How should health systems spend their “community benefit” dollars?

That question was at the heart of a discussion we participated in recently at a member board meeting. To maintain their nonprofit status, all health systems are required to devote a portion of their earnings to activities that benefit the communities they serve, based on an assessment of local health needs.

The question our member’s board was grappling with, led by the system’s executive team, was how to ensure their “investment” in the community is as leveraged as possible, and generates the greatest “bang for the buck” in terms of better community health.

As the importance of addressing the social determinants of health grows, many systems are trying to target their resources toward activities that that enhance their ability to improve health status, and to reduce the barriers to better health faced by many. That requires a level of rigor and commitment to “community ROI” that goes beyond simply pointing to charity care statistics and the number of uninsured served.

What most impressed us in the discussion was the application of the same investment mindset to community benefit that the system brings to capital allocation decisions—with due attention to implementation plans, outcomes metrics, and accountability.

As the system’s COO framed it, “We don’t just want to be a ‘piggy bank’ for charitable causes, we want to make sure our investment in the community is really making a difference” in local residents’ health. At the same time, the board recognized that its role extends beyond simply contributing dollars to acting as a convener and facilitator of other community organizations working together toward a common set of goals. A worthy discussion for the board, for sure, and a priority we’re seeing leading systems begin to embrace in a serious way.

Last week, Kaiser Family Foundation (KFF) released its Annual Employer Health Benefits Survey which included a surprise:

The average annual single premium and the average annual family premium each increased by 7% over the last year.

In 2022 as post-pandemic recovery was the focus for employers, the average single premium grew by 2% and the average family premium increased by 1%. Health costs and insurance premiums were not top of mind concerns to employers struggling to keep employees paid and door open. But 7% is an eye-opener.

The rest of the findings in the 2023 KFF Report are unremarkable: they reflect employer willingness to maintain benefits at/near pre-pandemic levels and slight inclination toward expanded benefits beyond mental health:

“The average annual premium for employer-sponsored health insurance in 2023 is $8,435 for single coverage and $23,968 for family coverage. Comparatively, there was an increase of 5.2% in workers’ wages and inflation of 5.8%2. The average single and family premiums increased faster this year than last year (2% vs. 7% and 1% vs. 7% respectively).

Over the last five years, the average premium for family coverage has increased by 22% compared to an 27% increase in workers’ wages and 21% inflation.

For single coverage, the average premium for covered workers is higher at small firms than at large firms ($8,722 vs. $8,321). The average premiums for family coverage are comparable for covered workers in small and large firms ($23,621 vs. $24,104) …

Most covered workers contribute to the cost of the premium for their coverage. On average, covered workers contribute 17% of the premium for single coverage and 29% of the premium for family coverage, similar to the percentages contributed in 2022…

90% of workers with single coverage have a general annual deductible that must be met before most services are paid for by the plan, similar to the percentage last year (88%).

The average deductible amount in 2023 for workers with single coverage and a general annual deductible is $1,735, similar to last year…

In 2023, among workers with single coverage, 47% of workers at small firms and 25% of workers at large firms have a general annual deductible of $2,000 or more. Over the last five years, the percentage of covered workers with a general annual deductible of $2,000 or more for single coverage has grown from 26% to 31%.

While nearly all large firms (firms with 200 or more workers) offer health benefits to at least some workers, small firms (3-199 workers) are significantly less likely to do so. In 2023, 53% of all firms offered some health benefits, similar to the percentage last year (51%).”

My take:

These findings show that employers are not prone to drastic changes in health benefits for their employees despite recognition it is expensive and unaffordable to small companies and for many of their own employees. But many large self-insured employers (except those in government, education and healthcare) are poised to make significant changes next year. They recognize themselves as the primary source of profits enjoyed by insurers, hospitals, physicians, drug companies and others.

They’re developing multi-year at risk direct contracts, value-based purchasing arrangements, primary care gatekeeping, narrow networks, restricted formularies, alternative care models and more to that leverage their clout. They’re going on offense.

The KFF Benefits Survey is a snapshot of where employer benefits are today, but it’s likely not the same next year. It appears employers are ready to engage the health industry head on.

PS Last week, the feud between Senate Health, Education, Labor and Pensions (HELP) Committee Chair Bernie Sanders and Not-for-Profit Health Systems heated up. On Oct. 10, he released a Majority Staff Report that said NFP hospitals do not deserve their tax exemptions as they spend “paltry amounts” on charity care. “Hospitals have gladly accepted the tax benefits that come with nonprofit status but have failed to provide the required community benefits. Non-profit hospitals spent only an estimated $16 billion on charity care in 2020, or about 57% of the value of their tax breaks in the same year.”

The same day, the American Hospital Association (AHA) released its analysis of hospital Schedule H filings concluding that tax-exempt hospitals provided $130 billion in community benefits in 2020 and called the HELP report “just plain wrong”.

