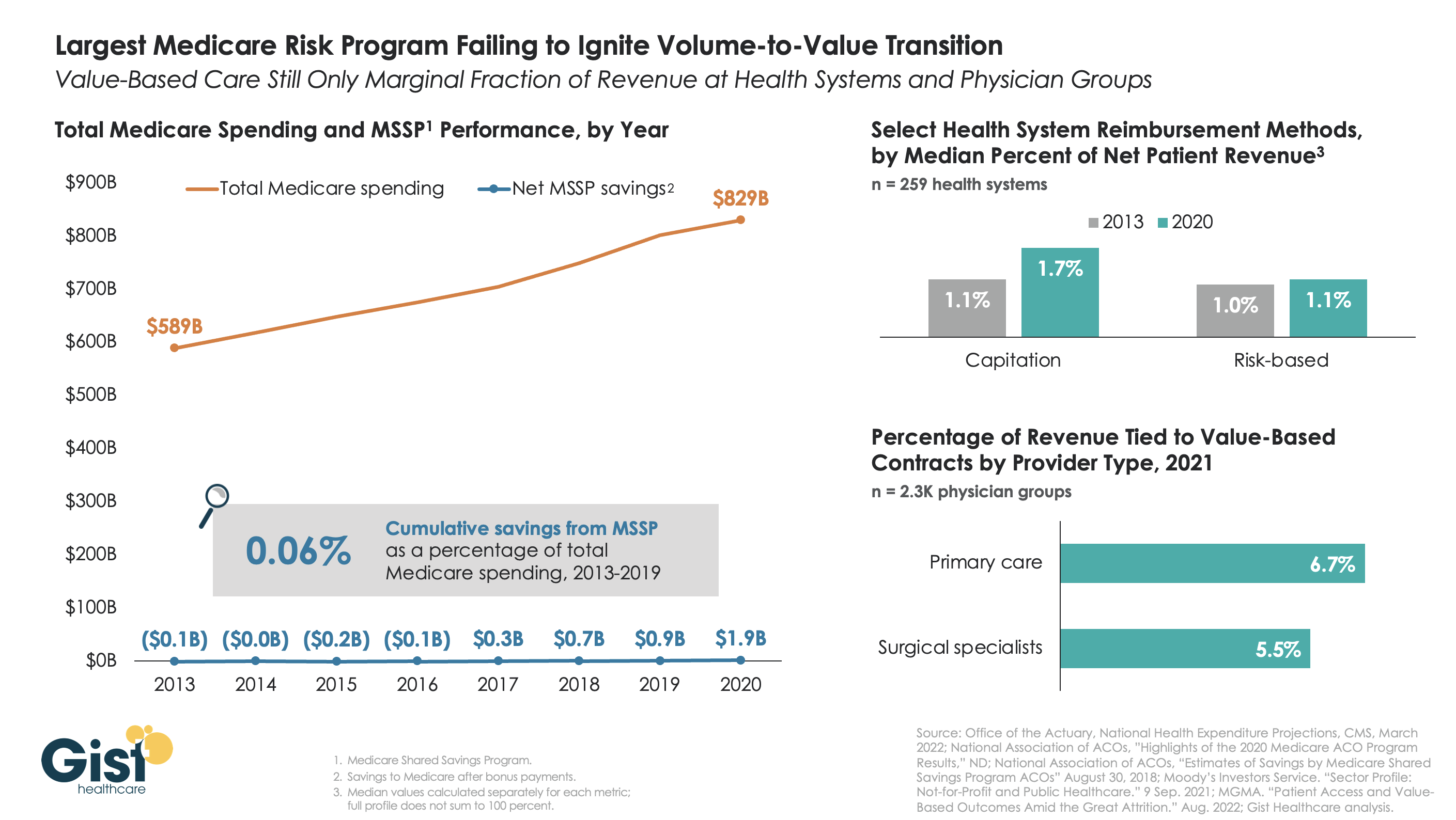

The belief that healthcare should, and would, transition from “volume to value” was a key pillar of the Affordable Care Act (ACA). However, with more than a decade of experience and data to consider, there is little indication that either Medicare or the healthcare industry at large has meaningfully shifted away from fee-for-service payment. Using data from the National Association of Accountable Care Organizations, the graphic below shows that the Medicare Shared Savings Program (MSSP)—the largest of the ACA’s payment innovations, with over 500 accountable care organizations (ACOs) reaching 11M assigned beneficiaries—has led to minimal savings for Medicare. In its first eight years, MSSP saved Medicare only $3.4B, or a paltry 0.06 percent, of the $5.6T that it spent over that time.

Policymakers had hoped that a Medicare-led move to value would prompt commercial payers to follow suit, but that also hasn’t happened. The proportion of payment to health systems in capitated or other risk-based arrangements barely budged from 2013 to 2020—remaining negligible for most organizations, and rarely amounting to enough to influence strategy. The proportion of risk-based payment for doctors is slightly higher, but still far below what is needed to enable wholesale change in care across a practice.

While Medicare has other options if it wants to increase value-based payment, like making ACOs mandatory, it’s harder to see how the trend in commercial payment will improve, as large payers, who are buying up scores of care delivery assets themselves, seem to have little motivation to deal providers in on risk.

While financial upside of moving to risk hasn’t been significant enough to move the market to date, we aren’t suggesting health systems throw out their population management playbook—to meet mounting cost labor pressures, systems must deliver lower cost care, in lower cost settings, with lower cost staff, just to maintain economic viability moving forward.

In a press release, London-based telemedicine provider Babylon Health said it intends to divest Meritage Medical Network, its 1,800-physician independent practice association located in Northern and Central California. Babylon claims the sale will allow it to better focus on its core business model of digital-first, value-based care contracts. After going public last year at $4.2B, Babylon’s valuation has fallen over 95 percent.

