It feels as though November 5, 2024 is far away, but for both Democrats and Republicans, the election is now. On the issue of healthcare, the two parties’ approaches differ sharply.

Think back to the behemoth effort by Republicans to “repeal and replace” the Affordable Care Act six years ago, an effort that left them floundering for a replacement, basically empty-handed. Recall the 2022 midterms, when their candidates in 10 of the tightest House and Senate races uttered hardly a peep about healthcare.

That reticence stood in sharp contrast to Democrats who weren’t shy about reiterating their support for abortion rights, simultaneously trying hard to ensure that Americans understood and applauded healthcare tenets in the Inflation Reduction Act.

As The Hill noted in early August, sounds like the same thing is happening this time around as America barrels toward November 2024. The publication said it reached to 10 of the leading Republican candidates about their plans to reduce healthcare costs and make healthcare more affordable, and only one responded: Rep. Will Hurd (R-Texas).

Healthcare ‘A Very Big Problem’

Maybe the party thinks its supporters don’t care. But, a Pew Research poll from June showed 64% of us think healthcare affordability is a “very big problem,” superseded only by inflation. In that research, 73% of Democrats and 54% of Republicans thought so.

Chuck Coughlin, president and CEO of HighGround, an Arizona-based public affairs firm, told The Hill that the results aren’t surprising.

“If you’re a Republican, what are you going to talk about on healthcare?” he said.

Observers note that the party has homed in on COVID-lockdowns, transgender medical rights, and yes, abortion.

Plans won’t offer coverage for preexisting conditions, maternity care, or prescription drugs, and they can set limits on coverage. The plans will make it easier for small employers to self-insure, so they don’t have to adhere to ACA or state insurance rules.

CHOICE would let large groups come together to buy Association Health Plans, said NPR, which noted that in the past, there have been “issues” with these types of plans.

Insurance experts say that the act takes a swing at the very foundation of the ACA. As one analyst described it, the act intends to improve America’s healthcare “through increased reliance on the free market and decreased reliance on the federal government.”

Democrats Tout Reduce-Price Prescriptions

Meanwhile, on Aug. 29, President Joe Biden spoke proudly in The White House: “Folks, there’s a lot of really great Republicans out there. And I mean that sincerely…But we’ll stand up to the MAGA Republicans who have been trying for years to get rid of the Affordable Care Act and deny tens of millions of Americans access to quality, affordable healthcare.” Current ACA enrollment is higher than 16 million.

He said that Big Pharma charges Americans more than three times what other countries charge for medications. And on that date, he announced that “the (Inflation Reduction Act) law finally gave Medicare the power to negotiate lower prescription drug prices.” He wasn’t shy about saying that this happened without help from “the other team.”

The New York Times said it feels this push for lower healthcare costs will be the centerpiece of his re-election campaign. The announcement confirmed that his administration will negotiate to lower prices on 10 popular—and expensive drugs—that treat common chronic illnesses.

It said previous research shows that as many as 80% of Americans want the government to have the power to negotiate.

The president also said that “Next year, Medicare will select more drugs for negotiation.” He added that his administration “is cracking down on junk health insurance plans that look like they’re inexpensive but too often stick consumers with big hidden fees.” And it’s tackling the extensive problem of surprise medical bills.

Earlier, on August 11, Biden and fellow Democrats celebrated the first anniversary of the PACT Act, legislation that provides healthcare to veterans exposed to toxic burn pits while serving. He said more than 300,000 veterans and families have received these services, with more than 4 million screened for toxic exposure conditions.

Push for High-Deductible Plans

Republicans want to reduce risk of high-deductible plans and make them more desirable—that responsibility is on insurers. According to Politico, these plans count more than 60 million people as members, and feature low premiums and tax advantages. The party said plans will also help lower inflation when people think twice about seeking unneeded care.

The plans’ low monthly premiums offer comprehensive preventive care coverage: physicals, vaccinations, mammograms, and colonoscopies, and have no co-payments, Politico said. The “but” in all this is that members will pay their insurers’ negotiated rate when they’re sick, and for medicines and surgeries. Minimum deductible is $1,500 or $3,000 for families—and can be even higher.

Members can fund health savings accounts but can’t fund flexible spending accounts. Proponents cite more access to care, and reduced costs due to promotion of preventive care. Nay-sayers worry about lower-income members facing costly bills due to insufficient coverage.

Republican Candidates Diverge on Medicaid

The American Hospital Association (AHA) doesn’t love these high deductible plans. It explained that members “find they can’t manage the gap between what their insurance pays and what they themselves owe as a result,” and that, AHA said, contributes to medical debt—something the association wants to change.

An Aug. 3 Opinion in JAMA Health Forum pointed out other ways the two parties diverge on healthcare. For example, the piece cited Biden’s incentives for Medicaid expansion. In contrast, Florida Governor Ron DeSantis, a Republican presidential candidate, has not worked to offer Medicaid to all lower-income residents under the ACA. Former Governor Nikki Haley of South Carolina feels the same, doing nothing. However, former New Jersey Governor Chris Christie has expanded it, as did former Vice President Mike Pence, when he governed Indiana.

Undoubtedly, as in presidential elections past, healthcare will be at least a talking point, with Democrats likely continuing to make it a central focus, as before.

Five years ago, I started the Fixing Healthcare podcast with the aim of spotlighting the boldest possible solutions—ones that could completely transform our nation’s broken medical system.

But since then, rather than improving, U.S. healthcare has fallen further behind its global peers, notching far more failures than wins.

In that time, the rate of chronic disease has climbed while life expectancy has fallen, dramatically. Nearly half of American adults now struggle to afford healthcare. In addition, a growing mental-health crisis grips our country. Maternal mortality is on the rise. And healthcare disparities are expanding along racial and socioeconomic lines.

Reflecting on why few if any of these recommendations have been implemented, I don’t believe the problem has been a lack of desire to change or the quality of ideas. Rather, the biggest obstacle has been the immense size and scope of the changes proposed.

To overcome the inertia, our nation will need to narrow its ambitions and begin with a few incremental steps that address key failures. Here are three actionable and inexpensive steps that elected officials and healthcare leaders can quickly take to improve our nation’s health:

1. Shore Up Primary Care

Compared to the United States, the world’s most-effective and highest-performing healthcare systems deliver better quality of care at significantly lower costs.

One important difference between us and them: primary care.

