Long-term debt has long been a staple in healthcare, but many hospitals and health systems are responding to the increasing cost of debt and debt service in the rising rates environment.

Highly levered health systems are looking to sell hospitals, facilities or business lines to reduce their debt leverage and secure long-term sustainability, which creates significant growth opportunities for systems with balance sheets on a more solid financial footing.

Forty-three health systems ranked by their long-term debt:

Note: This is not an exhaustive list. The following long-term debt figures are taken from each health system’s most recent financial report.

At the Annual Meeting of the American Hospital Association in DC last week, its all-out attack on “corporate insurance” was a prominent theme. In the meeting recap, AHA CEO Rick Pollack made the influential organization’s case:

“This year, there was special focus on educating policymakers that our health care system is suffering from multiple chronic conditions.These include continued government underpayment, cyberattacks, workforce shortages, broken supply chains, access to behavioral health, and irresponsible behavior by corporate commercial health insurance companies, among others — that put access to services in serious jeopardy.”

The AHA’s declaration of war came on the heels of last week’s Congressional investigation of Change Healthcare’ (UnitedHealth Group subsidiary) cybersecurity breech and the widely-noticed earnings release by Elevance (aka Anthem) that featured prominently its plans to build a $4 billion business unit focused on primary care and chronic care management. Per company CEO Gail Boudreaux:

“This will help us continue through having a focus on advanced primary care; it’s still very much focused on our chronic patients and complex patients. We are still building specialty care enablement, which is another very important component of what we’re trying to prime through… In time, Elevance Health will have full ownership of what we expect will be a leading platform for value-based care delivery and physician enablement at scale.”

To industry watchers, the war is no surprise.

It’s been simmering for years but most recently inflamed as operating margins for most hospitals eroded while profits among corporate insurers led by Big 6 (UnitedHealth, Humana, CVS-Aetna, Elevance, Cigna, Centene) swelled at double-digit rates.

To outsiders, it’s not quite so clear.

Big names (Brands) are prominent in both. Corporatization seems embedded in the business models for both. And both appear complicit in well-documented beliefs that the health system is failing as unnecessary higher costs make it less accessible, affordable and effective.

As the War intensifies, each combatant is inclined to make their cases aggressively contrasting “us” against “them.” Here’s where things stand today:

Consideration

Hospitals

Corporate Insurers

Advantage

Public Standing

Hospitals enjoy relatively strong public support but growing discontent about their costs, prices and household affordability. Hospitals blame insurers & drug companies for increasing health costs.Increased attention to affordability, value and low prices is a threat.

Insurers enjoy reasonably high support among middle & high-income consumers who think it necessary to their financial security. Insurers blame drug companies, hospitals and unhealthy consumer behaviors for increased health costs.

It’s a tossup. Though polls show trust in hospitals is higher than insurers, both are declining especially among younger, urban and low-middle income consumers

Regulatory positioning

Scrutiny of business practices & the impact of consolidation on consumer prices, workforce wage compression, competition et al is significant and increasing in 5 Congressional Committees and 3 Federal agencies. Hospitals also face state and local regulatory challenges around pricing, community benefits, et al.

Compliance with plan transparency rules, prior authorization requirements, Medicare Advantage marketing & coverage, and antitrust are targets. Levels of Congressional attention to business practices are relatively low. Insurers are primarily overseen by states, so the regulatory landscape varies widely except.

Insurers enjoy regulatory advantages today not withstanding current attention to UnitedHealth Group. Hospitals are “soft targets” for state legislatures, Congress and investigators in state and federal agencies.

Confidence of capital markets in their core businesses: Hospitals: inpatient, outpatient careInsurers: group & individual coverage, claims data commercialization

The acute sector, especially rural & systems operating in low-growth markets, face insurmountable headwinds due to reimbursement cuts, value-based purchasing initiatives by Medicare and private insurers and clinical innovations that drive demand away from inpatient care. Hospital Outpatient services are profitable for the near term despite growing competition from privately investors.

