U.S. jobless claims set a more than 50-year low last week as the red-hot labor market shows few signs of cooling in the near-term.

The Labor Department released its latest weekly jobless claims report Thursday at 8:30 a.m. ET. Here were the main metrics from the print, compared to consensus estimates compiled by Bloomberg:

Initial jobless claims, week ended March 19: 187,000 vs.210,000 expected and a revised 215,000 during prior week

Continuing claims, week ended March 12: 1.350 millionvs.1.400 million expected and a revised 1.417 million during prior week

At 187,000, new jobless claims improved for a back-to-back week and reached the lowest level since September 1969. Continuing claims also fell further to reach 1.35 million — the least since January 1970.

The labor market has remained a point of strength in the U.S. economy, with job openings still elevated but coming down from record levels as more workers rejoin the labor force from the sidelines.

Going forward, however, some economists warned that new cases of the fast-spreading sub-variant of Omicron, known as BA.2, could at least temporarily disrupt mobility and economic activity across the country. As of this week, about one-third of COVID-19 cases in the U.S. have been attributed to the sub-variant, though overall new infections have still been trending down from January’s record high. The impact on the labor market — and on demand in the service sector especially — remains to be seen.

“Right now, U.S. cases are in the sweet spot between the bottom of the initial Omicron wave and the impending explosion in BA.2 cases, but this probably won’t last long,” Ian Shepherdson, chief economist at Pantheon Macroeconomics, wrote in a note this week. “Our bet … is that the coming BA.2 wave will trigger a modest but visible pull-back in the discretionary services sector, thereby dampening consumption in the first month of the second quarter.”

Still, many economists and policymakers have pointed out that the labor market withstood prior disruptions due to the Omicron wave earlier this year. Non-farm payrolls grew more than expected in each of January and February despite the outbreak.

And Federal Reserve Chair Jerome Powell reiterated his assessment of the labor market’s strength earlier this week, just days after calling the current job market “tight to an unhealthy level” in his post-Fed meeting press conference last week.

“The labor market has substantial momentum. Employment growth powered through the difficult Omicron wave, adding 1.75 million jobs over the past three months,” Powell said in a speech Monday. “By many measures, the labor market is extremely tight, significantly tighter than the very strong job market just before the pandemic.”

The tightness of the labor market has also strongly informed the Fed’s decisions in pressing ahead with tightening monetary policy, with the economy showing clear signs of strength and the ability to handle less accommodative financial conditions. Last week, the Fed raised interest rates by 25 basis points in its first rate hike since 2018. And St. Louis Fed President Jim Bullard, the lone dissenter of that decision who had called for a more aggressive 50 basis point rate hike last week, justified his vote in part given the strength of the U.S. labor market even in the face of decades-high rates of inflation.

“U.S. labor markets are today already stronger than they have been in a generation,” Bullard said in a statement.

Good morning. Here’s Axios chief economic correspondent Neil Irwin and markets correspondent Emily Peck with what you need to know about today’s surprising jobs numbers.

After days of doom-and-gloom talk about how bad the January jobs numbers would be due to the Omicron variant, they turned out to be, um, great?

Employers added 467,000 jobs last month, despite millions out sick.

Why it matters: It’s rare for any jobs numbers to be stunning, but these were. They leave little doubt that this remains a tight job market in which employers are doing everything they can to hold on to their workers.

The big picture: Some of the biggest job gains were in categories that have strong seasonal patterns, normally adding workers in the fall and then cutting those temporary workers in January.

But employers, desperate for staff, appear to have held onto those workers in greater numbers than in a normal year.

Due to the statistical process of seasonal adjustment, “cutting fewer workers than usual for this time of year” gets translated as “adding lots of jobs.”

By the numbers: Leisure and hospitality added 151,000 jobs; retail added 61,000; and transportation and warehousing added 54,000.

Between the lines: The report offered more evidence that this is an exceptionally tight labor market with inflationary pressures brewing, giving the Federal Reserve the green light for interest rate increases.