In most high-income nations, primary care makes up roughly half of the physician workforce. In the United States, it accounts for less than 30% (with a projected shortage of 48,000 primary care physicians over the next decade).

Primary care—better than any other specialty—simultaneously increases life expectancy while lowering overall medical expenses by (a) screening for and preventing diseases and (b) helping patients with chronic illness avoid the deadliest and most-expensive complications (heart attack, stroke, cancer).

But considering that it takes at least three years after medical school to train a primary care physician, to make a dent in the shortage over the next five years the U.S. government must act immediately:

The first action is to expand resident education for primary care. Congress, which authorizes the funding, would allocate $200 million annually to create 1,000 additional primary-care residency positions each year. The cost would be less than 0.2% of federal spending on healthcare.

The second action requires no additional spending. Instead, the Centers for Medicare & Medicaid Services, which covers the cost of care for roughly half of all American adults, would shift dollars to narrow the $108,000 pay gap between primary care doctors and specialists. This will help attract the best medical students to the specialty.

Together, these actions will bolster primary care and improve the health of millions.

2. Use Technology To Expand Access, Lower Costs

A decade after the passage of the Affordable Care Act, 30 million Americans are without health insurance while tens of millions more are underinsured, limiting access to necessary medical care.

Furthermore, healthcare is expected to become even less affordable for most Americans. Without urgent action, national medical expenditures are projected to rise from $4.3 trillion to $7.2 trillion over the next eight years, and the Medicare trust fund will become insolvent.

With costs soaring, payers (businesses and government) will resist any proposal that expands coverage and, most likely, will look to restrict health benefits as premiums rise.

Almost every industry that has had to overcome similar financial headwinds did so with technology. Healthcare can take a page from this playbook by expanding the use of telemedicine and generative AI.

At the peak of the Covid-19 pandemic, telehealth visits accounted for 69% of all physician appointments as the government waived restrictions on usage. And, contrary to widespread fears at the time, patients and doctors rated the quality, convenience and safety of these virtual visits as excellent. However, with the end of Covid-19, many states are now restricting telemedicine, particularly when clinicians practice in a different state than the patient.

To expand telemedicine use—both for physical and mental health issues—state legislators and regulators will need to loosen restrictions on virtual care. This will increase access for patients and diminish the cost of medical care.

It doesn’t make sense that doctors can provide treatment to people who drive across state lines, but they can’t offer the same care virtually when the individual is at home.

Similarly, physicians who faced a shortage of hospital beds during the pandemic began to treat patients in their homes. As with telemedicine, the excellent quality and convenience of care drew praise from clinicians and patients alike.

Building on that success, doctors could combine wearable devices and generative AI tools like ChatGPT to monitor patients 24/7. Doing so would allow physicians to relocate care—safely and more affordably—from hospitals to people’s homes.

Translating this technology-driven opportunity into standard medical practice will require federal agencies like the FDA, NIH and CDC to encourage pilot projects and facilitate innovative, inexpensive applications of generative AI, rather than restricting their use.

3. Reduce Disparities In Medical Care

American healthcare is a system of haves and have-nots, where your income and race heavily determine the quality of care you receive.

Black patients, in particular, experience poorer outcomes from chronic disease and greater difficulty accessing state-of-the-art treatments. In childbirth, black mothers in the U.S. die at twice the rate of white women, even when data are corrected for insurance and financial status.

Generative AI applications like ChatGPT can help, provided that hospitals and clinicians embrace it for the purpose of providing more inclusive, equitable care.

Previous AI tools were narrow and designed by researchers to mirror how doctors practiced. As a result, when clinicians provided inferior care to Black patients, AI outputs proved equally biased. Now that we understand the problem of implicit human bias, future generations of ChatGPT can help overcome it.

The first step will be for hospitals leaders to connect electronic health record systems to generative AI apps. Then, they will need to prompt the technology to notify clinicians when they provide insufficient care to patients from different racial or socioeconomic backgrounds. Bringing implicit bias to consciousness would save the lives of more Black women and children during delivery and could go a long way toward reversing our nation’s embarrassing maternal mortality rate (along with improving the country’s health overall).

The Next Five Years

Two things are inevitable over the next five years. Both will challenge the practice of medicine like never before and each has the potential to transform American healthcare.

First, generative AI will provide patients with more options and greater control. Faced with the difficulty of finding an available doctor, patients will turn to chatbots for their physical and psychological problems.

Already, AI has been shown to be more accurate in diagnosing medical problems and even more empathetic than clinicians in responding to patient messages. The latest versions of generative AI are not ready to fulfill the most complex clinical roles, but they will be in five years when they are 30-times more powerful and capable.

Second, the retail giants (Amazon, CVS, Walmart) will play an ever-bigger role in care delivery. Each of these retailers has acquired primary care, pharmacy, IT and insurance capability and all appear focused on Medicare Advantage, the capitated option for people over the age of 65. Five years from now, they will be ready to provide the businesses that pay for the medical coverage of over 150 million Americans the same type of prepaid, value-based healthcare that currently isn’t available in nearly all parts of the country.

American healthcare can stop the current slide over the next five years if change begins now. I urge medical leaders and elected officials to lead the process by joining forces and implementing these highly effective, inexpensive approaches to rebuilding primary care, lowering medical costs, improving access and making healthcare more equitable.

Issue: Medical debt negatively affects many Americans, especially people of color, women, and low-income families. Federal and state governments have set some standards to protect patients from medical debt.

Goal: To evaluate the current landscape of medical debt protections at the federal and state levels and identify where they fall short.

Methods: Analysis of federal and state laws, as well as discussions with state experts in medical debt law and policy. We focus on laws and regulations governing hospitals and debt collectors.

Key Findings and Conclusion: Federal medical debt protection standards are vague and rarely enforced. Patient protections at the state level help address key gaps in federal protections. Twenty states have their own financial assistance standards, and 27 have community benefit standards. However, the strength of these standards varies widely. Relatively few states regulate billing and collections practices or limit the legal remedies available to creditors. Only five states have reporting requirements that are robust enough to identify noncompliance with state law and trends of discriminatory practices. Future patient protections could improve access to financial assistance, ensure that nonprofit hospitals are earning their tax exemption, and limit aggressive billing and collections practices.