The consolidation of power, financial strength & influence among the corporate insurers is assuring to lenders & investors who value their performance and support their vertical integration expansion role.

Lenders and investors favor “corporate insurers” over others. The potential (likelihood) that hospitals will lose on high profile revenue-enhancer issues (facility fees, site neutral payments, et al) and restrict tax exemptions for NFP hospital operators is concerning to the capital markets.

Relationships with Physicians

Hospitals employ 58% of physicians directly & relate to all. Regulations (i.e. Stark Laws, et al), capital deployment for hospital programs and administrative overhead are factors of high importance to physicians seeking clinical autonomy & financial security. Hospitals are a viable option to physicians seeking income security though not without concern.

Insurers employment of physicians plus contractual relationships with network physicians are transactional. Physicians inclined toward business relationships with “corporate insurers” believe their role in healthcare’s future is more stable than that of hospitals based on the belief hospitals are wasteful and non-responsive to physician input.

Hospitals enjoy a relationship advantage with most physicians. Corporate insurers enjoy a transactional relationship with physicians that’s premised on shared views about the future of the system vs. hospitals that focus on protecting the past. Hospitals enjoy a near-term advantage but the long-term is uncertain.

Unity of voice

Relatively strong around “chronic ailments” of the system but unclear about long-term destination and limited to universal hospital concerns (i.e. 340B) vs. cohort issues (tax exemptions for not for profits). The delineations between not-for-profit, investor-owned and public/government restricts the strength of hospital voice overall as each seeks unique recognition and regulatory protections.

Corporate insurers have corporate boards, broader membership, stronger balance sheets and scale. Their messaging is customized to their key customers and influencers and aligned with but not controlled by their trade groups. And they direct considerable resources to their proprietary messaging strategies.

Corporate insurers have fewer constraints in their messaging and enjoy an advantage in opining to issues that resonate with consumers (prices, quality, value).

Long-term Vision for the U.S. Health System

A private connected system of health in which hospitals coordinate and provide services for patients across the continuum of their care: preventive, chronic, acute and long-term.

A private system of comprehensive, customized products and services that operates efficiently, effectively and in the interests of all consumers.

The public and Congress aren’t sure which is better positioned to develop a “new” system of health.

This war has been simmering. It’s now a blaze. The outcome is uncertain despite the considerable resources both will spend to win.

Stay tuned.

Paul

P.S. Last week, I participated in Scottsdale Institute’s Annual Leadership Summit in Arizona. It’s 62 institutional members and corporate partners include most of the major not-for-profit health systems and the biggest names in healthcare information technology solutions.

I left with two strong impressions I’ll share:

1-How GenAI and HCIT influence the future of healthcare services delivery is very much speculative but no-less certain. It’s a work in process for everyone.

2- To navigate its evolution, knowledge sharing (and mistake sharing) among those in the trenches is essential. SI afforded a great venue for both, and also a platform for those of us who are easily overwhelmed by all this to ask honest questions and get candid answers.

Today is the federal income Tax Day. In 43 states, it’s in addition to their own income tax requirements. Last year, the federal government took in $4.6 trillion and spent $6.2 trillion including $1.9 trillion for its health programs. Overall, 2023 federal revenue decreased 15.5% and spending was down 8.4% from 2022 and the deficit increased to $33.2 trillion. Healthcare spending exceeded social security ($1.351 trillion) and defense spending ($828 billion) and is the federal economy’s biggest expense.

Along with the fragile geopolitical landscape involving relationships with China, Russia and Middle East, federal spending and the economy frame the context for U.S. domestic policies which include its health system. That’s the big picture.

Today also marks the second day of the American Hospital Association annual meeting in DC. The backdrop for this year’s meeting is unusually harsh for its members:

Increased government oversight:

Five committees of Congress and three federal agencies (FTC, DOJ, HHS) are investigating competition and business practices in hospitals, with special attention to the roles of private equity ownership, debt collection policies, price transparency compliance, tax exemptions, workforce diversity, consumer prices and more.

