Seniors face more than $50 billion in unpaid medical bills, many of which they shouldn’t have to pay, according to a federal watchdog report.

In an all-too-common scenario, medical providers charge elderly patients the full price of an expensive medical service rather than work with the insurer that is supposed to cover it. If the patient doesn’t pay, the provider sends the bill into collections, setting off a round of frightening letters, humiliating phone calls and damaging credit reports.

That is one conclusion of a recent report titled Medical Billing and Collections Among Older Americans, from the Consumer Financial Protection Bureau.

The report recounts a horror story from a patient in southern Pennsylvania over a hospital visit, which should have been covered by insurance.

“I never received a bill from anyone,” the patient said in a 2022 complaint. Then came a phone call from a collection agency. “The woman on the phone started off aggressively screaming at me,” saying the patient owed $2,300.

“I told her there must be some mistake, that both Medicare and my supplement insurance would have covered it. It has in the past. She started screaming, very loud, ‘If you don’t pay me right now, I will put this on your credit report.’ I told her, ‘If you keep screaming at me, I will hang up.’ She continued, so I hung up.”

Nearly 4 million seniors reported unpaid medical bills in 2020, even though 98 percent of them had insurance, the report found. Medicare, the national health insurance program, was created to protect older Americans from burdensome medical expenses.

Total unpaid medical debt for seniors rose from $44.8 billion in 2019 to $53.8 billion in 2020, even though older adults reported fewer doctor visits and lower out-of-pocket costs in 2020.

Medical debt among seniors is rising partly because health care costs are going up, agency officials said. But much of the $53.8 billion is cumulative, they said, debt carried over from one year to the next. Figures for 2020 were the latest available.

Millions of older Americans are covered by both Medicare and Medicaid, a second federal insurance program for people of limited means. Federal and state laws widely prohibit health care providers from billing those patients for payment beyond nominal copays.

Yet, those low-income patients are more likely than wealthier seniors to report unpaid medical bills. The agency’s findings suggest that health care companies are billing low-income seniors “for amounts they don’t owe.” The findings draw from census data and consumer complaints collected between 2020 and 2022.

Many complaints depict medical providers and collection agencies relentlessly pursuing seniors for payment on bills that an insurance company has rejected over an error, rather than correcting the error and resubmitting the claim.

“Many of these errors likely are avoidable or fixable,” the report states, “but only a fraction of rejected claims are adjusted and resubmitted.”

When a patient points out the error, the creditors might agree to fix it, only to ignore that pledge and double down on the debt collection effort.

An Oklahoma senior recounted a collection agency nightmare that followed a hospital stay. After paying all legitimate bills, the patient discovered new charges from a collection agency on a credit report. In subsequent months, additional charges appeared.

The patient assembled billing statements and correspondence, hoping to clear the bogus charges. “I then proceeded to spend every weekday, all day, for two weeks on the phone, trying to find out who was billing me and why,” the patient said in a 2021 complaint.

The Oklahoman eventually paid the bills, “even though I don’t owe them.” Then, more charges appeared.

“Nice racket they have going,” the patient quipped.

As anyone with health insurance knows, medical providers occasionally charge patients for services that should have been covered by the insurer. Someone forgets to submit the claim, or types the wrong billing code or omits crucial documentation. Some providers charge patients more than the negotiated rate, a discounted fee set between the provider and insurer.

Americans spend hours of their lives disputing such charges. But many seniors aren’t up to the task.

“It’s tiring to have multiple conversations, sitting on the phone for an hour, chasing representatives,” said Genevieve Waterman, director of economic and financial security at the National Council on Aging.

“I think technology is outpacing older adults,” she said. “If you don’t have the digital literacy, you’re going to get lost.”

Older adults are more likely than younger people to have multiple chronic health conditions, which can require more detailed insurance documentation and face greater scrutiny, yielding more billing errors and denied claims, the federal report says.

Seniors are also more likely to rely on more than one insurance plan. As of 2020, two-thirds of older adults with unpaid medical bills had two or more sources of insurance.

Multiple insurers means a more complex billing process, making it harder for either patient or provider to file a claim and see that it is paid. With Medicaid, “you have 50 states, plus the territories,” said one official from the federal agency, speaking on condition of anonymity. “They each have their own billing system.”

In an analysis of Medicare complaints filed between 2020 and 2022, the agency found that 53 percent involved debt collectors seeking money the patient didn’t owe. In a smaller share of cases, patients reported that collection agents threatened punitive action or made false statements to press their case.

The complaints “illustrate how difficult it is to identify an inaccurate bill, learn where it originated, and correct other people’s mistakes,” the report states. “Some providers refuse to talk to consumers because the account has already been referred to collections. Even when providers seem willing to correct their own mistakes, debt collectors may continue attempting to collect a debt that is not owed and refuse to stop reporting inaccurate data.”

