Wall Street has fallen out of love with big insurers that depend heavily on the federal government’s overpayments to the private Medicare replacement plans they market, deceptively, under the name, “Medicare Advantage.”

I’ll explain below. But first, thank you if you reached out to your members of Congress and the Biden administration last week as I suggested to demand an end to the ongoing looting by those companies of the Medicare Trust Fund.

As I wrote on March 26, the Center for Medicare and Medicaid Services was scheduled to announce this week how much more taxpayer dollars it would send to Medicare Advantage companies next year. On January 31, CMS said it planned to increase the amount slightly to account for the increased cost of health care, based on how much more the government likely would spend to cover people enrolled in the traditional Medicare program. It uses traditional Medicare as a benchmark.

Big insurers like UnitedHealthcare, Humana and Aetna, owned by CVS, howled when CMS released its preliminary 2025 rate notice that day. They claimed they wouldn’t be getting enough of taxpayers’ dollars. So they launched a high-pressure campaign to get CMS to give them more money. They demanded extra billions because, they said, their Medicare Advantage enrollees had used more prescription drugs and went to the doctor more often in 2023 and January of this year than the companies had expected.

CMS announced after the market closed Monday that it was sticking to its plan to increase payments to Medicare Advantage plans by 3.7% – more than $16 billion –from 2024 to 2025. That would mean that it would pay companies that operate MA plans between $500 and $600 billion next year, considerably less than insurers wanted.

Shocked investors began running for the exits right away. When the New York Stock Exchange closed at 4 p.m. ET on Tuesday, more than 52 million shares of the companies’ stock had been traded–many millions more than average–driving the share prices of all of them way down. And the carnage has continued throughout this week.

By the end of trading yesterday, UnitedHealth, Humana and CVS/Aetna had lost nearly $95 billion in market capitalization. To put that in perspective, that’s more than the entire market cap of CVS, which fell to $93 billion yesterday.

All seven of the big for-profit companies with Medicare Advantage enrollment had a bad week, although Cigna, where I used to work and which announced recently it is getting out of the Medicare Advantage business next year, suffered the least. Its shares were down a little more than 1% as of yesterday afternoon.

Humana, the second largest MA company, which last year said it was getting out of the commercial insurance business to focus more fully on Medicare Advantage, by contrast, was the biggest loser of the bunch–and one of the biggest losers on the NYSE. Its shares fell more than 13% on Tuesday. As of yesterday, they were still down nearly 12%.

Noting that Humana’s stock has fallen 40% this year, he wrote:

Last fall, the insurer Humana was on top of the world. The stock was trading above $520 per share, as the company’s major bet on Medicare Advantage—the privately-run, publicly-funded insurance program for U.S. seniors—seemed to be paying off.

Long a darling of Wall Street’s analyst class, the stock had returned nearly 290% since the start of 2015, handily outperforming the S&P 500 over the same period.

Over the past five months, that position has crumbled. Humana shares were down to $308 Tuesday morning, as the outlook for Medicare Advantage and, by extension, for Humana’s business, has grown dimmer and dimmer.

Humana shares dived 12.3% early Tuesday, after the latest blow to the future prospects for the profitability of the Medicare Advantage business. Late Monday, the Centers for Medicare and Medicaid Services announced Medicare Advantage payment rates for 2025 that fell short of investor expectations.

The other companies also had a disastrous week. Shares of UnitedHealth, the biggest of the group in terms of Medicare Advantage enrollment (and overall revenues and profits), had fallen by 7% by the end of the day yesterday. CVS/Aetna’s shares were down 7.1%; Elevance’s were down 3.37%; Molina’s were down 7.15%; and Centene’s were down 7.33%.

When I was at Cigna, one of my responsibilities was to handle media questions when the company announced quarterly earnings, mergers and acquisitions, and whenever there was a major event like the CMS rate notice. The worst days of my 20-year career in the industry were when some kind of news triggered a stock selloff. I had to try to put the best spin possible on the situation. But my job was relatively easy compared to what the CEO, CFO and the company’s investor relations team had to do.

You can be certain they have been on the phone and in Zooms all week with Wall Street financial analysts, big institutional investors and even the company’s big employer customers in attempts to persuade them that the sky has not fallen.

You can also be certain that the companies will now shift their focus to the political arena. To keep this from happening again, they will begin pouring enormous sums of your premium dollars into campaigns to help elect industry-friendly candidates for Congress and the presidency this November. We provided a glimpse of where they’re already sending those donations in a story last November. We will continue to monitor this in the months ahead.

Two newly published investigative reports, by the intrepid reporters at STAT News and The American Prospect, pull the curtains back a little more on the astonishing number of recent acquisitions UnitedHealth has made as it moves deeper and deeper into health care delivery, enabling it to grab ever-increasing chunks of our premium and tax dollars to reward its shareholders.

That’s a strategic move that allows the company to steer more seniors to facilities it owns, boosting revenues it gets from the government and padding its bottom line.

The bigger a company gets, the less it has to disclose about the acquisitions it makes in any easily obtainable way. That’s because publicly-traded companies are only required to immediately inform investors of individual deals that are “material to earnings.”

A material amount, as Investopedia explains, “can signify any sum or figure worth mentioning, as in account balances, financial statements, shareholder reports, or conference calls. If something is not a material amount, it is considered too insignificant or trivial to mention.”

UnitedHealth’s long string of acquisitions in recent years has catapulted the company to the #5 spot on the Fortune 500 list of American companies, based on revenue. Only Walmart, Exxon Mobile, Amazon and Apple are bigger.

That rapid growth means that fewer and fewer of UnitedHealth’s acquisitions reach the threshold of requiring prominent disclosure to shareholders.

