Walgreens’ decision to slash VillageMD’s clinical footprint has reverberated to the financial accounts of the primary care chain’s minority owner — Cigna.

Dive Brief:

Cigna has written off more than half of its multibillion-dollar investment in VillageMD amid the declining value of the primary care chain.

Cigna invested $2.5 billion into VillageMD in late 2022, with the goal of accelerating value-based care arrangements for employer clients by tying VillageMD’s physician network with Cigna’s health services business, Evernorth — hopefully reaping profits from shared savings as a result.

But on Thursday, Cigna wrote off $1.8 billion of that investment, citing VillageMD’s lackluster growth after its majority owner Walgreens elected to close underperforming clinics. The writedown drove Cigna’s shareholder earnings down to a net loss of almost $300 million, compared to profit of $1.3 billion in the same time last year.

Dive Insight:

Overall, Cigna’s first-quarter performance was solid, especially amid the mixed results of its insurer peers, analysts said. The Connecticut-based payer grew its revenue 23% year over year to $57.3 billion.

Yet Cigna’s bet on VillageMD is a new thorn in its side, as the investment’s value becomes increasingly bogged down by Walgreens’ operational decisions, along with broader challenges in the primary care sector.

Walgreens began closing underperforming VillageMD centers last year in a bid to force the segment to profitability, and quickly blew past its initial goal of 60 closures. Now, the retailer expects to close 160 clinics overall, majorly downsizing VillageMD’s footprint.

That decision is reverberating to the financial accounts of VillageMD’s minority owner — Cigna.

“The writedown was largely driven by some broader market dislocation that is hitting the space … as well as Village determining that they are going to pull in supply lines and constrain some of the growth in some of the new clinics that they were establishing,” CEO David Cordani told investors on a Thursday morning call.

However Cigna’s priorities for VillageMD remain unchanged, management said. Cigna is still aiming to link VillageMD’s primary care centers to its own clinical assets to build a high-quality provider network that can serve its own patients, and those of health plan and employer clients.

The partnership has already launched in four markets, and the companies plan to continue scaling, according to Cordani.

“At the macro level our strategic direction in terms of what we are seeking to innovate with Village has not changed despite the writedown of the asset,” Cordani said, though “no one likes a writedown of the asset.”

In the quarter, Cigna’s health benefits segment emerged unscathed by headwinds that buffeted other major payers: notably, spending and regulatory pressure in Medicare Advantage.

Yet the majority of Cigna’s business is with employer clients, which served as a “well-underwritten shelter from the MA storms,” TD Cowen analyst Gary Taylor wrote in a Thursday morning note.

Cigna is planning on getting out of Medicare coverage altogether, having agreed in January to sell its Medicare business to Chicago-based insurer Health Care Service Corporation. That deal remains on track, executives said, after a key waiting period for antitrust regulators to challenge the deal came and went in mid-April. The divestiture is expected to close in early 2025.

Cigna’s medical loss ratio — a marker of how much in premiums insurers spend on patient care — was 79.9% in the quarter, better than analysts had expected. Cigna did see higher utilization in areas like inpatient care for employer-sponsored members in the quarter, but the payer’s pricing decisions for its plans covered the trend, executives said.

Cigna cut its MLR guidance for 2024, along with raising earnings expectations. The insurer now expects an MLR between 81.7% and 82.5% this year, suggesting management is confident in their ability to control medical costs, J.P. Morgan analyst Lisa Gill wrote in a Thursday note.

CVS, which previously held the contract, cited its loss as a factor in declining revenue and income for its pharmacy benefit management business on Wednesday.

Cordani specifically called out specialty pharmacy — which already represents a major portion of Evernorth’s revenue — as an “accelerated growth opportunity” for the business.

Roughly a week ago, Evernorth announced it will have an interchangeable Humira biosimilar for $0 out-of-pocket cost for eligible patients of its specialty pharmacy arm, Accredo.

Currently, 100,000 Accredo patients use Humira or a biosimilar for the frequently prescribed immune disease drug, which has long been the top-selling drug for its manufacturer AbbVie. In addition, all of its PBM clients and patients will have access to the biosimilars, according to Cordani.

Evernorth has also taken steps to ramp up coverage of GLP-1s, expensive diabetes drugs that have soared in popularity for weight loss. In March, the company announced cost-sharing agreement for GLP-1s covered in a condition management program, to insulate health plan and employer clients from the soaring costs of the medication.

The program has seen “strong interest,” and Evernorth has enrolled more than 1 million people in it to date, Cordani said.

Sometimes a health policy story comes along that should be shouted from the rafters — well at least reported by media that cover the subject. Brett Arends’ story for Dow Jones’ MarketWatch is one of those stories.

The revelations about overpayments come from the Medicare Payment Advisory Commission, MedPAC for short, some of whose recommendations over the years have resulted in high rate increases for Advantage plan sellers that helped make it possible for them to offer groceries, bits of dental care, and other goodies seniors have snapped up. The media’s role in revealing and dissecting those overpayments is long overdue.

The last several months news outlets have been paying more attention to the downsides of Medicare Advantage plans.

Arends’ story focused on one thread in the story: MedPAC’s latest report to Congress that revealed something health policy wonks — but not the public — have known for a long time. Medicare Advantage plans are taking advantage of the federal gravy train.

“The private insurers who now run more than half of all Medicare plans are overcharging the taxpayers by a staggering $83 billion a year,” Arends wrote. “They are charging us taxpayers 22% more than it would cost us to provide the same health insurance to seniors directly if we just cut out the private insurance companies as middlemen.”

MedPAC was set up by the Balanced Budget Act of 1997, “back when people in Washington were actually doing their jobs,” Arends points out. The commission’s job is to advise Congress on issues involving Medicare. MedPAC reports discuss the financial situation of the Medicare trust funds, and over the years those reports often revealed that the private health plans have been overpaid. Until recently, there has been little to no pushback from the government or most of the media, in effect leaving the insurance industry a clear path to sell Medicare Advantage plans to more than half of the Medicare market. The media have recently begun to ask why.

Arends calls the Medicare Advantage arrangement “a rip-off, pure and simple,” noting that what sellers of the plan are paid “is more than twice as much as it would cost simply to provide free dental, hearing and vision care to all traditional Medicare beneficiaries, not just those in private ‘Medicare Advantage’ plans.”

I have covered Medicare for decades now and have often asked the experts why there couldn’t be a level playing field that would allow beneficiaries in the traditional program to receive vision and dental benefits. The answer was always, “We can’t afford that.”

Arends debunks that thinking by directly quoting the MedPAC report:

“It reads: ‘We estimate that Medicare spends approximately 22 percent more for MA enrollees than it would spend if those beneficiaries were enrolled in FFS (fee for service or traditional) Medicare, a difference that translates into a projected $83 billion in 2024.’ MedPAC reported that its review of private plan payments suggests that over the 39-year history with private plans, they “have never yielded aggregate savings for the Medicare program. Throughout the history of Medicare managed care, the program (Medicare Advantage) has paid more than it would have paid if beneficiaries had been in FFS (fee for service) Medicare.”

I checked in with Fred Schulte, who now writes for KFF Health News, and who over his career has written many prize-winning stories documenting the shenanigans insurers have used to enhance their reimbursements from Medicare, such as upcoding. That’s the practice of billing Medicare for ailments that are more serious than what patients actually have. “For example, instead of reporting a patient has diabetes, the insurers would say diabetes with neuropathy or eye problems and receive higher reimbursement,” he explained.

“It took a very long time for the government and the Justice Department to understand what was going on here with this coding,” Schulte said. “The codes just kept getting higher and higher, and profits kept going up and up.”

A year ago, Paul Ginsburg, a senior fellow at the University of Southern California’s Schaffer Center, said, “The current Medicare Advantage structure results in overpayments, markedly higher than previously understood.”

Even Michael Chernow, who heads the Medicare Payment Advisory Commission authorized by Congress in 1997, recently admitted on Twitter that Medicare Advantage “has never saved Medicare money.” But he added, “that doesn’t mean Medicare Advantage isn’t a key pillar of Medicare sustainability. At its best it can provide better care at lower cost.”

Arends’ story doesn’t sound hopeful about the direction of Medicare. He concludes, “Medicare Advantage isn’t making the rest of Medicare better. It is putting the rest of Medicare out of business. And not by being more efficient, but by being less efficient. It is driving up the overall cost of Medicare by 22%. And not by being more efficient but by being less efficient.

