UC Davis Medical Center in Sacramento, Calif., has broken ground on a $3.74 billion expansion that includes a 14-story hospital tower and a five-story medical pavilion.

The new tower will add nearly 1 million square feet of space to the existing medical center. It will include new operating rooms, an imaging center, facilities for pharmacy and burn care units, and about 334 private patient rooms.

More than 250 of the rooms are being designed for greater flexibility in the event of a patient surge such as a pandemic, wildfire or other disaster. These will easily convert into intensive-care-unit rooms with air isolation to treat patients of any level of hospitalization.

“We are building into this new tower some of the lessons we learned from the recent pandemic. As an example, three out of four of the rooms in this new tower can be easily converted to fully functional ICUs if needed, tripling our ICU capacity,” UC Davis Health CEO David Lubarsky said in a July 22 news release.

The current, 646-bed hospital will have between 675 and 700 inpatient beds when the project is completed in 2030.

“This project further harnesses the advantages of UC Davis Medical Center being Sacramento’s No. 1 hospital and delivering nationally ranked care,” Mr. Lubarsky said. “UC Davis Health is Sacramento County’s second-largest employer, and we’re making sure we are bringing not only healthcare, but jobs and community wealth-building to our surrounding neighborhoods.”

The entities agreed to maintain services, provide capital investments and protect competition in the healthcare market.

California Attorney General Rob Bonta announced a settlement agreement this week reached by The Regents of the University of California and UCSF Health regarding their $100 million purchase of Dignity Health’s two San Francisco hospitals, St. Mary’s Medical Center (SMMC) and Saint Francis Memorial Hospital (SFMH).

Dignity Health is a nonprofit public benefit corporation that owns and operates SFMH, a 259-licensed-bed general acute care hospital, and SMMC, a 240-licensed-bed general acute care hospital. Both hospitals serve a diverse community, including a large number of elderly, unhoused and publicly insured patients who may rely on Medi-Cal, Medicare or charity care to access essential health services.

Under the settlement agreement approved by the San Francisco Superior Court, The Regents and UCSF Health commit to maintain services for the unhoused and Medi-Cal and Medicare beneficiaries, provide $430 million in capital investments, protect competition in the healthcare market and safeguard the affordability of and access to services for residents of San Francisco.

WHAT’S THE IMPACT

The Regents and UCSF Health agreed to a number of conditions over the next 10 years, including operating and maintaining SFMH and SMMC as licensed general acute care hospitals with the same types and levels of services, and associated staffing. They also agreed to continue participating in Medi-Cal and Medicare.

Also agreed upon was providing an annual amount of charity care at SFMH equal to or greater than $6.5 million and at SMMC equal to or greater than $3.5 million, with an annual increase of 2.4% at both hospitals.

The two entities agreed to provide an annual amount of community benefit spending for community healthcare needs at SFMH equal to or greater than $1.6 million and at SMMC equal to or greater than $10.7 million, to increase yearly by 2.4% at both hospitals.

UCSF Health and The Regents also pledged to invest at least $430 million, including at least $80 million for electronic medical record systems and related technologies, and at least $350 million in deferred maintenance and physical infrastructure improvements at both hospitals.

In addition to those agreements, they also agreed to a number of conditions over a seven-year period meant to maintain competition in the healthcare market, in part by maintaining contracts with the City and County of San Francisco for services at SFMH and SMMC unless terminated for cause.

The Regents and UCSF Health agreed to not condition medical staff privileges or contracts on the employment, contracting, affiliation, or appointment status of a physician with UCSF Health or any affiliate; not impose any requirement on any member of the hospitals’ medical staff, as a condition of either their medical staff membership or privileges that restricts them from contracting with providers other than UC Health; and negotiate all payer contracts for the hospitals separately and independently from payer contracts for UCSF Health, and maintain an information firewall between the two negotiating teams.

Finally, the two entities agreed to require, for five years, a price growth cap that limits the maximum that the hospitals may charge a payer from year to year upon renegotiation of contracts.

THE LARGER TREND

Mergers and acquisitions are expected to rebound this year after M&A activity fell to its lowest level in 10 years globally in 2023, according to Reuters.

Deal making last year was weighed down by high interest rates, economic uncertainty and a regulatory scrutiny, with all but the last factor slowly abating for renewed confidence.

