Last week we met the CEO of the flagship hospital of a large academic health system. Like nearly every hospital, they are challenged in finding the staff they need to keep the hospital running at full capacity. Keeping all the hospital’s units open has been critical: “Over the past three months, we have been busting at the seams…more patients, and they’re sicker. And we’re not even really into flu season yet.” We asked what had changed, given that summer usually is lighter than other seasons for hospital admissions.

His diagnosis: local community hospitals, also strapped for staff, had begun to regularly shut down units to keep premium labor spend in check. “If they’re not running at full capacity, the patients still have to go somewhere. Given that we’re both the quaternary care provider and the community’s safety net, they’re coming downtown to us. We don’t have the luxury to shut down.” The system had to ramp up agency nursing to accommodate the demand, leading to a sharp rise in labor costs.

This CEO wasn’t backing away from the system’s mission, and vowed to expand capacity as much as they could, but felt that policymakers and payers needed to understand the dynamics in the market: “We’re getting criticized for not being able to control our costs, despite the fact that we’re absorbing what other hospitals can’t handle.” As we head into winter, flu will surely spike, and another COVID surge is possible—the hospitals at the top of the “care chain” will become even more strained in their mission to accommodate their communities’ needs.

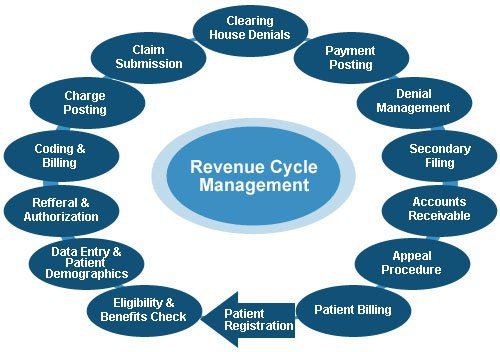

Revenue cycle challenges “seem to have intensified over the past year,” according to Kaufman Hall’s “2022 State of Healthcare Performance Improvement” report, released Oct. 18.

The consulting firm said that in 2021, 25 percent of survey respondents said they had not seen any pandemic-related effects on their respective revenue cycles. This year, only 7 percent said they saw no effects.

The findings in Kaufman Hall’s report are based on survey responses from 86 hospital and health system leaders across the U.S.

Here are the top five ways leaders said the pandemic affected the revenue cycle in 2022:

1. Increased rate claim denials — 67 percent

2. Change in payer mix: Lower percentage of commercially insured patients — 51 percent

3. Increase in bad debt/uncompensated care — 41 percent

4. Change in payer mix: Higher percentage of Medicaid patients — 35 percent

5. Change in payer mix: Higher percentage of self-pay or uninsured patients — 31 percent

Fall is typically a period of increased CFO turnover as hospitals and health systems begin searches for new executives for the beginning of the following year, but the pressures associated with high inflation, a projected recession and the continued effects of the pandemic have led to more churn than usual for top financial positions, The Wall Street Journal reported Oct. 23

Many economists and financial experts are expecting a recession to hit the U.S. in early- to mid-2023. This is pushing some executives to switch roles now before the labor market changes. Many healthcare organizations are also preparing for a potential economic downturn by searching for CFOs who are experienced in cutting costs or restructuring operations, according to the report.

Recession planning in healthcare is challenging because it can have both negative (payer mix, patient volume) and positive effects (decrease in labor and supply inflation) on financial performance, according to Daniel Morash, senior vice president of finance and CFO for Boston-based Brigham and Women’s Hospital.

“The best advice I would give is that hospitals need to consider recession scenarios when making long-term commitments on wage increases, capital expenditures and planning for capacity for patient access,” Mr. Morash told Becker’s Hospital Review. “Most of our focus needs to be on the acute challenges we are facing. Still, it’s important to be careful not to overreact or overcommit financially when a recession could change a number of trends we’re seeing now.”

Employers face a brutal increase in health-insurance premiums for 2023, Axios’ Arielle Dreher writes from a Kaiser Family Foundation report out this morning.

Why it matters: Premiums stayed relatively flat this year, even as wages and inflation surged. That reprieve was because many 2022 premiums were finalized last fall, before inflation took off.

“Employers are already concerned about what they pay for health premiums,” KFF president and CEO Drew Altman said.

“[B]ut this could be the calm before the storm … Given the tight labor market and rising wages, it will be tough for employers to shift costs onto workers when costs spike.”

