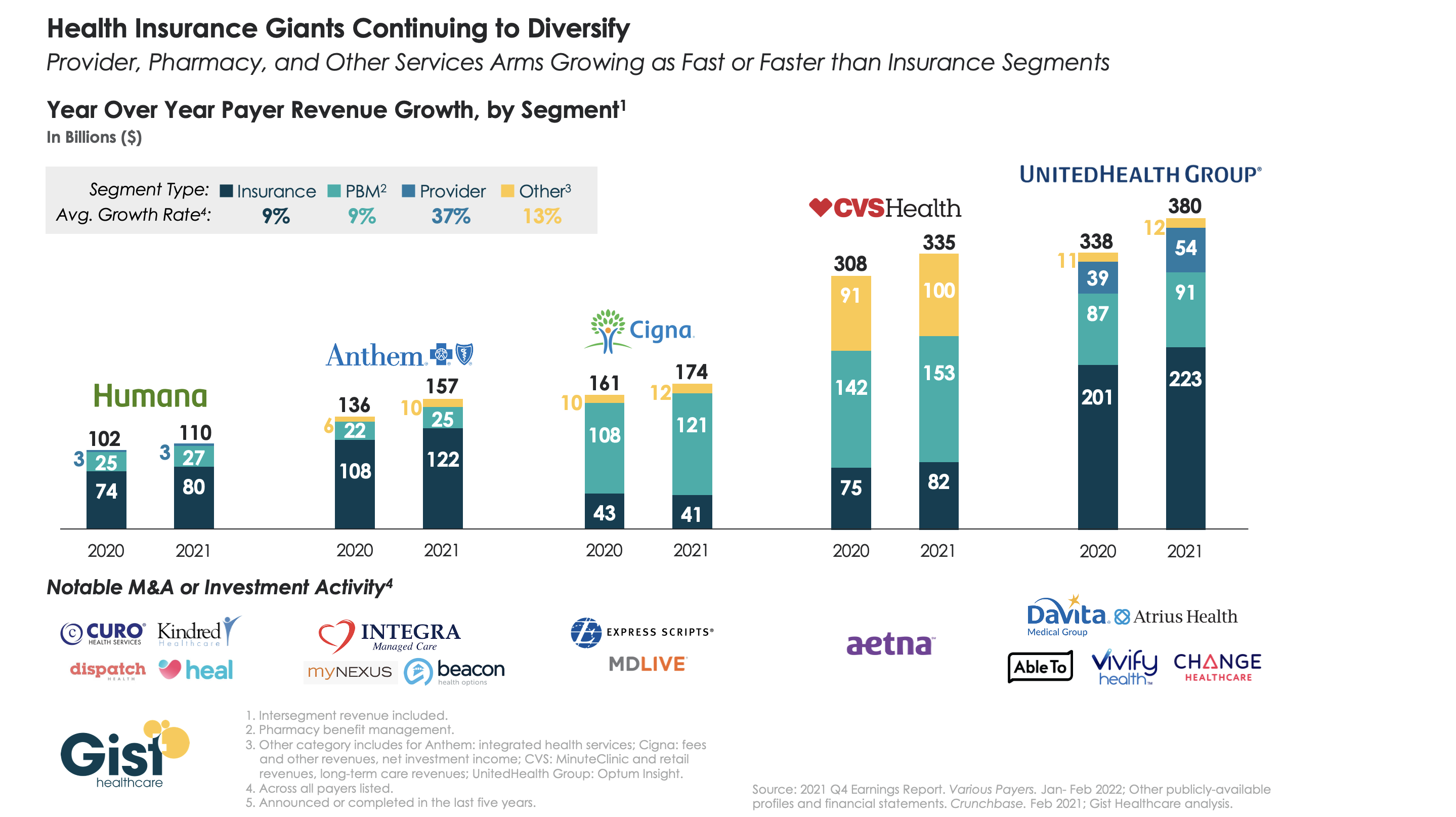

The largest health insurers are quickly becoming vertically integrated healthcare organizations that span the care and coverage continuum. While 2021 was a mixed year for these companies as healthcare volumes bounced back, their diversified portfolios helped cushion losses from higher claims.

