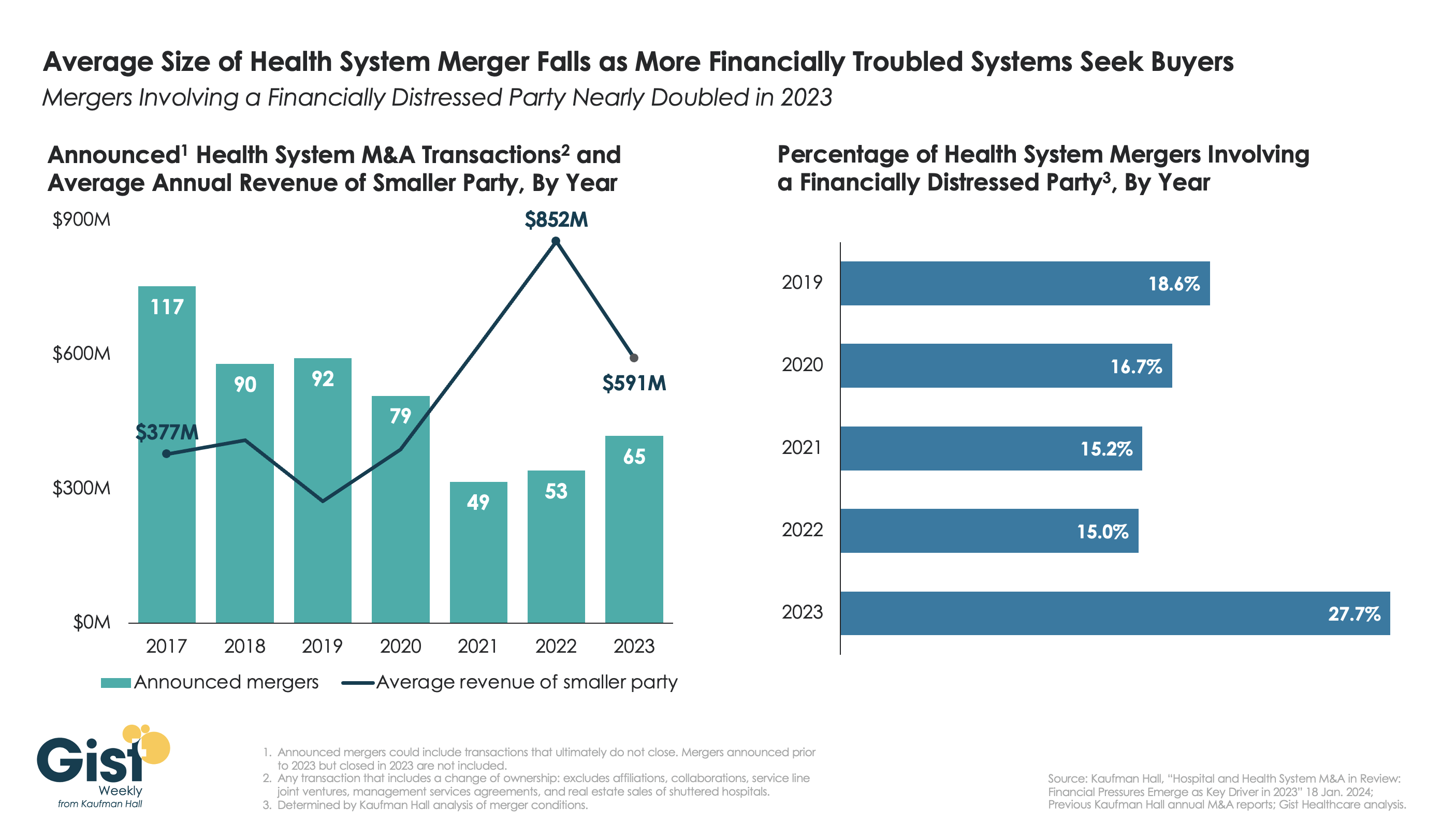

This week’s graphic highlights data from Kaufman Hall’s recently released 2023 Hospital and Health System M&A Report on the current dynamics in health system mergers and acquisitions (M&A) activity.

After a slowdown during the pandemic, 2023 saw an uptick in M&A activity with 65 announced transactions, the most since 2020. Continuing the trend of the past two years, the number of announced “mega mergers,” in which the smaller party had at least $1B in annual revenue, represented more than a tenth of total announced transactions.

However, the average size of mergers fell in 2023, as financial distress emerged as a key driver of M&A activity. The percent of mergers involving a financially distressed party spiked to nearly 28 percent in 2023, almost double the level seen in prior years.

CARES Act funding had buoyed some health systems’ balance sheets through the pandemic, but with the end of federal aid, more systems needed to seek shelter through scale.

With the median hospital operating margin still barely hitting two percent, we anticipate this heightened level M&A activity to continue in 2024 as health systems search for stronger partners that can help them stabilize financially.

Last Monday, two lawsuits were filed that strike at a fundamental challenge facing the U.S. health system:

In the District Court of NJ, a class action lawsuit (ANN LEWANDOWSKI v THE PENSION & BENEFITS COMMITTEE OF JOHNSON AND JOHNSON) was filed against J&J alleging the company had mismanaged health benefits in violation of the Employee Retirement Income Security Act (“ERISA”). As noted in the 74-page filing “This case principally involves mismanagement of prescription-drug benefits. “Over the past several years, defendants breached their fiduciary duties and mismanaged Johnson and Johnson’s prescription-drug benefits program, costing their ERISA plans and their employees millions of dollars in the form of higher payments for prescription drugs, higher premiums, higher deductibles, higher coinsurance, higher copays, and lower wages or limited wage growth… Defendants’ mismanagement is most evident in (but not limited to) the prices it agreed to pay one of its vendors—its Pharmacy Benefits Manager (“PBM”)—for many generic drugs that are widely available at drastically lower prices.”

The issue is this: what liability risk does a self-insured employer have in providing health benefits to their employees?

Is the structure of the plan, the selection of providers and vendors, and costs and prices experienced by employees subject to litigation? What’s the role of the employer in protecting employees against unnecessary costs?