Introduction

Medical debt, or personal debt incurred from unpaid medical bills, is a leading cause of bankruptcy in the United States. As many as 40 percent of U.S. adults, or about 100 million people, are currently in debt because of medical or dental bills. This debt can take many forms, including:

past-due payments directly owed to a health care provider

ongoing payment plans

money owed to a bank or collections agency that has been assigned or sold the medical debt

credit card debt from medical bills

money borrowed from family or friends to pay for medical bills.

This report discusses findings from our review of federal and state laws that regulate hospitals and debt collectors to protect patients from medical debt and its negative consequences. First, we briefly discuss the impact and causes of medical debt. Then, we present federal medical debt protections and discuss gaps in standards as well as enforcement. Then, we provide an overview of what states are doing to:

strengthen requirements for financial assistance and community benefits

regulate hospitals’ and debt collectors’ billing and collections activities

limit home liens, foreclosures, and wage garnishment

develop reporting systems to ensure all hospitals are adhering to standards and not disproportionately targeting people of color and low-income communities.

(See the appendix for an overview of medical debt protections in all 50 states and the District of Columbia.)

Impact of Medical Debt

More than half of people in medical and dental debt owe less than $2,500, but because most Americans cannot cover even minor emergency expenses, this debt disrupts their lives in serious ways. Fear of incurring medical debt also deters many Americans from seeking medical care. About 60 percent of adults who have incurred medical debt say they have had to cut back on basic necessities like food or clothing, and more than half the adults from low-income households (less than $40,000) report that they have used up their savings to pay for their medical debt.

A significant amount of medical debt is either sold or assigned to third-party debt-collecting agencies, who often engage in aggressive efforts to collect on the debt, creating stress for patients. Both hospitals and debt collectors have won judgments against patients, allowing them to take money directly from a patient’s paycheck or place liens on a patient’s home. In some cases, patients have also lost their homes. Medical debt can also have a negative impact on a patient’s credit score.

Key Terms Related to Medical Debt

Financial assistance policy: A hospital’s policy to provide free or discounted care to certain eligible patients. Eligibility for financial assistance can depend on income, insurance status, and/or residency status. A hospital may be required by law to have a financial assistance policy, or it may choose to implement one voluntarily. Financial assistance is frequently referred to as “charity care.”

Bad debt: Patient bills that a hospital has tried to collect on and failed. Typically, hospitals are not supposed to pursue collections for bills that qualify for financial assistance or charity care, so bad debt refers to debt owed by patients ineligible for financial assistance.

Community benefit requirements: Nonprofit hospitals are required by federal law and some state laws to provide community benefits, such as financial assistance and other investments targeting community need, in exchange for a tax exemption.

Debt collectors or collections agencies: Entities whose business model primarily relies on collecting unpaid debt. They can either collect on behalf of a hospital (while the hospital still technically holds the debt) or buy the debt from a hospital.

Sale of medical debt: Hospitals sometimes sell the debt patients owe them to third-party debt buyers, who can be aggressive in seeking repayment of the debt.

Creditor: A party that is owed the medical debt and often wants to collect on the medical debt. This can be a hospital, a debt collector acting on behalf of a hospital, or a third-party debt buyer.

Debtor: A patient who owes medical debt over unpaid medical bills.

Wage garnishment: The ability of a creditor to get a court order that would allow them to deduct a portion of a debtor-patient’s paycheck before it reaches the patient. Federal law limits how much can be withheld from a debtor’s paycheck, and some states exceed this federal protection.

Placing a lien: A legal claim that a creditor can place on a patient’s home, prohibiting the patient from selling, transferring, or refinancing their home without first paying off the creditor. Most states require creditors to get a court order before placing a lien on a home.

Foreclosure or forced sale: A creditor can repossess and sell a patient’s home to pay off their medical debt. Often, creditors are required to obtain a court order to do so.

Perhaps what is most troubling is that the burden of medical debt is not borne equally: Black and Hispanic/Latino adults and women are much more likely to incur medical debt. Black adults also tend to be sued more often as a result. Uninsured patients, those from low-income households, adults with disabilities, and young families with children are all at a heightened risk of being saddled with medical debt.

Causes of Medical Debt

Most people — 72 percent, according to one estimate — attribute their medical debt to bills from acute care, such as a single hospital stay or treatment for an accident. Nearly 30 percent of adults who owe medical debt owe it entirely for hospital bills.

Although uninsured patients are more likely to owe medical debt than insured patients, having insurance does not fully shield patients from medical debt and all its consequences. More than 40 percent of insured adults report incurring medical debt, likely because they either had a gap in their coverage or were enrolled in insurance with inadequate coverage. High deductibles and cost sharing can leave many exposed to unexpected medical expenses.

The problem of medical debt is further exacerbated by hospitals charging increasingly high prices for medical care and failing to provide adequate financial assistance to uninsured and underinsured patients with low income.

Key Findings

Federal Medical Debt Protections Have Many Gaps

At the federal level, the tax code, enforced by the Internal Revenue Service (IRS), requires nonprofit hospitals to broadly address medical debt. However, these requirements do not extend to for-profit hospitals (which make up about a quarter of U.S. hospitals) and have other limitations.

Further, the IRS does not have a strong track record of enforcing these requirements. In the past 10 years, the IRS has not revoked any hospital’s nonprofit status for noncompliance with these standards.

The Consumer Financial Protection Bureau and the Federal Trade Commission have additional oversight authority over credit reporting and debt collectors. The Fair Credit Reporting Act regulates credit reporting agencies and those that provide information to them (debt collectors and hospitals). Consumers have the right to dispute any incomplete or inaccurate information and remove any outdated, negative information. In some cases, patients can directly sue hospitals or debt collectors for inaccurately reporting medical debt to credit reporting agencies. In addition, the Federal Debt Collection Practices Act limits how aggressive debt collectors can be by restricting the ways and times in which they can contact debtors, requiring certain disclosures and notifications, and prohibiting unfair or deceptive practices. Patients can directly sue debt collectors in violation of the law. This law, however, does not limit or prohibit the use of certain legal remedies, like wage garnishment or foreclosure, to collect on a debt.

Many states have taken steps to fill the gaps in federal standards. Within a state, several agencies may play a role in enforcing medical debt protections. Generally speaking:

state departments of health are the primary regulators of hospitals and set standards for them

state departments of taxation are responsible for ensuring nonprofit hospitals are earning their exemption from state taxes

state attorneys general protect consumers from unfair and deceptive business practices by hospitals and debt collectors.

