New Medicaid funding rules proposed by Congress this week would halt efforts at the state level to better fund rural hospitals and deliver services to the most vulnerable populations in those areas. You can be certain that the administrators and staff of those hospitals, as well as leaders of the communities they serve, are watching closely to see if the cuts are enacted.

Lawmakers at the federal level are trying to make deeper cuts to Medicaid spending in an effort to lower the amount of deficit spending that would be created by President Trump’s spending plan. Trump has dubbed the plan his “big beautiful bill.”

Feds Would Strip Rural Hospitals of Lifeline Funds

Republican members of the Senate Finance Committee this week released their version of the bill that would drain funding for rural hospitals, which rely heavily on Medicaid funds to treat patients. It’s estimated that 25 to 40 percent of services provided by such hospitals are funded by Medicaid.

The federal government and states share the up-front medical costs for Medicaid patients. The federal government then reimburses states up to 50 percent of their Medicaid spending every year.

Many states fund their portion of the cost by taxing entities that provide those services to Medicaid patients.

The latest proposal in Congress would not only restrict how many patients could receive benefits, but it would also stop states from implementing those provider tax programs to help fund Medicaid services provided to residents.

At the federal level, the thinking is that if states keep taxing providers to fund Medicaid services, then the federal government will have to keep reimbursing states a portion of those costs.

The downside to that is many experts, along with several Republicans in Congress, namely Sens. Susan Collins of Maine, Lisa Murkowski of Alaska and Josh Hawley of Missouri, have predicted it will decimate rural hospitals.

West Virginia Republican Sen. Jim Justice went a step further, saying that the plan to limit states’ use of provider taxes will “really hurt a lot of folks.” Despite that statement, Justice said he is OK with the freeze.

State Lawmakers Sound the Alarm

There are 39 states with at least three or more provider taxes used to help fund Medicaid services. Alaska is the only state with no such tax.

Some states, such as Ohio, have set up a new rural hospital fund using provider taxes to help rural hospitals deliver Medicaid services to patients.

Ohio Governor Mike DeWine and the Republican-led state legislature set up a pilot program called the Rural Ohio Hospital Tax Pilot Program. The measure would allow counties to levy a tax on their local hospitals that would then be used to fund Medicaid services.

DeWine said the pilot program would help ease the financial stress rural hospitals face in Ohio. The plan contained in Ohio House Bill 96 has the blessing of the Ohio Hospital Association.

A group of Republican state lawmakers recently sent a letter to their federal counterparts pleading with them to remove the bill language because it would “torpedo” plans to keep rural hospitals functioning.

The American Hospital Association, a 130-year-old trade group of more than 5,000 hospitals and health care providers, this month released the impact on rural hospitals if this plan went into effect.

More than $50 billion would be lost by 2034, and more than 1.8 million rural Americans would lose health benefits.

Kentucky residents would be impacted the most, with 143,000 losing benefits, followed by 135,000 Californians. More than 86,000 Ohioans would lose Medicaid coverage under the plan by 2034, making it the third most impacted state.

To blunt the effects of the cuts, Collins reportedly is proposing the establishment of a $100 billion relief fund that could provide financial support to affected providers, rural hospitals in particular. Whether that or a similar but smaller fund will wind up in the final draft of the legislation apparently will be decided this weekend. Meanwhile, the Senate parliamentarian has ruled against many of the provisions of the Senate version of the bill, including the Finance Committee’s provider tax framework, which puts the whole thing in flux.

Senate leaders say they plan a long series of votes on amendments of the bill on Sunday. The “vote-arama” likely will go on throughout Sunday night and into Monday. If the Senate does pass its version of the bill, it will have to go back to the House. Lawmakers are under a self-imposed deadline to get the legislation to Trump by the July 4 holiday.

Some of America’s largest hospital systems saw their financials soar in the first half of 2024. And yet, more than 700 facilities across the country still are at risk of closing.

Why it matters:

It’s a familiar tale of the rich getting richer, as big, mostly for-profit health systems see improved margins while smaller facilities in outlying areas are barely hanging on.

That could worsen access for some of the most vulnerable Americans — and hasten consolidation in an industry that’s been a magnet for M&A.

The big picture:

Health systems with big footprints, including large academic medical centers, have weathered the pandemic and economic headwinds and are seeing margins as good or better than before COVID-19.

