Cartoon – Out of Pocket Experience

https://www.kaufmanhall.com/insights/blog/gist-weekly-april-12-2024

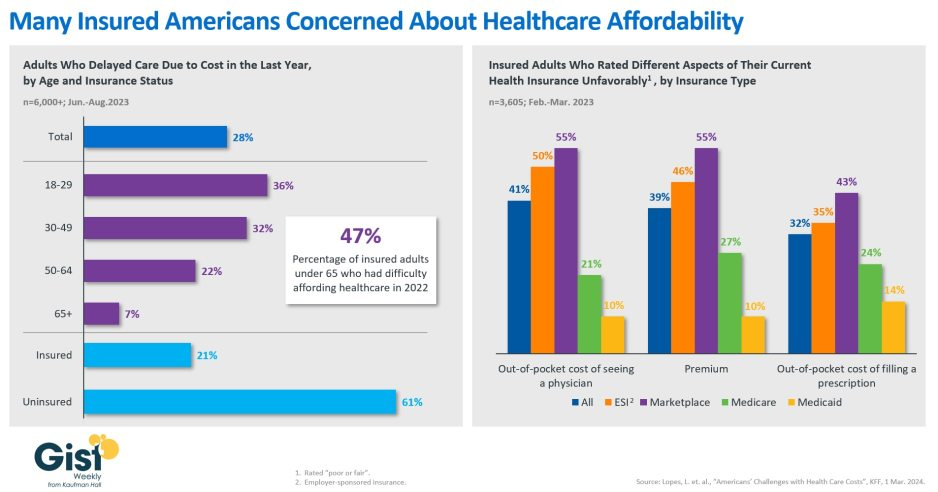

In this week’s graphic, we showcase recent KFF survey data on how healthcare costs impact the public, particularly those with health insurance.

Nearly half of US adults say it is difficult to afford healthcare, and in the last year, 28 percent have skipped or postponed care due to cost, with an even greater share of younger people delaying care due to cost concerns.

Although healthcare affordability has long been a problem for the uninsured, one in five adults with insurance skipped care in the past year because of cost. Insured Americans report low satisfaction with the affordability of their coverage.

In addition to high premiums, out-of-pocket costs to see a physician or fill a prescription are particular sources of concern. Adults with employer-sponsored or marketplace plans are far more likely to be dissatisfied with the affordability of their coverage, compared to those with government-sponsored plans.

With eight in ten American voters saying that it is “very important” for the 2024 presidential candidates to focus on the affordability of healthcare, we’ll no doubt see more attention focused on this issue as the presidential election race heats up.

Last week was significant for healthcare:

Just another week for healthcare: Congressional infighting about healthcare spending. Regulator announcements of new rules to stimulate competition and protect consumers in the healthcare market. Lobbying by leading trade groups to protect funding and disable threats from rivals. And so on.

At the macro level, it’s understandable: healthcare is an attractive market, especially in its services sectors. Since the pandemic, prices for services (i.e. physicians, hospitals et al) have steadily increased and remain elevated despite the pressures of transparency mandates and insurer pushback. By contrast, prices for most products (drugs, disposables, technologies et al) have followed the broader market pricing trends where prices for some escalated fast and then dipped.

While some branded prescription medicines are exceptions, it is health services that have driven the majority of health cost inflation since the pandemic.

UnitedHealth Group’s financial success is illustrative:

it’s big, high profile and vertically integrated across all major services sectors. In its year end 2023 financial report (January 12, 2024) it reported revenues of $371.6 Billion (up 15% Year-Over-Year), earnings from operations up 14%, cash flows from operations of $29.1 Billion (1.3x Net Income), medical care ratio at 83.2% up from 82% last year, net earnings of $23.86/share and adjusted net earnings of $25.12/share and guidance its 2024 revenues of $400-403 billion. They buy products using their scale and scope leverage to pay less for services they don’t own less and products needed to support them. It’s a big business in a buyer’s market and that’s unsettling to many.

Big business is not new to healthcare:

it’s been dominant in every sector but of late more a focus of unflattering regulator and media attention. Coupled with growing public discontent about the system’s effectiveness and affordability, it seems it’s near a tipping point.