Rather than carry on a fight with collection agents over multiple rounds of calls and correspondence, many seniors become ensnared in a “doom loop,” the report says, convinced their appeal is hopeless. They pay the erroneous bill.

“I think some people get to the point where they just throw up their hands and give up a credit card number just to make the problem go away,” said Juliette Cubanski, deputy director of the Program on Medicare Policy at KFF.

Debt takes a toll on the mental and physical health of seniors, research has shown. Older adults with debt are more prone to a range of ailments, including hypertension, cancer and depression.

As the Oklahoma patient said, recalling a years-long battle over unpaid bills, “It nearly sent me back to the hospital.”

The U.S. health system is big and getting bigger. It is labor intense, capital intense, and highly regulated. Each sector operates semi-independently protected by local, state and federal constraints that give incumbents advantages and dissuade insurgents.

Competition has been intramural:

Growth by horizontal consolidation within sectors has been the status quo for most to meet revenue and influence targets. In tandem, diversification aka vertical consolidation and, for some, globalization in each sector has distanced bigger players from smaller:

insurers + medical groups + outpatient facilities + drug benefit managers

retail pharmacies + primary & preventive care + health & wellbeing services + OTC products/devices

regulated medical devices + OTC products for clinics, hospitals, homes, workplaces and schools.

The landscape is no man’s land for the faint of heart but it’s golden for savvy private investors seeking gain at the expense of the system’s dysfunction and addictions—lack of price transparency, lack of interoperability and lack of definitive value propositions.

What’s ahead?

Everyone in the U.S. health system is aware that funding is becoming more scarce and regulatory scrutiny more intense, but few have invested in planning beyond tomorrow and the day after. Unlike drug and device manufacturers with global markets and long-term development cycles, insurers and providers are handicapped. Insurers respond by adjusting coverage, premiums and co-pays annually. Providers—hospitals, physicians, long-term care providers and public health programs– have fewer options. For most, long-range planning is a luxury, and even when attempted, it’s prone to self-protection and lack of objectivity.

Changes to the future state of U.S. healthcare are the result of shifts in these domains:

They apply to every sector in healthcare and define the context for the future of each organization, sector and industry as a whole:

The Clinical Domain: How health, diseases and treatments are defined and managed where and by whom; how caregivers and individuals interact; how clinical data is accessed, structured and translated through AI enabled algorithms; how medication management and OTC are integrated; how social determinants are recognized and addressed by caregivers and communities: and so on. The clinical domain is about more than doctors, nurses, facilities and pills.

The Technology Domain: How information technologies enable customization in diagnostics and treatments; how devices enable self-care; how digital platforms enable access; how systemness facilitates integration of clinical, claims and user experience data; how operating environments shift to automation lower unit costs; how sites of care emerge; how caregivers are trained and much more. Proficiency in the integration of technologies is the distinguishing feature of organizations that survive and those that don’t. It is the glue that facilitates systemness and key to the system’s transformation.

The Regulatory Domain: How affordability, value, competition, choice, healthcare markets, not-for-profit and effectiveness are defined; how local, state and federal laws, administrative orders by government agencies and executive actions define and change compliance risks; how elected officials assess and mitigate perceived deficiencies in a sector’s public accountability or social responsibility; how courts adjudicate challenges to the status quo and barriers to entry by outsiders/under-served populations; how shareholder ownership in healthcare is regulated to balance profit and the public good; et al. Advocacy on behalf of incumbents geared to current regulatory issues (especially in states) is compulsory table stakes requiring more attention; evaluating potential regulatory environment shifts that might fundamentally change the way a system is structured, roles played, funded and overseen is a luxury few enjoy.

The Capital Domain: how needed funding for major government programs (Medicare, Medicaid, Children’s, Military, Veterans, HIS, Dual Eligibles et al) is accessed and structured; how private investment in healthcare is encouraged or dissuaded; how monetary policies impact access to debt; how personal and corporate taxes impact capitalization of U.S. healthcare; how value-based programs reduce unnecessary costs and improve system effectiveness; how the employer tax exemption fares long-term as employee benefits shrink; how U.S. system innovations are monetized in global markets; how insurers structure premiums and out of pocket payments: et al. The capital domain thinks forward to the costs of capital it deploys and anticipated returns. But inputs in the models are wildly variable and inconsistent across sectors: hospitals/health systems vs. global private equity healthcare investors vs. national insurers’ capital strategies vary widely and each is prone to over-simplification about the others.

