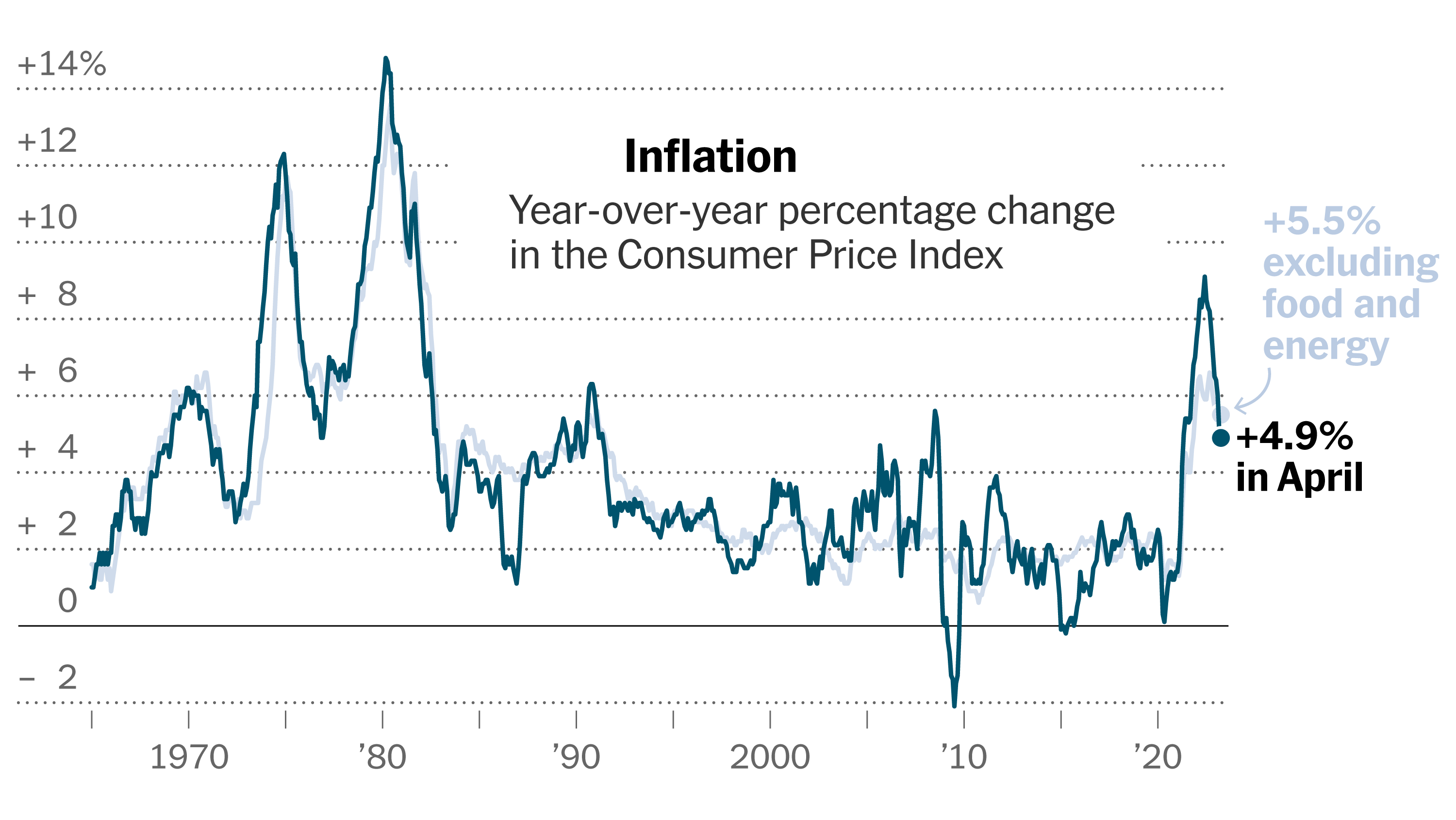

US consumer price increases cooled during the month of April, according to the latest data from the Bureau of Labor Statistics released Wednesday morning.

The Consumer Price Index (CPI) rose 0.3% over the previous month and 3.4% over the prior year in April, a slight deceleration from March’s 3.5% annual gain in prices and 0.4% month-over-month increase.

April’s monthly increase came in lower than economist forecasts of a 0.4% uptick. The annual rise in prices matched estimates, according to data from Bloomberg, and marked the slowest gain in three months.

