In the graphic above, we use the most recent data from software and analytics firm Strata Decision Technology to compare 2023 year-to-date (YTD) hospital volumes by admission type to both 2019 and 2022 volumes.

Compared to 2019, outpatient volumes in 2023 have increased by 14 percent, whileinpatient, observation, and emergency (ED) admissions are all down.However, compared to 2022, the reverse trend is true, with inpatient, observation, and ED volumes up from last year while outpatient volumes have dropped slightly.

This suggests that the net increase in outpatient volume and net loss in inpatient and ED volume over the past few years appears to be locked in. While the COVID-accelerated outpatient shift is here to stay, hospitals can take solace in the recent uptick in inpatient, observation, and ED volumes, which helps those still struggling to return to positive operating margins.

Importantly, there is significant regional variability among these volume data, suggesting that health system recovery will not be uniform.

Last week the Minnesota legislature passed a bill to initiate the creation of a public option health insurance plan available to state residents of all incomes. The bill funds an actuarial analysis of the policy and requires the state to apply for a Centers for Medicare and Medicaid Services (CMS) waiver to begin implementation by 2027. The public option plan will build upon MinnesotaCare, a state health plan currently covering residents with incomes below 200 percent of the federal poverty line.

The Gist: Minnesota joins Washington, Colorado, and Nevada as the fourth state to authorize a public option health plan. But unlike these other three states, whose public option programs rely on private payers to manage risk and administration with tighter price controls, Minnesota intends to create a “true” public option in which the government competes directly with private payers.

Analysis funded by a hospital and insurance trade group found that a public option could reduce Minnesota hospital revenues by more than $2B over 10 years, while only lowering the uninsured rate by half a percentage point.

Though Minnesota lawmakers were more concerned with lowering healthcare spending and improving health insurance affordability for state residents, the success of the program will depend in part on how it negotiates with providers, who justifiably fear a worsening payer mix that further threatens margins.

On Monday, Minnetonka, MN-based UHG’s Optum division made a $3.3B all-cash offer to acquire Baton Rouge, LA-based Amedisys, one of the country’s largest home health companies.

Optum’s bid came several weeks after Bannockburn, IL-based Option Care Health, a home health company specialized in drug and infusion services, offered to purchase Amedisys in an all-stock transaction valued at $3.6B. Amedisys itself acquired hospital-at-home company Contessa Health for $250M in 2021. While its Board of Directors is now evaluating whether UHG has made a “Superior Proposal”, a UHG acquisition of Amedisys would likely be subject to significant regulatory oversight, as the payer recently closed on its purchase of home health company and Amedisys-competitor LHC Group in a deal that was heavily scrutinized by the Federal Trade Commission.

The Gist: UHG, the nation’s largest health insurer, is on a tear to bring the country’s largest home health providers under its Optum umbrella—and it has the deep pockets to outbid nearly anyone else trying to do the same.

While some questioned the value of an Option Care-Amedisys combination, UHG would get to plug another asset into its scaled continuum of home-based care, allowing it to steer beneficiaries away from high-cost post acute care and continue to increase profitable intercompany eliminations.

If UHG’s bid for Amedisys is accepted, it would also gain its first hospital-at-home asset in Contessa, providing it with the opportunity to fully redirect—and reduce—its inpatient care spend.

At the end of a meeting last week with a health system executive team, the system’s COO asked us a question: “Your concept of a consumer-focused health system centered around treating patients as members describes exactly how we want to relate to our patients, but we’re not sure about the timing. Could you give us a list of the ‘no regrets’ investments you’d recommend for health systems looking to do this?”

We frequently get asked about “no regrets” strategies:

decisions or investments that will be accretive in both the current fee-for-service system as well as a future payment and operational model oriented around consumer value. The idea is understandably appealing for systems concerned about changing their delivery model too quickly in advance of payment change. And there is a long list of strategies that would make a system stronger in both fee-for-service and value: cost reduction, value-driven referral management, and online scheduling, just to name a few.

But as we pointed out, the decision to pursue only the no-regrets moves is a clear signal that the organization’s strategy is still tied to the current payment model.

If the system is truly ready to change, strategy development should start with identifying the most important investments for delivering consumer value. It’s fine to acknowledge that a health system is not yet ready, but we cautioned the team that they should not rely on the external market to provide signals for when they should undertake real change in strategy.