Late last week, Oregon Health & Science University (OHSU) and Legacy Health, both not-for-profit health systems based in Portland, OR, shared that they had signed a definitive agreement to merge after first announcing their intent to combine last August.

The combined system would be the largest in the Portland region, with 12 hospitals and a total annual revenue of about $6.6B. As part of the deal, OHSU has promised to invest about $1B over ten years to upgrade Legacy’s facilities.

The systems are expected to apply this summer for review by Oregon’s Health Care Market Oversight Program, which was established in 2022 and has the authority to deny or attach conditions to healthcare mergers in the state.

The Gist: If finalized, this merger would connect OHSU’s academic medical center to Legacy’s network of community hospitals and clinics, as well as secure Legacy a needed capital infusion.

Next steps include review by both federal regulatory agencies and Oregon, which is among a growing number of states to implement M&A oversight laws.

Jefferson Einstein Hospital in Philadelphia is implementing a two-year phased closure of its pediatric residency program, according to a Jan. 11 statement provided to Becker’s.

Residents currently enrolled will be able to complete the three-year program, but there will be no new class this year.

Jefferson Health, the hospital’s operator, said the decision was made in response to “the changing medical needs of our communities.”

“We consistently examine all opportunities to continually improve health care delivery in the communities we serve,” the system said in the statement. “We remain committed to caring for the outpatient pediatric patients in our community and will continue to provide inpatient services in the perinatal newborn unit and neonatal intensive care unit at Jefferson Einstein Hospital.”

Jefferson Einstein Hospital came under Jefferson’s umbrella after the health system merged with Einstein Healthcare Network in October 2021.

Earlier this week, Upland, Pa.-based Crozer-Chester Medical Center’s surgical residency program’s lost its accreditation, with the program needing to close by Jan. 12. Accreditation for the program — which had 15 filled resident positions — was withdrawn “under special circumstances,” according to a note on the ACGME’s website.

Health systems are recovering from the worst financial year in recent history. We surveyed strategic planners to find out their top priorities for 2024 and where they are focusing their energy to achieve growth and sustainability. Read on to explore the top six findings from this year’s survey.

Research questions

With this survey, we sought the answers to five key questions:

How do health system margins, volumes, capital spending, and FTEs compare to 2022 levels?

How will rebounding demand impact financial performance?

How will strategic priorities change in 2024?

How will capital spending priorities change next year?

Bigger is Better for Financial Recovery

What did we find?

Hospitals are beginning to recover from the lowest financial points of 2022, where they experienced persistently negative operating margins. In 2023, the majority of respondents to our survey expected positive changes in operating margins, total margins, and capital spending. However, less than half of the sample expected increases in full-time employee (FTE) count. Even as many organizations reported progress in 2023, challenges to workforce recovery persisted.

40%

Of respondents are experiencing margins below 2022 levels

Importantly, the sample was relatively split between those who are improving financial performance and those who aren’t. While 53% of respondents projected a positive change to operating margins in 2023, 40% expected negative changes to margin.

One exception to this split is large health systems. Large health systems projected above-average recovery of FTE counts, volume, and operating margins. This will give them a higher-than-average capital spending budget.

Why does this matter?

These findings echo an industry-wide consensus on improved financial performance in 2023. However, zooming in on the data revealed that the rising tide isn’t lifting all boats. Unequal financial recovery, especially between large and small health systems, can impact the balance of independent, community, and smaller providers in a market in a few ways. Big organizations can get bigger by leveraging their financial position to acquire less resourced health systems, hospitals, or provider groups. This can be a lifeline for some providers if the larger organization has the resources to keep services running. But it can be a critical threat to other providers that cannot keep up with the increasing scale of competitors.

Variation in financial performance can also exacerbate existing inequities by widening gaps in access. A key stakeholder here is rural providers. Rural providers are particularly vulnerable to financial pressures and have faced higher rates of closure than urban hospitals. Closures and consolidation among these providers will widen healthcare deserts. Closures also have the potential to alter payer and case mix (and pressure capacity) at nearby hospitals.

Volumes are decoupled from margins

What did we find?

Positive changes to FTE counts, reduced contract labor costs, and returning demand led the majority of respondents in our survey to project organizational-wide volume growth in 2023. However, a significant portion of the sample is not successfully translating volume growth to margin recovery.