The Consumer Domain: how individuals, households and populations perceive and use the system; how they assess the value of their healthcare spending; how they vote on healthcare issues; how and where they get information; how they assess alternatives to the status quo; how household circumstances limit access and compromise outcomes; et al. The original sin of the U.S, health system is its presumption that it serves patients who are incapable/unwilling to participate effectively and actively in their care. Might the system’s effectiveness and value proposition be better and spending less if consumerization became core to its future state?

For organizations operating in the U.S. system, staying abreast of trends in these domains is tough. Lag indicators used to monitor trends in each domain are decreasingly predictive of the future. Most Boards stay focused on their own sector/subsector following the lead of their management and thought leadership from their trade associations. Most are unaware of broader trends and activities outside their sector because they’re busy fixing problems that impact their current year performance. Environmental assessments are too narrow and short-sighted. Planning processes are not designed to prompt outside the box thinking or disciplined scenario planning. Too little effort is invested though so much is at risk.

It’s understandable. U.S. healthcare is a victim of its success; maintaining the status quo is easier than forging a new path, however obvious or morally clear. Blaming others and playing the victim card is easier than corrective actions and forward-thinking planning.

In 10 years, the health system will constitute 20% of the entire U.S. economy and play an outsized role in social stability. It’s path to that future and the greater good it pursues needs charting with open minds, facts and creativity. Society deserves no less.

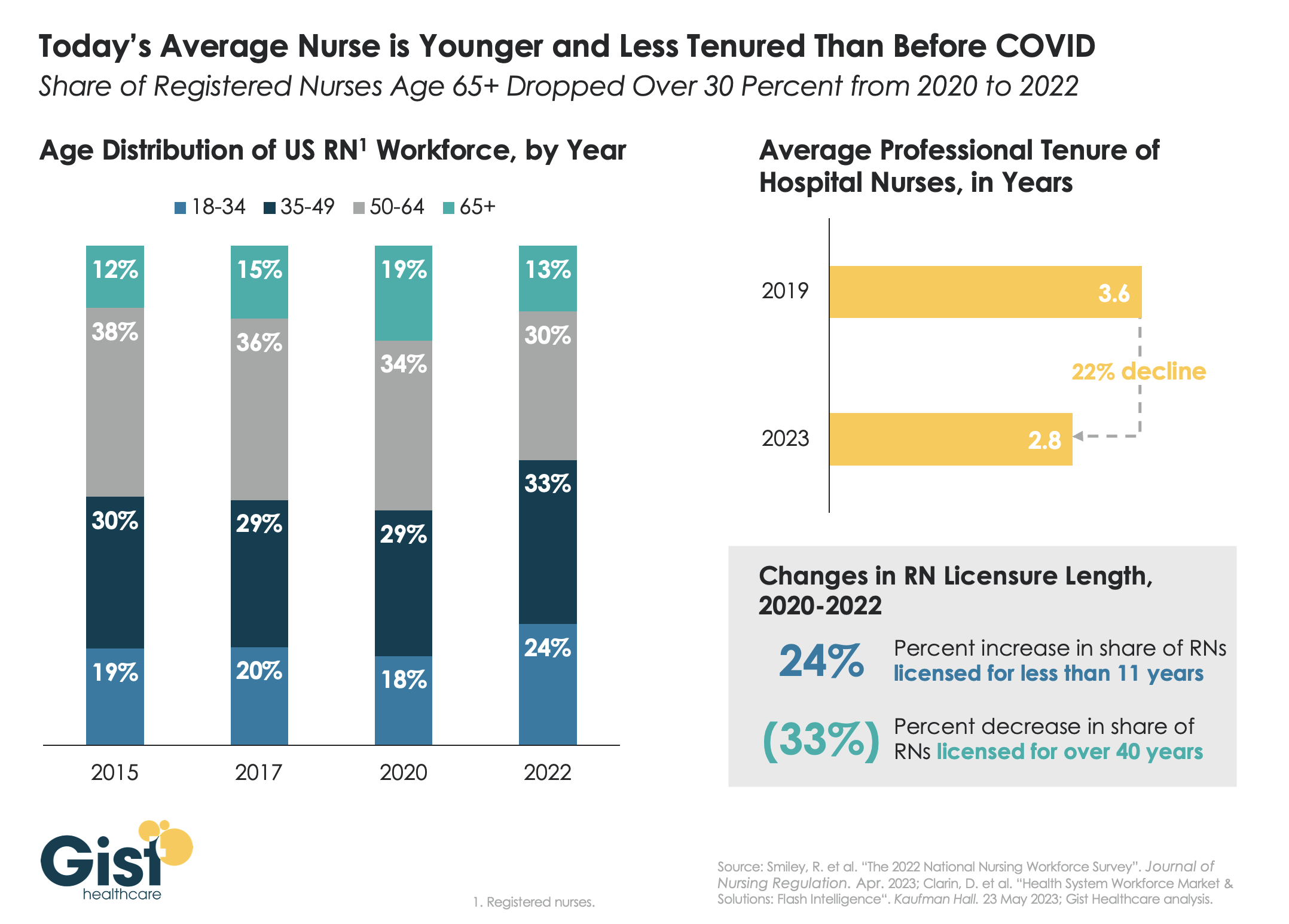

Last week we discussed how hospitals are still struggling to retain talent. This week’s graphic offers one explanation for this trend:

a significant share of older nurses, who continued to work during the height of the pandemic, have now exited the workforce, and health systems are even more reliant on younger nurses.

