Cartoon – When did Ignorance become a Point of View?

https://www.commonwealthfund.org/blog/2020/uncertain-future-medicare-trust-fund

The COVID-19 pandemic has increased pressures on an already-stressed public health care financing system. This is especially evident when it comes to the financial health of Medicare’s Hospital Insurance (HI) Trust Fund, which finances health care services related to hospital, skilled nursing facility, and hospice stays for Medicare beneficiaries.

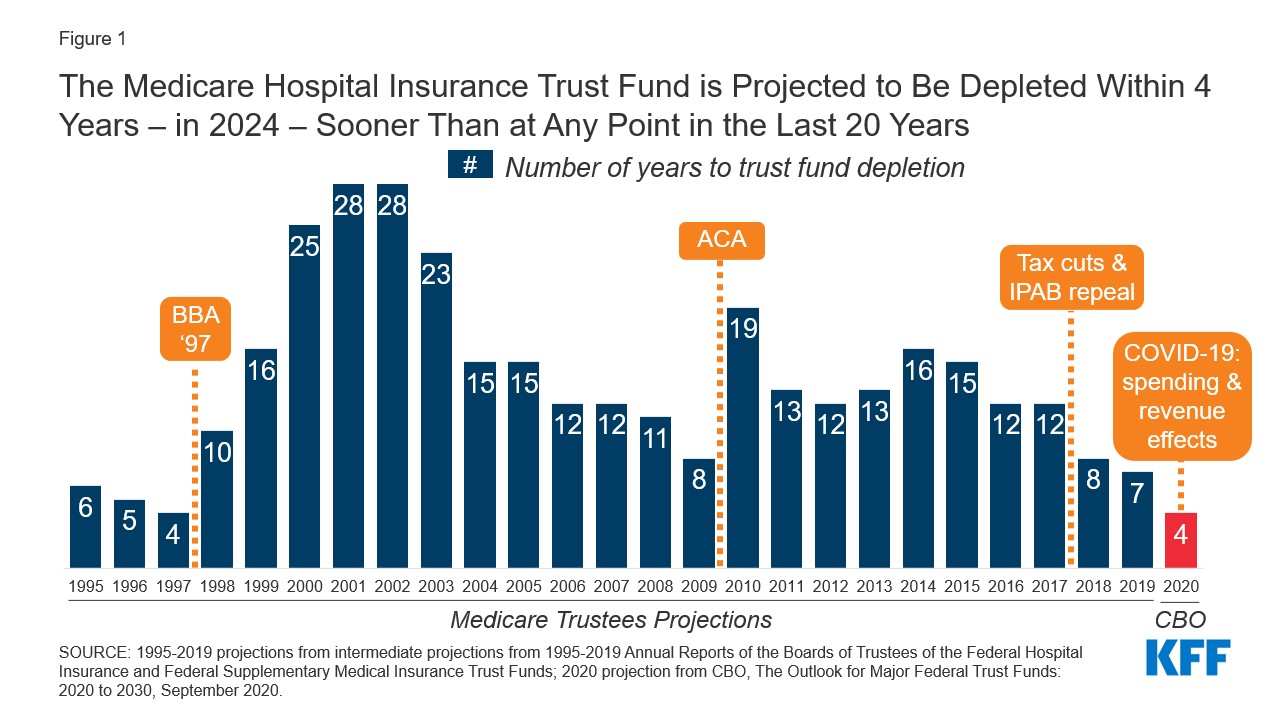

In April, using pre-COVID-19 data, the Trustees of Social Security and Medicare projected that the HI Trust Fund would become insolvent in 2026 — meaning that Medicare Part A claims submitted by providers would not be fully reimbursed. The Congressional Budget Office (CBO) made a similar projection when it issued its March 2020 baseline projections. In a September 2020 report, the CBO projected that the date of insolvency had moved up to 2024.

The pandemic has disrupted economic activity in the United States in several ways: a large and rapid rise in unemployment substantially reduced payments to the Trust Fund from payroll taxes, and hospitals experienced unprecedented financial stress from lost revenues because of a dramatic drop in admissions and procedures, along with new costs arising from the pandemic. One way that Congress provided relief to address these economic shocks was to make advance payments. Between $65 billion and $92 billion in advance payments were made to Medicare Part A providers that draw upon the HI Trust Fund. This increased claims on the Trust Fund in 2020 and lowers them for 2021 — assuming they are paid back in 2021. Together these economic dynamics create a situation that requires quick action to prevent insolvency; the margin for error is small.

