Two newly published investigative reports, by the intrepid reporters at STAT News and The American Prospect, pull the curtains back a little more on the astonishing number of recent acquisitions UnitedHealth has made as it moves deeper and deeper into health care delivery, enabling it to grab ever-increasing chunks of our premium and tax dollars to reward its shareholders.

That’s a strategic move that allows the company to steer more seniors to facilities it owns, boosting revenues it gets from the government and padding its bottom line.

The bigger a company gets, the less it has to disclose about the acquisitions it makes in any easily obtainable way. That’s because publicly-traded companies are only required to immediately inform investors of individual deals that are “material to earnings.”

A material amount, as Investopedia explains, “can signify any sum or figure worth mentioning, as in account balances, financial statements, shareholder reports, or conference calls. If something is not a material amount, it is considered too insignificant or trivial to mention.”

UnitedHealth’s long string of acquisitions in recent years has catapulted the company to the #5 spot on the Fortune 500 list of American companies, based on revenue. Only Walmart, Exxon Mobile, Amazon and Apple are bigger.

That rapid growth means that fewer and fewer of UnitedHealth’s acquisitions reach the threshold of requiring prominent disclosure to shareholders.

It was only through a close review of UnitedHealth’s latest annual report to investors and other financial documents that STAT was able to see what the company hides from most of us. As Herman noted:

UnitedHealth Group is so big that it doesn’t have to publicly announce a vast majority of its acquisitions. But a STAT analysis of company financial documents shows the health care conglomerate quietly acquired dozens of outpatient facilities in 2023, with a particular focus on surgery centers.

And it’s not adding random surgery centers, either. There seems to be an explicit strategy: Many of UnitedHealth’s new centers sit in geographic areas where the company is the biggest Medicare Advantage player, based on the latest insurance market share data. That overlap reinforces how UnitedHealth is looking to funnel more of its insurance members toward providers that it owns, with the overarching goal of capturing more profit.

As an example, STAT said it stumbled upon an entry–”buried within UnitedHealth’s annual report”–that revealed the company’s previously undisclosed December acquisition of National Cardiovascular Partners, which operates 21 cardiac cath and vascular labs. Not coincidentally, NCP’s facilities are “in places like Phoenix and large metro areas in Texas where UnitedHealth has the biggest MA market share.”

Tkacik wrote that last Thursday, UnitedHealthcare applied for an emergency exemption that would fast-track its takeover of a medical practice in Corvallis, Oregon, which is facing the prospect of closing its doors because of the financial crunch caused by the hack. As Tkacik explained, the hack interrupted the flow of information from Change Healthcare’s claims processing systems that enables physicians, hospitals, and other health care providers to get paid.

Perversely, UnitedHealth is telling Oregon regulators that the best solution is to allow the company’s proposed acquisition of the medical practice to go forward.

Tkacik reported that:

Although the specific reason for the exemption request is redacted from the publicly posted version of the application, a clinic insider says the “emergency” is the same one that has plunged thousands of other health providers across the nation into a terrifying cash crunch…

The situation underscores the perverse state of affairs in which UnitedHealth, which comprises some 2,642 separate companies that collectively raked in $371.6 billion last year, has arguably profited from the desperation that the hacking of its Change computer systems in late February has inflicted upon the health care system.

An estimated half of all health care transactions are processed or somehow otherwise touched by Change, a rollup of dozens of health care technology firms that provide 137 software applications that have been affected by the outage.

Tkacid added that “Every dollar in revenue that has disappeared from hospitals, medical practices, and pharmacies in the aftermath of the outage corresponds to an extra dollar sitting in the coffers of the nation’s health insurers, so UnitedHealth, which pays out roughly $662 million in medical claims each day, is presumably sitting on a mountain of unexpected cash.”

Tuesday, the, FTC, and DOJ announced creation of a task force focused on tackling “unfair and illegal pricing” in healthcare. The same day, HHS joined FTC and DOJ regulators in launching an investigation with the DOJ and FTC probing private equity’ investments in healthcare expressing concern these deals may generate profits for corporate investors at the expense of patients’ health, workers’ safety and affordable care.

Thursday’s State of the Union address by President Biden (SOTU) and the Republican response by Alabama Senator Katey Britt put the spotlight on women’s reproductive health, drug prices and healthcare affordability.

Friday, the Senate passed a $468 billion spending bill (75-22) that had passed in the House Wednesday (339-85) averting a government shutdown. The bill postpones an $8 billion reduction in Medicaid disproportionate share hospital payments for a year, allocates $4.27 billion to federally qualified health centers through the end of the year and rolls back a significant portion of a Medicare physician pay cut that kicked in on Jan. 1. Next, Congress must pass appropriations for HHS and other agencies before the March 22 shutdown.

And all week, the cyberattack on Optum’s Change Healthcare discovered February 21 hovered as hospitals, clinics, pharmacies and others scrambled to manage gaps in transaction processing. Notably, the American Hospital Association and others have amplified criticism of UnitedHealth Group’s handling of the disruption, having, bought Change for $13 billion in October, 2022 after a lengthy Department of Justice anti-trust review. This week, UHG indicates partial service of CH support will be restored. Stay tuned.

Just another week for healthcare: Congressional infighting about healthcare spending. Regulator announcements of new rules to stimulate competition and protect consumers in the healthcare market. Lobbying by leading trade groups to protect funding and disable threats from rivals. And so on.

At the macro level, it’s understandable: healthcare is an attractive market, especially in its services sectors. Since the pandemic, prices for services (i.e. physicians, hospitals et al) have steadily increased and remain elevated despite the pressures of transparency mandates and insurer pushback. By contrast, prices for most products (drugs, disposables, technologies et al) have followed the broader market pricing trends where prices for some escalated fast and then dipped.

While some branded prescription medicines are exceptions, it is health services that have driven the majority of health cost inflation since the pandemic.

UnitedHealth Group’s financial success is illustrative:

it’s big, high profile and vertically integrated across all major services sectors. In its year end 2023 financial report (January 12, 2024) it reported revenues of $371.6 Billion (up 15% Year-Over-Year), earnings from operations up 14%, cash flows from operations of $29.1 Billion (1.3x Net Income), medical care ratio at 83.2% up from 82% last year, net earnings of $23.86/share and adjusted net earnings of $25.12/share and guidance its 2024 revenues of $400-403 billion. They buy products using their scale and scope leverage to pay less for services they don’t own less and products needed to support them. It’s a big business in a buyer’s market and that’s unsettling to many.