David Johnson, one of the most thoughtful analysts of the health industry, reminded his readers last week that the current state of affairs in U.S. healthcare is not new citing the January 1970 Fortune cover story “Our Ailing Medical System”

“American medicine, the pride of the nation for many years, stands now on the brink of chaos. To be sure, our medical practitioners have their great moments of drama and triumph. But much of U.S. medical care, particularly the everyday business of preventing and treating routine illnesses, is inferior in quality, wastefully dispensed, and inequitably financed…

Whether poor or not, most Americans are badly served by the obsolete, overstrained medical system that has grown up around them helter-skelter. … The time has come for radical change.”

Johnson added: “The healthcare industry, however, cannot fight gravity forever. Consumerism, technological advances and pro-market regulatory reforms are so powerful and coming so fast that status-quo healthcare cannot forestall their ascendance. Properly harnessed, these disruptive forces have the collective power necessary for U.S. healthcare to finally achieve the 1970 Fortune magazine goal of delivering “good care to every American with little increase in cost.”

He’s right.

I believe the U.S. health system as we know it has reached its tipping point. The big-name organizations in every sector see it and have nominal contingency plans in place; the smaller players are buying time until the shoe drops. But I am worried.

I am worried the system’s future is in the hands of hyper-partisanship by both parties seeking political advantage in election cycles over meaningful creation of a health system that functions for the greater good.

I am worried that the industry’s aversion to price transparency, meaningful discussion about affordability and consistency in defining quality, safety and value will precipitate short-term gamesmanship for reputational advantage and nullify systemness and interoperability requisite to its transformation.

I am worried that understandably frustrated employers will drop employee health benefits to force the system to needed accountability.

I am worried that the growing armies of under-served and dissatisfied populations will revolt.

I am worried that its workforce is ill-prepared for a future that’s technology-enabled and consumer centric.

I am worried that the industry’s most prominent trade groups are concentrating more on “warfare” against their rivals and less about the long-term future of the system.

I am worried that transformational change is all talk.

It’s time to start an adult conversation about the future of the system. The starting point: acknowledging that it’s not about bad people; it’s about systemic flaws in its design and functioning. Fixing it requires balancing lag indicators about its use, costs and demand with assumptions about innovations that hold promise to shift its trajectory long-term. It requires employers to actively participate: in 2009-2010, Big Business mistakenly chose to sit out deliberations about the Affordable Care Act. And it requires independent, visionary facilitation free from bias and input beyond the DC talking heads that have dominated reform thought leadership for 6 decades.

Or, collectively, we can watch events like last week’s roll by and witness the emergence of a large public utility serving most and a smaller private option for those that afford it. Or something worse.

P.S. Today, thousands will make the pilgrimage to Orlando for HIMSS24 kicking off with a keynote by Robert Garrett, CEO of Hackensack Meridian Health tomorrow about ‘transformational change’ and closing Friday with a keynote by Nick Saban, legendary Alabama football coach on leadership. In between, the meeting’s 24 premier supporters and hundreds of exhibitors will push their latest solutions to prospects and customers keenly aware healthcare’s future is not a repeat of its past primarily due to technology. Information-driven healthcare is dependent on technologies that enable cost-effective, customized evidence-based care that’s readily accessible to individuals where and when they want it and with whom.

And many will be anticipating HCA Mission Health’s (Asheville NC) Plan of Action response due to CMS this Wednesday addressing deficiencies in 6 areas including CMS Deficiency 482.12 “which ensures that hospitals have a responsible governing body overseeing critical aspects of patient care and medical staff appointments.” Interest is high outside the region as the nation’s largest investor-owned system was put in “immediate jeopardy” of losing its Medicare participation status last year at Mission. FYI: HCA reported operating income of $7.7 billion (11.8% operating margin) on revenues of $65 billion in 2023.