The logical outcome is that traditional Medicare ceases to exist and that Medicare dollars pass through the hands of private insurance companies at 122 cents on the dollar.”

Arends’ prediction may well come true, but perhaps not without a fight. David Lipschutz, associate director at the Center for Medicare Advocacy, says a “confluence of factors have come together to make it harder to ignore the problems of Medicare Advantage by the press and policymakers.”

After covering the Medicare privatization crisis for over two years, an investigative reporter takes a step back and examines what’s at stake.

Medicare, the country’s largest and arguably most successful health care program, is under duress, weakened by decades of relentless efforts by insurance companies to privatize it.

A rapidly growing Medicare Advantage market — now 52% of Medicare beneficiaries, up from 37% in 2018 — controlled by some of the largest and most powerful corporations in the world, threatens to both drain the trust fund and eliminate Medicare’s most important and controversial component: its ability to set prices.

It is not an overstatement to call it a heist of historic proportions, endangering the health not only of the more than 65 million seniors and people with disabilities who depend on Medicare but all Americans who benefit from the powerful role that Medicare has historically played in reining in health care costs.

The giant corporations that dominate Medicare Advantage have rigged the system to maximize payments from our government to the point that they are now being overpaid between $88 billion and $140 billion a year. The overpayments could soar to new heights if the insurers get their way and eliminate traditional Medicare.

All of America’s seniors and disabled people who depend on Medicare could soon be moved to a managed care model of ever-tightening networks, relentless prior authorization requirements and limited drug formularies. The promise of a humane health care system for all would be sacrificed at the altar of the almighty insurer dollar.

The Medicare Payments Advisory Commission (MedPAC), the independent congressional agency tasked with overseeing Medicare, last month released a searing report which found that Medicare spends 22% more per beneficiary in Medicare Advantage plans than if those beneficiaries had been enrolled in traditional fee-for-service Medicare. That’s up from a 6% estimate in the prior year.

A similar cost trend exists for diagnosis coding.

Medicare Advantage plans and their affiliated providers increasingly upcoded diagnoses to get higher reimbursements. In 2024, overpayments due to upcoding could total $50 billion, according to MedPAC, up from $23 billion in 2023. These enormous overpayments drive up the cost of premiums — MedPAC’s conservative estimate is that the premiums paid to Medicare out of seniors’ Social Security checks will be $13 billion higher in 2024 because of those overpayments.

There is evidence that Americans and lawmakers are starting to wake up.

Medicare Advantage enrollment growth slowed considerably in 2023. Support within the Democratic Party for Medicare Advantage is cratering. In 2022, 147 House Democrats signed an industry-backed letter supporting Medicare Advantage. This year, just 24 House Democrats signed the letter. Earlier this month, the Biden administration cut Medicare Advantage base payments for the second year in a row(while still increasing payments overall), over the fierce opposition of the insurance lobby. The investment bank Stephens called Biden’s decision a “highly adverse” outcome for insurers. Wall Street has taken note, punishing the stock price of the largest Medicare Advantage insurers, with Barron’s noting that Wall Street’s “love affair” with Humana is “ending in tears.” The cargo ship is turning. It is up to us to determine if that will be enough.

We can’t attack a problem if we don’t know how to diagnose it. I spoke with some of the most knowledgeable critics of Medicare Advantage about the danger the rapid expansion of Medicare privatization presents to the American public.

Rick Gilfillan is a medical doctor who in 2010 became the first director of the Center for Medicare and Medicaid Innovation (CMMI). He would go on to serve as CEO of Trinity Health from 2013 to 2019. In 2021 he launched an effort to halt the involuntary privatization of Medicare benefits.

“Right now, all investigations are finding tremendous overpayments,” Gilfillan said. “The overpayments are based on medical diagnoses that may or may not be meaningful from a patient care standpoint. Insurers are using chart reviews, nurse home visits and AI software to find as many diagnoses as possible and thereby inflate the health risks of the patients and the premium they get from Medicare. The overpayments are just outrageous,” he said.

The problem could get worse if the Supreme Court curtails the powers of regulatory agencies, as it may do this year. “It would make a huge difference in what CMS would be able to do,” Gilfillan said.

The logic behind Medicare privatization is that seniors and people with disabilities use too much care, egged on by their doctors. If true, a solution could have been to enforce the Stark Law, which bans physicians from having financial relationships with providers they refer to, or other anti-kickback statutes. States could also enforce laws 33 of them have enacted that prohibit the “corporate practice of medicine.”

Instead, health insurers were invited and incentivized by previous administrations to compete with the original Medicare program and “manage” beneficiaries’ care. Under this model— set in its modern form in 2003 — Medicare Advantage insurers are paid a rate based on a complex risk modeling process and estimated costs.

But Medicare Advantage plans have never been cheaper than traditional Medicare, as MedPAC has repeatedly pointed out.

This is a far more complex approach than the fee-for-service model in which CMS sets prices in health care in a public and transparent manner, Gilfillan notes. The prices negotiated by Medicare Advantage companies, by contrast, are not disclosed.

“With fee-for-service, a patient is provided a service, treatment or medication. The physician who provides the service charges a specific amount for that service,” Gilfillan said. “And then Medicare pays whatever it decided it was worth for that service. The benefit is you pay for what you get.”

Some Medicare Advantage plans use a “capitated” approach in paying primary care physicians. The amount is based on the premium they receive for the patient. The more codes submitted, the higher the capitation, the greater the profit. That approach is having far-reaching economic impacts on health care, said Hayden Rooke-Ley, an Oregon-based lawyer and health care consultant who co-authored a recent New England Journal of Medicine article on the corporatization of primary care. It is the capitation model, he says, that drives the rampant upcoding among Medicare Advantage plans.

From Horizontal to Vertical

“An undercovered aspect of Medicare Advantage is the way it is fueling vertical consolidation” in the insurance business, Rooke-Ley added, noting that until recent years, insurers bulked up by buying smaller competitors (known as horizontal integration). “With so much government money, we’re seeing insurance companies restructuring themselves as vertically integrated conglomerates [through the acquisition of physician practices, clinics and pharmacy operations] to become even more profitable, especially in Medicare Advantage.”

“A key part of this strategy is to own primary care practices,” he said, citing Humana’s partnership with the private-equity firm Welsh Carson to become the largest owner of Medicare-based primary care, CVS/Aetna’s acquisition of Oak Street, and UnitedHealth’s roll up of doctors practices across the country.

As Rooke-Ley explained, control of primary care allows insurance companies to more easily manipulate “risk scores” to increase payments from the government by claiming patients are in worse health than they really are.

“The easiest way to increase risk scores, short of simply fabricating diagnosis codes, is to control the behavior of physicians and other clinicians,” he said.

“When an insurance company owns the physician practice, it can configure workflows, technology, and incentives to drive risk coding.

UnitedHealth, for example, can preferentially schedule Medicare Advantage patients – and it can choose to reach out to health plan enrollees it identifies with its data as having high ‘coding opportunities.’ It can require its doctors to go to risk-code training, and it can prohibit doctors from closing their notes before they address all the ‘suggested’ diagnosis codes.”

“While Medicare Advantage insurance companies tout all their provider acquisitions as investments in value-based care, the concern is that it’s really just looking like a game of financialization,” Rooke-Ley said. “MA was supposed to save Medicare money, but the exact opposite has happened.

According to MedPAC, the government will over-subsidize MA to the tune of $88 billion this year, with $54 billion of that due to excess risk coding relative to what we see in traditional Medicare. That’s a staggering amount of money that could go directly to patients and clinicians by strengthening traditional Medicare.”

Two Possible Futures

There are two options for the future of Medicare, said Dr. Ed Weisbart, former chief medical officer of the pharmacy benefit manager Express Scripts, which Cigna bought in 2018, who now leads the Missouri chapter of Physicians for a National Health Program.

In one future, he said, “We will change the trajectory and get rid of the profiteers, and manage to divert the funds that are being profiteered to patient care.”

In another future, the business practices of Medicare Advantage plans “will be unfettered and more damaging and harmful than they are today,” he said. “If we continue on this course we’ll find an increasingly polarized health care system that caters increasingly to the wealthy and privileged. The barriers to care will be worse.”

