This week we showcase data from a recent American Antitrust Institute study on the growth of private equity (PE)-backed physician practices, and the impact of this growth on market competition and healthcare prices.

From 2012 to 2021, the annual number of practice acquisitions by private equity groups increased six-fold, especially in high-margin specialties. During this same time period, the number of metropolitan areas in which a single PE-backed practice held over 30 percent market share rose to cover over one quarter of the country.

These “hyper-concentrated” markets are especially prevalent in less-regulated states with fast-growing senior populations, like Arizona, Texas, and Florida.

The study also found an association between PE practice acquisitions and higher healthcare prices. In highly concentrated markets, certain specialties, like gastroenterology, were able to raise prices rise by as much as 18 percent.

While new Federal Trade Commission proposals demonstrate the government’s renewed interest in antitrust enforcement, it may be too little, too late to mitigate the impact of specialist concentration in many states.

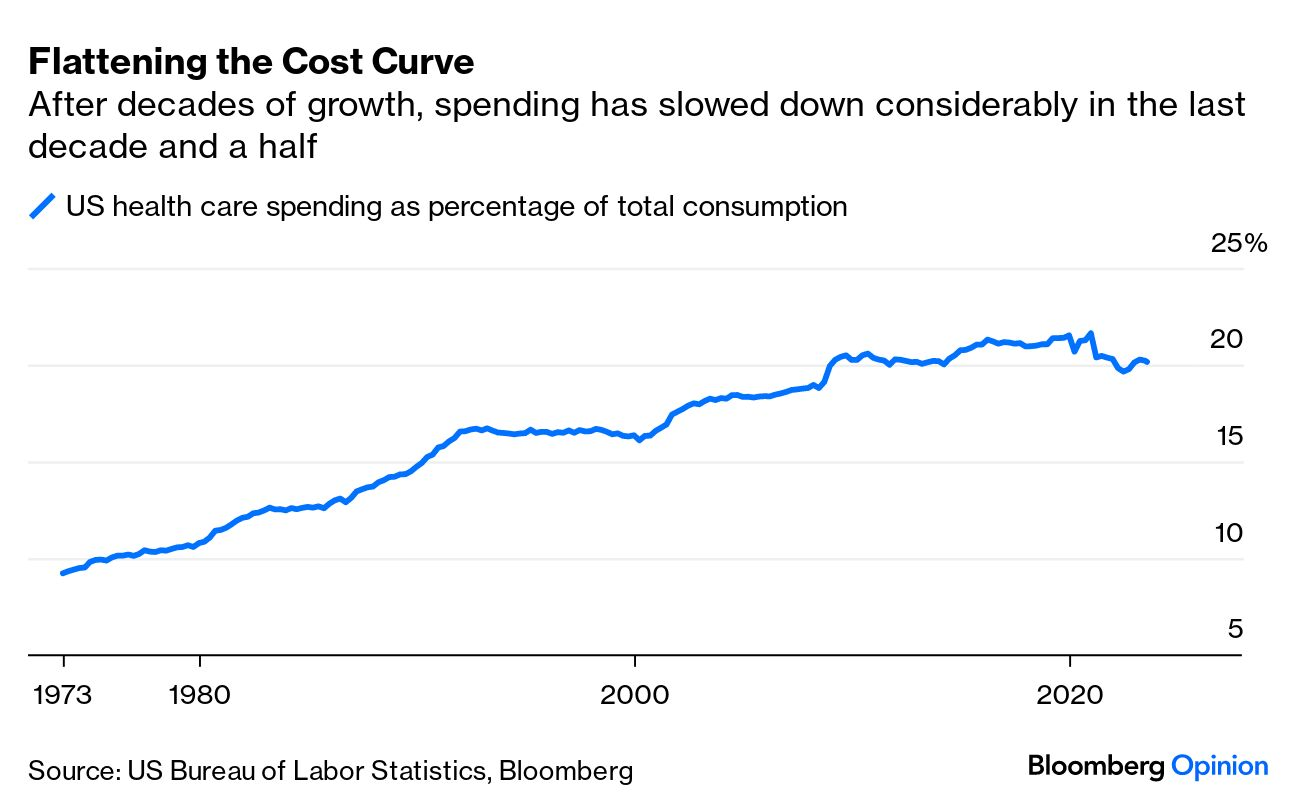

A piece published this week in the New York Times documents how Medicare spending per beneficiary has flattened since the early 2010s, coming in below projections by nearly $4T.

