Congress on Wednesday enters the eighth day of the federal shutdown with neither party giving an inch and the path to a resolution nowhere in sight.

But something will have to give if lawmakers hope to reopen the government in any timely fashion, and that movement will likely be the result of external forces exerting pressure on one party — or both of them — to break the deadlock.

That’s been the case in the protracted shutdowns of years past, when a number of outside factors — from economic sirens to public frustration — have combined to compel lawmakers to cede ground and carry their policy battles to another day.

Public sentiment

Among the most recycled quotes on Capitol Hill is attributed to Abraham Lincoln: “Public sentiment is everything.” The trouble, in these early stages of the shutdown fight, is that the verdict is still out on where that sentiment will land.

That uncertainty has led both parties to dig in while they await more concrete evidence of which side is bearing the brunt of the blame. But those polls are coming, and if history is any indication, they will be a potent factor in forcing at least one side to shift positions for the sake of ending the shutdown.

That was the case in 2013, when Republicans demanding a repeal of ObamaCare saw their approval ratings plummet — and dropped their campaign after 16 days without winning any concessions. A similar dynamic governed the shutdown of 2018 and 2019 — the longest in history — when Republicans agreed to reopen the government without securing the border wall money they’d insisted upon.

A recent CBS poll found that 39 percent of voters blame Trump and Republicans for the shutdown; 30 percent blame congressional Democrats; and 31 percent blame both parties equally.

A Harvard/Harris poll also showed that more respondents blame Republicans, 53 to 47 percent, but nearly two-thirds believe Democrats should accept the GOP’s stopgap funding bill without a fix for the expiring Affordable Care Act premium subsidies.

The ambiguity of those sentiments has heightened the partisan blame game — and has given both sides an incentive to hold the line until a clearer picture emerges.

Air traffic controller issues

It was nearly seven years ago that the 35-day shutdown ended after travel chaos and short-staffing of air traffic controllers brought immense strain on the aviation sector — and trouble is already starting up again.

An uptick of air traffic controllers calling in sick Monday forced numerous flight delays and cancellations, prompting concerns that a reprisal of what happened in 2019 could be starting up again.

“We should all be worried,” said Sen. Mike Rounds (R-S.D.), who was part of informal rank-and-file talks last week about a possible resolution.

Transportation Security Administration workers and air traffic controllers are all considered essential workers, with the Department of Transportation announcing more than 13,000 controllers are set to work without pay during this shutdown.

Those calling in sick prompted delays at numerous big airports, including Denver International Airport and Newark Liberty International Airport. The Hollywood Burbank Airport went without any air traffic controller on-site for nearly six hours Monday.

Just like the record-setting 2019 shutdown, Democrats are counting on this issue creating problems for Trump and Republicans. Sen. Chris Van Hollen (D-Md.) told reporters that he and other local officials are holding a press event at Baltimore/Washington International Thurgood Marshall Airport on Wednesday to highlight the rising issue.

“It had a direct impact on people’s abilities to get around the country,” Van Hollen said of the 2019 shutdown issue. “Donald Trump shut down the government in his first term, and he needs to end the shutdown he ended in the second term.”

Frozen paychecks

The central, defining factor of any shutdown is the scaling back of federal services and the siloing of hundreds of thousands of federal employees. Some of those workers are deemed “essential,” meaning they still have to come to work, while others are furloughed, meaning they’ll stay at home. But both groups share the unenviable position of not being paid until the government reopens.

That reality will hit home Oct. 10, when the first round of federal paychecks will fail to go out. The most immediate impact, of course, is on those workers and their families, who will have to find alternative ways to pay bills and make ends meet.

But the pain will also reverberate through the broader economy, as federal workers stay at home and avoid the types of routine daily purchases — lunches, cabs, haircuts — that can make local economies hum.

The numbers are enormous.

The White House Council of Economic Advisers has estimated that every week of the shutdown will reduce the nation’s gross domestic product by $15 billion.

“This is resulting in crippling economic losses right now,” Speaker Mike Johnson (R-La.) warned Tuesday. “A monthlong shutdown would mean not just 750,000 federal civilian employees furloughed right now, but an additional 43,000 more unemployed Americans across the economy, because that is the effect, the ripple effect, that it has in the private sector.”

In a typical shutdown, furloughed workers receive back pay for the days lost during the impasse, providing a delayed bump in economic activity. But even that customary practice is now in question in the face of a threat from Trump’s budget office to withhold back pay for certain workers. Others, Trump has said, will be fired altogether.