Big business is not new to healthcare:

it’s been dominant in every sector but of late more a focus of unflattering regulator and media attention. Coupled with growing public discontent about the system’s effectiveness and affordability, it seems it’s near a tipping point.

David Johnson, one of the most thoughtful analysts of the health industry, reminded his readers last week that the current state of affairs in U.S. healthcare is not new citing the January 1970 Fortune cover story “Our Ailing Medical System”

“American medicine, the pride of the nation for many years, stands now on the brink of chaos. To be sure, our medical practitioners have their great moments of drama and triumph. But much of U.S. medical care, particularly the everyday business of preventing and treating routine illnesses, is inferior in quality, wastefully dispensed, and inequitably financed…

Whether poor or not, most Americans are badly served by the obsolete, overstrained medical system that has grown up around them helter-skelter. … The time has come for radical change.”

Johnson added: “The healthcare industry, however, cannot fight gravity forever. Consumerism, technological advances and pro-market regulatory reforms are so powerful and coming so fast that status-quo healthcare cannot forestall their ascendance. Properly harnessed, these disruptive forces have the collective power necessary for U.S. healthcare to finally achieve the 1970 Fortune magazine goal of delivering “good care to every American with little increase in cost.”

He’s right.

I believe the U.S. health system as we know it has reached its tipping point. The big-name organizations in every sector see it and have nominal contingency plans in place; the smaller players are buying time until the shoe drops. But I am worried.

I am worried the system’s future is in the hands of hyper-partisanship by both parties seeking political advantage in election cycles over meaningful creation of a health system that functions for the greater good.

I am worried that the industry’s aversion toprice transparency, meaningful discussion about affordability and consistency in defining quality, safety and value will precipitate short-term gamesmanship for reputational advantage and nullify systemness and interoperability requisite to its transformation.

I am worried that understandably frustrated employers will drop employee health benefits to force the system to needed accountability.

I am worried that the growing armies of under-served and dissatisfied populations will revolt.

I am worried that its workforce is ill-prepared for a future that’s technology-enabled and consumer centric.

I am worried that the industry’s most prominent trade groups are concentrating more on “warfare” against their rivals and less about the long-term future of the system.

I am worried that transformational change is all talk.

It’s time to start an adult conversation about the future of the system. The starting point: acknowledging that it’s not about bad people; it’s about systemic flaws in its design and functioning. Fixing it requires balancing lag indicators about its use, costs and demand with assumptions about innovations that hold promise to shift its trajectory long-term. It requires employers to actively participate: in 2009-2010, Big Business mistakenly chose to sit out deliberations about the Affordable Care Act. And it requires independent, visionary facilitation free from bias and input beyond the DC talking heads that have dominated reform thought leadership for 6 decades.

Or, collectively, we can watch events like last week’s roll by and witness the emergence of a large public utility serving most and a smaller private option for those that afford it. Or something worse.

P.S. Today, thousands will make the pilgrimage to Orlando for HIMSS24 kicking off with a keynote by Robert Garrett, CEO of Hackensack Meridian Health tomorrow about ‘transformational change’ and closing Friday with a keynote by Nick Saban, legendary Alabama football coach on leadership. In between, the meeting’s 24 premier supporters and hundreds of exhibitors will push their latest solutions to prospects and customers keenly aware healthcare’s future is not a repeat of its past primarily due to technology. Information-driven healthcare is dependent on technologies that enable cost-effective, customized evidence-based care that’s readily accessible to individuals where and when they want it and with whom.

And many will be anticipating HCA Mission Health’s (Asheville NC) Plan of Action response due to CMS this Wednesday addressing deficiencies in 6 areas including CMS Deficiency 482.12 “which ensures that hospitals have a responsible governing body overseeing critical aspects of patient care and medical staff appointments.” Interest is high outside the region as the nation’s largest investor-owned system was put in “immediate jeopardy” of losing its Medicare participation status last year at Mission. FYI: HCA reported operating income of $7.7 billion (11.8% operating margin) on revenues of $65 billion in 2023.

Former New York Jets superstar Joe Namath can be seen every year during Medicare open enrollment hocking plans that tell seniors how great their life would be if only they signed up for a Medicare Advantage plan. From October 15 to December 7 last year alone, Joe Namath ads ran 3,670 times, according to iSpot, which tracks TV advertising.

But the company behind those ads, now called Blue Lantern Health, and their products, HealthInsurance.com and the Medicare Coverage Helpline, have an expansive rap sheet of misconduct, including prosecutions by the Securities and Exchange Commission and the Federal Trade Commission, and a recent bankruptcy filing that critics say is designed to jettison the substantial legal liabilities the firm has incurred. In September 2023, the company became Blue Lantern; before that, it was called Benefytt; and before that, Health Insurance Innovations. Forty-three state attorneys general had settled with the company in 2018, with it paying a $3.4 million fine. A close associate of the company, Steven Dorfman, has also been prosecuted by the FTC, in addition to the Department of Justice.

Namath himself has a bit of a checkered past when it comes to his business associates—in the early 1970s, he co-owned a bar frequented by members of the Colombo and Lucchese crime families, according to reporting at the time cited in a 2004 biography. Due to the controversy surrounding the bar, Namath was forced by the NFL Commissioner to sell his interest in it. Last year, it was revealed that Namath had employed a prolific pedophile coach at his football camp, also in the 1970s, and the 80-year-old ex-quarterback is now being sued by one of the coach’s victims.

The Namath ads are the main illustration of the behemoth Medicare Advantage marketing industry, which is designed to herd seniors into Medicare Advantage plans that restrict the doctors and hospitals that seniors can go to and the procedures they can access through the onerous “prior authorization” process, and it costs the federal government as much as $140 billion annually compared to traditional Medicare. Over half of seniors—nearly 31 million people—are now in Medicare Advantage, and there is little understanding of the drawbacks of the program. Seniors are aware that they may receive modest gym or food benefits but typically do not realize that they may be giving up their doctors, their specialists, their outpatient clinics, and their hospitals in favor of an in-network alternative that may be lower quality and farther away.

How so many seniors are lured into Medicare Advantage

Blue Lantern—with its powerful private equity owner Madison Dearborn—may be the key to understanding how so many people have been ushered into Medicare Advantage—and the pitfalls that private equity’s rapid entrance into health care can create for ordinary Americans.

While Blue Lantern is just one company, it is a Rosetta Stone for everything that is wrong with American health care today—fraud, profiteering, lawbreaking, no regard for patient care—where only the public comes out the loser.