Medicare payment shortfall:

CMS just issued (last week) its IPPS rate adjustment for 2025: a 2.6% bump that falls short of medical inflation and is certain to exacerbate wage pressures in the hospital workforce. Per a Bank of American analysis last week, “it appears healthcare payrolls remain below pre-pandemic trend” with hospitals and nursing homes lagging ambulatory sectors in recovering.”

Persistent negative media coverage:

The financial challenges for Mission (Asheville), Steward (Massachusetts) and others have been attributed to mismanagement and greed by their corporate owners and reports from independent watchdogs (Lown, West Health, Arnold Ventures, Patient Rights Advocate) about hospital tax exemptions, patient safety, community benefits, executive compensation and charity care have amplified unflattering media attention to hospitals.

Physicians discontent:

59% of physicians in the U.S. are employed by hospitals; 18% by private equity-backed investors and the rest are “independent”. All are worried about their income. All think hospitals are wasteful and inefficient. Most think hospital employment is the lesser of evils threatening the future of their profession. And those in private equity-backed settings hope regulators leave them alone so they can survive. As America’s Physician Group CEO Susan Dentzer observed: “we knew we’re always going to need hospitals; but they don’t have to look or operate the way they do now. And they don’t have to be predicated on a revenue model based on people getting more elective surgeries than they actually need. We don’t have to run the system that way; we do run the healthcare system that way currently.”

The Value Agenda in limbo:

Since the Affordable Care Act (2010), the CMS Center for Innovation has sponsored and ultimately disabled all but 6 of its 54+ alternative payment programs. As it turns out, those that have performed best were driven by physician organizations sans hospital control. Last week’s release of “Creating a Sustainable Future for Value-Based Care: A Playbook of Voluntary Best Practices for VBC Payment Arrangements.” By the American Medical Association, the National Association of ACOs (NAACOs) and AHIP, the trade group representing America’s health insurance payers is illustrative. Noticeably not included: the American Hospital Association because value-pursuers think for hospitals it’s all talk.

National insurers hostility:

Large, corporate insurers have intensified reimbursement pressure on hospitals while successfully strengthening their collective grip on the U.S. health insurance sector. 5 insurers control 50% of the U.S. health insurance market: 4 are investor owned. By contrast, the 5 largest hospital systems control 17% of the hospital market: 1 is investor-owned. And bumpy insurer earnings post-pandemic has prompted robust price increases: in 2022 (the last year for complete data and first year post pandemic), medical inflation was 4.0%, hospital prices went up 2.2% but insurer prices increased 5.9%.

Costly capital:

The U.S. economy is in a tricky place: inflation is stuck above 3%, consumer prices are stable and employment is strong. Thus, the Fed is not likely to drop interest rates making hospital debt more costly for hospitals—especially problematic for public, safety net and rural hospitals. The hospital business is capital intense: it needs $$ for technologies, facilities and clinical innovations that treat medical demand. For those dependent on federal funding (i.e. Medicare), it’s unrealistic to think its funding from taxpayers will be adequate. Ditto state and local governments. For those that are credit worthy, capital is accessible from private investors and lenders. For at least half, it’s problematic and for all it’s certain to be more expensive.

Campaign 2024 spotlight:

In Campaign 2024, healthcare affordability is an issue to likely voters. It is noticeably missing among the priorities in the hospital-backed Coalition to Strengthen America’s Healthcare advocacy platform though 8 states have already created “affordability” boards to enact policies to protect consumers from medical debts, surprise hospital bills and more.

Understandably, hospitals argue they’re victims. They depend on AHA, its state associations, and its alliances with FAH, CHA, AEH and other like-minded collaborators to fight against policies that erode their finances i.e. 340B program participation, site-neutral payments and others. They rightfully assert that their 7/24/365 availability is uniquely qualifying for the greater good, but it’s not enough. These battles are fought with energy and resolve, but they do not win the war facing hospitals.

