In May 2024 a set of articles were published in the journal Science that focused on the intersection of misinformation and social media. The results, while preliminary in the grand scheme of things, were really interesting (and maybe a little alarming).

Last week, I made my once a decade trek to a dealership to buy a new car. I did my research in advance (and even negotiated the price) so I was hoping for a stress-free experience.

It was – up until the point where I got locked in the finance manager’s office for “the talk”. You know, the one where you are made to feel like a neglectful parent unless you pony up for all the fixin’s – everything from nitrogen filled tires to paint protection (just in case I encounter a flock of migratory geese on the drive home). I shook my head no about ten times before we got to the pre-paid maintenance plan options. I decided to be polite and listen (plus I was curious since I was purchasing a car from a manufacturer notorious for costly repairs). As compelling as it was to pay nearly $5,000 to what ultimately would amount to a few tire rotations for my electric vehicle, I held firm. The finance manager angrily handed me my signed documents and whisked me out of his office.

I guess I can’t blame car dealers for applying massive mark-ups for services that are inexpensive to provide. Except similar financial chicanery is currently playing out in our health insurance system. If you swap out the finance manager for a health insurer and replace me with the average everyday consumer, the dealer’s tactics are analogous to how insurers game medical loss ratio (MLR) requirements (except as a health care consumer, you can’t say “no”).

A bit of background is in order to understand why I thought about health insurance and car dealers in the same breath.

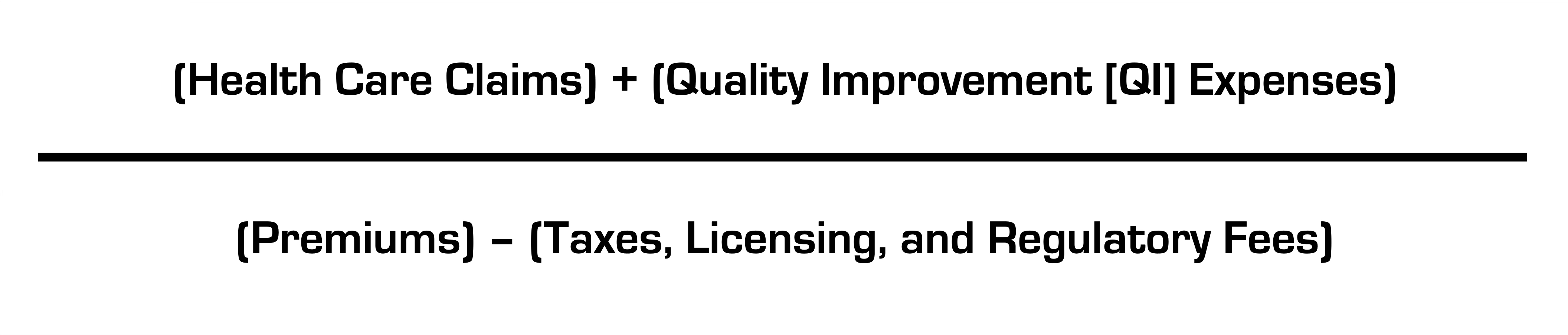

Insurance companies are required to spend a certain percentage of money they get from premiums on medical costs and quality improvement (QI); this is known as the medical loss ratio (MLR). If companies do not meet this ratio (usually 80-85%, depending on the product), they must refund the difference in the form of a rebate, or reduction in future premiums, to consumers.

Like any for-profit corporation in America today, a health insurer wants to avoid giving money back to consumers. Therefore, insurers have become adept at manipulating their MLRs through various accounting and financial engineering techniques. This manipulation optimizes their ability to meet MLR thresholds and avoid paying rebates, which runs afoul of its intended purpose: to ensure that patients receive the appropriate level of care.

So how do insurers game the system, and what evidence exists for this activity?

The current MLR formula is:

Health insurers do not control taxes and fees, but they can easily engineer the other variables. Below, I’ll explain how.

Step 1: Quality Improvement (QI) Expenses

The definition of allowable QI expenses is broad and includes activities to improve outcomes, patient safety, and reduce mortality (mom and apple pie stuff). Insurers played a big role in writing the MLR regulations after Congress enacted legislation and made sure they’d have wide latitude in what expenses are classified as QI (akin to the car dealer “option” list) and what product segments they assign them to.