Blue Lantern uses TV ads and, at least until regulators began poking around, a widespread telemarketing operation, being one of the main firms charged with generating “leads” that are then sold to brokers and insurers, as Medicare Advantage plans are banned from cold-calling. Court filings reviewed by HEALTH CARE Un-Covered allege that after legal discovery, Blue Lantern (then known as Benefytt) at minimum dialed seniors over 17 million times, potentially in violation of federal law that requires telemarketers to properly identify themselves and who they are working for—ultimately, in this case, insurers that generate huge profits from Medicare Advantage.

The Namath ads have been running since 2018 when the company was named Health Insurance Innovations—the same year the FTC began prosecuting Simple Health Plans, along with its then-CEO Steven Dorfman. The Fort Lauderdale Sun-Sentinel identified Health Insurance Innovations as a “successor” to Simple Health Plans. After five years of likely exceptionally costly litigation, for which Dorfman is represented by jet-set law firm DLA Piper, on February 9, the FTC won a $195 million judgment against Simple Health Plans and Dorfman. The FTC alleged in 2019 that Dorfman had lied to the court when he said that he did not control any offshore accounts. The FTC found $20 million, but the real number is probably higher.

Friends in high places

In February 2020, Trump’s Secretary of Health and Human Services, Alex Azar, said that the Namath ads might not “look or sound like the future of health care,” but that they represented “real savings, real options” for older Americans.

In March 2020, Health Insurance Innovations (HII) changed its name to Benefytt, and in August 2020, it was acquired by Madison Dearborn Partners. Madison Dearborn has close ties to the Illinois Democratic elite, pumping over $916,000 into U.S. Ambassador to Japan Rahm Emanuel’s campaigns for Congress and mayor of Chicago.

In September 2021, HII settled a $27.5 million class action lawsuit. The 230,000 victims received an average payout of just $80.

In July 2022, the SEC charged HII/Benefytt and its then-CEO Gavin Southwell with making fraudulent representations to investors about the quality of the health plans it was marketing. “HII and Southwell…told investors in earnings calls and investor presentations that HII’s consumer satisfaction was 99.99 percent and state insurance regulators received very few consumer complaints regarding HII. In reality, HII tracked tens of thousands of dissatisfied consumers who complained that HII’s distributors made misrepresentations to sell the health insurance products, charged consumers for products they did not authorize and failed to cancel plans upon consumers’ requests,” the SEC found, with HII/Benefytt and Southwell ultimately paying a $12 million settlement in November 2022.

By August 2022, Benefytt had paid $100 million to settle allegations that it had fraudulently directed people into “sham” health care plans. “Benefytt pocketed millions selling sham insurance to seniors and other consumers looking for health coverage,” the FTC’s Director of Consumer Protection, Samuel Levine, said at the time.

Bankruptcy and another name change

In May 2023, Benefytt declared Chapter 11 bankruptcy—where the company seeks to continue to exist as a going concern, as opposed to Chapter 9, when the company is stripped apart for creditors—in the Southern District of Texas. The plan of bankruptcy was approved in August. The Southern Texas Bankruptcy Court has been mired in controversy in recent months as one of the two judges was revealed to be in a romantic relationship with a woman employed by a firm, Jackson Walker, that worked in concert with the major Chicago law firm Kirkland and Ellis to move bankruptcy cases to Southern Texas and monopolize them under a friendly court. While the other judge on the two-judge panel handled the Benefytt case, Jackson Walker and Kirkland and Ellis were retained by Benefytt, and the fees paid to Jackson Walker by Benefytt were delayed by the court as a result of the controversy.

In September 2023, Benefytt exited bankruptcy and became Blue Lantern.

The August approval of the bankruptcy plan was vocally opposed by a group of creditors who had sued Benefytt over violations of the Telephone Consumer Privacy Act (TCPA). The creditors asserted that Benefytt had substantial liabilities, with millions of calls made where Benefytt did not identify the ultimate seller—Medicare Advantage plans run by UnitedHealth, Humana, and other firms prohibited from directly contacting people they have no relationship with—and violations fined at $1,500 per willful violation.

Attorneys for those creditors stated in a filing reviewed by HEALTH CARE Un-Covered that Madison Dearborn always planned “to steer Benefytt into bankruptcy,” if they were unable to resolve the substantial liabilities they owed under the TCPA.

Madison Dearborn “knew that Benefytt’s TCPA liabilities exceeded its value, but purchased Benefytt anyway, for the purpose of trying to quickly extract as much money and value as they could before those liabilities became due,”

the August 25, 2023, filing stated on behalf of Wes Newman, Mary Bilek, George Moore, and Robert Hossfeld, all plaintiffs in proposed TCPA class action suits. The filing went on to say that the bankruptcy was inevitable “if—after siphoning off any benefit from the illegal telemarketing alleged herein—[Madison Dearborn] could not obtain favorable settlements or dismissals for the telemarketing-related lawsuits against Benefytt.”

Under the bankruptcy plan, Blue Lantern/Benefytt is released from the TCPA claims, but individuals harmed can affirmatively opt-out of the release, which is why the bankruptcy court justified its approval. Over 7 million people—the total numbers in Benefytt’s database, according to the plaintiffs—opting out of the third-party release is an enormous administrative hurdle for plaintiffs’ lawyers to pass, massively limiting the likelihood of success of any class-action litigation against Blue Lantern going forward.

Their attorney, Alex Burke, stated in court that “[t]his bankruptcy is an intentional and preplanned continuation of a fraud.” His statement was before 3,670 more Namath ads ran during 2023 open enrollment.

In response to requests for comment from HEALTH CARE un-covered, the Centers for Medicare and Medicaid Services did not answer questions about Benefytt and why the company was simply not barred from the Medicare Advantage market altogether.

Corporations have used the bankruptcy process in recent years to free themselves from criminal and civil liability, with opioid marketer Purdue Pharma being the most prominent recent example. The Supreme Court is reviewing the legality of Purdue’s third-party releases currently, with a decision expected in late spring.

The role that private equity plays in keeping Benefytt going cannot be overstated.

Without Madison Dearborn or another private equity firm eager to take on such a risky business with such a long history of legal imbroglios, it is almost certain that Benefytt would no longer exist—and the Joe Namath ads would disappear from our televisions. Instead, Madison Dearborn keeps them going, suckering seniors into Medicare Advantage plans.

This is part and parcel of the ongoing colonization by private equity into America’s health care system. Private equity is making a major play into Medicare Advantage.

It has pumped billions of dollars into purchasing hospitals. It has invested in hospice care. It is gobbling up doctors’ groups. It is acquiring ambulance companies. It is hoovering up nurse staffing firms. It is making huge investments into health tech. It is in nursing homes. And it is in health insurance. Nothing about America’s health care system is untouched by private equity.

