CommonSpirit Health, which operates 142 hospitals in 21 states, reported an operating loss in the fiscal year ended June 30, but top executives say they expect the system’s performance to improve.

Chicago-based CommonSpirit was formed through the Feb. 1 merger of San Francisco-based Dignity Health and Englewood, Colo.-based Catholic Health Initiatives. Since the merger occurred less than a year ago, financial and operating results were presented on a pro forma basis, using accounting records of CHI and Dignity Health as if they had been combined for the full fiscal 2019.

CommonSpirit reported operating revenues of $28.8 billion in fiscal 2019, down from $29.2 billion in the year prior. The health system said the year-over-year decline in revenue was largely attributable to California provider-fee program income recognized in fiscal 2018. Last year’s results also included income from the operations of U.S. HealthWorks and the gain on its sale.

After factoring in a year-over-year increase in operating expenses, CommonSpirit posted an operating loss of $582 million in fiscal 2019. That’s compared to operating income of $244 million a year earlier. The system’s nonoperating income dropped from $966 million in fiscal 2018 to $328 million.

CommonSpirit CFO Daniel Morissette told Becker’s Hospital Review the results were expected given the scope and complexity of the merger.

“We’re simply not where we need to be in terms of performance,” he said. “The whole organization is motivated and is aware of the work that needs to be done to improve these results.”

Over the past eight months, CommonSpirit has centralized key functions, such as IT and contracting, and established 11 geographic divisions across 21 states. It has also begun to scale successful service lines and executed a $6.5 billion debt restructuring, which drew demand from investors and support from financial analysts.

Looking ahead, Mr. Morissette said a strong operating model and a systemwide performance plan will help CommonSpirit achieve an 8 percent EBIDA margin within the next four years. The plan will also help the system build healthier communities, which is the real purpose behind the merger, he said.

CommonSpirit’s CEOs Kevin E. Lofton and Lloyd H. Dean reiterated those goals.

“CommonSpirit has made huge strides toward creating a bold new health organization that will deliver care for many years to come and improve the health of communities across the country,” Mr. Dean said in an earnings release. “We know this is not an easy task and that we face challenges in the near term, which is why we are investing in a strong, disciplined business model that will help the organization evolve to meet the changing health care needs of our communities.”

When the price of an essential medicine rose to an unacceptable level, there was only one thing for pharmacist Marleen Kemper to do – start making it herself.

When Marleen Kemper was a child, she watched two of her primary-school classmates get ill. One had a brain tumour, and the other contracted an infection in his gut. Both of them died. Kemper was around ten at the time, and knew that she didn’t want to see another friend perish. She told her parents she wanted to do something that would prevent others dying. She wanted to be a doctor.

But training is hypercompetitive in the Netherlands, where Kemper was growing up. She didn’t quite have the grades. She liked chemistry, so chose a career in pharmacy instead. She studied for six years, and did a residency for another four. Today, she’s a highly respected hospital pharmacist based at Amsterdam UMC’s Academic Medical Center, a cavernous building crafted out of concrete on the south-east fringe of the Dutch capital.

To understand what happened next, you have to understand several things about Kemper. Two date back to her childhood. One was those early experiences of losing friends to illness, which ensured she’ll do everything she can to make sick people better.

The second is that, though she’s highly accomplished, Kemper is self-admittedly hard-headed, and has always had a rebellious streak. She once dyed her hair black to stand out from the crowd. Sometimes she likes to shock people.

Which leads into the third, more recent trait: a steely determination to do right by her patients, whatever the cost. And the cost can be great. In 2017, when the price of a drug to treat a rare genetic disorder skyrocketed, Kemper wasn’t happy. The result was a dispute that’s still going on today and has spread beyond the four walls of the UMC hospital. It’s spread beyond the city of Amsterdam. And it’s even spread beyond the borders of the Netherlands.

Most of us never have to worry about chenodeoxycholic acid (CDCA), one of the two primary bile acids produced by our livers. But for a tiny fraction of us, a rare genetic trait means we end up short.

Having this gene variant prevents the body from creating sterol 27-hydroxylase, a liver enzyme. Without it, the liver won’t convert enough cholesterol into CDCA. The result is an overabundance of other bile acids and substances, which then get pumped out of the liver and through the body, causing untold damage.

The illness that results is called cerebrotendinous xanthomatosis, or CTX. It can cause cataracts, dementia, neurological problems and seizures, but it can be treated. Since the 1970s, the pharma industry has been able to produce CDCA, and so people who need it can supplement their shortage. The system worked well; the drug was relatively cheap for such a niche illness. A year’s treatment cost around €30,000 per patient.

Until suddenly it didn’t. In 2017, Leadiant Biosciences, which was supplying CDCA to these patients in the EU, raised the price of its version of the drug – known as CDCA Leadiant – to over €150,000 per patient per year.

The price increase soon had an effect. The Netherlands has an insurance-based health system, and in April 2018, Dutch insurers – who had been paying for 50 or so patients across the country to receive the drug – balked at the fivefold increase, refusing to pay. Patients unable to pay themselves would have gone without treatment, so Kemper – whose hospital was one of the treatment centres for CTX – stepped in. Amsterdam UMC would produce the medicine for these patients itself, at cost price.

She was upset, she admits. “Patients have a medical need. If those patients with CTX don’t get their medication, they get neurological implications, they get complications with their cholesterol and dementia, epilepsy… it is an essential medicine.”

Anyone wanting to manufacture a drug must get a marketing authorisation to do so. But Leadiant had become the only game in town, the owner of exclusive rights to manufacture CDCA commercially in the EU.

Yet there was a solution. Under EU rules, pharmacies can make (or ‘compound’) a prescribed drug on a small scale for their patients.

So Kemper began researching where she could find the ingredients to make CDCA. It was difficult: in the pursuit of better margins, vast numbers of manufacturing companies have closed their factories across the world and concentrated their efforts in China, where the costs of producing pharmaceutical ingredients are lower. Just one European company manufactures the ingredients to EU standards.

Kemper approached them, and they declined to supply her the raw material. In the end, she found a Chinese manufacturer instead. She went to the hospital’s executive board and gained approval to manufacture the drug. It cost the pharmacy €28,000 per patient per year – pretty much exactly the same as the price of the drug beforehand.

CDCA wasn’t initially used to treat CTX. Originally it was developed to treat gallstones. This main use of the drug – which from the mid-1970s had been sold in the Netherlands as Chenofalk – became outmoded when the standard procedure to deal with troublesome gallstones became to just cut out the gallbladder entirely.

At the turn of the millennium, Dutch doctors started using Chenofalk off-label to treat CTX – a practice that carried on for several years. At this time, in the mid-2000s, a year’s supply of the drug cost less than €500.