Between 2020 and 2022, the number of nurses ages 65 and older decreased by 200K, resulting in a reduction of that age cohort from 19 percent to 13 percent of the total nursing workforce. While the total number of nurses in the workforce still increased, the younger nurses filling these roles are both earlier in their nursing careers (thus less experienced), and more likely to change jobs.

Case in point:

From 2019 to 2023, the average tenure of a hospital nurse dropped by 22 percent. The wave of Baby Boomer nurse retirements has also resulted in a 33 percent decrease from 2020 to 2022 in the number of registered nurses who have been licensed for over 40 years.

Given these shifts, hospitals must adjust their current recruitment, retention, training, and mentorship initiatives to match the needs of younger, early-career nurses.

We recently spoke with a health system COO who wanted help playing out scenarios regarding the relationship between specialist physicians and their private equity (PE) partners. The system is located in one of the markets referenced in a recent study that has some of the highest levels of private equity ownership in the country. One physician group, whose doctors provide almost all the system’s coverage for a key specialty, has worked with PE partners for five years, and the relationship is not going well. “We’re hearing that many of the younger doctors want to leave. And many of the others are close to retirement,” he shared.

“We’re really concerned about what could happen if the group implodes.” The key issue: the doctors signed very restrictive noncompete agreements when they sold their practice, which could prohibit them from working in the market.

The health system would consider bringing some of the doctors into their employed medical group, but executives are worried this might be impossible for the duration of the noncompete agreements. “If these doctors can’t stay locally, we might have to rebuild that specialty from scratch. And I can’t imagine how disruptive that would be,” he worried.

When the FTC announced a proposed rule earlier this year that would ban employers from imposing noncompete agreements, many health systems reacted with alarm, fearing the that the freedom to move would lead to frequent bidding wars, ultimately driving up the cost of physician talent in the market.

But the situation shows how perspectives would change depending on who holds the noncompete.

Mid-sized markets like this one, where coverage for several specialties may come from single groups, are particularly vulnerable. Regardless, this situation highlights the need to diversify physician relationships to guard against getting caught in a “coverage crisis”.

Of all the pandemic’s impacts still felt today, disruptions to the healthcare workforce and rising labor costs may be most impactful to current health system operations.

Over the next three editions of the Weekly Gist, we’ll be exploring the lingering effects of this workforce crisis, with a focus on nurse staffing and recruitment.

While wage increases helped reduce hospital registered nurse (RN) turnover rates from 27 percent in 2021 to 23 percent in 2022, nurses—along with hospital employees in general—are still changing jobs at higher rates than before the pandemic.

Over half of all hospitals still face nurse vacancy rates above 15 percent, a slight improvement from 2022 but still far more than before the pandemic.

While the worst of nursing turnover appears to have passed, the “rebasing” of wages (for nursing, 27 percent higher compared to 2019) will provide ongoing pressure to strained hospital margins.

A recent physician survey conducted by strategic healthcare communications firm Jarrard Inc. uncovered a startling finding: only 36 percent of physicians employed by or affiliated with not-for-profit health systems trust that their system’s leaders are honest and transparent. In contrast, a slight majority of physicians working with investor-owned health systems and practices answered that question in the opposite.

Overall, only around half of physicians trust their organization’s leaders when it comes to financial, operational, and patient care decision-making. Unsurprisingly, doctors put the most trust in peer physicians, by a wide margin.

The Gist: While the numbers, especially for nonprofit systems, are stark, this survey reflects an on-the-ground reality felt at health systems in recent years. Physician fatigue has spiked in the wake of the pandemic.

And health system-physician relationships are also being disrupted by cost pressures, payer and investor acquisitions, and the shift of care to ambulatory settings. We’ve heard from physicians that, compared to hospital owners, investor-backed systems provide greater transparency and clearer financial goals centered around the success of the business.

That physicians trust their peers so highly suggests a path forward: provide physician leaderswith greater transparency into system performance and agency over strategy, with clear goals and metrics.

