In mid-January, General Catalyst (GC) and Summa Health announced the signing of a non-binding LOI for GC to acquire Summa, which, if consummated, would be a groundbreaking transaction. Summa Health is a vertically integrated not-for-profit health system located in Akron, Ohio that operates acute care hospitals, a network of health care services, a physician group practice, and a health plan. Like much of the health system sector, Summa has found the operating environment for the past couple of years to be challenging.

GC is a venture capital firm that had approximately $25B in assets under management at the end of 2022, across a dozen fund families and a number of sectors, including its Health Assurance funds, that have a stated mission of “creating a more proactive, affordable & equitable system of care.”

Health Assurance has investments in more than 150 digital health companies worldwide and has implemented working relationships with more than a dozen of the country’s most noteworthy health systems and hospital operators.

In October, GC announced the formation of a new venture called the Health Assurance Transformation Corporation (HATCo), for the purpose of providing financial and operational advisory assistance to health systems, including using GC’s suite of digital health companies. At that time, HATCo announced plans to buy a health system in order to drive transformation in the delivery of care by leveraging technology, updating workforce/staffing models, and becoming more proactive in creating revenue streams for health systems.

Their plans included an intent to streamline operations and find efficiencies using technology, as well as implementing value-based payment models, including fully capitated risk contracts to incentivize better utilization management, an initiative that requires significant data analytics.

GC had been looking for a system with market relevance and a sweet spot in terms of size – big enough to have a full complement of services, but nimble enough to accept significant change. In Summa, it has also found a system that maintains its own health plan, which GC can use to help accelerate the shift to capitated models.

The transaction that Summa and GC are contemplating is a new and innovative attempt at addressing the underlying problems that plague the acute care industry.

In particular, 1) a continued reliance on fee-for-service revenue when reimbursement has been pressured from every angle and rate increases have failed to keep pace with the rising cost of providing care, 2) capital to fund a growing list of competing needs, and 3) the challenges of staffing for quality in a tight market for clinical labor. Summa appears to be banking on the idea that GC and the data- and technology driven solutions that reside within their portfolio companies can ease those pressures.

HATCo’s proposed purchase of Summa requires a conversion of the health system to for profit. The purchase price of the health system will contribute to the corpus for a large foundation that will address social determinants of health in the Akron community, and the operating entities would become subsidiaries of HATCo.

HATCo has stated publicly that it will continue Summa’s existing charity care commitment, that Summa’s existing management team will stay in place, and the health system Board will continue to have local community representation. HATCo has also emphasized that it plans to hold Summa for an extended period and have it serve as a digital innovation testing ground and incubation site for new healthcare IT, where it believes that aligning incentives will drive financial improvement and better care.

Innovative approaches to meaningful problems should be applauded but there is skepticism.

Will bottom line pressures affect the quality of care?

Will the typical investment horizon of venture capital align with the time frames needed to prove these solutions are taking hold?

Health system evolution has traditionally been measured in decades, rather than the 5-7 year hold periods that private capital prefers. There are also perceived conflicts to consider as Summa will be paying the GC-owned companies for their services. Acute care hospitals are central elements of their communities and their constituents are broader than most companies, often including large workforces, union leadership, politicians, government regulators, and of course patients and their families.

This transaction will receive significant scrutiny with any number of constituents taking issue with a health system’s purchase by a venture capital firm. One hurdle is the conversion process itself, which requires review and approval by the Ohio Attorney General and regulators may want to impose restrictions on GCs ability to operate that are incompatible with its plans. The hurdles to closing are daunting, but the challenges facing health systems are equally daunting.

And while this proposed combination may not come to fruition, the need for innovative solutions remains.

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.

“What if 10 percent, or even five percent, of the employers in our market decide to stop providing health benefits?” a Chief Strategy Officer (CSO) at a midsized health system in the Southeast recently asked.

“Their health insurance costs have been growing like crazy for 20 years. Some of these companies could easily decide to just give their employees some amount of tax-advantaged dollars and let them do their own thing.” An emerging option for employers is the relatively new individual coverage Health Reimbursement Arrangement (ICHRA), which allows employers to give tax-deductible contributions to employees to use for healthcare, including purchasing health insurance on an exchange.