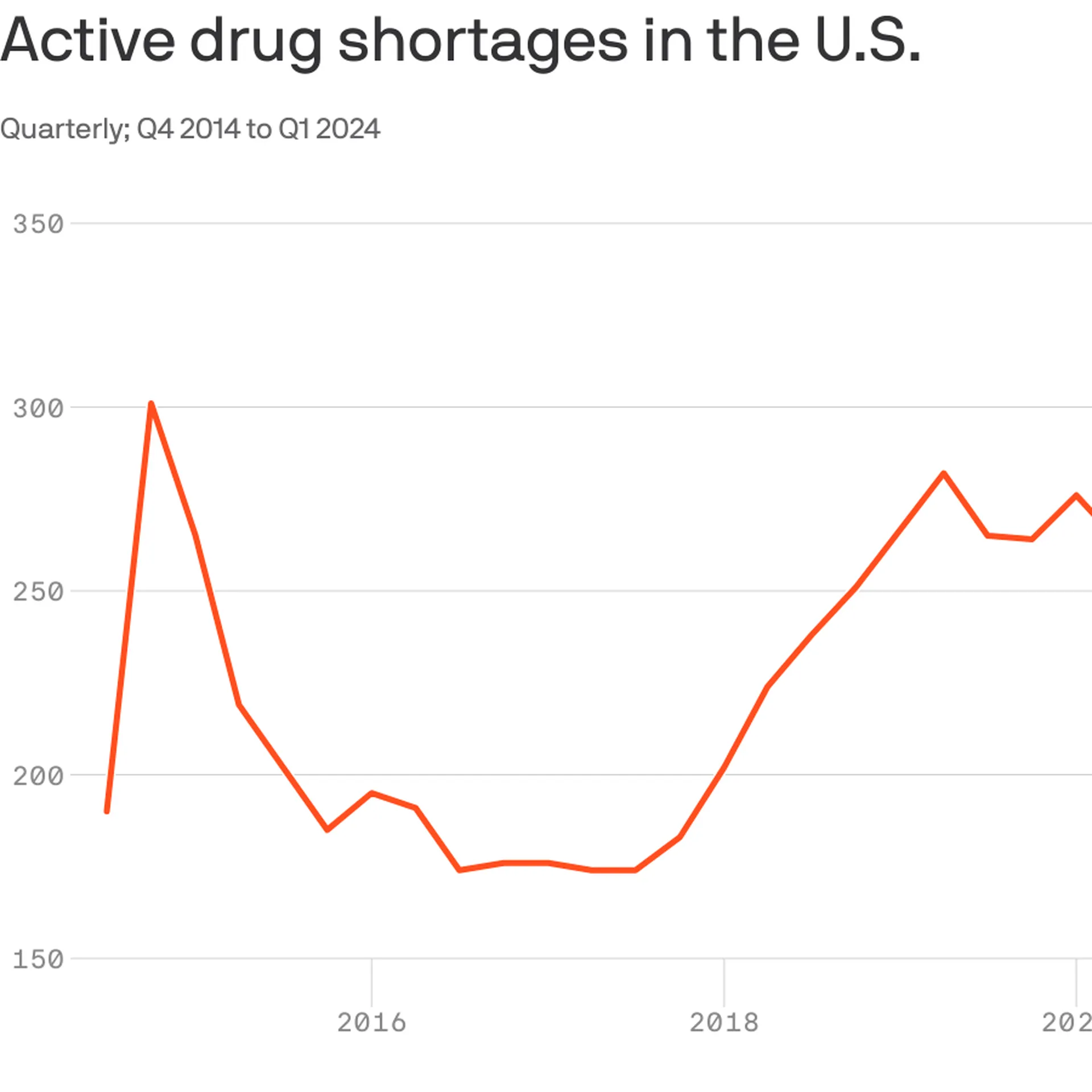

With 323 medicines in short supply, U.S. drug shortages have risen to their highest level since the American Society of Health-System Pharmacists began tracking in 2001.

Why it matters:

This high-water mark should energize efforts in Congress and federal agencies to address the broken market around what are often critical generic drugs, the organization says.

The Biden administration last week issued a drug-shortage plan that called on Congress to pass legislation that would reward hospitals for maintaining an adequate supply of key drugs, among other measures.

As a “first step,” Medicare yesterday proposed incentives for roughly 500 small hospitals to establish and maintain a six-month buffer stock of essential medicines.

The big picture:

Many of the issues behind shortages are tied to low prices for generics that leave manufacturers competing on price.

“It’s been a race to the bottom. We need more transparency around quality so that buyers have a reason to not chase the lowest price,” said Michael Ganio, senior director at the ASHP.

Drugmakers that can demonstrate safer, higher-quality manufacturing practices should earn a higher price, he said.

Manufacturing quality concerns in particular have fueled shortages of chemotherapy drugs and some antibiotics.

Between the lines: Other factors are also driving drug shortages.

Controlled substances, such as pain and sedation medications,account for12% of active shortages, which are tied to recent legal settlements and Drug Enforcement Administration changes to production limits, per ASHP.

Not surprisingly, the blockbuster category of anti-obesity drugs known as GLP-1s are in shortage largely because of outsized demand.

If Congress in the next year or two succeeds in transforming Medicare into something that looks like a run-of-the mill Medicare Advantage plan for everyone – not just for those who now have the plans – it will mark the culmination of a 30-year project funded by the Heritage Foundation.

A conservative think tank, the Heritage Foundation grew to prominence in the 1970s and ’80s with a well-funded mission to remake or eliminate progressive governmental programs Americans had come to rely on, like Medicare, Social Security and Workers’ Compensation.

Some 30 million people already have been lured into private Medicare Advantage plans, eager to grab such sales enticements as groceries, gym memberships and a sprinkling of dental coverage while apparently oblivious to the restrictions on care they may encounter when they get seriously ill and need expensive treatment. That’s the time when you really need good insurance to pay the bills.

Congress may soon pass legislation that authorizes a study commission pushed by Heritage and some Republican members aimed at placing recommendations on the legislative table that would end Medicare and Social Security, replacing those programs with new ones offering lesser benefits for fewer people.

In other words, they would no longer be available to everyone in a particular group. Instead they would morph into something like welfare, where only the neediest could receive benefits.

How did these popular programs, now affecting 67.4 million Americans on Social Security and nearly 67 million on Medicare, become imperiled?

As I wrote in my book, Slanting the Story: The Forces That Shape the News, Heritage had embarked on a campaign to turn Medicare into a totally privatized arrangement. It’s instructive to look at the 30-year campaign by right-wing think tanks, particularly the Heritage Foundation, to turn these programs into something more akin to health insurance sold by profit-making companies like Aetna and UnitedHealthcare than social insurance, where everyone who pays into the system is entitled to a benefit when they become eligible.

The proverbial handwriting was on the wall as early as 1997 when a group of American and Japanese health journalists gathered at an apartment in Manhattan to hear a program about services for the elderly. The featured speaker was Dr. Robyn Stone who had just left her position as assistant secretary for the Department of Health and Human Services in the Clinton administration.

Stone chastised the American reporters in the audience, telling them: “What is amazing to me is that you have not picked up on probably the most significant story in aging since the 1960s, and that is passage of the Balanced Budget Act of 1997, which creates Medicare Plus Choice” – a forerunner of today’s Advantage plans.

“This is the beginning of the end of entitlements for the Medicare program,” Stone said, explaining that the changes signaled a move toward a “defined contribution” program rather than a “defined benefit” plan with a predetermined set of benefits for everyone. “The legislation was so gently passed that nobody looked at the details.”

Robert Rosenblatt, who covered the aging beat for the Los Angeles Times, immediately challenged her. “It’s not the beginning of the end of Medicare as we know it,” he shot back. “It expands consumer choice.”

Consumer choice had become the watchword of the so-called “consumer movement,” ostensibly empowering shoppers – but without always identifying the conditions under which their choices must be made.

When consumers lured by TV pitchmen sign up for Medicare Advantage, how many of the sellers disclose that once those consumers leave traditional Medicare for an Advantage plan, they may be trapped. In most states, they will not be able to buy a Medicare supplement policy if they don’t like their new plan unless they are in super-good health.