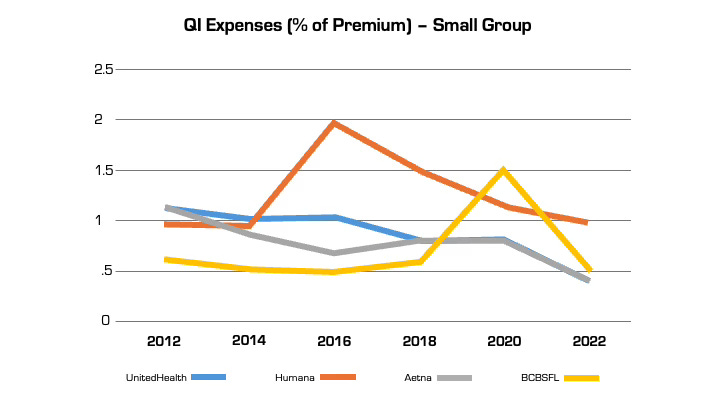

Looking at reported QI expenses sheds light on this practice. QI expenses vary between insurers. But they also vary widely for the same insurer from year to year (even after controlling for geography and product segment). In large part, this is attributable to financial engineering. QI costs can be effectively “transferred” on the income statement from one product segment to another, by adjusting the pro rata weightings). This enables them to optimize MLR performance across their insurance portfolio (i.e. by taking from a bucket with excess medical costs and putting it in another with insufficient costs) in a way that maximizes benefit to the insurer and is camouflaged from regulators and consumers. This is language from a recent UnitedHealth Group filing with the Securities and Exchange Commission: “Assets and liabilities jointly used are assigned to each reportable segment using estimates of pro-rata usage.”

Annual QI expenses across four insurers in Florida in the small group market.

Although these QI percentages are small, the associated dollar amounts are large. In 2022, UnitedHealth, Humana, and Aetna reported $494 million, $550 million, and $395 million respectively in allowable QI expenses for their national plans. While there is some legitimate QI activity at insurers (e.g., pharmacists who identify high risk medications in the elderly), the reality is that much of the QI work is already heavily resourced within provider organizations, where it is more effective. Insurers also can (and do) count “wellness and health promotion activities” despite limited evidence these programs improve health outcomes and are more often used by insurers as marketing tools.

Step 2. Health Care Claims

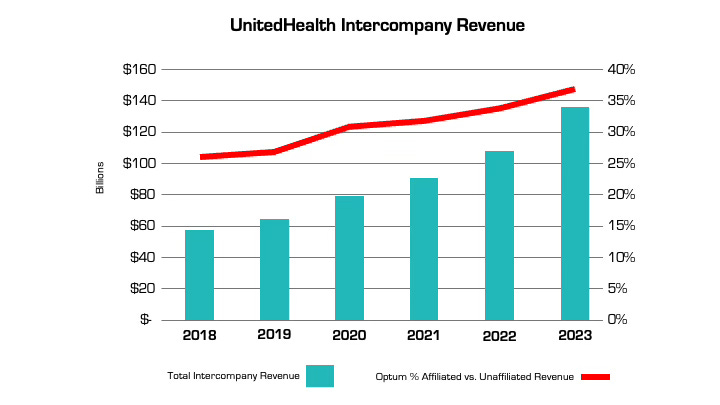

The other variable that insurers can manipulate is claims costs. The more an insurer is vertically integrated, the easier it is. The prime example is UnitedHealth, which has an insurance arm (UnitedHealthcare) and a big division that encompasses medical services, among many other things (Optum), as well as various other subsidiaries. Optum Health and Optum Rx receive a significant portion of their revenue from UnitedHealthcare for providing services like care and pharmacy benefit management to people enrolled in its health plans. In fact, the amount of UnitedHealth’s corporate “eliminations,” (meaning inter-company revenue that is reported on their consolidated financial statement) has more than doubled over the past five years (from $58.5 billion to $136.4 billion). The proportion of revenue Optum derives from UnitedHealthcare versus unaffiliated entities has increased by nearly 50% over the same period. A similar trend is playing out at every major insurer.

Take the example of the insurance company Aetna, the PBM CVS Caremark, and CVS Pharmacy, which are all vertically integrated and owned by CVS Health. If a patient goes to a CVS store to fill a prescription for Imatinib, a generic chemotherapy drug, the total cost the patient and insurance company pay is $17,710.21 for a 30-day supply. The same drug is sold by Cost Plus Drugs for $72.20 (the cost is calculated by adding the wholesale price and a 15% fee). When the patient fills the prescription at a CVS retail pharmacy, CVS Health can record that the patient paid a medical claim cost of $17,710.21 (even though the cost to acquire the drug is $70) and the remaining $17,640 can be retained as profits disguised as medical costs.

Insurers’ extensive acquisition of physician practices also facilitates gamification of the MLR via its ability to pay capitation (a set amount per person) to a risk-bearing provider organization (RBO) it owns, such as a medical group. This enables the insurer to lock in a set amount of premium as “medical expense” (usually around 85%) with the downstream provider group “managing” those costs. There’s a loophole, however. While the insurer has technically met its MLR requirement, the downstream RBO is subject to far fewer regulations on how it spends the money, which makes it easier to generate profits by skimping on care.