According to the CSO, “What happens is this: We’ll go from getting 250 percent of Medicare for beneficiaries in a commercial group plan to getting 125 percent for beneficiaries in a market plan. I don’t know any provider with the margins to withstand that kind of shift without significant pain—certainly not us.”

The conversation shifted to a discussion about treating employers like true customers that pay generously for healthcare services, which involves increasing engagement with them and better understanding their specific problems with their employees’ healthcare. What complaints are they hearing about their employee’s difficulties with things like making timely appointments or finding after-hours care?

Provider organizations can help keep employers in the health insurance market by regularly checking in with them about their healthcare challenges, meaningfully focusing on mitigating their pain points, and exploring new kinds of mutually beneficial partnerships.

They should also carefully monitor the employer market in their region and create financial assessments of the potential impact of employers shifting employees to health insurance stipend arrangements.

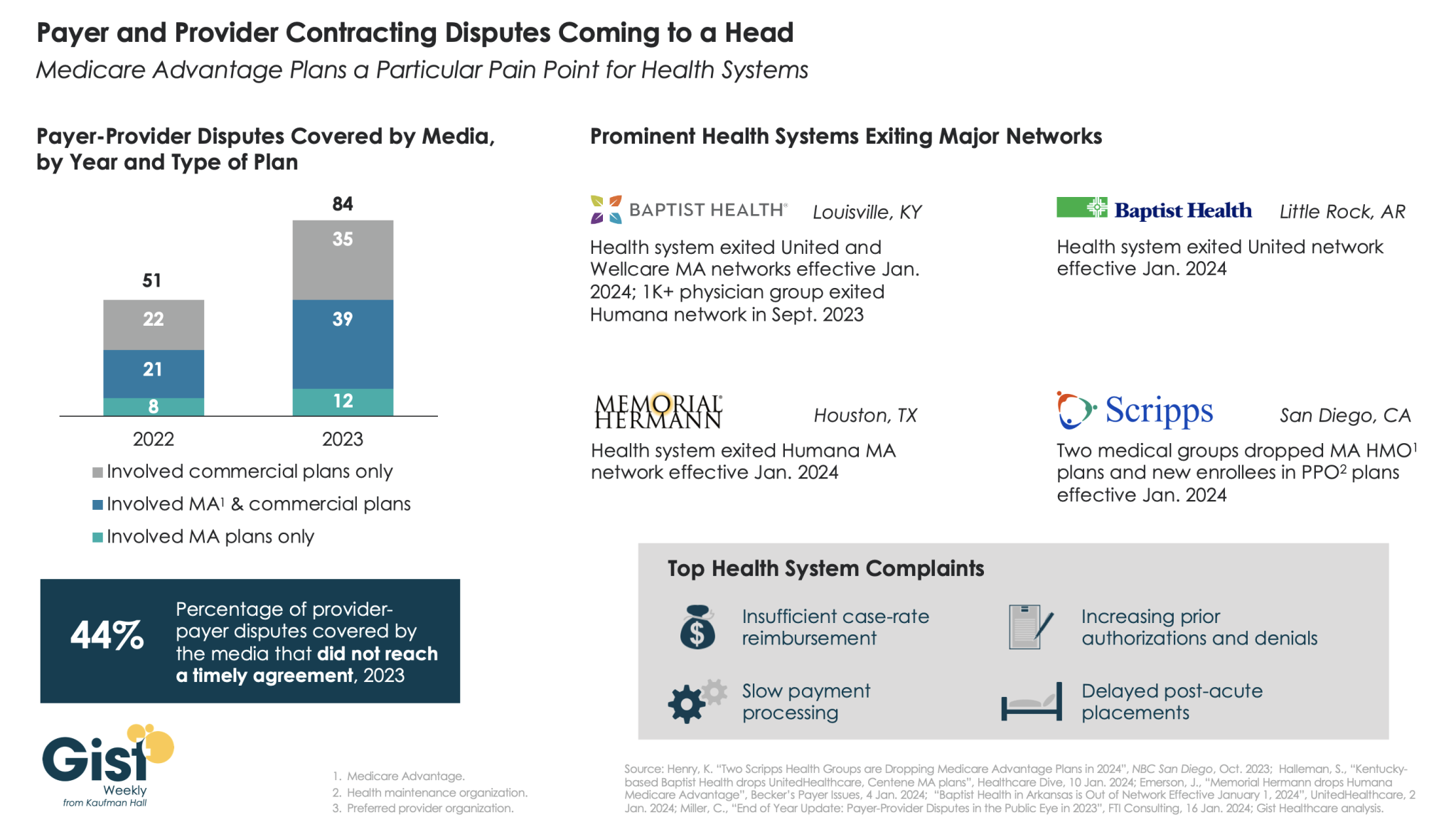

In this week’s graphic, we highlight new data on the increase in payer-provider contracting disputes covered by the media.

