On today’s episode of Gist Healthcare Daily, Kaufman Hall co-founder and Chair Ken Kaufman joins the podcast to discuss his recent blog that examines Ford Motor Company’s decision to stop producing internal-combustion sedans, and talk about whether there are parallels for health system leaders to ponder about whether their traditional strategies are beginning to age out.

Although Artificial intelligence has been around for 50 years and has experienced several starts and stops, the last 5 to 10 years have seen a considerable uptick in adoption, especially in healthcare. It’s embedded now in machine learning that enables faster and more precise imaging studies, clinical decision support tools in electronic medical records systems and many more. In recent months, its potential to play a bigger role, possibly replacing physician judgement among others, has received added attention.

The November 2022, the announcement of OpenAI’s ChatGPT platform drew widespread attention with speculation it might displace clinicians in diagnosing and treatment planning for patients. On March 22, 2023, tech moguls Elon Musk, Steve Wozniak and Andrew Yang called for a 6-month moratorium on generative AI stating: “Should we develop nonhuman minds that might eventually outnumber, outsmart, obsolete and replace us? Should we risk loss of control of our civilization? We call on all AI labs to immediately pause for at least 6 months the training of AI systems more powerful than GPT-4.” (1) To date, more than 13,000 have signed on to their appeal. Per Lumeris CTO Jean-Claude Saghbini “Putting aside our own opinions as to whether or not a moratorium should be implemented, our recent experience of the last three years in the inability to have effective cross-governmental alignment on policy to fight the COVID pandemic suggests that global alignment on AI policy will be impossible”.

There’s widespread belief generative AI and GPT-4 are game changers in healthcare.

How, what, when and how much ($$$) are the big questions. The near-term issues associated with implementation–data-security, workforce usefulness, regulation, investment costs—are expected to be resolved eventually. Thus, it is highly likely that health systems, medical groups, health insurers and retail and digital health solution providers will operate in a widely-expanded AI-enabled world in the next 3-5 years.

Questions:

What role will AI and ChatGPT play in hospitals/health systems and other provider settings? Will development of AI systems more powerful than GPT-4 be suspended in response to the appeal? How is your organization preparing for the next wave of AI?

Key Takeaways from Discussion:

‘Generative AI will not take the place of clinician judgement anytime soon. The processes of diagnosing and treating patients, especially complex conditions, will not be displaced. However, in primary and preventive health where standardization is more attainable, it will have profound impact perhaps sooner than in other areas.’

‘GPT-4 et al will have profound impact on the delivery of healthcare and hospital operations, but there are many unknowns and risks associated with its use beyond routine tasks that can be standardized based on pattern recognition. ‘

‘Continued development of platform solutions using GPT-4 and others in healthcare and other industries will accelerate. The moratorium will not happen. There’s too much at stake for investors and users.’

‘Non-profit hospitals and health systems are struggling financially as a result of the supply and labor cost increases, declining reimbursement from payers and negative returns on investing activities (non-operating income). Caution is key, so AI-related investing will be conservative in the near-term. An exception would be AI solutions that mitigate workforce shortages or reduce administrative costs for documentation.’

Nothing kills the momentum and excitement of race day more than the yellow flag and deployed safety car. Unsafe track conditions, usually caused by an accident, debris on the track or a stopped vehicle, can cause the marshals to slow down the race. Momentum moderates and adrenaline wanes. Drivers are forbidden from overtaking, and victory is temporarily out of sight for all but the lead car. As I watched the Indy 500, 24 Hours at Le Mans and a handful of Formula One grand prix over the last several weeks, it struck me that postacute sector M&A (home health, hospice, Medicaid PCS, pediatric PDN/therapy) is currently racing under yellow flag conditions. Temporary, but nonetheless frustrating for all constituents involved.

The post-acute sector’s two record setting years in terms of transaction activity, valuation multiples and quality of companies acquired, 2020 and 2021, now appear to be in the rearview mirror. In their stead is a sluggish 2022, with companies staying in their lanes, focused inwardly on operations and trying to regain levels of growth and profitability of prior years. It should come as no surprise that sector activity has slowed: (i) the supply of actionable platforms is materially lower than in the prior two years; (ii) the COVID spawned labor market continues to create one of the most challenging operating environments in recent memory; (iii) home health reimbursement faces a potentially challenging outlook when the CY 2023 HH PPS rule is finalized in the Fall; and (iv) buyers are less willing to give credit for COVID-related EBITDA adjustments.