The regulations on RBOs vary by state. In many cases, while RBOs need to meet minimum capital requirements, they are not subject to the same MLR provisions as insurers. For a vertically integrated insurer that gets a huge amount of revenue from taxpayer-supported programs like Medicare Advantage and Medicaid, this essentially means that (1) the Center for Medicare and Medicaid Services puts the money into the insurer’s right pocket, (2) the insurer moves it to the left pocket, and (3) CMS checks the right pocket – and just the right pocket – at the end of the year to make sure it’s mostly empty (without regard to the fact that the left one may be busting at the seams).

The good news is there are ways to address these issues, both through updating the MLR provisions in the Affordable Care Act (which are long in the tooth) and more rigorous and comprehensive reporting requirements and regulation of vertically integrated insurers.

Just like I don’t want car dealers pushing unnecessary add-ons to increase their profit margins, consumers deserve that the required portion of their hard spent premium dollar actually goes toward their health care instead of further enriching huge corporations, executives, and Wall Street shareholders.

Health systems are rightly concerned about Republican plans to cut Medicaid spending, end ACA subsidies and enact site neutral payments, says consultant Michael Abrams, managing partner of Numerof, a consulting firm.

“Health systems have reason to worry,” Abrams said shortly after President Donald Trump was inaugurated on Monday.

While Trump mentioned little about healthcare in his inauguration speech, the GOP trifecta means spending cuts outlined in a one-page document released by Politico and another 50-pager could get a majority vote for passage.

Of the insurers, pharmaceutical manufacturers and health systems that Abrams consults with, healthcare systems are the ones that are most concerned, Abrams said.

At the top of the Republican list targeting $4 trillion in healthcare spending is eliminating an estimated $2.5 billion from Medicaid.

“There’s no question Republicans will find savings in Medicaid,” Abrams said.

Medicaid has doubled its enrollment in the last couple of years due to extended benefits made possible by the Affordable Care Act, despite disenrolling 25 million people during the redetermination process at the end of the public health emergency, according to Abrams.

Upward of 44 million people, or 16.4% of the non-elderly U.S. population are covered by an Affordable Care Act initiative, including a record high of 24 million people in ACA health plans and another 21.3 million in Medicaid expansion enrollment, according to a KFF report.Medicaid expansion enrollment is 41% higher than in 2020.

The enhanced subsidies that expanded eligibility for Medicaid and doubled the number of enrollees are set to expire at the end of 2025 and Republicans are likely to let that happen, Abrams said. Eliminating enhanced federal payments to states that expanded Medicaid under the ACA are estimated to cut the program by $561 billion.

If enhanced subsidies end, the Congressional Budget Office has estimated that the number of people who will become uninsured will increase by 3.8 million each year between 2026 and 2034.

The enhanced tax subsidies for the ACA are set to expire at the end of 2025. This could result in another 2.2 million people losing coverage in 2026, and 3.7 million in 2027, according to the CBO.

WHY THIS MATTERS

For hospitals, loss of health insurance coverage means an increase in sicker, uninsured patients visiting the emergency department and more uncompensated care.

“Health systems are nervous about people coming to them who are uninsured,” Abrams said. “There will be people disenrolled.”

The federal government allowed more people to be added to the Medicaid rolls during the public health emergency to help those who lost their jobs during the COVID-19 pandemic, Numerof said. Medicaid became an open-ended liability which the government wants to end now that the unemployment rate is around 4.2% and jobs are available.

An idea floating around Congress is the idea of converting Medicaid to a per capita cap and providing these funds to the states as a block grant, Abrams said. The cost of those programs would be borne 70% by the federal government and 30% by states.

This fixed amount based on a per person amount would save money over the current system of letting states report what they spent.

Another potential change under the new administration includes site neutral Medicare payments to hospitals for outpatient services.

The HFMA reported the site neutral policy as a concern in a list it published Monday of preliminary federal program cuts totaling more than $5 trillion over 10 years. The 50-page federal list is essentially a menu of options, the HFMA said, not an indication that programs will actually be targeted leading up to the March 14 deadline to pass legislation before federal funding expires.

Other financial concerns for hospitals based on that list include: the elimination of the tax exemption for nonprofit hospitals, bringing in up to $260 billion in estimated 10-year savings; and phasing out Medicare payments for bad debt, resulting in savings of up to $42 billion over a decade.

Healthcare systems are the ones most concerned over GOP spending cuts, according to Abrams. Pharmacy benefit managers and pharmaceutical manufacturers also remain on edge as to what might be coming at them next.

THE LARGER TREND

President Donald Trump mentioned little about healthcare during his inauguration speech on Monday.