But in 2008, Leadiant acquired the rights to Chenofalk. Then, nine days before Christmas 2014, it succeeded in getting its version of CDCA classified as an “orphan medicine” for treating CTX. That classification gave Leadiant the exclusive right to manufacture its CDCA drug commercially in Europe for the next ten years. Leadiant then took Chenofalk off the market in 2015.

Introduced by EU regulation in the year 2000, orphan drug classification is given to drugs that treat serious illnesses that affect fewer than five in every 10,000 people in the EU. Its purpose is to help companies recoup the costs of developing treatments that would otherwise be unlikely to generate a profit. Without it, the pharma industry wouldn’t be incentivised to seek new drugs for the rarest diseases.

But in this case, CDCA was already known as a CTX treatment, with Chenofalk having been used off-label to treat it for years. Kemper believes that Leadiant is getting the financial benefits of orphan designation, but for a drug that had gone through development and been released to market long ago. “There were publications already in the 1980s,” she says. “There’s no patents, nothing. It’s really bizarre.”

Kemper isn’t the only one concerned about the price rise and CDCA’s orphan drug status. In September 2018, a lobby group, the Dutch Pharmaceutical Accountability Foundation, asked the Dutch competition authority to investigate the price increase. And this spring Test Achats, a nonprofit consumer-protection organisation in neighbouring Belgium, lodged a complaint against Leadiant with the Belgian Competition Authority.

“We noticed that in 2005, the price for the treatment of a patient in one year was around €500. Now it’s more than €150,000,” explains Laura Marcus, legal counsel to Test Achats. “It’s bad for the sick person but also for the Belgian health system, which is paying most of the [cost of the] treatment.”

When a drug company raises the price of its treatment, and a hospital pharmacy decides not to accept the increase but instead endeavours to compound its own version, undercutting the drug company’s price, things tend to get interesting.

In June 2018, Kemper received a phone call from the Dutch health inspectorate. It had received a letter of concern – who it came from, Amsterdam UMC doesn’t know, though the health inspectorate has said it was acting in response to an enforcement request from Leadiant – with a long list of things for the investigators to check.

Kemper took the news in her stride. She had expected a rocky road. “As a pharmacist, I am a professional and I know what I’m doing, and we have standards for compounding,” she explains. So she wasn’t worried when a team of four inspectorate monitors turned up at the door of her pharmacy in Amsterdam that summer. Two were there to take samples of the raw materials she was using to compound CDCA, and to ensure that all the correct processes were being followed. They rifled through the reams of paperwork and procedures that Kemper had spent hours developing for her staff to follow, while the other two inspectors combed through coverage of the case to ensure that Kemper and her team weren’t advertising their work, which isn’t allowed for medicines that haven’t been given market authorisation.

The lab checked out: its processes were up to standard, and the paperwork was all in order. But in July Kemper got a phone call that floored her: the inspectorate’s analysis of the raw materials her pharmacy was using to compound the CDCA had discovered that they weren’t up to snuff. Two components found in it were above allowed limits.

“As a professional you think: what did I miss? It was very emotional, a bit heavy,” she says. With the board of directors at the hospital, Kemper decided to immediately withdraw the product from patients; the health insurers said they’d step in and cover putting the patients back on the Leadiant version of the drug.

Kemper personally called the 50 or so patients she was providing with the drug. “The first one was hard,” she admits. “I expected they’d be angry or something like that. But no, no one [was]. The patients said: ‘Well, please go on with this job.’”

The Dutch inspectorate has said that Kemper can resume compounding CDCA provided she can find a raw material that doesn’t contain impurities – something Kemper is keeping tight-lipped about.

So, if she can get the materials she needs, Kemper is hopeful to be able to continue compounding CDCA in the future.

But for now, it’s back to square one – paying the full price for CDCA Leadiant.

These events have had wider consequences. What was initially a dispute inside the Netherlands has bled across borders, with Belgian patients with CTX now being affected.

It started with a conversation between the Dutch and Belgian health ministers shortly after Kemper’s production of CDCA was halted, says Thomas De Rijdt, head of pharmacy at University Hospitals Leuven. The Dutch minister wanted to know from his Belgian counterpart why Belgian hospitals were able to make the same drug without any issues.

“For Belgium, we have about ten patients,” De Rijdt says. “So ten patients are helped with the preparations from our hospital and the University Hospital in Antwerp.”

These hospitals had been compounding CDCA capsules for CTX patients for years. Leuven had sourced raw materials that had been tested and approved by a laboratory accredited by the Belgian government. But when the case in the Netherlands started entering conversation at diplomats’ dinners, the Belgian government wanted to double-check that its raw materials were OK.

It ran a second battery of tests – with a different accredited laboratory – which came back with a problem. A single impurity was found. The government ordered a quarantine of the raw material and recalled all the CDCA it had made.

“The patients had to return all their medication,” says De Rijdt. Recalling every capsule of the drug from Belgium, and freezing the work of the only two suppliers in the country, meant that people with CTX were suddenly left without any medicine.

“If you know the disease, you know you can deteriorate very quickly,” says De Rijdt. This was a problem. So, he says, the hospital pharmacists, the National Institute for Health and Disability Insurance, the health minister and the pharmaceutical inspectorate hit upon a solution. For a year, the Belgian government would reimburse the costs of Leadiant’s drug, allowing those patients to still be treated (normally the government only reimburses a portion of a person’s health costs, with the rest being picked up by the patient or insurance). Over the course of that year, the relevant authorities would then work together to adapt the requirements a raw material must comply with – to allow versions of drugs with minor impurities, providing they pose no threat to the patient.

“We have bought time to find a solution with the compounding, because we think by compounding we can save healthcare a lot of money for the same quality of therapy,” says De Rijdt. He hopes to have a solution by the end of 2019.

But in early September, things took another turn. Wouter Beke, the Belgian consumer affairs minister, used his price-regulation powers to bring down the price of CDCA Leadiant to just over €3,600 a month – roughly a quarter of the amount Leadiant was charging. If the drug becomes more cheaply available in Belgium, says De Rijdt, then it could end up being exported and available at a lower price elsewhere.

But exactly how this will pan out remains unclear. In the meantime, Beke has urged the Belgian Competition Authority to prioritise investigating Leadiant, following the complaint lodged by Test Achats.

Debate over what constitutes a fair price for drugs isn’t anything new. Nor is it limited to Europe.

Because of his willingness to play the bad guy in the press (and an odd moment when he bought a Wu-Tang Clan record), Martin Shkreli has attracted more criticism on drug pricing than perhaps anyone else. In 2015, Turing Pharmaceuticals, of which Shkreli was CEO, raised the price of its recently acquired antimalarial drug Daraprim, also used to treat AIDS-related illnesses. A pill went from $13.50 to $750 overnight – a 55-fold increase.