The Gist: Yet another highly touted healthcare startup with digital-first “solutions” has announced a massive pullback in its care footprint. As we wrote about Bright Health last week, these companies have failed to meet investor demands, and mustnowshutter services or sell assets to buy time to prove their core business model can actually turn a profit.

In Babylon’s case, integrating established physician practices into a digital-first, value-based care model was always going to be costly, challenging and time-consuming—too slow to deliver the returns demanded by an increasingly difficult investor market.

In a randomized controlled trial (RCT) study of 85K Europeans, published this week in the New England Journal of Medicine, colonoscopies were found to reduce incidence of colorectal cancer by only 18 percent—much less than earlier large studies—and have no impact on ten-year colorectal cancer mortality rates. This is the first study to directly compare individuals invited to receive colonoscopies with a control group receiving no cancer screening.

While the study’s findings surprised many researchers, an important caveat to the headline takeaways is that a secondary analysis of study participants who actually completed their colonoscopies found a 50 percent reduction in death, though the decision to accept the invitation likely correlates with other factors that improve mortality outcomes.

The Gist: We were surprised to learn this was the first RCT to assess the effectiveness of colonoscopies—15M of which are performed in the US each year—and which comprise a $36B market. While the study’s results need careful interpretation, it reminds us that much of established medical consensus has yet to be “proven” by rigorous scientific research.

While we don’t expect this study’s results to significantly change colonoscopy recommendations, it does place greater emphasis on the question of value generated by widespread preventative screenings. Colonoscopy will almost certainly remain the gold standard for colon cancer screening in the US, but if these results bear out, other less invasive types of screening, like home-based fecal immunochemical testing, could be viewed as equivalent options and receive more traction.