On a “core” basis, which strips out the more volatile costs of food and gas, prices in April climbed 0.3% over the prior month and 3.6% over last year — cooler than March’s data. Both measures met economist expectations.

Investors now anticipate two 25 basis point cuts this year, down from the six cuts expected at the start of the year, according to updated Bloomberg data.

Markets rose following the data’s release, with the 10-year Treasury yield (^TNX) falling about 6 basis points to trade around 4.38%.

“The lack of a nasty surprise this time around is welcomed,” Bankrate senior economist analyst Mark Hamrick wrote in reaction to the print. Still, Hamrick added, “with the 3.4% year-over-year headline increase and 3.6% in the core (excluding food and energy), these remain irritatingly high. The status of the battle against inflation requires that interest rates remain elevated in the near-term.”

Following the data’s release, markets were pricing in a roughly 53% chance the Federal Reserve begins to cut rates at its September meeting, according to data from the CME FedWatch Tool. That’s up from about a 45% chance the month prior.

Shelter, gas prices remain sticky

Notable call-outs from the inflation print include the shelter index, which rose 5.5% on an unadjusted, annual basis, a slowdown from March. The index rose 0.4% month over month and was the largest factor in the monthly increase in core prices, according to the BLS.

Sticky shelter inflation is largely to blame for higher core inflation readings, according to economists.

The index for rent and owners’ equivalent rent (OER) each rose 0.4% on a monthly basis, matching March’s rise. Owners’ equivalent rent is the hypothetical rent a homeowner would pay for the same property.

Lodging away from home decreased 0.2% in April after rising 0.1% in March.

Energy prices continued to rise in April, buoyed by higher gas prices. The index jumped another 1.1% last month, matching March’s increase. On a yearly basis, the index climbed 2.6%.

Gas prices rose 2.8% from March to April after climbing 1.7% the previous month.

The food index increased 2.2% in April over the last year, with food prices flat from March to April. The index for food at home decreased 0.2% over the month while food away from home rose another 0.3%.

Other indexes that increased in April included motor vehicle insurance, medical care, apparel, and personal care. Motor vehicle insurance, a standout in March’s report after the category jumped 2.6%, climbed another 1.8% in April.

The indexes for used cars and trucks, household furnishings and operations, and new vehicles were among those that decreased over the month, according to the BLS.

