Democrat lawmakers are urging Republicans debating cuts to Medicaid to focus instead on fraud, waste and abuse in another federal healthcare program: Medicare Advantage.

Curbing upcoding in the privatized Medicare plans, wherein insurers exaggerate the health needs of their members to inflate government reimbursement, is a better avenue for saving federal dollars than restricting benefits or cutting eligibility in Medicaid, the 36 Democrats wrote in a letter to GOP leadership on Wednesday.

The letter was addressed to Senate Majority Leader John Thune, R-S.D, and House Speaker Mike Johnson, R-La., and comes as Republicans debate different policies to reach savings targets.

Dive Insight:

Republicans in Congress are aiming to extend tax cuts from President Donald Trump’s first term. Their budget directs the House Energy and Commerce Committee to cut $880 billion in spending — a goal that’s impossible to reach without touching Medicaid, which (along with its sister program for children) provides safety-net insurance to some 80 million Americans.

Now, Democrats in both chambers are urging Republicans to redirect their attention from Medicaid to MA, privatized plans for Medicare seniors that can provide additional benefits but also restrict care in a way traditional Medicare is not allowed to do. Still, the plans have steadily grown in popularity and now cover more than half of the 68 million Americans in Medicare.

“Your directive to cut federal health care spending should come from reducing waste, fraud, and abuse like upcoding by for-profit insurance companies, not by cutting health care benefits for American families who rely on Medicaid to make ends meet,” the Democrats’ letter reads.

The letter cites a Wall Street Journal investigation into upcoding published last year that found MA insurers frequently added diagnoses for their members for which their members never received treatment or that went against doctors’ observations. The practice drove a total of $50 billion in additional payments to the private insurers over three years, according to the investigation.

Similarly, influential congressional advisory group MedPAC found CMS paid MA insurers $84 billion more in 2024 than the government would have if those members had been in traditional Medicare. Upcoding was responsible for almost half of those overpayments.

Traditionally, Republicans broadly support MA, which was created on the premise that private insurers could help the government manage Medicare more economically. However, there’s been rising bipartisan support for reforming the program in light of growing evidence of practices like upcoding that inflate government reimbursement to plans without helping enrollees.

In his confirmation hearing, Dr. Mehmet Oz, the surgeon and television personality tapped by Trump as the administrator of the CMS, agreed that tackling fraud, waste and abuse in MA was a “rational” way of lowering federal healthcare spending.

“We’re actually apparently paying more for Medicare Advantage than we’re paying for regular Medicare. So it’s upside down,” Oz said in front of the Senate Finance Committee in March.

Republicans in the House are currently trying to figure out how to achieve desired savings without slashing Medicaid, given the program’s political popularity, including among Republican voters.

GOP leadership recently appeared to rule out two Medicaid policies that would cause significant upheaval for enrollees in the program: lowering the portion of Medicaid costs borne by the federal government for the Medicaid expansion population, and per-capita caps on benefits for beneficiaries in expansion states.

“Moving forward with this dangerous plan to rip health care away from low- and middle-income Americans would be a man-made disaster for the health of the nation and the economy,” the Democrats’ letter reads. “We urge you instead to listen to Administrator Oz and tackle real fraud, waste, and abuse by private, for-profit health insurers in MA.”

House E&C is expected to hold its reconciliation markup next week.

To understand the fatal attack on UnitedHealthcare CEO Brian Thompson and the unexpected reaction on social media, you have to go back to the 1990s when managed care was in its infancy. As a consumer representative, I attended meetings of a group associated with the health care system–doctors, academics, hospital executives, business leaders who bought insurance, and a few consumer representatives like me.

It was the dawn of the age of managed care with its promise to lower the cost and improve the quality of care, at least for those who were insured.

New perils came with that new age of health coverage.

In the quest to save money while ostensibly improving quality, there was always a chance that the managed care entities and the doctors they employed or contracted with – by then called managed care providers – could clamp down too hard and refuse to pay for treatments, leaving some people to suffer medically. Groups associated with the health care industry tried to set standards to guard against that, but as the industry consolidated and competition among the big players in the new managed care system consolidated, such worries grew.

Over the years the squeeze on care got tighter and tighter as the giants like UnitedHealthcare–which grew initially by buying other insurance companies such as Travelers and Golden Rule–and Elevance, which gobbled up previously nonprofit Blue Cross plans in the 1990s, starting with Blue Cross of California, needed to please the gods of the bottom line. Shareholders became all important. Paying less for care meant more profits and return to investors, so it is no wonder that the alleged killer of the UnitedHealthcare chief executive reportedly left the chilling message:

‘‘DENY. DEFEND. DEPOSE,” words associated with insurance company strategies for denying claims.

The American health care system was far from perfect even in the days when more employers offered good coverage for their workers and often paid much or all of the cost to attract workers. Not-for-profit Blue Cross Blue Shield plans in many states provided most of the coverage, and by all accounts, they paid claims promptly. In my now very long career of covering insurance, I cannot recall anyone in the old days complaining that their local Blue Cross Blue Shield organization was withholding payment for care.

Today Americans, even those who thought they had “good” coverage, are now finding themselves underinsured, as a 2024 Commonwealth Fund study so clearly shows. Nearly one-quarter of adults in the U.S. are underinsured meaning that although they have health insurance, high deductibles, copayments and coinsurance make it difficult or impossible for them to pay for needed care. As many as one-third of people with chronic conditions such as diabetes said they don’t take their medications or even fill prescriptions because they cost too much.

Before he passed away last year, one of our colleagues, Marshall Allen, had made recommendations to his followers on how to deal with medical bills they could not pay. KFF reporters also investigated the problems families face with super-high bills. In 2022 KFF reporters offered readers a thorough look at medical debt in the U.S. and reported alarming findings.

In 2019, U.S. medical debt totaled $195 billion, a sum larger than the economy of Greece. Half of adults don’t have enough cash to cover an unexpected medical bill while 50 million adults – one in five in the entire country – are paying off bills on an installment plan for their or a family member’s care.