With the South Carolina Republican primary results in over the weekend, it seems a Biden-Trump re-match is inevitable. Given the legacies associated with Presidencies of the two and the healthcare platforms espoused by their political parties, the landscape for healthcare politics seems clear:

| Healthcare Issue | Biden Policy | Trump Policy |

| Access to Abortion | ‘It’s a basic right for women protected by the Federal Government’ | ‘It’s up to the states and should be safe and rare. A 16-week ban should be the national standard.’ |

| Ageism | ‘President Biden is alert and capable. It’s a non-issue.’ | ‘President Biden is senile and unlikely to finish a second term is elected. President Trump is active and prepared.’ |

| Access to IVF Treatments | ‘It’s a basic right and should be universally accessible in every state and protected’ | ‘It’s a complex issue that should be considered in every state.’ |

| Affordability | ‘The system is unaffordable because it’s dominated by profit-focused corporations. It needs increased regulation including price controls.’ | ‘The system is unaffordable to some because it’s overly regulated and lacks competition and price transparency.’ |

| Access to Health Insurance Coverage | ‘It’s necessary for access to needed services & should be universally accessible and affordable.’ | ‘It’s a personal choice. Government should play a limited role.’ |

| Public health | ‘Underfunded and increasingly important.’ | ‘Fragmented and suboptimal. States should take the lead.’ |

| Drug prices | ‘Drug companies take advantage of the system to keep prices high. Price controls are necessary to lower costs.’ | ‘Drug prices are too high. Allowing importation and increased price transparency are keys to reducing costs.’ |

| Medicare | ‘It’s foundational to seniors’ wellbeing & should be protected. But demand is growing requiring modernization (aka the value agenda) and additional revenues (taxes + appropriations).’ | ‘It’s foundational to senior health & in need of modernization thru privatization. Waste and fraud are problematic to its future.’ |

| Medicaid | ‘Medicaid Managed Care is its future with increased enrollment and standardization of eligibility & benefits across states.’ | ‘Medicaid is a state program allowing modernization & innovation. The federal role should be subordinate to the states.’ |

| Competition | ‘The federal government (FTC, DOJ) should enhance protections against vertical and horizontal consolidation that reduce choices and increase prices in every sector of healthcare.’ | ‘Current anti-trust and consumer protections are adequate to address consolidation in healthcare.’ |

| Price Transparency | ‘Necessary and essential to protect consumers. Needs expansion.’ | ‘Necessary to drive competition in markets. Needs more attention.’ |

| The Affordable Care Act | ‘A necessary foundation for health system modernization that appropriately balances public and private responsibilities. Fix and Repair’ | ‘An unnecessary government takeover of the health system that’s harmful and wasteful. Repeal and Replace.’ |

| Role of federal government | ‘The federal government should enable equitable access and affordability. The private sector is focused more on profit than the public good.’ | ‘Market forces will drive better value. States should play a bigger role’ |

My take:

Polls indicate Campaign 2024 will be decided based on economic conditions in the fall 2024 as voters zero in on their choice. Per KFF’s latest poll, 74% of adults say an unexpected healthcare bill is their number-one financial concern—above their fears about food, energy and housing. So, if you’re handicapping healthcare in Campaign 2024, bet on its emergence as an economic issue, especially in the swing states (Michigan, Florida, North Carolina, Georgia and Arizona) where there are sharp health policy differences and the healthcare systems in these states are dominated by consolidated hospitals and national insurers.

As the primary season wears on (in Michigan tomorrow and 23 others on/before March 5), how the health system is positioned in the court of public opinion will come into focus.

Abortion rights will garner votes; affordability, price transparency, Medicare solvency and system consolidation will emerge as wedge issues alongside.

PS: Re: federal budgeting for key healthcare agencies, two deadlines are eminent: March 1 for funding for the FDA and the VA and March 8 for HHS funding.

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.

Three critical healthcare struggles will define the year to come with cutthroat competition and intense disputes being played out in public:

1. A Nation Divided Over Abortion Rights

2. The Generative AI Revolution In Medicine

3. The Tug-Of-War Over Healthcare Pricing American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained. Let me know your thoughts once you read mine.

Modern medicine, for most of its history, has operated within a collegial environment—an industry of civility where physicians, hospitals, pharmaceutical companies and others stayed in their lanes and out of each other’s business.

It used to be that clinicians made patient-centric decisions, drugmakers and hospitals calculated care/treatment costs and added a modest profit, while insurers set rates based on those figures. Businesses and the government, hoping to save a little money, negotiated coverage rates but not at the expense of a favored doctor or hospital. Disputes, if any, were resolved quietly and behind the scenes.