External signals—from payers, competitors, or disruptors—will come too slowly, or perhaps never. At some point, the health system should be prepared to lead innovation, introduce a new model of value to the market, and define and promote the incentives to support it.

Real change will require disruption of parts of the current business and cannot be accomplished with “no-regrets investments” alone.

On April 1st, Medicaid’s pandemic-era continuous enrollment policy began to sunset, kicking off a 14-month window for states to reassess their Medicaid rolls. In this week’s graphic, we highlight new Congressional Budget Office projections showing the impact of Medicaid redeterminations on insurance coverage rates over the next decade for the under-65 population.

The Medicaid and Children’s Health Insurance Program (CHIP) coverage rate is expected to drop from 31 percent of all Americans under 65 in 2023, to 27 percent in 2024.

Meanwhile, after reaching an all-time low in 2023,the under-65 uninsured rate is projected to surpass nine percent in 2024 and climb to over 10 percent by 2033.

While over 15M Americans are expected to lose Medicaid coverage during redeterminations, a majority of those disenrolled will gain health insurance either through an employer-sponsored or non-group plan.

But over 6M people, nearly 40 percent of those losing Medicaid coverage, are projected to become uninsured, erasing nearly half the progress the country has made since 2019 at lowering the uninsured rate.

A number of hospitals and health systems are trimming their workforces or jobs due to financial and operational challenges.

Below are workforce reduction efforts or job eliminations that were announced within the past 10 months and/or take effect later this year.

1. Dartmouth Health is laying off 75 workers and eliminating 100 job vacancies. The layoffs came after the Lebanon, N.H.-based health system implemented a performance improvement plan in November.

2. Seattle Children’s is eliminating 135 leader roles, citing financial challenges. The management restructuring and reduction affects 1.5 percent of employees across the organization.

3. White Rock (Texas) Medical Centerlaid off 30 workers across 28 departments. The layoffs include clinical and administrative roles.

4. Jackson, Miss.-based St. Dominic Health Services is laying off 157 workers and ending behavioral health services. The reduction represents 5.5 percent of the hospital’s workforce.

5. Danville, Pa.-based Geisingerlaid off 47 employees from its IT department. The reduction is part of a restructuring plan to offset high labor and supply costs.

6. Cascade Behavioral Health Hospital in Tukwila, Wash., is winding down operations and laying off 288 employees. The 137-bed psychiatric facility is slated to close by July 31.

7. Cambridge (Mass.) Health Alliance is laying off 69 employees, reducing the hours of 15 others and eliminating 170 open positions, according to The Boston Globe. The reductions are primarily in management, administrative and support areas, a health system spokesperson told Becker’s.

8. Wenatchee, Wash.-based Confluence Health has eliminated its chief operating officer amid restructuring efforts and financial pressures, the health system confirmed to Becker’s May 16.

9. Conemaugh Memorial Medical Center, a Duke LifePoint hospital in Johnstown, Pa., has laid off less than 1 percent of its workforce, the hospital confirmed to Becker’s May 15.

10. Community Health Network, a nonprofit health system based in Indianapolis, plans to cut an unspecified number of jobs as it restructures its workforce and makes organizational changes. The health system confirmed the job cuts in a statement shared with Becker’s on May 11. It did not say how many jobs would be cut or which positions would be affected.

11. New Orleans-based Ochsner Healtheliminated 770 positions, or about 2 percent of its workforce, on May 11. This is the largest layoff to date for the health system.

12. Cedars-Sinai Medical Center eliminated the positions of 131 employees and cut about two dozen other jobs at related Cedars-Sinai facilities, a spokesperson confirmed via a statement shared with Becker’s May 7. The Los Angeles-based organization said reductions represent less than 1 percent of the workforce and apply to management and non-management roles primarily in non-patient care jobs.

13. Rochester (N.Y.) Regional Health is eliminating about 60 positions. A statement from RRH said the changes affect less than one-half percent of the system population, mostly in nonclinical and management positions.

14. Memorial Health Systemlaid off fewer than 90 people, or less than 2 percent of its workforce.The Gulfport, Miss.-based health system said May 2 that most of the affected positions are nonclinical or management roles, and the majority do not involve direct patient care.

15. Monument Health laid off at least 80 employees, or about 2 percent of its workforce. The Rapid City, S.D.-based system said positions are primarily corporate service roles and will not affect patient services. Unfilled corporate service positions were also eliminated.