Trump said the public health system does not deliver in times of disaster, referring to the hurricanes in North Carolina and other areas and to the fires in Los Angeles.

Trump also mentioned giving back pay to service members who objected to getting the COVID-19 vaccine.

He also talked about ending the chronic disease epidemic, without giving specifics.

“He didn’t really talk about healthcare even in the campaign,” Abrams said.

However, in his consulting work, Abrams said, “The common thread is the environment is changing quickly,” and that healthcare organizations need to do the same “in order to survive.”

Liberal advocacy groups are ramping up efforts to protect the Medicaid program from potential cuts by Republican lawmakers and the new Trump administration.

The Democratic group Protect Our Care launched Tuesday an eight-figure “Hands off Medicaid” ad campaign targeting key Republicans in the House and Senate, warning of health care being “ripped away” from vulnerable Americans.

The lawmakers include GOP Sens. Bill Cassidy (La.), Chuck Grassley (Iowa), Lisa Murkowski (Alaska) and Susan Collins (Maine), as well as Reps. David Schweikert (Ariz.), Mike Lawler (N.Y.) and David Valadao (Calif.).

The campaign will also include digital advertising across platforms targeting the Medicaid population in areas around nursing homes and rural hospitals, ads on streaming platforms as well as billboards and bus stop wraps.

Medicaid covers 1 in 5 Americans, and the group wants to highlight that includes “kids, moms, seniors, people of color, rural Americans, and people with disabilities.”

“The American people didn’t vote in November to have their grandparents kicked out of nursing homes or health care ripped away from kids with disabilities or expectant moms in order to give Elon Musk another tax cut,” Protect Our Care chair Leslie Dach said in a statement.

House Republicans have expressed openness to making some drastic changes in the Medicaid program to pay for extending President Trump’s signature tax cuts, including instituting work requirements and capping how much federal money is spent per person. The ideas have been conservative mainstays since they were included as part of the 2017 Obamacare repeal effort.

Separately, advocacy group Families USA led a letter with more than 425 national, state and local organizations calling on Trump to protect Medicaid.

The groups noted that if the Trump administration wants to trim health costs, “there are many well-vetted, commonsense and bipartisan proposals” that don’t involve slashing Medicaid.

“In 2017, millions upon millions of Americans rose up against proposed cuts and caps and made clear how much they valued Medicaid as a critical health and economic lifeline for themselves, their families, and their communities. The American people are watching once again, and we urge you to take this opportunity to choose a different path,” they wrote.

Downgrades continued to outpace upgrades in 2024 although at a lower rate than in 2023. When combining the rating actions of the three rating agencies, the number of downgrades (95) declined while the number of upgrades (37) increased, compared to 116 and 33, respectively, in 2023. Many of the downgrades reflected ongoing expense pressure that exceeded revenue growth, even as volumes headed back to pre-pandemic levels and the use of contract labor declined. Other downgrades reflected outsized increases in debt to fund pivotal growth strategies. Most of the upgrades reflected mergers of lower-rated hospitals into higher-rated systems. Rating affirmations remained the majority rating action in 2024, as in prior years.

Key takeaways include:

The ratio of downgrades to upgrades narrowed at Moody’s (2.0-to-1 in 2024 from 3.2-to-1 in 2023) and Fitch (1.5-to-1 from 3.5-to-1). S&P saw a wider spread in the ratio: 4.5-to-1 in 2024 from 3.8-to-1 in 2023.

Downgrades reflected a wide swath of hospitals, from small independent providers to large regional systems. Large academic medical centers and children’s hospitals saw downgrades, even with exclusive tertiary services that provided differentiation with payers. Shared, recurring downgrade factors included weaker financial performance, payer mix shifts to more governmental and less commercial, and thinner reserves. Many of the downgrades were concentrated along the two coasts: California and the Pacific Northwest and New York and Pennsylvania. Many of the ratings were already in low or below investment grade categories.

Multi-notch downgrades continued in 2024, ranging from two to four notch movements in one rating action. One of the hospitals that experienced a four-notch downgrade subsequently defaulted on an interest payment (Jackson Hospital & Clinics, AL). Multi-notch upgrades reflected mergers into higher-rated systems, the largest being a seven-notch upgrade of a small, single-site hospital into a 19-hospital system in the Midwest.

Five hospitals experienced multiple rating actions in 2024, with rating committees convening not once but two and three times during the year. These were distressed credits whose financial performance and reserve levels dropped materially from quarter to quarter, a characteristic of high-yield or speculative rated borrowers.