While the authors run through possible explanations, including changes made by the Affordable Care Act and to the Medicare Advantage program, the proliferation of effective cholesterol and blood-pressure medications, and fewer breakthroughs in new, expensive drug classes, they acknowledge that scholars have not reached a consensus on the primary drivers of this trend.

Beyond academic debate, there is also no agreement on how long the flattened spending pattern will hold—or what factors might reignite rapid cost growth.

The Gist:

Whatever the causes of this phenomenon, it has helped avert the kind of Medicare austerity measures that dominated political debates on the program in past decades.

We assume some of this flattening has to do with the fact that the average age of Medicare beneficiaries has dropped as Baby Boomers have entered the program in droves, given that younger beneficiaries are much less costly to insure.

In coming decades, the average age of Medicare beneficiaries will increase, along with their care costs, and the total number of Medicare beneficiaries will continue to rise.

By 2053, seniors will make up over 22 percent of the population and over 40 percent of the projected federal budget will be spent on programs for them.

Last Friday, CMS released a proposed rule that would require nursing homes and other long-term care facilities to provide a minimum 2.5 hours of care per patient per day from nursing aides and 33 minutes of care from registered nurses, at least one of whom must be on site at all times.

The standards are lower than many industry experts were expecting, but CMS still estimates that 75 percent of nursing homes will have to increase staffing to meet these minimums. CMS will also allow facilities a temporary hardship exception if they can prove their region has a local worker shortage, and they have made good faith efforts to hire and retain staff.

The Gist:

A proposal to strengthen long-term care staffing standards was expected, as COVID’s toll on nursing homes included over 200k deaths among residents and staff, as well as a mass exodus of its workforce.

But many facilities will struggle to meet these new standards, as nursing home employment is still down 11 percent from pre-pandemic levels.

Staffing shortages at long-term care facilities have been even more severe than those experienced by hospitals. The need to ramp up staffing levels will not only raise the cost of nursing home care, but will also exacerbate shortages for nursing talent in other care settings.

Facilities that decide to close rather than comply will impact other parts of the care continuum, including exacerbating acute hospital discharge delays.

On Tuesday, CMS announced the States Advancing All-Payer Health Equity Approaches and Development (AHEAD) Model, a new payment model that will give up to eight states or sub-state regions the ability to test global hospital budgets across an 11-year period.

Participating states will assume responsibility for managing healthcare costs for traditional Medicare and Medicaid populations, while encouraging private payers to pay hospitals under a similar relationship.

Primary care practices will have the option to participate in a primary care component of the model, called Primary Care AHEAD, in which they will receive a Medicare care management fee and be required to engage in state-led Medicaid transformation initiatives.

CMS is hoping that the AHEAD model will reduce healthcare cost growth, improve population health, and reduce health outcome disparities. It builds upon existing Innovation Center state-based models, including the Maryland Total Cost of Care Model, the Vermont All-Payer Accountable Care Organization Model, and the Pennsylvania Rural Health Model, which have all shown promise in lowering Medicare spending while improving patient outcomes.

Program applications will open late this year, and the first states selected would begin a pre-implementation period in summer 2024.

The Gist:

Shifting to a total-cost-of-care model will be a difficult undertaking for even the most motivated states.

Though a stable annual budget may be a welcome prospect to struggling hospitals, large regional systems may balk at the idea, especially as the Maryland Hospital Association has claimed that their state’s regulated rates have lagged hospital cost inflation by 1.3 percent per year.

With the Medicare Shared Savings Program (MSSP)saving only one quarter of one percent of Medicare’s total spending in 2022, CMS has good reason to explore other ways to reduce Medicare cost growth

—but these Innovation Center models will only achieve their goals if they can first induce sufficient participation.