That’s a problem, experts say.

“I’ve been screaming at the TV every time Joe Namath gets on—it is not an official Medicare website,” said Laura Katz Olson, a professor of political science at Lehigh University who has written on private equity’s role in the health care system.

“Private equity has so much money to deploy, which is far more than they have opportunities to buy. As such, they are desperately looking for opportunities to invest. There’s a lot of money in Medicare Advantage—it’s guaranteed money from the federal government, which makes it perfect for the private equity playbook.”

Eileen Appelbaum, the co-director at the Center for Economic and Policy Research, who has also studied private equity’s role in health care, concurred that private equity was a perfect fit for Medicare marketing organizations.

“I think basically the whole privatized Medicare situation is ready for all kinds of exploitation and misrepresentations and denying people the coverage that they need,” she said. “My email is inundated with these totally misleading ads. Private equity took a look at this and said, “look at that, it’s possible to do something that’s misleading and make a lot of money.”

Madison Dearborn receives a large portion of its capital from public pension funds like the California Public Employees Retirement System (CalPERS) and the Washington State Investment Fund—people who are dependent on Medicare. Appelbaum said that the pension funds exercise little oversight over their investments in private equity. “Pension funds may have the name of the company that they are invested in, they’re told that it’s ‘part of our health care investment portfolio,’ but they don’t find out what they really do until there’s a scandal.

It is amazing that pension funds give so much money to private equity with so little information about how their money is being spent.”

It’s no secret I feel strongly that “Medicare Advantage for All” is not a healthy end goal for universal health care coverage in our country. But I also recognize there are many folks, across the political spectrum, who see the program as one that has some merit. And it’s not going away anytime soon. To say the insurance industry has clout in Washington is an understatement.

As politicians in both parties increase their scrutiny of Medicare Advantage, and the Biden administration reviews proposed reforms to the program, I think it’s important to highlight common-sense, achievable changes with broad appeal that would address the many problems with MA and begin leveling the playing field with the traditional Medicare program.

1. Align prior authorization MA standards with traditional Medicare

Since my mother entered into an MA plan more than a decade ago, I’ve watched how health insurers have applied practices from traditional employer-based plans to MA beneficiaries. For many years, insurers have made doctors submit a proposed course of treatment for a patient to the insurance company for payment pre-approval — widely known as “prior authorization.”

While most prior authorization requests are approved, and most of those denied are approved if they are appealed, prior authorization accomplishes two things that increase insurers’ margins.

The practice adds a hurdle between diagnosis and treatment and increases the likelihood that a patient or doctor won’t follow through, which decreases the odds that the insurer will ultimately have to pay a claim. In addition, prior authorization increases the length of time insurers can hold on to premium dollars, which they invest to drive higher earnings. (A considerable percentage of insurers’ profits come from the investments they make using the premiums you pay.)

Last year, the Kaiser Family Foundation found the level of prior authorization requests in MA plans increased significantly in recent years, which is partially the result of the share of services subject to prior authorization increasing dramatically. While most requests were ultimately approved (as they were with employer-based insurance plans), the process delayed care and kept dollars in insurers’ coffers longer.

The outrage generated by older Americans in MA plans waiting for prior authorization approvals has moved the Biden administration to action.

Beginning in 2024, MA plans may be no more restrictive with prior authorization requirements than traditional Medicare.

That’s a significant change and one for which Health and Human Services Secretary Xavier Becerra should be lauded.

But as large provider groups like the American Hospital Association have pointed out, the federal government must remain vigilant in its enforcement of this rule. As I wrote about recently with the implementation of the No Surprises Act, well-intentioned legislation and implementation rules put in place by regulators can have little real-world impact if insurers are not held accountable. It’s important to note, though, that federal regulatory agencies must be adequately staffed and resourced to be able to police the industry and address insurers’ relentless efforts to find loopholes in federal policy to maximize profits. Congress needs to provide the Department of Health and Human Services with additional funding for enforcement activities, for HHS to require transparency and reporting by insurers on their practices, and for stakeholders, especially providers and patients, to have an avenue to raise concerns with insurers’ practices as they become apparent.

2. Protect seniors from marketing scams

If it’s fall, it’s football season. And that means it’s time for former NFL quarterback Joe Namath’s annual call to action on the airwaves for MA enrollment.

As Congresswoman Jan Schakowsky and I wrote about more than a year ago, these innocent-appearing advertisements are misleading at their best and fraudulent at their worst. Thankfully, this is another area the Biden administration has also been watching over the past year.

CMS now prohibits the use of ads that do not mention a specific plan name or that use the Medicare name and logos in a misleading way, the marketing of benefits in a service area where they are not available, and the use of superlatives (e.g., “best” or “most”) in marketing when not substantiated by data from the current or prior year.

As part of its efforts to enforce the new marketing restrictions, the Center for Medicare and Medicaid Services for the first time evaluated more than 3,000 MA ads before they ran in advance of 2024 open enrollment. It rejected more than 1,000 for being misleading, confusing, or otherwise non-compliant with the new requirements. These types of reviews will, I hope, continue.

CMS has proposed a fixed payment to brokers of MA plans that, if implemented, would significantly improve the problem of steering seniors to the highest-paying plan — with the highest compensation for the insurance broker. I think we can all agree brokers should be required to direct their clients to the best product, not the one that pays the broker the most. (That has been established practice for financial advisors for many years.) CMS should see this rule through, and send MA brokers profiteering off seniors packing.

A bonus regulation in this space to consider: banning MA plan brokers from selling the contact information of MA beneficiaries. Ever wonder why grandma and grandpa get so many spam calls targeting their health conditions? This practice has a lot to do with it. And there’s bipartisan support in Congress for banning sales of beneficiary contact information.

In addition, just as drug companies have to mention the potential side effects of their medications, MA plans should also be required to be forthcoming about their restrictions, including prior authorization requirements, limited networks, and potentially high out-of-pocket costs, in their ads and marketing materials.

3. Be real about supplemental benefits

Tell me if this one sounds familiar. The federal government introduced flexibility to MA plans to offer seniors benefits beyond what they can receive in traditional Medicare funded primarily through taxpayer dollars.

Those “supplemental” benefits were intended to keep seniors active and healthy. Instead, insurers have manipulated the program to offer benefits seniors are less likely to use, so more of the dollars CMS doles out to pay for those benefits stay with payers.