In response to the AHA report, Sanders noted that AHA had not included CEO Compensation for NFPs in its analysis though featured prominently in his Majority Staff Report: “In 2021, the most recent year for which data is available for all of the 16 hospital chains, those companies’ CEOs averaged more than $8 million in compensation and collectively made over $140 million…

The disparities between the paltry amounts these hospitals are spending on charity care and their massive revenues and excessive executive compensation demonstrates that they are failing to live up to their end of the non-profit bargain.”

This tit for tat between the Committee Chairman and AHA is notable for 2 reasons: it draws attention to the Schedule H information goldmine about how not-for-profit hospitals operate since they’re now required to attach their S-10 Medicare cost report worksheets. Quantifying charity care in Exhibit 3B (for which there’s no expectation of payment) and the myriad of claimed community benefits including bad debt in Schedule 3C will likely intensify scrutiny of NFPs even more. Second, it draws attention to Executive Pay in hospitals: in this regard the Majority Staff Report commentary on CEO pay is misleading: by combining Column B (wages, bonuses) with Columns C (Deferred compensation) and D (non-taxable benefits), the total is significantly higher than one-year’s actual take-home pay for the CEOs. But it makes headlines!

If not-for-profit systems wish to lead transformational change in U.S. healthcare, not-for-profit system boards and their trade associations must be prepared to address the storm clouds gathering above. The skirmish between the Senate HELP Chair and AHA mirrors an increasingly skeptical public who, with Congress, believe the system is being gamed.

Studies show healthcare affordability is an issue to voters as medical debt soars (KFF) and public disaffection for the “medical system” (per Gallup, Pew) plummets. But does it really matter to the hospitals, insurers, physicians, drug and device manufacturers and army of advisors and trade groups that control the health system?

Each sector talks about affordability blaming inflation, growing demand, oppressive regulation and each other for higher costs and unwanted attention to the issue.

Each play their victim cards in well-orchestrated ad campaigns targeted to state and federal lawmakers whose votes they hope to buy.

Each considers aggregate health spending—projected to increase at 5.4%/year through 2031 vs. 4.6% GDP growth—a value relative to the health and wellbeing of the population. And each thinks its strategies to address affordability are adequate and the public’s concern understandable but ill-informed.

As the House reconvenes this week joining the Senate in negotiating a resolution to the potential federal budget default October 1, the question facing national and state lawmakers is simple: is the juice worth the squeeze?

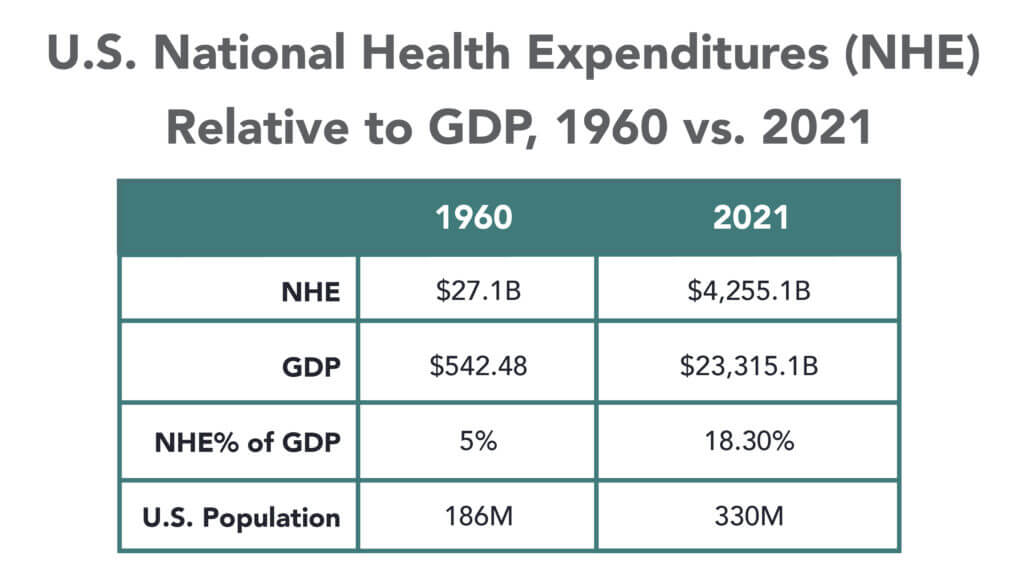

Is the US health system deserving of its significance as the fastest-growing component of the total US economy (18.3% of total GDP today projected to be 19.6% in 2031), its largest private sector employer and mainstay for private investors?

Does it deserve the legal concessions made to its incumbents vis a vis patent approvals, tax exemptions for hospitals and employers, authorized monopolies and oligopolies that enable its strongest to survive and weaker to disappear?

Does it merit its oversized role, given competing priorities emerging in our society—AI and technology, climate changes, income, public health erosion, education system failure, racial inequity, crime and global tension with China, Russia and others.