Average hourly earnings rose a robust 0.7%, and are up 5.7% over the last year. Employers are being forced to pay up to fill their job openings.

Yes, but: Omicron really did have an effect. The report said 6 million people were unable to work because their employers were closed or lost business due to the pandemic, up from 3.1 million in December.

What they’re saying: “Had the prior relationship between Covid cases and employment held true, 800k daily new Covid cases would have led to 2.3 million job losses,” Julia Pollak, chief economist at ZipRecuiter, tweeted. “Instead, we saw 467,000 job GAINS!”

The bottom line: This is an incredibly strong labor market that is poised to strengthen further as Omicron fades.

Many Americans, even those who don’t pay much attention to investing and the markets, know the name Warren Buffett.

Buffett, of course, is the billionaire philanthropist who created one of the greatest investment fortunes in history. Far fewer, however, know the name of his longtime business partner Charlie Munger.

And that’s a shame, because Munger is at least half the brains behind Berkshire Hathaway BRK.ABRK.B, the holding company he runs with Buffett and which manages billions and billions of investor dollars.

Munger turned 98 on Jan. 1. To celebrate his wit and market wisdom, here is a collection of quips from various interviews and question-and-answer sessions over the years.

On business education

Those of you who are about to enter business school, or who are there, I recommend you learn to do it our way. But at least until you’re out of school you have to pretend to do it their way.

On common sense

If people weren’t so often wrong, we wouldn’t be so rich.

On company earnings

Yeah, I think you would understand any presentation using the word EBITDA, if every time you saw that word you just substituted the phrase “bullsh** earnings.”

On a changing economy

So no, I’m optimistic about life. If I can be optimistic when I’m nearly dead, surely the rest of you can handle a little inflation.

On public spending

Everybody wants fiscal virtue but not quite yet. They’re like that guy who felt that way about sex. He was willing to give it up but not quite yet.

On legacy

Well, you don’t want to be like the motion picture executive in California. They said the funeral was so large because everybody wanted to make sure he was dead.

On stock buybacks

I think some people just buy it to keep the stock up. And that, of course, is insane. And immoral. But apart from that, it’s fine.

On marriage

Warren: Charlie is big on lowering expectations.

Munger: Absolutely. That’s the way I got married. My wife lowered her expectations.

On the purpose of money

Sure, there are a lot of things in life way more important than wealth. All that said…some people do get confused. I play golf with a man. He says: “What good is health? You can’t buy money with it.”

On money managers

The general system for money management requires people to pretend that they can do something that they can’t do, and to pretend to like it when they really don’t. I think that’s a terrible way to spend your life, but it’s very well paid.

On systematic investing

Well, I can’t give you a formulaic approach, because I don’t use one. If you want a formula you should go back to graduate school. They’ll give you lots of formulas that won’t work.

On human nature

As Samuel Johnson said, famously: “I can give you an argument, but I can’t give you an understanding.”

On financial innovation

It’s perfectly obvious, at least to me, that to say that derivative accounting in America is a sewer. is an insult to sewage.

On business competition

Competency is a relative concept. And what a lot of us needed to get ahead was to compete against idiots. And luckily there’s a large supply.

On cryptocurrency

I think the people who are professional traders that go into trading cryptocurrencies, it’s just disgusting. It’s like somebody else is trading turds and you decide, “I can’t be left out.”

On investment bankers

Once I asked a man who just left a large investment bank, and I said, “How does your firm make its money?” He said, “Off the top, off the bottom, off both sides, and in the middle.”

Over the past two years, historians and analysts have compared the coronavirus to the 1918 flu pandemic. Many of the mitigation practices used to combat the spread of the coronavirus, especially before the development of the vaccines, have been the same as those used in 1918 and 1919 — masks and hygiene, social distancing, ventilation, limits on gatherings (particularly indoors), quarantines, mandates, closure policies and more.

Yet, it may be that only now, in the winter of 2022, when Americans are exhausted with these mitigation methods, that a comparison to the 1918 pandemic is most apt.