44%

Of respondents who project volume increases also predict declining margins

On one hand, 84% of our sample expected to achieve volume growth in 2023. And 38% of respondents expected 2023 volume to exceed 2022 volume by over 5%. But only 53% of respondents expected their 2023 operating margins to grow — and most of those expected that the growth would be under 5%. Over 40% of respondents that reported increases in volume simultaneously projected declining margins.

Why does this matter?

Health systems struggled to generate sufficient revenue during the pandemic because of reduced demand for profitable elective procedures. It is troubling that despite significant projected returns to inpatient and outpatient volumes, these volumes are failing to pull their weight in margin contribution. This is happening in the backdrop of continued outpatient migration that is placing downward pressure on profitable inpatient volumes.

There are a variety of factors contributing to this phenomenon. Significant inflationary pressures on supplies and drugs have driven up the cost of providing care. Delays in patient discharge to post-acute settings further exacerbate this issue, despite shrinking contract labor costs. Reimbursements have not yet caught up to these costs, and several systems report facing increased denials and delays in reimbursement for care. However, there are also internal factors to consider. Strategists from our study believe there are outsized opportunities to make improvements in clinical operational efficiency — especially in care variation reduction, operating room scheduling, and inpatient management for complex patients.

Strategists look to technology to stretch capital budgets

What did we find?

Capital budgets will improve in 2024, albeit modestly. Sixty-three percent of respondents expect to increase expenditures, but only a quarter anticipate an increase of 6% or more. With smaller budget increases, only some priorities will get funded, and strategists will have to pick and choose.

Respondents were consistent on their top priority. Investments in IT and digital health remained the number one priority in both 2022 and 2023. Other priorities shifted. Spending on areas core to operations, like facility maintenance and medical equipment, increased in importance. Interest in funding for new ambulatory facilities saw the biggest change, falling down two places.

Why does this matter?

Capital budgets for health systems may be increasing, but not enough. With the high cost of borrowing and continued uncertainty, health systems still face a constrained environment. Strategists are looking to get the biggest bang for their buck. Technology investments are a way to do that. Digital solutions promise high impact without the expense or risk of other moves, like building new facilities, which is why strategists continue to prioritize spending on technology.

The value proposition of investing in technology has changed with recent advances in artificial intelligence (AI), and our respondents expressed a high level of interest in AI solutions. New applications of AI in healthcare offer greater efficiencies across workforce, clinical and administrative operations, and patient engagement — all areas of key concern for any health system today.

Building is reserved for those with the largest budgets

What did we find?

Another way to stretch capital budgets is investing in facility improvements rather than new buildings. This allows health systems to minimize investment size and risk. Our survey found that, in general, strategists are prioritizing capital spending on repairs and renovation while deprioritizing building new ambulatory facilities.

When the responses to our survey are broken out by organization type, a different story emerges. The largest health systems are spending in ways other systems are not. Systems with six or more hospitals are increasing their overall capital expenditures and are planning to invest in new facilities. In contrast, other systems are not increasing their overall budgets and decreasing investments in new facilities.

AMCs are the only exception. While they are decreasing their overall budget, they are increasing their spending on new inpatient facilities.

Why does this matter?

Health systems seek to attract patients with new facilities — but only the biggest systems can invest in building outpatient and inpatient facilities. The high ranking of repairs in overall capital expenditure priorities suggests that all systems are trying to compete by maintaining or improving their current facilities. Will renovations be enough in the face of expanded building from better financed systems? The urgency to respond to the pandemic-accelerated outpatient shift means that building decisions made today, especially in outpatient facilities, could affect competition for years to come. And our survey responses suggest that only the largest health system will get the important first-mover advantage in this space.

AMCs are taking a different tack in the face of tight budgets and increased competition. Instead of trying to compete across the board, AMCs are marshaling resources for redeployment toward inpatient facilities. This aligns with their core identity as a higher acuity and specialty care providers.

Partnerships and affiliations offer potential solutions for health systems that lack the resources for building new facilities. Health systems use partnerships to trade volumes based on complexity. Partnerships can help some health systems to protect local volumes while still offering appropriate acute care at their partner organization. In addition, partnerships help health systems capture more of the patient journey through shared referrals. In both of these cases, partnerships or affiliations mitigate the need to build new inpatient or outpatient facilities to keep patients.

Eighty percent of respondents to our survey continued to lose patient volumes in 2023. Despite this threat to traditional revenue, health systems are turning from revenue diversification practices. Respondents were less likely to operate an innovation center or invest in early-stage companies in 2023. Strategists also reported notably less participation in downside risk arrangements, with a 27% decline from 2022 to 2023.