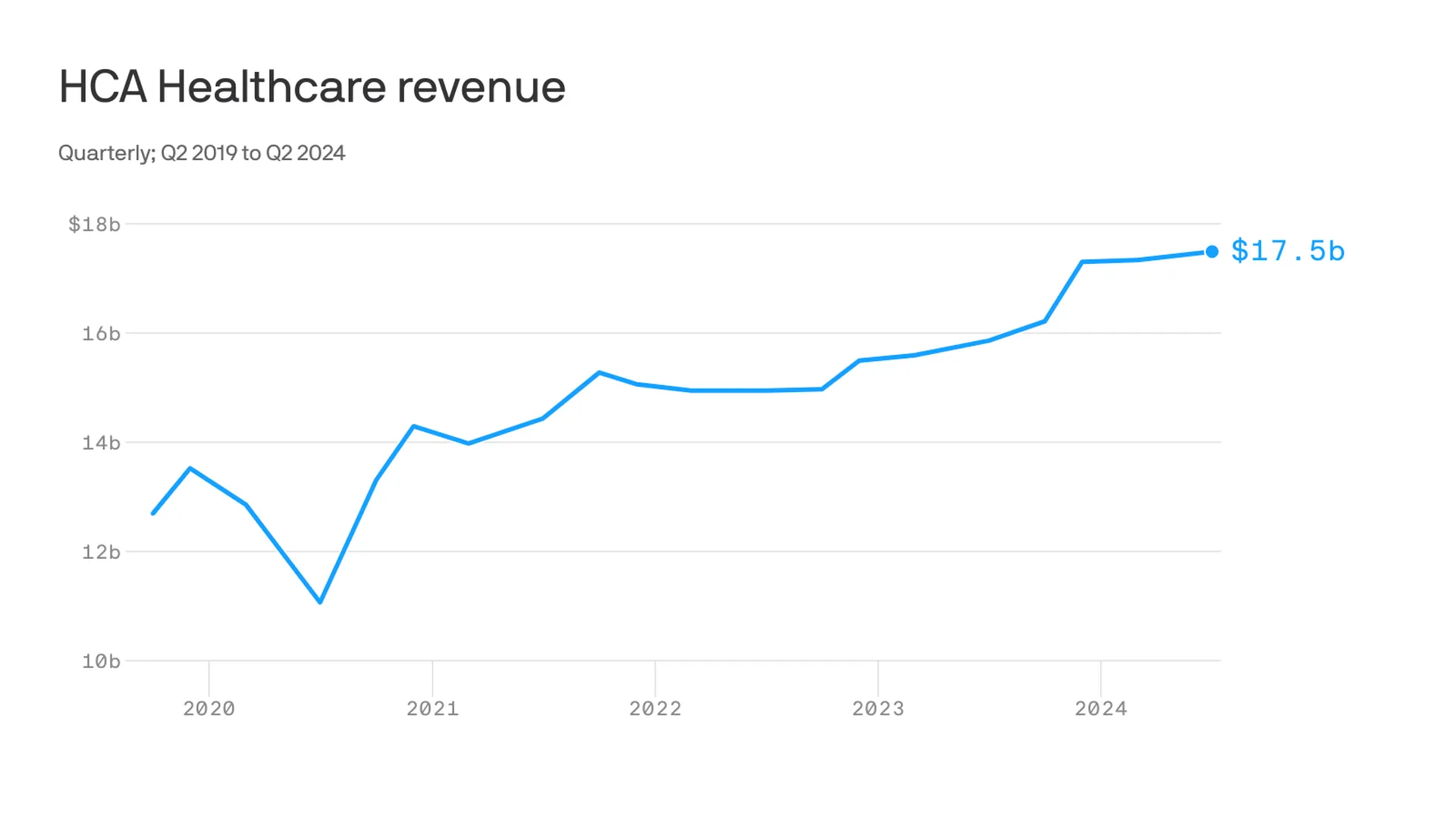

Nashville-based industry behemoth HCA Healthcare posted 23% year-over-year profit growth for the quarter, revising its forecast for the rest of the year, projecting it’ll reach as much as $6 billion. It posted a 10% year-over-year increase in revenue.

King of Prussia, Pennsylvania-based Universal Health Services similarly reported a strong quarter, posting nearly 69% growth on its bottom line over the same period last year while Dallas-based Tenet Healthcare reported a 111% jump in its net income over the same quarter last year.

Yes, but:

Smaller nonprofit hospitals, especially in rural areas, that made it through the crisis with the help of government aid are paring services like maternity wards and struggling to stay open.

“There are a lot of hospitals that survived, but their balance sheets are so weakened, their margin for error is basically zero at this point,” said Mike Eaton, senior vice president of strategy at population health company Navvis.

Hospitals that once could manage their expenses and the needs of communities are “going to really struggle to invest in what comes next,” he said.

Between the lines:

The biggest health systems have benefited from less volatility, seeing stabilizing drug prices and more predictable supply chains and labor costs, per a new report from Strata Decision Technology.