In the last 2 weeks, influential Republicans leaders (Burgess, Cassidy) announced plans to tackle health costs and the role AI will play in the future of the system. Last Tuesday, CMS announced its latest pilot program to tackle spending: the States Advancing All-Payer Health Equity Approaches and Development Model (AHEAD Model) is a total cost of care budgeting program to roll out in 8 states starting in 2026. The Presidential campaigns are voicing frustration with the system and the spotlight on its business practices intensifying.

So, is affordability to the federal government likely to get more attention?

Yes. Is affordability on state radars as legislatures juggle funding for Medicaid, public health and other programs?

Yes, but on a program by program, non-system basis.

Is affordability front and center in CMS value agenda including the new models like its AHEAD model announced last week? Not really.

CMS has focused more on pushing hospitals and physicians to participate than engaging consumers. Is affordability for those most threatened—low and middle income households with high deductible insurance, the uninsured and under-insured, those with an expensive medical condition—front of mind? Every minute of every day.

Per CMS, out-of-pocket spending increased 4.3% in 2022 (down from 10.4% in 2021) and “is expected to accelerate to 5.2%, in part related to faster health care price growth. During 2025–31, average out-of-pocket spending growth is projected to be 4.1% per year.” But these data are misleading. It’s dramatically higher for certain populations and even those with attractive employer-sponsored health benefits worry about unexpected household medical bills.

So, affordability is a tricky issue that’s front of mind to 40% of the population today and more tomorrow.

Legislation that limits surprise medical bills, requires drug, hospital and insurer price transparency, expands scope of practice opportunities for mid-level professionals, avails consumers of telehealth services, restricts aggressive patient debt collection policies and others has done little to assuage affordability issues for consumers.

Ditto CMS’ value agenda which is more about reducing Medicare spending through shared savings programs with hospitals and physicians than improving affordability for consumers. That’s why outsiders like Walmart, Best Buy and others see opportunity: they think patients (aka members, enrollees, end users) deserve affordability solutions more than lip service.

Affordability to consumers is the most formidable challenge facing the US healthcare industry–more than burnout, operating margins, reimbursement or alternative payment models. Today, it is not taken seriously by insiders. If it was, evidence would be readily available and compelling. But it’s not.

Last Monday, four U.S. Senators took aim at the tax exemption enjoyed by not-for-profit (NFP) hospitals in a letter to the IRS demanding detailed accounting for community benefits and increased agency oversight of NFP hospitals that fall short.

Last Tuesday, the Elevance Health Policy Institute released a study concluding that the consolidation of hospitals into multi-hospital systems (for-profit/not-for-profit) results in higher prices without commensurate improvement in patient care quality. “

Friday, Kaiser Health News Editor in Chief Elizabeth Rosenthal took aim at Ballad Health which operates in TN and VA “…which has generously contributed to performing arts and athletic centers as well as school bands. But…skimped on health care — closing intensive care units and reducing the number of nurses per ward — and demanded higher prices from insurers and patients.”

And also last week, the Pharmaceuticals’ Manufacturers Association released its annual study of hospital mark-ups for the top 20 prescription drugs used on hospitals asserting a direct connection between hospital mark-ups (which ranged from 234% to 724%) and increasing medical debt hitting households.

(Excerpts from these are included in the “Quotables” section that follows).

It was not a good week for hospitals, especially not-for-profit hospitals.

In reality, the storm cloud that has gathered over not-for-profit health hospitals in recent months has been buoyed in large measure by well-funded critiques by Arnold Ventures,Lown Institute, West Health, Patient Rights Advocate and others. Providence, Ascension, Bon Secours and now Ballad have been criticized for inadequate community benefits, excessive CEO compensation, aggressive patient debt collection policies and price gauging attributed to hospital consolidation.

This cloud has drawn attention from lawmakers: in NC, the State Treasurer Dale Folwell has called out the state’s 8 major NFP systems for inadequate community benefit and excess CEO compensation.

In Indiana, State Senator Travis Holdman is accusing the state’s NFP hospitals of “hoarding cash” and threatening that “if not-for-profit hospitals aren’t willing to use their tax-exempt status for the benefit of our communities, public policy on this matter can always be changed.” And now an influential quartet of U.S. Senators is pledging action to complement with anti-hospital consolidation efforts in the FTC leveraging its a team of 40 hospital deal investigators.

In response last week, the American Hospital Association called out health insurer consolidation as a major contributor to high prices and,

in a US News and World Report Op Ed August 8, challenged that “Health insurance should be a bridge to medical care, not a barrier.

Yet too many commercial health insurance policies often delay, disrupt and deny medically necessary care to patients,” noting that consumer medical debt is directly linked to insurer’ benefits that increase consumer exposure to out of pocket costs.

My take:

It’s clear that not-for-profit hospitals pose a unique target for detractors: they operate more than half of all U.S. hospitals and directly employ more than a third of U.S. physicians.

But ownership status (private not-for-profit, for-profit investor owned or government-owned) per se seems to matter less than the availability of facilities and services when they’re needed.