One would think that such grim statistics might prompt political action to help ease the debt burden on American families. But a look at the health proposals from the Republican Study Committee suggest that likely won’t happen. The committee’s proposed budget would cut $4.5 trillion dollars from the Affordable Care Act, Medicaid, and the Children’s Health Insurance Program leaving millions of Americans without health care.

From the Democrats, there appear to be no earth-shaking proposals in their immediate future, either. Late last summer STAT News reported, “With the notable exception of calling to erase medical debt by working with the states, Democrats are largely eyeing marginal extensions or reinstatements of their prior policy achievements.” Goals of the Democratic National Committee were shoring up the Affordable Care Act, reproductive rights, and addressing ambulance surprise bills.

A few years ago when I was traveling in Berlin, our guide paused by a statue of Otto von Bismarck, Germany’s chancellor in the late 1800s, who is credited with establishing the German health system. The guide explained to his American travelers how and why Bismarck founded the German system, pointing out that Germany got its national health system more than a hundred years before Obamacare. Whether the Americans got the point he was making, I could not tell for no one in the group appeared interested in Germany’s health care system. Today, though, they might pay more attention.

In the coming months, I will write about health systems in Germany and other developed countries that, as The Commonwealth Fund’s research over many years has shown, do a much better job than ours at delivering high quality care – for all of their citizens – and at much lower costs.

As Donald Trump begins his second term, America’s healthcare system is in crisis: medical costs are skyrocketing, life expectancy has stagnated, and burnout runs rampant among healthcare workers.

These problems are likely to become worse now that Trump has handed the federal budget over to Elon Musk. The world’s richest man now co-heads the Department of Government Efficiency (DOGE), a non-government entity tasked with slashing $500 billion in “wasteful” spending.

The harsh reality is that Musk’s mission can’t succeed without gutting healthcare access and coverage for millions of Americans.

Deleting dollars from American healthcare

Since Trump’s first term, the country’s economic outlook has worsened significantly. In 2016, the national debt was $19 trillion, with $430 billion allocated to annual interest payments. By 2024, the debt had nearly doubled to $36 trillion, requiring $882 billion in debt service—12% of federal spending that is legally untouchable.

Add to that another 50% of government expenditures that Trump has deemed politically off-limits: Social Security ($1.35 trillion), Medicare ($848 billion) and Defense ($1.13 trillion). That leaves just $2.6 trillion—less than 40% of the $6.75 trillion federal budget—available for cuts.

In a recent op-ed, Musk and DOGE co-chair Vivek Ramaswamy proposed eliminating expired or misused funds for programs like Public Broadcasting and Planned Parenthood, but these examples account for less than $3 billion total—not even 1% of their target.

This shortfall will require Musk to cut billions in government healthcare spending. But where will he find it?

With Medicare off limits to DOGE, the options for major reductions are extremely limited. Big-ticket healthcare items like the $300 billion in tax-deductibility for employer-sponsored health insurance and $120 billion in expired health programs for veterans will prove politically untouchable. One will raise taxes for 160 million working families and the latter will leave veterans without essential medical care.

This means DOGE will have to attack Medicaid and the ACA health exchanges. Here’s how 20 million people will likely lose coverage as a result.

1. Reduced ACA exchange funding

Since its enactment in 2010, the Affordable Care Act (ACA) has provided premium subsidies to Americans earning 100% to 400% of the federal poverty level. For lower-income families, the ACA also offers Cost Sharing Reductions, which help offset deductibles and co-payments that fund 30% of total medical costs per enrollee. Without CSRs, a family of four earning $40,000 could face deductibles as high as $5,000 before their insurance benefits apply.

If Congress allows CSR payments to expire in 2026, federal spending would decrease by approximately $35 billion annually. If that happens, the Congressional Budget Office expects 7 million individuals to drop out of the exchanges. Worse, without affordable coverage alternatives, 4 million families would lose their health insurance altogether.

2. Slashing Medicaid coverage and tightening eligibility

Medicaid currently provides healthcare for over 90 million low-income Americans, including children, seniors and individuals with disabilities. To meet DOGE’s $500 billion goal, several cost-cutting strategies appear likely:

Reversing Medicaid expansion: The ACA expanded Medicaid eligibility to those earning up to 138% of the federal poverty level, reducing the uninsured rate from 16% to 8%. Undoing this expansion would strip coverage from millions in the 40 states that adopted the program.

Imposing work requirements: Proponents argue this could encourage employment, but most Medicaid recipients already work for employers that don’t provide insurance. In reality, work requirements primarily create bureaucratic barriers that disqualify millions of eligible individuals, reducing program costs at the expense of coverage.

Switching to block grants: Unlike the current Medicaid system, which adjusts funding based on need, less-expensive block grants would provide states with fixed allocations. This will, however, force them to cut services and reduce enrollment.

Medicaid currently costs $800 billion annually, with the federal government covering 70%. Reducing enrollment by 10% (9 million people) could save over $50 billion annually, while a 20% reduction (18 million people) could save $100 billion.

Either outcome would devastate families by eliminating access to vital services including prenatal care, vaccinations, chronic disease management and nursing home care. As states are forced to absorb the financial burden, they’ll likely cut education budgets and reduce infrastructure investments.

The first 100 days

The numbers don’t lie: Musk and DOGE could slash Medicaid funding and ACA subsidies to achieve much of their $500 billion target. But the human cost of this approach would be staggering.

Fortunately, there are alternative solutions that would reduce spending without sacrificing quality. Shifting provider payments in ways that reward better outcomes rather than higher volumes, capping drug prices at levels comparable to peer nations, and leveraging generative AI to improve chronic disease management could all drive down costs while preserving access to care.

These strategies address the root causes of high medical spending, including chronic diseases that, if better managed, could prevent 30-50% of heart attacks, strokes, cancers, and kidney failures according to CDC estimates.