From 2022 to 2023, there was a 69 percent increase in the number of payer-provider contracting disputes that received media coverage. Nearly half of last year’s disputes did not reach agreement and resulted in network exits.

Large provider organizations—including Louisville, KY-based Baptist Health, Little Rock, AR-based Baptist Health, Houston, TX-based Memorial Hermann Health System, and two large medical groups affiliated with San Diego-based Scripps Health—dropped Medicare Advantage (MA) plans from at least one major payer, like United or Humana, as of Jan. 1, 2024.

Some dropped the payer’s commercial plans as well. Provider organizations leaving these networks have cited insufficient reimbursement rates and unsatisfactory business practices that drive up their cost of care delivery, especially around increased prior authorization requirements.

While contracting disputes will ultimately be influenced by the competitive strength of a given provider and payer in a particular market, it’s important for both sides to recognize thatthe patients in the middle of these disputes can be the ones most harmed when they can no longer see their trusted physicians.

On Monday, Fitch Ratings, the New York City-based credit rating agency, released a report predicting that the US not-for-profit hospital sector will see average operating margins reset in the one-to-two percent range, rather than returning to historical levels of above three percent.

Following disruptions from the pandemic that saw utilization drop and operating costs rise, hospitals have seen a slower-than-expected recovery.

But, according to Fitch, these rebased margins are unlikely to lead to widespread credit downgrades as most hospitals still carry robust balance sheets and have curtailed capital spending in response.

The Gist:As labor costs stabilize and volumes return, the median hospital has been able to maintain a positive operating margin for the past ten months.

But nonprofit hospitals are in a transitory period, one with both continued challenges—including labor costs that rebased at a higher rate and ongoing capital restraints—and opportunities—including the increase in outpatient demand, which has driven hospital outpatient revenue up over 40 percent from 2020 levels.

While the future margin outlook for individual hospitals will depend on factors that vary greatly across markets, organizations that thrive in this new era will be the ones willing to pivot, take risks, and invest heavily in outpatient services.

On Wednesday, Bloomfield, CT-based Cigna announced a definitive agreement with Chicago, IL-based Health Care Service Corporation (HCSC), a large Blue Cross Blue Shield insurer, to sell its 600K-member MA business, as well as its Medicare prescription drug plan and Medigap offerings, for $3.3B.

The two insurers also agreed to a four-year services agreement where Cigna’s Evernorth Health Services subsidiary, which includes Express Scripts, will continue to provide pharmacy benefit services to the Medicare businesses.

While Cigna is exiting the MA market, other major payers—including UnitedHealth and Humana—are seeing their MA profits drop amid an increase in utilization, according to analysis from Moody’s Investors Service.

The Gist:While it initially appeared that Cigna’s divesture of its MA business would position it to combine more smoothly with Humana, this deal with HCSC makes sense even in the wake of that reportedly called off merger.

Cigna has been a bit player in MA for years, covering only two percent of MA lives in 2023, and the shrinking pie of MA profits will discourage all but the most successful or uniquely positioned payers.

But while increasing utilization rates are contributing to a declining outlook for payers, MA is still a solidly profitable business, covering over half of Medicare beneficiaries and still growing by millions of lives each year.

The MA payers that last are going to have to work harder at integrating their various care and data assets, and more carefully manage spend for an aging cohort of seniors with increasingly complex needs.

Baptist Health said reimbursements for the medications were determined by a payment model that was later invalidated, and the insurer continues to benefit from a “windfall” of underpayments due to the health system, according to the lawsuit.

The suit comes months after the CMS finalized a rule that aimed to fix years of illegal payment cuts in the 340B program. Hospitals had previously argued the solution didn’t consider how MA insurers would benefit financially from the remedy.

Dive Insight:

The 340B program requires pharmaceutical companies to give discounts — which can range from 25% to 50% of the medication’s cost — to providers who serve low-income communities.