16. Habersham Medical Center in Demorest, Ga.,laid off four executives. The layoffs are part of cost-cutting measures before the hospital joins Gainesville-based Northeast Georgia Health System in July, nowhaberbasham.com reported April 27.

17. Scripps Health is eliminating 70 administrative roles, according to WARN documents filed by the San Diego-based health system in March. The layoffs take effect May 8 and affect corporate positions in San Diego and La Jolla, Calif.

18. Trinity Health Mid-Atlantic, part of Livonia, Mich.-based Trinity Health, eliminated fewer than 40 positions, a spokesperson confirmed to Becker’s April 24. The layoffs represent 0.5 percent of the health system’s approximately 7,000-person workforce.

19. PeaceHealth eliminated 251 caregiver roles across multiple locations. The Vancouver, Wash.-based health system said affected roles include 121 from Shared Services, which supports its 16,000 caregivers in Washington, Oregon and Alaska.

20. Toledo, Ohio-based ProMedica plans to lay off 26 skilled nursing support staff. The layoffs, effective in June, affect 20 employees who work remotely across the U.S, and six who work at the ProMedica Summit Center in Toledo, according to a Worker Adjustment and Retraining Notification filed April 18. Most affected positions support sales, marketing and administrative functions for the skilled nursing facilities, Promecia told Becker’s.

21. Northern Inyo Healthcare District, which operates a 25-bed critical access hospital in Bishop, Calif., anticipates eliminating about 15 positions, or less than 4 percent of its 460-member workforce, by April 21, a spokesperson confirmed to Becker’s. The layoffs include nonclinical roles within support and administration, according to a news release. No further details were provided about specific positions affected.

22. West Reading, Pa.-based Tower Health is eliminating 100 full-time equivalent positions. The move will affect 45 individuals, according to an April 13 news release the health system shared with Becker’s. The other 55 positions are either recently vacated or involve individuals who plan to retire in the coming weeks and months.

23. Grand Forks, N.D.-based Altru Health is trimming its executive team as its new hospital project moves forward. The health system is trimming its executive team from nine to six and incentivizing 34 other employees to take early retirement.

24. Tacoma, Wash.-based Virginia Mason Franciscan Healthlaid off nearly 400 employees, most of whom are in non-patient-facing roles. The job cuts affected less than 2 percent of the health system’s 19,000-plus workforce.

25. Katherine Shaw Bethea Hospital in Dixon, Ill., will lay off 20 employees, citing financial headwinds affecting health organizations across the U.S. It will also leave other positions unfilled to reduce expenses amid rising labor and supply costs and reductions in payments by insurance plans. Affected employees largely work in administrative support areas and not direct patient care.

26. Danbury, Conn.-based Nuvance Health will close a 100-bed rehabilitation facility in Rhinebeck, N.Y., resulting in 102 layoffs. The layoffs are effective April 12, according to the Daily Freeman.

27. Charleston, S.C.-based MUSC Health University Medical Centerlaid off an unspecified number of employees from its Midlands hospitals in the Columbia, S.C. area. Division President Terry Gunn also resigned after the facilities missed budget expectations by $40 million in the first six months of the fiscal year, The Post and Courier reported March 30.

28. Winston-Salem, N.C.-based Novant Healthlaid off about 50 workers, including C-level executives, the health system confirmed to Becker’s March 29. The layoffs affected Jesse Cureton, the health system’s executive vice president and chief consumer officer since 2013; Angela Yochem, its executive vice president and chief transformation and digital officer since 2020; and Paula Dean Kranz, vice president of innovation enablement and executive director of the Novant Health Innovation Labs.

29. Penn Medicine Lancaster (Pa.) General Health eliminated fewer than 65 jobs, or less than 1 percent of its workforce of about 9,700, the health system confirmed to Becker’s March 30. The layoffs include support, administrative and executive roles, and COVID-19-related support staff, spokesperson John Lines said, according to lancasteronline.com. Mr. Lines did not provide a specific number of affected workers.

30. McLaren St. Luke’s Hospital in Maumee, Ohio, will lay off 743 workers, including 239 registered nurses, when it permanently closes this spring. Other affected roles include physical therapists, radiology technicians, respiratory therapists, pharmacists and pharmacy support staff, and nursing assistants. The hospital’s COO is also affected, and a spokesperson for McLaren Health Care told Becker’s other senior leadership roles are also affected.