In an Oct. 5, 2022, commentary, Ken Kaufman offers a full-throated and heartfelt defense of non-profit healthcare during a time of significant financial hardship. Ken describes 2022 as “the worst financial year for hospitals in memory.” His concern is legitimate. The foundations of the nonprofit healthcare business model appear to be collapsing. I’ve known and worked with Ken Kaufman for decades. He is the life force behind Kaufman Hall, a premier financial and strategic advisor to nonprofit hospitals and health systems. The American Hospital Association uses Kaufman Hall’s analysis of hospitals’ underlying financial trends to support its plea for Congressional funding. Beyond the red ink, Ken laments the “media free-for-all challenging the tax-exempt status, financial practices, and ostensible market power of not-for-profit hospitals and health systems.” He is referring to three recent investigative reports on nonprofits’ skimpy levels of charity care (Wall Street Journal), aggressive collection tactics (New York Times) and 340B drug purchasing program abuses (New York Times). Ken has never been timid about expressing his opinions. He’s passionate, partisan and proud. His defense of nonprofit healthcare chronicles their selfless care of critically ill patients, the 24/7 demands on their resources and their commitment to treating the uninsured. These “must have clinical services…don’t just magically appear.” Nonprofit healthcare needs “our support and validation in the face of extreme economic conditions and organizational headwinds. ”Given his personality, it’s not surprising that Ken’s strident rhetoric in defending nonprofit healthcare reminds me of the famous “You can’t handle the truth” exchange between Lieutenant Kaffee (Tom Cruise) and Colonel Jessup (Jack Nicholson) from the 1992 movie “A Few Good Men.” Kaffee presses Jessup on whether he ordered a “code red” that led to the death of a soldier under his command. When Kaffee declares he’s entitled to the truth, Jessup erupts,… I have neither the time nor the inclination to explain myself to a man that rises and sleeps under the blanket of the very freedom I provide and then questions the manner in which I provide it. I would rather you say, “thank you” and be on your way. Should American society just say “thank you” to nonprofit healthcare and provide the massive incremental funding required to sustain their current operations?

Truth and Consequences (Download PDF here)The social theorist Thomas Sowell astutely observed, “If you want to help someone, tell them the truth. If you want to help yourself, tell them what they want to hear.” In this commentary, Ken Kaufman is telling nonprofit healthcare exactly what they want to hear. The truth is more nuanced, troubling and inconvenient. Healthcare now consumes 20 percent of the national economy and the American people are sicker than ever. Despite the high healthcare funding levels, the CDC recently reported in U.S. life expectancy dropped almost a full year in 2021. Other wealthy nations experienced increases in life expectancy. Combining 2020 and 2021, the 2.7-year drop in U.S. life expectancy is the largest since the early 1920s. During an interview regarding the September 28, 2022, White House Conference on Hunger, Nutrition and Health, Senator Cory Booker highlighted two facts that capture America’s healthcare dilemma. One in three government dollars funds healthcare expenditure. Half of Americans suffer from diabetes or pre-diabetes.As a nation, we’re chasing our tail by prioritizing treatment over prevention. Particularly in low-income rural and urban communities, there is a breathtaking lack of vital primary care, disease management and mental health services. Instead of preventing disease, our healthcare system has become adept at keeping sick people alive with a diminished life quality. There is plenty of money in the system to amputate a foot but little to manage the diabetes that necessitates the amputation. Despite mission statements to the contrary, nonprofit healthcare follows the money. The only meaningful difference between nonprofit and for-profit healthcare is tax status. Each seeks to maximize treatment revenues by manipulating complex payment formularies and using market leverage to negotiate higher commercial payment rates. According to Grandview Research, the market for revenue cycle management in 2022 is $140.4 billion and forecasted to grow at a 10% annual rate through 2030. By contrast, Ibis World forecasts the U.S. automobile market to grow 2.6% in 2022 to reach $100.9 billion. Unbelievably, in today’s America, processing medical claims is far more lucrative than manufacturing and selling cars and trucks. According to CMS’s National Expenditure Report for 2020, hospitals (31%) and physicians and clinical services (20%) accounted for over half of national healthcare expenditures. This included $175 billion allocated to providers through the CARES Act. Despite the massive waste embedded within healthcare delivery, the CARES Act funding gave providers the illusion that America would continue to fund its profligate and often ineffective operations. It’s not at all surprising that healthcare providers now want, even expect, more emergency funding. Change is hard. Not even during COVID did providers give up their insistence on volume-based payment. Providers did not embrace proven virtual care and hospital-at-home business practices until CMS guaranteed equivalent payment to existing in-hospital/clinic service provision. Even with parity payment and the massive CARES Act funding, there was uneven care access for COVID patients. Particularly in low-income communities, tens of thousands died because they did not receive appropriate care. More of the same approach to healthcare delivery will yield more of the same dismal results. Healthcare providers have had over a decade to advance value-based care (VBC). I define VBC as the right care at the right time in the right place at the right price. Instead of pursuing VBC, providers have doubled-down on volume-driven business models that attract higher-paying commercially-insured patients. Despite the relative ease of migrating service provision to lower-cost settings, providers insist on operating high-cost, centralized delivery models (think hospitals). They want society, writ large, to continue paying premium prices for routine care. It’s time to stop. As a country, we need less healthcare and more health.