The program aims to help safety-net providers better serve vulnerable groups, and it has grown significantly since 340B was created in 1992.

But in 2018, the CMS cut Medicare payments for certain drugs acquired under the 340B program, setting off a legal challenge that hospitals eventually won in front of the Supreme Court four years later.

To fix the underpayments, regulators decided to pay each hospital in 340B a lump sum that would total $9 billion overall. But the fix needed to be budget neutral, so the CMS would cut payments to all hospitals for non-drug items and services over 16 years.

In comments on the proposal, the American Hospital Association argued there was a “significant problem” with the plan, noting many MA insurers pay hospitals according to traditional Medicare rates.

Payers would benefit from reducing the non-drug payments to hospitals, and wouldn’t be required to repay 340B providers for the lower payments between 2018 and 2022, commenters argued on the rule, which was finalized in November.

In response, regulators said they appreciated the concerns, but that they were outside the scope of the rule and “CMS cannot interfere in the payment rates that MAOs [Medicare Advantage organizations] set in contracts with providers and facilities.”

In the Baptist lawsuit, the health system reported it contacted Humana multiple times about retroactive adjustments and remedy payments, but the insurer’s counsel disputed any obligation to make those payments.

“Humana’s refusal to act has worked a substantial windfall to Humana as it continues to hold funds provided by CMS for Humana’s Medicare Advantage plans without reimbursing Baptist Health for the amounts owed to it under the Agreement,” the system said in the lawsuit.

Humana said it does not comment on ongoing litigation.

The physician-led healthcare network formed to save hospitals from financial distress. Now, hospitals in its own portfolio need bailing out after years of alleged mismanagement.

Steward Health Care formed over a decade ago when a private equity firm and a CEO looking to disrupt a regional healthcare environment teamed up to save six Boston-based hospitals from the brink of financial collapse. Since that time, Steward has expanded from a handful of facilities to become the largest physician-led for-profit healthcare network in the country, operating 33 community hospitals in eight states, according to its own corporate site.

However, Steward has also found itself once again on the precipice of failure.

Steward’s ongoing issues in Massachusetts have played out in regional media outlets in recent weeks. Massachusetts Gov. Maura Healey warned there would be no bailout for Steward in an interview on WBUR’s Radio Boston.

The Massachusetts Department of Public Health said it is investigating concerns raised about Steward facilities and began conducting daily site inspections at some Steward sites to ensure patient safety beginning Jan. 31.

However, the tide may have begun to change. Steward executives said on Feb. 2 they had secured a deal to stabilize operations and keep Massachusetts hospitals open — for now. Steward will receive bridge financing under the deal and consider transferring ownership of one or more hospitals to other companies, a Steward spokesperson confirmed to Healthcare Dive on Feb. 7.

While politicians welcomed the news, some say Steward’s long term outlook in the state is uncertain. Other politicians sought answers for how a prominent system could seemingly implode overnight.

“I am cautiously optimistic at this point that [Steward] will be able to remain open, because it’s really critical they do,” said Brockton City Councilor Phil Griffin. “But they owe a lot of people a lot of money, so we’ll see.”

However, the business model wasn’t immediately a financial success. Steward didn’t turn a profit between 2011 and 2014, according to a 2015 monitoring report from the Massachusetts attorney general. Instead, Steward’s debt increased from $326 million in 2011 to $413 million at the end of the 2014 fiscal year, while total liabilities ballooned to $1.4 billion in the same period as Steward engaged in real estate sale and leaseback plays.

Under the 2010 deal, Steward agreed to assume Caritas’ debt and carry out $400 million in capital expenditures over four years to upgrade the hospitals’ infrastructure. However, that capital expenditure could come in part from financial engineering, such as monetizing Steward’s own assets, according to Zirui Song, associate professor of health care policy and medicine at the Harvard Medical School who has studied private equity’s impact on healthcare since 2019.

Cerberus did not contribute equity into Steward after making its initial investment of $245.9 million, according to the December 2015 monitoring report. Meanwhile, according to reporting at the time, de la Torre wanted to expand Steward. Steward was on its own to raise funds.

Such deals are typically short-sighted, Song explained. When hospitals sell their property, they voluntarily forfeit their most valuable assets and tend to be saddled with high rent payments.

Healthcare Dive spoke with four workers across Steward’s portfolio who said Steward’s emphasis on the bottom line negatively impacted the company’s operations for years.