It was only through a close review of UnitedHealth’s latest annual report to investors and other financial documents that STAT was able to see what the company hides from most of us. As Herman noted:

UnitedHealth Group is so big that it doesn’t have to publicly announce a vast majority of its acquisitions. But a STAT analysis of company financial documents shows the health care conglomerate quietly acquired dozens of outpatient facilities in 2023, with a particular focus on surgery centers.

And it’s not adding random surgery centers, either. There seems to be an explicit strategy: Many of UnitedHealth’s new centers sit in geographic areas where the company is the biggest Medicare Advantage player, based on the latest insurance market share data. That overlap reinforces how UnitedHealth is looking to funnel more of its insurance members toward providers that it owns, with the overarching goal of capturing more profit.

As an example, STAT said it stumbled upon an entry–”buried within UnitedHealth’s annual report”–that revealed the company’s previously undisclosed December acquisition of National Cardiovascular Partners, which operates 21 cardiac cath and vascular labs. Not coincidentally, NCP’s facilities are “in places like Phoenix and large metro areas in Texas where UnitedHealth has the biggest MA market share.”

Tkacik wrote that last Thursday, UnitedHealthcare applied for an emergency exemption that would fast-track its takeover of a medical practice in Corvallis, Oregon, which is facing the prospect of closing its doors because of the financial crunch caused by the hack. As Tkacik explained, the hack interrupted the flow of information from Change Healthcare’s claims processing systems that enables physicians, hospitals, and other health care providers to get paid.

Perversely, UnitedHealth is telling Oregon regulators that the best solution is to allow the company’s proposed acquisition of the medical practice to go forward.

Tkacik reported that:

Although the specific reason for the exemption request is redacted from the publicly posted version of the application, a clinic insider says the “emergency” is the same one that has plunged thousands of other health providers across the nation into a terrifying cash crunch…

The situation underscores the perverse state of affairs in which UnitedHealth, which comprises some 2,642 separate companies that collectively raked in $371.6 billion last year, has arguably profited from the desperation that the hacking of its Change computer systems in late February has inflicted upon the health care system.

An estimated half of all health care transactions are processed or somehow otherwise touched by Change, a rollup of dozens of health care technology firms that provide 137 software applications that have been affected by the outage.

Tkacid added that “Every dollar in revenue that has disappeared from hospitals, medical practices, and pharmacies in the aftermath of the outage corresponds to an extra dollar sitting in the coffers of the nation’s health insurers, so UnitedHealth, which pays out roughly $662 million in medical claims each day, is presumably sitting on a mountain of unexpected cash.”

The Department of Justice (DOJ) has been investigating UHG for anticompetitive behavior since last October, as first revealed by the Examiner News earlier this week and subsequently confirmed by the Wall Street Journal.

The DOJ is reportedly interested in Optum’s acquisitions of physician groups and how their relationships with UHG’s health plans affects competition.

The probe appears to be wide-ranging, but there are no indications of if or when the DOJ plans to file charges. UHG is no stranger to antitrust attention: the DOJ failed to block its purchase of Change Healthcare in 2022, and its planned acquisition of home healthcare company Amedisys is still subject to a federal probe.

The Gist: The Biden administration has made antitrust scrutiny a key plank of its policy platform, having recently launched high-profile investigations into several large companies including Apple, Amazon, and Google.

Although these probes span major sectors of the US economy, healthcare consolidation has been a particular focus for the White House.

As the nation’s both largest employer of physicians and largest health insurance company,UHG is an unsurprising target within the healthcare industry. Recently finalized federal merger guidelines have changed how the DOJ and Federal Trade Commission (FTC) gather M&A information, but not the laws or legal precedent upon which cases are ruled, so it remains to be seen if regulators’ new approach will translate into stronger enforcement.

Last week, Congress avoided a partial federal shutdown by passing a stop-gap spending bill and now faces March 8 and March 22 deadlines for authorizations including key healthcare programs.

This week, lawmakers’ political antenna will be directed at Super Tuesday GOP Presidential Primary results which prognosticators predict sets the stage for the Biden-Trump re-match in November. And President Biden will deliver his 3rd State of the Union Address Thursday in which he is certain to tout the economy’s post-pandemic strength and recovery.

The common denominator of these activities in Congress is their short-term focus: a longer-term view about the direction of the country, its priorities and its funding is not on its radar anytime soon.

The healthcare system, which is nation’s biggest employer and 17.3% of its GDP, suffers from neglect as a result of chronic near-sightedness by its elected officials. A retrospective about its funding should prompt Congress to prepare otherwise.

U.S. Healthcare Spending 2000-2022

Year-over-year changes in U.S. healthcare spending reflect shifting demand for services and their underlying costs, changes in the healthiness of the population and the regulatory framework in which the U.S. health system operates to receive payments. Fluctuations are apparent year-to-year, but a multiyear retrospective on health spending is necessary to a longer-term view of its future.

The period from 2000 to 2022 (the last year for which U.S. spending data is available) spans two economic downturns (2008–2010 and 2020–2021); four presidencies; shifts in the composition of Congress, the Supreme Court, state legislatures and governors’ offices; and the passage of two major healthcare laws (the Medicare Modernization Act of 2003 and the Affordable Care Act of 2010).

During this span of time, there were notable changes in healthcare spending:

In 2000, national health expenditures were $1.4 trillion (13.3% of gross domestic product); in 2022, they were $4.5 trillion (17.3% of the GDP)—a 4.1% increase overall, a 321% increase in nominal spending and a 30% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 333 million, per capita healthcare spending increased 178% from $4,845 to $13,493 due primarily to inflation-impacted higher unit costs for , facilities, technologies and specialty provider costs and increased utilization by consumers due to escalating chronic diseases.