The highly contagious omicron variant has rendered vaccines much less effective at preventing infections, thus producing skyrocketing caseloads. And that creates a direct parallel with the fall of 1918, which provides lessons for making January as painless as possible.

In February and March 1918, an infectious flu emerged. It spread from Kansas, through World War I troop and material transports, filling military post hospitals and traveling across the Atlantic and around the world within six months. Cramped quarters and wartime transport and industry generated optimal conditions for the flu to spread, and so, too, did the worldwide nature of commerce and connection. But there was a silver lining: Mortality rates were very low.

In part because of press censorship of anything that might undermine the war effort, many dismissed the flu as a “three-day fever,” perhaps merely a heavy cold, or simply another case of the grippe (an old-fashioned word for the flu).

Downplaying the flu led to high infection rates, which increased the odds of mutations. And in the summer of 1918, a more infectious variant emerged. In August and September, U.S. and British intelligence officers observed outbreaks in Switzerland and northern Europe, writing home with warnings that went largely unheeded.

Unsurprisingly then, this seemingly more infectious, much more deadly variant of H1N1 traveled west across the Atlantic, producing the worst period of the pandemic in October 1918. Nearly 200,000 Americans died that month. After a superspreading Liberty Loan parade at the end of September, Philadelphia became an epicenter of the outbreak. At its peak, nearly 700 Philadelphians died per day.

Once spread had begun, mitigation methods such as closures, distancing, mask-wearing and isolating those infected couldn’t stop it, but they did save many lives and limited suffering by slowing infections and spread. The places that fared best implemented proactive restrictions early; they kept them in place until infections and hospitalizations were way down, then opened up gradually, with preparations to reimpose measures if spread returned or rates elevated, often ignoring the pleas of special interests lobbying hard for a complete reopening.

In places in the United States where officials gave in to public fatigue and lobbying to remove mitigation methods, winter surges struck. Although down from October’s highs, these surges were still usually far worse than those in the cities and regions that held steady.

In Denver, in late November 1918, an “amusement” lobby — businesses and leaders invested in keeping theaters, movie houses, pool halls and other public venues open — successfully pressured the mayor and public health officials to rescind and then revise a closure order. This, in turn, generated what the Rocky Mountain News called “almost indescribable confusion,” followed by widespread public defiance of mask and other public health prescriptions.

In San Francisco, where resistance was generally less successful than in Denver, there was significant buy-in for a second round of masking and public health mandates in early 1919 during a new surge. But opposition created an issue. An Anti-Mask League formed, and public defiance became more pronounced. Eventually anti-maskers and an improving epidemic situation combined to end the “masked” city’s second round of mask and public health mandates.

The takeaway: Fatigue and removing mitigation methods made things worse. Public officials needed to safeguard the public good, even if that meant unpopular moves.

The flu burned through vulnerable populations, but by late winter and early spring 1919, deaths and infections dropped rapidly, shifting toward an endemic moment — the flu would remain present, but less deadly and dangerous.

Overall, nearly 675,000 Americans died during the 1918-19 flu pandemic, the majority during the second wave in the autumn of 1918. That was 1 in roughly 152 Americans (with a case fatality rate of about 2.5 percent). Worldwide estimates differ, but on the order of 50 million probably died in the flu pandemic.

In 2022, we have far greater biomedical and technological capacity enabling us to sequence mutations, understand the physics of aerosolization and develop vaccines at a rapid pace. We also have a far greater public health infrastructure than existed in 1918 and 1919. Even so, it remains incredibly hard to stop infectious diseases, particularly those transmitted by air. This is complicated further because many of those infected with the coronavirus are asymptomatic. And our world is even more interconnected than in 1918.

That is why, given the contagiousness of omicron, the lessons of the past are even more important today than they were a year ago. The new surge threatens to overwhelm our public health infrastructure, which is struggling after almost two years of fighting the pandemic. Hospitals are experiencing staff shortages (like in fall 1918). Testing remains problematic.