While some of the upgrades followed mergers, other upgrades reflected improved financial performance and stable or growing liquidity. Likewise, some of the upgraded hospitals began receiving new supplemental funds known as Direct Payment Programs (DPPs). Unlike other supplemental funds, DPPs are subject to annual federal and state approval, making their long-term reliability uncertain. Numerous types of providers saw upgrades—including academic medical centers, independent hospitals and regional health systems—and were located across the U.S. Most of the upgraded hospitals (excluding those involved in mergers) were already investment grade.

As in past years, rating affirmations represented the overwhelming majority of rating actions in 2024. This is welcome news for the industry as many hospitals and health systems will turn to the bond market to borrow for their capital projects. Investors’ view of the industry should be bolstered by the change in industry outlooks. S&P moved to Stable from Negative and Fitch moved to Neutral from Deteriorating in December 2024, joining Moody’s revision to Stable from Negative in 2023.

We expect rating affirmations will again be the majority rating action in 2025. However, even with the stability viewed by the agencies, we expect downgrades to outpace upgrades given a growing reliance on government payers, labor challenges and a competitive environment. Policy and funding changes will also cast uncertainty into the mix in 2025 and may cause credit deterioration in future years.

To understand the fatal attack on UnitedHealthcare CEO Brian Thompson and the unexpected reaction on social media, you have to go back to the 1990s when managed care was in its infancy. As a consumer representative, I attended meetings of a group associated with the health care system–doctors, academics, hospital executives, business leaders who bought insurance, and a few consumer representatives like me.

It was the dawn of the age of managed care with its promise to lower the cost and improve the quality of care, at least for those who were insured.

New perils came with that new age of health coverage.

In the quest to save money while ostensibly improving quality, there was always a chance that the managed care entities and the doctors they employed or contracted with – by then called managed care providers – could clamp down too hard and refuse to pay for treatments, leaving some people to suffer medically. Groups associated with the health care industry tried to set standards to guard against that, but as the industry consolidated and competition among the big players in the new managed care system consolidated, such worries grew.

Over the years the squeeze on care got tighter and tighter as the giants like UnitedHealthcare–which grew initially by buying other insurance companies such as Travelers and Golden Rule–and Elevance, which gobbled up previously nonprofit Blue Cross plans in the 1990s, starting with Blue Cross of California, needed to please the gods of the bottom line. Shareholders became all important. Paying less for care meant more profits and return to investors, so it is no wonder that the alleged killer of the UnitedHealthcare chief executive reportedly left the chilling message:

‘‘DENY. DEFEND. DEPOSE,” words associated with insurance company strategies for denying claims.

The American health care system was far from perfect even in the days when more employers offered good coverage for their workers and often paid much or all of the cost to attract workers. Not-for-profit Blue Cross Blue Shield plans in many states provided most of the coverage, and by all accounts, they paid claims promptly. In my now very long career of covering insurance, I cannot recall anyone in the old days complaining that their local Blue Cross Blue Shield organization was withholding payment for care.

Today Americans, even those who thought they had “good” coverage, are now finding themselves underinsured, as a 2024 Commonwealth Fund study so clearly shows. Nearly one-quarter of adults in the U.S. are underinsured meaning that although they have health insurance, high deductibles, copayments and coinsurance make it difficult or impossible for them to pay for needed care. As many as one-third of people with chronic conditions such as diabetes said they don’t take their medications or even fill prescriptions because they cost too much.

Before he passed away last year, one of our colleagues, Marshall Allen, had made recommendations to his followers on how to deal with medical bills they could not pay. KFF reporters also investigated the problems families face with super-high bills. In 2022 KFF reporters offered readers a thorough look at medical debt in the U.S. and reported alarming findings.

In 2019, U.S. medical debt totaled $195 billion, a sum larger than the economy of Greece. Half of adults don’t have enough cash to cover an unexpected medical bill while 50 million adults – one in five in the entire country – are paying off bills on an installment plan for their or a family member’s care.

One would think that such grim statistics might prompt political action to help ease the debt burden on American families. But a look at the health proposals from the Republican Study Committee suggest that likely won’t happen. The committee’s proposed budget would cut $4.5 trillion dollars from the Affordable Care Act, Medicaid, and the Children’s Health Insurance Program leaving millions of Americans without health care.

From the Democrats, there appear to be no earth-shaking proposals in their immediate future, either. Late last summer STAT News reported, “With the notable exception of calling to erase medical debt by working with the states, Democrats are largely eyeing marginal extensions or reinstatements of their prior policy achievements.” Goals of the Democratic National Committee were shoring up the Affordable Care Act, reproductive rights, and addressing ambulance surprise bills.

A few years ago when I was traveling in Berlin, our guide paused by a statue of Otto von Bismarck, Germany’s chancellor in the late 1800s, who is credited with establishing the German health system. The guide explained to his American travelers how and why Bismarck founded the German system, pointing out that Germany got its national health system more than a hundred years before Obamacare. Whether the Americans got the point he was making, I could not tell for no one in the group appeared interested in Germany’s health care system. Today, though, they might pay more attention.