There were notable changes where dollars were spent: Hospitals remained relatively unchanged (from $415 billion/30.4% of total spending to $1.355 trillion/31.4%), physician services shrank (from $288.2 billion/21.1% to $884.8/19.6%) and prescription drugs were unchanged (from $122.3 billion/8.95% to $405.9 billion/9.0%).

And significant changes in funding Out-of-pocket shrank from 14.2% ($193.6 billion in 2020) to (10.5% ($471 billion) in 2020, private insurance shrank from $441 billion/32.3% to $1.289 trillion/29%, Medicare spending grew from $224.8 billion/16.5% to $944.3billion/21%; Medicaid and the Children’s Health Insurance Program spending grew from $203.4 billion/14.9% to $7805.7billion/18%; and Department of Veterans Affairs healthcare spending grew from $19.1 billion/1.4% to $98 billion/2.2%.

Looking ahead (2022-2031), CMS forecasts average National Health Expenditures (NHE) will grow at 5.4% per year outpacing average GDP growth (4.6%) and resulting in an increase in the health spending share of Gross Domestic Product (GDP) from 17.3% in 2021 to 19.6% in 2031.

The agency’s actuaries assume

“The insured share of the population is projected to reach a historic high of 92.3% in 2022… Medicaid enrollment will decline from its 2022 peak of 90.4M to 81.1M by 2025 as states disenroll beneficiaries no longer eligible for coverage. By 2031, the insured share of the population is projected to be 90.5 percent. The Inflation Reduction Act (IRA) is projected to result in lower out-of-pocket spending on prescription drugs for 2024 and beyond as Medicare beneficiaries incur savings associated with several provisions from the legislation including the $2,000 annual out-of-pocket spending cap and lower gross prices resulting from negotiations with manufacturers.”

My take:

The reality is this: no one knows for sure what the U.S. health economy will be in 2025 much less 2035 and beyond. There are too many moving parts, too much invested capital seeking near-term profits, too many compensation packages tied to near-term profits, too many unknowns like the impact of artificial intelligence and court decisions about consolidation and too much political risk for state and federal politicians to change anything.

One trend stands out in the data from 2000-2022: The healthcare economy is increasingly dependent on indirect funding by taxpayers and less dependent on direct payments by users.

In the last 22 years, local, state and federal government programs like Medicare, Medicaid and others have become the major sources of funding to the system while direct payments by consumers and employers, vis-à-vis premium out-of-pocket costs, increased nominally but not at the same rate as government programs. And total spending has increased more than the overall economy (GDP), household wages and costs of living almost every year.

Thus, given the trends, five questions must be addressed in the context of the system’s long-term solvency and effectiveness looking to 2031 and beyond:

Should its total spending and public funding be capped?

Should the allocation of funds be better adapted to innovations in technology and clinical evidence?

Should the financing and delivery of health services be integrated to enhance the effectiveness and efficiency of the system?

Should its structure be a dual public-private system akin to public-private designations in education?

Should consumers play a more direct role in its oversight and funding?

Answers will not be forthcoming in Campaign 2024 despite the growing significance of healthcare in the minds of voters. But they require attention now despite political neglect.

PS: The month of February might be remembered as the month two stalwarts in the industry faced troubles:

United HealthGroup, the biggest health insurer, saw fallout from a cyberattack against its recently acquired (2/22) insurance transaction processor by ALPHV/Blackcat, creating havoc for the 6000 hospitals, 1 million physicians, and 39,000 pharmacies seeking payments and/or authorizations. Then, news circulated about the DOJ’s investigation about its anti-competitive behavior with respect to the 90,000 physicians it employs. Its stock price ended the week at 489.53, down from 507.14 February 1.

And HCA, the biggest hospital operator, faced continued fallout from lawsuits for its handling of Mission Health (Asheville) where last Tuesday, a North Carolina federal court refused to dismiss a lawsuit accusing it of scheming to restrict competition and artificially drive-up costs for health plans. closed at 311.59 last week, down from 314.66 February 1.

UnitedHealth is bracing for a struggle next year with the financial effects of shifting Medicare Advantage payment rates.

The health insurance giant released 2024 guidance on Tuesday that included a number of less favorable metrics than analysts expected.

During the company’s investor day in New York City on Wednesday, UnitedHealth executives blamed the outlook on an MA rate change issued by regulators earlier this year that insurers slam as a payment cut.

Pressured metrics include slower MA membership growth, lower margins at UnitedHealthcare and a higher medical loss ratio. UnitedHealth forecast a 2024 MLR of 84%, a full percentage point higher than analysts’ consensus expectation.

Despite the MA headwind, UnitedHealthcare’s financial targets overall still came in in-line or ahead of analyst expectations.

MA rates ‘ripple’ through UnitedHealth’s 2024

UnitedHealth is a behemoth in the U.S. healthcare industry, with one of the largest pharmacy benefits managers, an expanding healthcare IT arm and a growing presence in care delivery, including a network of tens of thousands of physicians.

UnitedHealth is also the dominant health insurer in many markets, including in MA. The Minnesota-based company is the largest provider of the privately-run Medicare plans.

Management has said they expect their share of the market to grow as more seniors age into the government insurance program and select MA over traditional Medicare.

However, UnitedHealth is now saying that MA growth could be depressed next year thanks to a rate notice from the CMS that’s deeply unpopular with insurers.

Earlier this year, the CMS finalized MA rates for 2024 that regulators said should result in a 3.3% increase in revenue for health insurers in the program. The changes also include a new approach to risk adjustment meant to curb upcoding, a practice where insurers inflate their members’ sicknesses to get higher payments from the government.