31. Bellevue, Wash.-based Overlake Medical Center and Clinicslaid off administrative staff, the health system confirmed to the Puget Sound Business Journal. The layoffs, which occurred earlier this year, included 30 workers across Overlake’s human resources, information technology and finance departments, a spokesperson said, according to the publication. This represents about 6 percent of the organization’s administrative workforce. Overlake’s website says it employs more than 3,000 people total.

32. Columbia-based University of Missouri Health Care is eliminating five hospital leadership positions across the organization, spokesperson Eric Maze confirmed to Becker’s March 20. Mr. Maze did not specify which roles are being eliminated saying that the organization won’t address individual personnel actions. According to MU Health Care, the move is a result of restructuring “to better support patients and the future healthcare needs of Missourians.”

33. Greensboro, N.C.-based Cone Healtheliminated 68 senior-level jobs. The job eliminations occurred Feb. 21, Cone Health COO Mandy Eaton told The Alamance News. Of the 68 positions eliminated, 21 were filled. Affected employees were offered severance packages.

34. The newly merged Greensburg, Pa.-based organization made up of Excela Health and Butler Health Systemeliminated 13 filled managerial jobs. The affected employees and positions are from across both sides of the new organization, Tom Chakurda, spokesperson for the Excela-Butler enterprise, confirmed to Becker’s. The positions were in various support functions unrelated to direct patient care.

35. Crozer Health, a four-hospital system based in Upland, Pa., is laying off roughly 215 employees amid financial challenges. The system announced the layoffs March 15 as part of its “operational restructuring plan” that “focuses on removing duplication in administrative oversight and discontinuing underutilized services.” Affected employees represent about 4 percent of the organization’s workforce.

36. Philadelphia-based Penn Medicine is eliminating administrative positions. The change is part of a reorganization plan to save the health system $40 million annually, the Philadelphia Business Journal reported March 13. Kevin Mahoney, CEO of the University of Pennsylvania Health System, told Penn Medicine’s 49,000 employees last week that changes include the elimination of a “small number of administrative positions which no longer align with our key objectives,” according to the publication. The memo did not indicate the exact number of positions that were eliminated.

37. Sovah Health, part of Brentwood, Tenn.-based Lifepoint Health, eliminated the COO positions at its Danville and Martinsville, Va., campuses. The responsibilities of both COO roles will now be spread across members of the existing administrative team.

38. Valley Health, a six-hospital health system based in Winchester, Va., eliminated 31 administrative positions. The job cuts are part of the consolidation of the organization’s leadership team and administrative roles.

39. Marshfield (Wis.) Clinic Health System said it would lay off 346 employees, representing less than 3 percent of its employee base.

41. Roseville, Calif.-based Adventist Health plans to go from seven networks of care to five systemwide to reduce costs and strengthen operations. The reorganization will result in job cuts, including reducing administration by more than $100 million.

42. Arcata, Calif.-based Mad River Community Hospital is cutting 27 jobs as it suspends home health services.

43. Hutchinson (Kan.) Regional Medical Center laid off 85 employees, a move tied to challenges in today’s healthcare environment.

44. Oklahoma City-based OU Healtheliminated about 100 positions as part of an organizational redesign to complete the integration from its 2021 merger.

45. Memorial Sloan Kettering Cancer Center announced it would lay off to reduce costs amid widespread hospital financial challenges. The layoffs are spread across 14 sites in New York City, and equate to about 1.8 percent of Memorial Sloan’s 22,500 workforce.

46. St. Louis-based Ascensioncompleted layoffs in Texas, the health system confirmed in January. A statement shared with Becker’s says the layoffs primarily affected nonclinical support roles. The health system declined to specify to Becker’s the number of employees or positions affected.

48. Chillicothe, Ohio-based Adena Health System announced it would eliminate 69 positions — 1.6 percent of its workforce — and send 340 revenue cycle department employees to Ensemble Health Partners’ payroll in a move aimed to help the health system’s financial stability.

49. Ascension St. Vincent’s Riverside in Jacksonville, Fla., will end maternity care at the hospital, affecting 68 jobs, according to a Workforce Adjustment and Retraining Notification filed with the state Jan. 17. The move will affect 62 registered nurses as well as six other positions.