And the public’s opinion about the business of running hospitals is relatively uninformed beyond their anecdotal use experiences that shape their perceptions. Thus, claims by not-for-profit hospital officials that their finances are teetering on insolvency fall on deaf ears, especially in communities where cranes hover above their patient towers and their brands are ubiquitous.

Demand for hospital services is increasing and shifting, wage and supply costs (including prescription drugs) are soaring, and resources are limited for most.

The size, scale and CEO compensation for the biggest not-for-profit health systems pale in comparison to their counterparts in health insurance and prescription drug manufacturing or even the biggest investor-owned health system, HCA…but that’s not the point.

NFPs are being challenged to demonstrate they merit the tax-exempt treatment they enjoy unlike their investor-owned and public hospital competitors and that’s been a moving target.

Thus, the methodology for consistently defining and accounting for community benefits needs attention. That would be a good start but alone it will not solve the more fundamental issue: what’s the future for the U.S. health system, what role do players including hospitals and others need to play, and how should it be structured and funded?

The issues facing the U.S. health industry are complex. The role hospitals will play is also uncertain. If, as polls indicate, the majority of Americans prefer a private health system that features competition, transparency, affordability and equitable access, the remedy will require input from every major healthcare sector including employers, public health, private capital and regulators alongside others.

It will require less from DC policy wonks and sanctimonious talking heads and more from frontline efforts and privately-backed innovators in communities, companies and in not-for-profit health systems that take community benefit seriously.

No sector owns the franchise for certainty about the future of U.S. healthcare nor its moral high ground. That includes not-for-profit hospitals.

The darkening cloud that hovers over not-for-profit health systems needs attention, but not alone, despite efforts to suggest otherwise.

Clarifying the community-benefit standard is a start, but not enough.

Are NFP hospitals a problem? Some are, most aren’t but all are impacted by the darkening cloud.

As 41% of American adults face medical debt, residents of this southern Colorado city contend their local nonprofit hospitals aren’t providing enough charity care to justify the millions in tax breaks they receive.

The two hospitals in Pueblo, Parkview Medical Center and Centura St. Mary-Corwin, do not pay most federal or state taxes. In exchange for the tax break, they are required to spend money to improve the health of their communities, including providing free care to those who can’t afford their medical bills. Although the hospitals report tens of millions in annual community benefit spending, the vast majority of that is not spent on the types of things advocates and researchers contend actually create community benefits, such as charity care.

And this month, four U.S. senators called on the Treasury’s inspector general for tax administration and the Internal Revenue Service to evaluate nonprofit hospitals’ compliance with tax-exempt requirements and provide information on oversight efforts.

The average hospital in the U.S. spends 1.9% of its operating expenses on charity care, according to an analysis of 2021 data by Johns Hopkins University health policy professor Ge Bai. Last year, Parkview provided 0.75% of its operating expenses, about $4.2 million, in free care.

Centura Health, a chain of 20 tax-exempt hospitals, reports its community benefit spending to the federal government in aggregate and does not break out specific numbers for individual hospitals. But St. Mary-Corwin reported $2.3 million in charity care in fiscal year 2022, according to its state filing. The filing does not specify the hospital’s operating expenses.

The low levels of charity care have translated into more debt for low-income residents.

About 15% of people in Pueblo County have medical debt in collections, compared with 11% statewide and 13% nationwide, according to 2022 data from the Urban Institute. Those Puebloans have median medical debt of $975, about 40% higher than in Colorado and the U.S. as a whole. And all of those numbers are worse for people of color.

“How far into debt do people have to go to get any kind of relief?” said Theresa Trujillo, co-executive director at the Center for Health Progress’ Pueblo office. “Once you understand that there are tens of millions of dollars every single year that hospitals are extracting from our communities that are meant to be reinvested in our communities, you can’t go back from that without saying, ‘Oh my gosh, that is a thread we need to pull on.’”

Trujillo is organizing a group of fed-up residents to engage both hospitals on their community benefit spending. The group of at least a dozen residents believe the hospitals are ignoring the needs identified by the community — things like housing, addiction treatment, behavioral health care, and youth activities — and instead spending those dollars on things that mainly benefit the hospitals and their staffs.

For the fiscal year ending June 2022, with total revenue of $593 million, Parkview reported $100 million in community benefit spending. But most of that — more than $77 million — represented the difference between the hospital’s cost of providing care and what Medicaid paid for it.

IRS guidelines allow hospitals to claim Medicaid shortfall as a community benefit, but many academics and health policy experts argue such balance sheet shifts aren’t the same as providing charity care to patients.

Parkview also reported $4.7 million for educating its medical staff and $143,000 in incentives to recruit health professionals as community benefit. The hospital spent only $44,000 on community health improvement projects, which appear to have consisted mainly of launching a new mobile app to streamline appointments and referrals.

Meanwhile, the hospital recently spent $58 million on a new orthopedic facility and $43 million on a new cancer center. Parkview also wrote off $39 million in bad debt in fiscal 2022, although that is different from charity care. The bad debt is money the hospitals tried to collect from patients and ultimately decided they’d never get. But by that time, those patients would likely have been sent to collections and potentially had their credit damaged. And outstanding debt often keeps patients from seeking other needed care.