And ominously, as in the fall of 1918, Americans fatigued by restrictions and a seemingly endless pandemic are increasingly balking at following the guidance of public health professionals or questioning why their edicts have changed from earlier in the pandemic. They are taking actions that, at the very least, put more vulnerable people and the system as a whole at risk — often egged on by politicians and media figures downplaying the severity of the moment.

Public health officials also may be repeating the mistakes of the past. Conjuring echoes of Denver in late 1918, under pressure to prioritize keeping society open rather than focusing on limiting spread, the Centers for Disease Control and Prevention changed its isolation recommendations in late December. The new guidelines halved isolation time and do not require a negative test to reenter work or social gatherings.

Thankfully, we have an enormous advantage over 1918 that offers hope. Whereas efforts to develop a flu vaccine a century ago failed, the coronavirus vaccines developed in 2020 largely prevent severe illness or death from omicron, and the companies and researchers that produced them expect a booster shot tailored to omicron sometime in the winter or spring. So, too, we have antivirals and new treatments that are just becoming available, though in insufficient quantities for now.

Those lifesaving advantages, however, can only help as much as Americans embrace them. Only by getting vaccinated, including with booster shots, can Americans prevent the health-care system from being overwhelmed. But the vaccination rate in the country remains a relatively paltry 62 percent, and only a scant 1 in 5 have received a booster shot. And as in 1918, some of the choice rests with public officials. Though restrictions may not be popular, officials can reimpose them — offering public support where necessary to those for whom compliance would create hardship — and incentivize and mandate vaccines, taking advantage of our greater medical technology.

As the flu waned in 1919, one Portland, Ore., health official reflected that “the biggest thing we have had to fight in the influenza epidemic has been apathy, or perhaps the careless selfishness of the public.”

The same remains true today.

Vaccines, new treatments and century-old mitigation strategies such as masks, distancing and limits on gatherings give us a pathway to prevent the first six weeks of 2022 from being like the fall of 1918. And encouraging news about the severity of omicron provides real optimism that an endemic future — in which the coronavirus remains but poses far less of a threat — is near. The question is whether we get there with a maximum of pain or a minimum. The choice is ours.

First-time unemployment filings fell by 8,000 claims from the previous week’s reading, marking the second lowest print during the pandemic and signaling continued recovery in the labor market as high demand for workers pours into the new year.

The Labor Department released its latest report on initial and continuing claims on Thursday at 8:30 a.m. ET. Here were the main metrics from the print, compared to consensus estimates compiled by Bloomberg:

Initial jobless claims, week ended Dec. 25: 198,000 vs. 206,000 expected and upwardly revised to 206,000 during prior week

Continuing claims, week ended Dec. 18: 1.716 million vs. 1.875 million expected and downwardly revised to 1.856 million during prior week

The newest print brings the four-week moving average to 199,300 in the week ending Dec. 25, Bloomberg data reflected. Continuing claims dropped to a fresh pandemic low of 1.716 million. Forecast for this week’s jobless claims release ranged from 190,000-225,000 from 22 economists surveyed by Bloomberg.

First-time filings for unemployment remained below the 2019 average of 218,000, when the unemployment rate was at a half-century low of 3.5%, according to Bloomberg. The current unemployment rate is also expected to edge down to 4.1% in December as the labor market continues to tighten.

At 205,000, last week’s initial unemployment claims were on par with economist forecasts and below pre-pandemic levels yet again. Earlier in December, jobless claims fell sharply to 188,000, the lowest level since 1969. The prints serve an early indication of the relative strength expected to show in December’s jobs report, though the economic impact of the virus remains unclear.

“Fortunately, there’s no evidence in this data of a new wave of fresh job loss,” Bankrate senior economic analyst Mark Hamrick said, commenting on last week’s figures. “New claims are only slightly above the lowest point in decades notched a couple of weeks ago.”

“With so much uncertainty now and the high level of concern about the Omicron variant, we’ll take stability when we can get it,” Hamrick added.