In the coming months, I will write about health systems in Germany and other developed countries that, as The Commonwealth Fund’s research over many years has shown, do a much better job than ours at delivering high quality care – for all of their citizens – and at much lower costs.

UnitedHealth executives made a valiant attempt yesterday to persuade investors that they have figured out how to improve customer service and keep Congress and the incoming Trump administration from passing laws that could shrink the company’s profit margins – and maybe even the company itself – but Wall Street wasn’t buying.

During their first call with investors since the murder of UnitedHealthcare CEO Brian Thompson, the company’s top brass pointed the finger of blame for rising health care costs everywhere but at themselves – primarily at hospitals and pharmaceutical companies – and made statements that simply were not true. Investors clearly did not find their comments reassuring or credible. By the end of the day shares of UnitedHealth’s stock were down more than 6% to $510.59. That marked a continuation of a slide that began after the stock price peaked at $630.73 on November 11 – a decline of almost 20%.

In a little more than two months, the company has lost an astonishing $110 billion in market capitalization, and shareholders have lost an enormous amount of the money they invested in UnitedHealth.

Earlier yesterday morning, the company released fourth-quarter and full-year 2024 earnings, which were slightly higher on a per share basis than Wall Street financial analysts had expected: $6.81 per share in the fourth quarter compared to analysts’ consensus estimate of $6.73 for the quarter. But the company posted lower revenue during the last three months of 2024 than analysts had expected. While revenue was up 7% over the same quarter in 2023, to $100.8 billion, analysts had expected revenue to grow to $101.6 billion.

And on a full-year basis, the company’s net profits fell an eye-popping 36%, from $22.4 billion in 2023 to $14.4 billion last year.

Bottom line: the company, which until last year had grown rapidly, actually shrank in some respects, especially in the division that operates the company’s health plans. UnitedHealthcare, which Thompson led, saw its revenue increase slightly but its profits fall. The other big division, Optum, which among other things owns and operates numerous physician practices and clinics and one of the country’s largest pharmacy benefit managers (PBMs), fared much better.

While Optum’s 2024 revenue was lower than UnitedHealthcare’s ($253 billion and $298 respectively), it made far more in profits on an operating basis ($16.7 billion and $15.6 respectively).

Optum’s operating profit margin was 6.6% while UnitedHealthcare’s was 5.2%.

The company’s executives blamed higher health care utilization, especially by people enrolled in its Medicare Advantage plans, for the decline in profits.

Witty and CFO John Rex pointed the finger of blame at hospitals and drug companies for rising medical prices. And they obscured the huge amounts of money the company’s PBM, Optum Rx, extracts from the pharmacy supply chain. While the company chose not to break out exactly how much of Optum’s revenues of $298 billion came from Optum Rx, it appears that more than half of it was contributed by the PBM. The company did note that Optum Rx revenues increased 15% during 2024.

Nevertheless, Witty and Rex blamed drug makers for high prices.

They also said that they would be changing the PBM’s business practices to pass through rebate discounts from drug makers to its customers, claiming that it already passes through 98% of them and will reach 100% by 2028. That clearly was a talking point aimed at Washington, where there is significant bipartisan support for legislation that would require all PBMs to do so. Despite UnitedHealth’s claim, there is no external verification to back up that they are passing 98% of rebates back to customers.

Another claim the executives made that is not true is that the Medicare Advantage program saves taxpayers money. Numerous government reports have shown the opposite, that the federal government spends considerably more on people enrolled in Medicare Advantage plans than those enrolled in the traditional Medicare program.

Reports have estimated that UnitedHealthcare, which is the largest Medicare Advantage company, and other MA plans are overpaid between $80 billion and $140 billion a year.

There is also growing bipartisan support to reform the Medicare Advantage program to reduce both the overpayments and the excessive denials of care at UnitedHealthcare and other MA insurers.

While company executives might be hoping that their fortunes will improve during the second Trump administration, Trump recently joined some Republican members of Congress, like Rep. Buddy Carter of Georgia, who are calling for significant reforms, especially to pharmacy benefit managers.

At a news conference last month, Trump promised to “knock out” those middlemen in the pharmacy supply chain.

“We are paying far too much, because we are paying far more than other countries,” he said. “We have laws that make it impossible to reduce [drug costs] and we have a thing called a ‘middleman’ … that makes more money than the drug companies, and they don’t do anything except they’re middlemen. We are going to knock out the middleman.”

The murder of UnitedHealthcare CEO Brian Thompson in December 2024 represented a horrific and indefensible act of violence. As a physician and healthcare leader, I initially declined to comment on the killing. I felt that speculating about the shooter’s intent would only sensationalize a terrible act.

