As the economic situation has worsened over the past few months, we’ve been working with several health systems to recalibrate strategy. For many, the anticipated “post-COVID recovery” period has turned into a struggle to reverse declining (often negative) margins, while still scrambling to address mounting workforce shortages. All this amid continued pressure from disruptive competitors and ever-rising consumer expectations.

In the graphic above, we’ve pulled together some of the most important changes we believe health systems need to make. These range from improvements to the operating model (shifting to a team-based approach to staffing, greater use of automation where appropriate, and moving to asset-light capital strategies) to transformations of the clinical model (moving care into lower-cost outpatient and community settings, integrating virtual care into clinical delivery, and creating tighter alignment with key physicians).

In general, the goal is to deliver lower-cost care in less expensive settings, using less expensive staff.

But those cost-saving strategies will need to be coupled with a new go-to-market approach, including new payment models that reward systems for shifting away from high-cost (and highly reimbursed) care models.

Employers and consumers will expect more solution-based offerings, which integrate care across the continuum into coherent bundles of service. This will require a more deliberate focus on service line strategies, moving away from a fragmented, inpatient-centric model.

Contracting approaches must align payment with this shift, changing incentives to reward coordinated, cost-effective, outcomes-driven care.

A key insight from our discussions with health system leaders: short-term cost-cutting initiatives to “stop the bleed” won’t suffice—instead, more permanent solutions will be required that address not only the core operating model, but also the approach to revenue generation.

The post-COVID environment is turning out to be a lot tougher than many had expected, to say the least.

Private insurers pay high and rising prices to hospitals. But whether this is “good” or “bad” depends on what’s behind this phenomenon. Do high prices reflect investments in quality? Or do they instead reflect issues like lack of competition due to hospital consolidation? The answer matters for efforts to reduce health care spending.

In a new paper in the Journal of Health Economics, Craig Garthwaite, Christopher Ody and Amanda Starc investigated whether the prospect of financial rewards drove differences in hospital quality measures — including things like mortality rates, patient experience, technology adoption and emergency department wait times. Specifically, the authors’ examined whether hospitals are more likely to invest in quality if they will be rewarded through higher prices. This is more feasible if they’re serving lots of commercially insured patients, since private insurers may pay higher rates if patients value those hospitals. But that strategy may not be successful in areas with large shares of the population on Medicare and Medicaid, which do not negotiate prices.

The researchers found that:

Hospitals in areas with more privately insured patients had higher quality scores compared to hospitals with more publicly insured patients.

Hospitals targeting more privately insured patients also had higher costs than those relying more on payers like Medicare and Medicaid.

These results suggest hospitals make strategic investments in quality to attract privately insured patients. This is consistent with what one might expect from market competition and the results of other recent research. These findings do not, however, imply that prices are “optimal.” Prices also reflect factors like provider consolidation that have little observable effects on quality. Indeed, hospital prices likely reflect a mix of valuable and wasteful spending.

The analysis does have limitations. The authors used the demographics of the areas around the hospital instead of each hospital’s actual potential mix of patients. In addition, it is possible that some quality differences across hospitals actually reflect differences between patients with private and public insurance which aren’t easy to capture in data. However, the authors’ results were similar across several quality measures, including those where this is less of a concern.

These results can help better inform efforts to reduce health care costs. Policymakers interested in reducing hospital prices should be aware that doing so might reduce investments in quality. This suggests placing a greater emphasis on policies that target prices stemming from clear sources of inefficiencies, like consolidation, since such tradeoffs are likely smaller.

Steward Health Care is abandoning its proposal to sell five Utah hospitals to HCA Healthcare, and New Jersey-based RWJBarnabas Health dropped its plan to purchase New Brunswick, NJ-based Saint Peter’s Healthcare System. These pivots come just weeks after the Federal Trade Commission (FTC) filed suits to block the transactions, saying they would reduce market competition. The FTC said in a statement that these deals “should never have been proposed in the first place,” and “…the FTC will not hesitate to take action in enforcing the antitrust laws to protect healthcare consumers who are faced with unlawful hospital consolidation.”