Many seniors in MA plans will see options to enroll in wellness plans, access gym memberships, acquire food vouchers, pick out new sneakers, and even help pay for pet care, believe it or not — all included under their MA plan. Those benefits are paid for by a pot of “rebate” dollars that CMS passes through to plans, with the presumed goal of improving health outcomes through innovative uses.

There is a growing sense, though, that insurers have figured out how to game this system. While some of these offerings seem appealing and are certainly a focus of marketing by insurers, how heavily are they being used? How heavily do insurers communicate to seniors that they have these benefits, once seniors have signed up for them? Are insurers offering things people are actually using? Or are insurers strategically offering benefits that are rarely used?

Those answers are important because MA plans do not have to pay unused rebate dollars back to the federal government.

CMS in 2024 is requiring insurers to submit detailed data for the first time on how seniors are using these benefits. The agency should lean into this effort and ensure plan compliance with the reporting. And as this year rolls on, CMS should be prepared to make the case to Congress that we expect the data to show that plans are pocketing many of these dollars, and they are not significantly improving health outcomes of older Americans.

4. Addressing coding intensity

If you’re a regular reader, you probably know one of my core views on traditional Medicare vs. Medicare Advantage plans. Traditional Medicare has straightforward, transparent payment, while Medicare Advantage presents more avenues for insurers to arbitrarily raise what they charge the government. A good example of this is in higher coding per patient found in MA plans relative to Traditional Medicare.

An older patient goes in to see their doctor. They are diagnosed, and prescribed a course of treatment. Under Traditional Medicare, that service performed by the doctor is coded and reimbursed. The payment is generally the same no matter what conditions or health history that patient brought into the exam room. Straightforward.

MA plans, however, pay more when more codes are added to a diagnosis.

Plans have advertised this to doctors, incentivizing the providers to add every possible code to a submission for reimbursement. So, if that same patient described above has diabetes, but they’re being treated for an unrelated flu diagnosis, the doctor is incentivized by MA to add a code for diabetes treatment. MA plans, in turn, get paid more by the government based on their enrollee’s health status, as determined based on the diagnoses associated with that individual.

Extrapolate that out across tens of millions of seniors with MA plans, and it’s clear MA plans are significantly overcharging the federal government because of over-coding.

One solution I find appealing: similar to fee-for-service, create a new baseline for payments in MA plans to remove the incentive to add more codes to submissions. Proposals I’ve seen would pay providers more than traditional Medicare but without creating the plan-driven incentive for doctors to over-code.

5. Focusing in on Medicare Advantage network cuts in rural areas

Rural America is older and unhealthier than the national average. This should be the area where MA plans should experience the highest utilization.

Instead, we’re seeing that the aggressive practices insurers use to maximize profits force many rural hospitals to cancel their contracts with MA plans. As we wrote about at length in December, MA is becoming a ghost benefit for seniors living in rural communities. The reimbursement rates these plans pay hospitals in rural communities are significantly lower than traditional Medicare. That has further stressed the low margins rural hospitals face.

As Congressional focus on MA grows, I predict more bipartisan recommendations to come forth that address the growing gap between MA plan payments and what hospitals need to be paid in rural areas.

If MA is not accepted by providers in older, rural America, then truly, what purpose does it serve?

STAT News today published an op-ed I coauthored with Dr. Philip Verhoef, president of Physicians for a National Health Program, making the point that investors are among the growing number of stakeholders who are souring on big, for-profit insurance companies like the ones I used to work for (Cigna and Humana).

We focused specifically on investors’ concerns about the continued profitability of Medicare Advantage plans most of the big insurers own and operate.

Several companies have lost billions of dollars in market capitalization over the past several weeks as they have reported what they maintain is higher than usual utilization of health care goods and services by seniors enrolled in MA plans.

Today, the companies–especially UnitedHealth Group, the market leader with 7.6 million Medicare Advantage enrollees–are losing billions more in market cap on the news, broke yesterday by the Wall Street Journal, that the Department of Justice is investigating UnitedHealth’s many acquisitions over the years.

UnitedHealth and most of the other companies are no longer just insurance companies. They’ve moved rapidly into health care delivery by buying physician practices and clinics, and three of them, UnitedHealth, Cigna and CVS/Aetna, control 80% of the pharmacy benefit management business.

Investors in MA insurance companies experienced a rude awakening in late January, with insurer stocks plummeting in the face of earnings reports showing profits falling far below expectations in the last quarter of 2023. Companies like CVS Health and UnitedHealth Group saw losses of 5.2% and 6.2% respectively, while Humana, whose business model relies heavily on the MA program, fell an astonishing 14.2%. These insurers cited higher than average health care utilization rates as the culprit and warned that 2024 would likely see more of the same. At the same time, private equity investment in MA has fallen, showing waning confidence in the program.

We went on to note that both Democrats and Republicans in Congress are increasingly concerned about MA insurers’ business practices and, among other things, have introduced bills to crack down on egregious overpayments to MA plans.

The WSJ reported yesterday that the Justice Department has launched an antitrust investigation into UnitedHealth, which has become not only the country’s biggest U.S. health insurer but also a leading manager of drug benefits “and a sprawling network of doctor groups.”

The investigators have in recent weeks been interviewing healthcare-industry representatives in sectors where UnitedHealth competes, including doctor groups, according to people with knowledge of the meetings.

The DOJ’s investigation of UnitedHealth is wide-ranging. Among other things, according to the Journal, “investigators have asked whether and how the tie-up between UnitedHealthcare [the insurance division] and Optum’s medical groups might affect its compliance with federal rules that cap how much a health-insurance company retains from the premiums it collects. (Optum is the company’s division that encompasses the pharmacy benefit manager Optum Rx and the many clinics and physician practices it owns.)

HEALTH CARE un-coveredexplained last month how UnitedHealth essentially is paying itself billions of dollars every month and circumventing the intent of a federal law that requires insurers to spend at least 80% of premium dollars on their health plan enrollees’ health care.

I know from sources within the Justice Department that investigators saw that piece, as well as the comprehensive analysis we published earlier of the scores of acquisitions UnitedHealth has made in recent years that have enabled it to catapult to the top five of the Fortune 500 list of American companies.

Those sources told me that the DOJ is very concerned about the consolidation within both the health insurance business and the hospital industry. Many U.S. hospitals, in an ongoing effort to negotiate from an enhanced position of strength with UnitedHealth and the other vertically integrated insurers, have merged with each other in recent years and become part of huge health-care delivery systems.

At the close of trading on the New York Stock Exchange yesterday, shares of UnitedHealth Group’s share were down $11.90 or 2.27%. Investors are continuing to head for the exits today. As I write this, the company’s stock price has fallen another $20 (4%) to $494.00. That’s way down from the company’s 52-week high of $554.70.