In other words, most seniors are stuck. That can leave beneficiaries medically stranded when they have a serious, costly illness at a time in life when many are using up or have already exhausted their resources. I once asked a Medicare counselor what beneficiaries with little income would do if they became seriously ill and their Advantage plan refused to pay many of the bills, an increasingly common predicament. The cavalier answer I got was: “They could just go on Medicaid.”

The push to privatize Medicare began in February 1995 when Heritage issued a six-page committee brief titled “A Special Report to the House Ways and Means Committee”, which was sent to members of Congress, editorial writers, columnists, talk show hosts and other media. Heritage then spent months promoting its slant on the story. Along with other right-wing groups dedicated to transforming Medicare from social insurance to a private arrangement like car insurance, Heritage clobbered reporters who produced stories that didn’t fit the conservative narrative.

The right-wing Media Research Center singled out journalists who didn’t use the prescribed vocabulary to describe Heritage plans. Its newsletter criticized CBS reporter Linda Douglas when she reported that the senior citizens lobby had warned that the Republican budget would gut Medicare. The group reprimanded another CBS reporter, Connie Chung, for reporting that the House and Senate GOP plans “call for deep cuts in Medicare and other programs.” Haley Barbour, then Republican National Committee chairman, vowed to raise “unshirted hell” with the news media whenever they used the word “cut.” He wined and dined reporters, “educating” them on the “difference” between cuts and slowing Medicare’s growth. Former Republican U.S. Rep. John Kasich of Ohio, who chaired the House budget committee, called reporters warning them not to use the word “cut,” later admitting he “worked them over.”

As I wrote at the time, by fall of that year reporters had fallen in line. Douglas, who had been criticized all summer, got the words right and reported that the Republican bill contained a number of provisions “all adding up to a savings of $270 billion in the growth of Medicare spending.”

Fast forward to now. The Heritage Foundation’s Budget Blueprint for fiscal year 2023 offered ominous recommendations for Medicare, some of which might be enacted in a Republican administration. The think tank yet again called for a “premium support system” for Medicare, claiming that if its implementation was assumed in 2025, it “would reduce outlays by $1 trillion during the FY 2023-2032 period.” Heritage argues that the controversial approach would foster “intense competition among health plans and providers,” “expand beneficiaries’ choices,” “control costs,” “slow the growth of Medicare spending,” and “stimulate innovation.”

The potential beneficiaries would be given a sum of money, often called a premium support, to shop in the new marketplace, which could resemble today’s sales bazaar for Medicare Advantage plans, setting up the possibility for more hype and more sellers hoping to cash in on the revamped Medicare program. Many experts fear that such a program ultimately could destroy what is left of traditional Medicare, which about half of the Medicare population still prefers.

In other words, most seniors are stuck.

That can leave beneficiaries medically stranded when they have a serious, costly illness at a time in life when many are using up or have already exhausted their resources. I once asked a Medicare counselor what beneficiaries with little income would do if they became seriously ill and their Advantage plan refused to pay many of the bills, an increasingly common predicament. The cavalier answer I got was: “They could just go on Medicaid.”

The push to privatize Medicare began in February 1995 when Heritage issued a six-page committee brief titled “A Special Report to the House Ways and Means Committee”, which was sent to members of Congress, editorial writers, columnists, talk show hosts and other media. Heritage then spent months promoting its slant on the story. Along with other right-wing groups dedicated to transforming Medicare from social insurance to a private arrangement like car insurance, Heritage clobbered reporters who produced stories that didn’t fit the conservative narrative.

The right-wing Media Research Center singled out journalists who didn’t use the prescribed vocabulary to describe Heritage plans. Its newsletter criticized CBS reporter Linda Douglas when she reported that the senior citizens lobby had warned that the Republican budget would gut Medicare. The group reprimanded another CBS reporter, Connie Chung, for reporting that the House and Senate GOP plans “call for deep cuts in Medicare and other programs.” Haley Barbour, then Republican National Committee chairman, vowed to raise “unshirted hell” with the news media whenever they used the word “cut.” He wined and dined reporters, “educating” them on the “difference” between cuts and slowing Medicare’s growth. Former Republican U.S. Rep. John Kasich of Ohio, who chaired the House budget committee, called reporters warning them not to use the word “cut,” later admitting he “worked them over.”

As I wrote at the time, by fall of that year reporters had fallen in line. Douglas, who had been criticized all summer, got the words right and reported that the Republican bill contained a number of provisions “all adding up to a savings of $270 billion in the growth of Medicare spending.”

Fast forward to now. The Heritage Foundation’s Budget Blueprint for fiscal year 2023 offered ominous recommendations for Medicare, some of which might be enacted in a Republican administration. The think tank yet again called for a “premium support system” for Medicare, claiming that if its implementation was assumed in 2025, it “would reduce outlays by $1 trillion during the FY 2023-2032 period.” Heritage argues that the controversial approach would foster “intense competition among health plans and providers,” “expand beneficiaries’ choices,” “control costs,” “slow the growth of Medicare spending,” and “stimulate innovation.”

The potential beneficiaries would be given a sum of money, often called a premium support, to shop in the new marketplace, which could resemble today’s sales bazaar for Medicare Advantage plans, setting up the possibility for more hype and more sellers hoping to cash in on the revamped Medicare program. Many experts fear that such a program ultimately could destroy what is left of traditional Medicare, which about half of the Medicare population still prefers.

In a Republican administration with a GOP Congress, some of the recommendations, or parts of them, might well become law. The last 30 years have shown that the Heritage Foundation and other organizations driven by ideological or financial reasons want to transform Medicare, and they are committed for the long haul. They have the resources to promote their cause year after year, resulting in the continual erosion of traditional Medicare by Advantage Plans, many of which are of questionable value when serious illness strikes.

The seeds of Medicare’s destruction are in the air.

The program as it was set out in 1965 has kept millions of older Americans out of medical poverty for over 50 years, but it may well become something else – a privatized health care system for the oldest citizens whose medical care will depend on the profit goals of a handful of private insurers. It’s a future that STAT’s Bob Herman, whose reporting has explored the inevitable clash between health care and an insurer’s profit goals, has shown us.

In the long term, the gym memberships, the groceries, the bit of dental and vision care so alluring today may well disappear, and millions of seniors will be left once again to the vagaries of America’s private insurance marketplace.

A story in Rolling Stone last month offered an ominous prediction about our nation’s health care. “The right-wing policy agenda written for a new Donald Trump presidency would ‘greatly accelerate’ efforts to privatize Medicare,” Andrew Perez wrote.

That story should be seen by the millions of seniors who might not read Rolling Stone but who have traditional Medicare coverage with a supplemental policy that pays for virtually every medical bill when they get sick. Those are the people who have not yet been enticed into Medicare Advantage plans with promises of groceries and gym memberships but with little or no notice about the delays in care and the up-front, out-of-pocket costs common in many plans.

As I pointed out in an earlier story, there are roadblocks to care that have been reported by hospitals that were no longer accepting Medicare Advantage plans from some companies.

The CEO of the Brookings Hospital System in Brookings, South Dakota, was candid: MA plans “pay less, don’t follow medical policy, coverage, billing, and payment rules and procedures, and they are always trying to figure out how to deny payment for services,” he said.

Yet, in his piece titled “Republicans Are Planning to Totally Privatize Medicare – And Fast,” Perez warns that privatizing Medicare is a goal conservative and right-wing interests have promoted since the 1990s, when former House Speaker Newt Gingrich, no fan of Medicare, predicted that the program would “wither on the vine because we think people are voluntarily going to leave it.”

Indeed, tens of millions of seniors have enrolled in or been forced by their former employers into Medicare Advantage plans, and even the 30 million or so seniors who still prefer to be in traditional Medicare, with its no-strings-attached coverage, may one day be forced to join the ranks of the MA crowd.

It’s time to once again sound the alarm, as Perez has done, that the government program that has brought millions of beneficiaries health insurance and security for more than five decades could eventually disappear.

Perez points out that one item buried in the 887-page Heritage Foundation blueprint written to inform a potential new Trump administration has attracted little attention so far. It is a scheme to “make Medicare Advantage the default enrollment option” for people who are newly eligible for Medicare, he wrote.

David Lipschutz, associate director of the Center for Medicare Advocacy, says the Heritage plan would hasten privatization. “Upon becoming eligible for Medicare now everyone starts with traditional Medicare as the default but can opt out of that program and later choose an Advantage plan,” Lipschutz says. The Heritage proposal, however, would have people start with Medicare Advantage plans, apparently with the opportunity to opt-out. With this arrangement, you can see how easy it would be for Medicare, as we know it, to ‘wither on the vine’ since many people new to Medicare are not well versed in the difference between the two options and instead are swayed by the TV advertising beckoning them to Medicare Advantage plans.