50. Visalia, Calif.-based Kaweah Health said it aimed to eliminate 94 positions as part of a new strategy to reduce labor costs. The job cuts come in addition to previously announced workforce reductions; the health system already eliminated 90 unfilled positions and lowered its workforce by 106 employees.

51. Oklahoma City-based Integris Health said it would eliminate 200 jobs to curb expenses. The eliminations include 140 caregiver roles and 60 vacant jobs.

52. Toledo, Ohio-based ProMedica announced plans to lay off 262 employees, a move tied to its exit from a skilled-nursing facility joint venture late last year. The layoffs will take effect between March 10 and April 1.

53. Employees at Las Vegas-based Desert Springs Hospital Medical Center were notified of layoffs coming to the facility, which will transition to a freestanding emergency department. There are 970 employees affected. Desert Springs is part of the Valley Health System, a system owned and operated by King of Prussia, Pa.-based Universal Health Services.

54. Philadelphia-based Jefferson Health plans to go from five divisions to three in an effort to flatten management and become more efficient. The reorganization will result in an unspecified number of job cuts, primarily among executives.

55. Pikeville (Ky.) Medical Center said it would lay off 112 employees as it outsources its environmental services department. The 112 layoffs were effective Jan. 1, 2023.

56. Southern Illinois Healthcare, a four-hospital system based in Carbondale, announced it would eliminate or restructure 76 jobs in management and leadership. The 76 positions fall under senior leadership, management and corporate services. Included in that figure are 33 vacant positions, which will not be filled. No positions in patient care are affected.

57. Citing a need to further reduce overhead expenses and support additional investments in patient care and wages, Traverse City, Mich.-based Munson Health said it would eliminate 31 positions and leave another 20 jobs unfilled. All affected positions are in corporate services or management. The layoffs represent less than 1 percent of the health system’s workforce of nearly 8,000.

58. West Reading, Pa.-based Tower Health on Nov. 16 laid off 52 corporate employees as the health system shrinks from six hospitals to four. The layoffs, which are expected to save $15 million a year, account for 13 percent of Tower Health’s corporate management staff.

59. Sioux Falls, S.D.-based Sanford Healthannounced layoffs affecting an undisclosed number of staff in October, a decision its CEO said was made “to streamline leadership structure and simplify operations” in certain areas. The layoffs primarily affect nonclinical areas.

60. St. Vincent Charity Medical Center in Clevelandclosed its inpatient and emergency room care Nov. 11, four days before originally planned — and laid off 978 workers in doing so. After the transition, the Sisters of Charity Health System will offer outpatient behavioral health, urgent care and primary care.

Minneapolis-based Allina Health System’s move to turn away patients with outstanding debt is a cost-saving measure is not uncommon, according to the Lown Institute.

Allina provides emergency care to indebted patients, but they can be cut off for other services if they have a certain amount of unpaid debt,The New York Times found. A spokesperson for Allina confirmed to the Times that it cut off patients only if they have at least $1,500 of unpaid debt three separate times.

A 2022 investigation from KFF Health News found 55 hospitals allow denials of nonemergency care for patients with medical debt, and 22 said the practice is allowed but not current practice.

Allina’s refusal of care for indebted patients could contribute to medical debt, the Lown Institute said in a June 2 report. Allina is a nonprofit hospital and is required to offer financial assistance to patients who cannot afford services. However, there are no federal regulations regarding how much hospitals have to spend on financial assistance or who can be eligible. When groups refuse care, it can make it harder for patients to get help.

According to the Lown Institute, Allina skirted $266 million in taxes in 2020 from its nonprofit status and spent $57 million on financial assistance and community investment. It could have spent $209 million more to reach its tax exemption value.

Academic medicine combines healthcare with higher education, the two sectors of the American economy that have exhibited outsized cost growth during the past 50 years. The result is a stunning disconnection between the business practices of academic medical centers (AMCs) and the supply-demand dynamics reshaping healthcare delivery.

Market, technological and regulatory forces are pushing the healthcare industry to deliver higher-value care that generates better outcomes at lower costs. A parallel movement is shifting resources out of specialty and acute care services into primary, preventive, behavioral health and chronic disease care services. In the process, care delivery is decentralizing and becoming more consumer-centric.

AMCs Double Down

Counter to these trends, academic medicine is doubling down on high-cost, centralized, specialty-focused care delivery. Privilege has its price. Several AMCs — including Mass General Brigham, IU Health, UCSF, Ohio State and UPMC — are undertaking multibillion-dollar expansions of their existing campuses. Collectively, AMCs expect American society to fund their continued growth and profitability irrespective of cost, effectiveness and contribution to health status.