“It’s stunning to see how much the rate has fallen in the last five months,” he told Yahoo Finance Live. “We expect that pace of decline to slow, but it doesn’t take much to get below 4%, even with a tick up in the labor participation rate, which has been depressed over the last year and a half.”

Record cases of COVID-19 may discourage workers from looking for work as U.S. households continue to cite fear of COVID or virus-related caretaking needs as reasons for staying out of the job market.

“The pandemic’s resurgence is affecting the economy,” Hamrick said in a note last week. “The question is for how long and how much, and it is too early to know the answers.”

Initial jobless claims, week ended Dec. 18: 205,000 vs. 205,000 expectedand a downwardly revised 205,000 during prior week

Continuing claims, week ended Dec. 11: 1.859 million vs. 1.835 million expected and an upwardly revised 1.867 million during prior week

This week’s new jobless claims report coincides with the survey week for the December monthly jobs report from the Labor Department, offering an early indication of the relative strength expected in that print due for release in early January.

At 205,000, initial unemployment claims were expected to come in below even pre-pandemic levels yet again, with jobless claims having averaged around 220,000 per week throughout 2019. Earlier this month, first-time unemployment filings fell sharply to 188,000, or the lowest level since 1969. And based on the latest report, the four-week moving average for new claims was near its lowest in 52 years, ticking up by 2,750 week-over-week to reach 206,250.

Continuing claims have also come down sharply from pandemic-era highs, albeit while remaining slightly above the 2019 average of about 1.7 million. This metric, which counts the total number of individuals claiming benefits across regular state programs, came in below 2 million for a fourth straight week and reached the lowest level since March 2020.

“The claims data indicate strong demand for workers and a reluctance by businesses to lay off workers,” Rubeela Farooqi, chief economist for High Frequency Economics, wrote in a note. “However, disruptions around Omicron and Delta could be a headwind if businesses have to close for health-related reasons.”

“Overall, the direction in the labor market recovery remains positive, with demand still strong,” she added. “Labor shortages are persisting, preventing a stronger recovery, although these appeared to ease somewhat in November.”

And indeed, policymakers have also taken note of the improving labor market situation. In a press conference last week, Federal Reserve Chair Jerome Powell maintained, “Amid improving labor market conditions and very strong demand for workers, the economy has been making rapid progress toward maximum employment.” And at the close of the Federal Open Market Committee’s latest policy-setting meeting, officials decided to speed their rate of asset-purchase tapering, paring back some crisis-era support in the economy as the recovery progressed.

Many Americans have also cited solid labor market conditions, especially as job openings hold at historically high levels. In the Conference Board’s latest Consumer Confidence report for December, 55.1% of consumers surveyed said jobs were “plentiful.” While this rate was down slightly from November’s 55.5%, it still represented a “historically strong reading,” according to the Conference Board.

The $1.7 trillion “social infrastructure” legislation passed by the House and now before the Senate would spur growth, expand employment and boost productivity with limited inflationary impact, according to Moody’s Investors Service.

The spending “would occur over 10 years, include significant revenue-raising offsets and would likely only start to flow into the economy later in 2022 at a time when inflationary pressures from disruptions to global supply chains and U.S. labor supply will likely have diminished,” Moody’s Vice President-Senior Analyst Rebecca Karnovitz said.

“Investments in childcare, education and workforce development have the potential to boost labor force participation and increase productivity over the medium and longer term,” she said. While the Senate will likely insist on amendments, the Build Back Better (BBB) bill currently would invest $555 billion in clean energy and “climate resilience” and $585 billion in childcare, universal prekindergarten and paid family leave.

Dive Insight:

CFOs concerned about rising prices and the risk of a wage-price spiral have found sympathy from some lawmakers who warn that the $5.7 trillion in spending Congress has already approved during the pandemic will further stoke inflation.

“Inflation is hammering working families across America,” Senate Minority Leader Mitch McConnell told the chamber last week. The Kentucky Republican called BBB a “socialist wish list” and an inflationary “taxing and spending spree.”