🧠 What’s happening: Nearly 159 million Americans get health coverage through work — and coverage costs and benefits have become a critical factor in a tight labor market.

Nonprofit hospitals are bracing for a challenging few months as healthcare and social assistance job vacancies remain high against a backdrop of low unemployment, Fitch Ratings said in an Oct. 25 update.

Healthcare and social assistance job openings fell for two consecutive months to 7.7 percent as of August, but the number of openings remains above the highest level recorded before the COVID-19 pandemic.

One encouraging sign is the slowly declining number of quits — 2.3 percent (486,000 quits) in August 2022 compared with a peak of 3.1 percent (626,000 quits) in November 2021. However, current quit rates remain high and are on track to exceed last year, according to Fitch.

“[not-for-profit] hospital quits will need to normalize to well below pre-pandemic levels in order to reduce staffing shortages and a reliance on contract/temporary labor,” Fitch Director Richard Park said in the news release.

The labor shortage saw hospital employees’ average weekly earnings increase 21.1 percent since February, significantly higher than the 13.6 percent earnings growth of overall private sector employees, according to Fitch. But ambulatory healthcare services employees’ earnings increased by only 12.6 percent over the same period.

“Wage increases and employee recruitment challenges may amplify the role of ambulatory care in the overall healthcare sector and continue the acceleration of inpatient care to outpatient settings,” Mr. Park said.