Terra Ciurro worked in the emergency department at Steward Health Care-owned Odessa Regional Medical Center in January 2022 as a travel nurse. She recalled researching Steward and being attracted to the fact the company was physician owned.

“I remember thinking, ‘That’s all I need to know. Surely, doctors will have their heart in the right place,’” Ciurro said. “But yeah — that’s not the experience I had at all.”

The emergency department was “shabby, rundown and ill-equipped,” and management didn’t fix broken equipment that could have been hazardous, she said. Nine weeks into her 13-week contract and three hours before Ciurro was scheduled to work, Ciurro said her staffing agency called to cut her contract unceremoniously short. Steward hadn’t paid its bills in six months, and the agency was pulling its nurses, she said she was told.

In Massachusetts, Katie Murphy, president of the Massachusetts Nurses Association, which represents more than 3,000 registered nurses and healthcare professionals who work in eight Steward hospitals, said there were “signals” that Steward facilities had been on the brink of collapse for “well over a year.”

Steward hospitals are often “significantly” short staffed and lack supplies from the basics, like dressings, to advanced operating room equipment, said Murphy. While most hospitals in the region got a handle on staffing and supply shortages in the aftermath of the COVID pandemic, at Steward hospitals shortages “continued to accelerate,” Murphy said.

A review of Steward’s finances by BDO USA, a tax and advisory firm contracted last summer by the health system itself to demonstrate it was solvent enough to construct a new hospital in Massachusetts, showed Steward had a liquidity problem. The health system had few reserves on hand last year to pay down its debts owed to vendors, possibly contributing to the shortages. The operator carried only 10.2 days of cash on hand in 2023. In comparison, most healthy nonprofit hospital systems carried 150 days of cash on hand or more in 2022, according to KFF.

One former finance employee, who worked for Steward beginning around 2018, said that the books were routinely left unbalanced during her tenure. Each month, she made a list of outstanding bills to determine who must be paid and who “we can get away with holding off” and paying later.

Food, pharmaceuticals and staff were always paid, while all other vendors were placed on an “escalation list,” she said. Her team prioritized paying vendors that had placed Steward on a credit hold.

The worker permanently soured on Steward when she said operating room staff had to “make do” without a piece of a crash cart — which is used in the event of a heart attack, stroke or trauma.

She stopped referring friends to Steward facilities, telling them “Don’t go — if you can go anywhere else, don’t go [to Steward], because there’s no telling if they’ll have the supplies needed to treat you.”

Away from regulatory review

Massachusetts officials maintain that it hasn’t been easy to see what was happening inside Steward.

Steward is legally required to submit financial data to the MA Center for Health Information and Analysis (CHIA) and to the Massachusetts Registration of Provider Organizations Program (MA-RPO Program), according to a spokesperson from the Health Policy Commission, which analyzes the reported data. Under the latter requirement, Steward is supposed to provide “a comprehensive financial statement, including information on parent entities and corporate affiliates as applicable.”

However, Steward fought the requirements. During Stuart Altman’s tenure as the chair of the Commission from 2012 to 2022, Altman told Healthcare Dive that the for-profit never submitted documents, despite CHIA levying fines against Steward for non-compliance. Steward even sued CHIA and HPC for relief against the reporting obligations.

Steward is currently appealing a superior court decision and order from June 2023 that required it to comply with the financial reporting requirements and produce audited financial reports that cover the full health system, Mickey O’Neill, communications director for the HPC told Healthcare Dive. As of Feb. 6, Steward’s non-compliance remained ongoing, O’Neill said.

Without direct insight into Steward’s finances, the state was operating at a disadvantage, said John McDonough, professor of the practice of public health at The Harvard T.H. Chan School of Public Health. He added that some regulators saw a crisis coming generally, “but the timing was hard to predict.”

Altman gives his team even more of a pass for not spotting the Steward problem.

“There was no indication while I was there that Steward was in deep trouble,” Altman said. Although Steward was the only hospital system that failed to report financial data to the HPC, that alone had not raised red flags for him. “[CEO] Ralph [de la Torre] was just a very contrarian guy. He didn’t do a lot of things.”

Song and his co-author, Sneha Kannan, a clinical research fellow at Harvard Medical School, are hopeful that in the future, regulatory agencies can make better use of the data they collect annually to track changes in healthcare performance over time. They can potentially identify problem operators before they become crises.