“It’s at least something you can manage to,” Steve Wasson, Strata’s chief data and intelligence officer, told Axios.

Revenues already were up thanks to renegotiated contracts health systems struck with payers last year, Wasson said.

There also have been changes on the federal side that boosted Medicare admissions and put some hospitals in line to be reimbursed for billions in underpayments from the 340B drug discount program.

Zoom in:

It’s all translated to operating margins that are up 17% year-to-date compared with the same time period in 2023, according to the latest Kaufman Hall National Hospital Flash Report.

Volumes as measured by hospital discharges per day are up 4% year-to-date.

Expenses per day are also up 6% year to date, including labor (4%), supplies (8%) and drugs (8%), but are far less volatile and thus easier to plan for, said Erik Swanson, senior vice president at Kaufman Hall.

But there’s a growing gulf between the top third of U.S. hospitals, which are seeing outsize growth, and the rest, Swanson said.

Threat level: A new report from the Center for Healthcare Quality and Payment Reform estimated 703 hospitals — or more than one-third of rural hospitals — are at risk of closure, based on Centers for Medicare and Medicaid Services financial information from July. Losses on privately insured patients are the biggest culprit.

“We’re looking at 50% of rural operating in the red. The situation is very challenging,” Michael Topchik, partner at Chartis Center for Rural Health, told Axios.

These smaller hospitals may still be there, but there will continue to be a steady erosion of the kinds of services they offer, such as obstetrics, cancer care and general surgery, he said.

What’s next:

Private equity investment in rural health care is already booming and with it, prospects for service and staffing cuts.

The South generally has the highest concentration of private equity-owned rural hospitals, often with lower patient satisfaction and fewer full-time staff compared with non-acquired hospitals, according to the Private Equity Stakeholder Project.

Congress is ramping up oversight of private equity investments in the sector, though most lawmakers are loath to take steps to actually halt deals.

Portland-based Oregon Health & Science University told staff June 6 that it plans to lay off at least 500 employees, citing financial issues.

“Our expenses, including supplies and labor costs, continue to outpace increases in revenue,” top leaders told staff in a message shared with Becker’s. “Despite our efforts to increase our revenue, our financial position requires difficult choices about internal structures, workforce and programs to ensure that we achieve our state-mandated missions and thrive over the long term.”

Willamette Week was first to report the news, which follows Oregon Health & Science University and Portland-based Legacy Health signing a binding, definitive agreement to come together as one health system under OHSU Health. OHSU Health would comprise 12 hospitals and, more than 32,000 employees and will be one of the largest providers of services to Medicaid members in Oregon.

An Oregon Health & Science University spokesperson told Becker’s more information about the layoffs will be provided in the coming weeks.

In the June 6 message, leaders told staff that “while we work to address short-term financial challenges, we must also plan for an impactful and successful future. We understand that last week’s announcement regarding the Legacy Health definitive agreement, while exciting and potentially transformational, raises questions about how we can afford the required investment in light of our financial situation.”

They added that a capital investment in Legacy “represents a strategic expansion designed to enhance our capacity,” and will be funded by borrowing with 30-year bonds.

“These capital dollars cannot be used to close gaps in our fiscal year 2025 OHSU budget or to pay our members. The OHSU Strategic Alignment and budgetary work would be necessary with or without the Legacy Health integration,” leaders said.

OHSU has planned a town hall next week to further discuss the combination with Legacy.

Leaders said discussions between managers and members about workforce reductions will begin after the annual review and contract renewal process, with additional reductions occurring over the next few months.

Since filing for bankruptcy Monday, Steward Health Care revealed it’s carrying more than $1 billion in debt and said its entire hospital portfolio is for sale.

Eleven minutes later, Steward employees had an email waiting from their CEO, Ralph de la Torre. The CEO told his staff that industrywide economic headwinds and delays in Steward’s planned asset sales had forced the physician-owned health network to initiate restructuring proceedings.

“It is incumbent on all of us to ensure that this process has no impact on the quality care our patients, their families, and our communities can continue to receive at our hospitals,” de la Torre wrote in an email viewed by Healthcare Dive. “To the vast majority of you, operations will either not be different or improve.”

“To be clear, this is a restructuring under chapter 11; it is not a closure and it is not a liquidation,” he wrote.

The email was the first time employees had heard directly from Steward leadership about the company’s financial distress — though rumorsanduncertainty about the operatorhad been festering for weeks, according to Marlishia Aho, regional communications director for the union 1199SEIU United Healthcare Workers East.

Leading up to Monday’s filing, state and federal lawmakers were increasingly worried about how a bankruptcy at the largest physician-led hospital operator in the country would impact access to care.