However, insurers have said the changes, which are being phased in over the next three years, will result in a net decrease to MA revenue overall.

“That rate notice has a material impact in terms of revenues associated with our Medicare Advantage portfolio, and as you can see that ripples through the metrics of the organization,” CEO Andrew Witty said during UnitedHealth’s investor day.

UnitedHealthcare, UnitedHealth’s health insurance division, now expects slower Medicare revenue and membership growth next year than analysts expected.

UnitedHealth expects to add between 325,000 and 375,000 Medicare Advantage members next year, representing almost 4% growth at the midpoint — “well below our model,” commented JP Morgan analyst Lisa Gill in a note.

That’s compared to 11% membership growth year to date in 2023, according to CMS data cited in a TD Cowen note. Previously, UnitedHealth leadership said they expected to grow above the overall MA industry growth rate in 2024, so “this appears to be a disappointment,” TD Cowen analyst Gary Taylor wrote.

However, “we are not materially surprised to see the slower growth rate in 2024 given the changes with the risk adjustment,” Gill said.

Some payers have said the rate changes could force them to cut benefits in MA. Yet, UnitedHealth has spent the last six months reconfiguring its plans in response to the rate notice, looking for ways to contain costs without curtailing benefits, Witty said.

UnitedHealthcare should bring in about $303 billion in revenue next year, mostly driven by Medicaid upside, the company said. TD Cowen’s Taylor noted he was unsure why UnitedHealth forecast the Medicaid improvement, given Medicaid payers are shedding members as states recheck eligibility for the safety-net insurance coming out of the COVID-19 pandemic.

UnitedHealth thinks its Medicaid enrollment will drop by up to 200,000 members next year due to redeterminations, the company said.

Eye on Optum Health

UnitedHealth leadership devoted half of their investor day to talking about the insurer’s plans to expand value-based care arrangements — a “core objective” for the next several years, Witty said.

A key actor in striving for that objective is Optum Health, UnitedHealth’s care delivery network that’s under the umbrella of its health services business Optum.

Optum released stronger 2024 guidance than analysts expected. Much of that growth is due to better-than-expected margins for Optum Health, analysts said.

Currently, Optum Health has about 4 million lives in fully accountable payment arrangements — a number that’s nearly doubled from 2021, said UnitedHealthcare CEO Brian Thompson during the investor day.

Optum Health expects to add another 750,000 lives by the end of next year.

”You should expect us to grow that number substantially each year,” Thompson said. “Our long-term ambition is to transition as many people as possible into value-based care.”

Overall, UnitedHealth expects 2024 adjusted profit of $27.50 to $28 a share, largely in line with what analysts expected.

Expected revenue is $400 billion to $403 billion, higher than Wall Street consensus.

Starting next month, UnitedHealthcare says it will move forward with plans to drop prior authorization requirements for a range of procedures, including dozens of radiology services and genetic tests, among others.

Why it matters:

UnitedHealth is among the health insurance giants who have announced plans to cut back on prior authorization as federal regulators consider tougher curbs on the practice.

Catch up quick:

Prior authorization is often criticized by patients and doctors, who complain they are an administrative burden or impede necessary care. Insurers, meanwhile, say prior authorization provides important guardrails against improper health care utilization, helping to keep costs down.

UnitedHealth, the largest commercial U.S. insurer, previously said its prior authorization removals will represent roughly 20% of its overall prior authorization volume.

Cigna and Aetna also announced plans to roll back some prior authorization requirements.

The Centers for Medicare and Medicaid Services proposed a rule to limit the amount of time insurers have to review requests on services for which they require prior approval, BenefitsPro previously reported.

Congress is also eyeing a plan to streamline and add transparency to the process by which Medicare Advantage plans can deny coverage for services via prior authorization.

Zoom in:

UnitedHealth says the removals will take effect Sept. 1 and Nov. 1 across the vast majority of its plans.

The company also spelled out which procedures would see prior authorization requirements removed. For instance, hundreds of codes for genetic testing — accounting for tens of thousands of prior authorization requests a year from commercial and Medicaid members — are among those that will be removed, officials said.

A code for cardiology stress test prior authorization for Medicare Advantage members will also be eliminated, reducing roughly 316,000 prior authorization requests a year.

The company next year also will roll out a “gold card” program eliminating most prior authorization requirements for doctors who have high approval rates.

Flashback: Earlier this summer, UnitedHealth walked back a controversial plan to require prior authorizations for colonoscopies and other endoscopic procedures.

Pent-up demand for delayed healthcare during the COVID-19 pandemic is pressuring medical costs for health insurers that had a financial windfall during the pandemic amid low utilization.

UnitedHealth, the parent company of the largest private payer in the U.S., expects its medical loss ratio — the share of premiums spent on member’s healthcare costs — to be higher than previously expected in the second quarter of 2023, due to a surge in outpatient care utilization among seniors, CFO John Rex said Tuesday during Goldman Sachs’ investor conference.

The news sent UnitedHealth’s stock down 7% in morning trade Wednesday, and affected other Medicare-focused health insurers as well. Humana, CVS and Centene — the three largest MA insurers by enrollee after UnitedHealth — dropped 13%, 6% and 8%, respectively.

Dive Insight:

The early days of COVID saw widespread halts in nonessential services, causing visits to plunge with an estimated one-third of U.S. adults delaying or foregoing medical care in the pandemic’s first year. By 2022, the sizable rebound in deferred care that many predicted had yet to materialize.

Now, early signs suggest utilization may again be increasing, with the cost of rebounding care coming around to hit payers. UnitedHealth now expects its MLR for the second quarter to reach or exceed its full-year target of 82.1% to 83.1%.

