormous pipeline of specialized high-cost therapies in development will see limited clinical use unless the entire industry prepares for paradigm shifts in evidence evaluation, utilization management, and financing. Keep reading on pg. 36

Insight #16

Self-funded employers, who are now liable for paying “reasonable” amounts, may contest the standard business practices of brokers and plans to avoid complex legal battles with poor optics. Keep reading on pg. 38