Hospitals’ business models are being upended by fundamental changes within the health care system, including one that presents a pretty existential challenge: People have far more options to get their care elsewhere these days.

Why it matters:

Health systems’ responses to major demographic, social and technological change have been controversial among policymakers and economists concerned about the impact on costs and competition.

- Communities depend on having at least some emergency services available, making the survival of hospitals’ core services crucial.

- But without adaptation — which is already underway in some cases — hospitals may be facing deep red balance sheets in the not-too-distant future, leading to facility closures and shuttered services.

The big picture:

Many hospitals have recovered from the sector’s post-pandemic financial slump, which was driven primarily by staffing costs and inflation. But systemic, long-term trends will continue to challenge their traditional business model.

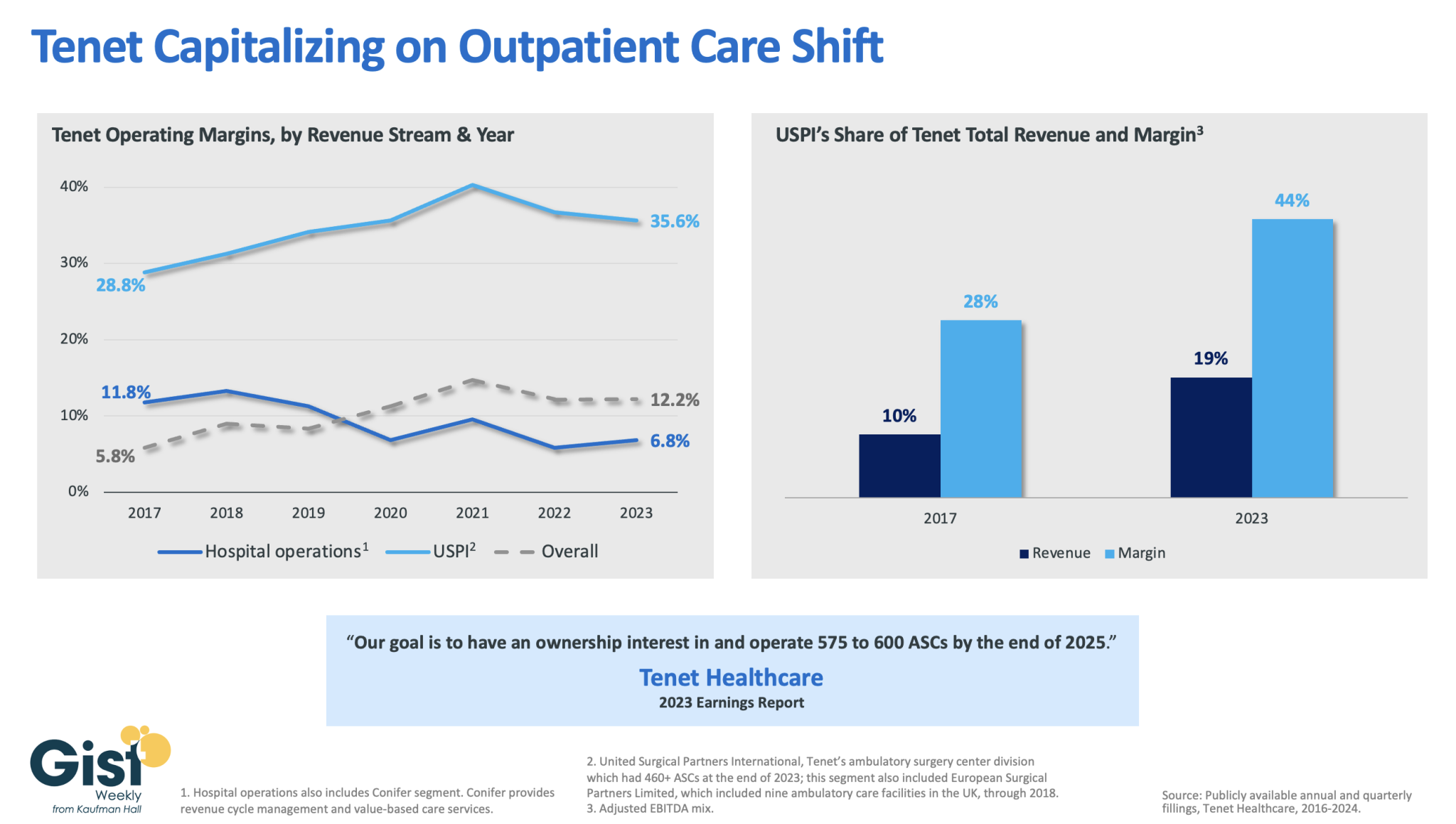

- Many of the services that are shifting toward outpatient settings — like oncology, diagnostics and orthopedic care — are the ones that typically make hospitals the most money and effectively subsidize less profitable departments.

- When hospitals lose these higher-margin services, “you’re starving the system that needs profits to provide services that we all might need, but particularly uninsured or underinsured people might need,” said UCLA professor Jill Horwitz.

And hospitals have long claimed that much higher commercial insurance rates make up for what they say are inadequate government rates.

- But as the population ages and moves out of employer-sponsored health plans, fewer people will have commercial insurance, forcing hospitals to either cut costs or find new sources of revenue.

By the numbers:

Consulting firms are projecting a bleak decade for health systems.

- Oliver Wyman recently predicted that under the status quo, hospitals will need to reduce their expenses by 15-20% by 2030 “to stay viable.”

- Boston Consulting Group last year projected that health systems’ annual financial shortfall will total more than $200 billion by 2027, and their operating margins will have dropped by 10 percentage points.

- To break even in 2027, a “typical” health system would need payment rate increases of between 5-8% annually — twice the rate growth over the last decade, according to BCG. If the load is borne solely by private insurers, hospitals will need a 10-16% year-over-year increase.