Times have changed as healthcare has taken a 180-degree turn. This year will be characterized by cutthroat competition and intense disputes played out in public. And as the once harmonious world of healthcare braces for battle, three critical struggles take centerstage. Each one promises controversy and profound implications for the future of medicine:

For nearly 50 years, from the landmark Roe v. Wade decision in 1973 to its overruling by the 2022 Dobbs case, abortion decisions were the province of women and their doctors. This dynamic has changed in nearly half the states.

This spring, the Supreme Court is set to hear another pivotal case, this one on mifepristone, an important drug for medical abortions. The ruling, expected in June, will significantly impact women’s rights and federal regulatory bodies like the FDA.

Traditionally, abortions were surgical procedures. Today, over half of all terminations are medically induced, primarily using a two-drug combination, including mifepristone. Since its approval in 2000, mifepristone has been prescribed to over 5 million women, and it boasts an excellent safety record. But anti-abortion groups, now challenging this method, have proposed stringent legal restrictions: reducing the administration window from 10 to seven weeks post-conception, banning distribution of the drug by mail, and mandating three in-person doctor visits, a burdensome requirement for many. While physicians could still prescribe misoprostol, the second drug in the regimen, its effectiveness alone pales in comparison to the two-drug combo.

Should the Supreme Court overrule and overturn the FDA’s clinical expertise on these matters, abortion activists fear the floodgates will open, inviting new challenges against other established medications like birth control.

In response, several states have fortified abortion rights through ballot initiatives, a trend expected to gain momentum in the November elections. This legislative action underscores a significant public-opinion divide from the Supreme Court’s stance. In fact, a survey published in Nature Human Behavior reveals that 60% of Americans support legal abortion.

Path to resolution: Uncertain. Traditionally, SCOTUS rulings have mirrored public opinion on key social issues, but its deviation on abortion rights has failed to shift public sentiment, setting the stage for an even fiercer clash in years to come. A Supreme Court ruling that renders abortion unconstitutional would contradict the principles outlined in the Dobbs decision, but not all states will enact protective measures. As a result, America’s divide on abortion rights is poised to deepen.

A year after ChatGPT’s release, an arms race in generative AI is reshaping industries from finance to healthcare. Organizations are investing billions to get a technological leg up on the competition, but this budding revolution has sparked widespread concern.

In Hollywood, screenwriters recently emerged victorious from a 150-day strike, partially focused on the threat of AI as a replacement for human workers. In the media realm, prominent organizations like The New York Times, along with a bevy of celebs and influencers, have initiated copyright infringement lawsuits against OpenAI, the developer of ChatGPT.

The healthcare sector faces its own unique battles. Insurers are leveraging AI to speed up and intensify claim denials, prompting providers to counter with AI-assisted appeals.

But beyond corporate skirmishes, the most profound conflict involves the doctor-patient relationship. Physicians, already vexed by patients who self-diagnose with “Dr. Google,” find themselves unsure whether generative AI will be friend or foe. Unlike traditional search engines, GenAI doesn’t just spit out information. It provides nuanced medical insights based on extensive, up-to-date research. Studies suggest that AI can already diagnose and recommend treatments with remarkable accuracy and empathy, surpassing human doctors in ever-more ways.

Path to resolution: Unfolding. While doctors are already taking advantage of AI’s administrative benefits (billing, notetaking and data entry), they’re apprehensive that ChatGPT will lead to errors if used for patient care. In this case, time will heal most concerns and eliminate most fears. Five years from now, with ChatGPT predicted to be 30 times more powerful, generative AI systems will become integral to medical care. Advanced tools, interfacing with wearables and electronic health records, will aid in disease management, diagnosis and chronic-condition monitoring, enhancing clinical outcomes and overall health.

From routine doctor visits to complex hospital stays and drug prescriptions, every aspect of U.S. healthcare is getting more expensive. That’s not news to most Americans, half of whom say it is very or somewhat difficult to afford healthcare costs.

But people may be surprised to learn how the pricing wars will play out this year—and how the winners will affect the overall cost of healthcare.