When I give speeches to healthcare audiences, I typically begin with three yes-or-no questions about U.S. healthcare to establish the foundation for my subsequent observations. Here they are. Question #1: The U.S. spends 20% of its economy on healthcare. The big country with the next highest percentage spend is France at 12%. How many believe we need to spend more than 20% of our economy to provide great healthcare to everyone in the country? No one ever raises their hand. Question #2: The CDC estimates that 90% of healthcare expenditure goes to treat individuals with chronic disease and mental health conditions. How many believe we’re winning the war against chronic disease and mental health conditions? No one ever raises their hand. Question #3: Given the answer to the previous two questions, how many believe the system needs to shift resources from acute and specialty care into health promotion, primary care, chronic disease management and behavioral health? Everyone raises their hands. This short exercise is quite revealing. It demonstrates that healthcare doesn’t have a funding problem. It has a distribution problem. It also demonstrates that providers aren’t adequately addressing our most critical healthcare challenge, exploding chronic disease and mental health conditions. Finally, the industry needs major restructuring.

The real questions about reforming healthcare are less about what to reform and more about how to undertake reform. The increasing media scrutiny that Ken Kaufman references as well as growing consumer frustrations with healthcare service provision, demonstrate that healthcare is losing the battle for America’s hearts and minds.

Markets are unforgiving. The operating losses most nonprofit providers are experiencing reflect a harsh reality. Their current business models are not sustainable. An economic reckoning is underway. The long arc of economics points toward value. As healthcare deconstructs, the nation’s acute care footprint will shrink, hospitals will close and value-based care delivery will advance. The process will be messy.

The devolving healthcare marketplace led me to ask a fourth question recently in Nashville during a keynote speech to the Council of Pharmacy Executives and Suppliers. Here it is. Question #4: As the healthcare system reforms, will that process be evolutionary (reflecting incremental change) or revolutionary (reflecting fundamental change). Two-thirds voted that the change would be revolutionary. That response is just one data point but it reflects why post-COVID healthcare reform is different than the reform efforts that have preceded it. The costs of maintaining status-quo healthcare are simply too high. From a policy perspective, either market-driven healthcare reforms will drive better outcomes at lower costs (that’s my hope) or America will shift to a government-managed healthcare system like those in Germany, France and Japan.

Like Ken Kaufman, I admire frontline healthcare workers and believe we need to make their vital work less burdensome. I also sympathize with health system executives who are struggling to overcome legacy business practices and massive operating deficits. Unfortunately, most are relying on revenue-maximizing playbooks rather than reconfiguring their operations to advance consumerism and value-based care delivery.