“State legislators, even national legislators, are not in the habit of comparing hospitals’ performances on [quality] measures to themselves over time — they compare to hospitals’ regional partners,” Kannan said. “Legislators, Medicare, [and] CMS has access to that information.”

However, although there’s interest from regulators in scrutinizing healthcare quality more closely — particularly when private equity gets involved — a streamlined approach to analyzing such data is still a “ways off,” according to the pair. For now, all parties interviewed for this piece agreed that the best way to avoid being caught off guard by a failing system was to know how such implosions could occur.

“If there’s a lesson from [Steward],” McDonough ventured, “it is that the entire state health system and state government need to be much more wary of all for-profits.”

Jayne Kleinman is bombarded with Medicare Advantage promotions every open enrollment period — even though she has no interest in leaving traditional Medicare, which allows seniors to choose their doctors and get the care they want without interference from multi-billion-dollar insurance companies.

“My biggest problem with being barraged is that so many of the ads were inaccurate,” Kleinman, a retired social services professional in New Haven County, Connecticut, told HEALTH CARE un-covered.

“They neglect to say that the amount of coverage you get is limited. They don’t talk about what you are losing by leaving traditional Medicare. It feels like insurance companies are manipulating us to get Medicare Advantage plans sold so that they can control the system, as opposed to treating us like human beings.”

Seniors face a torrent of Medicare Advantage advertising: an analysis by KFF found 9,500 daily TV ads during open enrollment in 2022. A recent survey by the Commonwealth Fund found that 30% of seniors received seven or more phone calls weekly from Medicare Advantage marketers during the most recent open enrollment (Oct. 15 to Dec. 7) for 2024 coverage.

In 2023, a critical milestone was passed: over half of seniors are now enrolled in privatized Medicare Advantage plans. The marketing for these plans nearly always fails to mention how hard it is to return to traditional Medicare once you are in Medicare Advantage, and that the MA plans have closed provider networks and require prior authorization for medical procedures. Instead, the marketing emphasizes the fringe benefits offered by Medicare Advantage plans like gym memberships.

U.S. Sen. Ron Wyden (D-Ore.), chairman of the Senate Finance Committee, criticized the widespread and predatory marketing of Medicare Advantage in a report in November 2022 and has continued to pressure the Biden administration to do more to address the problem.

The report said that consumer complaints about Medicare Advantage marketing more than doubled from 2020 to 2021 to 41,000. It cites cases such as that of an Oregon man whose switch to Medicare Advantage meant he could no longer afford his prescription drugs, as well as a 94-year-old woman with dementia in a rural area who bought a Medicare Advantage plan that required her to obtain care miles further from her residence than she had to travel before.

When open enrollment began last fall, it was “the start of a marketing barrage as marketing middlemen look to collect seniors’ information in order to bombard them with direct mail, emails, and phone calls to get them to enroll,” Wyden stated in a letter to the Centers for Medicare and Medicaid Services (CMS), which was signed by the other Democrats on the Senate Finance Committee.

Just three weeks after Wyden sent the letter, CMS released a proposed rule reforming Medicare Advantage practices that the main lobby group for Medicare Advantage plans, the Better Medicare Alliance, endorsed.

But key recommendations by Wyden were missing, including a ban on list acquisition by Medicare Advantage third-party marketing organizations, which includes brokers, and banning brokers that call beneficiaries multiple times a day for days in a row.

Among the prominent third-party marketing organizations is TogetherHealth, a subsidiary of Benefytt Technologies, which runs ads featuring former football star Joe Namath.

In August 2022, the Federal Trade Commission forced Benefytt to repay $100 million for fraudulent activities. The month before, the Securities and Exchange Commission levied more than $12 million in fines against Benefytt.

But CMS continues to allow Benefytt to work as a broker. Benefytt is owned by Madison Dearborn Partners, a Chicago-based private equity firm with ties to former Chicago mayor and current Ambassador to Japan Rahm Emanuel. Benefytt collects leads on potential customers, which they then sell to brokers and insurers to aggressively target seniors. CMS did not provide comment as to why they had not blocked Benefytt’s continuing work as a third-party marketing organization for Medicare.

Two different rounds of rule-making on Medicare Advantage marketing in 2023 instead focused on such reforms as reining in exaggerated claims and excessive broker compensation.