Shkreli’s capitalist tendencies were criticised by almost everyone. This was unlike the situation with CDCA Leadiant – there was no argument that this increase was to cover Daraprim’s development costs – and Shkreli himself was unrepentant: “If there was a company that was selling an Aston Martin at the price of a bicycle, and we buy that company and we ask to charge Toyota prices, I don’t think that that should be a crime,” he told reporters.

But the Daraprim situation was just the highest-profile example of a contest that is going on constantly between big pharmaceutical companies seeking to profit from drugs and medical staff on the frontline who worry that such profit-seeking does damage to patients needing treatment. (For what it’s worth, a competitor to Turing Pharmaceuticals announced soon after that it would produce a compound drug containing the same active ingredient in Daraprim – pyrimethamine – for $1 a pill, rather than the $750 Shkreli wanted to charge.)

One front in this battle has recently opened up in the US. In May, more than 40 states filed an antitrust lawsuit against some of the world’s biggest manufacturers of generic drugs, alleging they that have colluded to fix the price of more than a hundred medicines over a number of years. When prices should go down after a drug’s market exclusivity ended, the antitrust lawsuit claims that many prices have instead shot up – in some cases by more than 1,000 per cent.

And back in Europe, the consumer organisation Euroconsumers – of which Test Achats is part – is investigating the prices of other drugs beyond CDCA. “We’ve noticed a few problems with a few other drugs,” says Laura Marcus of Test Achats. “It’s often about drugs that are able to cure or deal with rare diseases. For sure, it’s not only CDCA.”

No one doubts that developing drugs costs money. A 2016 paper in the Journal of Health Economics estimated that the average cost of developing a prescription drug to the point of reaching the market is nearly $2.6 billion.

But the lack of hard, openly available statistics on the cost of drug development is something that many people, including Marcus and Marleen Kemper, want to change. “In most of the cases, society is willing to pay some price,” says Kemper, “but now the discussion is: what is an acceptable price?”

Marcus acknowledges that Leadiant has to cover its costs, but she thinks that cannot explain the rise of CDCA to over €150,000 – “the profit cannot be that high”. When I ask her how much profit she thought Leadiant was making from the drug, she admits she doesn’t know. “Of course we don’t have access to those numbers,” she says. “That’s what the Belgian Competition Authority is opening an inquiry for – to know more about the figures and the costs the company has to bear.” However, when the price for CDCA has surged from €500 to over €150,000, “nothing justifies it, because there was no new research, no new nothing,” she says.

Leadiant rejects this. Although CDCA had been authorised in the past, the company says that “the active pharmaceutical ingredient as well as the manufacturing of the finished product needed to be upgraded” to make sure that its version was compliant with current EU standards. These, Leadiant says, are more extensive and significantly more strict today than they were when earlier CDCA drugs were developed.

Leadiant says that its CDCA “is not a ‘copy’ of an old product”. The very fact that it gained orphan drug status proves this, it argues. The company also says that “there was no robust evidence that CDCA was effective in CTX until Leadiant produced the data”. Demonstrating this, it says, required “entirely new studies, creating new data sets” – which make up “the largest ever collection of clinical data for CTX”.

“CDCA Leadiant has been developed and brought to market at substantial cost,” the company says. “Our pricing is justified by our costs and investments.”

But the problem is not just that Leadiant’s drug is so expensive: potential alteratives have disappeared. Willemijn van der Wel, a lawyer working at European law firm AKD, has written about Leadiant’s connection to competitors who previously produced CDCA. After buying the marketing authorisations for other products that contained CDCA, he says, “Leadiant began to withdraw these alternative CDCA products from the market, until only one CDCA medicinal product remained”. Marcus has also queried what has happened to these products that might have been competitors to Leadiant’s. But, she says, it’s not clear what is behind their CDCA monopoly.

Leadiant, though, says that it’s willing to negotiate a lower price for its drug with the Dutch Ministry of Health and Dutch insurance companies. “The only reason an improvement has not been determined yet, is that the insurers have been uninterested or unwilling to enter into any substantive negotiations,” it claims. (Leadiant did not respond to follow-up questions asking for more details of the negotiations, or what level of price reduction the company was offering.) It also emphasises that it has not taken legal action against the UMC hospital for seeking to compound its own CDCA, but that it is “involved in a legal discussion with the Dutch Inspectorate about the interpretation of EU and Dutch medicines law”.

Regardless of the outcome of such discussions, something needs to be done. Having pharmacies self-compound medicines is not a sustainable model – it might reduce incentives for developing drugs for rare conditions.

It also, Leadiant argues, exposes patients to risk. Pharmacies do not have to have their compounding processes checked by the European Medicines Agency or the national regulator. “There is no product control by any independent regulatory authority before or after compounding.”

When it comes to market authorisation and orphan drugs, Leadiant says, “it should not be about small or large scale, but safe scale”.

Marleen Kemper’s husband warned her that taking on Leadiant would be more difficult than she first thought. “He said, ‘With this initiative, don’t be naive’,” she recalls. “The pharmaceutical industry is very powerful, so you really have to have back-up from the [hospital] board” – which she had. More than a year into her attempt to make her own version of the drug, she’s recognising just how deeply dug in both sides are to their positions.

She’s at pains to point out that she’s not against the pharma industry. “What people forget is that the pharmaceutical industry is responsible for a lot of innovation.” But if drug pricing means that patients potentially get left behind? “Then I’m getting angry,” she says.

But righteous anger alone can’t sustain someone over a months-long case involving lawyers and regulators, not least when they’re also raising a family, running part of a pharmacy that’s actively studying hundreds of drugs, and doing their job keeping patients supplied with medicine. At times Kemper has felt frustrated and worn down by the effort of taking on the price rise – but she vows to continue.

“I’ve said that sometimes I’ve thought, well, I’ll stop and quit doing it because it’s too much work, too emotionally draining. But due to the support, I think we’ll go on. I’m patient,” she says. “It has to be solved, for the patients.”

Kemper’s determined that she’s going to provide affordable care for her patients by following the letter of the law. “I’m using the rules,” she says. “I’m not cheating.” Leadiant, she accepts, has used the rules and followed them to serve its own purposes. So she will too.

“I’m allowed to make medication for patients. They don’t like it? So what. I’m following the rules.”

https://www.healthleadersmedia.com/clinical-care/why-hospitals-are-getting-housing-business

One patient at Denver Health, the city’s largest safety net hospital, occupied a bed for more than four years—a hospital record of 1,558 days.

Another admitted for a hard-to-treat bacterial infection needed eight weeks of at-home IV antibiotics, but had no home.

A third, with dementia, came to the hospital after being released from the Denver County Jail. His family refused to take him back.