AHA spent more than $30 million last year to influence federal legislation but it’s an uphill battle. 70% of the U.S. population think the health system is flawed and in need of transformative change. Hospitals are its biggest player (30% of total spending), among its most visible and vulnerable to market change.

Some think hospitals can hunker down and weather the storm of these 8 challenges; others think transformative change is needed and many aren’t sure. And all recognize that the future is not a repeat of the past.

For hospitals, including those in DC this week, playing victim is not a strategy. A vision about the future of the health system that’s accessible, affordable and effective and a comprehensive plan inclusive of structural changes and funding is needed. Hospitals should play a leading, but not exclusive, role in this urgently needed effort.

Lacking this, hospitals will be public utilities in a system of health designed and implemented by others.

A new generation of doctors struggling with ever-increasing workloads and crushing student debt is helping drive unionization efforts in a profession that historically hasn’t organized.

Why it matters:

Physicians in training, like their peers in other industries, increasingly see unions as a way to boost their pay and protect themselves against grueling working conditions as they launch their careers.

It also comes amid a wave of unionization and labor actions by nurses and other caregivers across a health care system that’s still dealing with high levels of burnout.

What they’re saying:

“We deserve an increased salary to be able to afford to live in one of the most expensive areas in the United States,” said Ali Duffens, a third-year internal medicine resident at Kaiser Permanente’s San Francisco Medical Center.

She’s among the 400 residents at Kaiser’s Northern California system filing to unionize earlier this month.

Duffens earns about $82,000 per year, while paying $3,000 a month for rent and facing $350,000 in medical school loans.

The big picture:

The Kaiser residents are part of a growing number of younger peers in medicine who have been unionizing in recent years.

The number of medical residents in unions has about doubled to more than 32,000 in three years, per CalMatters.

In the last year, residents at Montefiore Medical Center, Stanford Health Care, George Washington University and the University of Pennsylvania voted to unionize, per WBUR.

“The cost of day care … in a month is about half of my salary in total, and the cost of a nanny is essentially the entirety of my salary,” Leah Rethy, an internal medicine resident with Penn Medicine, told NPR last year.

Residents can work as much as 80 hours per week while earning far less than their older colleagues.

Yes, but: Just about 6%-7% of physicians are estimated to be in unions.

Historically, doctors have thought they could just suck up the long hours and relatively low pay in training as part of the tradition of medicine, said Robert Wachter, chair of the department of medicine at the University of California, San Francisco.

“For a new generation, they look at it and say, ‘That’s crazy. I can’t believe you did that. I want to work hard, but I also want a life and I want a family, and I want a reasonable income,'” he said.

And it’s not just younger doctors.

Those more established in their careers are also unionizing as they see the industry changing in ways that they think undermine their profession.

In recent months, attending physicians at Salem Hospital, owned by Mass General Brigham, and a Cedars Sinai-owned anesthesiology practice filed to unionize.

About 600 doctors at Allina Health in Minnesota and Wisconsin last fall agreed to form what appears to be the largest union of private sector physicians.

Zoom in:

The corporatization of American medicine is seen as a key driver. More than half of all U.S. doctors now work for a health system or large medical group rather than running an independent practice.

This shift has brought heavier workloads and less control over how they care for patients, said John August, director of health care labor relations in the Scheinman Institute on Conflict Resolution at the ILR School at Cornell.

That could mean demands to see more patients, limiting the time that doctors can spend with them.

“What you will hear from them 100% of the time in every conversation they have is they feel that they have lost control over the patient-physician relationship. I mean, every single physician says that now,” August said.

The other side:

Health systems and large practices generally say they value their doctors and the relationships they hold with patients.