Unlike Ken Kaufman, I believe it’s time for some tough love with nonprofit healthcare providers. Payers must tie new incremental funding to concrete movement into value-based care delivery. This was the argument Zeke Emanuel, Merrill Goozner and I made in a two-part commentary (part 1; part 2) in Health Affairs earlier this year. It’s also why the HFMA, where I serve on the Board, has made “cost effectiveness of health (CEoH)” its new operating mantra.

While this truth may be hard, it also is liberating. Freeing nonprofit organizations from their attachment to perverse payment incentives can create the impetus to embrace consumerism and value. Kinder, smarter and affordable care for all Americans will follow.

Cross-subsidy economics are increasingly challenged for America’s hospitals. Aging Baby Boomers are moving from commercial insurance to Medicare, decreasing the share of patients with lucrative private coverage, and insurers are increasingly reticent to provide the rate increases providers need to make up for the worsening mix.

At a recent executive retreat, one health system debated the best strategies to increase their capture of commercial volume. Most of the conversation focused on traditional market-based tactics to increase access and awareness in fast-growing, higher income areas of their service region.

For instance, the system’s chief marketing officer was pushing to increase advertising in the rapidly expanding suburbs, and advocated building ambulatory surgery centers in a wealthy area of town with a boom of new home construction.

The chief strategy officer shared a different perspective, supporting an employer-focused strategy. His logic: “In most businesses,the CEO and the janitor have the same benefit plans. If we only focus on the wealthy parts of town, we’re missing a big portion of the workers with good insurance.” He advocated for a new round of direct-to-employer contracting outreach, hoping to steer workers to high-value primary and specialty care solutions.

In reality, any system looking to move commercial share will need to do both—but even the best playbook for building commercial volume is unlikely to close the growing cross-subsidy gap. To maintain profitability in the long term, health systems must reduce costs for managing Medicare patients by delivering lower-cost care in lower-cost settings, with lower-cost staff.

According to a Wall Street Journal report, CVS is expected to submit a bid to purchase Dallas-based Signify Health, which supports physicians, payers, and health systems with tools and technology to provide in-home care. Signify acquired accountable care organization manager Caravan Health earlier this year. Last week, the Journalreported that Signify, valued at more than $4B, was looking for buyers. While CVS is said to be interested, so are private equity firms and other managed care companies.

The Gist: CVS CEO Karen Lynch told investors during last week’s earnings call that the company plans to grow its primary care and home health offerings through mergers and acquisitions. The Signify bid, along with reports that CVS considered acquiring concierge primary care company One Medical, suggests that the retail pharmacy and insurance giant is charging ahead with its strategy of creating a vertically-integrated healthcare company.

As several newly public digital health and value-based care companies have seen share prices plummet and capital dry up in a cooling economy, they are becoming targets for large insurers and tech companies who have seen their own fortunes grow during the pandemic. Watch for more announcements from these “platform assemblers” in the months to come.

Despite the hype, accountable care organizations (ACOs) and other Medicare-driven payment reform programs intended to improve quality and lower healthcare spending haven’t bent the cost curve to the extent many had hoped.

A recent and provocative opinion piece in STAT News, from health policy researcher Kip Sullivan and two single-payer healthcare advocates, calls for pressing pause on value-based payment experimentation. The authors argue that current attempts to pay for value have ill-defined goals and hard-to-measure quality metrics that incentivize reducing care and upcoding, rather than improving outcomes.

The Gist: We agree with the authors that current value-based care experiments have been disappointing.

The intention is good, but the execution has been bogged down by entrenched industry dynamics and slow-to-move incumbents. One fair criticism: ACOs and other “total cost management” reforms largely focus on the wrong problem. They address utilization, rather than excessive price.

But we’re having a price problem in the US, not a utilization problem.Europeans, for example, have more physician visits each year than Americans, yet spend less per-person on healthcare. It’s our high prices—for everything from physician visits to hospital stays to prescription drugs—that drive high healthcare spending.

The root cause: our third-party payer structure actively discourages real efforts to lower price—every player in the value chain, including providers, brokers, and insurers, does better economically as prices increase. That’s why price control measures like reference pricing or price caps have been nonstarters among industry participants.