In the first half of this year alone, the hospital treated more than 100 long-term patients. All had a medical issue that led to their initial hospitalization. But none of the patients had a medical reason for remaining in the hospital for most of their stay.

Legally and morally, hospitals cannot discharge patients if they have no safe place to go. So patients who are homeless, frail or live alone, or have unstable housing, can occupy hospital beds for weeks or months—long after their acute medical problem is resolved. For hospitals, it means losing money because a patient lingering in a bed without medical problems doesn’t generate much, if any, income. Meanwhile, acutely ill patients may wait days in the ER to be moved to a floor because a hospital’s beds are full.

“Those people are, for lack of a better term, stranded in our hospital,” said Dr. Sarah Stella, a Denver Health physician.

To address the problem, hospitals from Baltimore to St. Louis to Sacramento, Calif., are exploring ways to help patients find a home. With recent federal policy changes that encourage hospitals to allocate charity dollars for housing, many hospitals realize it’s cheaper to provide a month of housing than to keep patients for a single night.

Hospital executives find the calculus works even if they have to build affordable housing units themselves. It’s why Denver Health is partnering with the Denver Housing Authority to repurpose a mothballed building on the hospital campus into affordable senior housing, including about 15 apartments designated to help homeless patients transition out of the hospital.

“This is an experiment of sorts,” said Peg Burnette, the hospital’s chief financial officer. “We might be able to help better their lives, as well as help the financials of the hospital and help free up capacity for the patients that need to come to see us for acute care.”

Denver Health once used the shuttered 10-story building for office space but opted to sell it to the housing authority and grant a 99-year lease on the land for a minimal fee.

“It really lowers the construction costs for us,” said Ismael Guerrero, Denver Housing Authority’s executive director. “It was a great opportunity to build additional housing in a location that’s obviously close to the hospital, close to public transit, near the city center.”

Once the renovation is complete in late 2021, the housing group will hire a coordinator to assist tenants with housing-related issues, including helping those in the transitional units find permanent housing. The hospital will provide a case manager to help with their physical and behavioral health needs, preparing them for life on their own. Denver Health expects most patients will be able to move on from the transitional units within 90 days.

The hospital will pay for the housing portion itself. That will still be far cheaper than what the hospital currently spends.

It costs Denver Health $2,700 a night to keep someone in the hospital. Patients who are prime candidates for the transitional units stay on average 73 days, for a total cost to the hospital of nearly $200,000. The hospital estimates it would cost a fraction of that, about $10,000, to house a patient for a year instead.

“The hospital really is like the most expensive form of housing,” Stella said.

A recent report from the Urban Institute found that while most hospital officials are well aware of how poor housing affects a patient’s recovery, they were stymied about how to address the issue.

“It’s on the radar of almost all hospitals,” said Kathryn Reynolds, who co-authored the report. “But it seemed like actually making investments in housing, providing some type of financing or an investment in land or something that has a good amount of value seems to be less widespread.”

The report found housing investment has been more likely among hospitals with their own health plans or other types of arrangements in which they were receiving a fixed amount of money to care for a group of patients. Getting patients into housing could lower their costs and increase their operating margins. Others, particularly religiously affiliated and children’s hospitals, sought housing solutions as part of their charitable mission.

Reynolds said the trend is due in part to the Affordable Care Act, which requires hospitals to perform a community needs assessment to help guide their charitable efforts. That prompted more hospitals to consider the social needs of their patients and pushed housing concerns up the list. Additionally, the Internal Revenue Service clarified in 2015 that hospitals could claim housing investments as charitable spending required under their tax-free status. And provisions included in the 2017 tax cut bill provided significant tax savings for investors in newly designated opportunity zones, increasing their interest in affordable housing projects.

Some hospitals, she said, may use their cash reserves to invest in housing projects that generate a lower return than other investment options because it furthers their mission, not just their profits.

In other cases, hospital systems play a facilitator role—using their access to cheap credit or serving as an anchor tenant in a larger development—to help get a project off the ground.

“Housing is not their business,” Guerrero said. “It’s not an easy space to get into if you don’t have the experience, if you don’t have a real estate development team in-house to understand how to put these deals together.”

In the southwestern corner of Colorado, Centura Health’s Mercy Regional Medical Center has partnered with Housing Solutions for the Southwest to prioritize housing vouchers for frequent users of the emergency room.

Under a program funded by the Catholic Health Initiatives, Mercy hired a social worker and a case manager to review records of frequent emergency room patients. They quickly realized how big an issue housing was for those patients. Many had diabetes and depended on insulin—which needs refrigeration. Kidney failure was one of the most costly diagnoses for the hospital.

Once patients received housing vouchers and found stable housing, though, costs began to drop.

“We now knew where they were. We knew that they had a safe place to live,” said Elsa Inman, program coordinator at Mercy Regional. “We knew they would be more effective in managing their chronic conditions.”

The patients with stable housing were more likely to make it to their primary care and specialist appointments, more likely to stay on top of medications and keep their chronic conditions in check.

The combination of intensive case management and patient engagement helped to halve ER visits for the first 146 patients in the program, saving nearly $495,000 in Medicaid spending in less than three years.

“Hospitals are businesses and nonprofits are businesses,” said Brigid Korce, program development director for Housing Solutions. “They are bottom-line, dollars-and-cents people.”

Inman acknowledged that the hospital might have missed out on some revenue by reducing ER use by these patients. Hospitals are still largely paid by the number of patients they treat and the number of services they provide.

But most of those patients were covered by Medicaid, so reimbursements were low anyway. And the move freed up more ER beds for patients with more critical needs.

“We want to be prepared for life-threatening conditions,” Inman said. “If you’ve got most of your beds taken up by someone who can be receiving patient care outside in the community, then that’s the right thing to do.”

That was less of an issue for the inpatients at Denver Health. Because hospitals are generally paid a fixed amount for a given diagnosis, the longer a patient stays in the hospital, the more money the hospital loses.

“They’ve basically exhausted their benefit under any plan because they don’t meet medical necessity anymore,” Burnette said. “If they had a home, they would go home. But they don’t, so they stay in the hospital.”

California Attorney General Xavier Becerra alleges that Sutter Health used its pre-eminent market power to artificially inflate prices. Photo: Rich Pedroncelli/Associated Press

As a jury trial draws near in a major class-action lawsuit alleging anticompetitive practices by Northern California’s largest health system (PDF), a new CHCF study shows the correlation between the prices consumers pay and the extensive consolidation in the state’s health care markets. Importantly, the researchers estimated the independent effect of several types of industry consolidation in California — such as health insurers buying other insurers and hospitals buying physician practices. The report, prepared by UC Berkeley researchers, also examines potential policy responses.