Last week the Department of Justice (DOJ) and the Federal Trade Commission (FTC) proposed thirteen new merger guidelines that, if finalized, would provide federal regulators greater ability to scrutinize mergers across all industries, including healthcare.

The guidelines expand which mergers could be potentially illegal and therefore worth probing, including those with lower monetary value and those in which the newly combined organization would control 30 percent or greater market share, and would increase scrutiny on transactions that are part of a series of multiple acquisitions by an organization. They also seek to limit the ability of an organization to justify an acquisition on the grounds that the weaker party in the deal would be unable to continue to operate. Comments on the guidelines are being accepted until September 18.

The Gist: To date, federal regulators have struggled to prevent non-traditional mergers between companies that provide different services, operate in different markets, or are below the monetary threshold for review.

The proposed guidelines would significantly increase FTC and DOJ scrutiny at all levels of hospital mergers, and also jeopardize physician and other care asset acquisitions by health systems, payers, and private equity-backed organizations. They are the latest from the Biden Administration in a recent, multi-part push to reduce consolidation through greater antitrust enforcement.

This effort includes last month’s proposal to add additional reporting requirements for mergers outlined in the Hart-Scott-Rodino Act, as well as the FTC’s move earlier this month to withdraw two antitrust policy statements focused on healthcare markets that both agencies say are now “outdated.” Those now-rescinded statements provided guidance on antitrust safety zones, including for accountable care organizations participating in the Medicare Shared Savings Program and for mergers between two hospitals in which one is much smaller.

In January 2023, the Rockefeller Institute published a three-part blog series on trends to watch in healthcare in 2023. The series covered broad issues related to the healthcare workforce, economy, and health policy, and highlighted internal industry changes and trends in service delivery, quality, and equity.

Here, we provide a recap and mid-year update on those trends.

The Public Health Emergency:

In January, we anticipated the COVID-19 federal public health emergency (PHE) would end at some point during the year and its ending would impact the industry by rolling back flexibilities and programs that were temporarily put in place to combat the pandemic. The end of the PHE, while not a “trend” per se, held significant potential to alter the trajectory of trends in healthcare coverage, access, and care delivery that were occurring during the pandemic.

Mid-year Update: As predicted, the PHE was not renewed and ended on May 11, 2023. The most notable impact of the non-renewal of the PHE was the end of continuous Medicaid public health insurance coverage. The Kaiser Family Foundation’s Medicaid Enrollment Tracker shows that, as of July 5, 2023, 1,652,000 Medicaid enrollees were disenrolled by the District of Columbia and 28 states reporting data. For context, this means that 39% of people with a completed renewal were disenrolled in reporting states, though disenrollment rates varied significantly across those states from 16 percent in Virginia to 75 percent in South Carolina. The eligibility redetermination process that can lead to a potential disenrollment is being conducted differently in each state with some states moving quickly to make redeterminations and others doing the process more deliberately over the course of the year with a clear intent to avoid shedding people from the Medicaid program because of an inability to submit administrative paperwork.

The process for eligibility renewals will continue to play out over the course of the next year since states have until mid-2024 to update all Medicaid enrollees’ eligibility status. Also notable are some changes made under the purview of the PHE that persist despite the emergency’s conclusion. For example, access to COVID-19 vaccinations and certain COVID-19 treatments generally have not been affected. Some telehealth flexibilities that were allowed under the PHE are also staying in effect, at least until the end of 2024.

Healthcare Workforce Shortages:

Prior to the pandemic, larger demographic trends in society were already impacting the supply of the healthcare workforce. The number of people aging and needing healthcare services was growing while the number of people available to provide care was not keeping pace thus creating a long-term healthcare workforce shortage.

Mid-year Update:The workforce shortage continues. As outlined in a May 23rd Becker’s Hospital Review article, several sources point to a continued shortage. They include a report that says the US could see a deficit of 200,000 to 450,000 registered nurses by 2025. Within the next five years, another report also projects a shortage of more than 3.2 million lower-wage healthcare workers, such as medical assistants, home health aides, and nursing assistants. As a result, some healthcare providers are becoming more creative in their efforts to counteract the workforce shortage: creating alumni networks from which to recruit or providing other benefits to their workforce, such as housing or educational assistance. Policymakers can help counteract the negative impacts of the workforce shortage through a variety of strategies. With the shortage expected to continue, it will be important to enact additional policies that bolster the workforce.

Price Inflation:

As we noted, price inflation was significant in 2022 but was not unique to the health sector.Inflation was particularly exacerbated by the re-opening of the economy after the pandemic, the continued war in Ukraine, and supply chain challenges.