Fewer Than Half of States Exceed Federal Requirements for Financial Assistance, Protections Vary Widely

Federal law requires nonprofit hospitals to establish and publicize a written financial assistance policy, but these standards leave out for-profit hospitals and lack any minimum eligibility requirements. As the primary regulators of hospitals, states have the ability to fill these gaps and require hospitals to provide financial assistance to low-income residents. Twenty states require hospitals to provide financial assistance and set certain minimum standards that exceed the federal standard.

All but three of these 20 states extend their financial assistance requirements to for-profit hospitals. Of these 20 states, four states — Connecticut, Georgia, Nevada, and New York — apply their financial assistance requirements only to certain types of hospitals.

Policies also vary among the 31 states that do not have statutory or regulatory financial assistance requirements for hospitals. For example, the Minnesota attorney general has an agreement in place with nearly every hospital in the state to adhere to certain patient protections, though it falls short of requiring hospitals to provide financial assistance. Massachusetts operates a state-run financial assistance program partly funded through hospital assessments. Other states use far less prescriptive mechanisms to try to ensure that patients have access to financial assistance, such as placing the onus of treating low-income patients on individual counties or requiring hospitals to have a plan for treating low-income and/or uninsured patients without setting any specific requirements.

Enforcement of state financial assistance standards.

The only way to enforce the federal financial assistance requirement is to threaten a hospital’s nonprofit status, and the IRS has been reluctant to use this authority. Among the 20 states that have their own state financial assistance standards, 10 require compliance as a condition of licensure or as a legal mandate. These mandates are often coupled with administrative penalties, but some states have established additional consequences. For example, Maine allows patients to sue noncompliant hospitals.

Six states make compliance with their financial assistance standards a condition of receiving funding from the state. Two other states use their certificate-of-need process (which requires hospitals to seek the state’s approval before establishing new facilities or expanding an existing facility’s services) to impose their financial assistance mandates.

Setting eligibility requirements for financial assistance.

The federal financial assistance standard sets no minimum eligibility requirements for hospitals to follow. However, the 20 states with financial assistance standards define which residents are eligible for aid.

One way for states to ensure that financial assistance is available to those most in need is to prevent hospitals from discriminating against undocumented immigrants. Four states explicitly prohibit such discrimination in statute and regulation. Most states, however, are less explicit. Thirteen states define eligibility broadly, basing it most frequently on income, insurance status, and state residency. However, it is unclear how hospitals are interpreting this requirement when it comes to patients’ immigration status. In contrast, three states explicitly exclude undocumented immigrants from eligibility.

States also vary widely in terms of which income brackets are eligible for financial assistance and how much financial assistance they may receive.

At least three of the 20 states with financial assistance standards allow certain patients with heavy out-of-pocket medical expenses from catastrophic illness or prior medical debt to access financial assistance. Many states also require hospitals to consider a patient’s insurance status when making financial assistance determinations. At least six states make financial assistance available for uninsured patients only, while at least eight others also make financial assistance available to underinsured patients.

Standardizing the application process.

Cumbersome applications can discourage many patients from applying for financial assistance. Five states have developed a uniform application form, while three others have set minimum standards for financial assistance applications. Eleven states require hospitals to give patients the right to appeal a denial of financial assistance.

States Split in Requiring Nonprofit Hospitals to Invest in Community Benefits

Federal and state policymakers also can require nonprofit hospitals to invest in community benefits in return for tax exemptions. Federal law requires nonprofit hospitals to produce a community health needs assessment every three years and have an implementation strategy. Almost all states exempt nonprofit hospitals from a host of state taxes, including income, property, and/or sales taxes. However, only 27 impose community benefit requirements on nonprofit hospitals.

Community benefits frequently include financial assistance but also investments that address issues like lack of access to food and housing. In the long run, these investments can reduce medical debt burden by improving population health and the financial stability of a community. Most states that require nonprofit hospitals to provide community benefits allow nonprofit hospitals to choose how they invest their community benefit dollars. This hands-off approach has given rise to concerns about the lack of transparency in community benefit spending as well as questions about whether hospitals are investing this money in ways that are most helpful to the community, such as in providing financial assistance.

Applicability of community benefit standards.

Nineteen states impose community benefit requirements on all nonprofit hospitals in the state, but three states further limit these requirements to hospitals of a certain size. At least six states have extended these requirements to for-profit hospitals as well. Of these six, the District of Columbia, South Carolina, and Virginia have incorporated community benefit requirements into their certificate-of-need laws instead of their tax laws. As a result, any hospital seeking to expand in these states becomes subject to their community benefit requirement.

Interaction between financial assistance and community benefits.

The federal standard allows nonprofit hospitals to report financial assistance as part of their community benefit spending. Most states with community benefit requirements also allow hospitals to do this. However, only seven states require hospitals to provide financial assistance to satisfy their community benefit obligations.

Setting quantitative standards for community benefit spending.

Only seven states set minimum spending thresholds that hospitals must meet or exceed to satisfy state community benefit standards. For example, Illinois and Utah require nonprofit hospitals’ community benefit contributions to equal what their property tax liability would have been. Unique among states, Pennsylvania gives taxing districts the right to sue nonprofit hospitals for not holding up their end of the bargain, which has proven to be a strong enforcement mechanism.

Fewer Than Half the States Exceed Federal Standards for Billing and Collections

Hospital billing and collections practices can significantly increase the burden of medical debt on patients. However, the current federal standard does not regulate these practices beyond imposing waiting periods and prior notification requirements for certain extraordinary collections actions (ECAs), such as garnishing wages or selling the debt to a third party.

Requiring hospitals to provide payment plans.

Federal standards do not require hospitals to make payment plans available. However, a few states do require hospitals to offer payment plans, particularly for low-income and/or uninsured patients. For example, Colorado requires hospitals to provide a payment plan and limit monthly payments to 4 percent of a patient’s monthly gross income and to discharge the debt once the patient has made 36 payments.

Limiting interest on medical debt.

Federal law does not limit the amount of interest that can be charged on medical debt. However, eight states have laws prohibiting or limiting interest for medical debt. Some states like Arizona have set a ceiling for interest on all medical debt. Others like Connecticut further prohibit charging interest to patients who are at or below 250 percent of the federal poverty level and are ineligible for public insurance programs.