Recent reforms that increase price transparency, while not the entire solution, at least shine a light on the real challenges our healthcare system faces.

Citi, The American Hospital Association (AHA) and the Healthcare Financial Management Association (HFMA) recently hosted the 22nd annual Not-for-Profit Healthcare Investor Conference. The event was in person, after being virtual in 2021 and canceled in 2020 due to the pandemic. Leaders from over 25 diverse health systems, as well as private equity and fund managers, presented in panel discussions and traditional formats. The following summary attempts to synthesize key themes and particularly interesting work by leading health systems. The conference title was “Refining the Now, Reshaping What’s Next.”

Is Healthcare Headed for Best of Times or Worst of Times?

Clearly the pandemic showed how essential and adaptive the US healthcare industry is, and especially how incredible healthcare workers continue to be. It also exposed and accelerated many underlying dynamics, such as impact of disparities, clinical labor shortages and supply chain challenges. On balance, at this year’s conference presenters remained quite optimistic about the future, and felt that despite enormous pain, the pandemic has helped to accelerate positive transformation across healthcare.

At the same time, almost all presenters referenced future headwinds from labor and supply inflation, concerns about increasing payment pressures, and the continued need to address disparities and social justice. That being said, there was not much disclosure at the conference about just how bad things could get in the future given accelerated operational and financial risks.

As usual at such a conference, there was much passion, creativity, sharing and celebration. While each organization and market differ somewhat, the following are common themes discussed.

Key Themes

Enormous Workforce Challenges – Every speaker referenced workforce as being THE key issue they are facing, specifically retirement, recruitment, retention, well-being and cost. We have talked for years about a future caregiver shortage, but this reality was accelerated by the pandemic. The majority of health systems saw single-digit turnover rates grow to 20-30%, and the cost of temporary labor such as traveling nurses, decimate operating margins. The many strategies discussed at the conference went beyond simply paying more to attract and retain staff. A key question is whether organization-specific strategies will be enough, or whether we need a broader societal and industry-wide collaborative effort to dramatically increase training slots for nurses and other allied health professionals.

Pandemic Stressed Organizations and Accelerated Transformation – At the 2021 virtual Citi/AHA/HFMA conference, many posited that the country was past the worst of the pandemic. (In fact this author’s summary of last year’s conference was titled “Sunrise After the Storm”). That was before the Omicron wave hit hard in Q1 2022. First-quarter 2022 operating margins were negative for most but not all healthcare systems due to cumulative impact of Omicron, temporary labor and supply costs, especially since the governmental support that partially offset those costs in 2020 ended. Organizations and their teams remain resilient, but highly stressed. Risks and challenges associated with future waves continue, as well as high reliance on foreign drug and supply manufacturing. While highly distracting and painful, many organizations discussed how the pandemic actually accelerated the pace of transformation. Necessity drives required action, and at least temporarily overcomes political and cultural barriers to change.

Growing Pursuit of Scale, Including through M&A and Partnerships – All health systems continue to be highly complex with multiple competing “big-dot” priorities. Multiple systems described their current M&A and growth strategies, pursuit of scale, as well as how these strategies were impacted by the pandemic. While the provider community remains highly unconsolidated on a national basis, mergers are more frequent, including between non-contiguous markets. Systems said that larger size, coupled with disciplined management, can reduce cost structure and improve quality and patient experience. While some pursue scale through organic growth initiatives or M&A, others described success in creating scale by leveraging partnerships with “best-in-class” niche organizations and other outside expertise.

Health Equity, Diversity and ESG as Core to Mission – Consistent with last year, most speakers discussed their efforts to address health equity, social justice, diversity, and Social Determinants of Health. Many health systems have developed robust strategies quickly as the pandemic spotlighted the impact of existing disparities. There is increasing interest in Environment, Social and Governance (ESG) initiatives, including environmental stewardship to improve the health of their communities and the world by reducing their carbon footprint and medical waste.