Regulators in Massachusetts — where Steward operates eight hospitals — held closed-door strategy sessions to map out contingency in case of a bankruptcy, and workers staged rallies to protest possible hospital closures.

Steward provides care for more than 2 million patients each year across 31 hospitals and 400 facility locations, according to bankruptcy filings. The company also employs nearly 30,000 employees across its eight-state portfolio, including 4,500 primary and specialty care physicians.

Steward’s first-day bankruptcy motions shed light on the operator’s future — and outlines its strategy for paying down its massive debt by selling assets. Here are the biggest takeaways.

Steward’s sprawling debt

Steward has earned a reputation for being cagey about its finances — to the dismayof Massachusetts Gov. Maura Healey, who accused the company of operating in a “black box” in a letter to its CEO earlier this year.

The operator has refused to file routine finances with Massachusetts regulators for years, citing a need to protect confidential business data. Even as the company shutteredhospitals this winter, regulators said Steward still dragged its feet on providing financial data, frustrating policymakers’ efforts to build out contingency plans.

“One of the good things about bankruptcy is that Steward and its CEO … will no longer be able to lie,” said Healey during a press conference Monday morning. “Transparency is really important here, and that’s why you know we’re looking forward to seeing what is in the various documents … We need clarity about debts and liabilities.”

In a slew of first-day motions, Steward now revealed it owes around $1.2 billion in total loan debts and about $6.6 billion in long-term lease payments.

Steward owes north of $600 million to 30 of its largest lenders, which include UnitedHealth-owned Change Healthcare, Philips North America LLC, Medline Industries, AYA Healthcare and Cerner.

The healthcare operator owes $289.8 million in unpaid compensation obligations, including $68 million to its own workers in unpaid employee salaries, $105.6 million in payments for physician services and $47.7 million owed to staffing agencies.

It also has approximately $979.4 million outstanding in trade obligations, of which approximately 70% are over 120 days past due.

Though Steward had a consortium of six private lenders financing its asset-based loans this year, now only one lender is listed in bankruptcy filings as funding its debtor-in-possession financing: its landlord, Medical Properties Trust.

The change in vendors is notable, according to Laura Coordes, professor of law at the Sandra Day O’Connor College of Law at Arizona State University.

“Something went on to get these other lenders to drop out,” she said.

The landlord may be opting to fund Steward during bankruptcy proceedings in hopes of getting its own money back more expediently, according to Coordes.

Steward is MPT’s largest tenant and the healthcare network will owe MPT at least $6.9 billion in debt and lease obligations by 2041, according to the filings.

During Tuesday morning’s first day hearing a representative for Steward told Judge Chris Lopez that all of Steward’s 31 hospitals are for sale. But to receive the $225 million from MPT, Steward has to hit aggressive sales milestones. It must host an auction for all non-Florida hospitals by June 28 and all Florida properties by July 30.

Since February, MPT executives have said there is strong interest from buyers in taking over Steward leases. However, Steward has yet to sell a hospital.

Experts have told Healthcare Dive they’re skeptical other operators would take on Steward’s leases at MPT’s current rental rates.

“Given the unaffordability of the leases and given that it hasn’t worked in the past, I do think that really material rent concessions are going to be needed to get this done,” said Rob Simone, sector head of real estate investment trusts at analyst firm Hedgeye.

Steward also signed a letter of intent to sell its physician group, Stewardship Health, to UnitedHealth. Although the deal was first announced in March, regulators have not yet begun reviewing the deal, according to David Seltz, executive director of the Massachusetts Health Policy Commission. Seltz said missing paperwork is delaying the review.

The Stewardship deal is not tied to further funding. A representative from UnitedHealth declined to comment on the pending deal and whether the bankruptcy proceeding would impact the sale.

Future of Steward

Employees have received conflicting messages about the future of Steward hospitals.

On one hand, both de la Torre and Massachusetts officials said Monday that Steward hospitals would remain open this week. However, Healey also emphasized that she wants Steward out of the state.

“Ultimately, [bankruptcy] is a step toward our goal of getting Steward out of Massachusetts,” Healey said during a press conference Monday.

Some Steward facilities may wind down during the bankruptcy proceedings, said Massachusetts Attorney General Andrea Campbell. Her office will oversee that process closely, and Steward will be required to provide licensing and notice obligations.

A healthcare worker at Steward’s Nashoba Valley Hospital told Healthcare Dive Monday she’s particularly concerned about the fate of her facility, which she says serves 14 communities but is small compared to some other hospitals in Steward’s portfolio. She doesn’t want regulators to forget about Nashoba.