Making those privately operated plans the default “would hasten the end of the traditional Medicare program as well as its foundational premise: that seniors can go to any doctor or provider they choose,” Perez writes, noting that such a change also “would be a boon for private health insurers that generate massive profits and growing portions of their revenues from Medicare Advantage plans.”

Lipschutz agreed the plan would “greatly accelerate” Medicare privatization, noting that the Heritage Foundation’s selling points are “internally inconsistent.” The proposal says a Republican-led federal government would “give beneficiaries direct control of how they spend Medicare dollars,”

but Lipschutz pointed out that with a Medicare Advantage plan, a private insurer tells beneficiaries what procedures they can or cannot have by deciding which ones they will approve for payment. “That is the opposite of putting beneficiaries in control of how they spend their dollars,” Lipschutz says.

In one story about UnitedHealthcare, the largest Medicare Advantage company, the reporters noted that the insurer’s stunning financial success was driven by “brazen behavior,” such as cutting off payments for seriously ill patients and “denying rehabilitation care for older and disabled Americans as profits soared.”

UnitedHealth is far from alone in using such tactics to boost profits. Herman and Ross told of the struggle of a sick, 80-year-old North Carolina woman whose plan with Humana, the second largest Medicare Advantage company, would pay only for cheaper care in a nursing home instead of in a long-term acute-care facility.

The insurance industry’s mighty public relations machine makes it hard for ordinary Americans to understand their options when they turn 65. When a TV pitchman or woman is urging viewers to call right away and sign up for free groceries, the deck is stacked against traditional Medicare and supplemental coverage.

Meet the insurance industry’s “Better Medicare Alliance”

How many would-be beneficiaries know about the Better Medicare Alliance, an advocacy group promoting Medicare Advantage plans that swings into action at the slightest hint that lawmakers and regulators might curb the lucrative Medicare Advantage program? The organization’s website offered a sample letter for beneficiaries to send to their Congressional representatives urging them to “protect Medicare Advantage.”

Sixty-one members of Congress also made their preferences clear in a letter to Chiquita Brooks-LaSure, who heads the Center for Medicare and Medicaid Services, writing, “We are committed to our more than 32 million constituents across the United States who choose Medicare Advantage.” The letter was signed by prominent Democrats including Chuck Schumer, Senate Majority leader from New York; Sen. Amy Klobuchar of Minnesota; and Bob Casey of Pennsylvania, who chairs the Senate aging committee. With such high-powered supporters of Medicare Advantage, it’s easy to see why it’s difficult to put the program on an even playing field with traditional Medicare and supplemental insurance coverage.

Not long ago I received an email from David Marans, an 81-year-old Floridian who wanted to tell me about his experiences with Medicare and the supplemental Medigap insurance he had purchased at age 65. It covers Parts A and B deductibles, excess charges that doctors can impose if their state allows them to collect more than what Medicare has agreed to pay, and emergency room care that he told me “ has saved considerable medical expenses, avoided delays, allayed worries, and allowed peace of mind regarding medical treatment.” He said he just shows his card at any hospital or doctor’s office, no questions asked, and the “Medigap provider then handles all the rest.”

The older you get, Marans said, the harder it is to recover from illness; the added stress of finding the means of paying the medical bills and the stresses of Medicare Advantage restrictions and denials can prolong illness. Marans said a Medigap plan alleviates that stress. “In a subtle way, in part, Medigap helps pay for itself.”

Marans’ advice? “Force yourself to get a Medigap plan on your 65th birthday when you enroll in Medicare, and don’t lose it…

Seniors have to understand car insurance is for what might happen. Health insurance is for what very probably will happen.”

Last week, Congress avoided a partial federal shutdown by passing a stop-gap spending bill and now faces March 8 and March 22 deadlines for authorizations including key healthcare programs.

This week, lawmakers’ political antenna will be directed at Super Tuesday GOP Presidential Primary results which prognosticators predict sets the stage for the Biden-Trump re-match in November. And President Biden will deliver his 3rd State of the Union Address Thursday in which he is certain to tout the economy’s post-pandemic strength and recovery.

The common denominator of these activities in Congress is their short-term focus: a longer-term view about the direction of the country, its priorities and its funding is not on its radar anytime soon.

The healthcare system, which is nation’s biggest employer and 17.3% of its GDP, suffers from neglect as a result of chronic near-sightedness by its elected officials. A retrospective about its funding should prompt Congress to prepare otherwise.

U.S. Healthcare Spending 2000-2022

Year-over-year changes in U.S. healthcare spending reflect shifting demand for services and their underlying costs, changes in the healthiness of the population and the regulatory framework in which the U.S. health system operates to receive payments. Fluctuations are apparent year-to-year, but a multiyear retrospective on health spending is necessary to a longer-term view of its future.

The period from 2000 to 2022 (the last year for which U.S. spending data is available) spans two economic downturns (2008–2010 and 2020–2021); four presidencies; shifts in the composition of Congress, the Supreme Court, state legislatures and governors’ offices; and the passage of two major healthcare laws (the Medicare Modernization Act of 2003 and the Affordable Care Act of 2010).

During this span of time, there were notable changes in healthcare spending:

In 2000, national health expenditures were $1.4 trillion (13.3% of gross domestic product); in 2022, they were $4.5 trillion (17.3% of the GDP)—a 4.1% increase overall, a 321% increase in nominal spending and a 30% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 333 million, per capita healthcare spending increased 178% from $4,845 to $13,493 due primarily to inflation-impacted higher unit costs for , facilities, technologies and specialty provider costs and increased utilization by consumers due to escalating chronic diseases.

There were notable changes where dollars were spent: Hospitals remained relatively unchanged (from $415 billion/30.4% of total spending to $1.355 trillion/31.4%), physician services shrank (from $288.2 billion/21.1% to $884.8/19.6%) and prescription drugs were unchanged (from $122.3 billion/8.95% to $405.9 billion/9.0%).

And significant changes in funding Out-of-pocket shrank from 14.2% ($193.6 billion in 2020) to (10.5% ($471 billion) in 2020, private insurance shrank from $441 billion/32.3% to $1.289 trillion/29%, Medicare spending grew from $224.8 billion/16.5% to $944.3billion/21%; Medicaid and the Children’s Health Insurance Program spending grew from $203.4 billion/14.9% to $7805.7billion/18%; and Department of Veterans Affairs healthcare spending grew from $19.1 billion/1.4% to $98 billion/2.2%.

Looking ahead (2022-2031), CMS forecasts average National Health Expenditures (NHE) will grow at 5.4% per year outpacing average GDP growth (4.6%) and resulting in an increase in the health spending share of Gross Domestic Product (GDP) from 17.3% in 2021 to 19.6% in 2031.

The agency’s actuaries assume

“The insured share of the population is projected to reach a historic high of 92.3% in 2022… Medicaid enrollment will decline from its 2022 peak of 90.4M to 81.1M by 2025 as states disenroll beneficiaries no longer eligible for coverage. By 2031, the insured share of the population is projected to be 90.5 percent. The Inflation Reduction Act (IRA) is projected to result in lower out-of-pocket spending on prescription drugs for 2024 and beyond as Medicare beneficiaries incur savings associated with several provisions from the legislation including the $2,000 annual out-of-pocket spending cap and lower gross prices resulting from negotiations with manufacturers.”

My take:

The reality is this: no one knows for sure what the U.S. health economy will be in 2025 much less 2035 and beyond. There are too many moving parts, too much invested capital seeking near-term profits, too many compensation packages tied to near-term profits, too many unknowns like the impact of artificial intelligence and court decisions about consolidation and too much political risk for state and federal politicians to change anything.

One trend stands out in the data from 2000-2022: The healthcare economy is increasingly dependent on indirect funding by taxpayers and less dependent on direct payments by users.

In the last 22 years, local, state and federal government programs like Medicare, Medicaid and others have become the major sources of funding to the system while direct payments by consumers and employers, vis-à-vis premium out-of-pocket costs, increased nominally but not at the same rate as government programs. And total spending has increased more than the overall economy (GDP), household wages and costs of living almost every year.