While other states have initiated antitrust complaints against large hospital systems and medical groups in the past, the case against Sutter Health is unique in both the expansive nature of the alleged conduct and in the scale of the potential monetary damages. The complaint goes beyond claims of explicit anticompetitive contract terms and argues that by virtue of its very size and structure, the Northern California system imposed implicit or “de facto” terms that led to artificially inflated prices. Sutter Health vigorously denies the allegations.

The formation of large health systems like Sutter is neither new (PDF) nor unique to California (PDF). Several factors seem to be encouraging their growth, including payment models that place health care providers at financial risk for the cost of care, increased expectations from policymakers and payers around the continuum of patient needs that must be managed, and economies of scale for investments in information technology and administrative services. Some market participants also point to consolidation in other parts of the health care system, such as health plans and physician groups, as encouragement for their own mergers.

In general, economists study two major categories of market consolidation:

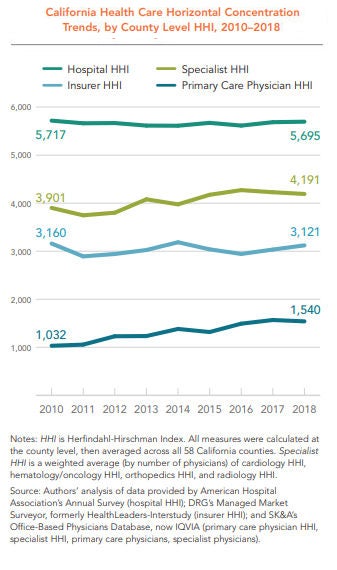

To measure market consolidation, the CHCF study relied on the Herfindahl-Hirschman Index (HHI), a metric used by the US Department of Justice and the Federal Trade Commission. An HHI of between 1,500 and 2,500 is considered moderately concentrated, and 2,500 or above is considered highly concentrated. According to this measure, horizontal concentration is high in California among hospitals, insurance companies, and specialist providers (and moderately high among primary care physicians), even though the level of concentration in all but primary care has remained relatively flat from 2010 to 2018.

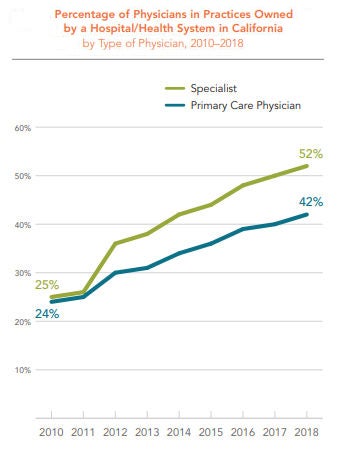

The percentage of physicians in practices owned by a hospital or health system increased dramatically in California between 2010 and 2018 — from 24% in 2010 to 42% in 2018. The percentage of specialists in practices owned by a hospital or health system rose even faster, from 25% in 2010 to 52% in 2018.

The percentage of physicians in practices owned by a hospital or health system increased dramatically in California between 2010 and 2018 — from 24% in 2010 to 42% in 2018. The percentage of specialists in practices owned by a hospital or health system rose even faster, from 25% in 2010 to 52% in 2018.

While this study defined and quantified the extent of consolidation across several industry segments in California, it is important to note that it did not define, quantify, or evaluate clinical integration within the state. Clinical integration has been defined by others in many ways, but generally involves arrangements for coordinating and delivering a wide range of medical services across multiple settings.

As the CHCF study authors point out, other analysis has shown that various types of clinical integration can lead to broader adoption of health information technology and evidence-based care management processes. Data from the Integrated Healthcare Association suggests that certain patient benefit designs and provider risk-sharing arrangements associated with clinical integration can lead to higher quality and lower costs.

Crucially, an emerging body of law (PDF) suggests that clinical integration does not require formal ownership and joint bargaining with payers.

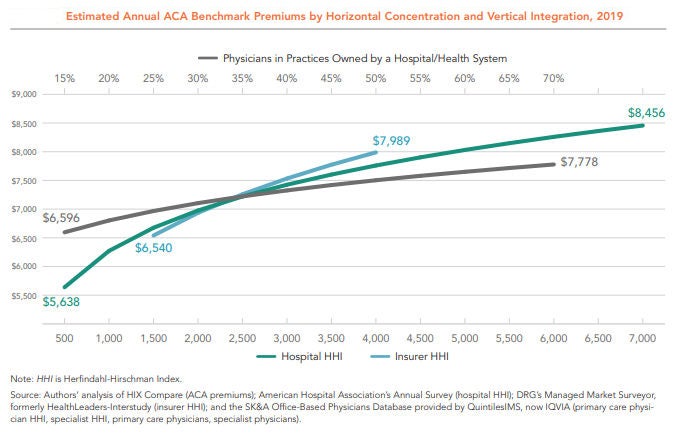

Among the six variables analyzed in the CHCF study, three showed a positive and statistically significant association with higher premiums: insurance company mergers, hospital mergers, and the percentage of primary care physicians in practices owned by hospitals and health systems. The remaining three variables studied — specialist provider mergers, primary care provider mergers, and the percentage of specialists in practices owned by a hospital and health system — were statistically insignificant.

The figure below shows the independent relationship between market concentration and premiums for these three variables. As the lines move left to right, concentration increases — that is, fewer individual insurers, hospitals, or providers occupy the market. The vertical axis shows the average premiums associated with each level of market concentration. In short, regardless of the industry structure represented by the other variables, insurer consolidation, hospital consolidation, and hospital-physician mergers each lead to higher premiums.

Unexplained Price Variation and Growth

Health insurance premiums rise when the underlying cost of medical care increases. California ranks as the 16th most expensive state on average in terms of the seven common services the researchers studied, after adjusting for wage differences across states. Among all states, California has the eighth-highest prices for normal childbirth, defined as vaginal delivery without complications. Childbirth is the most common type of hospital admission, and the relatively standardized procedure is comparable across states.

Even within California, prices vary widely and are growing rapidly. For example, the 2016 average wage-adjusted price for a vaginal delivery was twice as high in Rating Area 9 (which has Monterey as its largest county) as it was in Rating Area 19 (San Diego) — $22,751 versus $11,387. (See next figure.) Prices for the service are increasing rapidly across counties — rising anywhere from 29% in San Francisco from 2012 to 2016 to 40% in Orange County over the same period.

The authors of the CHCF report investigated the impact of various types of consolidation on the prices of individual medical services in California. For cesarean births without complications, a 10% rise in hospital HHI is associated with a 1.3% increase in price.

While the study shows significant associations between various types of market concentration and the prices consumers pay, policymakers should carefully consider implementing steps that restrain the inflationary impact of consolidation while allowing the benefits of clinical integration to proliferate. To that end, the authors of the CHCF report offered a series of recommendations, which include:

Enforce antitrust laws. Federal and state governments should scrutinize proposed mergers and acquisitions to evaluate whether the net result is procompetitive or anticompetitive.