Regardless of the circumstances, vigilante violence has no place in a free and just society.

Now, more than a month later, I feel compelled to address one aspect of the story that has been widely misunderstood: the public’s reaction to the news of Thompson’s murder. Specifically, why tens of thousands of individuals “liked” and “laughed” at a post on Facebook announcing the CEO’s death.

What causes someone to ‘like’ murder?

News analysts have attributed the social media response to America’s “simmering anger” and “frustration” with a broken healthcare system, pointing to rising medical costs, insurance red tape and time-consuming prior authorization requirements as justifications.

These are all, indeed, problems and may explain some of public’s reaction. Yet these descriptions grossly understate the lived reality for most of those affected. When I speak with individuals who have lost a child, parent or spouse because of what they perceive as an unresponsive and uncaring system, their pain is raw, intense. What they feel isn’t frustration—it’s agony.

By framing healthcare’s failures in terms of statistical measures and policy snafus, we reduce a deeply personal crisis to an intellectual exercise. And it’s this very detached, cognitive approach that has allowed our nation to disregard the emotional devastation endured by millions of patients and their families.

When journalists, healthcare leaders and policymakers cite eye-popping statistics on healthcare expenditures, highlight exorbitant insurer profits or deride the bloated salaries of executives, they leave out a vital part of the story. They omit the unbearable human suffering behind the numbers. And I fear that until we approach healthcare as a moral crisis—not merely an economic or political puzzle to solve—our nation will never act with the urgency required to relieve people’s profound pain.

A pain beyond reason

In Dante’s Inferno, hell is a place where suffering is eternal and the cries of the damned go unheard. For countless Americans who feel trapped in our healthcare system, that metaphor rings true. Their anguish and pleas for mercy are met with silence.

It is this sense of abandonment and powerlessness, not mere frustration, that fuels both a desperate rage and an anger at a system and its leaders who appear not to care. The response isn’t one of glee—it’s a visceral reaction born of pain and unrelenting remorse.

As a clinician, I’ve seen life-destroying pain in my patients—and even within my own family. When my cousin Alan died in his twenties from a then-incurable cancer, my aunt and uncle were powerless to save him. Their grief was profound, unrelenting and eternal.They never recovered from the loss. But Alan’s death, heartbreaking as it was, stemmed from the limits of science at the time.

What millions of Americans endure today is different. Their loved ones die not because cures don’t exist but because the healthcare system treats them like a number. Bureaucratic inefficiencies, profit-driven delays and systemic indifference produce avoidable tragedies.

To appreciate this depth of pain, imagine standing behind a chain-link fence, watching someone you love being tortured. You scream and plead for help, but no one listens. That is what healthcare feels like for too many Americans. And until all of us acknowledge and feel their pain, little will improve.

Curing America’s indifference

When we focus solely on cold numbers—the millions who’ve lost Medicaid coverage, the hundreds of thousands of avoidable deaths each year, or the life-expectancy gap between the U.S. and other nations—we strip healthcare of its humanity.

But once we stop framing these failures as bureaucratic inefficiencies or frustrations and, instead, focus on the devastation of having to watch a loved one suffer and die needlessly, we are forced to confront a moral imperative. Either we must act with urgency and resolve the problem or admit we simply don’t care.

In the halls of Congress, lawmakers continue to weigh modest reforms to prior authorization requirements and Medicaid spending—baby steps that won’t fix a system in crisis. The truth is that without bold, transformative action, healthcare will remain unaffordable and inaccessible for millions of families whose anguish will grow.

Here are three examples of the scale of transformation required:

Reverse the obesity epidemic with a two-part strategy. Congress will need to tax ultra-processed, sugary foods that drive hundreds of billions of dollars in healthcare costs each year. In parallel, lawmakers should cap the manufacturer-set price of weight-loss medications like Ozempic and Wegovy to be no higher than in peer nations.

Change clinician payments from volume to value. Current fee-for-service payment systems incentivize unnecessary tests, treatments and procedures rather than better health outcomes. Transitioning to pay-for-value would reward healthcare providers, and specifically primary care physicians, who successfully prevent chronic diseases, better manage existing conditions, and reduce complications such as heart attacks, strokes and kidney failure.

Empower patients and save lives with generative AI. Tools like ChatGPT can help reduce the staggering 400,000 annual deaths from misdiagnoses and 250,000 more from preventable medical errors. By integrating AI into healthcare, we can enable at-home care, continuous disease monitoring and personalized treatment, making medical care safer, more accessible and more efficient.

If elected officials, payers and regulators fail to act, they will have chosen to perpetuate the unbearable pain and suffering patients and families endure daily. They need to hear the cries of people. The time for transformative action is now.