Some Democrats — including Sens. Kyrsten Sinema of Arizona and Joe Manchin of West Virginia — have cautioned that excessive spending could push up prices and worsen the fiscal outlook.

Sinema and Manchin have said that they want less costly legislation. With Democrats holding the smallest possible Senate majority, support from the two senators is essential for final passage of the bill.

“I have been concerned about high levels of spending that are not targeted or are not efficient and effective,” Sinema told the Washington Post on Nov. 18 while noting rising inflation.

“The threat posed by record inflation to the American people is not ‘transitory’ and is instead getting worse,” Manchin said on Twitter this month after the Labor Department reported that consumer prices rose 6.2% in October on an annual basis.

CFOs face even higher price gains for wholesale goods. The producer price index for final demand, a measure of what suppliers charge, soared 8.6% in October from the prior year, according to the Labor Department. That was a record jump in a series of data first published in 2010.

The Moody’s analysis suggests that concerns about the impact of BBB on inflation and the U.S. fiscal outlook may be overblown.

“We expect the spending package to have a limited impact on inflation,” Moody’s said.

Referring to the U.S. credit outlook, Moody’s said, “we expect the legislation to have only a small effect on the sovereign’s fiscal position, given that the spending would be spread over a decade and the revenue-raising measures would help offset the impact on federal budget deficits.”

The Congressional Budget Office estimates that the House version of BBB would push up fiscal deficits by $367 billion over a 10-year period.

Yet the estimate excludes about $200 billion in revenue that would come from a provision in the bill funding tougher tax enforcement and collection, Moody’s said.

“Estimates of the bill’s impact on the deficit are likely to shift in accordance with provisions that may be stripped from the Senate’s final version of the legislation,” according to Moody’s.

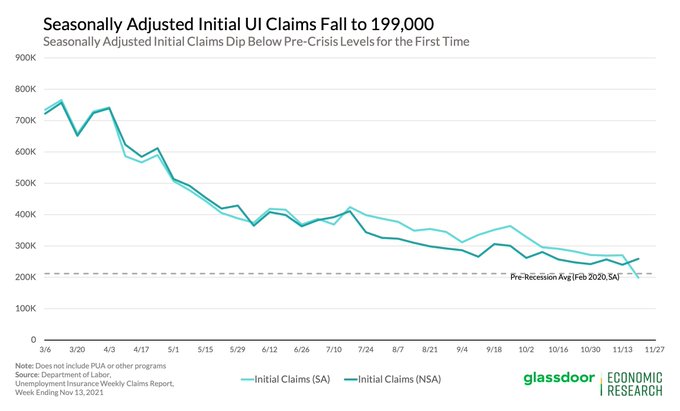

For the 1st time during the pandemic, initial UI claims have dipped below pre-crisis levels, falling to 199,000 (vs the Feb 2020 avg: 211,700). Layoffs are hitting new lows amid ongoing labor shortages as employers look to hold onto hard-to-find workers.

New weekly claims for jobless aid plunged to the lowest level in more than 50 years last week, according to data released Wednesday by the Labor Department.

In the week ending Nov. 20, there were 199,000 initial applications for unemployment insurance, according to the seasonally adjusted figures, a decline of 71,000 from the previous week. Claims fell to the lowest level since November 1969 and are now well below the pre-pandemic trough of 225,000 applications received the week of March 14, 2020.

The steep drop in unemployment applications comes after several strong months of job growth and rising consumer spending heading into the holiday shopping season. While high inflation has stressed many household budgets, U.S. job growth, economic production, stock values and corporate profits have all steamed ahead.

“Getting new claims below the 200,000 level for the first time since the pandemic began is truly significant, portraying further improvement,” said Mark Hamrick, chief economic analyst at Bankrate.com.

“The strains associated with higher prices, shortages of supplies and available job candidates are weighed against low levels of layoffs, wage gains and a falling unemployment rate,” he continued. “Growth will likely be above par for the foreseeable future, but within the context of historically high inflation which should relax its grip on the economy to some degree in the year ahead.”