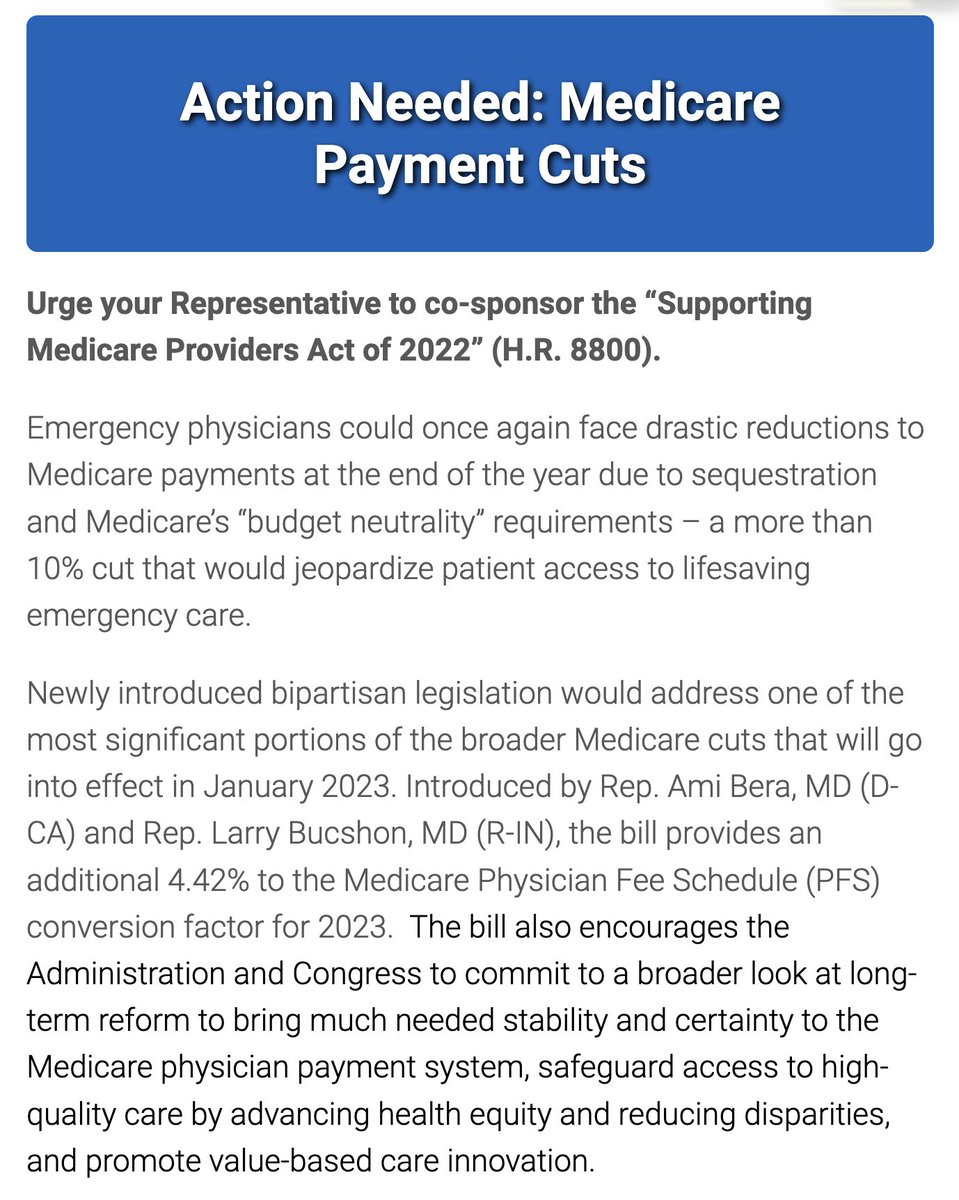

This critical, bipartisan legislation would stabilize Medicare for physicians and patients because it:

Stops the 4.42% of the Medicare cuts related to the budget neutrality adjustment in the Medicare Physician Fee Schedule (MPFS), helping to buoy physician practices that are still recovering from the pandemic;

Protects patients access to care, particularly in underserved communities; and

Provides a commitment to long-term Medicare payment reform.

Earlier this month, the Biden administration officially extended the federal public health emergency (PHE) declaration it had set in place for COVID-19. That means the PHE provisions will stay in effect for another 90 days — until mid-January at least.

When the PHE does end, a number of rules developed in response to the pandemic will sunset. One of those is a provision that temporarily requires states to let all Medicaid beneficiaries remain enrolled in the program — even if they have become ineligible during the pandemic.

Estimates suggest that millions could lose Medicaid coverage when this emergency provision ends. Among those who would lose coverage because they are no longer eligible for the program, about one-third are expected to qualify for subsidized coverage on the Affordable Care Act (ACA) marketplaces. Most others are expected to get coverage through an employer. It remains an open question, though, how many people will successfully transition to these other plans.

A recent paper by health economics researcher Laura Dague and colleagues in the Journal of Health Politics, Policy, and Law sheds light on these dynamics. The authors used a prior change in eligibility in Wisconsin’s Medicaid program to estimate how many people successfully transitioned to a private plan when their Medicaid eligibility ended.

Wisconsin’s Medicaid program is unique. Back in 2008 — before the ACA passed — Wisconsin broadly expanded Medicaid eligibility for non-elderly adults. After the ACA came into effect, Wisconsin reworked its Medicaid program in a way that made about 44,000 adults (mostly parents) with incomes above the federal poverty line ineligible for the program. To remain insured, they would have to switch to private coverage (via Obamacare or an employer).

Only about one-third of those 44,000 people had definitely enrolled in private coverage within two months of exiting the Medicaid program.

The remaining two-thirds of people were uninsured or their insurance status couldn’t be determined.

Even using the most optimistic assumptions to fill in that missing insurance status data, the authors estimated only up to 42% of people might have had private coverage within three months.

Nearly 1 in 10 enrollees had re-entered Medicaid coverage within six months, possibly due to fluctuations in household income.

This paper has several limitations. Health insurers are not required to participate in Wisconsin’s APCD, so the authors may not be capturing all successful transitions from Medicaid to private insurance. The paper also does not distinguish between different types of private insurance: Some coverage gains may have resulted from employer-based insurance rather than the ACA marketplace.

Still, the findings suggest that when a large number of Wisconsin residents lost Medicaid eligibility in 2014, many were not able to transition from Medicaid to private coverage. Wisconsin’s experience can help us understand what might happen when the national public health emergency ends and Medicaid programs resume removing people from their rolls.

There are few easy ways to cut expenses. But in hospitals and health systems, there are quieter ways.

Workforce reductions are never painless — or never should be, especially for those doing the reducing. Involuntary job loss is one of the most stressful events workers and families experience, carrying mental and physical health risks in addition to the disruption it poses to peoples’ short- and long-term life plans.

But as health systems find themselves in untenable financial positions and looming risk of an economic recession, job cuts and layoffs in hospitals and health systems are increasingly likely. In a report released Oct. 18 from Kaufman Hall based on response from 86 health system leaders, 46 percent said labor costs are the largest opportunity for cost reduction — up significantly from the 17 percent of leaders who said the same last year.

Job cuts at hospitals may seem counterintuitive given the nation’s widely known shortages of healthcare workers. But as hospitals weather one of their most financially difficult years, some are reducing their administrative staff, eliminating vacant jobs and reorganizing or shrinking their executive teams to curb costs.

