Cartoon – To Cut Costs

Stanford and Lucile Packard Children’s hospitals in Palo Alto, Calif., and the Committee for Recognition of Nursing Achievement reached a tentative agreement on a three-year contract for about 5,000 nurses represented by the union, according to hospital and union statements.

The sides reached the agreement April 29, the fifth day of a strike, and union members approved it May 1.

“After extensive discussions, we were able to reach consensus on a contract that reflects our shared priorities and enhances existing benefits supporting our nurses’ health, well-being and ongoing professional development,” Stanford said in its latest negotiations update.

With the new agreement, striking nurses will return to work May 3.

Meanwhile, in a news release shared with Becker’s, the union highlighted parts of the agreement, including improvements it said “ensure high patient acuity is reflected in staffing.”

The agreement also includes a combined 7 percent base wage increase in 2022 (a 5 percent increase followed by a 2 percent increase) for nurses, 5 percent in 2023 and 5 percent in 2024, as well as funds specifically for mental healthcare of workers, according to the union.

As part of the labor deal, the hospitals also agreed to continue medical benefits for striking nurses without disruption, the union said.

“From day one of our contract negotiations, CRONA nurses have been unified in our goals of improving staffing and making our profession more sustainable,” Colleen Borges, president of CRONA and pediatric oncology nurse at Packard hospital, said in the release. “We stood strong behind our demands for fair contracts that give us the resources and support we need to take care of ourselves, our families and our patients. We are proud to provide world-class patient care — and are glad the hospitals have finally listened to us.”

Dale Beatty, DNP, RN, chief nurse executive and vice president of patient care services for Stanford Health Care, and Jesus Cepero, PhD, RN, senior vice president of patient care and chief nursing officer for Stanford Children’s Health, acknowledged on the Stanford negotiations page that reaching an agreement has been challenging.

Now “we can all take pride in this agreement. And we are proud of our team for maintaining continuity of care for our patients,” they said.

More information on negotiations is available here and here.

St. Louis-based Ascension reported higher expenses in the three months ended March 31 and ended the quarter with a loss, according to financial documents filed April 29.

The 143-hospital system reported operating revenue of $6.69 billion in the first three months of this year, up from $6.56 billion in the same period of 2021.

Ascension’s operating expenses climbed to $7.34 billion in the first three months of 2022, up from $6.59 billion in the same period a year earlier. The increase was attributed to several factors, including higher salaries, wages and supply expenses.

Looking at the first nine months of the current fiscal year, Ascension’s operating expenses increased 8.7 percent year over year. Staffing challenges, increased use of contract labor and overtime spend pushed Ascension’s total salaries, wages and benefits up 10.1 percent year over year in the nine months ended March 31.

Ascension ended the most recent quarter with an operating loss of $671.14 million, compared to an operating loss of $16.71 million in the same period last year.

After factoring in nonoperating items, Ascension reported a net loss of $884.74 million for the three months ended March 31. A year earlier, the health system posted net income of $957.32 million. For the first nine months ended March 31, Ascension reported net income of $145.21 million, compared to $4.77 billion in the same period a year earlier.

As of March 31, Ascension had 295 days cash on hand, compared to 336 days as of June 30, 2021.