Mid-year Update: Prices for many consumer goods and services increased faster than usual, with overall inflation reaching a four-decade high in mid-2022. The Bureau of Labor Statistics (BLS) reported inflation rates have slowed, with overall prices growing by 6 percent in February 2023 compared to the previous year. Interestingly, prices for medical care increased only 2.3 percent. Similarly, BLS reported that the average price of health care in the United States increased by 0.7 percent in the 12 months ending May 2023, following a previous increase of 1.1 percent. The slower price growth in healthcare compared to other sectors of the economy is highly unusual,[i] and while inflation is not easily influenced by state-level policymakers’ actions alone, the trend is still worth monitoring to better understand the impacts on healthcare access and quality. As of early July, the latest predictions from PwC are that healthcare costs will rise 7% in 2024.

Declining Margins at Hospitals:

Previous analysis by the consulting firm Kaufman Hall predicted that more than half of all hospitals would have negative margins at the end of 2022. As we noted, this was due to such factors as higher-than-normal expenses for staff, supplies, and pharmaceuticals and lower revenues.

Mid-year Update: The latest report from Kaufman Hall offers data that shows a reversal in this trend for the first part of 2023. May was the third consecutive month in which hospital margins were positive after operating in the red for most of 2022. The return to normal is largely driven by revenues that are more in line with pre-pandemic levels. With revenues returning to more normal levels, expenses will be particularly important to watch for the remainder of 2023. If hospital expenses continue to outweigh revenues, policymakers may need to evaluate the financial health of providers and the potential impact that may have on access to services for patients.

Private Equity in Healthcare:

We predicted that private equity (PE) would continue to grow in healthcare, pointing to a PwC consulting report that indicated that PE companies still had plenty of “dry powder,” or money, to invest in 2023.

Mid-year Update:There has been a slowdown in private equity deals over the last year. But it is notable that there were still 200 private equity deals in healthcare in the first quarter of 2023, according to PitchBook’s healthcare services report released in May 2023. While lower than the year before, this is still considered active when compared to pre-pandemic PE dealmaking. Because of the waning of the pandemic and stability returning to the healthcare sector, it is more likely that PE deals stabilize in 2023. And some industry predictions indicate that dealmaking will bounce back further in the second half of 2023. As noted in our previous blog, it will be important to monitor the proliferation of PE in healthcare and determine its impact on healthcare markets, care delivery, innovation, and quality.

Consolidations:

Like many other industries, consolidations of all sorts have been happening in healthcare. The consolidations are both vertical—combining two or more stages of production normally operated by separate companies into one company, such as when hospitals or insurers employ physicians and/or acquire physician practices or other entities like pharmacies—and horizontal—combining organizations that provide the same or similar services, such as hospitals acquiring hospitals.

Mid-year Update: Consolidations of all sorts of healthcare entities continued in 2023 with some of the biggest potential consolidations yet. Those include the proposed merger of two major bi-coastal health system providers: Geisinger, based in Pennsylvania, and Kaiser, based in California. Although the deal must still go through regulatory approval, if completed, the two systems will create a nonprofit that will look to add five or six more systems nationally over the next five years. Other notable consolidations include the finalization of tech-giant Amazon’s purchase of One Medical, a primary care network. And Optum, one of the largest conglomerates that is a subsidiary of United Health Group, increased its net revenue growth by 25% to $54.1 billion in the first quarter of 2023, primarily due to more patients visiting OptumHealth clinics and growth in OptumRx pharmacy scripts processed. Optum’s growth is likely to continue in 2023 as they expect to add another 10,000 physicians. Case in point, in February of this year, Optum paid an undisclosed sum for Crystal Run Healthcare, a network of nearly 400 providers in New York. A goal of consolidation has been better coordination of patient care for improved outcomes and value. Results have been mixed and it is therefore an important trend for policymakers and researchers to monitor and to ensure the impacts are positive.

Alternate Payment Models:

Alternate payment models (APMs) in healthcare have been expanding especially since enactment of the Patient Protection and Affordable Care Act in 2010. They are primarily being developed by the Center for Medicare and Medicaid Innovation (CMMI) which has driven payment policy (including APMs) in the two big government healthcare programs: Medicaid and Medicare. There have been several iterations of APMs—over 50 models—but the one common theme is that all of them generally seek to reward better care.

Mid-year Update: Since the start of 2023, the most notable expansion of the trend toward more alternate payment models was CMMI’s introduction of a new primary care-focused APM called Making Care Primary. In addition to this model, it is expected that the Centers for Medicaid and Medicare Services (CMS), which oversees the operation of these two large public health insurance programs, will introduce more new payment models in 2023, including one that allows states to manage the total cost of care in a given region. This may take various forms, including something akin to Maryland’s global budget, which is used statewide. Since the total cost of care model has yet to be officially revealed, this trend and the emergence of any new developments is worth watching in the second half of 2023. Policymakers can learn from these various payment models and use them to inform the plans implemented in their own state or region in order to improve healthcare.