“As you look at a Q2, you would expect Q2 medical care ratio to be somewhere in the zone of probably the upper bound or moderately above the upper bound of our full-year outlook,” Rex said. “I would expect at this distance that the full year would probably settle in in the upper half of the existing range we set up.”

In comparison, the insurer reported an MLR of 82.2% in the first quarter of 2023. UnitedHealth’s MLR was 82% in 2022.

UnitedHealth said the MLR increase is because medical activity is normalizing after COVID kept seniors away from non-essential care.

“We’re seeing as behaviors kind of normalize across the country in a lot of different ways and mask mandates are dropped, especially in physician offices, we’re seeing that more seniors are just more comfortable accessing services for things that they might have pushed off a bit like knees and hips,” said Tim Noel, UnitedHealth’s chief executive for Medicare and retirement.

The Minnetonka, Minnesota-based insurer has seen strong outpatient demand through April, May and June, particularly in hips and knees with high volumes at its owned ambulatory surgical centers and within its Medicare business, executives said.

Inpatient volumes have remained consistent, and while outpatient utilization has increased, patient acuity has remained the same. Optum Health’s behavioral businesses are also seeing higher utilization in the second quarter, said Patrick Conway, CEO of Care Solutions at Optum, UnitedHealth’s health services division.

UnitedHealth doesn’t expect this higher activity to let up anytime soon. As a result, the payer incorporated higher outpatient utilization into its Medicare Advantage plan bids for 2024, which were placed in early June. The move attests to the longer duration of the trend, SVB Securities analyst Whit Mayo wrote in a note.

“Assuming it is going to end quickly wouldn’t be prudent on our part,” Rex said. “We’ll see how this progresses here.”

On Monday, Minnetonka, MN-based UHG’s Optum division made a $3.3B all-cash offer to acquire Baton Rouge, LA-based Amedisys, one of the country’s largest home health companies.

Optum’s bid came several weeks after Bannockburn, IL-based Option Care Health, a home health company specialized in drug and infusion services, offered to purchase Amedisys in an all-stock transaction valued at $3.6B. Amedisys itself acquired hospital-at-home company Contessa Health for $250M in 2021. While its Board of Directors is now evaluating whether UHG has made a “Superior Proposal”, a UHG acquisition of Amedisys would likely be subject to significant regulatory oversight, as the payer recently closed on its purchase of home health company and Amedisys-competitor LHC Group in a deal that was heavily scrutinized by the Federal Trade Commission.

The Gist: UHG, the nation’s largest health insurer, is on a tear to bring the country’s largest home health providers under its Optum umbrella—and it has the deep pockets to outbid nearly anyone else trying to do the same.

While some questioned the value of an Option Care-Amedisys combination, UHG would get to plug another asset into its scaled continuum of home-based care, allowing it to steer beneficiaries away from high-cost post acute care and continue to increase profitable intercompany eliminations.

If UHG’s bid for Amedisys is accepted, it would also gain its first hospital-at-home asset in Contessa, providing it with the opportunity to fully redirect—and reduce—its inpatient care spend.

In the mid-1980’s, managed care advocate Dr. Paul Ellwood predicted that eventually, US healthcare would be dominated by perhaps a dozen vast national firms he called SuperMeds that would combine managed care based health insurance with care delivery systems. Ellwood was a leader of the “managed competition” movement which advocated for a private sector alternative to a federal government-run National Health Insurance system. Ellwood and colleagues believed that Kaiser Foundation Health Plans and other HMOs would be able to stabilize health costs and thus affordably extend care to the uninsured.

The US political system and market dynamics would not co-operate with Ellwood and his Jackson Hole Group’s vision. In the ensuing thirty-five years, healthcare has remained both highly fragmented and regional in focus. However, unbeknownst to most, during the past decade, as a result of a major merger and relentless smaller acquisitions, two SuperMeds were born- CVS/Aetna and UnitedHealth Group, that whose combined revenues comprise 14% of total US health spending.

CVS/Aetna is slightly larger than United, by dint of grocery sales in its drugstores and its vast Caremark pharmacy benefits management business. However, CVS’s Aetna health insurance arm is one third the size of United’s, and though CVS is rapidly scaling up its care delivery apparatus through its in-store Health Hubs, it remains is a tiny fraction of United’s care footprint. Despite being slightly smaller at the top line, United’s market capitalization is more than 3.5 times that of CVS.

United’s vast scope is difficult to comprehend because much of it is not visible to the naked eye, and the most rapidly growing businesses are partly nested inside United’s health insurance business.

United employs over 300 thousand people. At $287.6 billion total revenues in 2021, United exceeded 7% of total US health spending (though $8.3 billion are from overseas operations).

In 2021, United was $100 billion larger than the British National Health Service. It is more than three times the size of Kaiser Permanente, and five times the size of HCA, the nation’s largest hospital chain. United is both larger and richer than energy giant Exxon Mobil. United has over $70 billion in cash and investments, and is generating about $2 billion a month in operating cash flow.

Its highly regulated health insurance business is the visible tip of a rapidly growing iceberg. Revenue from United’s core health insurance business grew at 11% in 2021, compared to 14% growth in United’s diversified Optum subsidiary. Optum generated $155.6 billion in 2021 (of which 60% were from INSIDE United’s health insurance business). You can see the relationship of Optum’s three major businesses to United’s health insurance operations in Exhibit I.

Optum is the Key to United’s Growth

Understanding the role of Optum is key to understanding United’s business. It is remarkable how few of my veteran health care colleagues have any idea what Optum is or what it does. Optum was once a sort of dumping ground for assorted United acquisitions without a seeming core purpose. A private equity colleague once derided Optum as “The Island of Lost Toys”. Now, however, Optum is driving United’s growth, and generates billions of dollars in unregulated profits both from inside the highly regulated core health insurance business and from external customers.