The Gist: These latest mergers follow the fate of the proposed Lifespan and Care New England merger in Rhode Island, and the New Jersey-based Hackensack Meridian Health and Englewood Health merger, which were both abandoned after FTC challenges earlier this year.

Antitrust observers find these recent challenges unsurprising, as all were horizontal, intra-market deals of the kind that commonly raise antitrust concerns. What will be more telling is whether antitrust regulators can successfully mount challenges of cross-market mergers, or vertical mergers between hospitals, physicians, and insurers.

Consumers and employers recently filed lawsuits against Hartford HealthCare, HCA Healthcare, and Advocate Aurora Health, accusing the health systems of using their market power to increase prices through anticompetitive contracting practices. New reporting from the Wall Street Journal finds that all three suits are receiving funding from billionaire John Arnold, through his charitable foundation Arnold Ventures, which has sponsored several efforts to reduce healthcare spending. While the health systems say that the claims are baseless, the law firm leading the suits, Fairmark Partners, says that it’s attempting to enforce antitrust laws through the courts.

The Gist: Amid the Biden administration’s increased scrutiny of health system anticompetitive behavior, state governments and philanthropic groups are also taking a more active role in challenging hospital deals and contracting practices.

While these groups have targeted hospital prices because they’re a significant source of increased healthcare spending, these lawsuits do little to address the perverse underlying incentives that push hospitals to seek higher prices from commercial patients, to cross-subsidize what they view as insufficient pricing from public payers.

LHC, a postacute care behemoth with several hundred home health and hospice locations, as well as a dozen long-term care hospitals, would greatly expand Optum’s ability to provide home-based and long-term care. The FTC’s second request for information threatens to delay the deal, which was set to close in the latter half of this year.

The Gist: The LHC deal is the second UnitedHealth Group (UHG) transaction that antitrust regulators have targeted recently. The Department of Justice filed alawsuit earlier this year to block UHG’s acquisition of Change Healthcare, alleging that acquiring a direct competitor for claims solutions would reduce competition.

The FTC has historically focused its efforts on horizontal integration, but the LHC scrutiny, in combination with a recent inquiry into pharmacy benefit managers, indicates its focus may be expanding to vertical integration.

This week’s contributor is Aditi Sen, the Director of Research and Policy at the Health Care Cost Institute. Her work uses HCCI’s unique data resources to conduct analyses that inform policy to promote a sustainable, accessible and high-value health care system.

High health care prices in the U.S. make it hard for people to access care, difficult for employers to provide insurance, and challenging for policymakers to balance health care spending with other budgetary priorities. That’s why it’s important to understand what drives prices higher and identify policies to keep prices from getting so high.

In a new paper in Health Affairs, Vilsa Curto, Anna Sinaiko and Meredith Rosenthal examined whether hospital and health systems’ acquisition of and contracting with physician practices – two forms of what is often called vertical integration – has led to higher prices for physician services. The researchers combined four sets of data from Massachusetts from 2013-2017 for their analysis.

They found that:

The percent of physicians who joined health systems grew meaningfully: The percent of primary care physicians who remained independent dropped from 42% in 2013 to 31.5% in 2017, and the percent of independent specialists fell from 26% to 17%.

Over this same period, prices for physician services rose. Price increases were especially large – 12% for primary care physicians and 6% for specialists – when physicians joined health systems that had a high share of admissions in their area.

This study stands out for several reasons. First, it shows vertical integration drives up health care prices. Second, the authors highlight actions states can and are considering taking to monitor and curb vertical integration, including antitrust enforcement and enacting laws to promote competition.