Yet, in their pursuit of immediate budgetary cuts, Musk and DOGE have omitted these kinds of reform options. As a result, the health of millions of Americans is at major risk.

A few weeks ago The Commonwealth Fund, a philanthropic organization in New York City, which keeps tabs on health care trends, released an ominous study signaling that the bedrock of the U.S. health system is in trouble.

The study found that the employer insurance market, where millions of Americans have received good, affordable coverage since the end of World War II, could be in jeopardy. The continuing rise in the costs of medical care, and the insurance premiums to pay for it, may well cause employers to make cutbacks, leaving millions of workers uninsured or underinsured, often with no way to pay for their care and the prospect of debt for the rest of their lives.

Indeed the Fund revealed that 23% of adults in the U.S. are underinsured, meaning that though they were covered by health insurance, high deductibles and coinsurance made it difficult or impossible to pay for the care they needed.

“They have health plans that don’t provide affordable access to care,” said Sara Collins, senior adviser and vice president at the Fund. “They have out-of-pocket costs and deductibles that are high relative to their income.”

This predicament has forced many to assume medical debt or skip needed care. The Fund found that as many as one-third of people with chronic conditions like heart failure and diabetes reported they don’t take their medication or fill prescriptions because they cost too much.

Others did not go to a doctor when they were sick, skipping a recommended follow-up visit or test, and did not see a specialist when one was recommended. Nearly half of the respondents reported they did not get care for an ongoing condition because of the cost. Two out of five working-age adults who reported a delay or skipped care told researchers their health problem had gotten worse. Those findings belie the narrative, deployed when changes to the system are discussed, that America has the best health care in the world, and we dare not change it.

The seeds of today’s underinsurance predicament were planted in the 1990s when the system’s players decided remedies were needed to curb Americans’ appetite for medical interventions.

They devised managed care, with its HMOs, PPOs, insurance company approvals, and other restrictions that are with us today. But health care is far more expensive than it was in the ’90s, leaving patients to struggle to pay the higher prices, or, as the study shows, go without needed care.

Perhaps one of the study’s most striking findings is that a vast majority of underinsured workers had employer insurance plans, which over the decades had provided good coverage. Researchers concluded that recent cost containment measures were simply shifting more costs to workers through higher deductibles and coinsurance.

I checked in with Richard Master, the CEO of MCS Industries in Easton, Pennsylvania. We’ve talked over the years about the rising cost of health insurance for his 91 workers who make picture frames and wall decorations. This year, he was expecting a 5 to 6% increase in insurance rates.

A family plan now costs more than $39,000, he said, adding that “29% of people with employee plans are underinsured and have high out-of-pocket costs.”

To help reduce his own costs, he told me he has put in place a high-deductible plan and was setting up health saving accounts that allow him to give a sum of money to each worker to use for their medical expenses.

As health insurance premiums continue to rise, more employers will likely heap more of those rising costs onto workers, many of whom will inevitably have a tough time paying for them.

Every time there has been a hint in the air that maybe, just maybe, America might embrace a universal system like peer nations across the globe that offer health care to all their citizens, the special interests—doctors, hospitals, insurers, employers, and others that benefit financially from the current system have snuffed out any possibility that might happen, worried that such a system could affect their profits.

For as long as I can remember, the public has been told America has the best health care system in the world. Major holes in our system exposed by The Commonwealth Fund belie that assumption.

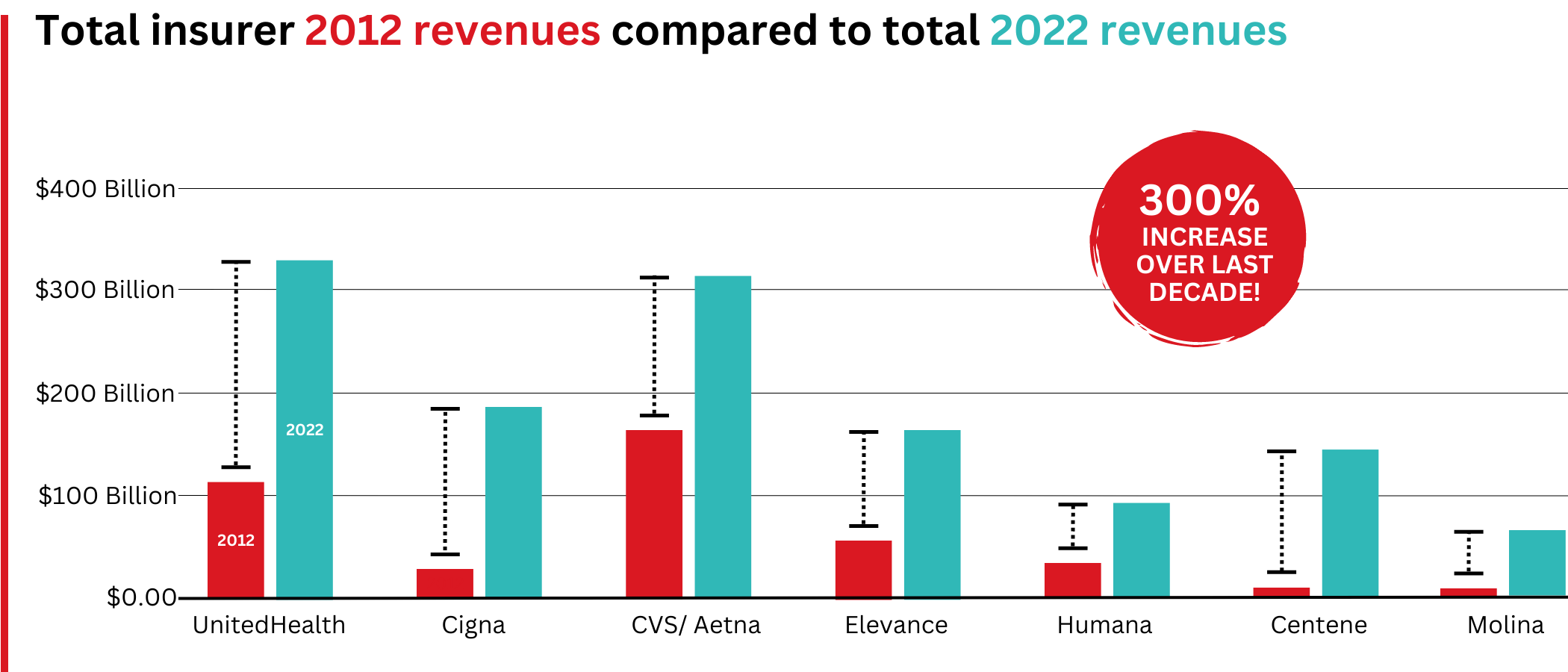

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare replacement plans they call Medicare Advantage.