Shares of most of the other big publicly traded insurers (Centene, Cigna, CVS/Aetna, Elevance, Humana and Molina) are also down, ranging from $.83 at CVS to $11.51 at Humana.

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.

“What if 10 percent, or even five percent, of the employers in our market decide to stop providing health benefits?” a Chief Strategy Officer (CSO) at a midsized health system in the Southeast recently asked.

“Their health insurance costs have been growing like crazy for 20 years. Some of these companies could easily decide to just give their employees some amount of tax-advantaged dollars and let them do their own thing.” An emerging option for employers is the relatively new individual coverage Health Reimbursement Arrangement (ICHRA), which allows employers to give tax-deductible contributions to employees to use for healthcare, including purchasing health insurance on an exchange.

According to the CSO, “What happens is this: We’ll go from getting 250 percent of Medicare for beneficiaries in a commercial group plan to getting 125 percent for beneficiaries in a market plan. I don’t know any provider with the margins to withstand that kind of shift without significant pain—certainly not us.”

The conversation shifted to a discussion about treating employers like true customers that pay generously for healthcare services, which involves increasing engagement with them and better understanding their specific problems with their employees’ healthcare. What complaints are they hearing about their employee’s difficulties with things like making timely appointments or finding after-hours care?

Provider organizations can help keep employers in the health insurance market by regularly checking in with them about their healthcare challenges, meaningfully focusing on mitigating their pain points, and exploring new kinds of mutually beneficial partnerships.

They should also carefully monitor the employer market in their region and create financial assessments of the potential impact of employers shifting employees to health insurance stipend arrangements.

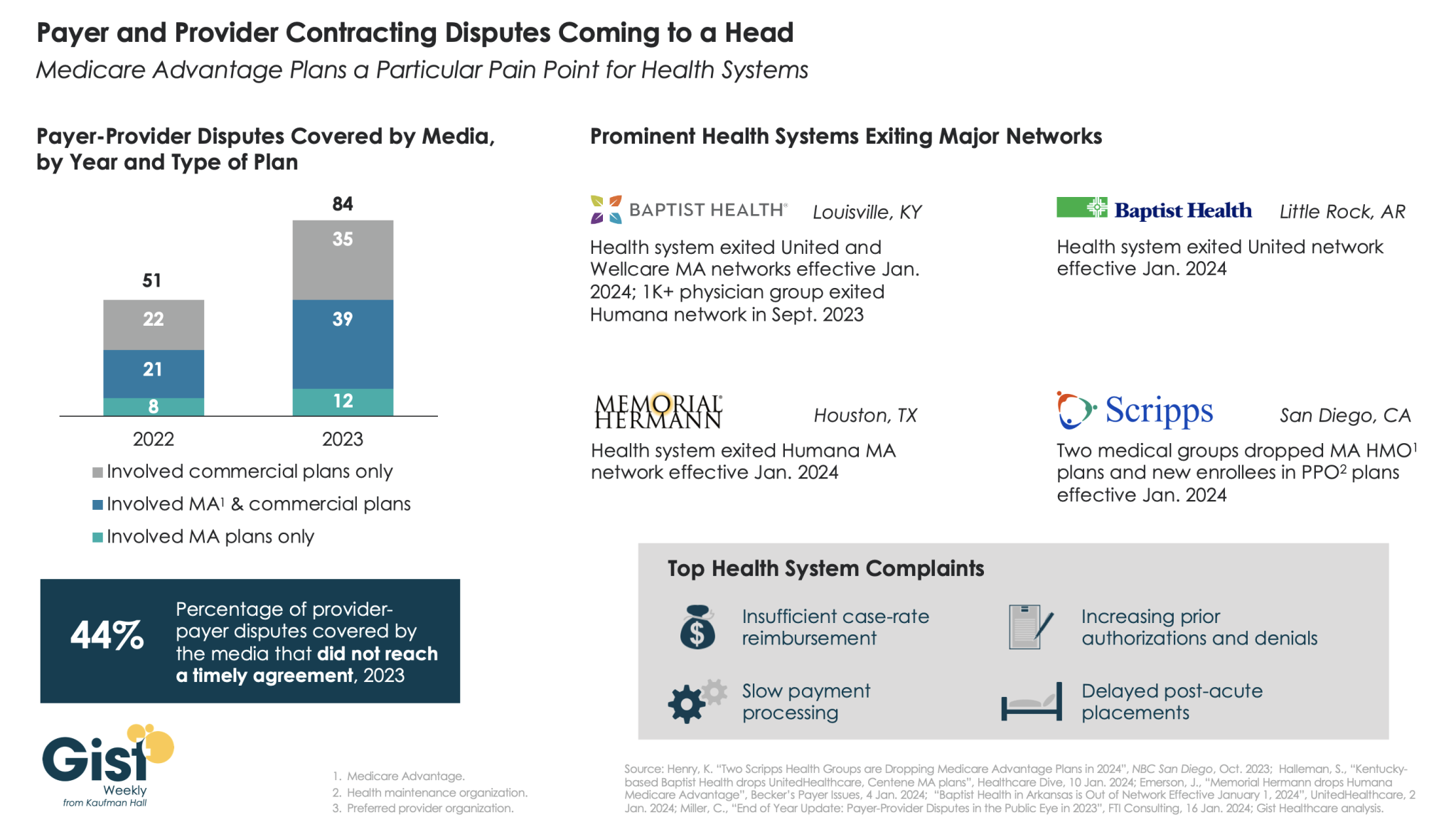

In this week’s graphic, we highlight new data on the increase in payer-provider contracting disputes covered by the media.

From 2022 to 2023, there was a 69 percent increase in the number of payer-provider contracting disputes that received media coverage. Nearly half of last year’s disputes did not reach agreement and resulted in network exits.

Large provider organizations—including Louisville, KY-based Baptist Health, Little Rock, AR-based Baptist Health, Houston, TX-based Memorial Hermann Health System, and two large medical groups affiliated with San Diego-based Scripps Health—dropped Medicare Advantage (MA) plans from at least one major payer, like United or Humana, as of Jan. 1, 2024.

Some dropped the payer’s commercial plans as well. Provider organizations leaving these networks have cited insufficient reimbursement rates and unsatisfactory business practices that drive up their cost of care delivery, especially around increased prior authorization requirements.

While contracting disputes will ultimately be influenced by the competitive strength of a given provider and payer in a particular market, it’s important for both sides to recognize thatthe patients in the middle of these disputes can be the ones most harmed when they can no longer see their trusted physicians.