Patient-Centric Care Transformation Continues as a Priority – The pandemic significantly accelerated the shift to telehealth and virtual care. Many health systems are increasing their efforts to design care around the patient instead of the traditional provider centric focus. While the need for inpatient care will always continue, more care is taking place in settings closer to or at home, with digital enablement. Expansion of personalized medicine, genetic testing and therapies, and drug discovery are transforming how healthcare is provided.

Affordability and Value-Based Care – US healthcare costs as a percentage of GDP increased from 18% in 2019 to almost 20% in 2020, mainly driven by the pandemic. There remains a dichotomy between reliance on fee-for-service payment and commitment to value-based care. Although only 11% of commercial payment is currently through two-sided risk arrangements, almost all presenting health systems discussed their strategies to continue moving to value-based care and to improve affordability. Some systems are leveraging their integrated health plans and/or expanding risk-based contracts. Many are trying to reduce unnecessary care through adoption of evidence-based models and to shift care to less costly settings.

Inflation and Accelerating Financial Pressures – Health systems are facing unprecedented increases in labor and supply costs, that are likely to continue into the foreseeable future. At the same time, commercial payment rate adjustments are “sticky low” as insurers and employers push back on rate increases. Governmental payment rate increases are less than cost inflation. In addition to current cuts like the re-implementation of sequestration, longer-term cuts to provider assessment programs, provider-based billing, disproportionate share and Medicaid expansion may severely impact many organizations over time. Benefits like 340b discounts are also experiencing pressure. Post-pandemic clinical-volume trends remain unclear, and additional governmental support associated with future pandemic waves is unlikely. Adding to these challenges, declines in stock and bond prices are negatively impacting currently strong balance sheets.

Conclusion: Best or Worst of Times in Healthcare?

Time will tell, in retrospect, if the next five years will be the best of times, worst of times, or both in healthcare. Optimists point to the resiliency of healthcare organizations; enormous opportunity to reduce unnecessary cost through adoption of evidence-based care and scale; pipeline of new cures and technology; and opportunities to address social and health equity. Pessimists point to likely unprecedented financial pressures and operational challenges due to endemic labor and supply shortages; high-cost inflation vs. constrained payment rates; and future uncertainty about the pandemic, the economy and investment markets.

The situation will undoubtedly vary by market and organization as reflected in conference presentations, but all systems will likely face substantial pressure. As one speaker noted “humans have a great ability to respond to pain,” so this may be the inflection point where more healthcare systems radically accelerate necessary change to improve health, make healthcare more equitable and affordable, with higher quality and better outcomes. Some health systems are clearly doing that, with pace, nimbleness and passion. Can the industry as a whole accomplish it successfully?