There is a disconnect between what the community said its biggest health needs were and where Parkview directed its spending. The hospital’s community needs assessment pegged access to care as the top concern, and the hospital said it launched the phone app in response.

The second-largest perceived health need was addressing alcohol and drug use. Yet, the only initiative Parkview cited in response was posting preventive health videos online, including some on alcohol and drug use. Meanwhile, the hospital shut down its inpatient psychiatric unit.

Parkview declined to answer questions about its charity care spending, but hospital spokesperson Todd Seip emailed a statement saying the hospital system “has been committed to providing extensive charity care to our community.”

Seip noted that 80% of Parkview’s patients are covered by Medicare or Medicaid, which pay lower rates than commercial insurance. The hospital posted a net loss of $6.7 million in the 2022 fiscal year, although its charity care wasn’t appreciably higher in previous years in which it posted a net gain.

Centura St. Mary-Corwin reported $16 million in Medicaid shortfall and $2 million in medical staff education in 2022, according to its state filing. The hospital spent about $38,000 for its community health improvement projects, primarily on emergency medical services outreach programs in rural areas. The hospital provided another $96,000 in services, mainly to promote covid-19 vaccination.

Centura also declined to answer questions about its charity care spending. Hospital spokesperson Lindsay Radford emailed a statement saying St. Mary-Corwin was aligning its community health needs assessment process with the Pueblo Department of Public Health and Environment “to develop shared implementation strategies for our community benefit funds, ensuring the resources are targeting the highest needs.”

Trujillo questioned how the hospital has conducted its community health assessments, relying on a social media poll to identify needs. After community members identified 12 concerns, she said, hospital leaders chose their priorities from the list.

“They talk about a community garden like they’re feeding the whole south side of the community,” Trujillo said. The hospital established a community garden in 2021, with 20 beds that could be adopted by residents to grow vegetables. Trujillo did praise the hospital for converting part of its building into dorms for a community college nursing program.

Trujillo’s group has spent much of the summer researching hospital charity spending and showing up at public meetings to have their views heard. They are working to gain seats on hospital and other state boards that influence how community benefit dollars are spent, and are urging hospitals to reconfigure their boards to better represent the demographics of their communities.

“We’ve made folks now aware that we want to be a part of those processes,” Trujillo said. “We’re willing to help them reach deeper into the community.”

Tax-exempt hospitals have been under increased state scrutiny for their charitable spending, especially after the Affordable Care Act and Medicaid expansion drove down the uninsured rate. That in turn cut the amount of care hospitals had to provide without being paid, potentially freeing up money to help more people without insurance or with high-deductible plans.

In Colorado, hospitals’ charity care spending and bad debt write-offs dropped from an average of $680 million a year in the five years prior to the ACA being fully implemented in 2014 to an average of $337 million in the years after, according to the Colorado Healthcare Affordability and Sustainability Enterprise Board, a state advisory group.

In states like Colorado, which used federal funding to expand the number of people covered by Medicaid, hospitals shifted more of their community benefit spending to cover Medicaid reimbursement shortfalls.

A January report from Colorado’s Department of Health Care Policy & Financing concluded that payments from public and private health plans help the state’s hospitals make more than enough money to offset lower Medicaid rates and still turn a profit while providing more true charity care.

Colorado has enacted two bills in the past five years to increase the transparency of hospitals’ charitable efforts with new reporting requirements.

“I think overall, we’re pleased with the amount of money that hospitals are reporting they spent,” said Kim Bimestefer, the executive director of the Department of Health Care Policy & Financing. “Is that money being expended in meaningful ways, ways that improve health and well-being of the community? Our reports right now can’t determine that.”

Five recent Supreme Court rulings have reset the context for U.S. jurisprudence for years to come and open a can of worms for healthcare operators.

Last year’s SCOTUS decision ruling in Dobbs v. Jackson Women’s Health (June 24, 2022) set the tone: in its 6-3 decision, the high court determined that that access to abortion is a state issue, not federal thus nullifying the 50-year-old legal precedent in Roe v. Wade and reversing 2 lower court rulings.

On June 1, 2023, in the United States v. Supervalu, petitioners sued SuperValu and Safeway under the False Claims Act (FCA) alleging they defrauded the Medicare and Medicaid by knowingly filing false claims. Essentially, the plaintiffs sought financial remedy because the retailers’ prices were not explicitly and specifically “usual and customary” prices. In its unanimous ruling, SCOTUS agreed that “the phrase ‘usual and customary’ is open to interpretation, but reasoned that “such facial ambiguity alone is not sufficient to preclude a finding that respondents knew their claims were false.”

On June 29, 2023, in Students for Fair Admissions, Inc. v. President and Fellows of Harvard College, the court ruled 6-3 that affirmative action policies at Harvard and the University of NC that consider an applicant’s race in college admissions are unconstitutional.