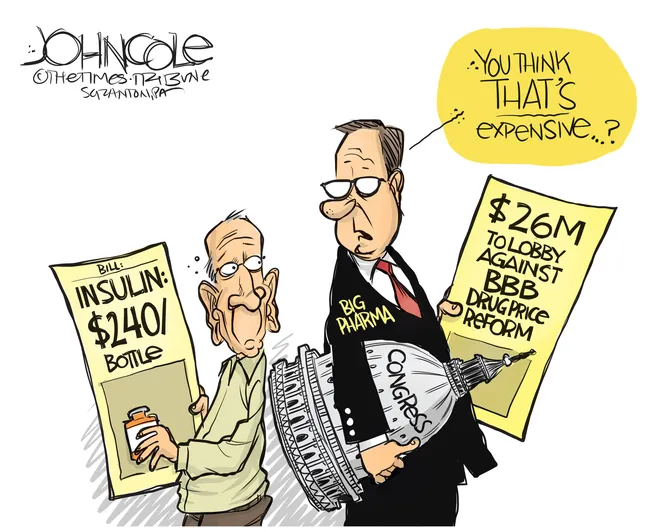

Last week, the Centers for Medicare and Medicaid Services (CMS) released the list of the first round of prescription drugs chosen for Medicare Part D price negotiations. The 2022 Inflation Reduction Act (IRA) granted CMS the authority to negotiate directly with pharmaceutical manufacturers, establishing a process that will ramp up to include 20 drugs per year and cover Part B medicines by 2029.

The majority of the initial 10 medications, including Eliquis, Jardiance, and Xarelto, are highly utilized across Medicare beneficiaries, treating mainly diabetes and cardiovascular disease. But three of the drugs (Enbrel, Imbruvica, and Stelara) are very high-cost drugs used by fewer than 50k beneficiaries to treat some cancers and autoimmune diseases.

Together the 10 drugs cost Medicare about $50B annually, comprising 20 percent of Part D spending. Drug manufacturers must now engage with CMS in a complex negotiation process, with negotiated prices scheduled to go into effect in 2026.

The Gist:

Most of the drugs on this list are not a surprise, with the Biden administration prioritizing more common chronic disease medications, with large total spend for the program, over the most expensive drugs, many of which are exempted by the IRA’s minimum seven-year grace period for new pharmaceuticals.

However, pharmaceutical companies are threatening to derail the process before it even begins. Several companies with drugs on the list have already filed lawsuits against the government on the grounds that the entire negotiation program is unconstitutional.

While President Biden is already touting lowering drug prices as a key plank of his reelection pitch, it will take years before these negotiations translate into lower costs for beneficiaries and reduced government spending. There also may be adverse unintended consequences, as drug companies may raise prices for commercial payers while increasing rebates to stabilize net prices, leading to higher costs for some consumers.

Still, it’s a step in the right direction for the US, given that we pay 2.4 times more than peer countries for prescription medications.

Last Tuesday, the Center for Medicare and Medicaid Services (CMS) announced the first 10 medicines that will be subject to price negotiations with Medicare starting in 2026 per authorization in the Inflation Reduction Act (2022). It’s a big deal but far from a done deal.

Here are the 10:

Eliquis, for preventing strokes and blood clots, from Bristol Myers Squibb and Pfizer

Jardiance, for Type 2 diabetes and heart failure, from Boehringer Ingelheim and Eli Lilly

Xarelto, for preventing strokes and blood clots, from Johnson & Johnson

Januvia, for Type 2 diabetes, from Merck

Farxiga, for chronic kidney disease, from AstraZeneca

Entresto, for heart failure, from Novartis

Enbrel, for arthritis and other autoimmune conditions, from Amgen

Imbruvica, for blood cancers, from AbbVie and Johnson & Johnson

Stelara, for Crohn’s disease, from Johnson & Johnson

Fiasp and NovoLog insulin products, for diabetes, from Novo Nordisk

Notably, they include products from 10 of the biggest drug manufacturers that operate in the U.S. including 4 headquartered here (Johnson and Johnson, Merck, Lilly, Amgen) and the list covers a wide range of medical conditions that benefit from daily medications.