The graphic above analyzes revenue growth by segment for the five largest insurers across the last two years. On averagethe insurance and pharmacy benefit management components of the companies grew at nine percent, while care delivery and integrated health services grew at much higher rates. UnitedHealth Group (UHG) and Anthem boasted the highest year-over-year revenue growth, driven by UHG’s Optum subsidiary and Anthem’s integrated health services.

Cigna and CVS Health each earned less than a quarter of their total revenue from their insurance arms lastyear. While Humana lags the others in topline revenue, it has assembled a robust portfolio of care delivery investments and partnerships, surpassed only by UHG.

As antitrust scrutiny on vertical integration increases (case in point: the DOJ is now challenging UHG’s acquisition of Change Healthcare), insurers will face the hard task of integrating their portfolio of service—and demonstrating that they deliver value to consumers and patients.

DOJ alleges that allowing UHG’s Optum subsidiary to acquire Change, a direct competitor used by most large commercial insurers for healthcare claims solutions, would give UHG 75 percent of the healthcare claims processing and management market. This would significantly reduce competition, the DOJ claims, while simultaneously giving UHG access to its competitors’ sensitive plan design and pricing information. UHG called the DOJ’s position ‘deeply flawed’ and promised to fight the case.

The Gist: This is the second big move by antitrust regulators in a week to put the brakes on consolidation in healthcare: shortly after the DOJ sued to block Rhode Island’s two largest health systems, Care New England and Lifespan, from merging, those systems abandoned plans to combine.

We are seeing the first real signs that the Biden administration is following through on plans to more closely scrutinize healthcare deals, including payer-led vertical integration. For both payers and providers, increased scrutiny will place a premium on the consumer value proposition of any combination—and force merging companies to deliver on the benefits of scale.

The Federal Trade Commission is suing to block Rhode Island’s two largest health systems from merging, alleging the tie-up between Lifespan and Care New England would increase prices and diminish the quality of care.

In the state’s own review, Rhode Island’s attorney general said the union would result in “extraordinary market power” and denied the merger application under state law that requires a review of such tie-ups. Rhode Island’s attorney general will join FTC’s federal lawsuit seeking to block the deal.

The FTC alleges that, together, Lifespan and Care New England would control at least 70% of Rhode Island’s market for inpatient hospital services and also reduce competition in several nearby Massachusetts communities.

Dive Insight:

The union between Lifespan, the state’s largest health system, and Care New England, the second largest, quickly raised alarms in Rhode Island.

A 25-page report from the state’s insurance department found that the merger would “significantly alter” the state’s healthcare market, which currently enjoys a “relatively competitive” market. State regulators were also concerned about the control the new system would have over physician services. Given these risks, the state insurance commissioner proposed a set of conditions on the deal including price caps. Health system executives were open to working under certain conditions.

However, executives seemed surprise by Thursday’s announcement that the deal to create an integrated academic medical system with Brown University at the forefront would be blocked.

“On four separate occasions in prior years, the FTC reviewed the same proposed merger and allowed it to proceed,” a joint statement released Thursday said. The management teams said they offered up 30 conditions to regulators to satisfy antitrust concerns about the merger, “but neither the FTC or the AG ever discussed these conditions or others with the two systems prior to today’s decisions,” according to the statement.

After flirting with the idea of combining the systems for years, Lifespan and Care New England inked a deal to merge last February after the coronavirus pandemic revived talks.

The two touted the deal as a way to create an integrated academic health system with Brown University’s medical school in a central role. Brown University committed $125 million to the creation of the new system.

However, FTC commissioners voted unanimously to block the union over concerns it would extinguish competition between the two.

And although regulators have long leaned on the argument that hospital mergers lead to higher prices, a joint letter from FTC Chair Lina Khan and Commissioner Rebecca Kelly Slaughter points to the harmful effects consolidation has on labor markets, an argument growing in importance within the agency.