Though many states do not have specific laws prohibiting or limiting interest that hospitals or debt collectors can charge on medical debt, all states do have usury laws, which limit the amount of interest than can be charged on any oral or written agreement. Usury limits are set state-by-state and can range anywhere from 5 percent to more than 20 percent, but most limits fall well below the average interest rate for a credit card (around 24%). At least one state, Minnesota, has sued a health system for charging interest rates on medical debt that exceeded the allowed limit in the state’s usury laws.

Interactions between hospitals, third-party debt collectors, and patients.

Unlike hospitals, debt collectors do not have a relationship with patients and can be more aggressive when collecting on the debt. Federal law neither limits when a hospital can send a bill to collections, nor does it require hospitals to oversee the debt collectors it uses. Most states (37) also do not regulate when a hospital can send a bill to collections, although some states have developed more protective approaches.

For example, Connecticut prohibits hospitals from sending the bills of certain low-income patients to collections, and Illinois requires hospitals to offer a reasonable payment plan first. Additionally, five states require hospitals to oversee their debt collectors.

Sale of medical debt to third-party debt buyers.

Hospitals sometimes sell old unpaid debt to third-party debt buyers for pennies on the dollar. Debt buyers can be aggressive in their efforts to collect, and sometimes even try to collect on debt that was never owed. Federal law considers the sale of medical debt an ECA and requires nonprofit hospitals to follow certain notice and waiting requirements before initiating the sale. Most states (44) do not exceed this federal standard.

Only three states prohibit the sale of medical debt. Two other states — California and Colorado — regulate debt buyers instead. For example, California prohibits debt buyers from charging interest or fees, and Colorado prohibits them from foreclosing on a patient’s home.

Reporting medical debt to credit reporting agencies.

Federal law considers reporting medical debt to a credit reporting agency to be an ECA and requires nonprofit hospitals to follow certain notice and waiting requirements beforehand. Most states (41) do not exceed this federal standard.

Of the 10 states that do go beyond the federal standard, a few like Minnesota fully prohibit hospitals from reporting medical debt. Most others require hospitals, debt collectors, and/or debt buyers to wait a certain amount of time before reporting the debt to credit agencies (Exhibit 8). Two states directly regulate credit agencies: Colorado prohibits them from reporting on any medical debt under $726,200, while Maine requires them to wait at least 180 days from the date of first delinquency before reporting that debt.

States Vary Widely on Patient Protections from Medical Debt Lawsuits

Federal law considers initiating legal action to collect on unpaid medical bills to be an extraordinary collections action and also limits how much of a debtor’s paycheck can be garnished to pay a debt.

In most states, hospitals and debt buyers can sue patients to collect on unpaid medical bills. Three states limit when hospitals and/or collections agencies can initiate legal action. Illinois prohibits lawsuits against uninsured patients who demonstrate an inability to pay. Minnesota prohibits hospitals from giving “blanket approval” to collections agencies to pursue legal action, and Idaho prohibits the initiation of lawsuits until 90 days after the insurer adjudicates the claim, all appeals are exhausted, and the patient receives notice of the outstanding balance.

Liens and foreclosures.

Most states (32) do not limit hospitals, collections agencies, or debt buyers from placing a lien or foreclosing on a patient’s home to recover on unpaid medical bills. However, almost all states provide a homestead exemption, which protects some equity in a debtor’s home from being seized by creditors during bankruptcy. The amount of homestead exemption available to debtors varies from state to state, ranging from just $5,000 to the entire value of the home. Seven states have unlimited homestead exemptions, allowing debtors to fully shield their primary homes from creditors during bankruptcy. Additionally, Louisiana offers an unlimited homestead exemption for certain uninsured, low-income patients with at least $10,000 in medical bills.

Ten states prohibit or set limits on liens or foreclosures for medical debt. For example, New York and Maryland fully prohibit both liens and foreclosures because of medical debt, while California and New Mexico only prohibit them for certain low-income populations.

Wage garnishment.

Under federal law, the amount of wages garnished weekly may not exceed the lesser of: 25 percent of the employee’s disposable earnings, or the amount by which an employee’s disposable earnings are greater than 30 times the federal minimum wage. Twenty-one states exceed the federal ceiling for wage garnishment. Only a few states go further to prohibit wage garnishment for all or some patients. For example, New York fully prohibits wage garnishment to recover on medical debt for all patients, yet California only extends this protection for certain low-income populations. While New Hampshire does not prohibit wage garnishment, it requires the creditor to keep going back to court every pay period to garnish wages, which significantly limits creditors’ ability to garnish wages in practice.

Many States Have Hospital Reporting Requirements, But Few Are Robust

Federal law requires all nonprofit hospitals to submit an annual tax form including total dollar amounts spent on financial assistance and written off as bad debt. However, these reporting requirements do not extend to for-profit hospitals and lack granularity. States, as the primary regulators of hospitals, would likely benefit from more robust data collection processes to better understand the impact of medical debt and guide their oversight and enforcement efforts.

Currently, 32 states collect some of the following:

financial data, including the total dollar amounts spent on financial assistance and/or bad debt

financial assistance program data, including the numbers of applications received, approved, denied, and appealed

demographic data on the populations most affected by medical debt

information on the number of lawsuits and types of judgments sought by hospitals against patients.

Fifteen states explicitly require hospitals to report total dollar amounts spent on financial assistance and/or bad debt, while 11 states also require hospitals to report certain data related to their financial assistance programs. Most of these 11 states limit the data they collect to the numbers of applications received, approved, denied, and appealed. However, a handful of them go further and ask hospitals to report on the amount of financial assistance provided per patient, number of financial assistance applicants approved and denied by zip code, number of payment plans created and completed, and number of accounts sent to collections.

Five states require hospitals to further break down their financial assistance data by race, ethnicity, gender, and/or preferred or primary language. For example, Maryland requires hospitals to break down the following data by race, ethnicity, and gender: the bills hospitals write off as bad debt and the number of patients against whom the hospital or the debt collector has filed a lawsuit.

Only Oregon asks hospitals to report on the number of patient accounts they refer for collections and extraordinary collections actions.

Discussion and Policy Implications

In 2022, the federal government announced administrative measures targeting the medical debt problem, which included launching a study of hospital billing practices and prohibiting federal government lenders from considering medical debt when making decisions on loan and mortgage applications. Although these measures will help some, only federal legislation and enhanced oversight will likely address current gaps in federal standards.