Finally, the Massachusetts data allow the public to better appreciate what’s happening across the state. Many earlier studies on health care consolidation have been limited to a subset of insurers, physicians or patients. Massachusetts is a leader when it comes to creating and sharing its data thanks to its all-payer claims database, which pulls together all the health care bills from private insurers and public programs like Medicare and Medicaid in the state. This critical information helps to illuminate patterns of care and prices and connect them to issues like consolidation and competition.Neither the federal government nor most states track how vertical integration mergers influence health care prices.

As these findings demonstrate, acquisitions and other forms of vertical integration impact what people pay for health care services. Given that prices in this sector continue to climb, this paper underscores the need for more state and national data to understand the downstream effects on all of us who use and participate in the U.S. health care system.

The digital platform is designed to provide consumers with a coordinated healthcare experience across care settings. It’s being sold to Aetna’s fully insured and self-insured plan sponsors, as well as CVS Caremark clients, and is due to go live next year. According to CVS Health, the new offering “enables consumers to choose care when and where they want,” whether that’s virtually, in a retail setting (including at a MinuteClinic or HealthHUB), or through at-home services.

Patients will have access to primary care, on-demand care, medication management, chronic condition management, and mental health services, as well as help in identifying other in-network care providers.

The Gist: CVS Health has been working to integrate its retail clinics, care delivery assets, and health insurance business. This new virtual-first care platform is aimed at coordinating care and experience across the portfolio, and streamlining how individuals access the range of services available to them.

CVS is not alone in focusing here: UnitedHealth Group, Cigna, and others have announced virtual-first health plans with a similar value proposition. Any payer or provider who aims to own the consumer relationship must field a similar digital care platform that streamlines and coordinates service offerings, lest they find themselves in a market where many patients turn first to CVS and other disruptors for their care needs.

The momentum behind Medicare Advantage is only growing as more baby boomers age into eligibility, and experts don’t expect the energy around the program to slow down any time soon.

A recent analysis from the Kaiser Family Foundation found that a record 3,834 plans were available for the 2022 plan year in MA, which represents an 8% increase over 2021 and the largest number on the market in a decade.

Open enrollment for Medicare ended Dec. 7, and enrollment numbers will begin trickling out as the year winds down. In 2021, 26 million Medicare beneficiaries, or about 42% of those eligible for the program, were enrolled in an MA plan.

“As Medicare Advantage enrollment continues to grow, insurers seem to be responding by offering more plans and choices to the people on Medicare,” the KFF analysts said.

Part of the appeal of MA to an increasingly savvy consumer base is that it offers additional benefits beyond those afforded people in traditional Medicare, such as vision and dental coverage as well as supports for members’ social needs.

Sachin Jain, M.D., CEO of SCAN Health Plan, told Fierce Healthcare that people are increasingly shopping around for plans, building greater awareness of MA as a whole as well as of the different types of benefits beneficiaries could select.

“We’re seeing that consumers are more sophisticated today than they were a decade ago,” he said. “I think people are realizing that fee-for-service Medicare doesn’t cover a lot of things.”

The KFF report shows that more than 90% of non-group MA plans offer some kind of vision, hearing, telehealth or dental benefits and that most (89%) include prescription drug coverage as well.

Elena McFann, president of Medicare at Anthem, told Fierce Healthcare that throughout the open enrollment period, plans built with benefits that target the social determinants of health and promote whole-person care resonated strongly with members.

Anthem, for example, offers plans that include a slate of essential extra benefits that members can choose from based on what they need the most. Options include grocery cards, transportation benefits and in-home supports.

She said that the grocery benefits and flex cards that allow members to purchase additional hearing, vision and dental coverage have proven particularly popular in this enrollment season.

“What those all point to is the concept of flexibility and helping them lead healthier lives where they really need the help where they are in their journey,” McFann said.

As these benefits prove popular, an increasing number of plans are offering them in tandem. The Better Medicare Alliance released a survey late last month that found the number of plans including supplemental benefits grew by 43% for the 2022 plan year.

The Centers for Medicare & Medicaid Services (CMS) has issued additional flexibilities that allow MA plans to address members’ social determinants of health as the program’s enrollment continues to swell.