Throughout U.S. healthcare, nurses are striking as doctors are unionizing. After a year of soaring inflation, healthcare supply-chain costs and wage expectations are through the roof. A notable example emerged in California, where a proposed $25 hourly minimum wage for healthcare workers was later retracted by Governor Newsom amid budget constraints.

Financial pressures are increasing. In response, thousands of doctors have sold their medical practices to private equity firms. This trend will continue in 2024 and likely drive up prices, as much as 30% higher for many specialties.

Meanwhile, drug spending will soar in 2024 as weight-loss drugs (costing roughly $12,000 a year) become increasingly available. A groundbreaking sickle cell disease treatment, which uses the controversial CRISPR technology, is projected to cost nearly $3 million upon release.

To help tame runaway prices, the Centers for Medicare & Medicaid Services will reduce out-of-pocket costs for dozens of Part B medications “by $1 to as much as $2,786 per average dose,” according to White House officials. However, the move, one of many price-busting measures under the Inflation Reduction Act, has ignited a series of legal challenges from the pharmaceutical industry.

Big Pharma seeks to delay or overturn legislation that would allow CMS to negotiate prices for 10 of the most expensive outpatient drugs starting in 2026.

Path to resolution: Up to voters. With national healthcare spending expected to leap from $4 trillion to $7 trillion by 2031, the pricing debate will only intensify. The upcoming election will be pivotal in steering the financial strategy for healthcare. A Republican surge could mean tighter controls on Medicare and Medicaid and relaxed insurance regulations, whereas a Democratic sweep could lead to increased taxes, especially on the wealthy. A divided government, however, would stall significant reforms, exacerbating the crisis of unaffordability into 2025.

American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained.

Yet, amidst the strife, hope glimmers: The rise of ChatGPT and other generative AI technologies holds promise for revolutionizing patient empowerment and systemic efficiency, making healthcare more accessible while mitigating the burden of chronic diseases. The debate over abortion rights, while deeply polarizing, might eventually find resolution in a legislative middle ground that echoes Roe’s protections with some restrictions on how late in pregnancy procedures can be performed.

Unfortunately, some problems need to get worse before they can get better. I predict the affordability of healthcare will be one of them this year. My New Year’s request is not to shoot the messenger.

https://mailchi.mp/169732fa4667/the-weekly-gist-november-17-2023?e=d1e747d2d8

This week, Express Scripts, the nation’s second-largest pharmacy benefit manager (PBM), which is owned by health insurer Cigna, announced a new pricing model.

It is giving employers and health plans the option to pay pharmacies up to 15 percent over acquisition costs, plus a dispensing fee, for covered drugs. This payment structure was popularized by the Mark Cuban Cost Plus Drugs Company, founded by the billionaire businessman in reaction to the opaque pricing and complicated discounts and rebates common among PBMs.

While Cigna is not promising that this new pricing model will result in lower prices, it says it will improve transparency and should benefit retail pharmacies, who will split the markup with Express Scripts.

Cigna projects that only some employers will lower their healthcare spending through the cost-plus model, and that patient cost-sharing should be similar under both approaches.

The Gist: Between disruptive competitors like Cuban’s venture and increasing scrutiny from Congress, PBMs are facing new pressures to improve transparency and account for their role in rising drug costs.

This move by Cigna is an attempt to address at least one of those concerns, possibly intended to preempt regulatory and legislative action.

After years of complaints surrounding their business practices, it appears that the Congressional tide may be turning toward PBM industry reform. However, patients—who by and large are unaware of what PBMs are or do—won’t be satisfied till they see their out-of-pocket prescription drug costs go down.