On the same day, in the District Court of Eastern Wisconsin, an 85-page class action lawsuit was filed against Advocate-Aurora Health (AAH) claiming it “uses its market power to raise prices, limit competition and harm consumers in Wisconsin:

Forces commercial health plans to include all its “overpriced facilities” in-network even when they would prefer to include only some facilities.

Goes to “extreme efforts to drive out innovative insurance products that save commercial health plans and their members money.”

Suppresses competition through “secret and restrictive contract terms that have been the subject of bipartisan criticism.”

Acquires new facilities, which then allows it to raise prices due to reduced competition

… without intervention, the health system will continue to use “anticompetitive contracting and negotiating tactics to raise prices on Wisconsin commercial health plans and their members and use those funds for aggressive acquisitions and executive compensation.”

The issue is this: is a health system’s liable when its consolidation activities result in higher prices for services provided communities and employers in communities where they operate?

Is there a direct causal relationship between a system’s consolidation activities and their prices, and how should alleged harm be measured and remedied?

Two complicated issues for two reputable mega-players in the U.S. health system. Both lawsuits were brought as class actions which guarantees widespread media attention and a protracted legal process. And each contributes directly to the gradual erosion of public trust in the health system since the plaintiffs essentially claim the business practices of J&J and Advocate-Aurora willfully harm the individuals they pledge to serve.

In the November 2023 Keckley Poll, I asked the sample of 817 U.S. adults to assess the health system overall. The results were clear:

69% think the system is fundamentally flawed and in need of major change vs. 7% who think otherwise.

60% believe it puts its profits above patient care vs. 13% who disagree.

74% think price controls are needed vs. 7% who disagree.

83% believe having health insurance that’s ‘affordable and comprehensive’ is essential to financial security vs 3% who disagree.

52% feel confident in their ability to navigate the U.S. system “when I have a problem” vs. 32% who have mixed feelings and 16% who aren’t.

And 76% think politicians avoid dealing with healthcare issues because they’re complex and politically risky vs/ 6% who think they tackle them head-on.

The poll also asked their level of trust and confidence in five major institutions “to develop a plan for the U.S. health system that maximizes what it has done well and corrects its major flaws.”

Clearly, trust and confidence in the health system is low, and expectations about solutions fall primarily on hospitals and doctors. Lawsuits like these widen suspicion that the industry’s dominated first and foremost by Big Businesses focused on their own profitability before all else. And they pose particular problems for sectors in healthcare dominated by not-for-profit and public ownership i.e. hospitals, home care, public health agencies and others.

My take

These lawsuits address two distinct issues: the roles of employers in designing their health benefits for employees including the use of PBMs, and the justification for consolidation of hospital and ancillary services in markets.

But each lawsuit s predicated on a legal theory that prices set by organizations are geared more to corporate profits than public good and justifiable costs.

Pricing is the Achilles of the health system. Pushback against price transparency by some, however justified, has amplified exposure to litigation risk like these two and contributed to the public’s loss of trust in the system.

It is unlikely greater price transparency and business practice disclosures by J&J and Advocate-Aurora could have avoided these lawsuits, but it’s clearly a message that needs consideration in every organization.

Healthcare organizations and their trade groups can no longer defend against lack of transparency by defaulting to the complexity of our supply chains and payment systems. They’re excuses. The realities of generative AI and interoperability assure information driven healthcare that’s publicly accessible and inclusive of prices, costs, outcomes and business practices. In the process, the public’s interest will heighten and lawsuits will increase.

Companies grappling with liquidity concerns are looking to cut costs and streamline operations, according to a new survey.

Dive Brief:

Over three-quarters of healthcare chief financial officers expect to see profitability increases in 2024, according to a recent survey from advisory firm BDO USA. However, to become profitable, many organizations say they will have to reduce investments in underperforming service lines, or pursue mergers and acquisitions.

More than 40% of respondents said theywill decrease investments in primary care and behavioral health services in 2024, citing disruptions from retail players. They will shift funds to home care, ambulatory services and telehealth that provide higher returns, according to the report.

Nearly three-quarters of healthcare CFOs plan to pursue some type of M&A deal in the year ahead, despite possible regulatory threats.

Dive Insight:

Though inflationary pressures have eased since the height of the COVID-19 pandemic, healthcare CFOs remain cognizant of managing costs amid liquidity concerns, according to the report.

The firmpolled 100 healthcare CFOs serving hospitals, medical groups, outpatient services, academic centers and home health providers with revenues from $250 million to $3 billion or more in October 2023.

Just over a third of organizations surveyed carried more than 60 days of cash on hand. In comparison, a recent analysis from KFF found that financially strong health systems carried at least 150 days of cash on hand in 2022.

Liquidity is a concern for CFOs given high rates of bond and loan covenant violations over the past year. More than half of organizations violated such agreements in 2023, while 41% are concerned they will in 2024, according to the report.

To remain solvent, 44% of CFOs expect to have more strategic conversations about their economic resiliency in 2024, exploring external partnerships, options for service line adjustments and investments in workforce and technology optimization.

Most organizations are interested in exploring sales, according to the report. Financially struggling organizations are among the most likely to consider deals. Nearly one in three organizations that violated their bond or loan covenants in 2023 are planning a carve-out or divestiture this year. Organizations with less than 30 days of cash on hand are also likely to consider carve-outs.

Organizations will also turn to automation to cut costs. Ninety-eight percent of organizations surveyed had pilotedgenerative AI tools in a bid to alleviate resource and cost constraints, according to the consultancy.

“Healthcare leaders believe AI will be essential to helping clinicians operate at the top of their licenses, focusing their time on patient care and interaction over administrative or repetitive tasks,” authors wrote. Nearly one in three CFOs plan to leverage automation and AI in the next 12 months.

However, CFOs are keeping an eye on the risks. As more data flows through their organizations, they are increasingly concerned about cybersecurity. More than half of executives surveyed said data breaches are a bigger risk in 2024 compared to 2023.

Earlier this month, we released our year-end report on hospital and health system M&A activity in 2023. As a follow-up to that report, here are our thoughts on the five most interesting transactions announced in the past year.[1]

The creation of Risant Health and its planned acquisition of Geisinger Health. This was the transaction that created the most buzz in 2023, promising the formation of a platform—supported by Kaiser Permanente—dedicated to the advancement of value-based care. Risant Health will be created by the Kaiser Foundation Hospitals and will acquire Geisinger as its first member. It will seek to add additional systems to the platform once the acquisition of Geisinger has been finalized.