States can also fill the gaps in federal patient protections by improving access to financial assistance, ensuring that nonprofit hospitals are earning their tax exemption, and protecting patients against aggressive billing and collections practices. States also can leverage underutilized usury laws to protect their residents from medical debt.

Finding the most effective ways to enforce these standards at the state level could also protect patients. Absent oversight and enforcement, patients from underserved communities continue to face harm from medical debt, even when states require hospitals to provide financial assistance and prohibit them from engaging in aggressive collections practices. Bolstering reporting requirements alone would not likely ensure compliance, but states could protect patients by strengthening their penalties, providing patients with the right to sue noncompliant hospitals, and devoting funding to increase oversight by state agency officials.

To develop a comprehensive medical debt protection framework, states could also bring together state agencies like their departments of health, insurance, and taxation, as well as their state attorney general’s office. Creating an interagency office dedicated to medical debt protection would allow for greater efficiency and help the state build expertise to take on the well-resourced debt collection and hospital industries.

Still, these measures only address the symptoms of the bigger problem: the unaffordability of health care in the United States. Federal and state policymakers who want to have a meaningful impact on the medical debt problem could consider the protections discussed in this report as part of a broader plan to reduce health care costs and improve coverage.

Albert Einstein determined that time is relative. And when it comes to healthcare, five years can be both a long and a short amount of time.

In August 2018, I launched the Fixing Healthcare podcast. At the time, the medium felt like the perfect auditory companion to the books and articles I’d been writing. By bringing on world-renowned guests and engaging in difficult but meaningful discussions, I hoped the show would have a positive impact on American medicine. After five years and 100 episodes, now is an opportune time to look back and examine how healthcare has improved and in what ways American medicine has become more problematic.

Here’s a look at the good, the bad and the ugly since episode one of Fixing Healthcare:

The Good

Drug breakthroughs and government actions headline medicine’s biggest wins over the past five years.

At first, health experts expressed doubts that Pfizer, Moderna and others could create a safe and effective Covid-19 vaccine with messenger RNA (mRNA) technology. After all, no one had succeeded in more than two decades of trying.

Thanks in part to Operation Warp Speed, the government-funded springboard for research, our nation produced multiple vaccines within less than a year. Previously, the quickest vaccine took four years to develop (mumps). All others required a minimum of five years.

The vaccines were pivotal in ending the coronavirus pandemic, and their success has opened the door to other life-saving drugs, including those that might prevent or fight cancer. And, of course, our world is now better prepared for when the next viral pandemic strikes.

Weight-Loss Drugs

Originally designed to help patients manage Type 2 diabetes, drugs like Ozempic have been helping people reverse obesity—a condition closely correlated with diabetes, heart disease and cancer.

For decades, America’s $150 billion a year diet industry has failed to curb the nation’s continued weight gain. So too have calls for increased exercise and proper nutrition, including restrictions on sugary sodas and fast foods.

In contrast, these GLP-1 medications are highly effective. They help overweight and obese people lose 15 to 25 pounds on average with side effects that are manageable for nearly all users.

The biggest stumbling block to their widespread use is the drug’s exorbitant price (upwards of $16,000 for a year’s supply).

Drug-Pricing Laws

With the Inflation Reduction Act of 2022, Congress took meaningful action to lower drug prices, a move the CBO estimates would reduce the federal deficit by $237 billion over 10 years.

It’s a good start. Americans today pay twice as much for the same medications as people in Europe largely because of Congressional legislation passed in 2003.

That law, the Medicare Prescription Drug Price Negotiation Act, made it illegal for Health and Human Services (HHS) to negotiate drug prices with manufacturers—even for the individuals publicly insured through Medicare and Medicaid.

Now, under provisions of the new Inflation Reduction Act, the government will be able to negotiate the prices of 10 widely prescribed medications based on how much Medicare’s Part D program spends. The lineup is expected to include prescription treatments for arthritis, cancer, asthma and cardiovascular disease. Unfortunately, the program won’t take effect until 2026. And as of now, several legal challenges from both drug manufacturers and the U.S. Chamber of Commerce are pending.

The Bad

Spiking costs, ongoing racial inequalities and millions of Americans without health insurance make up three disappointing healthcare failures of the past five years.

Cost And Quality

The U.S. spends nearly twice as much on healthcare per citizen as other countries, yet our nation lags 10 of the wealthiest countries in medical performance and clinical outcomes. As a result, Americans die younger and experience more complications from chronic diseases than people in peer nations.

As prices climb ever-higher, at least half of Americans can’t afford to pay their out-of-pocket medical bills, which remain the leading cause of U.S. bankruptcy. And with rising insurance premiums alongside growing out-of-pocket expenses, more people are delaying their medical care and rationing their medications, including life-essential drugs like insulin. This creates a vicious cycle that will likely prolong today’s healthcare problems well into the future.

Health Disparities

Inequalities in American medicine persist along racial lines—despite action-oriented words from health officials that date back decades.

Today, patients in minority populations receive unequal and inequitable medical treatment when compared to white patients. That’s true even when adjusting for differences in geography, insurance status and socioeconomics.

Racism in medical care has been well-documented throughout history. But the early days of the Covid-19 pandemic provided several recent and deadly examples. From testing to treatment, Black and Latino patients received both poorer quality and less medical care, doubling and even tripling their chances of dying from the disease.

The problems can be observed across the medical spectrum. Studies show Black women are still less likely to be offered breast reconstruction after mastectomy than white women. Research also finds that Black patients are 40% less likely to receive pain medication after surgery. Although technology could have helped to mitigate health disparities, our nation’s unwillingness to acknowledge the severity of the problem has made the problem worse.

Uninsurance

Although there are now more than 90 million Americans enrolled in Medicaid, there are still 30 million people without any health insurance. This disturbing reality comes a full decade after the passage of the Affordable Care Act.

On Capitol Hill, there is no plan in place to reduce the number of uninsured.

Moreover, many states are looking to significantly rollback their Medicaid enrollment in the post-Covid era. Kaiser Family Foundation estimates that between 8 million and 24 million people will lose Medicaid coverage during the unwinding of the continuous enrollment provisions implemented during the pandemic. Without coverage, people have a harder time obtaining the preventive services they need and, as a result, they suffer more chronic diseases and die younger.