Restrict anticompetitive behaviors. Anticompetitive behaviors, such as all-or-nothing and anti-incentive contract terms, should be addressed through legislation or the courts in markets where providers are highly concentrated.

Revise anticompetitive reimbursement incentives. Reimbursement policies that reduce competition, such as Medicare rules that implicitly reward hospital-owned physician groups, should be adjusted.

Reduce barriers to market entry. Policies that restrict who can participate in the health care market, such as laws prohibiting nurse practitioners from practicing independently from a physician, should be changed when markets are concentrated.

Regulate provider and insurer rates. If antitrust enforcement is not successful and significant barriers to market entry exist — including those in small markets unable to support a competitive number of hospitals and specialists — regulating provider and insurer rates should be considered.

Encouraging meaningful competition in health care markets is an exceedingly difficult task for policymakers. It is no easier to promote the benefits of clinical integration while restraining the inflationary aspects of economic consolidation through public policy. Despite these challenges, the rapid rise in health care premiums and prices in the state require a fresh look at the consequences of widespread horizontal and vertical consolidation in California.

https://www.healthleadersmedia.com/finance/top-5-differences-between-nfps-and-profit-hospitals

All hospitals serve patients, employ physicians and nurses, and operate in tightly regulated frameworks for clinical services. For-profit hospitals add a unique element to the mix: generating return for investors.

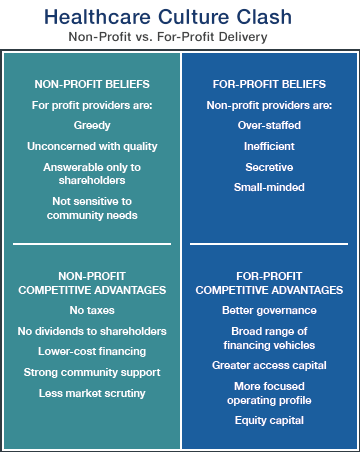

This additional ingredient gives the organizational culture at for-profits a subtly but significantly different flavor than the atmosphere at their nonprofit counterparts, says Yvette Doran, chief operating officer at Saint Thomas Medical Partners in Nashville, TN.

“When I think of the differences, culture is at the top of my list. The culture at for-profits is business-driven. The culture at nonprofits is service-driven,” she says.

Doran says the differences between for-profits and nonprofits reflect cultural nuances rather than cultural divides. “Good hospitals need both. Without the business aspects on one hand, and the service aspects on the other, you can’t function well.”

There are five primary differences between for-profit and nonprofit hospitals.

The most obvious difference between nonprofit and for-profit hospitals is tax status, and it has a major impact financially on hospitals and the communities they serve.

Hospital payment of local and state taxes is a significant benefit for municipal and state governments, says Gary D. Willis, CPA, a former for-profit health system CFO who currently serves as CFO at Amedisys Inc., a home health, hospice, and personal care company in Baton Rouge, LA. The taxes that for-profit hospitals pay support “local schools, development of roads, recruitment of business and industry, and other needed services,” he says.

The financial burden of paying taxes influences corporate culture—emphasizing cost consciousness and operational discipline, says Andrew Slusser, senior vice president at Brentwood, TN-based RCCH Healthcare Partners.

“For-profit hospitals generally have to be more cost-efficient because of the financial hurdles they have to clear: sales taxes, property taxes, all the taxes nonprofits don’t have to worry about,” he says.

“One of the initiatives we’ve had success with—in both new and existing hospitals—is to conduct an Operations Assessment Team survey. It’s in essence a deep dive into all operational costs to see where efficiencies may have been missed before. We often discover we’re able to eliminate duplicative costs, stop doing work that’s no longer adding value, or in some cases actually do more with less,” Slusser says.

With positive financial performance among the primary goals of shareholders and the top executive leadership, operational discipline is one of the distinguishing characteristics of for-profit hospitals, says Neville Zar, senior vice president of revenue operations at Boston-based Steward Health Care System, a for-profit that includes 3,500 physicians and 18 hospital campuses in four states.

“At Steward, we believe we’ve done a good job establishing operational discipline. It means accountability. It means predictability. It means responsibility. It’s like hygiene. You wake up, brush your teeth, and this is part of what you do every day.”

A revenue-cycle dashboard report is circulated at Steward every Monday morning at 7 a.m., including point-of-service cash collections, patient coverage eligibility for government programs such as Medicaid, and productivity metrics, he says. “There’s predictability with that.”

A high level of accountability fuels operational discipline at Steward and other for-profits, Zar says.

There is no ignoring the financial numbers at Steward, which installed wide-screen TVs in most business offices four years ago to post financial performance information in real-time. “There are updates every 15 minutes. You can’t hide in your cube,” he says. “There was a 15% to 20% improvement in efficiency after those TVs went up.”

Accountability for financial performance flows from the top of for-profit health systems and hospitals, says Dick Escue, senior vice president and chief information officer at the Hawaii Medical Service Association in Honolulu.

Escue worked for many years at a rehabilitation services organization that for-profit Kindred Healthcare of Louisville, Kentucky, acquired in 2011. “We were a publicly traded company. At a high level, quarterly, our CEO and CFO were going to New York to report to analysts. You never want to go there and disappoint. … You’re not going to keep your job as the CEO or CFO of a publicly traded company if you produce results that disappoint.”

Finance team members at for-profits must be willing to push themselves to meet performance goals, Zar says.

“Steward is a very driven organization. It’s not 9-to-5 hours. Everybody in healthcare works hard, but we work really hard. We’re driven by each quarter, by each month. People will work the weekend at the end of the month or the end of the quarter to put in the extra hours to make sure we meet our targets. There’s a lot of focus on the financial results, from the senior executives to the worker bees. We’re not ashamed of it.”

“Cash blitzes” are one method Steward’s revenue cycle team uses to boost revenue when financial performance slips, he says. Based on information gathered during team meetings at the hospital level, the revenue cycle staff focuses a cash blitz on efforts that have a high likelihood of generating cash collections, including tackling high-balance accounts and addressing payment delays linked to claims processing such as clinical documentation queries from payers.

For-profit hospitals routinely utilize monetary incentives in the compensation packages of the C-Suite leadership, says Brian B. Sanderson, managing principal of healthcare services at Oak Brook, IL–based Crowe Horwath LLP.

“The compensation structures in the for-profits tend to be much more incentive-based than compensation at not-for-profits,” he says. “Senior executive compensation is tied to similar elements as found in other for-profit environments, including stock price and margin on operations.”