The for-profits now control more than 80% of the national PBM market and more than 70% of the Medicare Advantage market.

In 2022, Big Insurance revenues reached $1.25 trillion and profits soared to $69.3 billion.

That’s a 300% increase in revenue and a 287% increase in profits from 2012, when revenue was $412.9 billion and profits were $24 billion.

Big insurers’ revenues have grown dramatically over the past decade, the result of consolidation in the PBM business and taxpayer-supported Medicare and Medicaid programs.

Sucking billions out of the pharmacy supply chain – and taxpayers’ pockets

What has changed dramatically over the decade is that the big insurers are now getting far more of their revenues from the pharmaceutical supply chain and from taxpayers as they have moved aggressively into government programs. This is especially true of Humana, Centene, and Molina, which now get, respectively, 85%, 88%, and 94% of their health-plan revenues from government programs.

The two biggest drivers are their fast-growing pharmacy benefit managers (PBMs), the relatively new and little-known middleman between patients and pharmaceutical drug manufacturers, and the privately owned and operated Medicare replacement plans they market as Medicare Advantage.

With the exception of Humana, Centene, and Molina, most of the companies that constitute Big Insurance continue to make substantial amounts of money selling policies and services in what they refer to as their commercial businesses – to individuals, families, and employers – but the seven companies’ commercial revenue grew just 260%, or $176 billion, over 10 years (from $110.4 billion to $287.1 billion). While that’s significant, profitable growth in the commercial sector has become a major challenge for big insurers – so much so that Humana just last week announced it is exiting the employer-sponsored health-insurance marketplace entirely.

The percentage of U.S. employers providing some level of health benefits to their workers dropped from 69% to 51% between 1999 and 2022 – including a dramatic 8% decrease last year alone. Growth in this category is largely the result of insurers “stealing market share” from each other or from smaller competitors.

As a consequence of this segment’s relative stagnation, PBMs and government programs have become the new cash cows for Big Insurance.

Spectacular PBM Growth

PBM HIGHLIGHTS

Cigna now gets far more revenue from its PBM than from its health plans. CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores.

UnitedHealth has the biggest share of both the PBM and Medicare markets and, through numerous acquisitions of physician practices, is now the largest U.S. employer of doctors.

PBMs are middlemen companies that manage prescription drug benefits for health insurers, Medicare Part D drug plans, employers, and, in some cases, unions. As the Commonwealth Fund has noted:

PBMs have a significant behind-the-scenes impact in determining total drug costs for insurers, shaping patients’ access to medications, and determining how much pharmacies are paid.

The Commonwealth Fund went on to say that PBMs have faced growing scrutiny about their role in rising prescription drug costs and spending. A big reason for the scrutiny – by Congress, state lawmakers and now also by the FTC – is that the biggest PBMs are now owned by Big Insurance.