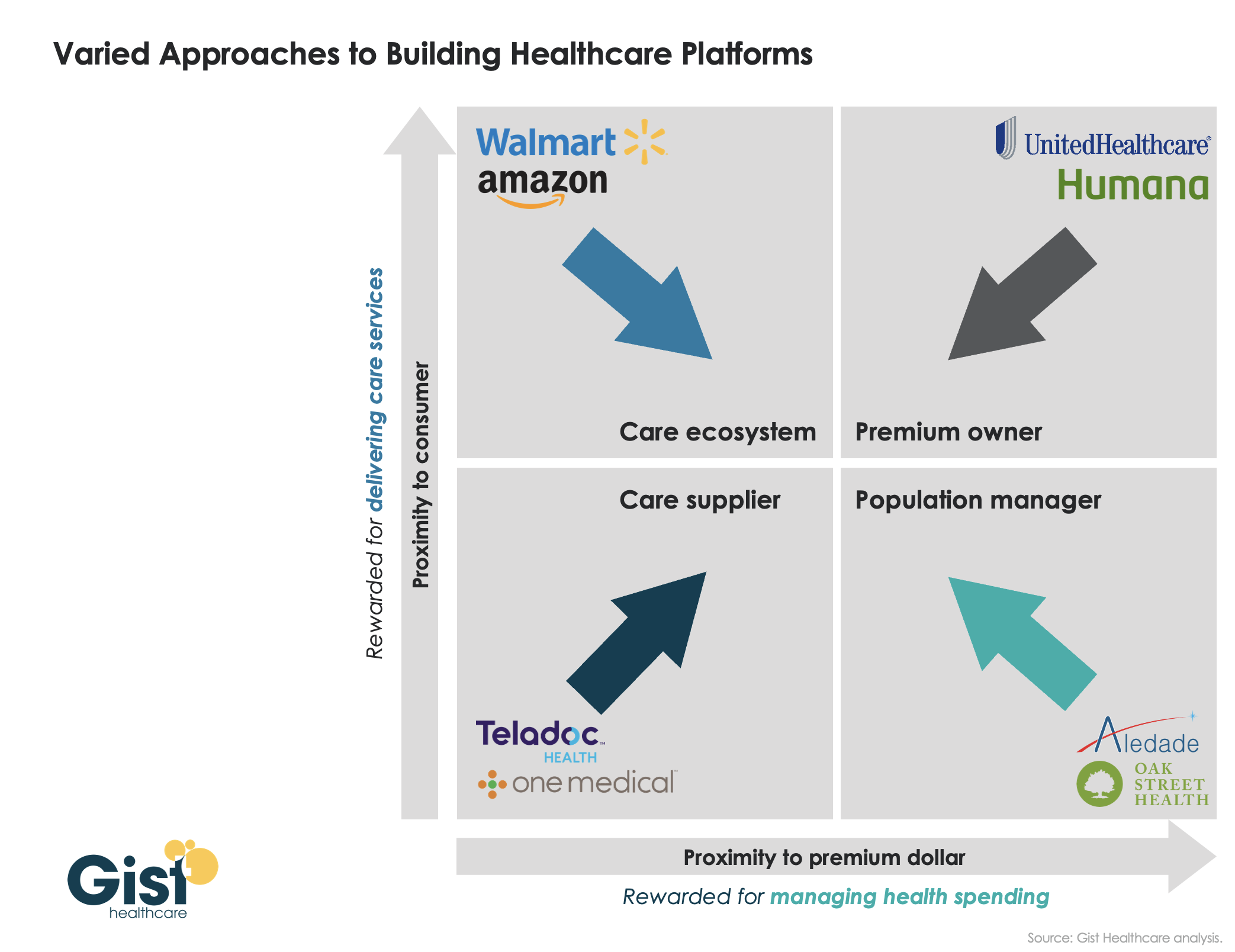

Last week, we introduced our framework for value delivery as a “healthcare platform”, in which an organization’s proximity to both the consumer and to the premium dollar determines how it competes as a “care supplier,” a “care ecosystem,” a “premium owner,” or a “population manager.” Traditionally, different healthcare companies have operated primarily in one of these four domains. However, as shown in the graphic below, we’ve recently seen many shift their business into one or more additional quadrants, as they seek to expand their value propositions. UnitedHealth Group is an obvious example: it has moved well beyond the traditional insurance business, via numerous provider and care delivery acquisitions across the continuum.

Other players have shifted from their own “pure play” positions toward more comprehensive “platform” strategies as well: One Medical adding Iora Health to enhance population health capabilities; Walmart moving beyond retail and pharmacy services, partnering with Oak Street Health to expand its ability to manage Medicare patients; Amazon getting into the employer health business.

There’s a clear pattern emerging—value propositions are converging on a “strategic high ground” that encompasses all four dimensions of platform value, creating a comprehensive set of solutions to deliver accessible care, promote health, and grow consumer loyalty, with an aligned financial model centered on managing the total cost of care. Health systems looking to build platform strategies will find many of these competitors also vying for pride of place as the “platform of choice” for healthcare consumers and purchasers.