https://mailchi.mp/df8b77a765df/the-weekly-gist-may-6-2022?e=d1e747d2d8

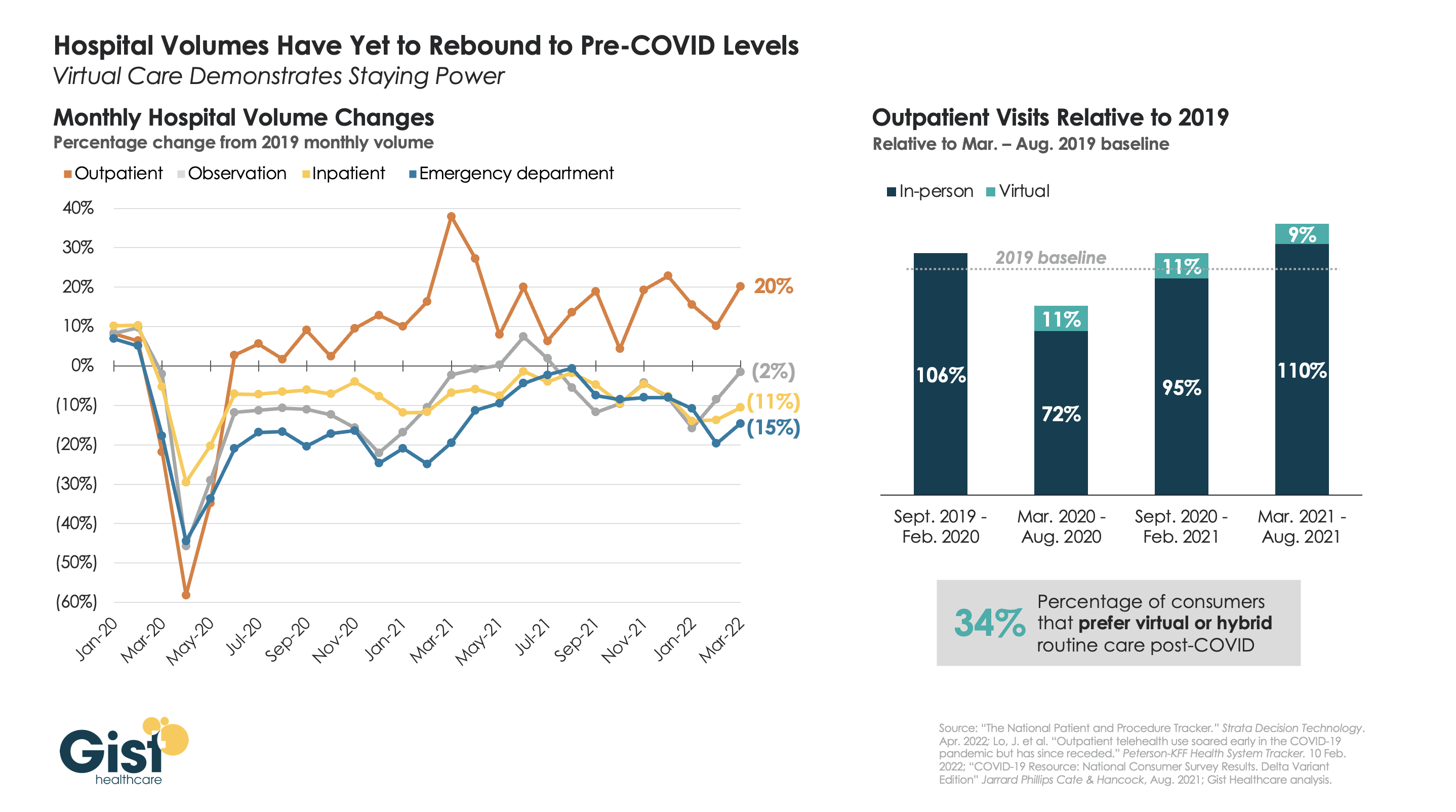

More than two years after the pandemic’s onset, some types of hospital volume still haven’t returned to pre-pandemic levels. The graphic above uses recent data from analytics firm Strata Decision Technology to track monthly hospital volume across various care settings.

While outpatient volume continues to exceed pre-COVID levels, inpatient, emergency department (ED), and observation volume is still below the 2019 baseline. The unpredictability of volume trends is likely to continue, as COVID continues to ebb and flow regionally, and care continues to shift outpatient.

By contrast, the volume of virtual care visits has remained consistent, even as consumers return to in-person outpatient visits, driving up the overall level above the pre-pandemic baseline. Some of this increase in outpatient visit volume has been driven by consumers turning to urgent care clinics or doctors’ offices—either in-person or virtually—for their lower-acuity care needs.