Next up on this front: seeing which provisions targeting PBMs, many which have bipartisan support, make it into the Senate’s broad healthcare legislation planned for the end of this year, and in what form that bill ultimately passes.

https://mailchi.mp/d0e838f6648b/the-weekly-gist-september-8-2023?e=d1e747d2d8

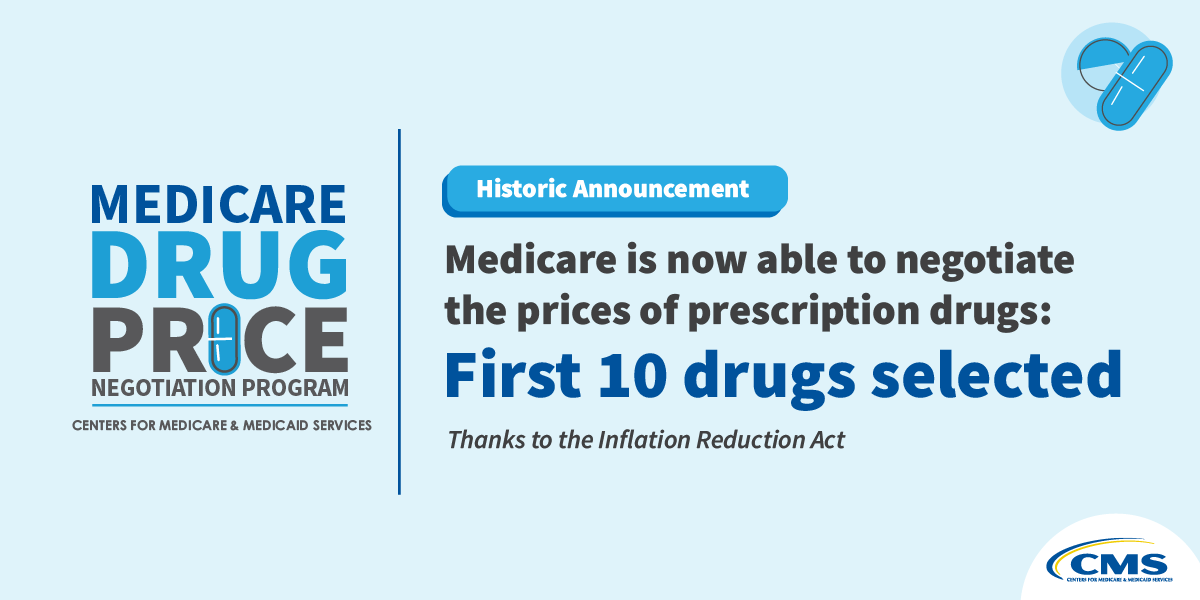

Last week, the Centers for Medicare and Medicaid Services (CMS) released the list of the first round of prescription drugs chosen for Medicare Part D price negotiations. The 2022 Inflation Reduction Act (IRA) granted CMS the authority to negotiate directly with pharmaceutical manufacturers, establishing a process that will ramp up to include 20 drugs per year and cover Part B medicines by 2029.

The majority of the initial 10 medications, including Eliquis, Jardiance, and Xarelto, are highly utilized across Medicare beneficiaries, treating mainly diabetes and cardiovascular disease. But three of the drugs (Enbrel, Imbruvica, and Stelara) are very high-cost drugs used by fewer than 50k beneficiaries to treat some cancers and autoimmune diseases.

Together the 10 drugs cost Medicare about $50B annually, comprising 20 percent of Part D spending. Drug manufacturers must now engage with CMS in a complex negotiation process, with negotiated prices scheduled to go into effect in 2026.

The Gist:

Most of the drugs on this list are not a surprise, with the Biden administration prioritizing more common chronic disease medications, with large total spend for the program, over the most expensive drugs, many of which are exempted by the IRA’s minimum seven-year grace period for new pharmaceuticals.

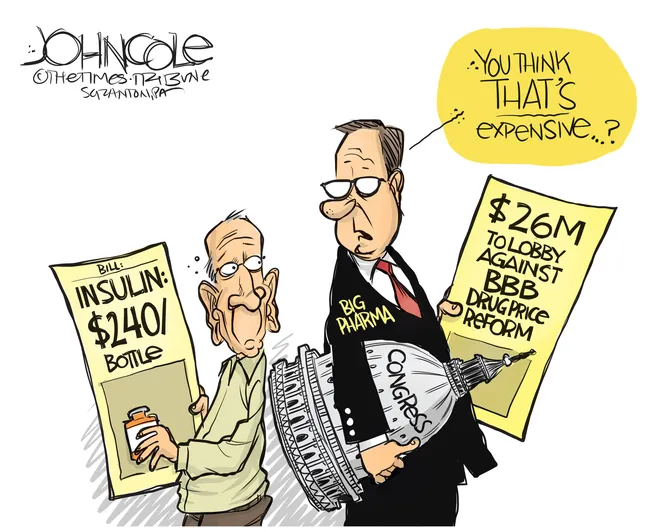

However, pharmaceutical companies are threatening to derail the process before it even begins. Several companies with drugs on the list have already filed lawsuits against the government on the grounds that the entire negotiation program is unconstitutional.