“What I’m hoping for is that our state representatives and our local representatives really push to keep the hospital open,” she said. “But my concern is we get overlooked.”

State officials said they would continue monitoring Steward facilities to ensure quality care and push for the appointment of a patient care ombudsman to represent the interests of patients and employees during bankruptcy proceedings. Officials have already launched a website to offer resources about the bankruptcy process.

Still, employees are unsure of the path forward.

The Nashoba Valley Hospital employee told Healthcare Dive they’re conflicted about whether to stay at the hospital they’ve worked at for years or try to find a new position while they can.

“I’ve used the hospital since I moved out here. I’ve been living out in this area for like 25 years … I’ve brought my mother to this hospital,” the worker said. “It’s my hospital. It’s not just where I work. It’s what I use, and it’s vitally important to the community.”

Since 2022, S&P Global Ratings has tracked an increase in violations of debt agreements as macro economic pressures and low operating margins challenge providers.

Dive Brief:

The number of nonprofit health systems violating their financial agreements with lenders or investors has increased since 2022 as providers struggle to meet debt obligations amid challenging operating conditions, according to a new report from credit agency S&P Global Ratings.

This year, nonprofits will continue to be at heightened risk of violating covenant agreements, or conditions of debt that are put in place by lenders. Recently, the most common violations among nonprofits have been debt service coverage — the amount of days-cash-on-hand to debt ratios — as the sector continues to weather high expenses and weak revenues.

Most nonprofits have recently received extra time to remedy finances in the form of waivers or forbearance agreements, but other systems have merged with more financially stable organizations to meet lending agreements, according to the report.

Dive Insight:

Financial covenant violations among nonprofits began to increase at the onset of the COVID-19 pandemic.

In the early stages of the pandemic, violations were often tied to one-time pressures on operating income, such as mandatory stoppages of services.

However, violations have since evolved and now reflect nonprofits’ struggles with ongoing labor shortages and inflationary pressures, according to the report.

Providers in the speculative rating category were more likely to have violated financial covenants over the past two years and accounted for 60% of violations in S&P’s rated universe.

Long-term debt has long been a staple in healthcare, but many hospitals and health systems are responding to the increasing cost of debt and debt service in the rising rates environment.

Highly levered health systems are looking to sell hospitals, facilities or business lines to reduce their debt leverage and secure long-term sustainability, which creates significant growth opportunities for systems with balance sheets on a more solid financial footing.

Forty-three health systems ranked by their long-term debt:

Note: This is not an exhaustive list. The following long-term debt figures are taken from each health system’s most recent financial report.

Earlier this month, leaders from more than 400 organizations descended on San Francisco for J.P. Morgan‘s 42nd annual healthcare conference to discuss some of the biggest issues in healthcare today. Here’s how Advisory Board experts are thinking about Modern Healthcare’s 10 biggest takeaways — and our top resources for each insight.

How we’re thinking about the top 10 takeaways from JPM’s annual healthcare conference

Following the conference, Modern Healthcare provided a breakdown of the top-of-mind issues attendees discussed.

Here’s how our experts are thinking about the top 10 takeaways from the conference — and the resources they recommend for each insight.

1. Ambulatory care provides a growth opportunity for some health systems

By Elizabeth Orr, Vidal Seegobin, and Paul Trigonoplos

At the conference, many health system leaders said they are evaluating growth opportunities for outpatient services.

However, results from our Strategic Planner’s Survey suggest only the biggest systems are investing in building new ambulatory facilities. That data, alongside the high cost of borrowing and the trifurcation of credit that Fitch is predicting, suggests that only a select group of health systems are currently poised to leverage ambulatory care as a growth opportunity.

Systems with limited capital will be well served by considering other ways to reach patients outside the hospital through virtual care, a better digital front door, and partnerships. The efficiency of outpatient operations and how they connect through the care continuum will affect the ROI on ambulatory investments. Buying or building ambulatory facilities does not guarantee dramatic revenue growth, and gaining ambulatory market share does not always yield improved margins.

While physician groups, together with management service organizations, are very good at optimizing care environments to generate margins (and thereby profit), most health systems use ambulatory surgery center development as a defensive market share tactic to keep patients within their system.

This approach leaves margins on the table and doesn’t solve the growth problem in the long term. Each of these ambulatory investments would do well to be evaluated on both their individual profitability and share of wallet.

On January 24 and 25, Advisory Board will convene experts from across the healthcare ecosystem to inventory the predominant growth strategies pursued by major players, explore considerations for specialty care and ambulatory network development, understand volume and site-of-care shifts, and more. Register here to join us for the Redefining Growth Virtual Summit.