Optum consists of three parts:Optum Health, its care delivery enterprise ($54 billion revenues in 2021), Optum Rx, its pharmacy benefits management enterprise ($91 billion revenues in 2021) and Optum Insight, a diversified business services enterprise ($12.2 billion in 2021). Virtually all of United’s acquisitions join one of these three businesses.

Optum Health: The Third Largest Care Delivery Enterprise in the US

By itself, Optum Health is almost the size of HCA ($54 billion in 2021 vs HCA’s $58.7 billion) and consists of a vast national portfolio of care delivery entities: large physician groups, urgent care centers, surgicenters, imaging centers, and now by dint of the recently announced $5.7 billion acquisition of LHC, home health agencies. Optum Health has studiously avoided acquiring beds of any kind: hospitals, nursing homes, etc. and likely will continue to do so. Optum Health’s physician groups not only generate profits on their own, but also provide powerful leverage for United to control health costs for its own subscribers, pushing down United’s highly visible and regulated Medical Loss Ratio (MLR), and increasing health plan profits.

Optum Health began in 2007 when United acquired Nevada-based Sierra Health, and thus became the new owner of a small multispecialty physician group which Sierra owned. The group did not belong in United’s health insurance business and came to rest over in Optum. Over the past twelve years, Optum Health has acquired an impressive percentage of the major capitated medical groups in the US- Texas’ WellMed, California’s HealthCare Partners (from DaVita), as well as Monarch, AppleCare and North American Medical Management, Massachusetts’ Reliant (formerly Fallon Clinic) and Atrius in Massachusetts (pending) , Kelsey Seybold Clinic (also pending) in Houston, TX and Everett Clinic and PolyClinic in Seattle.

Optum Health claims over 60 thousand physicians, though many of these are actually independent physicians participating in “wrap around” risk contracting networks. By comparison, Kaiser Permanente’s Medical Groups employ about 23 thousand physicians. United’s management claims that Optum Health provides continuing care to about 20 million patients, of whom 3 million are covered by some form of so-called “value based” contracts. Perhaps half of this smaller number are covered by capitated (percentage of premium-PMPM) contracts.

Optum Health straddles fierce competitive relationships between United’s health insurance business and competing health plans in well more than a dozen metropolitan areas. Almost half (44%) of Optum Health’s revenues come from providing care for health plans other than United.

When Optum acquires a large physician group, it acquires those groups’ contracts with United’s health insurance competitors, some of which contracts have been in place for decades. Premium revenues from other health plans, presumably capitation or per member per month (PMPM) revenues, are one-quarter of Optum Health’s $54 billion total revenues. These “external” premium revenues have quadrupled since 2018, largely for Medicare Advantage subscribers. Optum Health contributes about $4.5 billion in operating profit to United. It is impossible to determine from United’s disclosures how much of this profit comes from Optum Health’s services provided to United’s insured lives and how much from its medical groups’ extensive contracts with competing health plans.

Optum Health’s surgicenters and urgent care centers provide affordable alternatives to using expensive hospital outpatient services and emergency departments, potentially further reducing United medical expense. This creates obvious tensions with United’s hospital networks, since Optum Health can use its large medical practices and virtual care offerings to divert patients from hospitals to its own services, or else render those services unnecessary.

Though some observers have termed Optum/United’s business model “vertical integration”-ownership of the suppliers to and distributors of a firm’s product– Optum Health has actually grown less vertical since 2018, with revenues from competing health plans growing from 36% of total revenues in 2018 to 44% in 2021. A 2018 analysis by ReCon Strategy found at best a sketchy matchup between United’s health plan enrollment by market and its Optum Health assets (https://reconstrategy.com/2018/04/uniteds-medicare-advantage-footprint-and-optumcare-network-do-not-overlap-much-so-far/.

Optum Rx: The Nation’s Third Largest Pharmacy Benefits Management Business

Optum’s largest business in revenues is its Optum Rx pharmaceutical benefits management (PBM) business, which generates $91 billion in revenues, and processes over a billion pharmacy claims not only for United but also many competing insurers and employer groups. Pharmaceutical costs are a rapidly growing piece of total medical expenses, and controlling them is yet another source of largely unregulated profits for United; Optum Rx generated over $4.1 billion of operating profit in 2021.

Optum Rx is the nation’s third largest PBM business after Caremark, owned by CVS/Aetna and Express Scripts, owned by CIGNA, and processes about 21% of all scripts written in the US. Pharmacy benefits management firms developed more than two decades ago to speed the conversion of patients from expensive branded drugs to generics on behalf of insurers and self-funded employers. They were given a big boost by George Bush’s 2004 Medicare Part D Prescription Drug benefit, as a “pro-competitive” private sector alternative to Medicare directly negotiating prices with pharmaceutical firms.

Reducing drug spending is one key to United’s profitability. Since generics represent almost 90% of all prescriptions written, Optum Rx now relies on fees generated by processing prescriptions and on rebates from pharmaceutical firms to promote their costly branded drugs as preferred drugs on Optum Rx’s formularies. These rebates are determined based on “list” prices for those drugs vs. the contracted price for the PBMs, and are actual cash payments from manufacturers to PBMs.

Drug rebates represent a significant fraction of operating profits for health insurers that own PBMs, particularly for their older Medicare Advantage patients that use a lot of expensive drugs. Unfortunately, PBMs have incentives to inflate the list price, because rebates are caculated based on the spread between list prices and the contract pricel Unfortunately, this increases subscribers’ cash outlays, because patient cost shares are based on list prices.