While President Biden is already touting lowering drug prices as a key plank of his reelection pitch, it will take years before these negotiations translate into lower costs for beneficiaries and reduced government spending. There also may be adverse unintended consequences, as drug companies may raise prices for commercial payers while increasing rebates to stabilize net prices, leading to higher costs for some consumers.

Still, it’s a step in the right direction for the US, given that we pay 2.4 times more than peer countries for prescription medications.

Last Tuesday, the Center for Medicare and Medicaid Services (CMS) announced the first 10 medicines that will be subject to price negotiations with Medicare starting in 2026 per authorization in the Inflation Reduction Act (2022). It’s a big deal but far from a done deal.

Here are the 10:

Notably, they include products from 10 of the biggest drug manufacturers that operate in the U.S. including 4 headquartered here (Johnson and Johnson, Merck, Lilly, Amgen) and the list covers a wide range of medical conditions that benefit from daily medications.

But only one cancer medicine was included (Johnson & Johnson and AbbVie’s Imbruvica for lymphoma) leaving cancer drugs alongside therapeutics for weight loss, Crohn’s and others to prepare for listing in 2027 or later.

And CMS included long-acting insulins in the inaugural list naming six products manufactured by the Danish pharmaceutical giant Novo Nordisk while leaving the competing products made by J&J and others off. So, there were surprises.

To date, 8 lawsuits have been filed against the U.S. Department of Health and Human Services by drug manufacturers and the likelihood litigation will end up in the Supreme Court is high.

These cases are being brought because drug manufacturers believe government-imposed price controls are illegal. The arguments will be closely watched because they hit at a more fundamental question:

what’s the role of the federal government in making healthcare in the U.S. more affordable to more people?

Every major sector in healthcare– hospitals, health insurers, medical device manufacturers, physician organizations, information technology companies, consultancies, advisors et al may be impacted as the $4.6 trillion industry is scrutinized more closely . All depend on its regulatory complexity to keep prices high, outsiders out and growth predictable. The pharmaceutical industry just happens to be its most visible.

The Pharmaceutical Industry

The facts are these:

It’s a big, high-profile industry that claims 7 of the Top 10 highest paid CEOs in healthcare in its ranks, a persistent presence in social media and paid advertising for its brands and inexplicably strong influence in politics and physician treatment decisions.

The industry is not well liked by consumers, regulators and trading partners but uses every legal lever including patents, couponing, PBM distortion, pay-to-delay tactics, biosimilar roadblocks et al to protect its shareholders’ interests. And it has been effective for its members and advisors.

My take:

It’s easy to pile-on to criticism of the industry’s opaque pricing, lack of operational transparency, inadequate capture of drug efficacy and effectiveness data and impotent punishment against its bad actors and their enablers.

It’s clear U.S. pharma consumers fund the majority of the global industry’s profits while the rest of the world benefits.

And it’s obvious U.S. consumers think it appropriate for the federal government to step in. The tricky part is not just government-imposed price controls for a handful of drugs; it’s how far the federal government should play in other sectors prone to neglect of affordability and equitable access.

There will be lessons learned as this Inflation Reduction Act program is enacted alongside others in the bill– insulin price caps at $35/month per covered prescription, access to adult vaccines without cost-sharing, a yearly cap ($2,000 in 2025) on out-of-pocket prescription drug costs in Medicare and expansion of the low-income subsidy program under Medicare Part D to 150% of the federal poverty level starting in 2024. And since implementation of these price caps isn’t until 2026, plenty of time for all parties to negotiate, spin and adapt.

But the bigger impact of this program will be in other sectors where pricing is opaque, the public’s suspicious and valid and reliable data is readily available to challenge widely-accepted but flawed assertions about quality, value, access and outcomes. It’s highly likely hospitals will be next.

Stay tuned.