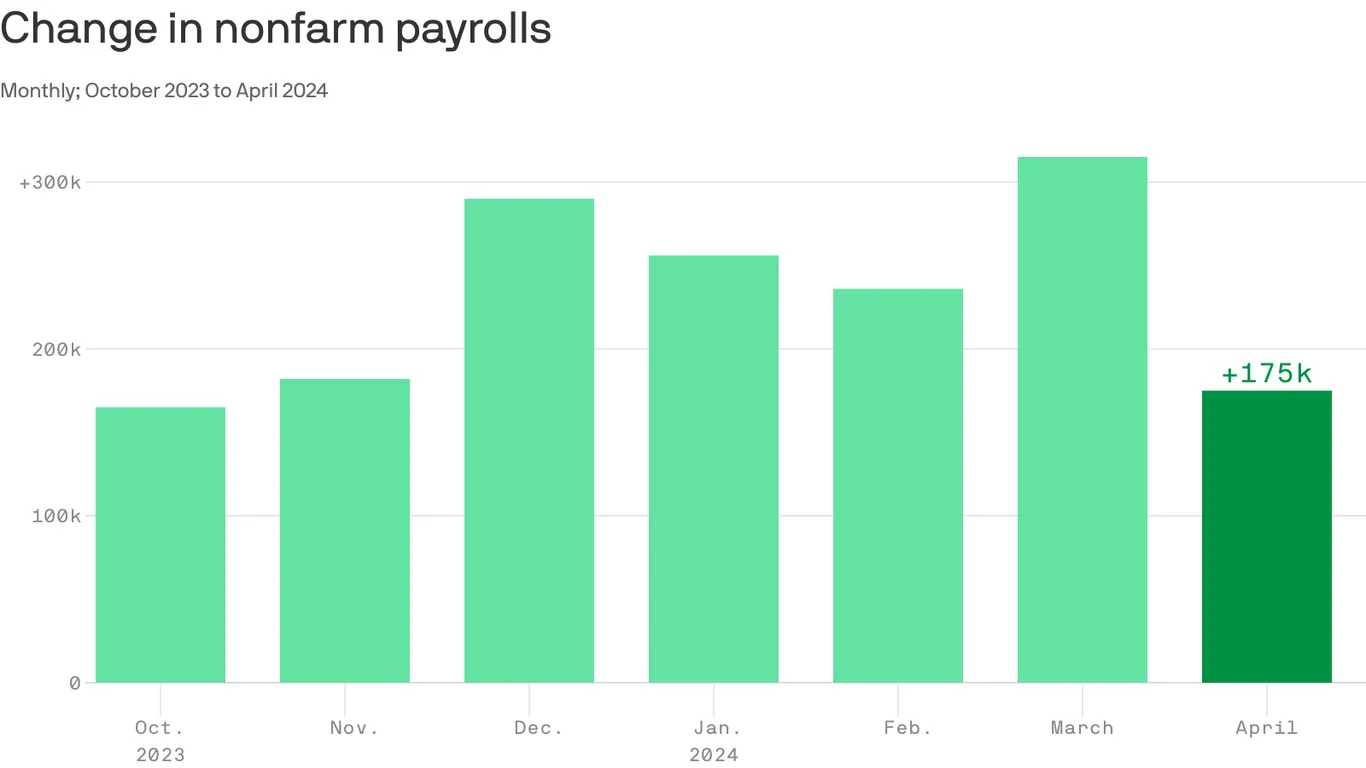

The U.S. economy added 175,000 jobs in April, while the unemployment rate ticked up to 3.9% from 3.8%, the Labor Department said on Friday.

Why it matters:

Jobs growth slowed from the prior month’s hot pace, but the data suggests that the labor market is still chugging along with healthy demand for workers.

The pace of hiring was notably slower than economists’ estimate of 240,000 jobs in April.

Job gains in March were slightly better than previously thought, upwardly revised to 315,000 from 303,000—though payrolls in February were revised lower by 34,000 to 236,000.

Driving the news:

The lower-than-expected job gains were concentrated in health care, social assistance, transportation and warehousing

Average hourly earnings, a measure of wage growth, rose 0.2%.

Over the past 12 months, average hourly earnings increased 3.9%.

State of play:

Friday’s data is the latest evidence that the labor market is holding steady — an important development for the broader economy.

The Federal Reserve this week kept interest rates at the highest level in more than two decades.

Its policymakers suggested that any rate cuts would happen later than previously thought due to stalled progress on curbing inflation.

Fed chair Jerome Powell this week said that the central bank would be “prepared to respond to an unexpected weakening in the labor market.”

Today is the federal income Tax Day. In 43 states, it’s in addition to their own income tax requirements. Last year, the federal government took in $4.6 trillion and spent $6.2 trillion including $1.9 trillion for its health programs. Overall, 2023 federal revenue decreased 15.5% and spending was down 8.4% from 2022 and the deficit increased to $33.2 trillion. Healthcare spending exceeded social security ($1.351 trillion) and defense spending ($828 billion) and is the federal economy’s biggest expense.

Along with the fragile geopolitical landscape involving relationships with China, Russia and Middle East, federal spending and the economy frame the context for U.S. domestic policies which include its health system. That’s the big picture.

Today also marks the second day of the American Hospital Association annual meeting in DC. The backdrop for this year’s meeting is unusually harsh for its members:

Increased government oversight:

Five committees of Congress and three federal agencies (FTC, DOJ, HHS) are investigating competition and business practices in hospitals, with special attention to the roles of private equity ownership, debt collection policies, price transparency compliance, tax exemptions, workforce diversity, consumer prices and more.

Medicare payment shortfall:

CMS just issued (last week) its IPPS rate adjustment for 2025: a 2.6% bump that falls short of medical inflation and is certain to exacerbate wage pressures in the hospital workforce. Per a Bank of American analysis last week, “it appears healthcare payrolls remain below pre-pandemic trend” with hospitals and nursing homes lagging ambulatory sectors in recovering.”

Persistent negative media coverage:

The financial challenges for Mission (Asheville), Steward (Massachusetts) and others have been attributed to mismanagement and greed by their corporate owners and reports from independent watchdogs (Lown, West Health, Arnold Ventures, Patient Rights Advocate) about hospital tax exemptions, patient safety, community benefits, executive compensation and charity care have amplified unflattering media attention to hospitals.