Hospitals have also struggled with pandemic-era financial shortfalls, including increasing labor costs.

The bottom line:

While this is a labor issue, it ultimately trickles down to quality and safety for patients, said Rachel Flores, organizing director of the Union of American Physicians and Dentists.

“Patients should care because that’s less time to address their issues,” she said. “Patients should care because there’s not enough staff to support the physician.”

Here are 23 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings and Moody’s Investors Service released in 2024.

Avera Health has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Sioux Falls, S.D.-based system’s strong operating risk and financial profile assessments, and significant size and scale, Fitch said.

Cedars-Sinai Health System has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Los Angeles-based system’s consistent historical profitability and its strong liquidity metrics, historically supported by significant philanthropy, Fitch said.

Children’s Health has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Dallas-based system’s continued strong performance from a focus on high margin and tertiary services, as well as a distinctly leading market share, Moody’s said.

Children’s Hospital Medical Center of Akron (Ohio) has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the system’s large primary care physician network, long-term collaborations with regional hospitals and leading market position as its market’s only dedicated pediatric provider, Moody’s said.

Children’s Hospital of Orange County has an “AA-” rating and a stable outlook with Fitch. The rating reflects the Orange, Calif.-based system’s position as the leading provider for pediatric acute care services in Orange County, a position solidified through its adult hospital and regional partnerships, ambulatory presence and pediatric trauma status, Fitch said.

Cook Children’s Medical Center has an “Aa2” rating and stable outlook with Moody’s. The ratings agency said the Fort Worth Texas-based system will benefit from revenue diversification through its sizable health plan, large physician group, and an expanding North Texas footprint.

El Camino Health has an “AA” rating and a stable outlook with Fitch. The rating reflects the Mountain View, Calif.-based system’s strong operating profile assessment with a history of generating double-digit operating EBITDA margins anchored by a service area that features strong demographics as well as a healthy payer mix, Fitch said.

JPS Health Network has an “AA” rating and stable outlook with Fitch. The rating reflects the Fort Worth, Texas-based system’s sound historical and forecast operating margins, the ratings agency said.

Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Somerville, Mass.-based system’s strong reputation for clinical services and research at its namesake academic medical center flagships that drive excellent patient demand and help it maintain a strong market position, Moody’s said.

McLaren Health Care has an “AA-” rating and stable outlook with Fitch. The rating reflects the Grand Blanc, Mich.-based system’s leading market position over a broad service area covering much of Michigan, the ratings agency said.

Med Center Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Bowling Green, Ky.-based system’s strong operating risk assessment and leading market position in a primary service area with favorable population growth, Fitch said.

Novant Health has an “AA-” rating and stable outlook with Fitch. The ratings agency said the Winston-Salem, N.C.-based system’s recent acquisition of three South Carolina hospitals from Dallas-based Tenet Healthcare will be accretive to its operating performance as the hospitals are highly profited and located in areas with growing populations and good income levels.

Oregon Health & Science University has an “Aa3” rating and stable outlook with Moody’s. The rating reflects the Portland-based system’s top-class academic, research and clinical capabilities, Moody’s said.

Orlando (Fla.) Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the health system’s strong and consistent operating performance and a growing presence in a demographically favorable market, Fitch said.

Presbyterian Healthcare Services has an “AA” rating and stable outlook with Fitch. The Albuquerque, N.M.-based system’s rating is driven by a strong financial profile combined with a leading market position with broad coverage in both acute care services and health plan operations, Fitch said.

Rush University System for Health has an “AA-” rating and stable outlook with Fitch. The rating reflects the Chicago-based system’s strong financial profile and an expectation that operating margins will rebound despite ongoing macro labor pressures, the rating agency said.

Saint Francis Healthcare System has an “AA” rating and stable outlook with Fitch. The rating reflects the Cape Girardeau, Mo.-based system’s strong financial profile, characterized by robust liquidity metrics, Fitch said.