Optum Rx generates about 39% of its revenues (and an undeterminable percentage of its profits) serving other health insurers and self-funded employers. Many of those self-funded employers demand that Optum pass through the rebates directly to them (even if it means being charged higher administrative fees!).

Unlike the situation with Optum Health, the “verticality” of Optum’s PBM business-the percentage of Optum revenues derived from serving United subscribers- has increased in the last seven years, to more than 60% of Optum Rx’s total business. What happens to the billions of dollars in rebates generated by Optum Rx is impossible to determine from United’s disclosures. However, our best guess is that pharmaceutical rebates represent as much as a quarter of United’s total corporate profits.

Optum Insight: “Intelligent” Business Solutions

The fastest growing and by far the most profitable Optum business is its business intelligence/business services/consulting subsidiary. Optum Insight was generated $12.2 billion in revenues in 2021, but a 27.9% operating margin, five times that of United’s health insurance business. Optum Insight is strategically vital to enhancing the profitability of United’s health insurance activities, but also generates outside revenues selling services to United’s health insurance competitors and hospital networks.

The core of Optum Insight is a business intelligence enterprise formerly known as Ingenix, which provided “big data” to United and other insurers about hospital and pricing behavior and utilization-crucial both for benefits design and administration. In 2009, Ingenix was accused by New York State of under reporting prices for out of network health services for itself and its clients, which had the effect of reducing its own medical reimbursements, and increasing patient cost shares. United signed a consent decree to alter Ingenix business practices and settled a raft of lawsuits filed on behalf of patients, physicians and employers. Its name was subsequently changed to Optum Insight.

By dint of aggressive acquisitions, Optum Insight has dramatically increased its medical claims management business, consulting services and business process outsourcing activities. . Most of United’s investment in artificial intelligence can be found inside Optum Insight. Big data plays a crucial role in United’s overall strategy. Optum Insight’s claims management software uses vast medical claims data bases and artificial intelligence/machine learning software to spot and deny medical claims for which documentation is inadequate or where services are either “inappropriate” or else not covered by an individual’s health plan. Providers also claim that the same software rejects as many as 20% of their claims, often for problems as tiny as a mis-spelled word or a missing data field.

Optum Insight software plays a crucial role in helping United’s health insurance plans manage their medical expense. Traditional health plan profitability is generated by reducing medical expense relative to collected premiums to increase underwriting profit. These profits are regulated, with highly variable degrees of rigor by state health insurance commissioners, and also by provisions of ObamaCare enacted in 2010.

Though its acquisition of Equian in 2019 and the proposed $13 billion acquisition of health information technology conglomerate Change Healthcare in 2021, United came within an eyelash of a near monopoly on “intelligent” medical claims processing software. The Justice Department challenged this latter acquisition and United may agree to divest Change’s claims processing software business as a condition of closing the deal. Even without the Change acquisition, Optum Insight processes hundreds of millions of medical claims annually not only for United’s health insurance business but for many of United’s competitors.

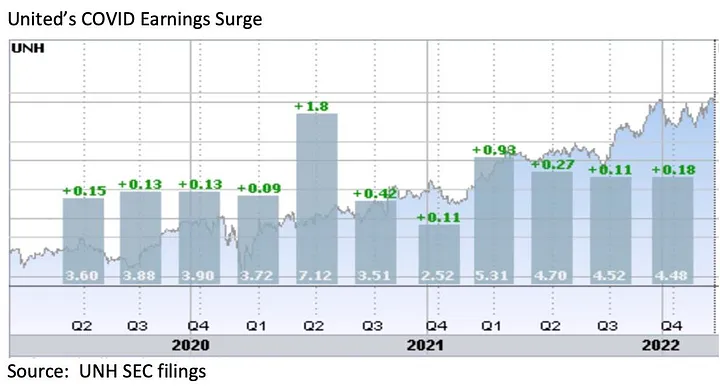

However, Optum Insight’s claims management system can also be used to increase MLR if medical expense unexpectedly declines, exposing the firm to federal requirement that it rebate excessive ‘savings’ to subscribers. This happened in 2020, when the COVID pandemic dramatically and unexpectedly added billions to United’s earnings due to hospitals suspending elective care. The chart below shows United’s 2Q2020 earnings per share almost doubling due to the precipitous drop in its medical claims expenses!

Hospital finance colleagues reported an immediate and substantial drop in medical claims denials from United and other carriers in the summer and fall of 2020. United’s quarterly profits dutifully and steeply declined in the subsequent two quarters, because its medical expenses sharply rebounded. The rise in

United’s medical expenses helped the firm avoid premium rebates to patients required by provisions of the ObamaCare legislation passed in 2010. The firm did voluntarily rebate about $1.5 billion to many of its customers in June, 2020.

However the most rapidly growing part of Optum Insight is its Optum 360 business process outsourcing business, which helps hospitals manage their billing and collections revenue cycle, as well as information technology operations, supply chain (purchasing and materials management) and other services. Through Optum 360, Optum Insight has signed five long term master contracts in the past two years’ worth many billions of dollars with care providers in California, Missouri and other states to provide a broad range of business services.

With all these different businesses, it is theoretically possible for one piece of Optum to be reducing a hospital’s cash flow by denying medical claims for United subscribers, while United’s health insurance network managers bargain aggressively to reduce the hospital’s reimbursement rates while yet another piece of Optum runs the billing and collection services for the same hospital and its employed physicians, while yet another piece of Optum competes with the hospital’s physicians and ambulatory services, diverting patients from its ERs and clinics, reducing the hospital’s revenues.

It is not difficult to imagine a future in which Optum/United offers hospital systems an Optum 360 outsourcing contract that run most of the business operations of a hospital system in exchange for preferred United health plan rates, an AI-enabled EZ pass on its medical claims denials and inpatient referrals from Optum physician groups and urgent care centers, at the expense of competing hospitals.