Physicians discontent:

59% of physicians in the U.S. are employed by hospitals; 18% by private equity-backed investors and the rest are “independent”. All are worried about their income. All think hospitals are wasteful and inefficient. Most think hospital employment is the lesser of evils threatening the future of their profession. And those in private equity-backed settings hope regulators leave them alone so they can survive. As America’s Physician Group CEO Susan Dentzer observed: “we knew we’re always going to need hospitals; but they don’t have to look or operate the way they do now. And they don’t have to be predicated on a revenue model based on people getting more elective surgeries than they actually need. We don’t have to run the system that way; we do run the healthcare system that way currently.”

The Value Agenda in limbo:

Since the Affordable Care Act (2010), the CMS Center for Innovation has sponsored and ultimately disabled all but 6 of its 54+ alternative payment programs. As it turns out, those that have performed best were driven by physician organizations sans hospital control. Last week’s release of “Creating a Sustainable Future for Value-Based Care: A Playbook of Voluntary Best Practices for VBC Payment Arrangements.” By the American Medical Association, the National Association of ACOs (NAACOs) and AHIP, the trade group representing America’s health insurance payers is illustrative. Noticeably not included: the American Hospital Association because value-pursuers think for hospitals it’s all talk.

National insurers hostility:

Large, corporate insurers have intensified reimbursement pressure on hospitals while successfully strengthening their collective grip on the U.S. health insurance sector. 5 insurers control 50% of the U.S. health insurance market: 4 are investor owned. By contrast, the 5 largest hospital systems control 17% of the hospital market: 1 is investor-owned. And bumpy insurer earnings post-pandemic has prompted robust price increases: in 2022 (the last year for complete data and first year post pandemic), medical inflation was 4.0%, hospital prices went up 2.2% but insurer prices increased 5.9%.

Costly capital:

The U.S. economy is in a tricky place: inflation is stuck above 3%, consumer prices are stable and employment is strong. Thus, the Fed is not likely to drop interest rates making hospital debt more costly for hospitals—especially problematic for public, safety net and rural hospitals. The hospital business is capital intense: it needs $$ for technologies, facilities and clinical innovations that treat medical demand. For those dependent on federal funding (i.e. Medicare), it’s unrealistic to think its funding from taxpayers will be adequate. Ditto state and local governments. For those that are credit worthy, capital is accessible from private investors and lenders. For at least half, it’s problematic and for all it’s certain to be more expensive.

Campaign 2024 spotlight:

In Campaign 2024, healthcare affordability is an issue to likely voters. It is noticeably missing among the priorities in the hospital-backed Coalition to Strengthen America’s Healthcare advocacy platform though 8 states have already created “affordability” boards to enact policies to protect consumers from medical debts, surprise hospital bills and more.

Understandably, hospitals argue they’re victims. They depend on AHA, its state associations, and its alliances with FAH, CHA, AEH and other like-minded collaborators to fight against policies that erode their finances i.e. 340B program participation, site-neutral payments and others. They rightfully assert that their 7/24/365 availability is uniquely qualifying for the greater good, but it’s not enough. These battles are fought with energy and resolve, but they do not win the war facing hospitals.

AHA spent more than $30 million last year to influence federal legislation but it’s an uphill battle. 70% of the U.S. population think the health system is flawed and in need of transformative change. Hospitals are its biggest player (30% of total spending), among its most visible and vulnerable to market change.

Some think hospitals can hunker down and weather the storm of these 8 challenges; others think transformative change is needed and many aren’t sure. And all recognize that the future is not a repeat of the past.

For hospitals, including those in DC this week, playing victim is not a strategy. A vision about the future of the health system that’s accessible, affordable and effective and a comprehensive plan inclusive of structural changes and funding is needed. Hospitals should play a leading, but not exclusive, role in this urgently needed effort.

Lacking this, hospitals will be public utilities in a system of health designed and implemented by others.

Tuesday, the, FTC, and DOJ announced creation of a task force focused on tackling “unfair and illegal pricing” in healthcare. The same day, HHS joined FTC and DOJ regulators in launching an investigation with the DOJ and FTC probing private equity’ investments in healthcare expressing concern these deals may generate profits for corporate investors at the expense of patients’ health, workers’ safety and affordable care.

Thursday’s State of the Union address by President Biden (SOTU) and the Republican response by Alabama Senator Katey Britt put the spotlight on women’s reproductive health, drug prices and healthcare affordability.