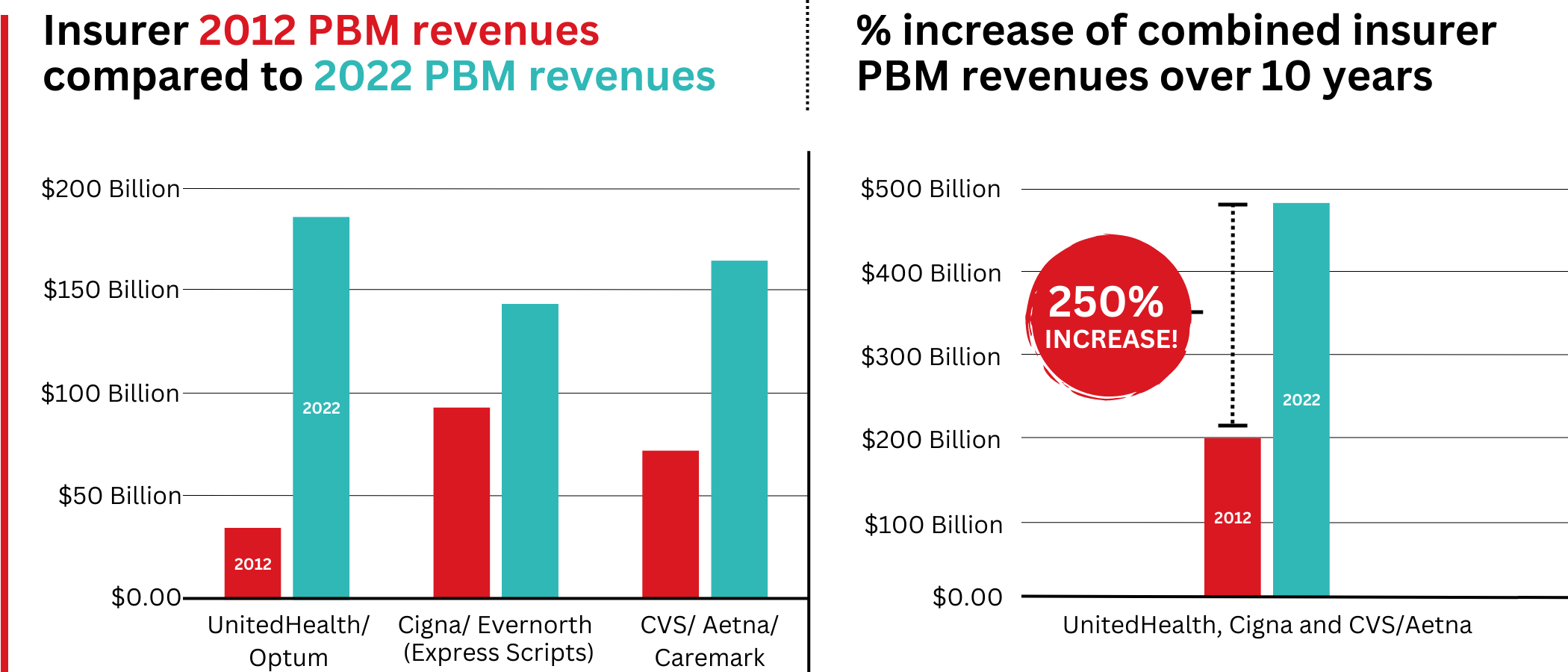

Through mergers and acquisitions in recent years, three of the seven for-profit insurers – Cigna, CVS/Aetna, and UnitedHealth – now control 80% of the U.S. pharmacy benefits market.

They determine which drugs will be listed in each of their formularies (lists of drugs they will “cover” based on secret deals they negotiate with pharmaceutical companies) and how much patients will have to pay out of their own pockets at the pharmacy counter – in many cases hundreds or thousands of dollars – before their coverage kicks in. The PBMs also “steer” health-plan enrollees to their preferred or owned pharmacies (and, increasingly, away from independent pharmacists), thereby capturing even more of what we spend on our prescription medications.

Cigna, CVS/Aetna, and UnitedHealth now control 80% of the U.S. PBM market. Correction: this graph was initially published with inaccurate numbers. The source for this information can be found here.

Ten years ago, PBMs contributed relatively little to the three companies’ revenues and profits. But since then, the rapid growth of PBMs has transformed all of the companies. The combined revenues from their PBM business units increased 250% between 2012 and 2022, from $196.7 billion to $492.4 billion.

Changes in PBM revenues between 2012 and 2022 for UnitedHealth Group, Cigna, and CVS/Aetna (Editor’s note: Cigna acquired PBM Express Scripts in 2018. To reflect revenue growth, Express Scripts’ pre-acquisition 2012 revenues are included in the Cigna total for that year.)

PBM Profit Generation

The PBM profit growth at the three companies over the past decade was even more dramatic than revenue growth. Collectively, their PBM profits increased 438%, from $6.3 billion in 2012 to $27.6 billion in 2022.

As a result of this fast growth, more than half (52%) of three companies’ profits in 2022 came from their PBM business units: Cigna’s Evernorth, CVS/Aetna’s Caremark, and UnitedHealth’s Optum. Cigna now gets far more revenue and profits from its PBM than from its health plans. And CVS gets more revenue from its PBM than from either Aetna’s health plans or its nearly 10,000 retail stores. (The companies’ business units that include their PBMs have also moved aggressively in recent years into health-care delivery through acquisitions of physician practices, clinics, dialysis centers, and other facilities. Notably, UnitedHealth Group is now the largest U.S. employer of physicians.)