The duration of the pandemic and the timing and size of an economic recovery remain highly uncertain. While unemployment has declined notably, from 14.7 percent in April to 8.4 percent in August, new spikes in COVID-19 cases across the country continue to dampen economic activity. The recent jobs report also suggested a slowing of employment recovery. Further, there is great uncertainty about the timing, availability, and effectiveness of a potential vaccine. As a result, we are quite unsure when payroll tax revenues will recover or to what degree hospital finances will recover.

The Federal Reserve Bank of St. Louis recently underscored the uncertainty when it issued the following assessment:

“The COVID-19 pandemic — like all pandemics — will come to an end. Of course, nobody knows when that will be. No one also knows whether there will be subsequent waves of the virus that trigger a nationwide resumption of strict social distancing protocols or whether a proven vaccine allows a swift return to pre-COVID norms. Thus, the trajectory of the recovery is the key unknown at this point.”

Together these forces create policy tensions. It is important to continue to support hospitals and nursing homes whose revenues have not yet recovered, and those that continue to incur unusual costs because they are still carrying heavy financial burdens stemming from COVID-19. At the same time state and federal health care financing programs are under extreme financial stress.

Recent legislation negotiated between Congress and the Trump administration would permit hospitals to request an extension for repaying advance payment loans and also reduce the interest rate. Together, these provisions recognize the continued financial stress and provide relief but also introduce new uncertainty. That is, by lengthening the repayment period and reducing the costs of carrying the loans it becomes less certain when they will be paid back in full and returned to the Trust Fund, making the solvency date of the Trust Fund less certain (as specified further in Centers for Medicare and Medicaid Services guidance). In addition, this assumes that the full amounts of the loan will be paid back.

The timing of the COVID-19 pandemic has been especially unfortunate in terms of maintaining the Medicare HI Trust Fund’s solvency. The Trustees issued a warning that action was needed when insolvency was estimated to occur in 2026; it has now been pushed up to 2024. One way to address the uncertainty would be to make a fund transfer from general revenues to the Trust Fund in the amount of the outstanding loans, thereby removing any additional uncertainty around timing of repayment. This could help mitigate risks in a world with highly uncertain economic and epidemiological forecasts but would risk further increasing federal spending during an economic downturn.

https://www.commonwealthfund.org/blog/2020/health-care-2020-presidential-election-whats-stake

As the presidential election draws near, we reflect on the meaningful differences in health policy priorities and platforms between the two candidates, which we’ve described more fully in our recent blog series.

While similarities exist in some areas — most notably prescription drug pricing and proposals to control health care costs — the most striking differences between the positions taken by President Donald Trump and those of former Vice President Joe Biden are on safeguarding access to affordable health care coverage, advancing health equity for those who have been historically disadvantaged by the current system, and managing the novel coronavirus pandemic.

The importance of maintaining or expanding access to affordable health care in the midst of a pandemic cannot be understated. Going into the crisis, 30 million Americans lacked health coverage, with many more potentially at risk as a result of the current economic downturn. And even for many with coverage, costs are a barrier to receiving care. Moreover, despite efforts by Congress and the Trump administration to ease the financial burden of COVID-19 testing and treatment, many people remain concerned about costs; examples of charges for COVID-related medical expenses are not uncommon.

In this context, President Trump’s efforts to repeal the Affordable Care Act (ACA) is the most important signal of his position on health care. The administration’s legal challenge of the law will be considered by the Supreme Court this fall. With no Trump proposal for a replacement to the ACA, if the Court strikes the law in its entirety or in part, many voters cannot be certain that their health coverage will be secure. By undermining the ACA — the vast law that protects Americans with preexisting health conditions and makes health coverage more affordable through a system of premium subsidies and cost-sharing assistance — the president has put coverage for millions at risk.

Trump issued an executive order to preserve preexisting condition protections. If the ACA remains intact, the order is redundant. But if the ACA is repealed by the Court, the order is meaningless because it lacks the legal underpinning and legislative framework to take effect.

In contrast, Vice President Biden has proposed expanding coverage through the ACA by adding a public option, enhancing subsidies to make health care more affordable, filling the gap for low-income families living in states that did not expand Medicaid, and giving people with employer health plans the option to enroll in marketplace coverage and take advantage of premium subsidies. For sure, if Biden is elected, many policy details must be ironed out; passing legislation in a deeply divided Congress is never easy. Despite these challenges, Biden proposes expanding health coverage rather than revoking it.