On June 30, 2023, in 303 Creative LLC v. Elenis (June 30, 2023) By a vote of 6-3, SCOTUS ruled that the First Amendment right of free speech prohibits Colorado from forcing a website designer to create expressive designs speaking messages with which the designer disagrees.

On June 30, 2023, in Department of Education v. Brown: By a unanimous vote, SCOTUS ruled that the 2 plaintiffs lacked standing to “Article III standing to assert a procedural challenge to the student-loan debt-forgiveness plan adopted by the Secretary of Education pursuant to Higher Education Relief Opportunities for Students Act of 2003 (HEROES Act).” In effect, the court vacated and remanded the judgment of the United States Court of Appeals for the 5th Circuit because it felt Myra Brown and Alexander Taylor (plaintiffs) did not prove that any injury suffered from not having their loans forgiven. Therefore, the court had no jurisdiction to address their procedural claim.

Each of these is specific to a circumstance but collectively they expose industries like healthcare to greater compliance risk, potential court challenges and operational complexity. Here’s an example:

The 58-year-old Kennedy-era legal precedent of affirmative action to redress racial inequity was the focus in Students for Fair Admissions, Inc. v. President and Fellows of Harvard College. SCOTUS essentially sided with plaintiffs who argued affirmative action violates the 14th Amendment’s Equal Protection guarantee. In healthcare, research shows access to the healthcare system is disproportionately inaccessible to persons of color, especially if they’re poor. They improve when individuals are treated by clinicians of the same race but only about 5% of doctors in America are Black, compared to 12% of the general population and only 6% of doctors in the U.S. are Hispanic while the group accounts for nearly almost 20% of the general population.

Notwithstanding the uncanny similarities between higher education and healthcare (both have raised prices above GDP and overall inflation rates for 2 decades, both jealously protect their reputations against outside transparency and unflattering report cards, both feature competition between public and private institutions and both face questions about the value of their efforts), the issue of diversity is central in both. Affirmative action is a means to that end, but at least for now and in higher education, it’s not constitutional.

Might workforce diversity and clinician training efforts be stymied by the prospect of court challenges? Might “affirmative action” in healthcare be replaced by “holistic review” to enable consideration of an applicant’s life or quality of character as some conservative jurists have suggested?

My take:

Affirmative action per the example above is only one of many constructs widely accepted in healthcare today where court challenges may alter the future. Individual rights and free speech including online medical advice, the role of state governments, fraud and abuse and other domains are equally exposed.

It’s clear this court is not threatened by legal precedent nor cautious about public opinion on touchy issues. Thus, immediate imperatives for healthcare organizations are these:

Revisit legal precedents on which the ways we operate are based: Roles and responsibilities in US healthcare are sacrosanct and protected by legal precedent: Physicians diagnose and treat; others don’t. Insurers pay claims but don’t practice medicine. Not for profit hospitals serve community needs in exchange for tax-exemption. Public health programs that serve the poor are funded by local and state governments. Employer sponsored benefits underwrite the system’s profitability and fund its hospital Part A obligations and so on. Might a conservative court revisit these in the context of the constitution’s “general welfare” purpose and redirect its focus, roles and structure?

Revisit terms and phrases where consensus is presumed but specific definition is lacking: Just as SCOTUS recognized ambiguity in applying terms like “usual and customary” in its Supervalu-Safeway ruling, it is likely to challenge other widely used phrases used in healthcare that often lack specific referents i.e., quality, safety, efficacy, effectiveness, community benefit, charity care, evidence-based care, cost-effectiveness, not-for-profit, competition, value” and many others. Might SCOTUS force the industry to more specifically define its most widely used phrases in order to justify its claims?

For everyone in healthcare, these rulings open a can of worms. Compliance risk assessments, scenario plan updates required!

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

Correction: An earlier version incorrectly referenced a Texas deal between Houston Methodist and Baylor Scott and White. News about deals is sensitive and unnecessarily disruptive to reputable organizations like these. I sourced this news from a reputable deal advisor: it was inaccurate. My apology!

Congressional Republicans and the White House spared Main Street USA the pain of defaulting on the national debt last week. No surprise.

Also not surprising: another not-for-profit-mega deal was announced:

St. Louis, MO-based BJC HealthCare and Kansas City, MO-based Saint Luke’s Health System announced their plan to form a $9.5B revenue, 28-hospital system with facilities in Missouri, Kansas, and Illinois.

This follows recent announcements by four other NFP systems seeking the benefits of larger scale:

Gundersen Health System & Bellin Health (Nov 2022): 11 hospitals, combined ’22 revenue of $2.425B

Froedtert Health & ThedaCare (Apr 2023 LOI): 18 hospitals, combined ’22 revenues of $4.6B

And all these moves are happening in an increasingly dicey environment for large, not-for-profit hospital system operators:

Increased negative media attention to not-for-profit business practices that, to critics, appear inconsistent with a “NFP” organization’s mission and an inadequate trade for tax exemptions each receives.