Why does this matter?

The retreat from revenue diversification and risk arrangements suggests that health systems have little appetite for financial uncertainty. Health systems are focusing on financial stabilization in the short term and forgoing practices that could benefit them, and their patients, in the long term.

Strategists should be cautious of this approach. Retrenchment on innovation and value-based care will hold health systems back as they confront ongoing disruption. New models of care, patient engagement, and payment will be necessary to stabilize operations and finances. Turning from these programs to save money now risks costing health systems in the future.

Market intelligence and strategic planning are essential for health systems as they navigate these decisions. Holding back on initiatives or pursuing them in resource-constrained environments is easier when you have a clear course for the future and can limit reactionary cuts.

Advisory Board’s long-standing research on developing strategy suggests five principles for focused strategy development:

Strategic plans should confront complexity. Sift through potential future market disruptions and opportunities to establish a handful of governing market assumptions to guide strategy.

Ground strategy development in answers to a handful of questions regarding future competitive advantage. Ask yourself: What will it take to become the provider of choice?

Communicate overarching strategy with a clear, coherent statement that communicates your overall health system identity.

A strategic vision should be supported by a limited number of directly relevant priorities. Resist the temptation to fill out “pro forma” strategic plan.

Pair strategic priorities with detailed execution plans, including initiative roadmaps and clear lines of accountability.

Strategists align on a strategic vision to go back to basics

What did we find?

Despite uneven recovery, health systems widely agree on which strategic initiatives they will focus more on, and which they will focus less on. Health system leaders are focusing their attention on core operations — margins, quality, and workforce — the basics of system success. They aim to achieve this mandate in three ways. First, through improving efficiency in care delivery and supply chain. Second, by transforming key elements of the care delivery system. And lastly, through leveraging technology and the virtual environment to expand job flexibility and reduce administrative burden.

Health systems in our survey are least likely to take drastic steps like cutting pay or expensive steps like making acquisitions. But they’re also not looking to downsize; divesting and merging is off the table for most organizations going into 2024.

Why does this matter?

The strategic priorities healthcare leaders are working toward are necessary but certainly not easy. These priorities reflect the key challenges for a health system — margins, quality, and workforce. Luckily, most of strategists’ top priorities hold promise for addressing all three areas.

This triple mandate of improving margins, quality, and workforce seems simple in theory but is hard to get right in practice. Integrating all three core dimensions into the rollout of a strategic initiative will amplify that initiative’s success. But, neglecting one dimension can diminish returns. For example, focusing on operational efficiency to increase margins is important, but it’ll be even more effective if efforts also seek to improve quality. It may be less effective if you fail to consider clinicians’ workflow.

Health systems that can return to the basics, and master them, are setting a strong foundation for future growth. This growth will be much more difficult to attain without getting your house in order first.

Vendors and other health system partners should understand that systems are looking to ace the basics, not reinvent the wheel. Vendors should ensure their products have a clear and provable return on investment and can map to health systems’ strategic priorities. Some key solutions health systems will be looking for to meet these priorities are enhanced, easy-to-follow data tools for clinical operations, supply chain and logistics, and quality. Health systems will also be interested in tools that easily integrate into provider workflow, like SDOH screening and resources or ambient listening scribes.

Going back to basics

Craft your strategy

1. Rebuild your workforce.

One important link to recovery of volume is FTE count. Systems that expect positive changes in FTEs overwhelmingly project positive changes in volume. But, on average, less than half of systems expected FTE growth in 2023. Meanwhile, high turnover, churn, and early retirement has contributed to poor care team communication and a growing experience-complexity gap. Prioritize rebuilding your workforce with these steps:

Recover: Ensure staff recover from pandemic-era experiences by investing in workforce well-being. Audit existing wellness initiatives to maximize programs that work well, and rethink those that aren’t heavily utilized.

Recruit: Compete by addressing what the next generation of clinicians want from employment: autonomy, flexibility, benefits, and diversity, equity, and inclusion (DEI). Keep up to date with workforce trends for key roles such as advance practice providers, nurses, and physicians in your market to avoid blind spots.