The enormous profits generated by Medicare Advantage plans — costing the federal government as much as $140 billion annually in overpayments to private companies — explains what drives the aggressive and often unethical marketing practices, said David Lipschutz, an associate director at the Center for Medicare Advocacy.

“The fact is, there is an increasingly imbalanced playing field between Medicare Advantage and traditional Medicare,” he said. “Medicare Advantage is being favored in many ways. Medicare Advantage plans are paid more than what traditional Medicare spends on a given beneficiary.

Those factors combined with the fact that they generate such profits for insurance companies, leads to those companies doing everything they can to maximize enrollment.”

Adding to the problem, Lipschutz argued, was the enormous influence of the health insurance industry in Washington. Health insurers spent more than $33 million lobbying Washington in just the first three quarters of 2023 alone.

“There is no real organized lobby for traditional Medicare, or organized advertising efforts,” he said. “During open enrollment, 80% of Medicare-related ads have to do with Medicare Advantage. We regularly encounter very well-educated and savvy folks who are tripped up by advertising and lured in by the bells and whistles. The deck is stacked against the consumer.”

Private equity firms have made a large investment in the Medicare Advantage brokerage and marketing sector, in addition to Madison Dearborn’s acquisition of Benefytt. Bain Capital, which Sen. Mitt Romney (R-Utah) co-founded, invested $150 million in Enhance Health, a Medicare Advantage broker, in 2021.

The CEO of EasyHealth, another private equity-backed brokerage, toldModern Healthcare in 2021 that “Insurance distribution is our Trojan horse into healthcare services.”

As federal law requires truth in advertising, a group of advocacy organizations–led by the Center for Medicare Advocacy, Disability Rights Connecticut, and the National Health Law Project–cited what they considered blatantly deceptive marketing by UnitedHealthcare to people who are eligible for both Medicare and Medicaid, in a complaint to CMS.

UnitedHealthcare had purchased ads in the Hartford Courant asking seniors in large bold-faced type: “Eligible for Medicare and Medicaid? You could get more with UnitedHealthcare.”

People who are eligible for both Medicare and Medicaid due to their income level are better off in traditional Medicare than Medicare Advantage given that Medicaid covers their out-of-pocket costs, meaning that they have wide latitude to choose their doctors, hospitals and medical procedures.

Sheldon Toubman, an attorney with Disability Rights Connecticut who worked to draft the complaint, framed the ad in the broader context of poor marketing practices by the Medicare Advantage industry.

“I have been aware for a long time of basically fraudulent advertising in the MA insurance industry,” Toubman told HEALTH CARE un-covered. “There’s an overriding misrepresentation — they tell you how great Medicare Advantage is, and never the downsides.

“There are two big downsides of going out of traditional Medicare:

They don’t tell you that you give up the broad Medicare provider network, which has nearly every doctor. And should you need expensive medical care in Medicare Advantage, you will learn there are prior authorization requirements. Traditional Medicare does almost no prior authorization, so you don’t have that obstacle. They don’t ever tell you any of that,” he said.

But it is marketing to dual-eligible individuals that is arguably the most problematic, Toubman argued. “They have Medicare and they are also low income. Because they are low-income, they also have Medicaid.

“Medicaid is a broader program — it covers a lot of things that Medicare doesn’t cover.

In Connecticut, 92,000 dual-eligible seniors have been ‘persuaded’ to sign up for Medicare Advantage. What’s outrageous about the marketing is they get you to sign up by offering extra services. … If you look at the ad in the Hartford Courant, it says you could get more, with the only real benefit being $130 per month toward food. But you now have this problem of a more limited provider network and prior authorization. UnitedHealth is doing false advertising.”

It’s a nationwide problem, Toubman said. “All insurers are doing this everywhere. We’re asking CMS and the Federal Trade Commission to conduct a nationwide investigation of this kind of problem. The failure to tell people that they give up their broader Medicare network — they don’t tell anybody that.”

For Jayne Kleinman, the unending ads are about one thing only: insurance industry profits. “Medicare Advantage has been strictly based on the people who make millions of dollars at the top of the company making more,” she said. “It’s all about money, not about you as an individual. Every time I saw an ad I’d get angry every single time — because I felt they were misleading people. The Medicare Advantage insurers are trying to scam people out of an interest of making money.”