Novant Health’s acquisition of three hospitals from Tenet Healthcare. This transaction represented several of the 2023 M&A trends highlighted in our year-end report. It offers an example of for-profit health system portfolio realignment: Tenet announced that the proceeds of the sale—a pre-tax book gain of approximately $1.6 billion—will be used primarily for debt retirement. It also offers an example of regional market development, as Novant continues to expand its network in North and South Carolina. And with a valuation of the deal at 16 times adjusted EBITDA—based on the $2.4 billion sale price and $150 million adjusted EBITDA reported in the press release—this transaction reflects the value of investing in high-growth markets: in this case, coastal South Carolina.

Henry Ford Health System’s joint venture with Ascension. Offering another example of regional market development, this transaction, when finalized, would also provide an example of how secular and faith-based organizations can work together in partnership. The press release announcing the transaction noted that both organizations “are committed to working to maintain the Catholic identity of the Ascension Michigan facilities included in the transaction.”

The combination of BJC Health System and Saint Luke’s Health System. This transaction, announced in May 2023, closed on January 1, 2024, and provides an example of the cross-market transactions that have emerged as a significant trend in hospital and health system M&A. Also—given the relatively close geographic alignment of the two systems—it provides another example of regional market development. It is the largest of the regional development transactions called out in our year-end report: others included the Novant/Tenet transaction described above, as well as the combination of Froedtert Health and ThedaCare in eastern Wisconsin and Vandalia Health’s development of a statewide network in West Virginia.[2]

Centura Health’s acquisition of Steward Health’s Utah care sites. In another example of a for-profit system divesting its interest in a geographic market, Steward Health announced the sale of its Utah care sites—including five hospitals and more than 35 medical group clinics—to Centura Health, which is part of CommonSpirit Health. CommonSpirit will own the assets, which will be managed by Centura Health. For Centura, the transaction offers an opportunity to enter the growing Utah market, which has demographics similar to its home base in Colorado.

We are early in the year, but 2024 has started with a bang: the announced acquisition of Summa Health, based in Akron, Ohio, by General Catalyst’s Healthcare Assurance Transformation Corporation (HATCo).[3]The acquisition, when completed, would launch HATCo on its path to fulfill one of the three goals set forth during the October 2023 announcement of its formation: “acquiring and operating a health system for the long term where we can demonstrate the blueprint of [healthcare] transformation for the rest of the industry.”

Last week, venture capital firm General Catalyst announced its plan to acquire Summa Health, an Akron, OH-based integrated delivery system with three hospitals, a large medical group, a health plan, and an annual revenue of around $2B. The terms of the deal were not disclosed, though General Catalyst previously indicated it aimed to spend $1-3B to acquire a health system.

Pending regulatory approval, Summa will convert to a for-profit entity and become a fully owned subsidiary of General Catalyst’s recently launched Health Assurance Transformation Corporation (HATCo).

HATCo, under the leadership of former Intermountain Health CEO Marc Harrison, was founded with the intention of acquiring a health system to serve as a blueprint for General Catalyst’s vision of healthcare transformation.

The Gist:While there’s a dearth of evidence for what kind of health system makes a good venture capital investment, Summa’s concentrated footprint of integrated delivery assets, robust Medicare Advantage plan, and position in an aging, yet competitive, market certainly seem attractive given HATCo’s stated goals.

If it closes, the partnership will provide Summa with an influx of capital and General Catalyst with a “proving ground” for both its vision of healthcare transformation and its portfolio of technology solutions. But while it’s one thing to get Summa’s board to sign on, General Catalyst will now have to reckon with other important stakeholders.

Summa’s physicians will be the gatekeepers of change at the local level, and their buy-in will be required for any continued push toward value-based care or successful product roll-out.

And, behind the scenes, General Catalyst will have to convince its investors that this longer-term play to rethink care delivery will offer financial returns worth the wait.

The lawsuit filed in federal court seeks to represent thousands of other UPMC employees.

Dive Brief:

A nurse is suing the University of Pittsburgh Medical Center for allegedly leveraging its monopoly control over the employment market in Pennsylvania to keep wages down and prevent workers from leaving for competitors, all while increasing their workload.

The lawsuit, filed late last week in a federal court, seeks class action status to represent other staff at the nonprofit health system. Plaintiff Victoria Ross, who worked as a nurse at UPMC Hamot in Erie, Pennsylvania, seeks damages and is asking the judge to enjoin UPMC from continuing its unfair business practices.

If granted class action status, the lawsuit could represent thousands of current and former UPMC workers, including registered nurses, medical assistants and orderlies. UPMC has denied the allegations in statements to other outlets but did not respond to a request for comment by time of publication.

Dive Insight:

UPMC has grown steadily over the past few decades into the largest private employer in Pennsylvania, employing 95,000 workers overall.

From 1996 to 2018, the system acquired 28 competing healthcare providers, greatly expanding its market power, according to the lawsuit. The acquisitions also shrunk the availability of healthcare services. Over the same period, UPMC closed four hospitals and downsized operations in three other facilities, eliminating 1,800 full- and part-time jobs, the lawsuit said.

UPMC relied on “draconian” mobility restrictions and labor law violations to lock employees into lower pay and subcompetitive working conditions, according to the 44-page complaint.

Specifically, the system enacted restraints like noncompete clauses and “do-not-rehire blacklists” to stop workers from leaving. Meanwhile, UPMC allegedly suppressed workers’ labor law rights to prevent them from unionizing.

“Each of these restraints alone is anticompetitive, but combined, their effects are magnified.UPMC wielded these restraints together as a systemic strategy to suppress worker bargaining power and wages,” the lawsuit said. “As a result, UPMC’s skilled healthcare workers were required to do more while earning less — while they were also subjected to increasingly unfair and coercive workplace conditions.”

According to the complaint, UPMC has faced 133 unfair labor practice charges since 2012, and 159 separate allegations. Roughly 74% of the violations were related to workers’ efforts to unionize, the lawsuit said.