Also, check out our resources to help you plan for shifts in patient utilization:

2. Rebounding patient volumes further strain capacity

By Jordan Peterson, Eliza Dailey, and Allyson Paiewonsky

Many health system leaders noted that both inpatient and outpatient volumes have surpassed pre-pandemic levels, placing further strain on workforces.

The rebound in patient volumes, coupled with an overstretched workforce, underscores the need to invest in technology to extend clinician reach, while at the same time doubling down on operational efficiency to help with things like patient access and scheduling.

For leaders looking to leverage technology and boost operational efficiency, we have a number of resources that can help:

3. Health systems aren’t specific on AI strategies

By Paul Trigonoplos and John League

According to Modern Healthcare, nearly all health systems discussed artificial intelligence (AI) at the conference, but few offered detailed implementation plans and expectations.

Over the past year, a big part of the work for Advisory Board’s digital health and health systems research teams has been to help members reframe the fear of missing out (FOMO) that many care delivery organizations have about AI.

We think AI can and will solve problems in healthcare. Every organization should at least be observing AI innovations. But we don’t believe that “the lack of detail on healthcare AI applications may signal that health systems aren’t ready to embrace the relatively untested and unregulated technology,” as Modern Healthcare reported.

The real challenge for many care delivery organizations is dealing with the pace of change — not readiness to embrace or accept it. They aren’t used to having to react to anything as fast-moving as AI’s recent evolution. If their focus for now is on low-hanging fruit, that’s completely understandable. It’s also much more important for these organizations to spend time now linking AI to their strategic goals and building out their governance structures than it is to be first in line with new applications.

Check out our top resources for health systems working to implement AI:

Digital health companies like Teladoc, R1 RCM, Veradigm, and Talkspace all spoke out about their use of generative AI.

This does not surprise us at all. In fact, we would be more surprised if digital health companies were not touting their AI capabilities. Generative AI’s flexibility and ease of use make it an accessible addition to nearly any technology solution.

However, that alone does not necessarily make the solution more valuable or useful. In fact, many organizations would do well to consider how they want to apply new AI solutions and compare those solutions to the ones that they would have used in October 2022 — before ChatGPT’s newest incarnation was unveiled. It may be that other forms of AI, predictive analytics, or robotic process automation are as effective at a better cost.

Again, we believe that AI can and will solve problems in healthcare. We just don’t think it will solve every problem in healthcare, or that every solution benefits from its inclusion.

During the conference, providers criticized insurers for the rate of denials, Modern Healthcare reports.

Denials — along with other utilization management techniques like prior authorization — continue to build tension between payers and providers, with payers emphasizing their importance for ensuring cost effective, appropriate care and providers overwhelmed by both the administrative burden and the impact of denials on their finances.

Many health plans have announced major moves to reduce prior authorizations and CMS recently announced plans to move forward with regulations to streamline the prior authorization process. However, these efforts haven’t significantly impacted providers yet.

In fact, most providers report no decrease in denials or overall administrative burden. A new report found that claims denials increased by 11.99% in the first three quarters of 2023, following similar double digit increases in 2021 and 2022.

Our team is actively researching the root cause of this discrepancy and reasons for the noted increase in denials. Stay tuned for more on improving denials performance — and the broader payer-provider relationship — in upcoming 2024 Advisory Board research.

For now, check out this case study to see how Baptist Health achieved a 0.65% denial write-off rate.

6. Insurers are prioritizing Star Ratings and risk adjustment changes

By Mallory Kirby

Various insurers and providers spoke about “the fallout from star ratings and risk adjustment changes.”

2023 presented organizations focused on MA with significant headwinds. While many insurers prioritized MA growth in recent years, leaders have increased their emphasis on quality and operational excellence to ensure financial sustainability.

With an eye on these headwinds, it makes sense that insurers are upping their game to manage Star Ratings and risk adjustment. While MA growth felt like the priority in years past, this focus on operational excellence to ensure financial sustainability has become a priority.

We’ve already seen litigation from health plans contesting the regulatory changes that impact the bottom line for many MA plans. But with more changes on the horizon — including the introduction of the Health Equity Index as a reward factor for Stars and phasing in of the new Risk Adjustment Data Validation model — plans must prioritize long-term sustainability.

Check out our latest MA research for strategies on MA coding accuracy and Star Ratings:

Pharmacy benefit manager (PBM) leaders discussed the ways they are preparing for potential congressional action, including “updating their pricing models and diversifying their revenue streams.”

Healthcare leaders should be prepared for Congress to move forward with PBM regulation in 2024. A final bill will likely include federal reporting requirements, spread pricing bans, and preferred pricing restrictions for PBMs with their own specialty pharmacy. In the short term, these regulations will likely apply to Medicare and Medicaid population benefits only, and not the commercial market.