Lower Inventory of Actionable Platforms Many of the most actionable privately-held and sponsor-owned platforms transacted at a kinetic pace in 2019, 2020 and 2021. As a result, the number of available platforms is relatively low, and the sector is currently in a holding pattern, where businesses are (i) focused on operating in a challenging environment, (ii) too early in their hold period, or (iii) waiting for financial performance to improve, before coming to market. There is a large and growing backlog of businesses that we expect to come to market when overall conditions improve, potentially as early as Q4 2022. But in the meantime, the market is generally in wait and see mode.

Labor Market’s Impact on Performance Q4 2021 was one of the most challenging quarters for post-acute operators, particularly hospice, as the Omicron variant wreaked havoc on staffing and admissions volumes. Despite strong referral volumes and demand for post-acute services, the inability to

sufficiently hire and retain clinical staff has had a material impact on monthly sequential growth and TTM performance. For many, Q1 2022 was only marginally better, and for some, Q2 2022 continues to present challenges, although, anecdotally, the clinical labor market appears to be improving and may even accelerate due to the looming recession. As a result, companies are deciding, or being forced, to delay sale processes as they attempt to replace poor financial performance in Q4 2021 and Q1 2022 with improved 2H 2022 growth and profitability.

Pending CY 2023 Home Health PPS Rule Based on the proposed rule released last week, CMS estimates that Medicare payments to home health agencies in CY 2023 would decrease in the aggregate by -4.2%, or -$810 million compared to CY 2022. Without getting too technical and comprehensive, this decrease reflects the effects of the proposed 2.9% home health payment update percentage ($560 million increase), an estimated 6.9% decrease that reflects the effects of the proposed prospective, permanent behavioral assumption adjustment of -7.69% ($1.33 billion decrease), and an estimated 0.2% decrease that reflects the effects of a proposed update to the fixed-dollar loss ratio (FDL) used in determining outlier payments ($40 million decrease). Prospective home health sellers will most likely wait for better clarity on the final rule before coming to market.

Market Push Back on COVID-Related EBITDA Adjustments Buyers and lenders have materially increased their scrutiny of COVID-related volume adjustments to EBITDA. Early in the pandemic, the market was quite willing to pay sellers for normalized volumes and financial performance, as if “COVID had not happened.” 27 months later, the market is taking a harder line. “What if” earnings credit is no longer being given wholesale. The market has taken the position that labor staffing challenges and higher labor wage expense are here to stay (for now), and, unless a seller has clearly demonstrated a trend to the contrary, little to no valuation / leverage credit will be given for such adjustments. As a result, prospective sellers must increasingly rely on actual earnings to ensure the achievement of valuation expectations.

Returning to our racing analogy, post-acute sector M&A is currently under a yellow flag. And while yellow flag conditions produce little to no racing action, and can last for many laps, they are still only temporary. Drivers and their teams can use the time to their advantage – to “box” or “pit” in order to change tires, refuel or tweak the car – so that they are ready to drop the hammer once the yellow flag is lifted. This is exactly what the higher quality post-acute platforms are doing. Some of the most exciting action in a race comes once the safety car exits the track and green flag racing resumes. Given the strong near- and long-term demographic and sector trends supporting the post-acute sector, and the almost unlimited demand for high quality post-acute platforms, there is little doubt that M&A activity will resume with a vengeance.

As Warren Buffett turns 90, the story of one of America’s most influential and wealthy business leaders is a study in the logic and discipline of understanding future value.

Patience, caution, and consistency. In volatile times such as these, it may be difficult for executives to keep those attributes in mind when making decisions. But there are immense advantages to doing so. For proof, just look at the steady genius of now-nonagenarian Warren Buffett. The legendary investor and Berkshire Hathaway founder and CEO has earned millions of dollars for investors over several decades (exhibit). But very few of Buffett’s investment decisions have been reactionary; instead, his choices and communications have been—and remain—grounded in logic and value.