Meanwhile, UPMC workers’ wages have fallen at a rate of 30 to 57 cents per hour on average compared to other hospital workers for every 10% increase in UPMC’s market share, said the lawsuit, citing a consultant’s economic analysis.

The lawsuit also noted that UPMC’s staffing ratios have been decreasing, even as staffing ratios on average have increased at other Pennsylvania hospitals.

The alleged labor abuses and UPMC’s market power are linked, according to the complaint.

“Had UPMC been subject to competitive market forces, it would have had to raise wages to attract more workers and provide higher staffing levels in order to avoid degrading the care it provided to its patients, and in order to prevent losing patients to competitors who could provide better quality care,” the lawsuit said.

UPMC is facing similar labor allegations. In May, two unions filed a complaint asking the Department of Justice to investigate labor abuses at the nonprofit.

Hospitals were plagued by staffing shortages during the COVID-19 pandemic. Many facilities still bemoan the difficulty of hiring and retaining full-time workers, and point to shortages (of nurses in particular) as the reason for overworked employees and poor staffing ratios.

Yet some studies suggest that’s not the case. One recent analysis of Bureau of Labor Statistics data found employment in hospitals — including registered nurses — is now slightly higher than it was at the start of the pandemic.

Despite the controversy, UPMC — which now operates 40 hospitals with annual revenue of $26 billion — continues to try and expand its market share. Late last year, the system signed a definitive agreement to acquire Washington Health Care Services, a Pennsylvania system with more than 2,000 employees and two hospitals. The deal faces pushback from local unions.

Private equity (PE) acquisitions in healthcare have exploded in the past decade. The number of private equity buyouts of physician practices increased six-fold from 2012-2021. At least 386 hospitals are now owned by private equity firms, comprising 30% of for-profit hospitals in the U.S.

Emerging evidence shows that the influence of private equity in healthcare demands attention. Here’s what’s in the latest research.

What is private equity?

There are a few key characteristics that differentiate private equity firms from other for-profit companies. At a 2023 event hosted by the NIHCM Foundation, Assistant Professor of Health Care Management at The Wharton School at the University of Pennsylvania Dr. Atul Gupta explained these factors:

Financial engineering. PE firms primarily use debt to finance acquisitions (that’s why they’re often known as “leveraged buyouts”). But unlike in other acquisitions, this debt is placed on the balance sheet of the the target company (ie. the physician practice or hospital).

Short-term goals. PE firms make the majority of their profits when they sell, and they look to exit within 5-8 years. That means they generally look for ways to cut costs quickly, like reducing staff or selling real estate.

Moral hazard. PE companies can make a big profit even if their target firm goes bankrupt. This is different from most investments where the success of the investor depends on how well the target company does.

The nature of private equity itself has serious implications for healthcare, in which the health of communities depends on the long-term sustainability and quality improvement of hospitals and physician practices. But are these concerns borne out in the real world?

PE acquisition and adverse events

A recent study in JAMA from researchers at Harvard Medical School and the University of Chicago analyzed patient mortality and the prevalence of adverse events at hospitals acquired by private equity compared to non-acquired hospitals. The study used Medicare claims from more than 4 million hospitalizations from 2009-2019, comparing claims at 51 PE-acquired hospitals and 249 non-acquired hospitals to serve as controls.

In-hospital mortality decreased slightly at PE-acquired hospitals compared to controls, but not 30-day mortality. This may be because the patient mix at PE-acquired hospitals shifted more toward a lower-risk group, and transfers to other acute care hospitals increased.

However, there were concerning results for patient safety. The rate of adverse events at PE-acquired hospitals compared to control hospitals increased by 25%, including a 27% increase in falls, 38% increase in central line-associated bloodstream infections (CLABSI), and double the rate of surgical site infections. The authors found the rates of CLABSI and surgical site infections at PE-acquired hospitals alarming because overall surgical volume and central line placements actually decreased.

What could be behind these higher rates of adverse events after PE acquisition? In a Washington Post op-ed, Dr. Ashish Jha, dean of the School of Public Health at Brown University, writes that it’s down to two things: staffing levels and adherence to patient safety protocols. “Both cost money, and it is not a stretch to connect cuts in staffing and a reduced focus on patient safety with an increased risk of harm for patients,” he writes.

Social responsibility impact

Private equity acquisitions may have a negative effect on patient safety, but what about social responsibility? In a recent report from PE Stakeholder on the impact of Apollo Global Management’s reach into healthcare, the authors use the Lown Institute Hospitals Index to understand hospitals owned by Apollo perform on social responsibility. Lifepoint Health, a health system owned by Apollo, was ranked 222 out of 296 systems on social responsibility nationwide. And in Virginia, North Carolina, and Arizona, some of the worst-ranked hospitals in the state for social responsibility are those owned by Lifepoint Health, the PE Stakeholder report shows.

Apollo Global Management is the second largest private equity firm in the United States, with $598 billion total assets under management, according to thereport. The PE stakeholder report outlines concerning practices by Apollo, including putting high levels of debt that lowers hospitals’ credit ratings and increases their interest rates, cutting staff and essential healthcare services, and selling off real estate for a quick buck. If we care about hospital social responsibility we should clearly be concerned about private equity acquisitions.

The bigger picture

Private equity buyouts did not come from out of nowhere, so what does this trend tell us about our healthcare system? PE acquisitions are in many ways a symptom of larger issues in healthcare, such as increasing administrative burden, tight margins, and lack of regulation on consolidation. For owners of private physician practices that face a lot of administrative work, deciding to sell to a PE firm to reduce this workload and focus on patient care (not to mention, getting a hefty payout) is a tempting proposal.

In the Washington Post, Ashish Jha describes what made his colleague decide to sell his practice to a PE firm: “The price he was getting was very good, and he was happy to outsource the headache of running the business (managing billing, making sure there was adequate coverage for nights and weekends, etc.).”

“In many ways, private equity is both a response to and an accelerator of broader health system trends – one in which consolidation is happening quickly, care is being delivered by larger and larger entities, and corporate influence is growing.”Jane M. Zhu, MD, MPP, MSHP, Associate Professor of Medicine at Oregon Health & Science University, at NIHCM Foundation Event

PE buyouts are also indicative of a larger trend, what some researchers call the “financialization” of health. As Dr. Joseph Bruch at the University of Chicago and colleagues describe in the New England Journal of Medicine, financialization refers to the “transformation of public, private, and corporate health care entities into salable and tradable assets from which the financial sector may accumulate capital.”