Despite being tax-exempt and having access to a large pool of free labor (residents), AMCs charge the highest treatment prices in most markets. [1] Archaic formulas allocate residency “slots” and lucrative Graduate Medical Education payments (over $20 billion annually) disproportionately into specialty care and more-established AMCs. Given their cushy funding arrangements, it’s no wonder AMCs fight vigorously to maintain an out-of-date status quo.

Legacy practices from the early 1900s still dominate medical education, medical research and clinical care. Like tenured faculty, academic physicians manage their practices with little interference. Clinical deans rule their departments with a free hand. With few exceptions, interdisciplinary coordination is an oxymoron. The result is fragmented care delivery that tolerates duplication, medical error and poor patient service.

Irresistible consumerism confronts immovable institutional inertia. As exhibited by substantial operating losses at many AMCs, their foundations are beginning to crack. [2]

Medicine’s Rise from Poverty to Prosperity

In his 1984 Pulitzer Prize-winning work, Paul Starr chronicles the social transformation of American medicine during the 19th and 20th centuries. Prior to the 1900s, doctors had low social status. Most care took place in the home. Pay was low. The profession lacked professional standards. There were too many quacks. Most doctors lived hand-to-mouth.

As the century turned, several cultural, economic, scientific and legal developments converged to elevate the profession’s status in American society. Stricter licensing reduced the supply of physicians and closed most existing medical schools. Legislation and legal rulings restricted corporate ownership of medical practices and enshrined physicians’ operating autonomy. Scientific breakthroughs gave medicine more healing power.

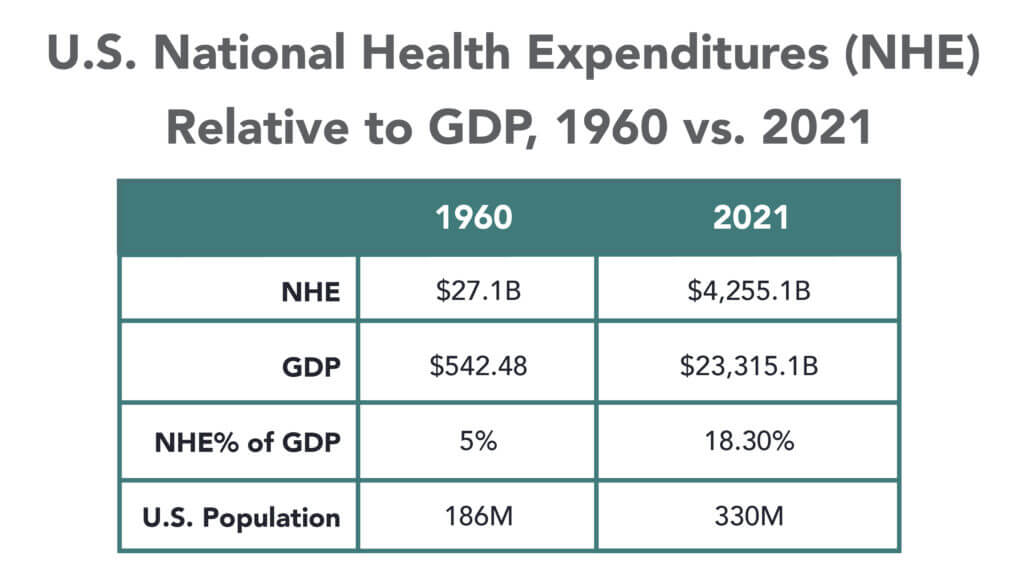

Through the decades that followed, the American Medical Association and state medical societies frustrated external attempts to control medical delivery externally and institute national health insurance. They insisted on fee-for-service payment and the absolute right of patients to choose their doctors. These are causal factors underlying healthcare’s skyrocketing cost increases, growing from 5% of the U.S. gross domestic product (GDP) in 1960 to over 18% in 2021.

Academic and community-based physicians have always had a tenuous relationship. Status and prestige accompany academic affiliations. Academic practices require referrals from community physicians but rarely consult with them on treatment protocols. For their part, community physicians marvel at the lack of market awareness exhibited by academic practices. They have tolerated one another to perpetuate collective physician control over healthcare operations.