On Wednesday, Bloomfield, CT-based Cigna announced a definitive agreement with Chicago, IL-based Health Care Service Corporation (HCSC), a large Blue Cross Blue Shield insurer, to sell its 600K-member MA business, as well as its Medicare prescription drug plan and Medigap offerings, for $3.3B.

The two insurers also agreed to a four-year services agreement where Cigna’s Evernorth Health Services subsidiary, which includes Express Scripts, will continue to provide pharmacy benefit services to the Medicare businesses.

While Cigna is exiting the MA market, other major payers—including UnitedHealth and Humana—are seeing their MA profits drop amid an increase in utilization, according to analysis from Moody’s Investors Service.

The Gist:While it initially appeared that Cigna’s divesture of its MA business would position it to combine more smoothly with Humana, this deal with HCSC makes sense even in the wake of that reportedly called off merger.

Cigna has been a bit player in MA for years, covering only two percent of MA lives in 2023, and the shrinking pie of MA profits will discourage all but the most successful or uniquely positioned payers.

But while increasing utilization rates are contributing to a declining outlook for payers, MA is still a solidly profitable business, covering over half of Medicare beneficiaries and still growing by millions of lives each year.

The MA payers that last are going to have to work harder at integrating their various care and data assets, and more carefully manage spend for an aging cohort of seniors with increasingly complex needs.

Jayne Kleinman is bombarded with Medicare Advantage promotions every open enrollment period — even though she has no interest in leaving traditional Medicare, which allows seniors to choose their doctors and get the care they want without interference from multi-billion-dollar insurance companies.

“My biggest problem with being barraged is that so many of the ads were inaccurate,” Kleinman, a retired social services professional in New Haven County, Connecticut, told HEALTH CARE un-covered.

“They neglect to say that the amount of coverage you get is limited. They don’t talk about what you are losing by leaving traditional Medicare. It feels like insurance companies are manipulating us to get Medicare Advantage plans sold so that they can control the system, as opposed to treating us like human beings.”

Seniors face a torrent of Medicare Advantage advertising: an analysis by KFF found 9,500 daily TV ads during open enrollment in 2022. A recent survey by the Commonwealth Fund found that 30% of seniors received seven or more phone calls weekly from Medicare Advantage marketers during the most recent open enrollment (Oct. 15 to Dec. 7) for 2024 coverage.

In 2023, a critical milestone was passed: over half of seniors are now enrolled in privatized Medicare Advantage plans. The marketing for these plans nearly always fails to mention how hard it is to return to traditional Medicare once you are in Medicare Advantage, and that the MA plans have closed provider networks and require prior authorization for medical procedures. Instead, the marketing emphasizes the fringe benefits offered by Medicare Advantage plans like gym memberships.

U.S. Sen. Ron Wyden (D-Ore.), chairman of the Senate Finance Committee, criticized the widespread and predatory marketing of Medicare Advantage in a report in November 2022 and has continued to pressure the Biden administration to do more to address the problem.

The report said that consumer complaints about Medicare Advantage marketing more than doubled from 2020 to 2021 to 41,000. It cites cases such as that of an Oregon man whose switch to Medicare Advantage meant he could no longer afford his prescription drugs, as well as a 94-year-old woman with dementia in a rural area who bought a Medicare Advantage plan that required her to obtain care miles further from her residence than she had to travel before.

When open enrollment began last fall, it was “the start of a marketing barrage as marketing middlemen look to collect seniors’ information in order to bombard them with direct mail, emails, and phone calls to get them to enroll,” Wyden stated in a letter to the Centers for Medicare and Medicaid Services (CMS), which was signed by the other Democrats on the Senate Finance Committee.

Just three weeks after Wyden sent the letter, CMS released a proposed rule reforming Medicare Advantage practices that the main lobby group for Medicare Advantage plans, the Better Medicare Alliance, endorsed.

But key recommendations by Wyden were missing, including a ban on list acquisition by Medicare Advantage third-party marketing organizations, which includes brokers, and banning brokers that call beneficiaries multiple times a day for days in a row.

Among the prominent third-party marketing organizations is TogetherHealth, a subsidiary of Benefytt Technologies, which runs ads featuring former football star Joe Namath.

In August 2022, the Federal Trade Commission forced Benefytt to repay $100 million for fraudulent activities. The month before, the Securities and Exchange Commission levied more than $12 million in fines against Benefytt.

But CMS continues to allow Benefytt to work as a broker. Benefytt is owned by Madison Dearborn Partners, a Chicago-based private equity firm with ties to former Chicago mayor and current Ambassador to Japan Rahm Emanuel. Benefytt collects leads on potential customers, which they then sell to brokers and insurers to aggressively target seniors. CMS did not provide comment as to why they had not blocked Benefytt’s continuing work as a third-party marketing organization for Medicare.

Two different rounds of rule-making on Medicare Advantage marketing in 2023 instead focused on such reforms as reining in exaggerated claims and excessive broker compensation.

The enormous profits generated by Medicare Advantage plans — costing the federal government as much as $140 billion annually in overpayments to private companies — explains what drives the aggressive and often unethical marketing practices, said David Lipschutz, an associate director at the Center for Medicare Advocacy.

“The fact is, there is an increasingly imbalanced playing field between Medicare Advantage and traditional Medicare,” he said. “Medicare Advantage is being favored in many ways. Medicare Advantage plans are paid more than what traditional Medicare spends on a given beneficiary.

Those factors combined with the fact that they generate such profits for insurance companies, leads to those companies doing everything they can to maximize enrollment.”

Adding to the problem, Lipschutz argued, was the enormous influence of the health insurance industry in Washington. Health insurers spent more than $33 million lobbying Washington in just the first three quarters of 2023 alone.

“There is no real organized lobby for traditional Medicare, or organized advertising efforts,” he said. “During open enrollment, 80% of Medicare-related ads have to do with Medicare Advantage. We regularly encounter very well-educated and savvy folks who are tripped up by advertising and lured in by the bells and whistles. The deck is stacked against the consumer.”

Private equity firms have made a large investment in the Medicare Advantage brokerage and marketing sector, in addition to Madison Dearborn’s acquisition of Benefytt. Bain Capital, which Sen. Mitt Romney (R-Utah) co-founded, invested $150 million in Enhance Health, a Medicare Advantage broker, in 2021.

The CEO of EasyHealth, another private equity-backed brokerage, toldModern Healthcare in 2021 that “Insurance distribution is our Trojan horse into healthcare services.”