Huge strides in privatizing both Medicare and Medicaid

GOVERNMENT PROGRAMS HIGHLIGHTS

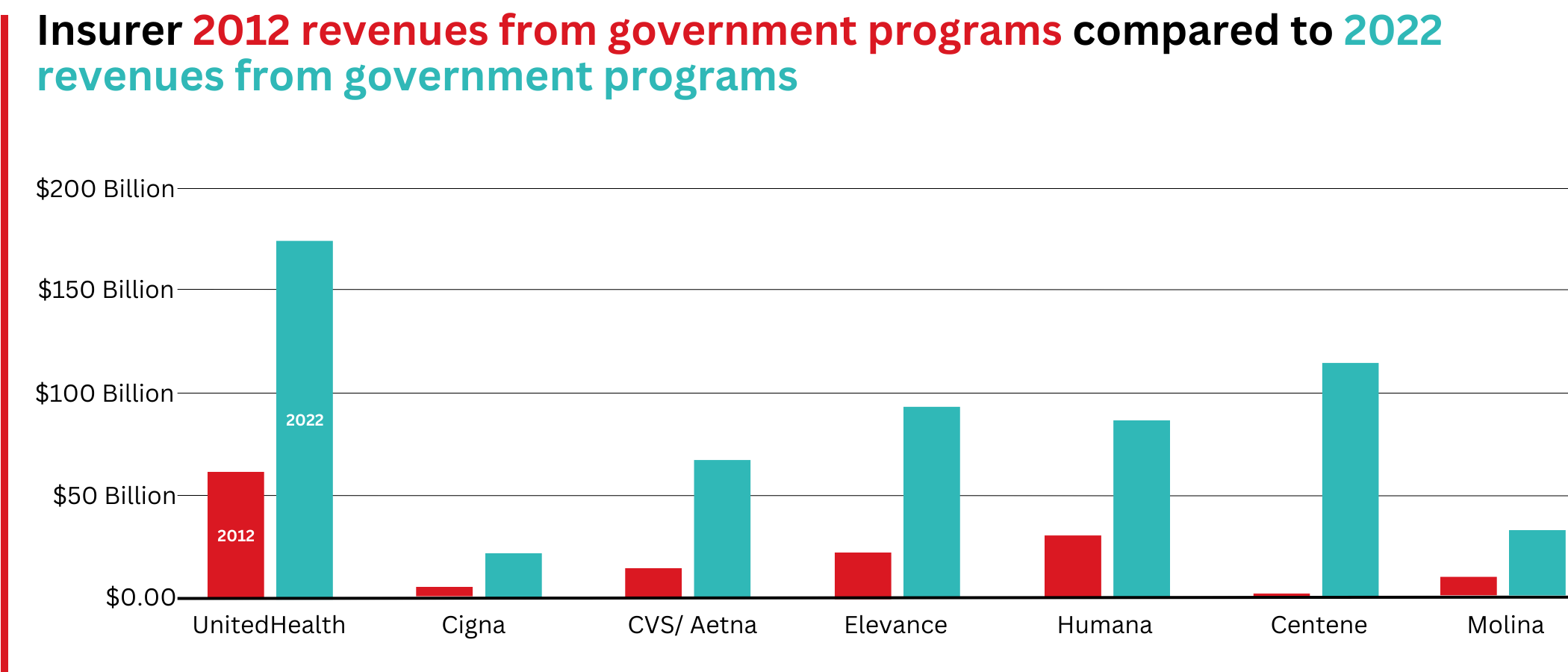

More than 90% of health-plan revenues at three of the companies come from government programs as they continue to privatize both Medicare and Medicaid, through Medicare Advantage in particular.

Enrollment in government-funded programs increased by 261% in 10 years; by contrast commercial enrollment increased by just 10% over the past decade.

Commercial enrollment actually declinedat both UnitedHealth and Humana.

85% of Humana’s health-plan members are in government-funded programs; at Centene, it is 88%, and at Molina, it is 94%.

The big insurers now manage most states’ Medicaid programs – and make billions of dollars for shareholders doing so – but most of the insurers have found that selling their privately operated Medicare replacement plans is even more financially rewarding for their shareholders.

Revenue growth from government programs has been dramatic over the past 10 years. (Note the numbers do not include revenue from the Medicare Part D program, federal subsidy payments for many ACA marketplace plan enrollees, or Medicare supplement policies.)

This is especially apparent when you see that the Big Seven’s combined revenues from taxpayer-supported programs grew 500%, from $116.3 billion in 2012 to $577 billion in 2022.

These numbers should be of interest to the Biden administration and members of Congress, many of whom are calling for much greater scrutiny of the Medicare Advantage program. Numerous media and government reports have shown that the federal government is overpaying private insurers billions of dollars a year, largely because of loopholes in laws and regulations that enable them to get more taxpayer dollars by claiming their enrollees are sicker than they really are. The companies also make aggressive use of prior authorization, largely unknown in traditional Medicare, to avoid paying for doctor-ordered care and medications.

In addition to their focus on Medicare and Medicaid, the companies also profit from the generous subsidies the government pays insurers to reduce the premiums they charge individuals and families who do not qualify for either Medicare or Medicaid or who work for an employer that does not offer subsidized coverage. But many people enrolled in those types of plans – primarily through the health insurance “marketplaces” established by the Affordable Care Act – cannot afford the deductibles and other out-of-pocket requirements they must pay before their insurers will begin paying their medical claims.

Dramatic Enrollment Shifts

Changes in health-plan enrollment over the past decade show how dramatic this shift has been. Between 2012 and 2022, enrollment in the companies’ private commercial plans increased by 10%, from 85.1 million in 2012 to 93.8 million in 2022.

By comparison, growth in enrollment in taxpayer-supported government programs increased 261%, from 27 million in 2012 to 70.4 million in 2022.

For-profit insurers dominate the Medicare Advantage market. Note that Anthem mentioned above is now known as Elevance. It owns 14 of the country’s Blue Cross Blue Shield plans.