But only one cancer medicine was included (Johnson & Johnson and AbbVie’s Imbruvica for lymphoma) leaving cancer drugs alongside therapeutics for weight loss, Crohn’s and others to prepare for listing in 2027 or later.

And CMS included long-acting insulins in the inaugural list naming six products manufactured by the Danish pharmaceutical giant Novo Nordisk while leaving the competing products made by J&J and others off. So, there were surprises.

To date, 8 lawsuits have been filed against the U.S. Department of Health and Human Services by drug manufacturers and the likelihood litigation will end up in the Supreme Court is high.

These cases are being brought because drug manufacturers believe government-imposed price controls are illegal. The arguments will be closely watched because they hit at a more fundamental question:

what’s the role of the federal government in making healthcare in the U.S. more affordable to more people?

Every major sector in healthcare– hospitals, health insurers, medical device manufacturers, physician organizations, information technology companies, consultancies, advisors et al may be impacted as the $4.6 trillion industry is scrutinized more closely . All depend on its regulatory complexity to keep prices high, outsiders out and growth predictable. The pharmaceutical industry just happens to be its most visible.

The Pharmaceutical Industry

The facts are these:

66% of American’s take one or more prescriptions: There were 4.73 billion prescriptions dispensed in the U.S. in 2022

Americans spent $633.5 billion on their medicines in 2022 and will spend $605-$635 billion in 2025.

This year (2023), the U.S. pharmaceutical market will account for 43.7% of the global pharmaceutical market and more than 70% of the industry’s profits.

41% of Americans say they have a fair amount or a great deal of trust in pharmaceutical companies to look out for their best interests and 83% favor allowing Medicare to negotiate pricing directly with drug manufacturers (the same as Veteran’s Health does).

There were 1,106 COVID-19 vaccines and drugs in development as of March 18, 2023.

The U.S. industry employs 811,000 directly and 3.2 million indirectly including the 325,000 pharmacists who earn an average of $129,000/year and 447,000 pharm techs who earn $38,000.

And, in the U.S., drug companies spent $100 billion last year for R&D.

It’s a big, high-profile industry that claims 7 of the Top 10 highest paid CEOs in healthcare in its ranks, a persistent presence in social media and paid advertising for its brands and inexplicably strong influence in politics and physician treatment decisions.

The industry is not well liked by consumers, regulators and trading partners but uses every legal lever including patents, couponing, PBM distortion, pay-to-delay tactics, biosimilar roadblocks et al to protect its shareholders’ interests. And it has been effective for its members and advisors.

My take:

It’s easy to pile-on to criticism of the industry’s opaque pricing, lack of operational transparency, inadequate capture of drug efficacy and effectiveness data and impotent punishment against its bad actors and their enablers.

It’s clear U.S. pharma consumers fund the majority of the global industry’s profits while the rest of the world benefits.

And it’s obvious U.S. consumers think it appropriate for the federal government to step in. The tricky part is not just government-imposed price controls for a handful of drugs; it’s how far the federal government should play in other sectors prone to neglect of affordability and equitable access.

There will be lessons learned as this Inflation Reduction Act program is enacted alongside others in the bill– insulin price caps at $35/month per covered prescription, access to adult vaccines without cost-sharing, a yearly cap ($2,000 in 2025) on out-of-pocket prescription drug costs in Medicare and expansion of the low-income subsidy program under Medicare Part D to 150% of the federal poverty level starting in 2024. And since implementation of these price caps isn’t until 2026, plenty of time for all parties to negotiate, spin and adapt.

But the bigger impact of this program will be in other sectors where pricing is opaque, the public’s suspicious and valid and reliable data is readily available to challenge widely-accepted but flawed assertions about quality, value, access and outcomes. It’s highly likely hospitals will be next.

The GOP Presidential debate marked the unofficial start of the 2024 Presidential campaign. With the exception of continued funding for Ukraine, style points won over issue distinctions as each of the 8 White House aspirants sought to make the cut to the next debate September 27 at the Reagan Library in Simi Valley, CA.