Retain: Support young and entry-level staff early and often while ensuring tenured staff feel valued and are given priority access to new workforce arrangements like hybrid and gig work. Utilize virtual inpatient nurses and virtual hubs to maintain experienced staff who may otherwise retire. Prioritize technologies that reduce the burden on staff, rather than creating another box to check, like ambient listening or asynchronous questionnaires.

2. Become the provider of choice with patient-centric care.

Becoming the provider of choice is crucial not only for returning to financial stability, but also for sustained growth. To become the provider of choice in 2024, systems must address faltering consumer perspectives with a patient-centric approach. Keep in mind that our first set of recommendations around workforce recovery are precursors to improving patient-centered care. Here are two key areas to focus on:

Front door: Ensure a multimodal front door strategy. This could be accomplished through partnership or ownership but should include assets like urgent care/extended hour appointments, community education and engagement, and a good digital experience.

Social determinants of health: A key aspect of patient-centered care is addressing the social needs of patients. Our survey found that addressing SDOH was the second highest strategic priority in 2023. Set up a plan to integrate SDOH screenings early on in patient contact. Then, work with local organizations and/or build out key services within your system to address social needs that appear most frequently in your population. Finally, your workforce DEI strategy should focus on diversity in clinical and leadership staff, as well as teaching clinicians how to practice with cultural humility.

3. Recouple volume and margins.

The increasingly decoupled relationship between volume and margins should be a concern for all strategists. There are three parts to improving volume related margins: increasing volume for high-revenue procedures, managing costs, and improving clinical operational efficiency.

Revenue growth: Craft a response to out-of-market travel for surgery. In many markets, the pool of lucrative inpatient surgical volumes is shrinking. Health systems are looking to new markets to attract patients who are willing to travel for greater access and quality. Read our findings to learn more about what you need to attract and/or defend patient volumes from out-of-market travel.

Cost reduction: Although there are many paths health systems can take to manage costs, focusing on tactics which are the most likely to result in fast returns and higher, more sustainable savings, will be key. Some tactics health systems can deploy include preventing unnecessary surgical supply waste, making employees accountable for their health costs, and reinforcing nurse-led sepsis protocols.

Clinical operational efficiency: The number one strategic priority in 2023, according to our survey, was clinical operational efficiency, no doubt in response to faltering margins. Within this area, the top place for improvement was care variation reduction (CVR). Ensure you’re making the most out of CVR efforts by effectively prioritizing where to spend your time. Improve operational efficiency outside of CVR by improving OR efficiency and developing protocols for complex inpatient management.

Big, industry-shaking acquisitions including Oakland, Calif.-based Kaiser Permanente’s purchase of Danville, Pa.-based Geisinger, could redefine healthcare delivery with an eye toward value. Regional deals, such as Detroit-based Henry Ford Health’s planned joint venture with Ascension Michigan and St. Louis-based BJC HealthCare’s plan to acquire Saint Luke’s Health System to create a $10 billion organization, have also made waves.

There were 18 hospital and health system transactions announced in the third quarter, up from 10 transactions over the same time period in 2022, according to Kaufman Hall’s third quarter M&A report. Financial pressures with inflation catapulting staffing and supply costs, and reimbursement rates growing much more slowly, have forced some systems to look for a buyer while others aim to increase market share.

Academic health systems are also seeking community partners at a higher rate than in the past, according to the Kaufman Hall report.

But not all announced deals have gone according to plan.

The Federal Trade Commission is scrutinizing deals more closely than ever before to ensure costs don’t increase after an acquisition in some cases. In other cases, the two partners aren’t able to agree upon the details after announcing their plans. The dissolved merger between Sioux Falls, S.D.-based Sanford Health and Minneapolis-based Fairview Health Services fell apart amid contention in Minnesota, and West Des Moines, Iowa-based UnityPoint Health’s plans to merge with Presbyterian Healthcare Services in Albuquerque, N.M., was halted without a publicly stated reason.

Will there be more or fewer health system deals in the next three years?

Seth Ciabotti, CEO of MSU Health Care at Michigan State University in East Lansing, thinks so, at least when it comes to academic medical centers.

“There will be more consolidation to mitigate risk,” he told Becker’s. “I believe we are heading down a path of having only a dozen or so non-academic medical centers/health systems being left in the near future in the U.S.”

Mark Behl, president and CEO of NorthBay Health in Fairfield, Calif., has a similar outlook for the next three years.

“I suspect we will see more mergers and acquisitions with a continued desire to grow larger and remain relevant,” he told Becker’s. “Independent regional health systems will fight for relevance, and sometimes survival.”