In contrast to offering generous incentives that reward robust financial performance, for-profits do not hesitate to cut costs in lean times, Escue says.

“The rigor around spending, whether it’s capital spending, operating spending, or payroll, is more intense at for-profits. The things that got cut when I worked in the back office of a for-profit were overhead. There was constant pressure to reduce overhead,” he says. “Contractors and consultants are let go, at least temporarily. Hiring is frozen, with budgeted openings going unfilled. Any other budgeted, but not committed, spending is frozen.”

The for-profit hospital sector is highly concentrated.

There are 4,862 community hospitals in the country, according to the American Hospital Association. Nongovernmental not-for-profit hospitals account for the largest number of facilities at 2,845. There are 1,034 for-profit hospitals, and 983 state and local government hospitals.

In 2016, the country’s for-profit hospital trade association, the Washington, DC–based Federation of American Hospitals, represented a dozen health systems that owned about 635 hospitals. Four of the FAH health systems accounted for about 520 hospitals: Franklin, TN-based Community Hospital Systems (CHS); Nashville-based Hospital Corporation of America; Brentwood, TN–based LifePoint Health; and Dallas-based Tenet Healthcare Corporation.

Scale generates several operational benefits at for-profit hospitals.

“Scale is critically important,” says Julie Soekoro, CFO at Grandview Medical Center, a CHS-owned, 372-bed hospital in Birmingham, Alabama. “What we benefit from at Grandview is access to resources and expertise. I really don’t use consultants at Grandview because we have corporate expertise for challenges like ICD-10 coding. That is a tremendous benefit.”

Grandview also benefits from the best practices that have been shared and standardized across the 146 CHS hospitals. “Best practices can have a direct impact on value,” Soekoro says. “The infrastructure is there. For-profits are well-positioned for the consolidated healthcare market of the future… You can add a lot of individual hospitals without having to add expertise at the corporate office.”

The High Reliability and Safety program at CHS is an example of how standardizing best practices across the health system’s hospitals has generated significant performance gains, she says.

“A few years ago, CHS embarked on a journey to institute a culture of high reliability at the hospitals. The hospitals and affiliated organizations have worked to establish safety as a ‘core value.’ At Grandview, we have hard-wired a number of initiatives, including daily safety huddles and multiple evidence-based, best-practice error prevention methods.”

Scale also plays a crucial role in one of the most significant advantages of for-profit hospitals relative to their nonprofit counterparts: access to capital.

Ready access to capital gives for-profits the ability to move faster than their nonprofit counterparts, Sanderson says. “They’re finding that their access to capital is a linchpin for them. … When a for-profit has better access to capital, it can make decisions rapidly and make investments rapidly. Many not-for-profits don’t have that luxury.”

There are valuable lessons for nonprofits to draw from the for-profit business model as the healthcare industry shifts from volume to value.

When healthcare providers negotiate managed care contracts, for-profits have a bargaining advantage over nonprofits, Doran says. “In managed care contracts, for profits look for leverage and nonprofits look for partnership opportunities. The appetite for aggressive negotiations is much more palatable among for-profits.”

:format(webp)/cdn.vox-cdn.com/uploads/chorus_image/image/65358995/843175548.jpg.0.jpg)

Is the rapidly rising cost of employer-sponsored health insurance sustainable?

Half of all Americans get their health insurance through work. Trouble is, doing so is becoming less and less affordable — especially for already low-wage workers.

In 2019, the Kaiser Family Foundation Employer Health Benefits Survey — an annual account of roughly 2,000 small and large businesses’ employer-sponsored insurance — found the average annual premium to cover a family through work was a whopping $20,576, and $7,188 for an individual. Employers cover most of that, but families still contributed an average of $6,015 in premiums, and single Americans covered about $1,242 of the annual cost.

The kicker? Over the past 10 years, the cost of the portion of employer-sponsored health insurance premiums that falls on American families has increased by 71 percent. Overall, premiums have gone up 54 percent since 2009. That’s faster than the rate of inflation and faster than the average wage growth.

Nearly half of all Americans get their health insurance through work, a system that covers roughly 153 million people. And for lower-wage workers it’s a system that is increasingly unaffordable.

Workers at companies with a significant number of low-wage employees (which the Kaiser Family survey quantifies as a company in which at least 35 percent of employees are making an annual salary of $25,000 or less) have lower premiums than those who work at companies with fewer low-wage workers, probably because their plans cover less. But at the same time, workers at firms with a significant number of low-wage employees are faced with high-deductible plans, and also pay a larger share of the premium cost than workers at companies with fewer lower-wage employees.

According to the survey, workers at lower-wage companies pay an average of $7,000 a year family plan — $1,000 more than employees at companies with higher salaried workers.

“When workers making $25,000 a year have to shell out $7,000 a year just for their share of family premiums,” Drew Altman, the president of Kaiser Family Foundation, said in a statement, that’s where cost becomes prohibitive. Such employees are putting almost 30 percent of their salaries toward premiums.

The takeaway is clear. Health care is getting more and more expensive, and families and employers are having to bear more of the cost, which research has shown not only has an effect on how much workers are actually getting paid, but how many workers are hired.

As Sarah Kliff reported for Vox, there are a lot of studies spanning decades that show how a rapid rise in health insurance premiums has unfavorable outcomes for workers. This is in large part because employers think of compensation in totality; they lump together an employee’s salary, as well as their benefits as one total cost. So if covering a worker’s health insurance gets more and more expensive, employers see less room to give the worker a raise.

For example, a 2006 study from Katherine Baicker and Amitabh Chandra, both with the National Bureau of Economic Research, found that an overall 10 percent increase in health insurance premiums reduced wages by 2.3 percent and actually reduced the probability of becoming employed by 1.2 percent.

Results such as these, and the high premiums low-wage workers must pay, led the Kaiser survey’s authors to explicitly question the tenability of employer-sponsored insurance: “the national debate about expanding Medicare or creating public program options provides an opportunity to step back and evaluate how well employer-based coverage is doing in achieving national goals relating to costs and affordability,” the report reads.

The United States is unique in its reliance on employers to provide health insurance. And, as Democratic candidates for president continue to go in circles debating health care, employer-sponsored insurance is often the biggest sticking point.

Several candidates, like Sen. Bernie Sanders, who popularized a plan for Medicare-for-all, a single government-run program, and Sen. Elizabeth Warren, who supports Sanders’s plan, have called for getting rid of the employer-based system, and private insurance, all together.

But their critics always bring up the same talking point: that the people who like their health insurance plans through work, should be able to keep it. The Kaiser survey raises questions as to how affordable those plans really are, and, as Democrats debate ideas like Medicare-for-all, how sustainable the current trajectory is.