For the candidates in Milwaukee, it’s about “Stayin’ Alive” per the BeeGee’s hit song: that means avoiding self-inflicted harm while privately raising money to keep their campaigns afloat. And, based on Debate One, with the exception of abortion, that means they’ll not face questions about their positions on the litany of issues that dominate healthcare these days i.e., drug prices, hospital consolidation, price transparency, workforce burnout and many others. In Milwaukee, healthcare was essentially ‘out of sight our of mind’ to the moderators and debaters despite being 18% of the U.S. economy and its biggest employer.

For now, each will enlist ghostwriters to produce position papers for their websites, and, on occasion, reporters will press for specifics to test their grasp on a topic but that’s about it. Based on last Wednesday’s 2-hour event, it’s unlikely general media outlets like Fox News (which also hosts Debate Two) will explore healthcare issues except for abortion.

That means healthcare will be subordinated to the economy, inflation, immigration and crime—the top issues to GOP voters—for most of the Presidential primary season.

Next November, voters will also elect 34 US Senators, 435 members of the House of Representatives, 11 Governors and their representatives in 85 state legislative bodies. This will be the first election cycle after reapportionment of votes in the United States Electoral College following the 2020 United States census. Swing states (WI, MI, PA, NV, AZ, GA, FL, OH, CO, VA) will again be keys to the Presidential results since demographics and population shifts have increased the concentrations of each party’s core voters in so-called Blue States and Red States:

The Democratic voter core is diverse, educated and culturally liberal with its strongest appeal to African-Americans, Latinos, women, educated professionals and urban voters. Blue States are predominantly in the Northeast, Upper Midwest and West Coast regions.

The Republican voter core consists of rural white voters, evangelicals, the elderly, and non-college educated adults. Red States are predominantly in the South and Southwest.

The increased concentrations of Blue or Red voters in certain states and regions has contributed to political polarization in the U.S. electorate and presents an unusual challenge to healthcare. Per Gallup: “Political polarization since 2003 has increased most significantly on issues related to federal government power, global warming and the environment, education, abortion, foreign trade, immigration, gun laws, the government’s role in providing healthcare, and income tax fairness. Increased polarization has been less evident on certain moral issues and satisfaction with the state of race relations.”

Thus, healthcare issues are increasingly subject to hyper partisanship and often misinformation.

Given the limited knowledge voters have on most health issues and growing prevalence of social media fueled misinformation, political polarization creates echo chambers in healthcare—one that thinks the system works for those who can afford it and another that thinks that’s wrong.

It’s dicey for politicians: it’s political malpractice to offer specific solutions on anything, especially healthcare. It’s safer to attack its biggest vulnerabilities—affordability and equitable access—even though they mean something different in every echo chamber.

My take:

Barring a second Covid pandemic or global conflict with Russia/China, it’s unlikely healthcare issues will be prominent in Campaign 2024 at the national level except for abortion. At least through the May primary season, here’s the political landscape for healthcare:

Affordability and inequitable access will be the focus of candidate rhetoric at the national level: Trust and confidence in the U.S. health system has eroded. That’s fertile political turf for critics.

In Congress, the fiercest defenders of the status quo have joined efforts to impose restrictions on consolidation and price transparency for hospitals and price controls for prescription drugs. There’s Bipartisan acknowledgement that inequities in accessing care are significant and increasing, especially in minority and low income populations. They differ over the remedy. Employers expect their health costs to increase at least 8% next year and blame hospitals and drug companies for price gauging and want Congress to do more. 85% of Democrats think “the government should insure everyone” vs. 33% of Republican voters which calcifies inaction in a divided Congress though. Opposition to the Affordable Care Act (2010) has softened and Medicaid expansion has passed in 40 Blue and Red states.

In the 2024 election cycle, remedies for increased access and more affordability will pit Republicans calling for more competition, consumerism and transparency and Democrats calling for more government funding, regulation and fairness.