Buffett learned his craft from “the father of value investing,” Columbia University professor and British economist Benjamin Graham. Perhaps as a result, Buffett typically doesn’t invest in opportunities in which he can’t reasonably estimate future value—there are no social-media companies, for instance, or cryptocurrency ventures in his portfolio. Instead, he banks on businesses that have steady cash flows and will generate high returns and low risk. And he lets those businesses stick to their knitting. Ever since Buffett bought See’s Candy Shops in 1972, for instance, the company has generated an ROI of more than 160 percent per year —and not because of significant changes to operations, target customer base, or product mix. The company didn’t stop doing what it did well just so it could grow faster. Instead, it sends excess cash flows back to the parent company for reinvestment—which points to a lesson for many listed companies: it’s OK to grow in line with your product markets if you aren’t confident that you can redeploy the cash flows you’re generating any better than your investor can.

As Peter Kunhardt, director of the HBO documentary Becoming Warren Buffett, said in a 2017 interview, Buffett understands that “you don’t have to trade things all the time; you can sit on things, too. You don’t have to make many decisions in life to make a lot of money.” And Buffett’s theory (roughly paraphrased) that the quality of a company’s senior leadership can signal whether the business would be a good investment or not has been proved time and time again. “See how [managers] treat themselves versus how they treat the shareholders .…The poor managers also turn out to be the ones that really don’t think that much about the shareholders. The two often go hand in hand,” Buffett explains.

Every few years or so, critics will poke holes in Buffett’s approach to investing. It’s outdated, they say, not proactive enough in a world in which digital business and economic uncertainty reign. For instance, during the 2008 credit crisis, pundits suggested that his portfolio moves were mistimed, he held on to some assets for far too long, and he released others too early, not getting enough in return. And it’s true that Buffett has made some mistakes; his decision making is not infallible. His approach to technology investments works for him, but that doesn’t mean other investors shouldn’t seize opportunities to back digital tools, platforms, and start-ups—particularly now that the COVID-19 pandemic has accelerated global companies’ digital transformations.

Still, many of Buffett’s theories continue to win the day. A good number of the so-called inadvisable deals he pursued in the wake of the 2008 downturn ended paying off in the longer term. And press reports suggest that Berkshire Hathaway’s profits are rebounding in the midst of the current economic downturn prompted by the global pandemic.

At age 90, Buffett is still waging campaigns—for instance, speaking out against eliminating the estate tax and against the release of quarterly earnings guidance. Of the latter, he has said that it promotes an unhealthy focus on short-term profitsat the expense of long-term performance.

“Clear communication of a company’s strategic goals—along with metrics that can be evaluated over time—will always be critical to shareholders. But this information … should be provided on a timeline deemed appropriate for the needs of each specific company and its investors, whether annual or otherwise,” he and Jamie Dimon wrote in the Wall Street Journal.

Yes, volatile times call for quick responses and fast action. But as Warren Buffett has shown, there are also significant advantages to keeping the long term in mind, as well. Specifically, there is value in consistency, caution, and patience and in simply trusting the math—in good times and bad.

For most people, the effect of Covid-19 on the body is temporary. A dry cough. Fever. Shortness of breath. Then recovery.

But the way the pandemic has altered the behavior of consumers may turn out to be a more permanent shift.

A recent article in the Wall Street Journal reported that the global cosmetics market is down 8%, with less people venturing out of their homes. Demand for at-home cooking products such as Hellman’s Mayonnaise, Knorr soup cubes, and frozen dinners are on the rise. Consumers are ordering more online, embracing food-delivery services, and buying cleaning and hygiene products in droves.

And this is just the tip of the iceberg.

Here are three ways the pandemic has shifted consumers’ mindsets and purchasing behavior, with the data to prove it.

1) Live entertainment in the age of coronavirus

The live entertainment industry has experienced significant disruption since Covid-19 began spreading globally in January. The NBA suspended its season in early March. The International Olympic Committee postponed this summer’s Olympic Games in Tokyo until next year. Concert venues have been shuttered as many countries have limited social gatherings to 50, 10, or even 2 people.

What does the future hold for live entertainment? Data suggests that consumers’ fear of Covid-19 might keep them from returning to arenas, concert halls, and other venues even after the industry kicks back into gear. A recent global survey by Dynata, the world’s largest first-party survey platform, found that over half of people expressed significant concern about returning to live events.