Congress isn’t the only entity calling for change. Several states passed bills in the last year targeting PBM transparency and pricing structures. The Federal Trade Commission‘s ongoing investigation into select PBMs looks at some of the same practices Congress aims to regulate. PBM commercial clients are also applying pressure. In 2023, Blue Cross Blue Shield of California‘s (BSC) decided to outsource tasks historically performed by their PBM partner. A statement from BSC indicated the change was in part due to a desire for less complexity and more transparency.

Here’s what this means for PBMs:

Transparency is a must

The level of scrutiny on transparency will force the hand of PBMs. They will have to comply with federal and state policy change and likely give something to their commercial partners to stay competitive. We’re already seeing this unfold across some of the largest PBMs. Recently, CVS Caremarkand Express Scripts launched transparent reimbursement and pricing models for participating in-network pharmacies and plan sponsors.

While transparency requirements will be a headache for larger PBMs, they might be a real threat to smaller companies. Some small PBMs highlight transparency as their main value add. As the larger PBMs focus more on transparency, smaller PBMs who rely on transparent offerings to differentiate themselves in a crowded market may lose their main competitive edge.

PBMs will have to try new strategies to boost revenue

PBM practice of guiding prescriptions to their own specialty pharmacy or those providing more competitive pricing is a key strategy for revenue. Stricter regulations on spread pricing and patient steerage will prompt PBMs to look for additional revenue levers.

PBMs are already getting started — with Express Scripts reporting they will cut reimbursement for wholesale brand name drugs by about 10% in 2024. Other PBMs are trying to diversify their business opportunities. For example, CVS Caremark’s has offered a new TrueCost model to their clients for an additional fee. The model determines drug prices based on the net cost of drugs and clearly defined fee structures. We’re also watching growing interest in cross-benefitutilization management programs for specialty drugs. These offerings look across both medical and pharmacy benefits to ensure that the most cost-effective drug is prescribed for patients.

At the conference, retailers such as CVS, Walgreens, and Amazon doubled down on their healthcare services strategies.

Typically, disruptors do not get into care delivery because they think it will be easy. Disruptors get into care delivery because they look at what is currently available and it looks so hard — hard to access, hard to understand, and hard to pay for.

Many established players still view so-called disruptors as problematic, but we believe that most tech companies that move into healthcare are doing what they usually do — they look at incumbent approaches that make it hard for customers and stakeholders to access, understand, and pay for care, and see opportunities to use technology and innovative business models in an attempt to target these pain points.

CVS, Walgreens, and Amazon are pursuing strategies that are intended to make it more convenient for specific populations to get care. If those efforts aren’t clearly profitable, that does not mean that they will fail or that they won’t pressure legacy players to make changes to their own strategies. Other organizations don’t have to copy these disruptors (which is good because most can’t), but they must acknowledge why patient-consumers are attracted to these offerings.

For more information on how disruptors are impacting healthcare, check out these resources:

9. Financial pressures remain for many health systems

By Vidal Seegobin and Marisa Nives

Health systems are recovering from the worst financial year in recent history. While most large health systems presenting at the conference saw their finances improve in 2023, labor challenges and reimbursement pressures remain.

We would be remiss to say that hospitals aren’t working hard to improve their finances. In fact, operating margins in November 2023 broke 2%. But margins below 3% remain a challenge for long-term financial sustainability.

One of the more concerning trends is that margin growth is not tracking with a large rebound in volumes. There are number of culprits: elevated cost structures, increased patient complexity, and a reimbursement structure shifting towards government payers.

For many systems, this means they need to return to mastering the basics: Managing costs, workforce retention, and improving quality of care. While these efforts will help bridge the margin gap, the decoupling of volumes and margins means that growth for health systems can’t center on simply getting bigger to expand volumes.

Maximizing efficiency, improving access, and bending the cost curve will be the main pillars for growth and sustainability in 2024.

To learn more about what health system strategists are prioritizing in 2024, read our recent survey findings.

Also, check out our resources on external partnerships and cost-saving strategies:

During the conference, MA insurers reported seeing a spike in utilization driven by increased doctor’s visits and elective surgeries.

These increased medical expenses are putting more pressure on MA insurers’ margins, which are already facing headwinds due to CMS changes in MA risk-adjustment and Star Ratings calculations.

However, this increased utilization isn’t all bad news for insurers. Part of the increased utilization among seniors can be attributed to more preventive care, such as an uptick in RSV vaccinations.