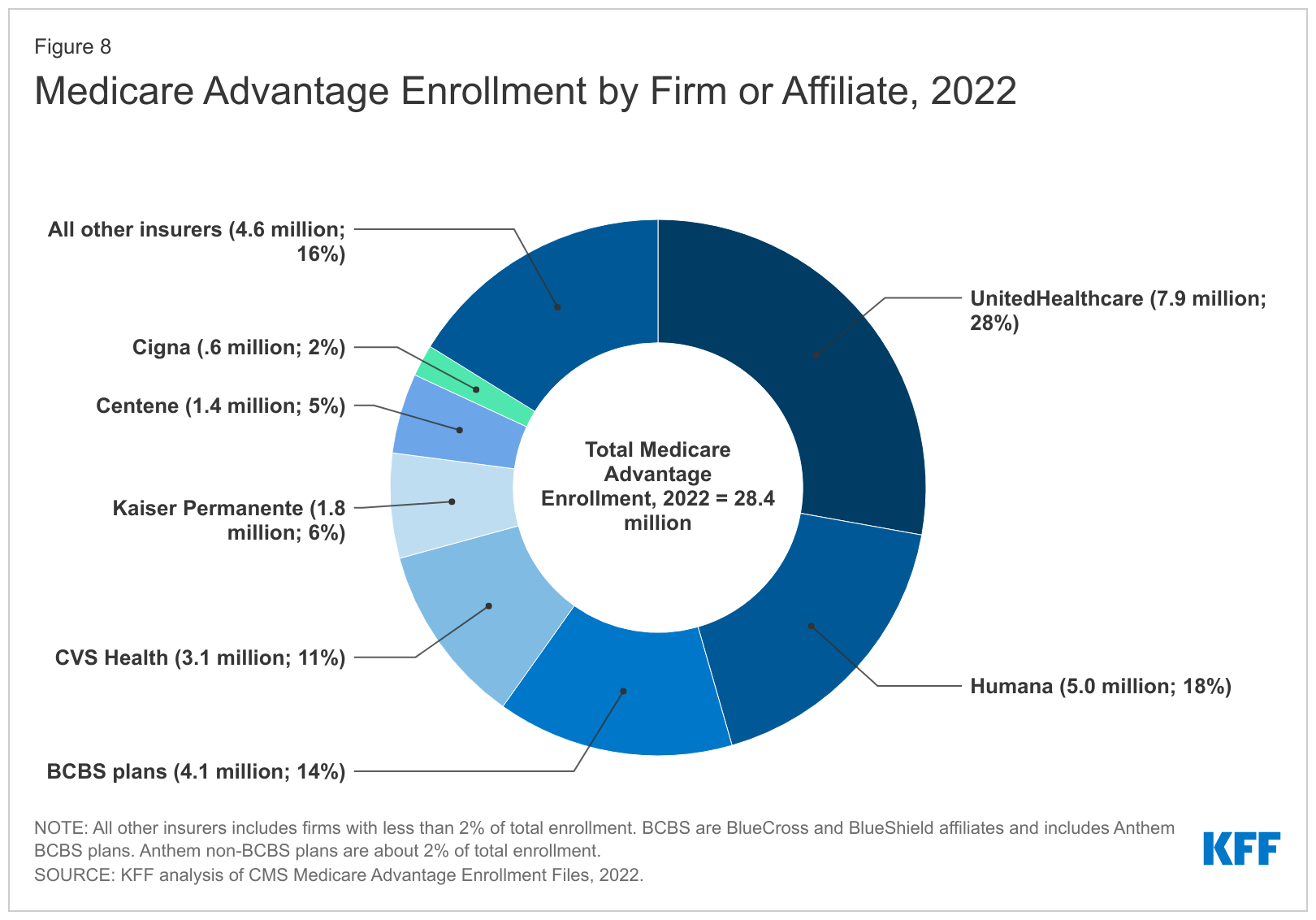

Within that category, Medicare Advantage enrollment among the Big Seven increased 252%, from 7.8 million in 2012 to 19.7 million in 2022.

Nationwide, enrollment in Medicare Advantage plans increased to 28.4 million in 2022 (and to 30 million this year). That means that the Big Seven for-profit companies control more than 70% of the Medicare Advantage market.

UnitedHealth, Humana, Elevance, and CVS/Aetna have captured most of the Medicare Advantage market since the Affordable Care Act was passed in 2010.

The remaining growth in the government segment occurred in the Medicaid programs that a subset of the Big Seven (UnitedHealth, Elevance, Centene, and Molina in particular) manages for several states.

A few other facts and figures to keep in mind as Big Insurance thrives:

100 million of us – almost one of every three people in this country – now have medical debt.

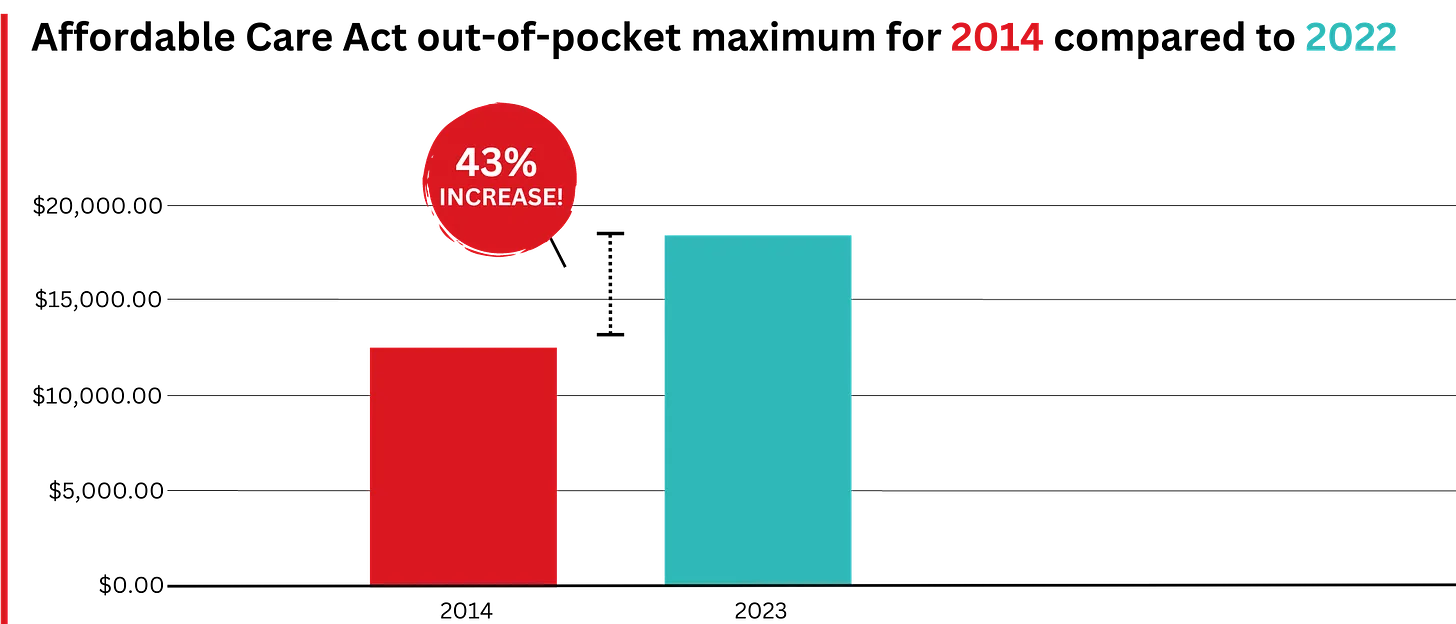

In 2023, U.S. families can be on the hook for up to $18,200 in out-of-pocket requirements before their coverage kicks in, up 43% since 2014 when it was $12,700.The Affordable Care Act allows the out-of-pocket maximum to increase annually – 43% since the maximum limit went into effect in 2014.

44% of people in the United States who purchased coverage through the individual market and (ACA) marketplaces were underinsured or functionally uninsured.

42% said they hadproblems paying medical bills or were paying off medical debt.

Half (49%) said they would be unable to pay an unexpected medical bill within 30 days, including 68% of adults with low income, 69% of Black adults, and 63% of Latino/Hispanic adults.

In 2021, about $650 million, or about one-third of all funds raised by GoFundMe, went to medical campaigns. That’s not surprising when you realize that in the United States, even people with insurance all too often feel they have no choice but to beg for money from strangers to get the care they or a loved one needs.