Managing these potential conflicts will be an increasing challenge as these various businesses grow, placing intense pressure on United’s leadership to get the various pieces of United to work together. To many anxious hospital executives, United resembles nothing so much as the Kraken, rising up out of the sea, surrounding and engulfing them- a powerful friend perhaps or a fearsome foe. As you might expect, United’s growing market power and growth has generated a fierce backlash in the hospital management community.

What Business is United Healthcare In?

United Healthcare is the most successful business in the history of American healthcare. The rapid growth of Optum and continued health insurance enrollment growth from government programs like Medicaid and Medicare has created a cash engine which generates nearly $2 billion a month in free cash flow. Optum’s portfolio has given United an impressive array of tools, unequalled in the industry, to improve its profitability and to reach into every corner of the US health system. United Healthcare is managed care on steroids.

United’s diversified portfolio of businesses gives the firm what a finance-savvy colleague termed “optionality”- the ability to redirect capital and management attention to areas of growth and away from areas that have ceased to grow, in the US or overseas. With its substantial investable capital, it will have the pick of the litter of the 11 thousand digital health companies as the overextended digital health market consolidates. United will be able to use its vast resources to build state-of-the-art digital infrastructure to reach and retain patients and manage their care.

United’s main short term business risks seem to be running out of accretive transactions effectively to deploy its growing horde of capital and managing the firm’s rising political exposure. United has had tremendous business discipline and has shied away from speculative acquisitions that are not immediately accretive to earnings. If its earnings growth falters, however, it will also encounter pressure from the investment community to increase dividends (presently about 1.2%) or share buybacks to bolster its share price, or else divest some or all of Optum in order to “maximize shareholder value”.

Answering the question, “What Business is United In” is simple: just about everything in health but hospitals and nursing homes.

Answering the questions- who are its customers and what do they want? — is a great deal harder. The customers United serves are in a sort of cold war with one another. United’s original business was protecting employers from health cost growth , and tempering the influence of hospitals and doctors by reducing their rates and utilization. By fostering so-called Consumer Directed Health Plans that expose many of their subscribers to very high front-end copayments, United and its health insurance brethren, have also increased their out-of-pocket costs, whether they have the savings to pay them or not.

There are also some ironies in United’s development. Optum Insight’s suite of hospital business services are designed to reduce administrative costs created in major part by United and other insurers’ medical claims data requirements. Its PBM business, originally intended to reduce drug spending by bargaining aggressively with pharmaceutical manufacturers has ended up pushing up drug list prices and consumer cost shares.

While presumably everybody benefits if United can somehow help patients become and remain healthy, it is still far from obvious how to do this. Managing all these markedly divergent customer needs will be a tremendous management challenge for whoever succeeds United’s reclusive (and very effective) 70 year old Chairman Stephen Hemsley.

What Does Society Get from this Vast Enterprise?

However, as Peter Drucker told a different generation of business giants, businesses are not entities unto themselves, accountable only to shareholders and customers. They are organs of society, and are expected to create social value. Americans are suspicious of vast enterprises, as businesses from Standard Oil, US Steel and ATT to Microsoft and Facebook have learned. As businesses grow and become more successful, public suspicion grows.

Private health insurers already face strident opposition from progressive Democrats, who believe that health coverage ought to be a public good, a right of citizenship provided publicly; in other words, that private health insurers have no business being in business. And large insurers like United also face intense opposition from hospitals and many physicians because they reduce their incomes and impose major administrative burdens upon them.

In the age of Twitter and TikTok, United is highly vulnerable to “event risks” that confirm the hostile narratives of the firm’s detractors that United is mainly about maximizing its own profits, not about improving the health of its subscribers or the communities it serves. It is not clear how many the tens of millions of United subscribers have warm and fuzzy feelings about their giant health insurer. Memories of the HMO backlash of the 1990’s reside in the firm’s corporate memory.

United has grown to its present immense scale largely without public knowledge. United has within its reach the capability of constraining overall health cost growth across dozens of metropolitan areas and regions, not merely cost growth for its own beneficiaries (roughly one in seven US citizens already get their health insurance through United). With its expanding digital health operations, it can deploy state of the art tools for helping United’s 50 million subscribers avoid illness and live healthier lives.

United also has the ability to damage the financial operations of beloved local hospitals and deny coverage to families, raising their out of pocket expenses. How United frames and defends its social mission and how it manages all the delicate and increasingly fraught customer relationships will determine its future, and in important ways, ours as well.

UnitedHealth Group expects Optum to see a long-term double-digit revenue growth rate and bring in a range between $212 billion to $214 billion in 2023 revenues.

The Minnetonka, Minn.-based healthcare giant shared Nov. 29 it projects growth margins of over 20 percent for technology products and low- to mid-single-digit growth for pharmacy care services.

2023 projections:

Optum Health Revenues: $91 billion to $92 billion Earnings: $7.4 billion to $7.6 billion

Optum Insight Revenues: $18.6 billion to $19.3 billion Earnings: $4.4 billion to $4.5 billion

OptumRx Revenues: $105.5 billion to $106.5 billion Earnings: $4.8 billion to $4.9 billion

UnitedHealth Group expects 2023 revenues of $357 billion to $360 billion, net earnings of $23.15 to $23.65 per share, and adjusted net earnings of $24.40 to $24.90 per share. Cash flows from operations are expected to be $27 billion to $28 billion.

UnitedHealthcareexpects 2023 revenues to range from $274 billion to $276 billion. By the end of this year, the payer’s revenues are expected to hit $249.2 billion, up from $222.9 billion in 2021.