Just as COVID-19 has exposed gaps in health coverage and affordability, it also has highlighted the poor health outcomes stemming from racial and ethnic inequities in the U.S. health system. Communities of color — Black, Hispanic, and American Indian and Alaska Native people — have higher rates of COVID cases, hospitalizations, and deaths compared to white people. These disparities are a result of myriad factors, many of which are deeply rooted in structural racism. The candidates’ plans to address health disparities and advance health equity set them apart.

The ACA has played a critical role in reducing disparities in access to health care and narrowed the uninsured rate among Black and Hispanic people compared to white people. Medicaid expansion has been key to improving racial equity. Repealing the ACA, as President Trump has sought to do, would reverse these gains. Even beyond repealing the ACA, this administration has pursued policies intended to limit Medicaid eligibility — for example, by permitting states to impose work requirements and other restrictions that would lead to fewer people covered. These measures and others are already having an impact; coverage gains achieved through the ACA have eroded since 2016. Health care for legal immigrants also has declined as a result of policies like the recently finalized “public charge” rule, which seems also to have caused an increase in uninsurance among children. The administration has further revoked ACA antidiscrimination and civil rights protections for LGBTQ people.

In addition to restoring and expanding coverage under the ACA, Vice President Biden has pledged to address health disparities and reinstate antidiscrimination protections. He has a proposal to advance racial equity not just in health care but across the economy. If successful, his plan could address underlying factors contributing to higher rates of COVID-19 cases and deaths among people of color, as well as their higher rates of heart disease, diabetes, and other health conditions tied to social determinants of health.

Finally, the candidates differ deeply in their approaches to the coronavirus pandemic. President Trump has failed to orchestrate a national strategy for combating coronavirus and has routinely undermined accepted public health advice with respect to mask-wearing and social distancing. He has delegated to the states responsibility for controlling the pandemic when it is clear that the virus travels freely across the country, regardless of state borders. Lax states can negate the efforts of those states sacrificing to bring the pandemic under control. Vice President Biden has strongly signaled, though his personal conduct and rhetoric, that he intends more aggressive federal leadership in fighting the virus.

In a recent Commonwealth Fund survey of likely voters, control of the pandemic and covering preexisting conditions were very important factors in choosing a president. In seven battleground states, protections for preexisting conditions outweighed COVID-19 and health costs as the leading health care issue voters are considering. In all 10 battleground states included in the survey, Vice President Biden was viewed as the more likely candidate to address these critical health care issues.

Perhaps since the Civil War, the United States has never faced starker choices in a presidential election. In health and other areas, there are profound differences in the positions of President Trump and former Vice President Biden. Voting this November is literally a matter of life and death for the American people.

Overall approach: Repeal the ACA and replace it with market-driven coverage options aimed at lowering premiums and increasing choice of plans tailored to individual preferences; give states more flexibility in designing coverage options; require more accountability for people with low incomes enrolled in public programs; protect preexisting conditions.

Medicaid: Repeal the ACA Medicaid expansion for adults; provide block grants to states to design their own programs; increase accountability through work requirements.

Individual market and marketplaces: Has promoted weaker regulations on plans that don’t comply with the ACA’s preexisting condition protections and other requirements; elimination of advertising and enrollment assistance during open enrollment; elimination of payments to insurers to offer lower-deductible plans.

Employer coverage: Has promoted weaker regulations on association health plans that don’t comply with the ACA and allowed employers to fund accounts for employees to buy health plans on their own, including products that don’t comply with the ACA.

Overall approach: Protect insurance for people with preexisting conditions by supporting and building on the ACA; expand insurance coverage and reduce consumers’ health care costs by enhancing the ACA’s marketplace subsidies, covering people currently eligible for Medicaid in nonexpansion states, and giving more people in employer plans the option to enroll in marketplace plans with subsidies.

Medicaid: Expand enrollment by allowing eligible people in 12 states without Medicaid expansion to enroll in a public plan through the marketplaces with no premiums; make enrollment easier with autoenrollment.

Individual market and marketplaces: Expand enrollment through enhanced subsidies, greater advertising and enrollment assistance: no one pays more than 8.5 percent of income on marketplace coverage; change the benchmark plan from silver to gold to reduce deductibles and cost-sharing.

Employer coverage: Allows anyone with employer coverage to enroll in a public plan through the marketplaces and be eligible for subsidies.

Medicare: Would allow people ages 60 to 65 to enroll in a Medicare-like heath plan.