Saint Luke’s Health System has an “Aa2” rating and stable outlook with Moody’s. The Kansas City, Mo.-based system’s rating was upgraded from “A1” after its merger with St. Louis-based BJC HealthCare was completed in January.

Salem (Ore.) Health has an”AA-” rating and stable outlook with Fitch. The rating reflects the system’s dominant marketing positive in a stable service area with good population growth and demand for acute care services, Fitch said.

Seattle Children’s Hospital has an “AA” rating and a stable outlook with Fitch. The rating reflects the system’s strong market position as the only children’s hospital in Seattle and provider of pediatric care to an area that covers four states, Fitch said.

SSM Health has an “AA-” rating and stable outlook with Fitch. The St. Louis-based system’s rating is supported by a strong financial profile, multistate presence and scale with good revenue diversity, Fitch said.

University of Colorado Health has an “AA” rating and stable outlook with Fitch. The Aurora-based system’s rating reflects a strong financial profile benefiting from a track record of robust operating margins and the system’s growing share of a growth market anchored by its position as the only academic medical center in the state, Fitch said.

Willis-Knighton Medical Center has an “AA-” rating and positive outlook with Fitch. The outlook reflects the Shreveport, La.-based system’s improving operating performance relative to the past two fiscal years combined with Fitch’s expectation for continued improvement in 2024 and beyond.

Health system operating margins improved in 2023 after a tumultuous 2022. Increased revenue from rebounding patient volumes helped offset the high costs of labor and supplies for many systems, but some continue to face challenges turning a financial corner.

In a Feb. 21 analysis, Kaufman Hall noted that too many hospitals are losing money but high-performing hospitals are faring far better, “effectively pulling away from the pack.”

Average operating margins have see-sawed over the last 12 months, from a -1.2% low in February 2023 to 5.5% highs in June and December. In February, average operating margins dropped to 3.96% before the Change Healthcare data breach, which has impacted claims processing.

Here are 42 health systems ranked by operating margins in their most recent financial results.

Editor’s note: The following financial results are for the 12 months ending Dec. 31, 2023, unless otherwise stated.

Revenue: $20.55 billion Expenses: $18.31 billion Operating income/loss: $2.5 billion (*Includes grant income and equity in earnings of unconsolidated affiliates) Operating margin: 12.2%

*Results for the first six months ending Dec. 31 Revenue: $2.1 billion Expenses: $2 billion Operating income/loss: $22.9 million Operating margin: 1.1%

Prices for non-trauma inpatient admissions were 4.4 percent higher at trauma center hospitals than at hospitals without a trauma designation.

Hospitals designated as trauma centers charged higher prices for non-trauma inpatient admissions and emergency department visits compared to non-trauma center hospitals, a Health Affairs study found.

Hospital prices are the largest driver of rising healthcare spending in the commercial market and are often influenced by the structure of hospital markets. Trauma centers are a critical aspect of the hospital market as they are highly regulated and endowed by regulators with monopoly power over trauma patients in their service areas.

In most states, regulations are designed to encourage the entry of new trauma centers in areas that do not already have one and restrict new entry into areas that already have a trauma center. Additional regulations often require all trauma patients within an area to be transported or transferred to the designated hospital serving the area.

These restrictions create local monopolies for hospitals that are designated as trauma centers. Those in favor of the regulations argue that the monopolies are necessary to ensure each trauma center has sufficient volume to support high-quality and low-cost care. However, this structure could allow hospitals with market power over trauma services to raise prices for non-trauma services.

Researchers used claims data from 2011 to 2018 to assess whether hospitals designated as trauma centers use their market power for trauma services to receive above-market rates for non-trauma services. The sample included 2,000 hospitals with more than two million inpatient admissions and ten million emergency department visits over the study period.

The share of hospitals included in the sample serving as trauma centers increased from 21 percent in 2012 to 28 percent in 2018, resulting in a net addition of 138 trauma centers. The share of non-trauma inpatient admissions and emergency department visits at hospitals serving as trauma centers also increased between 2012 and 2018.