But more important, voter and employer frustration with partisan bickering sans solutions will set the stage for the vigorous debate about a single payer system in 2026 and after,

State elections will give more attention to healthcare issues than the Presidential race: That’s because Governors and state legislators set direction on issues like abortion rights, drug price controls, Medicaid funding, scope of practice allowances and others.

Increasingly, state Attorney’s General and Treasurers are weighing in on consolidation and spending. States referee workforce issues like nurse staffing requirements and others. And ballot referenda on healthcare issues trail only public education as a focus of grassroots voter activity. At the top of that list is abortion rights:

In 25 states and DC, there are no restrictions on access; in 14 states, abortion is banned and in 11 abortions—both procedures and medication—are legal, but with gestational limits from 6 weeks (GA), to between 12 and 22 weeks (AZ, UT, NE, KS, IA, IN, OH, NC, SC, FL). It’s an issue that divides legislators and increasingly delineates Blue and Red states and in many states remains unsettled.

Other healthcare issues, like ageism, will surface in Campaign 2024 in the context of other topics: Finally, healthcare will factor into other issues: Example: The leading Presidential candidates are seniors: President Biden was the oldest person to assume the office at age 78 and would be would be 86 at the end of his second term. Former President Trump was 70 when elected in 2016 and would be 81 if elected when his second term ends.

The majority of Americans are concerned about the impact of age on fitness to serve among aspirants for high office: cognitive impairment, dementia, physical limitations et al. will be necessary talking points in campaigns and media coverage. Similarly, cybersecurity looms as a focus where healthcare’s data-rich dependence is directly impacted. Growing concern about climate and the food supply, sourcing of raw good and materials from China used in drug manufacturing and many other headlines will infer healthcare context.

Summary:

Healthcare will be on the ballot in 2024 and might very well make the difference in who wins and loses in many state and local elections.

It will make a difference in the Presidential campaign as part of the economy and a major focus of government spending. Beyond abortion, the lack of attention to other aspects of the health system in the Milwaukee debate last week should in no way be interpreted as a pass for healthcare insiders.

Voters are restless and healthcare is contributing. Healthcare is far from ‘out of sight, out of mind’ in Campaign 2024.

Studies show healthcare affordability is an issue to voters as medical debt soars (KFF) and public disaffection for the “medical system” (per Gallup, Pew) plummets. But does it really matter to the hospitals, insurers, physicians, drug and device manufacturers and army of advisors and trade groups that control the health system?

Each sector talks about affordability blaming inflation, growing demand, oppressive regulation and each other for higher costs and unwanted attention to the issue.

Each play their victim cards in well-orchestrated ad campaigns targeted to state and federal lawmakers whose votes they hope to buy.

Each considers aggregate health spending—projected to increase at 5.4%/year through 2031 vs. 4.6% GDP growth—a value relative to the health and wellbeing of the population. And each thinks its strategies to address affordability are adequate and the public’s concern understandable but ill-informed.

As the House reconvenes this week joining the Senate in negotiating a resolution to the potential federal budget default October 1, the question facing national and state lawmakers is simple: is the juice worth the squeeze?

Is the US health system deserving of its significance as the fastest-growing component of the total US economy (18.3% of total GDP today projected to be 19.6% in 2031), its largest private sector employer and mainstay for private investors?

Does it deserve the legal concessions made to its incumbents vis a vis patent approvals, tax exemptions for hospitals and employers, authorized monopolies and oligopolies that enable its strongest to survive and weaker to disappear?

Does it merit its oversized role, given competing priorities emerging in our society—AI and technology, climate changes, income, public health erosion, education system failure, racial inequity, crime and global tension with China, Russia and others.

In the last 2 weeks, influential Republicans leaders (Burgess, Cassidy) announced plans to tackle health costs and the role AI will play in the future of the system. Last Tuesday, CMS announced its latest pilot program to tackle spending: the States Advancing All-Payer Health Equity Approaches and Development Model (AHEAD Model) is a total cost of care budgeting program to roll out in 8 states starting in 2026. The Presidential campaigns are voicing frustration with the system and the spotlight on its business practices intensifying.

So, is affordability to the federal government likely to get more attention?