Decisions to reduce administrative labor tend to garner quieter reactions compared to budgetary decisions to end service lines or close sites of patient care, including hospitals. While the implications of administrative shakeups may be felt throughout a health system, the disruption they pose to patients is less immediately palpable. Few people know the name of their community hospitals’ senior vice presidents, but most do know how many minutes it takes to travel to a nearby site of care for an appointment during a workday or a tolerable amount of time to wait for said appointment.

It doesn’t hurt that hospital and health systems’ administrative ranks have ballooned compared to their patient-facing counterparts. While the number of practicing physicians in the U.S. grew 150 percent between 1975 and 2010, the number of healthcare administrators increased 3,200 percent in the same period. More broadly, administrative spending accounts for 15 to 30 percent of healthcare spending in the U.S. and at least half of that “does not contribute to health outcomes in any discernible way,” according to a report published Oct. 6 in Health Affairs.

A couple of health systems have denoted their plans to cut nonclinical employees and jobs in the past week.

Cleveland-based University Hospitals announced efforts to reduce system expenses by $100 million Oct. 12, including the elimination of 326 vacant jobs and layoffs affecting 117 administrative employees. The workforce reduction comes as the 21-hospital system faces a net operating loss of $184.6 million from the first eight months of 2022.

Sioux Falls, S.D.-based Sanford Health is laying off an undisclosed number of staff, a decision the organization’s top leader says is “to streamline leadership structure and simplify operations” in certain areas, the Argus Leader reported Oct. 19. Bill Gassen, president and CEO of Sanford Health, also said the layoffs primarily affect nonclinical areas and that they will “not adversely impact patient or resident care in any way.”

These developments are only several days old, but have not yet triggered any newsworthy follow-up developments or pushback. Cost reduction efforts that close facilities or reduce services tend to — on the other hand — catalyze scrutiny, debate and conflict in communities that can span for months and even years.

Look to Atlanta. Marietta, Ga.-based Wellstar unexpectedly announced on Aug. 31 that its 460-bed Atlanta Medical Center will end operations on Nov. 1, with plans to progressively wind down services leading up to that date. The system attributed the decision to the $107 million loss incurred operating the hospital over the last 12 months. Noteworthy is that the system has said that 1,430 (82 percent) of Atlanta Medical Center workers affected by the facility’s impending closure have accepted job offers at other Wellstar Health System facilities.

Since, the decision to close one of Atlanta’s level 1 trauma centers has drawn attention from Georgia’s governor and gubernatorial candidate, congressional members and Atlanta Mayor Andre Dickens, who in a town hall Oct. 19 said that in closing Atlanta Medical Center, “Wellstar said they don’t want to be in the business of urban healthcare.”

The decision has also spilled over to affect area hospitals, namely Atlanta’s public Grady Health System, which received a $130 million cash infusion from the state and reported a 30 percent increase in patient volume after the emergency department of Atlanta Medical Center closed.

Health systems have a lot to weigh. Their administrative layers are thick, varied and necessary to a degree, meaning this broad category of workers still poses tough decisions when it comes to cost containment efforts. But in a very simple view, laying off people who care for patients will only hurt health systems’ chances of recruiting and retaining clinical talent — in a time when no health systems’ odds of doing so are especially outsized.