Trump: The number of people without health insurance has increased under the president’s watch in part because of policies that have eliminated the promotion and advertising of marketplace open-enrollment periods, enrollment restrictions in Medicaid, and immigration policies that have had a chilling effect on enrollment of legal immigrants and their children. Trump supports a lawsuit now before the Supreme Court that argues for repeal of the ACA, which would eliminate coverage for as many as 20 million people. Says he will come up with a replacement but has yet to do so.

Biden: Has introduced proposals to build on the ACA by covering people in the 12 states that haven’t expanded Medicaid and enhance subsidies for marketplace plans. This would provide new options for people who are currently uninsured and increase coverage over time.

Trump: The ACA currently provides this protection. Trump supports the lawsuit before the Supreme Court that argues for repeal of the ACA and its preexisting conditions provision. Trump issued an executive order that said preexisting conditions are protected, but without the ACA or new legislation the order has no effect and is purely symbolic.

Biden: The vice president pledges to support and build on the ACA, retaining its preexisting condition protections.

Trump: The president eliminated payments to insurers to reimburse them for offering lower-deductible plans in the ACA marketplaces to people with lower incomes, as required by the law. This had the effect of increasing premiums for people not eligible for subsidies. He has promoted the sale of non-ACA-compliant health plans, like short-term plans. These plans have lower premiums for healthy people but screen for preexisting conditions and often provide little cost protection if someone becomes sick. He has loosened regulations for association health plans, although that was turned back under legal challenge. The repeal of the ACA would mean the loss of marketplace subsidies and preexisting-condition protections, making coverage unavailable or unaffordable for people with low and moderate incomes and those with health problems.

Biden: The vice president’s proposal to enhance marketplace subsidies will cap the amount of premiums people pay at 8.5 percent of income, including people in employer plans who would have the option to enroll in the marketplaces. By linking subsidies to gold plans, deductibles would also fall for those who choose those plans.

Trump: Uninsured rates among Hispanic people have risen under the president’s watch. Repealing the ACA would further eliminate coverage gains made by Hispanics, as well as Black people and Asian Americans, widening racial disparities in coverage and access.

Biden: The vice president’s proposals to expand coverage under the ACA will particularly benefit people of color. This is because people living in the 12 states that have not yet expanded Medicaid are disproportionately Black and Hispanic.

https://www.commonwealthfund.org/blog/2020/introducing-health-care-2020-presidential-election-series

Before each presidential election, the Commonwealth Fund analyzes the major health policy positions of the Democratic and Republican candidates to assist Americans in making informed choices. In 2020, with health care rising to the top of the electorate’s concerns for myriad reasons, this information has never been more important.

In the next week, we will be publishing a series of analyses that compare the positions of President Donald Trump and his challenger, former Vice President Joe Biden, on topics like:

prescription drug policy;

the affordability and availability of health care and insurance, including the issue of preexisting conditions;

questions concerning older adults, like Medicare; how best to control the costs of health care;

addressing mental and behavioral health concerns;

and strategies for advancing health care equity.

In most previous presidential election years, we have had the opportunity to compare fairly well-delineated party and candidate programs. In 2020, President Trump and the Republican party have chosen not to issue any party platform or formal policy positions. Therefore, we have derived our description of President Trump’s program from the policies he espoused, and decisions made during his first term. Vice President Biden’s information comes from his campaign platform.

We hope you find these summaries helpful as you weigh your choices for Election Day.

One of Medicare’s trust funds is expected to run out of money in the next few years, but we’ve heard almost nothing about it on the campaign trail. We explain what would happen, how things got so bad, and what can be done to fix it.

Listen to the full episode below, read the transcript or scroll down for more information.

Click here for more of our 2020 election coverage.https://embed.acast.com/tradeoffs/themedicarecliff/?brandColor=e65a4b

Medicare is a federal health insurance program that covers Americans 65 years or older as well as some Americans with certain disabilities. The federal government spends $800 billion a year — 15% of the overall federal budget — on care for the roughly 60 million Medicare beneficiaries.

Medicare is split into four parts:

Covers inpatient hospital visits, as well as hospice, post-acute care and graduate medical education.

Covers physician and outpatient services.

Also known as Medicare Advantage. Allows beneficiaries to get Part A and B benefits through a private insurer.

Covers prescription drugs.

Medicare Part A comes out of the Hospital Insurance (HI) trust fund, which is primarily funded by a 2.9% payroll tax split evenly between employers and employees.