Financialization is a sort of merging of the financial and healthcare sectors; not only are financial actors like private equity buying up healthcare providers, but healthcare institutions are also acting like financial firms. For example, 22 health systems have investment arms, including nonprofit system Ascension, which has its own private equity operation worth $1 billion. The financialization of healthcare is also reflected in the boards of nonprofit hospitals. A 2023 study of US News top-ranked hospitals found that a plurality of their board members (44%) were from the financial sector.

What we can do about it?

What can we do to mitigate harms caused by PE acquisitions? In Health Affairs Forefront, executive director of Community Catalyst Emily Stewart and executive director of the Private Equity Stakeholder Project Jim Baker provide some policy ideas to stop the “metastasizing disease” of private equity:

Joint Liability. Currently PE firms can put all of their debt on the balance sheet of the firm they acquire, letting them off the hook for this debt and making it harder for the acquired company to succeed. “Requiring private equity firms to share in the responsibility of the debt…would prevent them from making huge profits while they are saddling hospitals and nursing homes with debts that ultimately impact worker pay and cut off care to patients,” write Stewart and Baker.

Regulate mergers. Private equity acquisitions often go under the radar because the acquisitions are small enough to not be reported to authorities. But the U.S. Federal Trade Commission could be more aggressive in evaluating mergers and buyouts by PE, as they have done recently in Texas, where a PE firm has been buying up numerous anesthesia practices.

Transparency of PE ownership. It can be hard to know when hospitals are bought by a PE firm. The Department of Health and Human Services could require disclosure of PE ownership for hospitals as they have done for nursing homes.

Remove tax loopholes. The carried interest loophole allows PE management fees to be taxed at as capital gains, which is a lower rate than corporate income. Closing this loophole would remove a big incentive that makes PE buyouts so attractive for firms.

“It is clear that the problem is not the lack of solutions but rather the lack of political will to take on private equity,” write Steward and Baker.

We need not to not only stem the tide of PE acquisitions sweeping through healthcare, but address the financialization of healthcare more broadly, to put patients back at the center of our health system.

Private equity firm Apollo Global Management’s ownership of two large health systems — Louisville, Ky.-based ScionHealth and Brentwood, Tenn.-based Lifepoint Health — downgrades hospital services, hurts workers and puts patients at risk, according to a study published Jan. 11 by the Private Equity Stakeholder Project.

Since acquiring Lifepoint in 2018 and spinning off ScionHealth in 2021, Apollo has consolidated ownership of 220 hospitals in 36 states, with a workforce of about 75,000 employees. Many of the hospitals have experienced service cuts, layoffs, poor quality ratings and regulatory investigations, according to the report.

The report comes amid rising scrutiny of private equity hospital ownership.

In December, the Senate Budget Committee launched an investigation into the effects of private equity ownership on hospitals that specifically mentioned Apollo’s ownership of Lifepoint. Iowa Sen. Chuck Grassley and Rhode Island Sen. Sheldon Whitehouse requested “documents and detailed answers” about certain hospital transactions and the degree to which private equity firms are calling the shots at hospitals.

A Harvard Medical School-led study published Dec. 26 in JAMA also found that hospitals that are bought by private equity-backed companies are less safe for patients. On average, patients at private equity-purchased facilities had 25.4% more hospital-acquired conditions, according to the study.

“Apollo’s purchase of these hospital systems follows a disturbing pattern of harm caused by the growing influence of private equity in the healthcare sector,” PESP Healthcare Director Eileen O’Orady, said in a news release. “Private equity’s utmost priority to maximize short-term profit over the long-term viability of the companies it controls leads to excessive debt, cost cutting, worse outcomes for patients and deteriorating working conditions for employees. Apollo’s management of its hospitals seems to follow the usual playbook.”

The study, “Apollo’s Stranglehold on Hospitals Harms Patients and Healthcare Workers,” was developed in conjunction with the American Federation of Teachers and the International Association of Machinists and Aerospace Workers. Clickhere to access the full report.

Apollo, Lifepoint and ScionHealth did not respond to Becker’s request for comment.

The Nelson A. Rockefeller Institute of Government is a public policy think tank founded in 1981 that conducts cutting-edge research and analysis to inform lasting solutions to the problems facing New York State and the nation.

Introduction & Definitions

In 2023, I noted10 trends within three broad categories in healthcare worth watching and provided a mid-year update on those trends. They included: the impact of unwinding the Public Health Emergency on insurance coverage, healthcare workforce shortages, price inflation, declining margins at hospitals, private equity in healthcare, consolidations, alternate payment models, attention to health equity, digital telehealth expansion, and the expansion of non-traditional providers in healthcare. These trends continue to be worth watching in 2024.

More significant than any one of these trends is the combined interaction of the trends in the industry overall—what I’ll call a “mega-trend,” which results in a trifurcation of the industry. Currently, there are parts of the healthcare industry struggling to exist. This is due to different factors, including high expenses, staffing challenges, and a lack of access to capital and technology, among other things. I call the types of healthcare entities that fall into this category “Today” entities because they exist now but may or may not exist in the future. In contrast, there is another set of entities in healthcare that have emerged in the last five or so years. They are becoming larger through consolidation and integration, and have greater access to capital and technology. I call these types of healthcare entities the “Tomorrow” entities because their size, resources, and forward-looking strategies are changing the future of healthcare.

In between these two categories, are existing and traditional entities in healthcare that seek sustaining strategies. I call these entities the “Striving Survivors” whose success and ability to persevere is still an open question. Most look like the healthcare entities of Today, but what distinguishes them is their ability to partner, use technology, and diversify what they offer. To understand the mega–trend phenomena of this trifurcation in healthcare and what’s happening within and across each of these three categories, this blog dissects how the trends I highlighted in 2023 are impacting the Today and the Tomorrow entities and discusses how the Striving Survivors are attempting to keep pace as the healthcare industry evolves.