Incomes and prestige for both community and academic physicians rose as the medical profession limited practitioner supply, established payment guidelines, encouraged specialization, controlled service delivery and socialized capital investment. One hundred years later, the business of healthcare still exhibits these characteristics. Gleaming new medical centers testify to the profession’s success in socializing capital investment and maintaining autonomy over hospital operations.

Entrenched beliefs and behaviors explain why most hospitals, despite their high construction costs, are largely deserted after 4 p.m. and on weekends. They explain the maldistribution of facilities and practitioners. They explain the overdevelopment of specialty care. They explain the underinvestment in preventive care, mental health services and public health.

Value-Focused Backlash Portends Reckoning

These beliefs and behaviors are contributing to AMC’s current economic dislocation. Dependent upon public subsidies and premium treatment payments to maintain financial sustainability, high-cost AMCs are particularly vulnerable to value-based competitors.

The marketplace is attacking inefficient clinical care with tech-savvy, consumer-friendly business models. Care delivery is decentralizing even as many AMCs invest more heavily in campus-based medicine. A market-based reckoning confronts academic medicine.

A visit up north illustrates the general unwillingness of academic physicians to accept market realities and their continued insistence on maintaining full control over the academic medical enterprise. It’s like watching a train wreck occur in slow motion.

Minnesota Madness

After experiencing severe economic distress, the University of Minnesota sold its University of Minnesota Medical Center (UMMC) to Fairview Health in 1997. Fairview currently operates UMMC in partnership with the University of Minnesota Physicians (UMP) under the banner of M Health Fairview.

In September 2022, Sanford Health and Fairview Health signed a letter of intent to merge. The new combined company would bear the Sanford name with its headquarters in Sioux Falls, South Dakota. Despite the opportunity to double its catchment area for specialty referrals, the University and UMP oppose the merger with Sanford. They fear out-of-state ownership could compromise the integrity of UMMC’s operations.

Fairview wants the Sanford merger to help it address massive operating losses resulting, in part, from its contractual arrangements with UMP. Negotiations between the parties have become acrimonious. Amid the turmoil, the University and UMP announced in January 2023 their intention to acquire UMMC from Fairview and build a new state-of-the-art medical center on the University’s Minneapolis campus.

The University has named this proposal “MPact Health Care Innovation.” It calls for the Minnesota state legislature to fund the multibillion-dollar cost of acquiring, building and operating the new medical enterprise. Typical of academic medical practices, UMP expects external sources to pony up the funding to support their high-cost centralized business model while they continue to call the shots.

The arrogance and obliviousness of the University’s proposal is staggering. Minnesota struggles with rising rates of chronic disease and inequitable healthcare access for low-income urban and rural communities. The idea that a massive governmental investment in academic medicine will “bridge the past and future for a healthier Minnesota” as the MPact tagline proclaims is ludicrous.

Out of Touch

Like the rest of the country, Minnesota is experiencing declining life expectancy. Despite spending more than double the average per-capita healthcare cost of other wealthy countries, the United States scores among the worst in health status measures. Spending more on high-end academic medicine won’t change these dismal health outcomes. Spending more on preventive care, health promotion and social determinants of health could.

The real gem in the University of Minnesota’s medical enterprise is its medical school. It has trained 70% of the state’s physicians. It ranks third and fourth nationally in primary care and family medicine. It is advancing a progressive approach to interdisciplinary and multi-professional care.

If the Minnesota state legislature really wants to advance health in Minnesota, it should expand funding for the University’s aligned health schools and community-based programs without funding the acquisition and expansion of the University’s clinical facilities.

No Privilege Without Performance

Our nation must stop enabling academic medicine’s excesses. Funding AMCs’ insatiable appetite for facilities and specialized care delivery is counterproductive. It is time for academic medicine to embrace preventive health, holistic care delivery and affordable care access.

Privilege comes with responsibility. AMCs that resist the pivot to value-based care and healthier communities deserve to lose market relevance.

America has the means to create a healthier society. It requires shifting resources out of healthcare into public health. We must have the will to make community-based health networks a reality. It starts by saying no to needless expansion of acute care facilities.

The median year-to-date operating margin index for hospitals improved slightly in April to 0 percent. While recent reports show signs of improving margins, they remain far below historical norms, and inflation and workforce expenses continue to challenge hospitals’ bottom lines.