The Ugly

An overall decrease in longevity, along with higher maternal mortality and a worsening mental-health crisis, comprise the greatest failures of U.S. healthcare over the past five years.

Life Expectancy

Despite radical advances in medical science over the past five years, American life expectancy is back to where it was at the turn of the 20th century, according to CDC data.

Alongside environmental and social factors are a number of medical causes for the nation’s dip in longevity. Research demonstrated that many of the 1 million-plus Covid-19 deaths were preventable. So, too, was the nation’s rise in opioid deaths and teen suicides.

Regardless of exact causation, Americans are living two years less on average than when we started the Fixing Healthcare podcast five years ago.

Maternal Mortality

Compared to peer nations, the United States is the only country with a growing rate of mothers dying from childbirth. The U.S. experiences 17.4 maternal deaths per 100,000 live births. In contrast, Norway is at 1.8 and the Netherlands at 3.0.

The risk of dying during delivery or in the post-partum period is dramatically higher for Black women in the United States. Even when controlling for economic factors, Black mothers still suffer twice as many deaths from childbirth as white women.

And with growing restrictions on a woman’s right to choose, the maternal mortality rate will likely continue to rise in the United States going forward.

Mental Health

Finally, the mental health of our country is in decline with rates of anxiety, depression and suicide on the rise.

These problems were bad prior to Covid-19, but years of isolation and social distancing only aggravated the problem. Suicide is now a leading cause of death for teenagers. Now, more than 1 in every 1,000 youths take their own lives each year. The newest data show that suicides across the U.S. have reached an all-time high and now exceed homicides.

Even with the expanded use of telemedicine, mental health in our nation is likely to become worse as Americans struggle to access and afford the services they require.

The Future

In looking at the three lists, I’m reminded of a baseball slugger who can occasionally hit awe-inspiring home runs but strikes out most of the time. The crowd may love the big hitter and celebrate the long ball, but in both baseball and healthcare, failing at the basics consistently results in more losses than wins.

Over the past five years, American medicine has produced a losing record. New drugs and surgical breakthroughs have made headlines, but the deeper, more systemic failures of American healthcare have rarely penetrated the news cycle.

If our nation wants to make the next five years better and healthier than the last five, elected officials and healthcare leaders will need to make major improvements. The steps required to do so will be the focus of my next article.

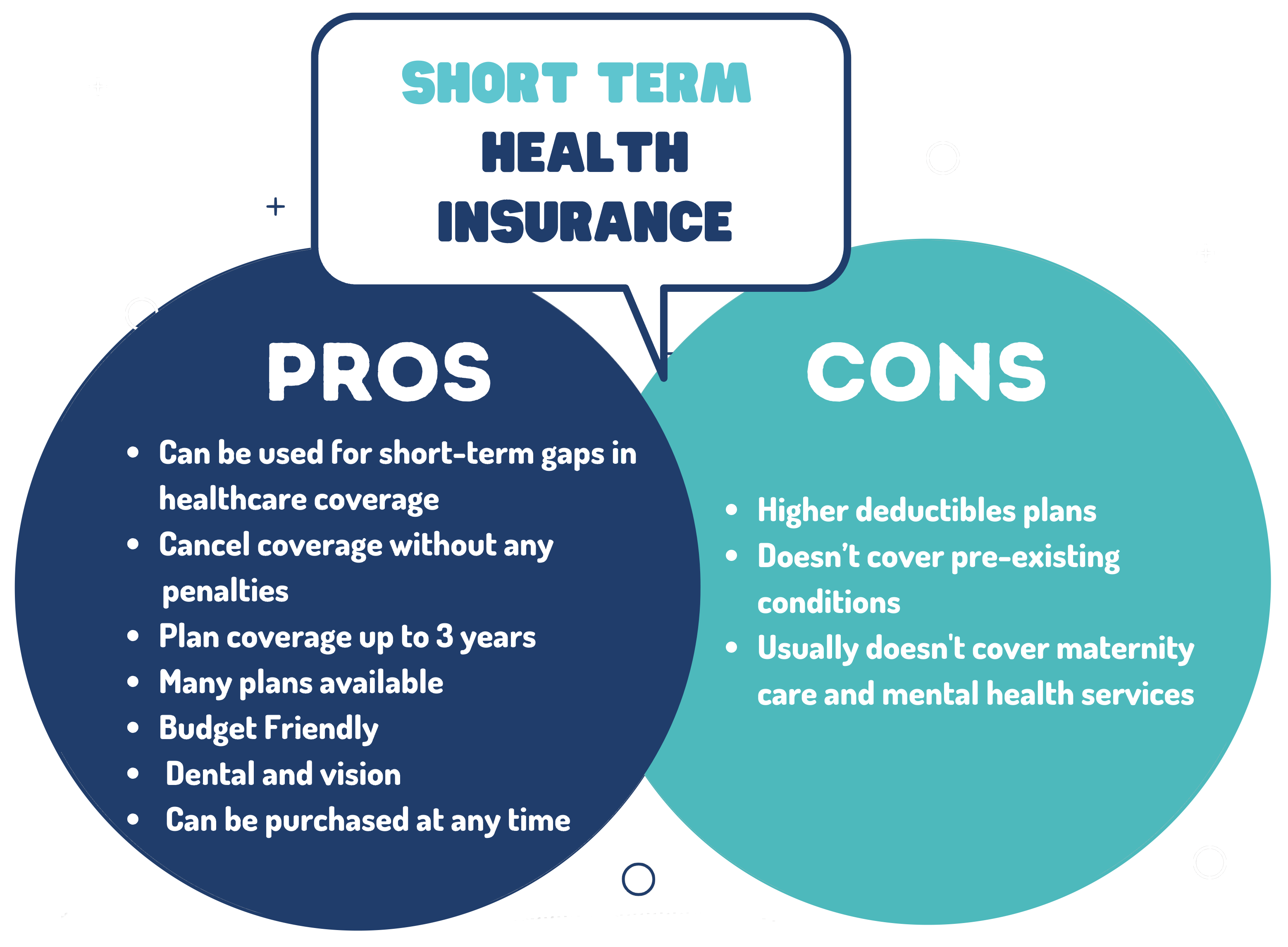

Last Friday, the Department of Health and Human Services, the Treasury Department, and the Department of Labor jointly issued several proposed rules to shore up consumer healthcare protections, including reversal of a Trump administration policy that allowed consumers to enroll in short-term health plans, which were intended to serve as limited coverage options during transitional periods, for up to three years. Approximately 3M people were enrolled in these plans in 2019.