Hospitals serving as trauma centers every year from 2012 to 2018 were categorized as an always trauma center. Opened trauma centers were those not serving as a trauma center in 2012 but serving as one by 2018. Hospitals serving as a trauma center in 2012 but not in 2018 were closed trauma centers, and hospitals that did not serve as a trauma center at all during the study period were called “never trauma centers.”

The average price for non-trauma inpatient admissions among all hospitals was $21,112. Always trauma center hospitals had a higher average price of $22,568 per inpatient admission. The average price per admission was $22,097 at opened centers, $20,589 at closed centers, and $19,769 at never centers. Emergency department prices were similar, with always and opened center hospitals having higher prices than closed and never trauma center facilities.

Always trauma center hospitals were generally larger compared to the other hospital types and were more likely to be in more concentrated hospital markets. The average new injury severity score among emergency department visits in never trauma center hospitals was smaller compared to scores at other hospitals. The average MS-DRG weight for always trauma center hospitals was 1.61 compared to 1.54 for opened and never trauma center hospitals.

Holding these patient and hospital characteristics constant, prices for non-trauma inpatient admissions were 4.4 percent higher in hospitals with trauma center designation than at non-trauma center hospitals. Prices for non-trauma emergency department visits were 5.2 percent higher in trauma center hospitals.

“The results presented here provide an example of an important challenge: How to ensure access to specialized services and protect public health while also accounting for and possibly managing the effects of concomitant market failure,” researchers wrote.

“Our findings provide empirical support for the notion that provider market power in one area can be leveraged to affect prices in other areas.”

The No Surprises Act limits the amounts that hospitals can charge to out-of-network patients for emergency services, including trauma services. This may help limit trauma emergency cross-service leverage pricing, researchers said.