Yes. Is affordability on state radars as legislatures juggle funding for Medicaid, public health and other programs?

Yes, but on a program by program, non-system basis.

Is affordability front and center in CMS value agenda including the new models like its AHEAD model announced last week? Not really.

CMS has focused more on pushing hospitals and physicians to participate than engaging consumers. Is affordability for those most threatened—low and middle income households with high deductible insurance, the uninsured and under-insured, those with an expensive medical condition—front of mind? Every minute of every day.

Per CMS, out-of-pocket spending increased 4.3% in 2022 (down from 10.4% in 2021) and “is expected to accelerate to 5.2%, in part related to faster health care price growth. During 2025–31, average out-of-pocket spending growth is projected to be 4.1% per year.” But these data are misleading. It’s dramatically higher for certain populations and even those with attractive employer-sponsored health benefits worry about unexpected household medical bills.

So, affordability is a tricky issue that’s front of mind to 40% of the population today and more tomorrow.

Legislation that limits surprise medical bills, requires drug, hospital and insurer price transparency, expands scope of practice opportunities for mid-level professionals, avails consumers of telehealth services, restricts aggressive patient debt collection policies and others has done little to assuage affordability issues for consumers.

Ditto CMS’ value agenda which is more about reducing Medicare spending through shared savings programs with hospitals and physicians than improving affordability for consumers. That’s why outsiders like Walmart, Best Buy and others see opportunity: they think patients (aka members, enrollees, end users) deserve affordability solutions more than lip service.

Affordability to consumers is the most formidable challenge facing the US healthcare industry–more than burnout, operating margins, reimbursement or alternative payment models. Today, it is not taken seriously by insiders. If it was, evidence would be readily available and compelling. But it’s not.

Five years ago, I started the Fixing Healthcare podcast with the aim of spotlighting the boldest possible solutions—ones that could completely transform our nation’s broken medical system.

But since then, rather than improving, U.S. healthcare has fallen further behind its global peers, notching far more failures than wins.

In that time, the rate of chronic disease has climbed while life expectancy has fallen, dramatically. Nearly half of American adults now struggle to afford healthcare. In addition, a growing mental-health crisis grips our country. Maternal mortality is on the rise. And healthcare disparities are expanding along racial and socioeconomic lines.

Reflecting on why few if any of these recommendations have been implemented, I don’t believe the problem has been a lack of desire to change or the quality of ideas. Rather, the biggest obstacle has been the immense size and scope of the changes proposed.

To overcome the inertia, our nation will need to narrow its ambitions and begin with a few incremental steps that address key failures. Here are three actionable and inexpensive steps that elected officials and healthcare leaders can quickly take to improve our nation’s health:

1. Shore Up Primary Care

Compared to the United States, the world’s most-effective and highest-performing healthcare systems deliver better quality of care at significantly lower costs.

One important difference between us and them: primary care.

In most high-income nations, primary care makes up roughly half of the physician workforce. In the United States, it accounts for less than 30% (with a projected shortage of 48,000 primary care physicians over the next decade).

Primary care—better than any other specialty—simultaneously increases life expectancy while lowering overall medical expenses by (a) screening for and preventing diseases and (b) helping patients with chronic illness avoid the deadliest and most-expensive complications (heart attack, stroke, cancer).

But considering that it takes at least three years after medical school to train a primary care physician, to make a dent in the shortage over the next five years the U.S. government must act immediately:

The first action is to expand resident education for primary care. Congress, which authorizes the funding, would allocate $200 million annually to create 1,000 additional primary-care residency positions each year. The cost would be less than 0.2% of federal spending on healthcare.

The second action requires no additional spending. Instead, the Centers for Medicare & Medicaid Services, which covers the cost of care for roughly half of all American adults, would shift dollars to narrow the $108,000 pay gap between primary care doctors and specialists. This will help attract the best medical students to the specialty.

Together, these actions will bolster primary care and improve the health of millions.

2. Use Technology To Expand Access, Lower Costs

A decade after the passage of the Affordable Care Act, 30 million Americans are without health insurance while tens of millions more are underinsured, limiting access to necessary medical care.