The “Today” Healthcare Entities

As noted in my 2023 blog,price inflation and expense growth—particularly as they relate toworkforce and labor costs—were two trends impacting existing healthcare organizations. Today’s healthcare entities are heavily reliant on people, and, unsurprisingly, increased expenses for personnel, which had a major impact on organizations’ bottom lines for the past few years, as did general inflation and increased supply prices. However, for some providers, revenue and patient volume have returned to levels comparable to pre–pandemic. According to Kaufman Hall, a healthcare consulting firm, by the end of 2023, some hospitals’ margins were beginning to stabilize.

In looking at what may happen in 2024 for providers, however, the return of patient volume and, therefore, more predictable revenue may not be enough to yield positive margins. This is because expenses are predicted to be challenging. Industry experts estimate that healthcare prices will grow 7 percent in the coming year. The estimate reflects increases in pharmaceutical costs, growing provider expenses given the high labor and supply costs noted earlier, and insurer rate increases.

Another challenge to the healthcare entities of Today is the availability of capital to make strategic investments. More of this capital is now being provided by private equity firms, an estimated $750 billion in the last decade. To secure capital in the private market, bond rating agencies typically favor larger providers because they are less risky. This, among other factors, has contributed to growing consolidation in the industry among physician groups, insurers, and hospitals. Not only do these entities need capital for projects like upgrades to existing facilities, but to also make strategic investments. Such investments include acquisitions of other providers or companies that add to the revenue base, or technologies that allow improvements in care delivery.

The Today entities are increasingly challenged with adapting to consumer demands for tech–enabled care options. Consumers want more tech–supported smart applications that allow them to book appointments or get assistance with care more quickly via chatbots. Consumers also want new options for care at home—including hospital–at–home, which provides acute care in a home-based setting, and home–based care. As noted in my November blog on AI in healthcare, access to such technologies is not only creating further separation between healthcare entities, but can also create further inequities among consumers.

The “Tomorrow” Healthcare Entities

With the challenges for the healthcare entities of Today outlined above, it is important to note that those same challenges are not as significant for the healthcare players of Tomorrow. This is because most are substantial in size and have sufficient revenue, technology, and capital resources—often in the form of private equity. And many of them did not start in healthcare. They include, for example, Amazon—which started as an online bookstore and now has annual revenues of over $500 billion, CVS—which started as a retail pharmacy and now has revenues close to $300 billion; Uber—which started as a tech-enabled taxi-like transport application and now has revenues of over $30 billion, and Microsoft—which started as computer company but has expanded into healthcare with annual revenues of over $200 billion.

Some of these companies have entered healthcare by partnering with, or acquiring companies already in the sector such as Amazon’s 2023 acquisition of One Medical, a tech–enabled primary care entity; the 2022 partnership between United Health Group and Change Healthcare, a technology company; and CVS’s official 2023 acquisition of Signify, a home health organization. This was on top of CVS’s earlier (2018) merger with health insurance company Aetna, and its 2022 partnership announcement with Uber with the stated aim of improving access to care and decreasing health inequities in underserved communities across the country. Other entities have increased their footprint in healthcare by launching their products, such as Microsoft’s 2020 launch of Cloud services, specifically for healthcare. Some of these companies are now collaborating, including the 2021 partnership between CVS Health and Microsoft, which was designed to customize care further, enable frontline workers to more easily access and use data, and digitize operations.

In addition to these large nontraditional healthcare entities, the health insurance industry has also experienced large–scale consolidation and diversification that enables them to compete. One of the most notable companies in the world of healthcare integration is the nation’s largest insurer, United Health Group (UHG). UHG continued to outpace provider margins, with 2023 third quarter margins for UHG at levels 14 percent higher year-over-year. The continued growth at UHG was largely due to the increasing number of individuals served and a growing provider base of 90,000 physicians, or 10 percent of all physicians nationwide. This contrasts with one of the largest provider margins (Kaiser) whose 2023 third-quarter margin was only $239 million, an improvement from the $1.5 billion loss they experienced in the third quarter from the previous year. Although no other insurers are as big as UHG, the next biggest including, Aetna, Anthem, Cigna, and Humana all had 2023 third–quarter net incomes ranging from $1 billion to $1.4 billion.

The Striving Survivors

Not all traditional healthcare entities are being left behind; I call these the Striving Survivors. They may currently be considered Today entities, but they are attempting to put in place strategies so they can be Tomorrow entities in the future. Here are three primary strategies that may help these entities survive into the future:

Partnering—The number of independent hospitals as well as the number of independent physician groups has shrunk dramatically in the past decade, and there is increasing pressure for both to consider merging. A report by Kaufman Hall prepared at the request of the American Hospital Association, shows that merging can have advantages such as creating economies of scale, improving leverage to bargain for better payments from increasingly large insurance companies, and allowing better access to capital markets. Other advantages to partnering include diversifying what services can be offered to patients, allowing providers to assume risk for the care of a larger population, or leveraging complementary strengths for strategic investments. Although many of these consolidations used to be regional in nature (providers would merge with neighboring providers), new mergers are occurring across broader geographic areas, as was the case with the merger of west–coast–based Kaiser and Pennsylvania-based Geisinge.

Maximizing Technology—Striving Survivors are also seeking to compete and survive into the future by partnering to maximize technology. Technologies like telehealth, remote monitoring, artificial intelligence, and hospital–at–home, are growing because they are delivering care in ways that are preferable to consumers. As recently noted by Deloitte, “Adopting new technologies and business models—while under sustained financial pressure—might be the biggest challenge health care executives will face in 2024.” The good news for the healthcare players of Today is the use of data and technology in new and creative ways can counteract some of their current financial and care delivery challenges. Technology can make care more convenient for consumers, reduce costs, or provide care in places where it is sometimes inaccessible. Some recent examples of partnerships between technology companies and today’s healthcare entities include women’s health tech startup Tia’s partnership with Common Spirit, one of the largest healthcare systems in the country. Similarly, Strive Health is managing kidney patients for Bon Secours Mercy Health; Carbon Health is providing tech–enabled urgent care for Milwaukee–based Froedtert Health. Even Best Buy, a home electronics store, has begun offering homecare through several partnerships, including, for example, Mass General Brigham.