Friday, the Senate passed a $468 billion spending bill (75-22) that had passed in the House Wednesday (339-85) averting a government shutdown. The bill postpones an $8 billion reduction in Medicaid disproportionate share hospital payments for a year, allocates $4.27 billion to federally qualified health centers through the end of the year and rolls back a significant portion of a Medicare physician pay cut that kicked in on Jan. 1. Next, Congress must pass appropriations for HHS and other agencies before the March 22 shutdown.

And all week, the cyberattack on Optum’s Change Healthcare discovered February 21 hovered as hospitals, clinics, pharmacies and others scrambled to manage gaps in transaction processing. Notably, the American Hospital Association and others have amplified criticism of UnitedHealth Group’s handling of the disruption, having, bought Change for $13 billion in October, 2022 after a lengthy Department of Justice anti-trust review. This week, UHG indicates partial service of CH support will be restored. Stay tuned.

Just another week for healthcare: Congressional infighting about healthcare spending. Regulator announcements of new rules to stimulate competition and protect consumers in the healthcare market. Lobbying by leading trade groups to protect funding and disable threats from rivals. And so on.

At the macro level, it’s understandable: healthcare is an attractive market, especially in its services sectors. Since the pandemic, prices for services (i.e. physicians, hospitals et al) have steadily increased and remain elevated despite the pressures of transparency mandates and insurer pushback. By contrast, prices for most products (drugs, disposables, technologies et al) have followed the broader market pricing trends where prices for some escalated fast and then dipped.

While some branded prescription medicines are exceptions, it is health services that have driven the majority of health cost inflation since the pandemic.

UnitedHealth Group’s financial success is illustrative:

it’s big, high profile and vertically integrated across all major services sectors. In its year end 2023 financial report (January 12, 2024) it reported revenues of $371.6 Billion (up 15% Year-Over-Year), earnings from operations up 14%, cash flows from operations of $29.1 Billion (1.3x Net Income), medical care ratio at 83.2% up from 82% last year, net earnings of $23.86/share and adjusted net earnings of $25.12/share and guidance its 2024 revenues of $400-403 billion. They buy products using their scale and scope leverage to pay less for services they don’t own less and products needed to support them. It’s a big business in a buyer’s market and that’s unsettling to many.

Big business is not new to healthcare:

it’s been dominant in every sector but of late more a focus of unflattering regulator and media attention. Coupled with growing public discontent about the system’s effectiveness and affordability, it seems it’s near a tipping point.

David Johnson, one of the most thoughtful analysts of the health industry, reminded his readers last week that the current state of affairs in U.S. healthcare is not new citing the January 1970 Fortune cover story “Our Ailing Medical System”

“American medicine, the pride of the nation for many years, stands now on the brink of chaos. To be sure, our medical practitioners have their great moments of drama and triumph. But much of U.S. medical care, particularly the everyday business of preventing and treating routine illnesses, is inferior in quality, wastefully dispensed, and inequitably financed…

Whether poor or not, most Americans are badly served by the obsolete, overstrained medical system that has grown up around them helter-skelter. … The time has come for radical change.”

Johnson added: “The healthcare industry, however, cannot fight gravity forever. Consumerism, technological advances and pro-market regulatory reforms are so powerful and coming so fast that status-quo healthcare cannot forestall their ascendance. Properly harnessed, these disruptive forces have the collective power necessary for U.S. healthcare to finally achieve the 1970 Fortune magazine goal of delivering “good care to every American with little increase in cost.”

He’s right.

I believe the U.S. health system as we know it has reached its tipping point. The big-name organizations in every sector see it and have nominal contingency plans in place; the smaller players are buying time until the shoe drops. But I am worried.

I am worried the system’s future is in the hands of hyper-partisanship by both parties seeking political advantage in election cycles over meaningful creation of a health system that functions for the greater good.

I am worried that the industry’s aversion toprice transparency, meaningful discussion about affordability and consistency in defining quality, safety and value will precipitate short-term gamesmanship for reputational advantage and nullify systemness and interoperability requisite to its transformation.

I am worried that understandably frustrated employers will drop employee health benefits to force the system to needed accountability.

I am worried that the growing armies of under-served and dissatisfied populations will revolt.

I am worried that its workforce is ill-prepared for a future that’s technology-enabled and consumer centric.

I am worried that the industry’s most prominent trade groups are concentrating more on “warfare” against their rivals and less about the long-term future of the system.

I am worried that transformational change is all talk.