Between the lines:

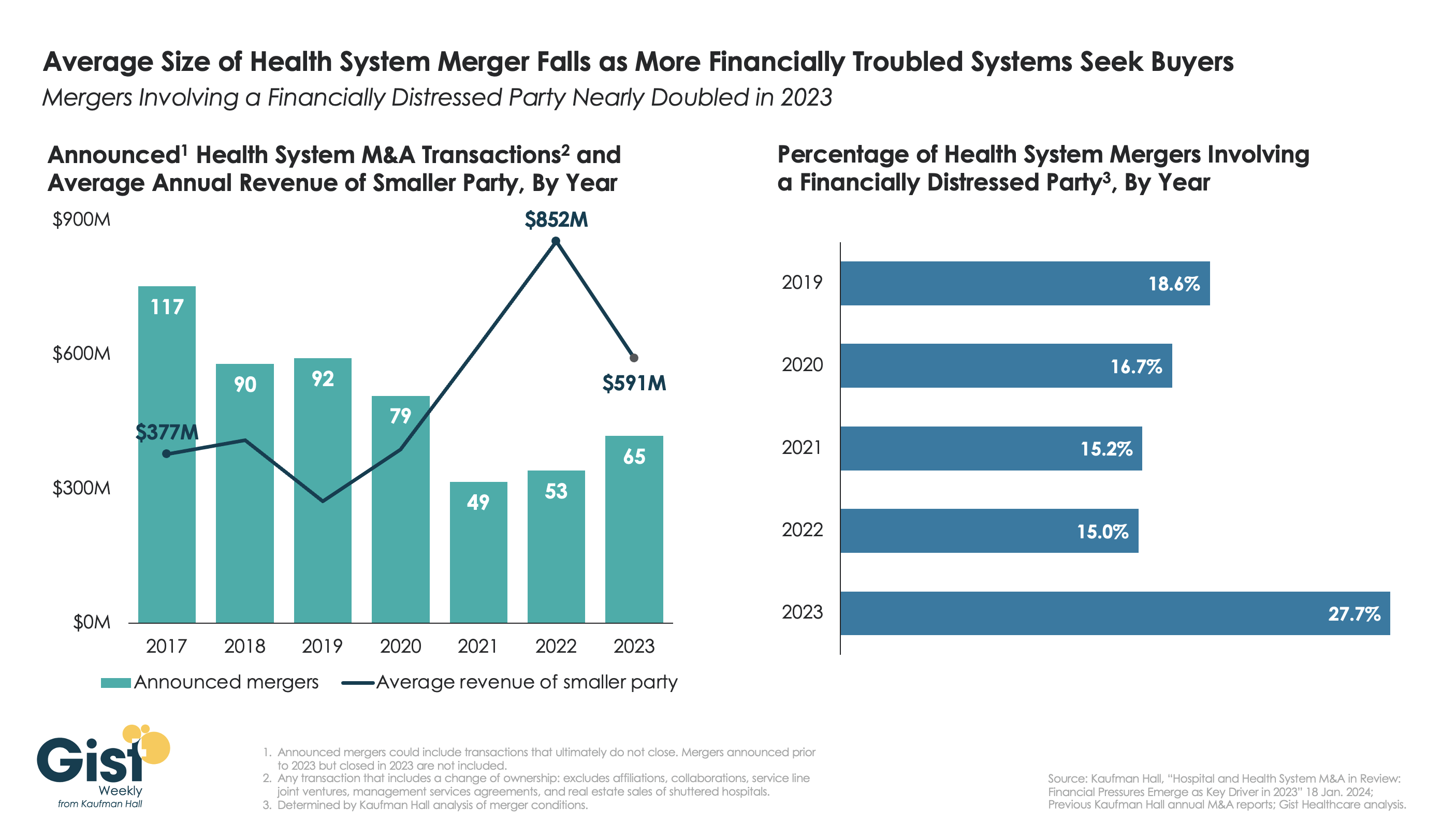

This is the lens through which to view health systems’ spree of mergers and acquisitions, which have increasingly drawn criticism from policymakers, regulators and economists as being anticompetitive.

- For better or worse, when hospitals have a larger market share, they are in a better position to negotiate and bring in more patients, and they can dilute some of the financial pain of poorer-performing facilities.

- And when they acquire physician practices or other outpatient clinics, they’re still getting paid for delivering care even when patients aren’t receiving it in a traditional hospital setting.

- “I think the hospitals have sort of said … ‘We can keep doing things the same way and we can just merge and get higher markups,'” said Yale economist Zack Cooper. “That push to consolidate is saying, ‘Let’s not move forward, let’s dig in.'”

Yes, but:

A big bonus of outpatient care is that it’s supposed to be cheaper. But when hospitals charge more for care than an independent physician’s office would have, or they tack on facility fees, costs don’t go down.

- And there’s a growing body of research showing that when hospitals consolidate, costs go up.

- “They’ve protected their portfolio, and that’s added to the cost of health care,” said Johns Hopkins professor Gerard Anderson.

The other side:

Hospitals are typically on the losing end of negotiations with insurers right now, thanks to how large insurers have become, and are “in an extremely difficult competitive position,” said Ken Kaufman, co-founder of consulting agency Kaufman Hall.

- Criticizing their mergers and acquisitions as anticompetitive is a “complete misunderstanding of the situation,” he said, and moving toward a new care model will take “an incredible amount of resources.”

Reality check:

Hospitals account for 30% of the country’s massive health spending tab, and they’ll have to be at the forefront of any real efforts to contain costs.

- They’re also anchors in their communities and are powerful lobbyists, which helps explain why Congress has struggled to modestly reduce what Medicare pays hospital outpatient departments.