Thus, given the trends, five questions must be addressed in the context of the system’s long-term solvency and effectiveness looking to 2031 and beyond:

Should its total spending and public funding be capped?

Should the allocation of funds be better adapted to innovations in technology and clinical evidence?

Should the financing and delivery of health services be integrated to enhance the effectiveness and efficiency of the system?

Should its structure be a dual public-private system akin to public-private designations in education?

Should consumers play a more direct role in its oversight and funding?

Answers will not be forthcoming in Campaign 2024 despite the growing significance of healthcare in the minds of voters. But they require attention now despite political neglect.

PS: The month of February might be remembered as the month two stalwarts in the industry faced troubles:

United HealthGroup, the biggest health insurer, saw fallout from a cyberattack against its recently acquired (2/22) insurance transaction processor by ALPHV/Blackcat, creating havoc for the 6000 hospitals, 1 million physicians, and 39,000 pharmacies seeking payments and/or authorizations. Then, news circulated about the DOJ’s investigation about its anti-competitive behavior with respect to the 90,000 physicians it employs. Its stock price ended the week at 489.53, down from 507.14 February 1.

And HCA, the biggest hospital operator, faced continued fallout from lawsuits for its handling of Mission Health (Asheville) where last Tuesday, a North Carolina federal court refused to dismiss a lawsuit accusing it of scheming to restrict competition and artificially drive-up costs for health plans. closed at 311.59 last week, down from 314.66 February 1.

With the South Carolina Republican primary results in over the weekend, it seems a Biden-Trump re-match is inevitable. Given the legacies associated with Presidencies of the two and the healthcare platforms espoused by their political parties, the landscape for healthcare politics seems clear:

Healthcare Issue

Biden Policy

Trump Policy

Access to Abortion

‘It’s a basic right for women protected by the Federal Government’

‘It’s up to the states and should be safe and rare. A 16-week ban should be the national standard.’

Ageism

‘President Biden is alert and capable. It’s a non-issue.’

‘President Biden is senile and unlikely to finish a second term is elected. President Trump is active and prepared.’

Access to IVF Treatments

‘It’s a basic right and should be universally accessible in every state and protected’

‘It’s a complex issue that should be considered in every state.’

Affordability

‘The system is unaffordable because it’s dominated by profit-focused corporations. It needs increased regulation including price controls.’

‘The system is unaffordable to some because it’s overly regulated and lacks competition and price transparency.’

Access to Health Insurance Coverage

‘It’s necessary for access to needed services & should be universally accessible and affordable.’

‘It’s a personal choice. Government should play a limited role.’

Public health

‘Underfunded and increasingly important.’

‘Fragmented and suboptimal. States should take the lead.’

Drug prices

‘Drug companies take advantage of the system to keep prices high. Price controls are necessary to lower costs.’

‘Drug prices are too high. Allowing importation and increased price transparency are keys to reducing costs.’

Medicare

‘It’s foundational to seniors’ wellbeing & should be protected. But demand is growing requiring modernization (aka the value agenda) and additional revenues (taxes + appropriations).’

‘It’s foundational to senior health & in need of modernization thru privatization. Waste and fraud are problematic to its future.’

Medicaid

‘Medicaid Managed Care is its future with increased enrollment and standardization of eligibility & benefits across states.’

‘Medicaid is a state program allowing modernization & innovation. The federal role should be subordinate to the states.’

Competition

‘The federal government (FTC, DOJ) should enhance protections against vertical and horizontal consolidation that reduce choices and increase prices in every sector of healthcare.’

‘Current anti-trust and consumer protections are adequate to address consolidation in healthcare.’

Price Transparency

‘Necessary and essential to protect consumers. Needs expansion.’

‘Necessary to drive competition in markets. Needs more attention.’

The Affordable Care Act

‘A necessary foundation for health system modernization that appropriately balances public and private responsibilities. Fix and Repair’

‘An unnecessary government takeover of the health system that’s harmful and wasteful. Repeal and Replace.’

Role of federal government

‘The federal government should enable equitable access and affordability. The private sector is focused more on profit than the public good.’

‘Market forces will drive better value. States should play a bigger role’

My take:

Polls indicate Campaign 2024 will be decided based on economic conditions in the fall 2024 as voters zero in on their choice. Per KFF’s latest poll, 74% of adults say an unexpected healthcare bill is their number-one financial concern—above their fears about food, energy and housing. So, if you’re handicapping healthcare in Campaign 2024, bet on its emergence as an economic issue, especially in the swing states (Michigan, Florida, North Carolina, Georgia and Arizona) where there are sharp health policy differences and the healthcare systems in these states are dominated by consolidated hospitals and national insurers.

Three issues will be the primary focus of both campaigns: women’s health and access to abortion, affordability and competition. On women’s health, there are sharp differences; on affordability and competition, the distinctions between the campaigns will be less clear to voters. Both will opine support for policy changes without offering details on what, when and how.

The Affordable Care Act will surface in rhetoric contrasting a ‘government run system’ to a ‘market driven system.’ In reality, both campaigns will favor changes to the ACA rather than repeal.

Both campaigns will voice support for state leadership in resolving abortion, drug pricing and consolidation. State cost containment laws and actions taken by state attorneys general to limit hospital consolidation and private equity ownership will get support from both campaigns.

Neither campaign will propose transformative policy changes: they’re too risky. integrating health & social services, capping total spending, reforms of drug patient laws, restricting tax exemptions for ‘not for profit’ hospitals, federalizing Medicaid, and others will not be on the table. There’s safety in promoting populist themes (price transparency, competition) and steering away from anything more.

As the primary season wears on (in Michigan tomorrow and 23 others on/before March 5), how the health system is positioned in the court of public opinion will come into focus.

Abortion rights will garner votes; affordability, price transparency, Medicare solvency and system consolidation will emerge as wedge issues alongside.

PS: Re: federal budgeting for key healthcare agencies, two deadlines are eminent: March 1 for funding for the FDA and the VA and March 8 for HHS funding.

Jayne Kleinman is bombarded with Medicare Advantage promotions every open enrollment period — even though she has no interest in leaving traditional Medicare, which allows seniors to choose their doctors and get the care they want without interference from multi-billion-dollar insurance companies.

“My biggest problem with being barraged is that so many of the ads were inaccurate,” Kleinman, a retired social services professional in New Haven County, Connecticut, told HEALTH CARE un-covered.

“They neglect to say that the amount of coverage you get is limited. They don’t talk about what you are losing by leaving traditional Medicare. It feels like insurance companies are manipulating us to get Medicare Advantage plans sold so that they can control the system, as opposed to treating us like human beings.”

Seniors face a torrent of Medicare Advantage advertising: an analysis by KFF found 9,500 daily TV ads during open enrollment in 2022. A recent survey by the Commonwealth Fund found that 30% of seniors received seven or more phone calls weekly from Medicare Advantage marketers during the most recent open enrollment (Oct. 15 to Dec. 7) for 2024 coverage.

In 2023, a critical milestone was passed: over half of seniors are now enrolled in privatized Medicare Advantage plans. The marketing for these plans nearly always fails to mention how hard it is to return to traditional Medicare once you are in Medicare Advantage, and that the MA plans have closed provider networks and require prior authorization for medical procedures. Instead, the marketing emphasizes the fringe benefits offered by Medicare Advantage plans like gym memberships.

U.S. Sen. Ron Wyden (D-Ore.), chairman of the Senate Finance Committee, criticized the widespread and predatory marketing of Medicare Advantage in a report in November 2022 and has continued to pressure the Biden administration to do more to address the problem.

The report said that consumer complaints about Medicare Advantage marketing more than doubled from 2020 to 2021 to 41,000. It cites cases such as that of an Oregon man whose switch to Medicare Advantage meant he could no longer afford his prescription drugs, as well as a 94-year-old woman with dementia in a rural area who bought a Medicare Advantage plan that required her to obtain care miles further from her residence than she had to travel before.

When open enrollment began last fall, it was “the start of a marketing barrage as marketing middlemen look to collect seniors’ information in order to bombard them with direct mail, emails, and phone calls to get them to enroll,” Wyden stated in a letter to the Centers for Medicare and Medicaid Services (CMS), which was signed by the other Democrats on the Senate Finance Committee.