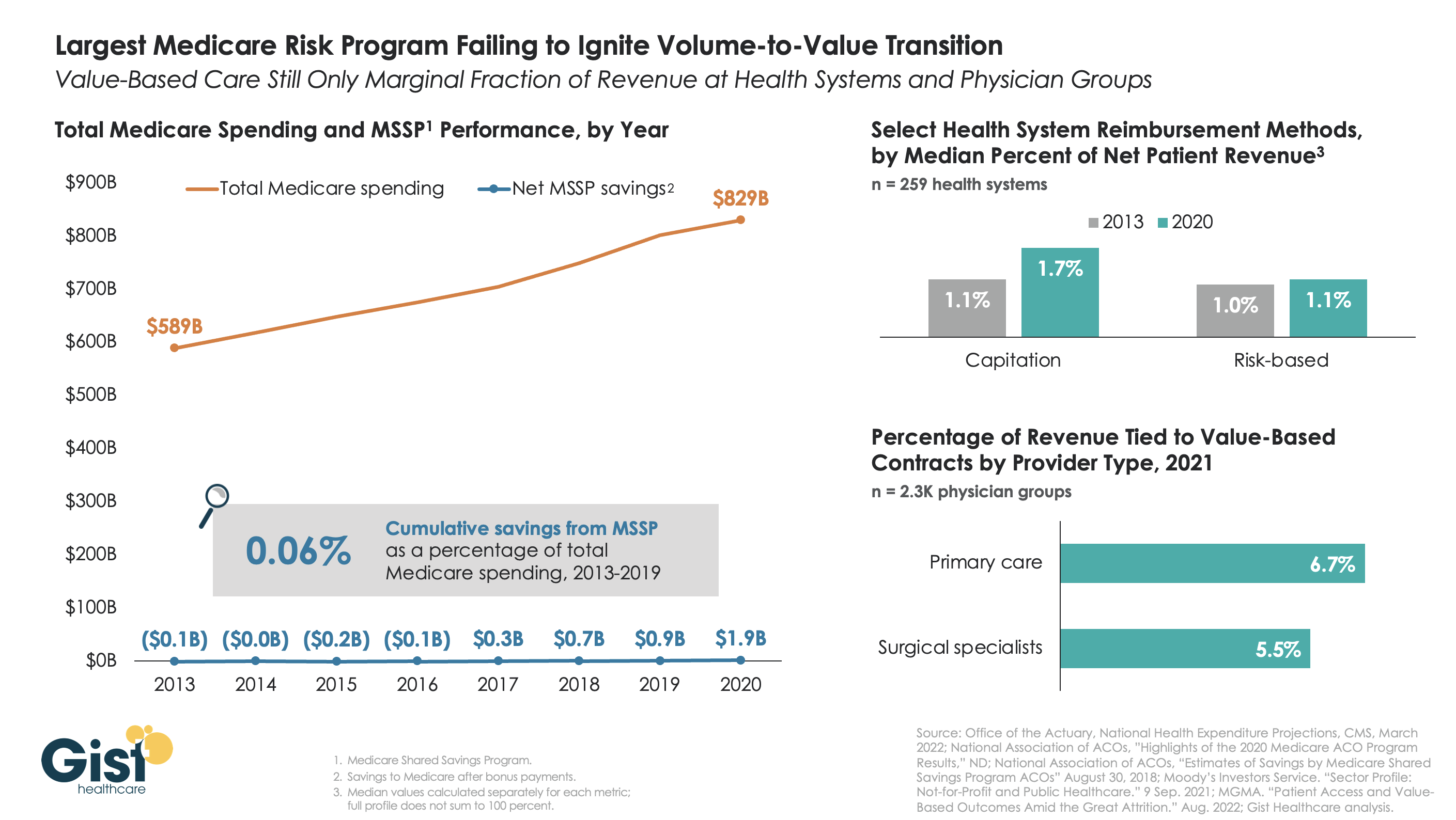

The belief that healthcare should, and would, transition from “volume to value” was a key pillar of the Affordable Care Act (ACA). However, with more than a decade of experience and data to consider, there is little indication that either Medicare or the healthcare industry at large has meaningfully shifted away from fee-for-service payment. Using data from the National Association of Accountable Care Organizations, the graphic below shows that the Medicare Shared Savings Program (MSSP)—the largest of the ACA’s payment innovations, with over 500 accountable care organizations (ACOs) reaching 11M assigned beneficiaries—has led to minimal savings for Medicare. In its first eight years, MSSP saved Medicare only $3.4B, or a paltry 0.06 percent, of the $5.6T that it spent over that time.

Policymakers had hoped that a Medicare-led move to value would prompt commercial payers to follow suit, but that also hasn’t happened. The proportion of payment to health systems in capitated or other risk-based arrangements barely budged from 2013 to 2020—remaining negligible for most organizations, and rarely amounting to enough to influence strategy. The proportion of risk-based payment for doctors is slightly higher, but still far below what is needed to enable wholesale change in care across a practice.

While Medicare has other options if it wants to increase value-based payment, like making ACOs mandatory, it’s harder to see how the trend in commercial payment will improve, as large payers, who are buying up scores of care delivery assets themselves, seem to have little motivation to deal providers in on risk.

While financial upside of moving to risk hasn’t been significant enough to move the market to date, we aren’t suggesting health systems throw out their population management playbook—to meet mounting cost labor pressures, systems must deliver lower cost care, in lower cost settings, with lower cost staff, just to maintain economic viability moving forward.