Jain said SCAN has seen similar interest in supplemental benefits, and that flexibility afforded to MA plans to adapt to seniors’ needs and expectations is a critical factor in the program’s success.

“When you’re in the business of serving seniors, a lot of what you have to do is anticipate needs that those seniors may not anticipate that they have, give them things they didn’t know they needed,” he said.

McFann said that beneficiaries value plans like these that unite brands they trust and recognize and that partners like Kroger enable insurers to more effectively meet seniors where they are. In its co-branded plans, members can access benefits like Healthy Grocery Cards and stipends to purchase over-the-counter health items.

She said that there has been significant “excitement” around those plans, which are available in four states, during the current enrollment period.

“It gives the Medicare eligibles a sense of familiarity and a sense of comfort, again meeting them on their terms,” McFann said.

However, while many established insurers have set ambitious growth targets in this market and new startups enter the space regularly, they still have plenty of work to do if they want to catch up with the market’s dominant forces: UnitedHealthcare, Humana and Blues plans.

UHC and Humana together account for 45% of the MA market in 2021, according to the KFF analysis. Humana offers plans in 85% of counties and UHC in 74% for 2022.

That means, 89% of Medicare eligibles have access to a Humana plan and 90% have access to a UHC MA plan if they choose, according to the report.

Competition is continuing to grow, though, and both McFann and Jain said they don’t feel the momentum around MA slowing down anytime soon.

“It is those extras and social drivers of health solutions that really have caught on with the Medicare-eligible segment and we expect to see that expand even further,” McFann said.

Everyone agrees that the US healthcare system is not working so great. Compared to the rest of the world, our healthcare is extremely expensive and yet we suffer worse health by many measures. And we can’t seem to agree on what’s to blame, or what we should do about it. Do we have too much, or not enough, competition? Should the government intervene in health care markets more or less?

Basic economics can help us better understand what’s happening.

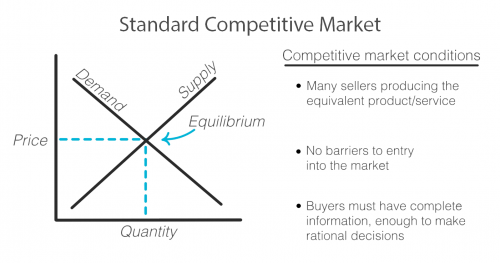

As with any exchange of goods and services, the standard competitive market model has the familiar upward sloping supply curve and downward sloping demand curve, illustrating that when prices are higher, demand decreases and supply increases as sellers are incentivized to produce more of that good or service at its higher price. Sellers and buyers arrive at what quantity to produce and consume and at what price based on where these two lines intersect, called the equilibrium. Both buyer and seller are happy with the deal they’ve struck!

But not every market works this way. There are actually standards that need to be met in order for a market to fit this model and for it to work efficiently for both the buyer and seller.

First, there must exist multiple sellers competing to sell the same goods or services and new sellers must be able to easily enter the market.

There must be a sufficient open exchange of information between buyer and seller about price, availability, and value of a service or good.

And buyers must make, or be in a position to make, rational decisions using the information they possess about the market.

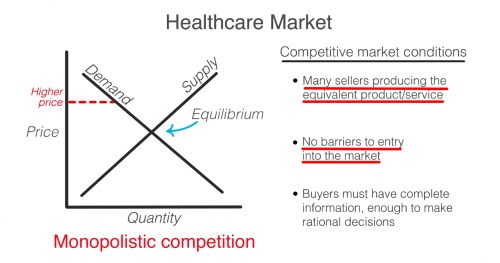

Healthcare does not meet these standards and when these standards are not met, the equilibrium cannot be reached or accurately known. Any price and quantity that falls outside of the equilibrium is considered a market failure. Using only this model, we can see how healthcare’s market failures contribute to high prices.