Furthermore, healthcare is expected to become even less affordable for most Americans. Without urgent action, national medical expenditures are projected to rise from $4.3 trillion to $7.2 trillion over the next eight years, and the Medicare trust fund will become insolvent.

With costs soaring, payers (businesses and government) will resist any proposal that expands coverage and, most likely, will look to restrict health benefits as premiums rise.

Almost every industry that has had to overcome similar financial headwinds did so with technology. Healthcare can take a page from this playbook by expanding the use of telemedicine and generative AI.

At the peak of the Covid-19 pandemic, telehealth visits accounted for 69% of all physician appointments as the government waived restrictions on usage. And, contrary to widespread fears at the time, patients and doctors rated the quality, convenience and safety of these virtual visits as excellent. However, with the end of Covid-19, many states are now restricting telemedicine, particularly when clinicians practice in a different state than the patient.

To expand telemedicine use—both for physical and mental health issues—state legislators and regulators will need to loosen restrictions on virtual care. This will increase access for patients and diminish the cost of medical care.

It doesn’t make sense that doctors can provide treatment to people who drive across state lines, but they can’t offer the same care virtually when the individual is at home.

Similarly, physicians who faced a shortage of hospital beds during the pandemic began to treat patients in their homes. As with telemedicine, the excellent quality and convenience of care drew praise from clinicians and patients alike.

Building on that success, doctors could combine wearable devices and generative AI tools like ChatGPT to monitor patients 24/7. Doing so would allow physicians to relocate care—safely and more affordably—from hospitals to people’s homes.

Translating this technology-driven opportunity into standard medical practice will require federal agencies like the FDA, NIH and CDC to encourage pilot projects and facilitate innovative, inexpensive applications of generative AI, rather than restricting their use.

3. Reduce Disparities In Medical Care

American healthcare is a system of haves and have-nots, where your income and race heavily determine the quality of care you receive.

Black patients, in particular, experience poorer outcomes from chronic disease and greater difficulty accessing state-of-the-art treatments. In childbirth, black mothers in the U.S. die at twice the rate of white women, even when data are corrected for insurance and financial status.

Generative AI applications like ChatGPT can help, provided that hospitals and clinicians embrace it for the purpose of providing more inclusive, equitable care.

Previous AI tools were narrow and designed by researchers to mirror how doctors practiced. As a result, when clinicians provided inferior care to Black patients, AI outputs proved equally biased. Now that we understand the problem of implicit human bias, future generations of ChatGPT can help overcome it.

The first step will be for hospitals leaders to connect electronic health record systems to generative AI apps. Then, they will need to prompt the technology to notify clinicians when they provide insufficient care to patients from different racial or socioeconomic backgrounds. Bringing implicit bias to consciousness would save the lives of more Black women and children during delivery and could go a long way toward reversing our nation’s embarrassing maternal mortality rate (along with improving the country’s health overall).

The Next Five Years

Two things are inevitable over the next five years. Both will challenge the practice of medicine like never before and each has the potential to transform American healthcare.

First, generative AI will provide patients with more options and greater control. Faced with the difficulty of finding an available doctor, patients will turn to chatbots for their physical and psychological problems.

Already, AI has been shown to be more accurate in diagnosing medical problems and even more empathetic than clinicians in responding to patient messages. The latest versions of generative AI are not ready to fulfill the most complex clinical roles, but they will be in five years when they are 30-times more powerful and capable.

Second, the retail giants (Amazon, CVS, Walmart) will play an ever-bigger role in care delivery. Each of these retailers has acquired primary care, pharmacy, IT and insurance capability and all appear focused on Medicare Advantage, the capitated option for people over the age of 65. Five years from now, they will be ready to provide the businesses that pay for the medical coverage of over 150 million Americans the same type of prepaid, value-based healthcare that currently isn’t available in nearly all parts of the country.

American healthcare can stop the current slide over the next five years if change begins now. I urge medical leaders and elected officials to lead the process by joining forces and implementing these highly effective, inexpensive approaches to rebuilding primary care, lowering medical costs, improving access and making healthcare more equitable.