While temporary reimbursement and licensing policies for telehealth have been the main stumbling blocks for many organizations’ longer-term planning for virtual visits, about half of states have now implemented permanent payment parity for telemedicine. As such, provider organizations that are still taking a “wait and see approach” must develop an economically sustainable virtual care model to reduce costs and meet evolving consumer demands.

https://mailchi.mp/df8b77a765df/the-weekly-gist-may-6-2022?e=d1e747d2d8

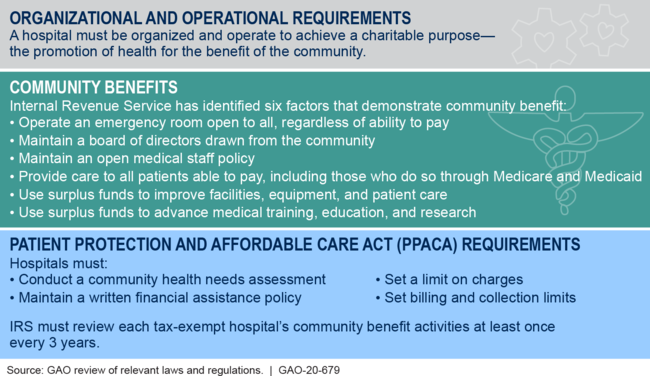

A report from The Lown Institute, a Boston-based think tank, finds that many health systems—227 of the 275 evaluated—spend less on providing “community benefit” than the value of their tax exemptions. The American Hospital Association (AHA) criticized the report’s methodology, claiming it “cherry-picks categories of community investment.” This report builds on previous analyses that have found that, taken together, nonprofit hospitals spend less on charity care than government or for-profit hospitals.

The Gist: Policymakers and academics, prompted by massive capital projects, high executive salaries, and—especially—aggressive pricing and billing strategies, are increasingly questioning whether nonprofit health systems provide sufficient community benefit to retain their tax-exempt status. A recent piece in Health Affairs suggests updating the community benefit standard, which the Internal Revenue Service (IRS) uses to evaluate nonprofit status, to focus on social determinants of health and measurable health outcomes.

We’d expect tougher scrutiny on this topic in the future, especially if state budgets come under pressure from a deterioration in the broader economy.

https://mailchi.mp/df8b77a765df/the-weekly-gist-may-6-2022?e=d1e747d2d8

If the leaked Supreme Court draft opinion overturning Roe v. Wade—which in 1973 established an individual’s constitutional right to an abortion—is finalized, as many as 26 states are either certain or likely to ban abortion. The resulting patchwork of abortion laws across the country could create confusion for providers and hospitals on multiple fronts, including cases related to the Federal Emergency Medical Treatment and Labor Act (EMTALA), as well as for health systems that operate in multiple states. Medical training on the procedure could become much more limited, as about half of the nation’s obstetrics and gynecology residencies are in states likely to ban abortion.

Recognizing the precarious position that abortion bans will put some providers in, the American Medical Association released a statement on Thursday saying that it is “deeply concerned” with the draft opinion, and that it “would lead to government interference in the patient-physician relationship, dangerous intrusion into the practice of medicine, and potentially criminalizing care.”

The Gist: Abortion is just one of a raft of issues where the provision of health services increasingly intersects with charged politics in this country. If Roe is overturned, medication abortion—the use of abortion pills—which already accounts for more than half of all abortions, will increase, although multiple states are already seeking to limit access.

Restricting access to safe abortions will also further exacerbate health disparities, driving up the already distressingly high US maternal mortality rate, especially among Black women. And overturning Roe would have implications far beyond access to abortion, especially for patients experiencing miscarriages, ectopic pregnancies, or other life-threatening medical conditions related to pregnancy.

Organizations should prepare themselves for a continuation of quits as a new culture of quitting becomes the norm as the annual quit rate stands to jump up nearly 20 percent from annual pre pandemic levels, according to Gartner.

The pre pandemic average for quits stood at 31.9 million, but that figure could rise to 37.4 million this year, said executive consultancy Gartner in an April 28 news release.

“An individual organization with a turnover rate of 20 percent before the pandemic could face a turnover rate as high as 24 percent in 2022 and the years to come,” Piers Hudson, senior director in the Gartner HR practice said in the news release. “For example, a workforce of 25,000 employees would need to prepare for an additional 1,000 voluntary departures.”

The reason for the likely increase in quits is new flexibility in work arrangements and employees’ higher expectations, according to Gartner. A misalignment between leaders and workers is also contributing to the attrition.

“Organizations must look forward, not backward, and design a post-pandemic employee experience that meets employees’ changing expectations and leverages the advantages of hybrid work,” said Mr. Hudson.