It’s time to start an adult conversation about the future of the system. The starting point: acknowledging that it’s not about bad people; it’s about systemic flaws in its design and functioning. Fixing it requires balancing lag indicators about its use, costs and demand with assumptions about innovations that hold promise to shift its trajectory long-term. It requires employers to actively participate: in 2009-2010, Big Business mistakenly chose to sit out deliberations about the Affordable Care Act. And it requires independent, visionary facilitation free from bias and input beyond the DC talking heads that have dominated reform thought leadership for 6 decades.

Or, collectively, we can watch events like last week’s roll by and witness the emergence of a large public utility serving most and a smaller private option for those that afford it. Or something worse.

P.S. Today, thousands will make the pilgrimage to Orlando for HIMSS24 kicking off with a keynote by Robert Garrett, CEO of Hackensack Meridian Health tomorrow about ‘transformational change’ and closing Friday with a keynote by Nick Saban, legendary Alabama football coach on leadership. In between, the meeting’s 24 premier supporters and hundreds of exhibitors will push their latest solutions to prospects and customers keenly aware healthcare’s future is not a repeat of its past primarily due to technology. Information-driven healthcare is dependent on technologies that enable cost-effective, customized evidence-based care that’s readily accessible to individuals where and when they want it and with whom.

And many will be anticipating HCA Mission Health’s (Asheville NC) Plan of Action response due to CMS this Wednesday addressing deficiencies in 6 areas including CMS Deficiency 482.12 “which ensures that hospitals have a responsible governing body overseeing critical aspects of patient care and medical staff appointments.” Interest is high outside the region as the nation’s largest investor-owned system was put in “immediate jeopardy” of losing its Medicare participation status last year at Mission. FYI: HCA reported operating income of $7.7 billion (11.8% operating margin) on revenues of $65 billion in 2023.

Inflation moderated as economists forecasted last month, according to the Federal Reserve’s favored inflation metric, bringing welcome news for investors, home buyers and consumers alike looking for interest rate cuts.

KEY FACTS

Americans spent 2.4% more in January than they did in January 2023, according to the personal consumption expenditures (PCE) price index released Thursday morning by the Bureau of Economic Analysis.

That meets consensus economist estimates of 2.4% annual PCE inflation and comes in lower than last month’s 2.6%.

It’s the lowest PCE reading since March 2021.

Core PCE inflation, which tracks expenditures for goods and services other than the less sticky food and services inputs, was 2.8% in January, in line with forecasts of 2.8%.

It’s similarly the lowest core PCE reading since March 2021 and checks in significantly lower than January 2023’s 4.7% inflation.

KEY BACKGROUND

Core PCE inflation, which is Fed Chairman Jerome Powell’s inflation measure of choice, is still well above the Fed’s long-term 2% target.

Earlier this month, PCE’s sister consumer price index (CPI)revealed far worse CPI inflation than economists projected, sending the S&P 500 stock index to its biggest loss in almost 12 months as sticky inflation would likely cause the Fed to delay the much-anticipated rate cuts until more tangible progress toward 2% inflation is apparent. CPI measures the average prices nationwide of a predetermined basket of goods and services, while PCE measures how much Americans actually spend monthly, earning the latter policymakers’ affection as it arguably paints a better picture of the health of Americans’ wallets.

The series of hotter than anticipated inflation data has dramatically pushed back expectations of when and by how much the Fed will slash rates in 2024. Higher inflation typically keeps rates higher for longer, making loans such as mortgages more expensive, exemplified by mortgage rates more than doubling over the last two years to their highest levels since the turn of the century.

The futures market currently prices in June as the most likely date of the first cut and 75 basis points of cuts as the most likely outcome, according to the CME Group’s FedWatch Tool, much softer than a month ago’s implied forecasts of the first reduction coming in May and 125 basis points of cuts.

The U.S. economy added 353,000 jobs in January, while the unemployment rate held at 3.7%, the Labor Department said Friday.

Why it matters:

The first look at the 2024 labor market shows it’s on fire — not slowing down as previously thought.

Details:

The January payroll figures show hiring picked up from the 333,000 added the prior month, which itself was revised higher by 117,000.

Job gains in November were revised slightly higher, too, by 9,000 to 182,000 jobs added.

What’s new:

The hiring boom last month came amid strong job gains in health care, retail and professional and business services, while mining and oil and gas extraction are among the sectors that shed jobs.

Meanwhile, the labor force participation rate — the share of workers with or looking for a job — was 62.5% in January.