The U.S. added 531,000 jobs in October and job growth in the previous months was revised substantially higher after a string of what first appeared to be meager gains. While businesses have struggled to hire enough workers to meet surging consumer demand, the decline in jobless claims appears to be a sign of an improving labor market.

“Layoffs are hitting new lows amid ongoing labor shortages as employers look to hold onto hard-to-find workers,” said Daniel Zhao, senior economist at Glassdoor, in a Wednesday thread on Twitter.

Even so, Zhao said the sharp decline below pre-pandemic levels may have been due to a lower than expected seasonal impact on hiring.

“As you can see from the above chart, this is in part due to the seasonal adjustment expecting a much larger jump in non-seasonally adjusted claims, so this dip below pre-crisis levels may be short-lived,” he explained.

The job market added a stunning 531,000 jobs last month. The unemployment rate ticked down to 4.6% — a new pandemic-era low.

Why it matters: America’s job market recovery has been on track all along.

Between the lines: Revisions to prior months are often overlooked. Not this month: Upgrades to both August and September were so enormous — fully 366,000 jobs higher than originally reported — that they have definitively reversed the narrative that there was a Delta-induced hiring slump in late summer.

By the numbers:America has now recovered 80% of the jobs lost at the depth of the recession in 2020.

The big picture: Leisure and hospitality added 164,000 jobs last month — but jobs growth was widespread. The disappointment — again — came in public sector education. State and local education shed a combined 65,000 jobs.

Wages are still rising: Average hourly earnings rose another 11 cents an hour in October, to $30.96. That’s enough to keep up with inflation.

What to watch: Millions of workers remain on the sidelines — and there wasn’t much improvement in pulling them back into the workforce.

The bottom line: “The Fall hiccup is now at best a Fall deep breath,” tweeted University of Michigan economist Justin Wolfers.

The delta variant of the coronavirus is sweeping through the United States, raising the average number of cases to 30,000-per-day, crowding hospitals in areas with large number of unvaccinated people and spurring questions about the nation’s recovery from the pandemic.

Stocks tanked on Monday, with the Dow Jones Industrial average dropping 725 points after being down more than 900 points at one time.

It was the worst one-day performance in the Dow since last October, and followed losses in markets around the world as investor fears about how the delta virus might slow both the health and economic recovery took hold.

Health officials have described the latest stage of the coronavirus as a pandemic of the unvaccinated while emphasizing that those who have had their shots are relatively safe.

Yet Los Angeles County on Saturday reinstated a mask mandate for indoor public settings, a sign that local communities may decide to reimpose restrictions as a safety measure.

An Olympic gymnast and an Olympic women’s basketball player both announced they had tested positive as they prepared for the Games, which is being held in a state of emergency in Tokyo where the rate of vaccinations is behind the United States.

Canada had also been well behind the U.S. in its vaccination rate but surpassed its southern neighbor on Monday, a sign of how much more slowly the vaccination rate now is in the United States. A big reason is that many people who are unvaccinated do not want to get the vaccine, something the Biden administration has increasingly blamed on social media and some conservative media outlets.

While the 30,000 cases per day on average is more than double the 13,000 average at the end of June, that rate is still well below highs from last fall and earlier this year.

Still, deaths are also ticking back up, at around 240 per day.

Because vaccinated people are still overwhelmingly protected, especially from severe outcomes, case and death numbers are likely to stay well below the worst of last winter’s surges, before vaccines were widely available.

But unvaccinated people are at increasing risk, especially given the rise of the highly transmissible delta variant, and the vaccination campaign is hitting a wall, leaving more than 30 percent of adults without any shots and exposed to the full dangers of the virus.

States with lower vaccination rates are seeing the worst outbreaks. Arkansas, Missouri, Florida and Louisiana are the four states with the highest per capita new cases per day, according to data from the Covid Act Now tracking site. The percentage of the population with at least one shot in those states is 44 percent, 47 percent, 56 percent, and 40 percent, respectively.