A new rule would limit consumer access to these plans to just three months, with an optional one-month extension, while also requiring payers to disclose clearly how their plans fall short of comprehensive health insurance.

The Gist: In an expected move, theBiden administration continues its unwinding of the Trump-era policies it sees as undermining the Affordable Care Act’s (ACA’s) mission of guaranteeing robust, accessible insurance for all.

Short-term plans, which were granted an exemption from the ACA requirement that health plans cover ten essential health benefits, have been found to discriminate against people with pre-existing conditions, revoke coverage for enrollees retroactively, and generate excess surprise bills due to their limited networks.

On July 1st, Georgia will launch its Pathways to Coverage program, which partially expands its Medicaid program to enroll individuals with incomes up to 100 percent of the federal poverty line (FPL), but only if they demonstrate at least 80 hours a month of work, education, job training, or community service.

This expansion is only projected to extend Medicaid coverage to an additional 50K state residents, far short of the 400K that full Medicaid expansion (without work requirements, to individuals earning up to138 percent of the FPL) would have covered. Georgia’s plan was approved by the Trump administration in 2020, but the Biden administration rescinded its waiver prior to implementation. Georgia then sued the Biden administration, and a Federal District Court sided with the state, allowing the partial expansion with work requirements to proceed. The Biden administration chose not to appeal.

The Gist: Though Georgia’s implementation is more limited in scope compared with other states which are currently pursuing Medicaid work requirements, Georgia sets a precedent to motivate those states that are looking to pursue similar strategies.

Research has shown that most adults on Medicaid who do not face barriers to work are already working,and that the cost of systems to monitor beneficiary work status likely offsets any savings in reduced Medicaid spending.

The burden of having to report work status is onerous for potential Medicaid enrollees, discouraging some from seeking coverage altogether.

Billionaire investor Charlie Munger has been vocal in expressing his concerns about U.S. healthcare, stating that it is “shot through with rampant waste” and has become “immoral.”

Munger says there are substantial problems that need to be addressed, including the presence of unnecessary costs and inefficiencies that plague the medical field.

Drawing a vivid analogy at a Daily Journal Annual Meeting, Munger compared the experience of a dying old person in many American hospitals to that of a carcass on the plains of Africa. He painted a bleak picture, describing how vultures, jackals, hyenas and other scavengers swarm around the helpless creature.

In an attempt to address these issues, Berkshire Hathaway, Amazon.com Inc., and JPMorgan Chase joined forces to establish Haven Healthcare a venture that despite their combined efforts failed to achieve its objectives.

Some startups have seen success where they failed. iRemedy, for example, is a startup using artificial intelligence (AI) technology, that offers a solution to the healthcare system’s challenges through its large procurement marketplace. Its platform streamlines the supply chain, enabling faster and more affordable access to lifesaving supplies for doctors, hospitals and healthcare providers.

Munger, vice chairman of Berkshire Hathaway Inc., criticized the high costs and inefficiencies in medical care as both expensive and wrong. In a CNBC interview, he went on to claim that some medical providers artificially prolong death to increase their profits.

With over 35 years of experience as board chairman of Good Samaritan Hospital in Los Angeles, Munger expressed his belief that certain healthcare practices are absurd.

“A lot of the medical care we do deliver is wrong — so expensive and wrong. It’s ridiculous,” he said in a “Squawk Box” interview.

In 2018, Munger predicted that when Democrats gain control of all three branches of government, there will be a push for a single-payer healthcare system. He highlighted the need for a complete change forced by the government because of the severity of the issues in the current system. He suggested that a universal healthcare system with an opt-out option would be a reasonable solution.

Warren Buffett, Munger’s longtime investing partner, shares similar concerns regarding healthcare spending, referring to it as a “tapeworm on the economic system.” Buffett believes the private sector can make substantial contributions to cost-reduction efforts.

A recent investigation conducted by Kaiser Health News-NPR shed light on the alarming reality of medical debt in the United States. The study reveals that over 100 million Americans are burdened with medical debt, placing a significant financial strain on their lives. Further analysis of the data reveals that approximately one-fourth of American adults carrying this debt owe more than $5,000.

What makes this issue even more concerning is the fact that it is not primarily driven by a lack of insurance coverage. Contrary to popular belief, the majority of people grappling with medical debt are not uninsured. Instead, it is the problem of being underinsured that is prevalent.

Many people have health insurance plans that do not offer sufficient coverage, leaving them vulnerable to high out-of-pocket expenses and accumulating medical debt.

On April 1st, Medicaid’s pandemic-era continuous enrollment policy began to sunset, kicking off a 14-month window for states to reassess their Medicaid rolls. In this week’s graphic, we highlight new Congressional Budget Office projections showing the impact of Medicaid redeterminations on insurance coverage rates over the next decade for the under-65 population.

The Medicaid and Children’s Health Insurance Program (CHIP) coverage rate is expected to drop from 31 percent of all Americans under 65 in 2023, to 27 percent in 2024.

Meanwhile, after reaching an all-time low in 2023,the under-65 uninsured rate is projected to surpass nine percent in 2024 and climb to over 10 percent by 2033.

While over 15M Americans are expected to lose Medicaid coverage during redeterminations, a majority of those disenrolled will gain health insurance either through an employer-sponsored or non-group plan.

But over 6M people, nearly 40 percent of those losing Medicaid coverage, are projected to become uninsured, erasing nearly half the progress the country has made since 2019 at lowering the uninsured rate.

Last week, Marlee Stark and I published an op-ed in the Arkansas Democrat Gazette on why the Arkansas Department of Human Services (DHS) should press pause on its Medicaid unwinding process. Earlier this month, DHS released its first report laying out how many people lost coverage in April, as the state resumed its redetermination process.

As we write,

According to DHS’ recent report, over 50,000 people were disenrolled for procedural reasons, like failure to return paperwork or requested information, or because the state didn’t have their correct address on file. Only 15 percent of those who were disenrolled were confirmed truly ineligible or said they no longer needed their coverage, likely because they acquired another source of coverage during the pandemic.

In our piece, we argue that DHS should take a look at why so many people are losing coverage even though they may still be eligible—and outline some of the consequences the state may face if it chooses not to do so.