Average hourly earnings, a measure of wage growth, soared by 0.6%. Over the past 12 month, average hourly earnings increased by 4.5%.

The big picture:

The data is the latest in recent weeks to show that the economy is revving up, with fading inflation and steady hiring — a welcome development for the Biden administration that is touting its economic agenda ahead of the 2024 election.

The intrigue:

The strong growth in both jobs and earnings will make the Federal Reserve reluctant to cut interest rates soon, out of fear that labor market strength could reverse progress on inflation.

Already this week, Fed chair Jerome Powell threw cold water on the idea of a March rate cut.

The bottom line:

Despite high profile layoffs at media and technology companies, the report shows that broader labor market is heating up.

Forget the much-discussed prospect of a soft landing for the U.S. economy. In 2023, there was no landing at all.

Why it matters:

Big economic rules broke last year. The latest data to confirm that is the new GDP report showing very strong economic growth to conclude 2023, even amid a big cooldown in inflation.

Mainstream economists and policymakers believed a period of below-trend growth would be necessary to make progress on inflation.

Instead, above-trend growth in 2023 coincided with inflation falling sharply, reflecting improvement in the economy’s supply potential.

Driving the news:

The economy expanded at a 3.3% annualized rate in the fourth quarter, well above the 2% forecasters expected. That followed the previous quarter’s blockbuster 4.9% growth.

GDP was 3.1% higher in the fourth quarter than a year earlier.

That represents an acceleration from 0.7% GDP growth in 2022, and trounced the growth rates of most other advanced countries — and the 1.8%-ish rate that economists consider the United States’ long-term trend.

Details:

The fourth quarter’s hot growth resulted from bustling activity across the economy.

Consumers spent more on goods and services, with personal consumption expenditures rising at a 2.8% annualized pace. That was responsible for nearly 2 percentage points of the fourth quarter’s GDP rise.

Businesses spent on equipment, factories and intellectual property at a solid pace, with nonresidential fixed investment increasing at 1.9% — up from the previous quarter.

The intrigue:

For two years now, Fed officials have spoken of the need for a period of below-trend growth to bring inflation into line. Now, they face the decision of whether to cut rates — to essentially declare victory on inflation — even as below-trend growth is nowhere to be seen.

A flourishing labor market, strong productivity gains and supply-side improvements — more workers joining the workforce, for instance — has (at least so far) meant the economy can keep growing at a solid pace without risking a pickup in price pressure.

“[W]e had significant supply-side gains with strong demand,” Fed chair Jerome Powell said in his December press conference, adding that potential growth may have been higher than usual “just because of the healing on the supply side.”

“So that was a surprise to just about everybody,” Powell said.

What they’re saying:

“This report feels like a supersonic Goldilocks: very strong GDP reading with cool inflation,” Beth Ann Bovino, chief economist at U.S. Bank, tells Axios. “Good news is good news.”

“With high productivity levels, we can have strong growth with less inflation. That was the case during the last soft landing in the 90s,” Bovino adds.

The U.S. economy added 216,000 jobs last month while the unemployment rate held at 3.7%, the Labor Department said on Friday.

Why it matters:

The final snapshot of the 2023 labor market shows hot hiring — the latest sign that the American job market continues to defy expectations of a slowdown.

The figure is well-above the roughly 170,000 jobs economists expected.

The big picture:

The Federal Reserve has hinted it likely won’t raise interest rates again with encouraging signs that inflation is easing and the labor market is cooling.

That concludes an aggressive rate hiking cycle that began in 2022 and lasted through much of last year.

For now, however, there is little evidence those rate hikes translated into pain for workers in 2022.

American consumers, however, remain dissatisfied with the economy — a problem that may continue to weigh on the Biden White House as the 2024 election heats up.

Details:

Friday’s jobs report shows the labor market stayed strong. Hiring increased in sectors including government, health care, and construction. Transportation and warehousing shed jobs.

Average hourly earnings, a measure of wages, rose by 0.4% last month. Compared to the prior year, average hourly earnings rose 4.1%.

The share of the population with in the labor force — that is, with a job or looking for one — was 62.5% in December, roughly 0.3 percentage point less than the prior month.

The Labor Department also said the economy added a combined 71,000 fewer jobs than initially estimated in October and November.

The bottom line:

The hotter-than-expected jobs figures are one of several more key economic reports due before Federal Reserve officials meet at the end of the month.