As Donald Trump begins his second term, America’s healthcare system is in crisis: medical costs are skyrocketing, life expectancy has stagnated, and burnout runs rampant among healthcare workers.

These problems are likely to become worse now that Trump has handed the federal budget over to Elon Musk. The world’s richest man now co-heads the Department of Government Efficiency (DOGE), a non-government entity tasked with slashing $500 billion in “wasteful” spending.

The harsh reality is that Musk’s mission can’t succeed without gutting healthcare access and coverage for millions of Americans.

Deleting dollars from American healthcare

Since Trump’s first term, the country’s economic outlook has worsened significantly. In 2016, the national debt was $19 trillion, with $430 billion allocated to annual interest payments. By 2024, the debt had nearly doubled to $36 trillion, requiring $882 billion in debt service—12% of federal spending that is legally untouchable.

Add to that another 50% of government expenditures that Trump has deemed politically off-limits: Social Security ($1.35 trillion), Medicare ($848 billion) and Defense ($1.13 trillion). That leaves just $2.6 trillion—less than 40% of the $6.75 trillion federal budget—available for cuts.

In a recent op-ed, Musk and DOGE co-chair Vivek Ramaswamy proposed eliminating expired or misused funds for programs like Public Broadcasting and Planned Parenthood, but these examples account for less than $3 billion total—not even 1% of their target.

This shortfall will require Musk to cut billions in government healthcare spending. But where will he find it?

With Medicare off limits to DOGE, the options for major reductions are extremely limited. Big-ticket healthcare items like the $300 billion in tax-deductibility for employer-sponsored health insurance and $120 billion in expired health programs for veterans will prove politically untouchable. One will raise taxes for 160 million working families and the latter will leave veterans without essential medical care.

This means DOGE will have to attack Medicaid and the ACA health exchanges. Here’s how 20 million people will likely lose coverage as a result.

1. Reduced ACA exchange funding

Since its enactment in 2010, the Affordable Care Act (ACA) has provided premium subsidies to Americans earning 100% to 400% of the federal poverty level. For lower-income families, the ACA also offers Cost Sharing Reductions, which help offset deductibles and co-payments that fund 30% of total medical costs per enrollee. Without CSRs, a family of four earning $40,000 could face deductibles as high as $5,000 before their insurance benefits apply.

If Congress allows CSR payments to expire in 2026, federal spending would decrease by approximately $35 billion annually. If that happens, the Congressional Budget Office expects 7 million individuals to drop out of the exchanges. Worse, without affordable coverage alternatives, 4 million families would lose their health insurance altogether.

2. Slashing Medicaid coverage and tightening eligibility

Medicaid currently provides healthcare for over 90 million low-income Americans, including children, seniors and individuals with disabilities. To meet DOGE’s $500 billion goal, several cost-cutting strategies appear likely:

Reversing Medicaid expansion: The ACA expanded Medicaid eligibility to those earning up to 138% of the federal poverty level, reducing the uninsured rate from 16% to 8%. Undoing this expansion would strip coverage from millions in the 40 states that adopted the program.

Imposing work requirements: Proponents argue this could encourage employment, but most Medicaid recipients already work for employers that don’t provide insurance. In reality, work requirements primarily create bureaucratic barriers that disqualify millions of eligible individuals, reducing program costs at the expense of coverage.

Switching to block grants: Unlike the current Medicaid system, which adjusts funding based on need, less-expensive block grants would provide states with fixed allocations. This will, however, force them to cut services and reduce enrollment.

Medicaid currently costs $800 billion annually, with the federal government covering 70%. Reducing enrollment by 10% (9 million people) could save over $50 billion annually, while a 20% reduction (18 million people) could save $100 billion.

Either outcome would devastate families by eliminating access to vital services including prenatal care, vaccinations, chronic disease management and nursing home care. As states are forced to absorb the financial burden, they’ll likely cut education budgets and reduce infrastructure investments.

The first 100 days

The numbers don’t lie: Musk and DOGE could slash Medicaid funding and ACA subsidies to achieve much of their $500 billion target. But the human cost of this approach would be staggering.

Fortunately, there are alternative solutions that would reduce spending without sacrificing quality. Shifting provider payments in ways that reward better outcomes rather than higher volumes, capping drug prices at levels comparable to peer nations, and leveraging generative AI to improve chronic disease management could all drive down costs while preserving access to care.

These strategies address the root causes of high medical spending, including chronic diseases that, if better managed, could prevent 30-50% of heart attacks, strokes, cancers, and kidney failures according to CDC estimates.

Yet, in their pursuit of immediate budgetary cuts, Musk and DOGE have omitted these kinds of reform options. As a result, the health of millions of Americans is at major risk.