In contrast, Vermont and Massachusetts, where the vaccination rate is over 70 percent, are faring much better.

Vaccine resistance among some leading conservative commentators and lawmakers is raising fears that many of the remaining unvaccinated may never get the shots.

Sten Vermund, a professor at the Yale School of Public Health, said he is “not particularly worried” about COVID-19 for himself, because he is fully vaccinated.

“What worries me is my fellow Americans who for a variety of reasons choose not to get vaccinated; they continue to be in harm’s way,” Vermund said.

In the rare instances where vaccinated people do get COVID-19 cases, symptoms are likely to be much milder.

CDC Director Rochelle Walensky said Friday that 97 percent of people entering the hospital with COVID-19 are unvaccinated, part of why she said it “is becoming a pandemic of the unvaccinated.”

Conservative resistance to vaccination is stiffening. A Washington Post-ABC News poll released earlier this month found that 47 percent of Republicans said they were unlikely to get vaccinated, compared to just six percent of Democrats. Among Republicans, 38 percent said they definitely would not get the shots.

Former President Trump has previously encouraged people to get vaccinated, though he has not made a forceful push, for example by recording a public service announcement or getting his own shots in public.

On Sunday, though, Trump appeared to justify people not taking the vaccine, blaming President Biden.

“He’s way behind schedule, and people are refusing to take the Vaccine because they don’t trust his Administration, they don’t trust the Election results, and they certainly don’t trust the Fake News, which is refusing to tell the Truth,” Trump said in a statement.

Asked if Biden would request Trump film a public service announcement on vaccination, White House press secretary Jen Psaki said “we don’t believe that requires an embroidered invitation to be a part of.”

“Certainly any role of anyone who has a platform where they can provide information to the public that the vaccine is safe, it is effective, we don’t see this as a political issue,” Psaki said. “We’d certainly welcome that engagement.”

She also emphasized, though, that the administration is focusing on local doctors and community leaders to try to boost vaccination rates, not national officials.

The effort is hitting its limits, though. The pace of vaccinations has fallen to around 500,000 per day, down from over 3 million at the peak in April, according to Our World in Data.

“I’m not that hopeful that we’re going to get to people who have refused to be vaccinated,” said Preeti Malani, an infectious disease expert at the University of Michigan.

Experts increasingly say the best remaining hopes of reaching the remaining unvaccinated are school and employer mandates for their workers or students to get vaccinated.

France is experiencing a surge in vaccinations after President Emmanuel Macron announced this month that proof of vaccination, or a negative test, would be required for everyday activities like going to restaurants. The Biden administration has repeatedly ruled out a national vaccine passport in the U.S., though, and Republicans have rebelled against the idea.

Full approval of the vaccines from the Food and Drug Administration, as opposed to the current emergency authorization, could also help assuage some people’s fears, and some experts have called on the FDA to move faster on issuing a full approval.

The Biden administration has stepped up its calls for Facebook and other technology companies to do more to fight vaccine misinformation on their platforms.

Biden on Friday said social media companies are “killing people” with misinformation. On Monday, though, he dialed the criticism back down, instead pointing to 12 people responsible for much of the disinformation.

“Facebook isn’t killing people, these 12 people are out there giving misinformation,” Biden said.

“My hope is that Facebook, instead of taking it personally, that somehow I’m saying Facebook is killing people, that they would do something about the misinformation, the outrageous misinformation about the vaccine,” Biden added. “That’s what I meant.”

For its part, Facebook said over the weekend, before Biden’s walk-back, that the administration was “finger pointing” and the company was not the reason the president’s goal of getting 70 percent of adults at least one shot by July 4 was missed.

Los Angeles County’s move to return to an an indoor mask mandate, even for vaccinated people,

got mixed reviews from experts, but either way, it is unlikely to be replicated in places that are the hardest hit, given that places that are resistant to vaccines tend to also be resistant to masks.

“Vaccines are really the only way out,” Malani said. “We can’t live in masks forever.”