In UnitedHealth Group‘s* Q4 earnings call, CFO John Rex noted that, “Interest in getting the shot, especially among the senior population, got some people into the doctor’s office when they hadn’t visited in a while,” which led to primary care physicians addressing other care needs. As seniors are referred to specialty care to address these needs, plans need to have strategies in place to better manage their specialist spend.

Three Philadelphia-based hospitals are reportedly up for sale, according to an email notice from Los Angeles-based investment bank Xnergy, The Philadelphia Inquirer reported Dec. 19.

The names of three hospitals are not confirmed. And the notice, which was obtained by the publication, did not name an owner of the hospitals. However, it did describe the hospitals’ owner as one that has acute care facilities with an average of 136 beds.

Three Philadelphia-area hospitals fit the bed parameters in the notice: Bristol-based Lower Bucks Hospital, Philadelphia-based Roxborough Memorial Hospital, and Norristown-based Suburban Community Hospital. All three are owned by Ontario, Calif.-based Prime Healthcare Services, The Philadelphia Inquirer reported.

Roxborough and Lower Bucks were acquired by Prime in 2012, with Suburban acquired by Prime’s nonprofit affiliate Prime Healthcare Foundation in 2016. The hospitals have also seen significant annual operating loss over the last five years with a 43% combined inpatient volume drop, from 3,795 discharges in 2018 to 2,250 discharges in 2022, the publication shared.

Members of the Pennsylvania Association of Staff Nurses & Allied Professionals at both Suburban and Lower Bucks are also set to launch five-day strikes Dec. 22 due to ongoing labor contract negotiations for things like increased wages and important benefits, a union spokesperson told Becker’s.

“Prime Healthcare’s mission is to always do what’s best for our communities and patients, however, we do not comment on strategic merger and acquisition initiatives,” Elizabeth Nikels, vice president of communications and public relations for Prime Healthcare, said in an email response to Becker’s regarding the sale.

StoneBridge Healthcare, a hospital turnaround firm, is looking to enter a management contract with Delaware-based WoodBridge, a nonprofit organization, to acquire West Reading, Pa.-based Tower Health for $706 million, the Philadelphia Business Journal reported Dec.12.

WoodBridge, a sister organization to StoneBridge, was expected to share a nonbinding agreement in principle with Tower Health on Dec. 12, which includes the intent to purchase the system’s assets, the publication reported.

An initial cash payment of $550 million, including the assumption of finance leases with liabilities of $156 million, and a commitment of hiring nearly all the system’s 11,000 employees are featured in the proposed deal.

Tower Health operates Reading Hospital, Pottstown Hospital and Phoenixville Hospital. St. Christopher’s Hospital for Children in Philadelphia is also under the system in partnership with Drexel University.

If all goes well, the plan would involve StoneBridge negotiating a management agreement with WoodBridge, Joshua Nemzoff, founder and CEO of StoneBridge, told the Journal. However, Mr. Nemzoff said WoodBridge is only interested in acquiring the Reading, Pottstown and Phoenixville hospitals.

This is not the first time that StoneBridge has attempted to acquire the system. Last November, the firm offered Tower Health $675 million, which was turned down. StoneBridge, in partnership with Allentown, Pa.-based Lehigh Valley Health Network, also made two conditional offers in 2021 to acquire the system’s assets for $600 million, which were also declined.

Formed in 2020, StoneBridge’s mission is to purchase and turn around acute care hospitals that are in significant economic distress. The firm currently does not own or operate any hospitals. Like StoneBridge, WoodBridge also hasn’t completed hospital deals, and will have its own separate board of directors, the publication reported.

Becker’s has reached out to StoneBridge Healthcare and Tower Health for comments on the potential acquisition.

West Reading, Pa.-based Tower Health continues to make progress on its performance improvement plan as its operating margin for the three months ended Sept. 30 rose to -4.2% from -8% during the same period in 2022. Its operating cash flow margin also increased from -0.9% to 2.3%.

During the first quarter of fiscal 2024, the three months ending Sept. 30, revenue decreased 2.9% year over year to $457.4 million. Expenses decreased 6.4% to $476.5 million.

Tower’s operating loss for the period was $19.1 million, compared with a loss of $37.6 million for the prior-year period.

As of Sept. 30, total balance sheet unrestricted cash and board-designated investment funds for capital improvements totalled $154 million — a decrease of $54 million from June 30, 2023. The main factors for the decrease were $15 million of debt service payments, physician incentive compensation payments of $9 million, capital expenditures of $6 million, negative changes in working capital of $32 million, partially offset by EBITDA of $10 million.

Total days of cash on hand for the system was 30 on Sept. 30.

After including the performance of its investment portfolio and other nonoperating items, the health system ended the three-month period with a net loss of $20.9 million, compared with a net loss of $37.6 million for the same period in 2022.