Decreased demand for inpatient services—the core business for most NFP hospital operations. Though respected sources (Strata, Kaufman Hall, Deloitte, IBIS et al) disagree somewhat on the magnitude and pace of the decline, all forecast decreased demand for traditional hospital inpatient services even after accounting for an increasingly aging population, a declining birthrate, higher acuity in certain inpatient populations (i.e. behavioral health, ortho-neuro et al) and hospital-at-home services.

Increased hostility between national insurers and hospitals over price transparency and operating costs.

Increased employer, regulator and consumer concern about the inadequacy of hospital responsiveness to affordability in healthcare.

And heightened antitrust scrutiny by the FTC which has targeted hospital consolidation as a root cause of higher health costs and fewer choices for consumers. This view is shared by the majorities of both parties in the House of Representatives.

In response, Boards and management in these organizations assert…

Health Insurers—especially investor-owned national plans—enjoy unfettered access to capital to fund opportunistic encroachment into the delivery of care vis a vis employment of physicians, expansion of outpatient services and more.

Private equity funds enjoy unfettered opportunities to invest for short-term profits for their limited partners while planning exits from local communities in 6 years or less.

The payment system for hospitals is fundamentally flawed: it allows for underpayments by Medicaid and Medicare to be offset by secret deals between health insurers and hospitals. It perpetuates firewalls between social services and care delivery systems, physical and behavioral health and others despite evidence of value otherwise. It requires hospitals to be the social safety net in every community regardless of local, state or federal funding to offset these costs.

These reactions are understandable. But self-reflection is also necessary. To those outside the hospital world, lack of hospital price transparency is an excuse. Every hospital bill is a surprise medical bill. Supporting the community safety net is an insignificant but manageable obligation for those with tax exemption status. Advocacy efforts to protect against 340B cuts and site-neutral payment policies are about grabbing/keeping extra revenue for the hospital. What is means to be a “not-for-profit” anything in healthcare is misleading since moneyball is what all seem to play. And short of government-run hospitals, many think price controls might be the answer.

My take:

The headwinds facing large not-for-profit hospitals systems are strong. They cannot be countered by contrarian messaging alone.

What’s next for most is a new wave of operating cost reductions even as pre-pandemic volumes are restored because the future is not a repeat of the past. Being bigger without operating smarter and differently is a recipe for failure.

What’s necessary is a reset for the entire US health system in which not-for-profit systems play a vital role. That discussion should be led by leaders of the largest NFP systems with the full endorsements of their boards and support of large employers, physicians and public health leaders in their communities.

Everything must be on the table: funding, community benefits, tax exemption, executive compensation, governance, administrative costs, affordability, social services, coverage et al. And mechanisms for inaction and delays disallowed.

It’s a unique opportunity for not-for-profit hospitals. It can’t wait.

We caught up recently with a healthcare leader who had spent time in Atlanta in a previous role, and the conversation turned to last year’s closure of Atlanta Medical Center.

One major impact: the closure immediately left the Atlanta metro region, home to over 6M people, with only one Level 1 trauma center (a second Level 1 center opened an hour north of the city in February). “It’s devastating for the community to lose those services,” he shared, “but I also get why the health system made that choice, given how hard the economy has hit hospitals.” When all health systems are feeling the worst margin pressures in more than a decade, most would be reticent to step in and launch a new trauma program, which despite bringing prestige, is often a money-loser.

The conversation got us thinking about whether healthcare needs a new approach to securing essential services needed by the community which aren’t well supported by the payment system.

Our current model largely relies on nonprofit systems to meet the community need as a tenet of that status. But as one CMO shared, “If there’s more than one system in the market, we toss the responsibility back and forth like a hot potato.”

His solution: there needs to be top-down redesign of urgently needed critical services like trauma and behavioral health, as well as highly specialized services like transplant and pediatric subspecialty care, which he considered oversupplied in his market, with multiple subscale programs.

His hope was that health systems could cross competitive lines and collaborate to think about a rational approach to “regional healthcare master planning”, along with a new funding model.

It’s a tall order, he continued, but if health systems can’t find a solution on their own, they leave themselves open to government intervention that might mandate a solution—or further questions of the value communities are receiving from supporting nonprofit status.

Last week, 35,000 gathered in Chicago to hear about the future of health information technologies at the HIMSS Global Health Conference & Exhibition where generative AI, smart devices and cybersecurity were prominent themes.

Yesterday, the Annual Meeting of the American Hospital Association convened. Its line-up includes some big names in federal health policy and politics along with some surprising notaries like Chris Wray, Head of the FBI and others. In tandem, a new TV ad campaign launched yesterday by the Coalition to Protect America’s Health Care, of which the AHA is a founding member to pressure Congress to avoid budget cuts to hospitals to “protect care for seniors”.

These events bracket what has been a whip-lash week for the U.S. healthcare industry…

Throughout the week, the fate of medication-abortion mifepristone was in suspense ending with a Supreme Court emergency-stay decision late Friday night that defers prohibitions against its use until court challenges are resolved.