To start, it’s true that healthcare is failing the market standards when it comes to competition. The number of sellers in the market is decreasing due to both an increase in barriers to entry and due to consolidation, including hospital mergers. This causes an imbalance in power of the seller over the buyer that can begin to reflect what economists call monopolistic competition where sellers can charge a price above the perfect competition equilibrium. In the extreme, when there is only one seller, the market is a monopoly.

So then, don’t we just need more competition? Unfortunately, a lack of competition isn’t the only reason that healthcare fails the market standards.

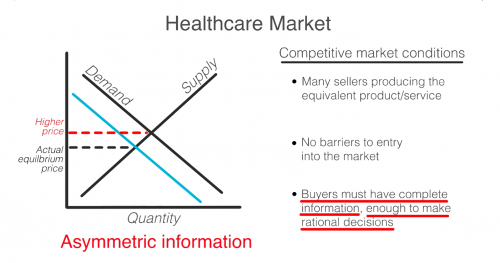

Another failure is that consumers in healthcare, patients, do not have all the information that providers, like doctors and hospitals, do. This is known as asymmetric information. Patients often have no idea before getting care how much it will cost, what the prices available to them elsewhere are, or what the quality will be. When consumers are in the dark about these basic features, the true demand and supply will be different than the model. The true demand may be lower if patients knew ahead of time how much it cost or how much less valuable the service is compared to how it is promoted. This means prices can be set higher than they likely would be if the true demand was known.

Even if patients had full information, they are not always in a position to act as rational consumers. A patient’s decision may be influenced by their concern for their health, or their ability to think rationally may itself be affected by their condition.

So, as you can see, the problem is that a lack of competition only accounts for part of the reason why healthcare doesn’t meet the market standards. No matter how much the government either steps back to allow for more competition or invests to foster competition, the market will never fix ALL of these failures on its own. Healthcare is not and can never be a free market. It simply does not fit this model.

In 1963, economist and later Nobel prize winner, Kenneth Arrow, warned us about this looming healthcare crisis. He explains that “If the actual market differs significantly from the competitive model […] coordination of purchases and sales must take place”

That coordination he is referring to is government intervention.

Dr. Mike Chernew, Health Economist and Professor of Health Policy at Harvard Medical School agrees…“an unregulated health care market is unlikely to lead to desired outcomes.”

In reality, health care always has, and always will, involve a combination of both government intervention and market forces to control prices and increase quality. The debate isn’t really whether or not the government should intervene, but by how much and in what way.

The combined health system will become the sixth largest nationwide, with $27B in revenue and 67 hospitals across six Midwest and Southeast states. The system will be based in Charlotte, and known as Advocate Health, though Atrium will continue to use its name in its markets.

Atrium CEO Gene Woods is slated to ultimately lead the combined entity, after an 18-month co-CEO arrangement with Advocate Aurora CEO Jim Skogsbergh. While the cross-market merger is unlikely to create antitrust concerns about increased pricing leverage, the Biden administration has been making noises about applying stricter scrutiny to the impact of health system consolidation on labor market competition.

The Gist: Earlier this year, Utah-based Intermountain Healthcare and Colorado-based SCL Health combined to create a 33-hospital, $14B health system, which became the 11th largest nationwide. While these mega-mergers of regional systems can realize cost savings from back-office synergies, there is a significant opportunity to create larger “platforms” of care to win consumer loyalty, deploy digital capabilities, attract talent, and become more desirable partners for nontraditional players like Amazon, Walmart, and One Medical.

It will be critical to watch whether the governance and cultural challenges that often hinder health system mergers come into play here. Advocate Aurora has had two prospective mergers fall apart in recent years, the first with Chicago-based NorthShore University HealthSystem, and the second with Michigan-based Beaumont Health (who subsequently finalized a merger with Spectrum Health earlier this year).

But the combination with Atrium is structured as a joint operating agreement, essentially creating a new superstructure atop the two legacy systems. This may allow the combined entity more flexibility in local decision-making, but the ultimate question will be how the combined entity will create value for consumers. Time will tell.