Revenue Diversification—Revenue diversification has long been a growth strategy in many industries. Up until recently, there hasn’t been the same pressure for such diversification for healthcare entities. That is changing, in part, because many of the healthcare entities of Tomorrow come from non–health–related industries. Diversification can occur using either of the strategies noted above (partnership or maximizing the use of technology). Diversification might also include providing services in areas of healthcare where demand is growing (e.g. urgent care or outpatient instead of legacy inpatient services). It might also include services that are not currently widely used but are likely to become more commonplace in the future, such as precision medicine or hospital–at–home.

Conclusion

In 2024, it will not only be important for healthcare policymakers to monitor single trends such as the continued focus on health equity, the expansion of alternate payment models, or the cost of the healthcare workforce, but it will also be important to understand how trends may be interacting with each other to create larger market trends. Such is the case for the emergence of non-traditional players in healthcare, the influx of private equity, digital expansion, and major consolidations— which when combined —are resulting in a mega trend of trifurcation of the industry into Today, Tomorrow, and Striving entities in healthcare that are seeking to survive into the future. For healthcare policymakers, all these trends along with their interaction will be worth monitoring and understanding so that effective policies can be developed that result in a healthcare system that supports innovation, protects patients, reduces inequities, and results in better health outcomes at lower cost.

The new year dawned on a health insurance industry beset by challenges.

Only 7% of health plan executives view 2024 positively after being hammered by the coronavirus pandemic, regulatory turbulence and rising cost pressures, according to a Deloitte survey.

Costs are spiking, and health insurers remain uncertain how the lingering effects of COVID-19 will impact care utilization. Medicaid redeterminations are rewriting the coverage landscape state by state, while Medicare Advantage — the darling of payers’ business sheets — experiences significant regulatory upheaval.

Meanwhile, 2024 is a presidential election year. That’s adding more political uncertainty into the picture as Washington hammers payers over claims denials and the business practices of pharmacy benefit units.

Here’s what experts see coming down the pike for health insurers this year.

The uninsured rate will go up

The number of Americans without insurance coverage is almost certainly going to rise this year as states overhaul their Medicaid rolls, experts say.

During the pandemic, continuous enrollment protections led a record number of people to enroll in Medicaid. But earlier this year, states resumed checking eligibility for the safety-net program. Around 14.4 million Americans have been removed from Medicaid due to the redeterminations process, many for administrative reasons like incorrect paperwork despite remaining eligible.

“We are going to see an increase in the uninsured rate for children and probably adults as well as a consequence,” said Joan Alker, executive director of the Georgetown University Center for Children and Families.

The question is how big of an increase, experts said. Redeterminations began in April, but lagging information and state differences in data reporting has made it difficult to determine where individuals are turning for coverage, and in what numbers.

Early signs suggest some people losing Medicaid have found plans in the Affordable Care Act exchanges, though it’s probably “a very small percentage,” Alker said. More than 20 million people have signed up for ACA coverage since open enrollment began in November — an all-time high, according to data released by the Biden administration in early January.

Experts say the growth is due in part to redeterminations, along with the effects of more generous federal subsidies. Those subsidies are slated to expire in 2025, meaning ACA enrollment should stay elevated until then.

But it’s unlikely everyone who loses Medicaid will find a home on the marketplaces. The cost of family coverage without an employer remains out of reach for many Americans. It’s also too early to determine how many people terminated from Medicaid have shifted into employer coverage — that data should also emerge as 2024 continues, said Matt Fiedler, a senior fellow with the Brookings Schaeffer Initiative on Health Policy.

Federal regulators have also taken a number of actions to try and curb improper procedural Medicaid losses, like cracking down on states with high levels of child disenrollments. Yet, procedural terminations are unlikely to improve significantly this year, experts said.

“We do see a very hopeful trend” in some states, like Washington and Oregon, embracing longer periods of continuous eligibility, Alker noted.

The government has ramped up ACA marketplace outreach, which — along with macro forces like a strong labor market — are positive signs that individuals no longer eligible for Medicaid may find alternative coverage, whether in the ACA exchanges or through employment.

But “it’s likely we’ll see an increase in the uninsured rate. I think the question is how much,” Fiedler said.

Increasing vigilance around costs

Healthcare costs are projected to grow much faster in 2024 than the historical average, fueled by inflation, supply chain disruption and labor pressures increasing provider wages. Those costs are burdening employers already stressed by worker mental health and deferred preventive screenings that could worsen health conditions down the line.

As a result, employers are investing heavily in mental health and substance use disorder services. Seven out of ten employers say mental healthcare access is a priority in 2024, and employers say they’ll turn to virtual care providers to address the need, according to a Business Group on Health survey.

As a result, employers are increasingly demanding integrated platforms combining different benefits, continuing a pivot away from the point solutions they were deluged with during the pandemic. Payers are racing to meet that need.

This year, UnitedHealthcare plans to integrate more than 20 standalone products into a “supported benefits platform,” said Dan Kueter, CEO of the payer’s employer and individual business, during an investor day in November.

Cigna, which focuses on employer-sponsored plans, plans to add more services to its behavioral health navigator to help employers personalize the platform for their employees this year, said CEO David Cordani during a November earnings call.

For their part, health insurers are likely to raise premiums and combat hospital reimbursement hikes in 2024 to control costs, according to credit rating agency Fitch Ratings.

However, that outlook is complicated by uncertainty around how much elevated care utilization seen in 2023 will continue. Some payers, like UnitedHealth and Humana, are forecasting high utilization, while others like CVS have said they expect it to drop.

More payers might pursue mergers and acquisitions or build out internal musculoskeletal management programs to control costs, said Prateesh Maheshwari, a managing director at venture capital firm Maverick Ventures. Hip and knee surgeries were an oft-cited driver of utilization last year.

Still, publicly traded health insurance companies could see their margins moderately decrease in 2024, Fitch said.

GLP-1 coverage will increase — slowly

Surging demand for GLP-1s means insurance coverage for the drugs is expected to increase next year, putting more stress on the nation’s pressured healthcare payment system. GLP-1s, or glucagon-like peptide-1 drugs, have historically been used to treat diabetes but have shown efficacy in weight loss.