At HIMSS last Monday, EHR juggernaut EPIC and Microsoft announced they are expanding their partnership and integrating Microsoft’s Azure Open AI Service into Epic’s EHR software. Epic’s EHR system will be able to run generative AI solutions through Microsoft’s Open AI Azure Service. Microsoft uses Open Ai’s language model GPT-4 capabilities in its Azure cloud solution.

Thursday HHS posted data online showing who owns 6,000 hospices and 11,000 home health agencies that are reimbursed by Medicare.

Bell-weather companies HCA (investor-owned hospitals), Johnson and Johnson (prescription drugs) and Elevance (health insurers) reported strong 1Q profits and raised their guidance to shareholders for year-end performance.

And Monday, House Speaker Kevin McCarthy told an audience at the New York Stock Exchange that Republicans will agree to increase the $31.4 trillion debt-limit if it is accompanied by spending cuts i.e. a requirement that all “able bodied Americans without children” work to receive benefits like Medicaid, re-setting federal spending to 2022 levels and others.

Each of these is newsworthy. The partisan brinksmanship about the debt ceiling is perhaps the most immediately consequential for healthcare because it will draw attention to 2 themes:

Healthcare is profitable for some. Big companies and others with access to capital are advantaged in the current environment. Healthcare is fast-becoming a land of giants: it’s almost there in health insurance (the Big 7 in the US), prescription drugs (36 major players globally), retail drugstores (the Big 5), PBMs (the Big 4) and even the accountancies who monitor their results (the Big 4).

By contrast, the hospital and long-term care sectors sectors remain fragmented though investor-owned systems now own a quarter of operations in both.

Physicians and other clinical service provider sectors (physical therapy, dentistry, et al) are transitioning toward two options—corporatization via private equity roll-ups or hospital employment.

The 1Q earnings reported by HCA, J&J and Elevance last week give credence to beliefs among budget hawks that healthcare is a business that can be lucrative for some and expensive for all. That view aka “Survival of the Fittest” will figure prominently into the debt ceiling debate.

The regulatory environment in which U.S. healthcare operates is hostile because the public thinks it needs more scrutiny. 82% of U.S. adults think the health system puts its profits above all else. The public’s antipathy toward the system feeds regulatory activism toward healthcare.

At a federal level, the debt ceiling debate in Congress will be intense and healthcare cuts a likely by-product of negotiations between hawks and doves.

In addition, government accountants and lawmakers will increase penalties for fraud and compliance suspecting healthcare’s ripe for ill-gotten gain and/or excess. Federal advocacy in each sector will be strained by increasingly significant structural fault-lines between non-profit and for profits, and public health programs that operate on shoestrings below the radar. Two committees of the House (Ways and Means and Energy and Commerce) and two Senate Committee’s) will hold public hearings on issues including not-for-profit hospitals consolidation, price transparency and others with unprecedented Bipartisan support for changes likely “uncomfortable” for industry insiders.

At a state level, matters are even more complicated: states are the gatekeeper for the healthcare system’s future. States will increasingly control the supply and performance criteria for providers and payers. Ballot referenda will address issues reflective of the state’s cultural and political values—abortion rights, public health funding, gun control, provider and prescription drug price controls, and many more.

My take

The upcoming debt ceiling debate comes at a pivotal time for healthcare because it does not enjoy the good will it has in decades past. The pandemic, dysfunctional political system and the struggling economy have taken a toll on public confidence. Long-term planning for the system’s future is subordinated to the near term imperative to control costs in the context of the debt ceiling debate.

The federal debt will hit its ceiling in June. Speaker McCarthy’s ‘Limit, Save, Grow Act’ would return the government’s discretionary spending to fiscal year 2022 levels, cap annual spending growth at 1% for a decade and raise the debt ceiling until March 31, 2024, or until the national debt increases by $1.5 trillion, whichever comes first.

That means healthcare program cuts. That’s why this debt ceiling expansion is more than perfunctory: it’s an important barometer about the system’s future in the U.S. and how it MIGHT evolve:

In 8-10 years, it MIGHT be dominated by fewer players with heightened regulatory constraints.

It MIGHT be funded by higher taxes in exchange for better performance.

It MIGHT be restructured with acute services as a public utility. It might be a B2C industry in which employers play a lesser role and a national platform powered by generative AI and GPT4 enables self-care and interoperability.

It MIGHT be an industry wherein public health and social services programs are seamlessly integrated with non-profit health systems.

It MIGHT be built on the convergence of financing and delivery into regional systems of health.

It MIGHT bifurcate into two systems—one public for the majority and one private for some who can afford it.

It MIGHT replace the trade-off between community benefits and tax exemption.

It MIGHT re-define distinctions between non-profit hospitals and plans with their predicate investor-owned operators, and so on.

No one knows for sure, but everyone accepts the future will NOT be a repeat of the past. And the resolution of the debt ceiling in the next 60 days will set the stage for healthcare for the next decade.