Parts B and D are funded by the Supplementary Medical Insurance (SMI) trust fund, which is primarily funded by general tax revenues and beneficiary premiums.

Medicare Advantage (or Part C) is supported by set per enrollee payments from the HI and SMI trust funds, as well as additional enrollee premiums in some cases.

For many years, the payroll taxes coming into Medicare Part A exceeded the benefits the program needed to pay out. This has allowed Medicare Part A to build up a reserve in the HI trust fund.

Over time, two main factors have often pushed Part A’s annual benefits payments higher than its tax revenue, forcing Medicare to dip into its reserves:

In April, the Medicare Board of Trustees reported that the Part A trust fund had around $200 billion in reserves and that, barring any changes, it would run out in 2026.

But with significant job losses during the pandemic, far lower levels of payroll taxes are expected to be collected, leading the Congressional Budget Office and the Committee for a Responsible Federal Budget to now estimate the HI trust fund will run out — or become insolvent — in 2024.

If Congress is unable to make any changes before the trust fund runs out, Medicare would effectively be operating paycheck-to-paycheck — only able to use current payroll taxes to pay out claims. The Congressional Budget Office estimates that would only cover about 85% of Part A’s bills, leaving providers likely to receive late and incomplete payments, which could lead them to accept fewer Medicare patients or stop taking them altogether.

Congress has never let Medicare Part A run completely dry. When it has gotten close to exhaustion — most recently in 1997 and 2009 — lawmakers used a combination of three tactics to extend the life of the trust fund.

Congress can lower how much it pays hospitals and other providers for different services. It did this as part of the Balanced Budget Act of 1997 and the Affordable Care Act in 2010. One area that has been mentioned this time around as a potential place to cut are payments to post-acute care facilities.

Congress can increase the amount of money coming into the trust fund. It did this as part of the ACA by adding a 0.9% payroll tax surcharge to people earning more than $200,000 a year.

Congress can also ease the burden on the trust fund by deciding to pay for certain benefits from somewhere other than the HI trust fund. For example, in 1997, Congress moved some home health payments into Medicare Part B, which is funded by general tax revenues and premiums.

While leaders from both parties have suggested similar policies to address Medicare’s financial troubles, any spending cuts or tax increases are likely to be politically difficult and generate opposition. Any fix will also take time to implement, meaning that the next president and Congress will have to act quickly to avoid more abrupt and painful remedies.

Coronavirus hospitalizations are increasing in 39 states, and are at or near their all-time peak in 16.

The big picture: No state is anywhere near the worst-case situation of not having enough capacity to handle its COVID-19 outbreak. But rising hospitalization rates are a sign that things are getting worse, at a dangerous time, and a reminder that this virus can do serious harm.

By the numbers: 39 states saw an increase over the past two weeks in the percentage of available hospital beds occupied by coronavirus patients.

Yes, but: The all-time peak of coronavirus hospitalizations happened in the spring, when 40% of New Jersey’s beds were occupied by COVID patients. Thankfully, even the the worst-performing states today are still a far cry from that.

Between the lines: These numbers, combined with the nationwide surge in new infections, confirm that the pandemic in the U.S. is getting worse — just as cold weather begins to set in in some parts of the country, which experts have long seen as a potentially dangerous inflection point.

As a new wave of coronavirus cases hits the U.S. and Europe, governments are shifting away from total shutdowns toward more geographically targeted lockdowns to stifle the virus’ spread.

Why it matters: Precision shutdowns can slow emerging outbreaks while lessening the overall economic impact of the response. But they risk a backlash from those who are targeted, and may not be strong enough to keep a highly contagious virus under control.

Driving the news: New York City tried to control a flare-up of new coronavirus cases this month by instituting partial shutdowns on a neighborhood-by-neighborhood basis, curtailing economic and social activity in areas harder hit by the virus while continuing reopening elsewhere.

What’s new: Some early research indicates more-targeted lockdowns can effectively smother outbreaks while leaving broader city and regional economies mostly intact.

Yes, but: Individuals move around a city, and some epidemiologists worry that over time cases will break out of targeted lockdown areas and spark a wider outbreak.

What to watch: A targeted lockdown is inevitably going to appear to single out specific groups of people, which risks creating a backlash that can undermine public support for long-term control measures.

The bottom line: Targeted lockdowns can throttle the virus while minimizing economic damage, at least in the short term. But one thing we’ve learned is that if COVID-19 gets out of control in one place, it may be only a matter of time before it ends up everywhere else.