“Our findings suggest a mood of caution as people think about a return to live experiences,” state the researchers at Dynata. “Sixty-five percent overall say they will return to live concerts quite slowly or not at all; 55% say the same for movies, 57% for sporting events and 64% for live theater.”

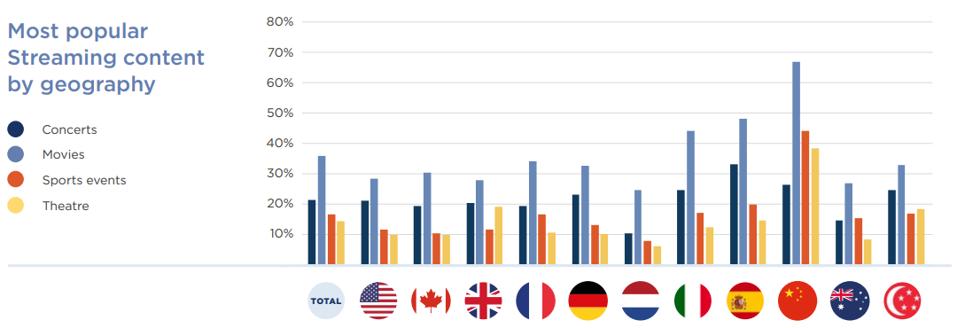

The team at Dynata also found that, since the pandemic started, more than half of those surveyed have live-streamed a concert, movie, sports event, or theatrical production, with movies being the most popular choice of entertainment. Live-streaming events is most common in China, where close to 70% of Chinese people have live-streamed at least one movie since the pandemic began.

DYNATA, 2020

Consumers aren’t nearly as shy about returning to restaurants. A recent survey by the Cincinnati-based experiential marketing firm AGAR found that consumers were more likely to indicate a desire to return to restaurants than sporting events, concerts, and cultural holidays and fairs.

Moreover, consumers are voicing a growing interest in health-conscious event planning. Asking consumers what event features they would most desire in the future, the team at AGAR found that hand sanitizing kiosks, social distancing ground stickers, and spaced-apart seating were on the top of the list. Interestingly, over a third of people expressed a willingness to pay a premium to attend smaller events with limited capacities.

“The results of the study clearly show us the path forward, what must be done to bring people back and to make them comfortable,” said AGAR founder, Josh Heuser. “It’s vital that we ensure people feel supported, safe and cared for while attending events.”

2) Contactless payment is becoming the rule not the exception

Covid-19 may have finally given contactless payment the nudge it needs to become the go-to mode of payment. The team at AGAR found that consumers view contactless payment as a necessary feature at live events moving forward.

Prior to the pandemic, approximately 22% of the more than 11,000 global respondents surveyed by Dynata expressed a preference for cash. This has now fallen to 15%. The countries most prepared to make the shift to contactless payment are China, Singapore, and the United Kingdom.

“The past few months have seen an increase in the availability of contactless methods,” according to researchers at Dynata. “The biggest growth has been seen in the USA, moving from 38% to 46% ownership of a contactless method of payment.”

3) Adjusting to telemedicine

According to the researchers at Dynata, 84% of people using telemedicine services during the pandemic were doing so for the first time. And the data show that it is here to stay; 55% of people using telemedicine found the experience to be extremely or very satisfactory. Interestingly, people in the United Kingdom, United States, and Canada were most satisfied with the experience, perhaps because there is a relatively low number of doctors per capita in these countries.

Beyond telemedicine, consumers are increasingly interested in products that provide protection against environmental contaminants and pathogens. Wesley LaPorte, co-founder and CEO of PhoneSoap, a company that makes UV light phone sanitizers, notes a significant uptick (+500%) in PhoneSoap web traffic.

“As awareness of the spread of COVID-19 began to grow in the country, PhoneSoap quickly sold out of UV-C light sanitizers,” said LaPorte. “After the spike in March, web traffic is still significantly higher than last year, with consumers continuing to place pre-orders at unprecedented levels.”

Conclusion: Sigmund Freud was famous for popularizing the idea that human behavior is largely guided by sex, attraction, and the pleasure principle. Covid-19 provides a compelling counterpoint to Freud’s theory — that, especially during times of heightened panic and threat, it is the survival instinct that trumps all other motivations.