The combination is sure to exacerbate a volatile economy that’s already been roiled by declining consumer confidence, sinking job creation and Trump’s tariffs. Whichever party suffers the blame for the economic strain will come under the most pressure to cave in the shutdown fight.

Military paychecks

Pay for members of the military has been a constant talking point in past shutdowns, and that’s no different this go-around.

Military service members could miss their paychecks Oct. 15, a date front and center for lawmakers.

Johnson huddled with Senate Republicans on Tuesday during their weekly policy luncheon and told reporters afterward that he is considering having the House vote on a bill to pay troops.

“I’m certainly open to that. We’ve done it in the past. We want to make sure our troops are paid,” Johnson said, noting one GOP member has filed legislation aimed at doing that. “We’re looking forward to processing all of this as soon as we gather everybody back up.”

The Speaker added that the shutdown would need to end by Monday in order to process the paychecks by Oct. 15.

One problem for Johnson, though, is that the House is not slated to return until Monday at the earliest, and he has indicated that he will keep the chamber out of session until the shutdown is over.

Democrats indicated they are also worried about those impacts, but say Johnson has bigger fish to fry.

“I’m concerned about all the impacts of a shutdown. … There’s a lot of impacts of a shutdown,” Sen. Chris Murphy (D-Conn.) said. “How on earth does Mike Johnson say anything with a straight face right now when he won’t even bring his members here to vote on anything? How does he know what he can deliver if his members aren’t even here?”

“It’s not worth listening to anything the Speaker says until he tells his people to get back and show up for work.”

Health care factors

Democrats have made health care the lynchpin of their opposition to the Republicans’ short-term spending bill, demanding a permanent extension of enhanced Affordable Care Act (ACA) subsidies set to expire at the end of the year.

Citing that expiration date, GOP leaders have refused to negotiate on the issue as part of the current debate, saying there’s time to have that discussion after the government opens up.

“That’s a Dec. 31 issue,” Johnson told reporters Tuesday.

But there are several related factors that will surface long before Jan. 1, and they could put pressure on GOP leaders to reconsider their position in the coming weeks.

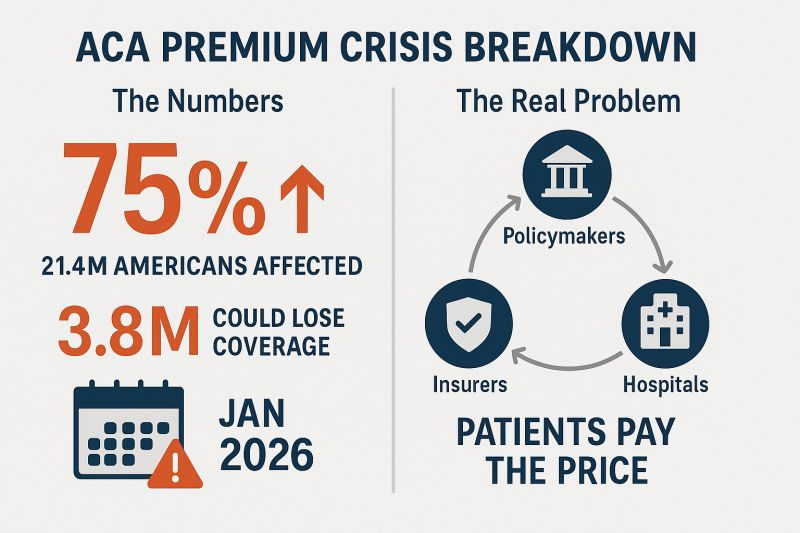

For one thing, private insurance companies that sponsor plans on the ObamaCare marketplace are already sending out rate notices to inform patients of next year’s costs. Those rates are crunched based on current law — not predictions about what Congress might do later — meaning they’re being calculated under the assumption that the enhanced subsidies, which were established during the COVID-19 pandemic, will expire Jan. 1.

That distinction is enormous: If Congress doesn’t act, the average out-of-pocket premium for patients enrolled in ObamaCare marketplace plans would jump by 75 percent, according to KFF. Those are the figures patients are already getting in the mail. And faced with drastically higher rates, many are likely to buy lesser coverage next year — or no coverage at all.

Adding to the time squeeze, the ACA’s open enrollment period begins Nov. 1, meaning patients will begin making their decisions long before GOP leaders say they’re ready to act.

“Insurers aren’t waiting around to set rates for next year,” Senate Minority Leader Chuck Schumer (D-N.Y.) warned this week. “They’re doing it right now — not three months from now.”