The drugs are exceedingly expensive, butthat hasn’t stopped peoplefrom trying to get theirhands on GLP-1s — off-label or not. TD Cowen predicts GLP-1 sales could reach $102 billion by 2030, with $41 billion of that for obesity.

More private payers are considering covering the drugs next year, though the doors to coverage aren’t being thrown wide open. According to a November survey by the International Foundation of Employee Benefit Plans, while 76% of employers provide GLP-1 drug coverage for diabetes, just 27% provide coverage for weight loss.

Yet, 13% are considering adding coverage for weight loss.

As insurance coverage increases, payers will ensure only eligible patients are accessing the drugs through checks like step therapy, said Nathan Ray, head of healthcare M&A at consultancy West Monroe. As a result, access could remain restricted.

Payers will also tie coverage for GLP-1s to additional behavioral management programs. That trend has proved a gold rush for chronic condition management companies and telehealth providers, which have rushed to stand up new business lines for weight loss that include GLP-1s.

“Things like this, that include the opportunity for medication along with the accompaniment of behavioral change, is where I think the market will go in 2024,” said Heather Dlugolenski, Cigna’s U.S. commercial strategy officer.

Proponents of weight loss medication are also eyeing a potential overturn of the ban on Medicare coverage of weight loss drugs next year. A growing number of lawmakers (and drugmakers standing to profit from Medicare coverage) have come out in support of a bill introduced in 2023 to allow Medicare to cover anti-obesity drugs.

The bill is unlikely to be prioritized given Washington has a lot on its plate during the election year, but passage isn’t out of the realm of possibility, experts said.

Medicare Advantage will continue to grow under Washington’s watchful eye

In MA, the government contracts with private insurers to manage the care of Medicare seniors. MA has become increasingly popular, swelling to cover 31 million people last year — a boon for insurers offering the coverage, which can be twice as profitable for private payers than other types of plans.

As such, MA plans have been advertising heavily, trumpeting their supplemental benefits like gym memberships or subsidized groceries. Seniors find those benefits attractive, Brookings’ Fiedler said, and may not understand that MA plans may not cover as much medical care as traditional Medicare.

”My best bet would be MA enrollment in the near term continues to grow,” Fiedler said. “I don’t think we’re at the ceiling yet.”

Despite elevated costs in 2023 from seniors using more medical care, insurers generally didn’t cut back on plan benefits this year as they continue to compete for members.

Yet, the program hasn’t been without its complications. Payers cried foul last year over tweaks to MA rates, star ratings and reimbursement audits, with Humana and Elevance suing to stop the changes.

MA “should remain a key long-term growth driver for managed care, but we see a more challenging setup in 2024 as weaker funding, risk coding changes, and lower Star ratings combine to pressure margins,” J.P. Morgan analysts wrote in an outlook report published late last year.

Insurers were also plagued in 2023 by congressional hearings and lawsuits over their claims reviews processes, sparking criticism that seniors may not be receiving the care they’re due.

Scrutiny from Washington around such practices is likely to continue.

“We are seeing both in the Senate and House a lot of interest in peeling back the layers of the onion of how big health plans are operating their Medicare Advantage programs. That’s going to continue to be an issue,” said Reed Stephens, a healthcare chair at law firm Winston & Strawn who focuses on risk.

Though it’s unlikely that legislation will be passed reforming MA, Reed said. Overall, regulatory and political turbulence should subside somewhat this year.

The rate and marketing changes were “short of the last train out of the station,” said Brookings’ Fiedler. “The administration is unlikely to want a big fight with MA plans in an election year.”

The Mark Cuban effect: Payers with PBMs will launch more ‘transparent’ options

Major pharmacy benefit managers will introduce more options billed as transparent and cost-effective to retain clients after some turned to upstart competitors last year.

PBM clients are clamoring for outcomes-based pricing, with structures tying PBM compensation to measures like adherence, according to a J.P. Morgan survey from late 2023. Clients also want transparency, whether more data sharing or full administration models.

The changes aren’t revolutionary, but they hint at ongoing distrust of major PBMs from benefits teams, J.P. Morgan said.

UnitedHealth’s Optum Rx, Cigna’s Express Scripts and CVS Caremark — which together control 80% of prescriptions in the U.S. — have all recently launched new programs, partnerships or models they say are more affordable and transparent to meet the demand.

The industry is likely to see more moves along those lines in 2024, experts say — especially as Congress considers legislation to reform PBMs. The Lower Costs, More Transparency Act passed the House in December. The bill is seen as unlikely to clear the Senate, but specific measures, like forced PBM transparency, could make it into larger legislative packages.

The passing of measures around transparency could satisfy politicians’ need for a win when it comes to drug pricing without creating meaningful reform in the sector, according to Jefferies analyst Brian Tanquilut.

Yet, momentum to do something about high drug costs will certainly carry into this year. Presidential candidates on both sides of the aisle are expected to wield the issue on the campaign trail.

“The companies in those markets are going to have to stay nimble and keep on their toes,” said Winston & Strawn’s Stephens.

M&A, especially vertical integration, carries on

Companies like UnitedHealth, CVS and Humana will continue building out networks of physical care sites in 2024. New M&A guidelines from the Department of Justice and Federal Trade Commission could raise the bar for merger approvals, but the value proposition for insurers to acquire healthcare providers is too high for them to be dissuaded, experts said.

Payers will continue to pursue as many deals “as they can find willing, available targets,” said West Monroe’s Ray.

By directing members to owned locations for medical needs, health insurers can essentially pay themselves for providing a service, keeping more revenue in-house. As a result, payers — especially those with a large presence in MA, which incentivizes organizations to better manage cost — will stay on the hunt for acquisition targets.

While healthcare M&A was relatively slow in 2023, 68% of senior leaders in the sector expect deal volume to rise in 2024, according to a survey by investment bank Jefferies.

Optum — which employs or is affiliated with around one-tenth of all doctors in the U.S. — is already eyeing M&A. The health services arm of UnitedHealth is currently pursuing an acquisition of a physician-owned clinic chain in Oregon, even as it comes off a number of big provider buys in 2023, including the multi-billion-dollar acquisitions of home health providers Amedisys and LHC Group.

Cigna has also said it plans to look for smaller strategic acquisitions to grow its business, after a potential merger with rival Humana crumbled late last year.