Attention to Health Equity:

A notable aspect of the pandemic was the disparate impact it had on people of color and other marginalized groups. In response, policymakers and providers began paying more attention to the underlying cause of these disparities. In 2021, President Joe Biden signed an executive order to focus federal resources and attention on reducing health disparities.

Mid-year Update: Increased attention to health equity in healthcare has continued. Ernst and Young, an international consulting group, released its first-ever report on the state of health equity in the United States, which involved a survey of over 500 providers to begin tracking their methods for, and progress in, addressing health disparities. More recently, in June 2023, The Joint Commission on the Accreditation of Healthcare Organizations (JCAHO) announced that it will be adding a certification program for healthcare organizations specifically targeted towards improving health equity. While attention to equity has grown, what will be interesting to watch in the second half of 2023 is the degree to which such efforts are having an impact on actually reducing disparities. Understanding the impacts of various interventions can help policymakers expand efforts that are effective.

Digital TeleHealth Delivery Expansion:

The use of digital health expanded dramatically from 2020 to 2022 as social distancing practices were adopted and telehealth options became more widely available. As noted in our blog series, digital health “includes mobile health (mHealth), health information technology (IT), wearable devices, telehealth and telemedicine, and personalized medicine.” It also includes, “mobile medical apps and software that support the clinical decisions doctors make every day to do artificial intelligence and machine learning.”

Mid-year Update: At the end of 2022 and the start of 2023, the ability to infuse capital to drive the expansion of digital health seemed tenuous, in part due to the collapse of Silicon Valley Bank (SVB). As noted by the publication Pitchbook and CB Insights, venture capital funding in the digital health space totaled $7.5 billion in 2022, a 57 percent year-over-year drop. Although the fast pace of investment in digital health may have slowed since its explosion during the pandemic, the expansion of digital health continues. Our January blog suggested that areas such as behavioral health, care at home, and maternal health were areas to watch. In 2023, digital access is expanding in other areas, such as in-home urgent primary care to allow for the treatment of complex injuries and illnesses with the goal of reducing emergency department visits. And other important digital health deals are still occurring: health tech startup Florence picked up Zipnosis from Bright Health to expand its virtual care capabilities. And with the launch of consumer-facing tech products, such as Chat GPT and Apple Vision Pro in the first half of 2023, additional opportunities for applying such technologies in healthcare may fuel further expansion of digital health. Policies that are developed in the future may want to support the growth of such innovation, while also being mindful to monitor the potential impacts on care.

Expansion of Non-Traditional Providers:

In January, we noted an emergence of companies in healthcare whose genesis was something other than healthcare. The blog pointed to examples of how companies such as Walgreens, CVS, and Amazon were expanding their offerings in healthcare.

Mid-year Update:Non-traditional entities continue to expand in the healthcare space. Notable examples include the recent acquisitions and expansions made by CVS. One of these expansions is being done through its affiliation with the insurance company, Aetna. Through Aetna, CVS has entered the insurance exchange market in four more states in 2023, in addition to the 12 states in which it already operates. CVS also closed a deal in the first half of 2023 to acquire Oak Street Health for over $10 billion. And, in March 2023, CVS announced it had officially acquired Signify Health, a digital telehealth company that enables more care to occur in-home. As noted earlier, Amazon officially completed its deal to acquire OneMedical and United Health Group is working on expanding its use of value-based care through a partnership with Walmart. Monitoring the impact of these emerging companies in healthcare will be important for policymakers that have historically only focused on more traditional providers, such as hospitals. These non-traditional entrants, in many cases, are large organizations with substantial resources and their impact may be just as significant if not greater than traditional providers.

Conclusion

These trends merit close attention in the second half of 2023. As healthcare takes on new shapes, the implications for those in the sector and all who depend on it will be huge. In addition, there are important implications for state and federal policymakers who will need to consider how these trends impact access, affordability, and quality of health care, so they can determine whether and how government might help to accelerate beneficial innovations, invest in promising trends, prevent or reverse harmful trends, and monitor the impacts on consumers.

As first half 2023 financial results are reported and many prepare for a busy last half, strategic planning for healthcare services providers and insurers point to 4 issues requiring attention in every boardroom and C suite:

Private equity maturity wall:

The last half of 2023 (and into 2024) is a buyer’s market for global PE investments in healthcare services: 40% of PE investments in hospitals, medical groups and insurtech will hit their maturity wall in the next 12 months. Valuations of companies in these portfolios are below their targeted range; limited partner’ investing in PE funds is down 28% from pre-pandemic peak while fund raising by large, publicly traded, global funds dominate fund raising lifting PE dry powder to a record $3.7 trillion going into the last half of 2023.