And health systems won’t be the only buyers. Private equity, health insurers and non-traditional owners are on the hunt for health systems. General Catalyst has strengthened its healthcare presence recently and announced it plans to acquire a system in the near future.

“I believe that over the next three years, the landscape of acquisitions, divestitures and joint ventures will continue to reshape the healthcare industry,” said Dennis Sunderman, system director of HR M&A, non-employee and provider services at CommonSpirit Health, told Becker’s. “Current and proposed legislation, the continued evolution of ownership groups, nonprofit, for profit, and private equity, and the drive to hire and retain exceptionally talented teams, will lead to new innovations and an enhanced focus on the associates affected by the transaction.”

Health systems will need to optimize their operations to expand their value-based care efforts and digital transformation, including telehealth and remote patient monitoring services. Not all systems have the expertise and resources to fully make this transition, but with the right partners and strategic alignments, they can accelerate care transformation.

“There will likely be more collaborations and partnerships to expand services and increase access versus brick and mortar acquisitions,” said Cliff Megerian, MD, CEO of University Hospitals in Cleveland. “Innovative thinking is critical for success and quite frankly survival in our industry, so health systems should already be investing in growing in-house expertise dedicated to ideating new models of care, but in three years, these efforts should be producing tangible results.”

Michelle Fortune, BSN, CEO of Atrium St. Luke’s Hospital in Columbus, N.C., pointed to recent collaborations between Mercy, Microsoft and Mayo Clinic as examples of how health systems can partner on important initiatives such as improved data sharing, generative AI, digital transformation and more.

“I expect to see an increase in collaborations and connections between health systems to a degree that has never existed before as part of the focus on bringing the right care to people across the full continuum, when and where they need it,” she said.

Kaufman Hall sees more minority ownership deals ahead, which allows the smaller system to maintain near-autonomy while benefiting from the resources of a larger system.

“Health systems are also engaging in creative transaction structures that allow partners to maintain their independence while building strategic alliances that enhance access to care,” the report notes. “Announced transactions in Q3 included [Charlottesville, Va.-based] UVA Health’s acquisition of 5% ownership interest in [Newport News, Va.-based] Riverside Health System as part of a strategic alliance design ‘to expand patient access to innovative care for complex medical conditions, transplantation, and the latest clinical trials.'”

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

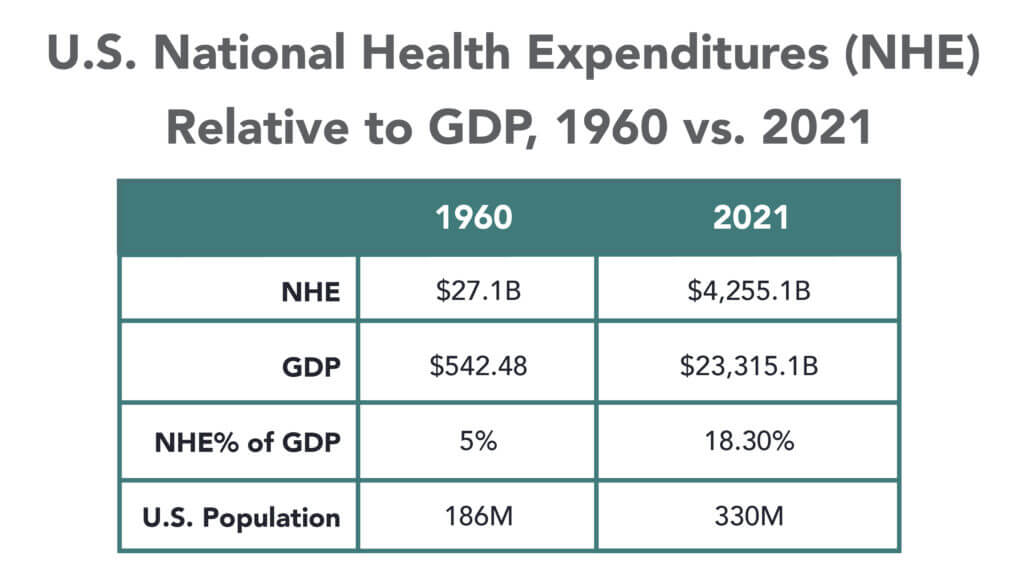

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

Resident and fellow physicians at Palo Alto, Calif.-based Stanford Health Care have voted in favor of representation by the Committee of Interns and Residents, according to a May 3 news release.