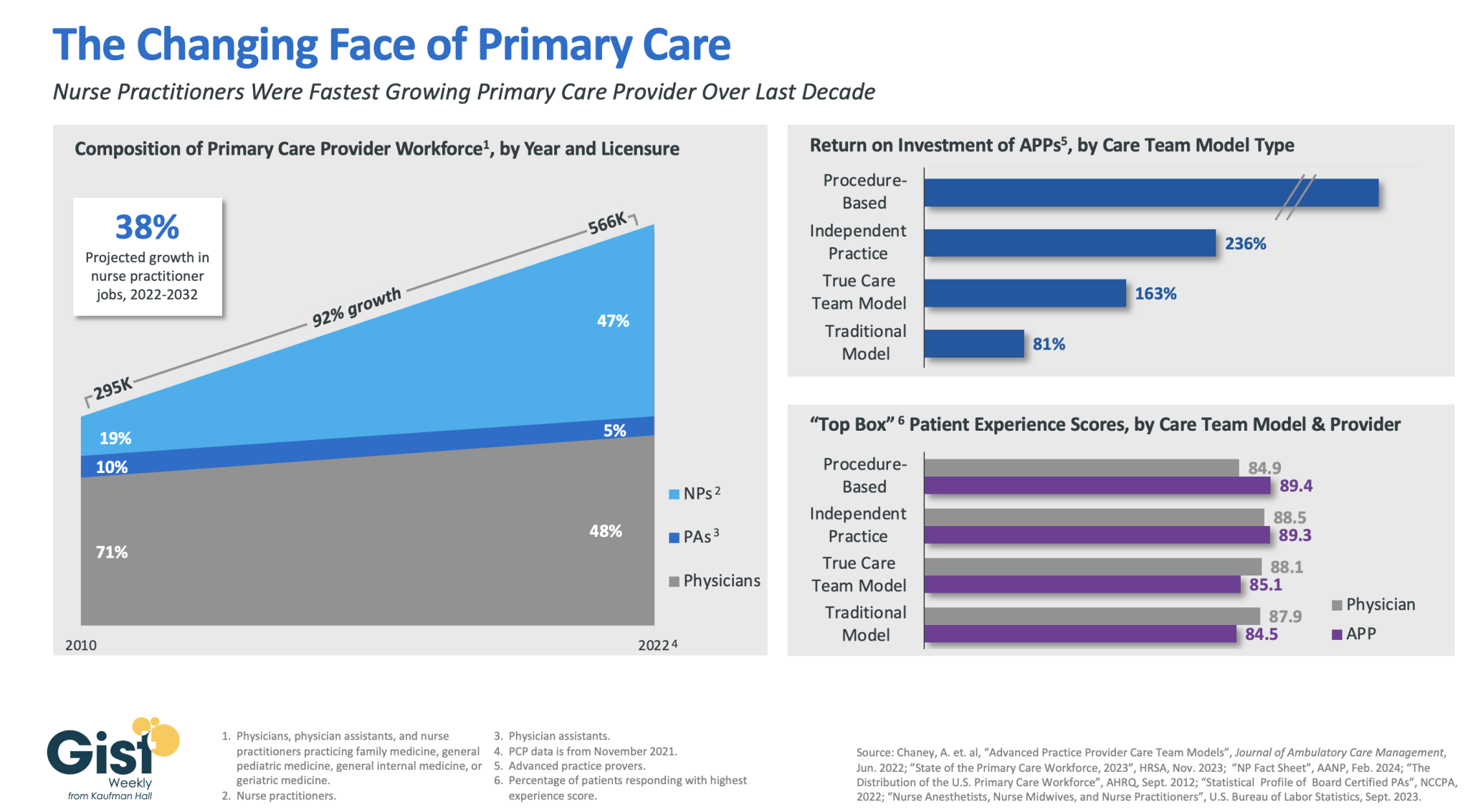

In this week’s graphic, we highlight how the primary care provider workforce has evolved over the past decade in both the pursuit of team-based care models and value-based care, as well as in response to rising labor costs and physician shortages.

In 2010, physicians made up more than 70 percent of the primary care workforce. But over the next 12 years, the number of primary care providers nearly doubled, largely driven by immense growth of nurse practitioners in the workforce.

As of 2022, more than half of primary care providers were advanced practice providers (APPs), who continue to have a strong job outlook across the next decade (especially nurse practitioners).This shift has been beneficial to many provider organizations.

In a study from the Mayo Clinic, the return on investment was positive across a variety of APP practice models, especially in procedural-based specialties but across both independent practice models and full care team models as well.

APPs also receive similar patient experience scores as their physician counterparts.

Continued integration of APPs in team-based care models remains a key strategy for health systems seeking to improve access while lowering costs, especially in primary care.

A recent engagement with a health system executive team to discuss an underperforming service line uncovered a serious issue that’s becoming more common across the industry.

“Our providers are more productive than ever,” the CFO informed our team, “and yet we keep losing money on the service line.”

After digging into their physician compensation model, we came upon one source of the system’s issue. Because it was incentivizing physician RVUs equally across all payers, its providers responded, quite rationally, by picking up market share where growth was easiest: Medicaid patients, who weren’t generating any margin.

“We recognize that we’ve been employing these physicians as loss leaders in order to generate downstream revenue,” the CFO shared, “but what’s the point of that revenue if there’s no longer any downstream margin?”

The economics of physician employment becomes a tough conversation very quickly; it’s a sensitive topic to many, and one with myriad facets.

But the loss leader physician employment model obviously only works when it produces positive downstream margins.

We’re in a critical window of time, where hospital margins are just beginning to recover as volumes return—but those volumes are not necessarily in the same places as before.

The opportunity is ripe for systems to work closely with their aligned physicians to reexamine the post-pandemic margin picture for individual service lines and ensure incentives are aligning all parties to hit operating margin goals.

Are these kinds of conversations taking place at your health system?