In the U.S. healthcare services market, conditions favor well-capitalized big players—global private equity funds and large cap aggregators (i.e., Optum, CVS, Goldman Sachs, Blackstone et al) who have $1 trillion to invest in deals that enhance their platforms. Deals done via special purpose acquisition corporations (SPACS) and smaller PE funds in physicians, hospitals, ambulatory services and others are especially vulnerable. (see Bain and Pitchbook citations below). Addressing the growing role of large-cap PE and strategic investors as partners, collaborators, competitors or disruptors is table stakes for most organizations recognizing they have the wind at their backs.

Consolidation muscle by DOJ and FTC:

Healthcare is in the crosshair of the FTC and DOJ, especially hospitals and health insurers. Hospital markets have become increasingly concentrated: only 12% of the 306 Hospital Referral Regions is considered unconcentrated vs. 23% in 2008. In the 384 insurance markets, 23% are unconcentrated, down from 35% in 2020. Wages for healthcare workers are lower, prices for consumers are higher and choices fewer in concentrated markets prompting stricter guidelines announced last week by the oversight agencies. Big hospitals and big insurers are vulnerable to intensified scrutiny. (See Regulatory Action section below).

Defamatory attacks on nonprofit health systems:

In the past 3 years, private, not-for-profit multi-hospital systems have been targeted for excess profits, inadequate charity care and executive compensation. Labor unions (i.e., SEIU) and privately funded foundations (i.e., West, Arnold Venture, Lown Institute) have joined national health insurers in claims that NFP systems are price gaugers undeserving of the federal, state and local tax exemptions they enjoy. It comes at a time when faith in the U.S. health system is at a modern-day low (Gallup), healthcare access and affordability concerns among consumers are growing and hospital price transparency still lagging (36% are fully compliant with the 2021 Executive Order).

Notably, over the last 20 years, NFP hospitals have become less dominant as a share of all hospitals (61% in 2002 vs. 58% last year) while investor-owned hospitals have shown dramatic growth (from 15% in 2002 to 24% last year). Thus, the majority of local NFP hospitals have joined systems creating prominent brands and market dominance in most regions. But polling indicates many of these brands is more closely associated with “big business” than “not-for-profit health” so they’re soft targets for critics. It is likely unflattering attention to large, NFP systems will increase in the next 12 months prompting state and federal regulatory actions and erosion of public support. (See New England Journal citation in Quotables below)

Campaign 2024 healthcare rhetoric:

Republican candidates will claim healthcare is not affordable and blame Democrats. Democrats will counter that the Affordable Care Act’s expanded coverage and the Biden administration’s attack on drug prices (vis a vis the Inflation Reduction Act) illustrate their active attention to healthcare in contrast to the GOP’s less specific posturing.

Campaigns in both parties will call for increased regulation of hospitals, prescription drug manufacturers, health insurers and PBMs. All will cast the health industry as a cesspool for greed and corruption, decry its performance on equitable access, affordability, price transparency and improvements in the public’s health and herald its frontline workers (nurses, physicians et al) as innocent victims of a system run amuck.

To date, 16 candidates (12 R, 3 D, 1 I) have announced they’re candidates for the White House while campaigns for state and local office are also ramping up in 46 states where local, state and national elections are synced. Healthcare will figure prominently in all. In campaign season, healthcare is especially vulnerable to misinformation and hyper-attention to its bad actors. Until November 5, 2024, that’s reality.

My take:

These issues frame the near-term context for strategic planning in every sector of U.S. healthcare. They do not define the long-term destination of the system nor roles key sectors and organizations will play. That’s unknown.

What’s known for sure is that AI will modify up to 70% of the tasks in health delivery and financing and disrupt its workforce.

Black Swans like the pandemic will prompt attention to gaps in service delivery and inequities in access.

People will be sick, injured, die and be born.

And the economics of healthcare will force uncomfortable discussions about its value and performance.

In the U.S. system, attention to regulatory issues is a necessary investment by organizations in every state and at the federal level. Details about these efforts is readily accessible on websites for each organization’s trade group. They’re the rule changes, laws and administrative actions to which all are attentive. They’re today’s issues.

Less attention is given the long-term. That focus is often more academic than practical—much the same as Robert Oppenheimer’s early musings about the future of nuclear fusion. But the Manhattan Project produced two bombs (Little Boy and Fat Man) that detonated above the Japanese cities of Hiroshima and Nagasaki in 1945, triggering the end of World War II.

The four issues above should be treated as near and present dangers to the U.S. health system requiring attention in every organization. But responses to these do not define the future of the U.S. system. That’s the Manhattan Project that’s urgently needed in our system.