Of the nearly 1,050 ballots counted, 835 were in favor of representation, the National Labor Relations Board website showed.

The vote comes after resident physicians led a protest in December 2020 against Stanford’s COVID-19 vaccination plan that excluded house staff from the initial round of shots. The health system immediately revised the plan to prioritize resident physicians.

In February, physicians also demanded the health system voluntarily recognize the Committee of Interns and Residents as their exclusive representative for collective bargaining.

Now the union said its members are looking forward to negotiations.

“Our doctors are united by our desire to provide the best possible patient care and strong worker protections,” said Ben Solomon, MD, a pediatric resident physician, said in the release. “One thing the pandemic has made abundantly clear, in addition to the widespread equity issues in our healthcare system, is that our needs as physicians cannot be separated from those of our patients.”

The National Labor Relations Board must certify the election results before they are final. Stanford does not plan to challenge the results, the health system said in a statement shared with Becker’s on May 3.

“As we begin the collective bargaining process, our goal remains unchanged: providing our residents and fellows with a world-class training experience,” Stanford said. “We will bring this same focus to negotiations as we strive to support their development as physician leaders.”

The Committee of Interns and Residents is a local chapter of the Service Employees International Union. The union represents more than 20,000 resident physicians and fellows, including University of Massachusetts physicians in training, who unionized in March 2021.

Philadelphia-based Temple University has signed a binding definitive agreement to sell the Fox Chase Cancer Center and its bone marrow transplant program to Thomas Jefferson University in Philadelphia.

The announcement comes after nearly a year of negotiations. Temple expects to complete the sale of the cancer center and bone marrow transplant program in the spring of 2020.

Temple also entered into an agreement to sell its membership interest in Health Partners Plan, a Philadelphia-based managed care program, to Jefferson. A closing date for the transaction has not yet been determined.

With the agreements in place, Temple and Jefferson are looking for other ways to collaborate. The two organizations are exploring a broad affiliation that would help them address social determinants of health, enhance education for students at both universities, collaborate on healthcare innovation, and implement a long-term oncology agreement that would expand access to resources for Temple residents, fellows and students.

“Healthcare is on the cusp of a revolution and it will require creative partnerships to have Philadelphia be a center of that transformation,” Stephen Klasko, MD, president of Thomas Jefferson University and CEO of Jefferson Health, said in a news release. “For Jefferson, our relationship with Temple will accelerate our mission of improving lives and reimagining health care and education to create unparalleled value.”

University of Chicago Medical Center has closed its level 1 trauma center for adult and pediatric patients as it prepares for about 2,200 nurses to go on strike next week, medical center leaders announced.

Medical center leaders said UCMC closed its pediatric level 1 trauma program Nov. 18 and its adult trauma program Nov. 20. Its adult and pediatric emergency rooms continue to take walk-in patients.

Nurses are scheduled to strike Nov. 26, two days before Thanksgiving. The nurses also walked off the job Sept. 20 in a strike organized by National Nurses Organizing Committee/National Nurses United. They were allowed to return to work Sept. 25, after the medical center said it fulfilled its contract with temporary nurses to replace the striking ones for five days.

In preparation for the strike, UCMC announced earlier this week that it is moving about 50 babies and 20 children in its neonatal and pediatric intensive care units to other facilities.

UCMC President Sharon O’Keefe is also recruiting about 900 replacement nurses.

However, “it’s exceptionally difficult to hire people who are willing to leave their families during Thanksgiving,” she said in a news release. “At the same time, other hospitals in the city are already at or near capacity, which means they will not be able accept transfers of current inpatients if that need arises when nurses walk out. The combination of the two led us to take the step of temporarily closing our trauma program ahead of the strike.”

UCMC said the hospital was required to offer replacement nurses five days of work “to best recruit qualified and experienced replacement nurses.” Therefore, the nurses on strike will not be able to return to work until 7 a.m. Dec. 1.

Negotiations between UCMC and National Nurses Organizing Committee/National Nurses United began earlier this year. Medical center leaders say incentive pay — and whether the hospital should end the pay for newly hired nurses — is a sticking point in negotiations, according to the Chicago Tribune. The union has continued to express concerns about staffing levels.

The nurses said they plan to strike unless an agreement is reached.