“Hospital and health system leaders must figure out how to navigate the new financial reality and begin to take action,” Erik Swanson, senior vice president of data and analytics with Kaufman Hall, said in a May 31 report. “In the face of operating margins that may never fully recover and inflated expenses, developing and executing a strategic path forward to a future that is financially sustainable is crucial.”

Here are 29 health systems ranked by their operating margins in the first quarter:

Correction: An earlier version incorrectly referenced a Texas deal between Houston Methodist and Baylor Scott and White. News about deals is sensitive and unnecessarily disruptive to reputable organizations like these. I sourced this news from a reputable deal advisor: it was inaccurate. My apology!

Congressional Republicans and the White House spared Main Street USA the pain of defaulting on the national debt last week. No surprise.

Also not surprising: another not-for-profit-mega deal was announced:

St. Louis, MO-based BJC HealthCare and Kansas City, MO-based Saint Luke’s Health System announced their plan to form a $9.5B revenue, 28-hospital system with facilities in Missouri, Kansas, and Illinois.

This follows recent announcements by four other NFP systems seeking the benefits of larger scale:

Gundersen Health System & Bellin Health (Nov 2022): 11 hospitals, combined ’22 revenue of $2.425B

Froedtert Health & ThedaCare (Apr 2023 LOI): 18 hospitals, combined ’22 revenues of $4.6B

And all these moves are happening in an increasingly dicey environment for large, not-for-profit hospital system operators:

Increased negative media attention to not-for-profit business practices that, to critics, appear inconsistent with a “NFP” organization’s mission and an inadequate trade for tax exemptions each receives.

Decreased demand for inpatient services—the core business for most NFP hospital operations. Though respected sources (Strata, Kaufman Hall, Deloitte, IBIS et al) disagree somewhat on the magnitude and pace of the decline, all forecast decreased demand for traditional hospital inpatient services even after accounting for an increasingly aging population, a declining birthrate, higher acuity in certain inpatient populations (i.e. behavioral health, ortho-neuro et al) and hospital-at-home services.

Increased hostility between national insurers and hospitals over price transparency and operating costs.

Increased employer, regulator and consumer concern about the inadequacy of hospital responsiveness to affordability in healthcare.

And heightened antitrust scrutiny by the FTC which has targeted hospital consolidation as a root cause of higher health costs and fewer choices for consumers. This view is shared by the majorities of both parties in the House of Representatives.

In response, Boards and management in these organizations assert…

Health Insurers—especially investor-owned national plans—enjoy unfettered access to capital to fund opportunistic encroachment into the delivery of care vis a vis employment of physicians, expansion of outpatient services and more.

Private equity funds enjoy unfettered opportunities to invest for short-term profits for their limited partners while planning exits from local communities in 6 years or less.

The payment system for hospitals is fundamentally flawed: it allows for underpayments by Medicaid and Medicare to be offset by secret deals between health insurers and hospitals. It perpetuates firewalls between social services and care delivery systems, physical and behavioral health and others despite evidence of value otherwise. It requires hospitals to be the social safety net in every community regardless of local, state or federal funding to offset these costs.

These reactions are understandable. But self-reflection is also necessary. To those outside the hospital world, lack of hospital price transparency is an excuse. Every hospital bill is a surprise medical bill. Supporting the community safety net is an insignificant but manageable obligation for those with tax exemption status. Advocacy efforts to protect against 340B cuts and site-neutral payment policies are about grabbing/keeping extra revenue for the hospital. What is means to be a “not-for-profit” anything in healthcare is misleading since moneyball is what all seem to play. And short of government-run hospitals, many think price controls might be the answer.

My take:

The headwinds facing large not-for-profit hospitals systems are strong. They cannot be countered by contrarian messaging alone.

What’s next for most is a new wave of operating cost reductions even as pre-pandemic volumes are restored because the future is not a repeat of the past. Being bigger without operating smarter and differently is a recipe for failure.

What’s necessary is a reset for the entire US health system in which not-for-profit systems play a vital role. That discussion should be led by leaders of the largest NFP systems with the full endorsements of their boards and support of large employers, physicians and public health leaders in their communities.

Everything must be on the table: funding, community benefits, tax exemption, executive compensation, governance, administrative costs, affordability, social services, coverage et al. And mechanisms for inaction and delays disallowed.

It’s a unique opportunity for not-for-profit hospitals. It can’t wait.