Just three weeks after Wyden sent the letter, CMS released a proposed rule reforming Medicare Advantage practices that the main lobby group for Medicare Advantage plans, the Better Medicare Alliance, endorsed.

But key recommendations by Wyden were missing, including a ban on list acquisition by Medicare Advantage third-party marketing organizations, which includes brokers, and banning brokers that call beneficiaries multiple times a day for days in a row.

Among the prominent third-party marketing organizations is TogetherHealth, a subsidiary of Benefytt Technologies, which runs ads featuring former football star Joe Namath.

In August 2022, the Federal Trade Commission forced Benefytt to repay $100 million for fraudulent activities. The month before, the Securities and Exchange Commission levied more than $12 million in fines against Benefytt.

But CMS continues to allow Benefytt to work as a broker. Benefytt is owned by Madison Dearborn Partners, a Chicago-based private equity firm with ties to former Chicago mayor and current Ambassador to Japan Rahm Emanuel. Benefytt collects leads on potential customers, which they then sell to brokers and insurers to aggressively target seniors. CMS did not provide comment as to why they had not blocked Benefytt’s continuing work as a third-party marketing organization for Medicare.

Two different rounds of rule-making on Medicare Advantage marketing in 2023 instead focused on such reforms as reining in exaggerated claims and excessive broker compensation.

The enormous profits generated by Medicare Advantage plans — costing the federal government as much as $140 billion annually in overpayments to private companies — explains what drives the aggressive and often unethical marketing practices, said David Lipschutz, an associate director at the Center for Medicare Advocacy.

“The fact is, there is an increasingly imbalanced playing field between Medicare Advantage and traditional Medicare,” he said. “Medicare Advantage is being favored in many ways. Medicare Advantage plans are paid more than what traditional Medicare spends on a given beneficiary.

Those factors combined with the fact that they generate such profits for insurance companies, leads to those companies doing everything they can to maximize enrollment.”

Adding to the problem, Lipschutz argued, was the enormous influence of the health insurance industry in Washington. Health insurers spent more than $33 million lobbying Washington in just the first three quarters of 2023 alone.

“There is no real organized lobby for traditional Medicare, or organized advertising efforts,” he said. “During open enrollment, 80% of Medicare-related ads have to do with Medicare Advantage. We regularly encounter very well-educated and savvy folks who are tripped up by advertising and lured in by the bells and whistles. The deck is stacked against the consumer.”

Private equity firms have made a large investment in the Medicare Advantage brokerage and marketing sector, in addition to Madison Dearborn’s acquisition of Benefytt. Bain Capital, which Sen. Mitt Romney (R-Utah) co-founded, invested $150 million in Enhance Health, a Medicare Advantage broker, in 2021.

The CEO of EasyHealth, another private equity-backed brokerage, toldModern Healthcare in 2021 that “Insurance distribution is our Trojan horse into healthcare services.”

As federal law requires truth in advertising, a group of advocacy organizations–led by the Center for Medicare Advocacy, Disability Rights Connecticut, and the National Health Law Project–cited what they considered blatantly deceptive marketing by UnitedHealthcare to people who are eligible for both Medicare and Medicaid, in a complaint to CMS.

UnitedHealthcare had purchased ads in the Hartford Courant asking seniors in large bold-faced type: “Eligible for Medicare and Medicaid? You could get more with UnitedHealthcare.”

People who are eligible for both Medicare and Medicaid due to their income level are better off in traditional Medicare than Medicare Advantage given that Medicaid covers their out-of-pocket costs, meaning that they have wide latitude to choose their doctors, hospitals and medical procedures.

Sheldon Toubman, an attorney with Disability Rights Connecticut who worked to draft the complaint, framed the ad in the broader context of poor marketing practices by the Medicare Advantage industry.

“I have been aware for a long time of basically fraudulent advertising in the MA insurance industry,” Toubman told HEALTH CARE un-covered. “There’s an overriding misrepresentation — they tell you how great Medicare Advantage is, and never the downsides.

“There are two big downsides of going out of traditional Medicare:

They don’t tell you that you give up the broad Medicare provider network, which has nearly every doctor. And should you need expensive medical care in Medicare Advantage, you will learn there are prior authorization requirements. Traditional Medicare does almost no prior authorization, so you don’t have that obstacle. They don’t ever tell you any of that,” he said.

But it is marketing to dual-eligible individuals that is arguably the most problematic, Toubman argued. “They have Medicare and they are also low income. Because they are low-income, they also have Medicaid.

“Medicaid is a broader program — it covers a lot of things that Medicare doesn’t cover.

In Connecticut, 92,000 dual-eligible seniors have been ‘persuaded’ to sign up for Medicare Advantage. What’s outrageous about the marketing is they get you to sign up by offering extra services. … If you look at the ad in the Hartford Courant, it says you could get more, with the only real benefit being $130 per month toward food. But you now have this problem of a more limited provider network and prior authorization. UnitedHealth is doing false advertising.”

It’s a nationwide problem, Toubman said. “All insurers are doing this everywhere. We’re asking CMS and the Federal Trade Commission to conduct a nationwide investigation of this kind of problem. The failure to tell people that they give up their broader Medicare network — they don’t tell anybody that.”

For Jayne Kleinman, the unending ads are about one thing only: insurance industry profits. “Medicare Advantage has been strictly based on the people who make millions of dollars at the top of the company making more,” she said. “It’s all about money, not about you as an individual. Every time I saw an ad I’d get angry every single time — because I felt they were misleading people. The Medicare Advantage insurers are trying to scam people out of an interest of making money.”

For many providers, 2023 provided a return to profitability (albeit at modest levels) following the devastating operating and investment losses experienced in 2022.Kaufman Hall’s National Hospital Flash Report data illustrated generally improving operating margins throughout the year, leveling off at 2.0% in November on a year-to-date basis.

This level of performance is commendable given 2022 and early 2023 margins, although it is still well below the 3% to 4% range which we believe is needed for long-term sustainability in the not-for-profit healthcare world. We may well have reached a point of stability with respect to operating performance, but at a lower level.

The question for hospital and health system leaders is whether this level of operating stability provides sustainability?

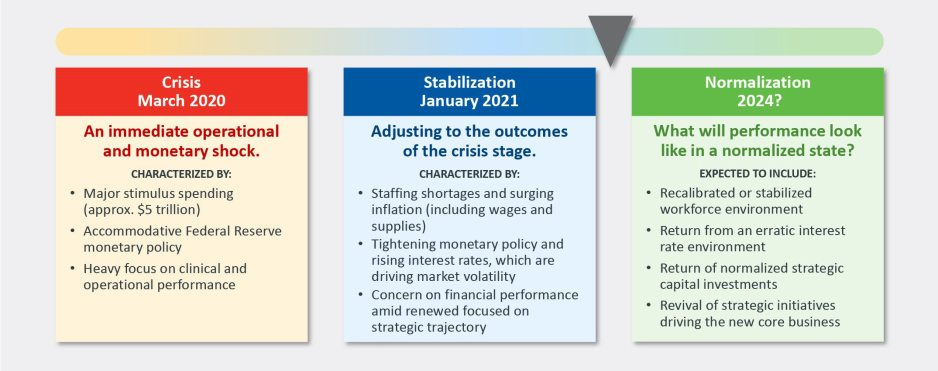

From stabilization to normalization

Since the pandemic began in 2020, the progress of recovery has been viewed over three phases: crisis, stabilization, and normalization. In last year’s outlook, we noted that we were in the midst of a potentially multi-year stabilization phase, which would continue to be marked with volatility—including ongoing labor market dislocations, inflationary pressures, and restrictive monetary policies. As we enter 2024, there are signs that we are now at the bridge between stabilization and normalization (Figure 1).

Figure 1: The Three Phases of Recovery from the Covid Pandemic

“The question for hospital and health system leaders is whether that level of stability provides sustainability?”

These signs include evidence that the first two indicators for normalization—a recalibrated or stabilized workforce environment and a return from an erratic interest rate environment—are coming into place. In our 2023 State of Healthcare Performance Improvement survey, respondents indicated that the spike in contract labor utilization that has been a dominant factor in operating expense increases was subsiding. Sixty percent of respondents said that utilization of contract labor was decreasing, and 36% said it was holding steady. Only 4% noted an increase in contract labor usage. Overall employee cost inflation seems to be subsiding as well: for all three labor categories in our survey (clinical, administrative, and support services), more organizations were able to hold salary increases to the 0% – 5% range in 2023 than in 2022.