Even as we spend about $4.5 trillion on health care a year, Americans are now dying younger than people in other wealthy countries. Life expectancy in the United States actually decreased by 2.8 years between 2014 and 2021, erasing all gains since 1996, according to the Centers for Disease Control and Prevention.

BOTTOM LINE:

The companies that comprise Big Insurance are vastly different from what they were just 10 years ago, but policymakers, regulators, employers, and the media have so far shown scant interest in putting their business practices under the microscope.

Changes in federal law, including the Medicare Modernization Act of 2003, which created the lucrative Medicare Advantage market, and the Affordable Care Act of 2010, which gave insurers the green light to increase out-of-pocket requirements annually and restrict access to care in other ways, opened the Treasury and Medicare Trust Fund to Big Insurance. In addition, regulators have allowed almost all of their proposed acquisitions to go forward, which has created the behemoths they are today.

CVS/Health is now the 4th largest company on the Fortune 500 list of American companies. UnitedHealth Group is now No. 5 – and all the others are climbing toward the top 10.

I never met Brian Thompson. His senseless death is first and foremost a human tragedy.

Second, it’s a business story that continues to unfold. Speculation about the shooter’s motive and whereabouts runs rampant.

But media attention has seized on a larger theme: the business of health insurance and its role in U.S. healthcare.

Headlines like these illustrate the storyline that has evolved in response to the killing: health insurance is part of a complicated industry where business practices are often geared to corporate profit.

Some on Social Media See Suspect in C.E.O. Killing as a Folk Hero New York Times

In this coverage and social media postings, health insurer denials are the focal point: journalists and commentators have seized on the use of Artificial intelligence-based tools used by plans like United, Cigna, Aetna and most others to approve/deny claims and Thompson’s role as CEO of UHG’s profitable insurance division.

The bullet-casing etchings “Deny. Defend. Depose” is now a T-shirt whistle to convey a wearer’s contempt for corporate insurers and the profit-seeking apparatus in U.S. healthcare.

Laid bare in the coverage of Brian’s death is this core belief: the majority of Americans think the U.S. health system is big business and fundamentally flawed.

As noted in last week’s Gallup Poll, and in previous polling by Pew, Harris, Kaiser Family Foundation and Keckley, only one in three Americans believe the health system performs well. Accessibility, costs, price transparency and affordability are dominant complaints. They believe the majority of health insurers, hospitals and prescription drug companies put their financial interests above the public’s health and wellbeing. They accept that the health system is complex and expensive but feel helpless to fix it.

This belief is widely held: its pervasiveness and intensity lend to misinformation and disinformation about the system and its business practices.

Data about underlying costs and their relationship to prices are opaque and hard to get. Clinical innovation and quality of care are understood in the abstract: self-funded campaigns touting Top 100 recognition, Net Promoter Scores are easier. The business of healthcare financing and delivery is not taught: personal experiences with insurers, hospitals, physicians and drugs are the basis for assessing the system’s effectiveness…and those experiences vary widely based on individual/household income, education, ethnicity and health status.

The majority accept that operators in every sector of healthcare apply business practices intended to optimize their organization’s finances. Best practices for every insurer, hospital, drug/device manufacturer and medical practice include processes and procedures to maximize revenues, minimize costs and secure capital for growth/innovation.

But in healthcare, the notion of profit remains problematic: how much is too much? and how an organization compensates its leaders for results beyond short-term revenue/margin improvement are questions of growing concern to a large and growing majority of consumers.

In every sector, key functions like these are especially prone to misinformation, disinformation and public criticism:

Among insurers, provider credentialing, coverage allowance and denial management, complaint management and member services, premium pricing and out-of-pocket risks for enrollees, provider reimbursement, prior authorization, provider directory accuracy, the use of AI in plan administration and others.

Among hospitals, price setting, employed physician compensation, 340B compliance, price and cost transparency, revenue-cycle management and patient debt collection, workforce performance composition, evaluation and compensation, integration of AI in clinical and administrative decision-making, participation in gainsharing/alternative payment programs, clinical portfolio and others.

And across every sector, executive compensation and CEO pay, Board effectiveness, and long-term strategies that balance shareholder interests with broader concern for the greater good.

The bottom line:

The public is paying attention to business practices in healthcare. The death of Brian Thompson opened the floodgate for criticism of health insurers and the U.S. healthcare industry overall. It cannot be ignored. The public thinks industry folks are shrewd operators and they’re inclined to conclude they’re screwed as a result.

A major health insurance company is backing off of a controversial plan to limit coverage of anesthesia, according to public officials.

Why it matters:

Anthem Blue Cross Blue Shield recently decided to “no longer pay for anesthesia care if the surgery or procedure goes beyond an arbitrary time limit, regardless of how long the surgical procedure takes,” according to the American Society of Anesthesiologists, which opposed the decision.

The decision was based on surgery time metrics from federal health data, NPR reported.

The policy applied to plans in Connecticut, New York and Missouri.

The latest:

“After hearing from people across the state about this concerning policy, my office reached out to Anthem, and I’m pleased to share this policy will no longer be going into effect here in Connecticut,” Connecticut Comptroller Sean Scanlon said Thursday on X.

Shortly afterward, New York Gov. Kathy Hochul issued a statement saying, “We pushed Anthem to reverse course and today they will be announcing a full reversal of this misguided policy.”

What they’re saying:

The initial coverage decision was very unusual for a major health insurer, said Marianne Udow-Phillips, who teaches insurance classes at the University of Michigan School of Public Health and formerly made coverage decisions at Blue Cross Blue Shield of Michigan.

The big picture:

Anthem’s initial decision was controversial at the time — but outrage erupted this week after the murder of UnitedHealthcare CEO Brian Thompson in New York City cast a spotlight on divisive insurance decisions.

On social media, critics of health insurers drew a direct line from controversial coverage decisions to the death of Thompson.