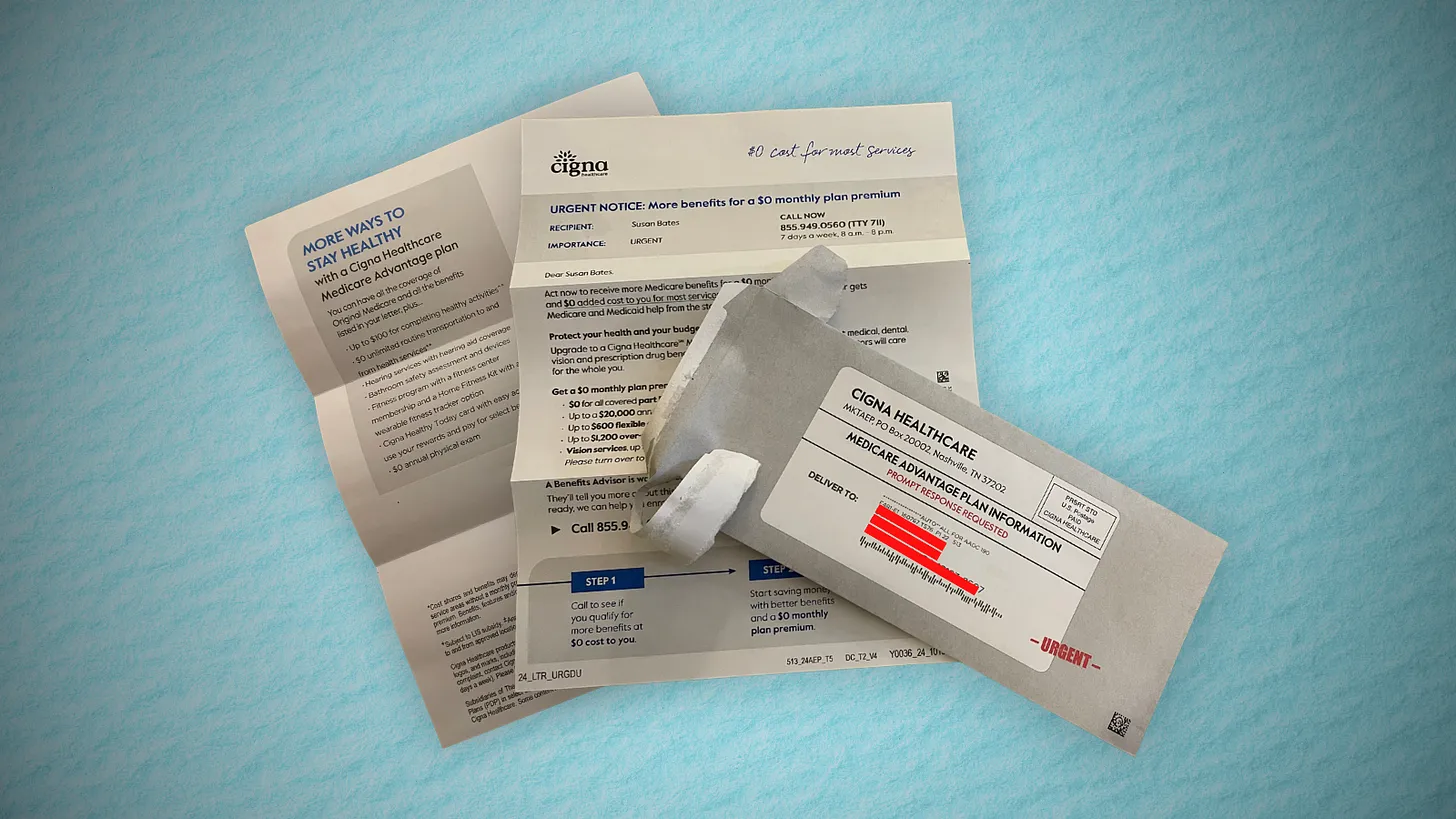

As federal law requires truth in advertising, a group of advocacy organizations–led by the Center for Medicare Advocacy, Disability Rights Connecticut, and the National Health Law Project–cited what they considered blatantly deceptive marketing by UnitedHealthcare to people who are eligible for both Medicare and Medicaid, in a complaint to CMS.

UnitedHealthcare had purchased ads in the Hartford Courant asking seniors in large bold-faced type: “Eligible for Medicare and Medicaid? You could get more with UnitedHealthcare.”

People who are eligible for both Medicare and Medicaid due to their income level are better off in traditional Medicare than Medicare Advantage given that Medicaid covers their out-of-pocket costs, meaning that they have wide latitude to choose their doctors, hospitals and medical procedures.

Sheldon Toubman, an attorney with Disability Rights Connecticut who worked to draft the complaint, framed the ad in the broader context of poor marketing practices by the Medicare Advantage industry.

“I have been aware for a long time of basically fraudulent advertising in the MA insurance industry,” Toubman told HEALTH CARE un-covered. “There’s an overriding misrepresentation — they tell you how great Medicare Advantage is, and never the downsides.

“There are two big downsides of going out of traditional Medicare:

They don’t tell you that you give up the broad Medicare provider network, which has nearly every doctor. And should you need expensive medical care in Medicare Advantage, you will learn there are prior authorization requirements. Traditional Medicare does almost no prior authorization, so you don’t have that obstacle. They don’t ever tell you any of that,” he said.

But it is marketing to dual-eligible individuals that is arguably the most problematic, Toubman argued. “They have Medicare and they are also low income. Because they are low-income, they also have Medicaid.

“Medicaid is a broader program — it covers a lot of things that Medicare doesn’t cover.

In Connecticut, 92,000 dual-eligible seniors have been ‘persuaded’ to sign up for Medicare Advantage. What’s outrageous about the marketing is they get you to sign up by offering extra services. … If you look at the ad in the Hartford Courant, it says you could get more, with the only real benefit being $130 per month toward food. But you now have this problem of a more limited provider network and prior authorization. UnitedHealth is doing false advertising.”

It’s a nationwide problem, Toubman said. “All insurers are doing this everywhere. We’re asking CMS and the Federal Trade Commission to conduct a nationwide investigation of this kind of problem. The failure to tell people that they give up their broader Medicare network — they don’t tell anybody that.”

For Jayne Kleinman, the unending ads are about one thing only: insurance industry profits. “Medicare Advantage has been strictly based on the people who make millions of dollars at the top of the company making more,” she said. “It’s all about money, not about you as an individual. Every time I saw an ad I’d get angry every single time — because I felt they were misleading people. The Medicare Advantage insurers are trying to scam people out of an interest of making money.”