There is good news on the interest rate front as well. After a series of rate increases in 2023, the Federal Reserve has held steady the last six months and has signaled rate cuts in 2024. Inflation has cooled markedly (albeit not yet at target levels), and employment rates have held steady. The Fed may have achieved a “soft landing” that satisfies its dual mandate of stable prices and maximum sustainable employment. Borrowing costs for not-for-profit hospital issuers have declined nearly 100 basis points in the last two months and we are expecting a return to more normal issuance levels in the first half of 2024.

There are other indications of normalization, including in the rating agencies’ outlooks for 2024. Regardless of the headline, all saw significant improvement in healthcare performance 2023.

The final answer to the question of whether the healthcare industry is entering the normalization phase likely will hinge on the last two indicators. Will we see a return of normalized strategic capital investments, and will we see a revival of strategic initiatives driving the core business (perhaps newly imagined)?

In effect, are health care systems simply surviving or are they thriving?

Looking forward, several factors could either bolster or undermine healthcare leaders’ confidence and willingness to resume a more normal level of investment in both capital needs and strategic growth. These include:

Politics and the 2024 elections. When North Carolina—a state that has traditionally leaned “red”—decided to opt into the Affordable Care Act’s (ACA’s) Medicaid expansion in 2023, it seemed that political debates over the ACA might be in the rearview mirror. But last November, former president Trump—currently the leading candidate for the Republican presidential nomination after strong wins in the Iowa caucuses and New Hampshire primary—indicated his intent to replace the ACA with something else. President Biden is now making protection and expansion of the ACA a key part of his 2024 campaign. What had appeared to be a settled issue may be a significant point of contention in the 2024 presidential election and beyond.

Although we do not anticipate any significant healthcare-related legislation in advance of the 2024 elections, healthcare leaders should be prepared for renewed attention to the costs of government-funded healthcare programs leading up to and following the elections. The national debt has increased rapidly over the past 20 years, tripling from $11 trillion in 2003 to $33 trillion in 2023. If the deficit and national debt become an important issue in the election, a move toward a balanced budget—akin to the Balanced Budget Act of 1997—post election could lead to further cuts to Medicare and Medicaid.

Temporary relief payments. Health systems continue to receive one-time cash infusions through the 340B settlement, Federal Emergency Management Agency (FEMA) payments and other governmental programs. Approximately 1,600 hospitals have or will be receiving a lump-sum payment to compensate them for a change in the Department of Health & Human Services’ (HHS’s) reimbursement rates for the 340B program from 2018 to 2022, which was ruled unlawful by the Supreme Court in a 2022 decision. The total amount to be distributed is approximately $9 billion and began hitting bank accounts in January 2024.

But what the right hand giveth, the left hand taketh away. Budget neutrality requirements will force HHS to recoup this offset—amounting to approximately $7.8 billion—which it will do by reducing payments for non-drug items and services to all Outpatient Prospective Payment System (OPPS) providers by 0.5% until the offset has been fully recouped, beginning in calendar year 2026. HHS estimates that this process will take approximately 16 years. Is this a harbinger of lower payments on other key governmental programs?

Many hospitals also continue to receive Covid-related payments from FEMA for expenses occurred during the pandemic. In addition, state supplemental payments—especially under Medicaid managed care and fee-for-service programs—are providing some relief. The Centers for Medicare & Medicaid Services has issued a proposed rule, however, that would limit states’ use of provider-based funding sources, such as provider taxes, and cap the rate of growth for state-directed payments.

As all of these payment programs dry up over the next few years, hospitals will need to replace the revenue and/or get leaner on the expense side in order to maintain today’s level of performance.

The hollowing of the commercial health insurance market. Our colleague, Joyjit Saha Choudhury, recently published a blog on the hollowing of the commercial health insurance market, driven by long-term concerns over the affordability of healthcare. While volumes have been recovering to pre-pandemic levels, this hollowing threatens the loss of the most profitable volumes and will pressure hospitals and health systems to create and deliver value, compete for inclusion in narrow networks, and develop more direct relationships with the employer community.

Related, the growing penetration of Medicare Advantage plans is reducing the number of traditional Medicare beneficiaries. Many CFOs report that these programs can be the most difficult with which to work given their high denial rates and required pre-authorization rates. A new rule requiring insurers to streamline prior authorizations for Medicare Advantage, Medicaid, and Affordable Care Act plans may help alleviate this issue; however, it will be incumbent upon management teams to stay ahead of them. Aging demographics are also reducing the percentage of commercially insured patients for many hospitals and health systems, further exacerbating the problem. This combination of fewer commercial patients (who often subsidize governmental patients) and more pressure on receiving the duly owed commercial revenue threatens to be an ongoing headache for management teams.

Ongoing impact of the Baby Boom generation. Despite the good news on inflation—and indications that the Fed may begin lowering interest rates in 2024—the economy is by no means out of the woods yet. The Baby Boom generation, which holds more than 50% of the wealth in the U.S. and is seemingly price agnostic, still has many years of spending ahead, in healthcare and general purchasing. This will likely continue to pressure inflation, especially in the healthcare sector, where demand will continue to grow. As the generation starts to shrink, the resulting wealth transfer will be the largest ever in our country’s history and have profound (and unforeseen) consequences on the overall economy and healthcare in general.

In sum, these other factors will continue to affect the sector (both positively and negatively) and require health system management teams to navigate an everchanging world. While many signs point toward short-term relief, the longer-term challenges persist. Improvements in the short term may, however, provide the opportunity to reposition organizations for the future.

How hospitals and health systems should respond

Healthcare leaders should view ongoing uncertainty in the political and economic climate as a tailwind as much as a headwind. This uncertainty, in other words, should be a motivation to put in place strategies that will buffer healthcare organizations from potential bumps in the road ahead. Setting balance sheet strategy should be a part of an organization’s planning process.

How an organization sets that strategy, measures its performance, and makes improvements will set apart top-performing organizations.

Although heightened debt issuance early in 2024 signals a return for many systems to a climate of investment, there is still limited energy around strategy and debt conversations in many boardrooms, especially in those organizations where financial improvement continues to lag. The last two years have illustrated that hospitals and health systems will not be able to cut their way to profitability. Lackluster performance cannot and will not improve without some level of strategic change, whether it is through market share gains, payer mix shift, or operational improvements. This strategic change requires investment and investment requires capital. Capital can be obtained in many forms—whether through growth in capital reserves, improved cash flow, or new debt issuance—but is essential for change. Reengaging in conversations about strategy and growth should be an imperative in 2024 and will require reexamining how that growth is funded.

Healthcare leaders should engage their partners as they continue or refocus on:

Changing the conversation from debt capacity to capital capacity. Management teams need to determine what they can afford to spend on capital if the new normal of cash flow will be constrained going forward. Capital capacity is and should be agnostic to the source of that capital, such as debt, cash flow from operations, or liquidity reserves. Healthcare leaders must focus on what they can spend, before deciding how to fund that spending. The conversation will need to balance investment for the future with maintaining key credit metrics in the short term.

Conducting a capitalization analysis. Separate but related to the previous entry, how much leverage should your organization have relative to its overall capitalization? Ostensibly, many organizations have been paying principal while curtailing borrowing needs, so capitalization may have improved. While that may be the case, many organizations have depleted reserves and/or experienced investment losses that have reduced capitalization. Understanding where the organization stands is an essential next step.

Evaluating surplus return. Consider surplus return as investment income net of interest expense. Organizations should evaluate their ability to reliably generate both operating cash flow and net surplus. How an organization’s balance sheet is positioned to generate returns and manage risk will be a critical success factor.

Focusing on the metrics that matter. These include operating cashflow margin, cash to debt, debt to revenue, and days cash on hand. As key metrics for rating analysts and investors continue to evolve, management teams need to make sure they are focused on the correct numbers. The discussion should be dually focused on ensuring adequate-to-ample headroom to basic financial covenants as well as a comparison to key medians and peers. Strong financial planning will address how these metrics can be improved over time through synergies, growth, and diversification strategies.

Although it has been a difficult few years, hospitals and health systems seem to have moved onto a more stable footing over the last twelve months. In order to build upon the upward trajectory, now is the time to harness strategy, planning, and investment to move organizations from stability to sustainability.