The debate over healthcare and how it should proceed has apparently come down to either keeping what we’ve got, going back to what we had, or Medicare for All. At least, that’s how things are being framed for a coming presidential election. At stake is the cost and delivery of 17.9% of the country’s entire gross domestic product—$3.5 trillion in 2017 and heading north from there.

There have been previous attempts, of course, to change healthcare, whether the addition of Medicare and Medicaid under Lyndon Johnson, Bill and Hillary Clinton’s unsuccessful attempt to reshape the healthcare system, the addition of prescription drug coverage to Medicare signed by George W. Bush, or the Affordable Care Act under Barack Obama.

As a country, we periodically seek a better approach to healthcare—this way, that way, but not straying far from where we were. Understandable, to a (small, these days) degree. There is no guarantee that a quick change won’t cause more problems than it solves. Some people like their coverage, it’s true. But a great many do not.

Importantly, the day is coming (if it’s not right here) that most people can’t afford reasonable care. Average annual premiums for employer-sponsored healthcare for a family have reached $20,576, according to a survey by the Kaiser Family Foundation. Of that, $6,015 are paid by the employee and $14,561 by the employer.

The problem of cost is immense, especially when overall healthcare in the U.S. ranks as mediocre at best (which doesn’t mean good care isn’t available, but more likely is an indication of how relatively few people obtain it).

But many who have a vested interest in the system as it exists, whether for political or financial gain, loudly exclaim that any sort of solution that involves government as an insurer—like Medicare, which many participants prize given much lower rates than typical market-based programs—becomes untenable. “Can you afford how much taxes will go up?” they say.

Some voices have pushed back and we need more, because the question is a loaded one. Government-sponsored insurance would reduce the need for and expense of private insurance.

At issue is an analytic approach often used in business: the total cost of ownership. When taking up a new technology or operational strategy, a smart company analyzes the full costs. Not just the obvious price tag, but all that accompanying costs. It’s the corporate equivalent of an informed car buyer, who, beyond sticker price, is interested in the likely costs of fuel and maintenance, how well the vehicle maintains price in the used or trade-in markets, reliability, and other factors that represent accompanying expenses.

Taxes under a Medicare for All approach would go up. But, at the same time, commercial premiums come down (even if, as with Medicare, many people buy supplemental insurance to expand coverage). There may lower out-of-pocket costs, as is true in many countries with some sort of national coverage.

There is also an argument for resulting higher worker pay. Companies no longer be paying that $14,561 could shift that savings, or at least some, into additional wages or salary. Not increasing pay would effectively be a tax cut, as benefits are part of compensation.

The thought behind healthcare reform like Medicare for All is that it should be possible for the U.S. to do better. To gain improved coverage across the board at lower per-capita prices, as the rest of the developed world has managed to do for decades. People with better care can live better lives, which—and I take this as an article of faith—eventually comes back to communities and the country.

Consideration of changes requires a full understanding of the costs and financial gains throughout the system. Taxes go up, premiums go down, maybe pay increases (should increase), and a sudden illness doesn’t cause automatic financial stress for an individual or a family. Whenever someone makes sweeping claims like “taxes will go up” without context, others should step up and note that it’s like complaining about investing in mass transit without acknowledging that using an automobile to make the same commute will be much more expensive and that one may mean you don’t need the other.

The health-care sector just closed out a third straight month in the red, its longest losing streak in three years.

A fourth monthly decline would be its worst stretch since 2011, and one trader says there could be more pain ahead.

“I view the whole sector as a wounded target right now,” said Boris Schlossberg of BK Asset Management on CNBC’s “Trading Nation” on Monday. “Health care, in my opinion, is the most bloated, the most bureaucratic, the most inefficient sector of the economy. At 20% of the GDP and at $20,000 premium per capita at this point, they pretty much have squeezed all the rentier profits out of the system that they can at this point.”

The sector also has a target on its back as the 2020 presidential election draws closer. The XLV health care ETF has fallen more than 3% in the past three months as Democratic presidential candidates such as Elizabeth Warren have pushed for a “Medicare For All” solution.

“Even if the Democrats do not win, there’s going to be tremendous amount of pressure to cut costs, control drug prices,” said Schlossberg. “Any way you slice it, basically the sector is a ‘sell the rally’ trade at this point. Any time you have a pop in the sector, it’s going to be a sell for quite a long time.”

Health-care stocks faced similar pressure in 2015 and 2016 as Democratic presidential candidate Hillary Clinton pledged health-care reform. At its worst, the XLV ETF plummeted 11% in the third quarter of 2015.

However, Miller Tabak equity strategist Matt Maley does not see that degree of decline this time.

“I don’t think it’ll be anywhere near as bad as it was four years ago because the setup is much, much different. In the 12 months leading into the summer before the election year the last time around, the XLV had outperformed the S&P by two times,” said Maley on “Trading Nation” on Monday. “This group had become very overbought, and very over-owned.”

This time around, Maley says the XLV ETF had performed in line with the S&P 500 before beginning its breakdown in April.

“I don’t think you’ll have that forced selling or at least that reweighting that you had going forward. So even though I think it’s a problem, it’s not as big a problem,” said Maley.

For only the second time this year, hospitals of all sizes experienced monthly profitability declines, primarily due to “softening volumes,” according to a Kaufman Hall report released Tuesday.

In the month of August, both overall hospital operating EBITDA margins and operating margins fell by 9.4% and 11.4% year-over-year, respectively.

Kaufman Hall compared the August stagnation to the challenges hospitals faced in June, specifically referencing the ineffective approaches to adjust expenses when patient volumes sputter.

Delving into geographic differences, Midwest hospitals continue to show more resiliency than other areas, according to the report.

Hospitals in the northeast and Mid-Atlantic regions witnessed the largest declines in August, a 15.8% year-over-year drop in operating EBITDA margin, while the Great Plains posted profitability of 16.7% above budget.

Despite a relatively promising year thus far where hospitals rebounded from market volatility in 2018, provider organizations hit the financial skids in August due to inconsistent volume metrics.

Most volume metrics took a hit, with discharges, adjusted discharges, emergency department visits, and operating room minutes falling by more than 1.2% each.

Meanwhile, adjusted patient days and average length of stay increased by more than 1.6% as well.

Additionally, expense metrics were mixed for most hospitals, as total expenses per adjusted discharge rose 4% year-over-year, while labor expenses for the same metric increased 2.4%.

Purchased service expenses per adjusted discharge rose 6.1% while non-labor expenses and supply expenses for the same metric rose more than 3.5%.

On the non-operating side, the U.S. labor market continued its strong performance in the face of global headwinds and fears about a potential recession in the coming months.

Kaufman Hall described August as “weak month” for investment assets, noting that investment portfolio returns for hospitals declined 0.46%, the first monthly decline since May.