“Just as we want firms to compete with each other to sell goods and services to their customers, we want employers to compete with each other to attract and retain workers,” the letter states. “Indeed, there is a growing body of empirical research about the potential for competitive harm to labor markets from consolidation and concentration.”

The news follows reports that the Department of Justice is preparing to sue to stop UnitedHealth Group’s blockbuster acquisition of Change Healthcare, a healthcare technology firm. Concerned about the “massive consolidation” of healthcare data, the American Hospital Association urged antitrust regulators to thoroughly examine the proposed transaction in a letter sent to DOJ last spring.

After taking office, President Joe Biden has signaled his administration would take an aggressive antitrust stance, including getting tough on hospital mergers. Last summer, the president issued an executive order that called on antitrust regulators to “review and revise” merger guidelines to ensure patients are not harmed by proposed deals.

Biden specifically called out the healthcare industry, rife with consolidation and accompanying research that shows hospital unions lead to higher prices.

“Thanks to unchecked mergers, the ten largest healthcare systems now control a quarter of the market,” the release from the White House said.

Still, the FTC has become overwhelmed by the sheer number of proposed transactions. In August, the agency said it was hit by a “tidal wave” of merger filings and warned applicants it may not vet all submissions before the applicable deadlines. But in letters sent to merging companies, the FTC warned the delay should not be interpreted as a green light for any deal.

“Companies that choose to proceed with transactions that have not been fully investigated are doing so at their own risk,” the regulator said in a statement.

Los Angeles-based Prospect Medical Holdings has inked deals to sell its seven hospitals in Connecticut and Pennsylvania.

The company announced Feb. 10 that it is selling three Connecticut hospitals with a combined 708 beds to Yale New Haven (Conn.) Health System. The deal is expected to close later this year. If the deal is finalized, the hospitals will transition from for-profit to nonprofit organizations.

Prospect Medical Holdings announced Feb. 11 that it is selling Crozer Health, a four-hospital system based in Springfield, Pa., to Newark, Del.-based ChristianaCare. Under the deal, ChristianaCare would acquire Crozer’s hospitals, medical group, ambulatory centers and clinics. Crozer’s hospitals have more than 800 beds combinded.

The deal with ChristianaCare was announced the same day Crozer got a new CEO. The health system appointedKevin Spiegel, senior vice president of strategy and revenue development at Prospect, as its new CEO. He replaced Peter Adamo, who served in that role at Crozer for two years. Mr. Adamo’s last day at Crozer was Feb. 11, according to the Philadelphia Business Journal.

“The pandemic has demonstrated the vital importance of working together to meet the clinical needs of the communities we serve,” Mr. Spiegel said in a Feb. 11 news release. “We are excited by the potential to join these two great organizations so that we can continue to provide the high-quality, accessible care that our communities — Delaware County and beyond — rely on.”

The sale of the hospitals to ChristianaCare is expected to close in the second half of this year. If the deal is finalized, Crozer would become a nonprofit organization.

Overall health sector M&A activity bounced back in 2021 across nearly every subsector except one: hospitals, which saw a significant decrease in deal volume. Drawing on data from Kaufman Hall, the graphic above shows the scale of the most recent wave of health system consolidation, driven by last year’s eight “mega-mergers” between entities with over $1B in annual revenue each.

While the total number of hospital transactions decreased, the average seller size increased, with the total valuation of all hospital M&A activity nearly tripling from 2020 to 2021. With a dwindling number of independent hospitals left, health systems are pursuing larger combinations with their peers, to achieve greater scale and maintain economic “relevance.”

But as systems who have struggled to complete such mergers can attest, getting a larger deal across the finish line isn’t easy. The path to hospital consolidation now hinges on navigating complex organizational structures and issues of cultural compatibility, in addition to simply identifying “synergies” and avoiding antitrust pitfalls.

HCA has purchased MD Now Urgent Care, Florida’s largest urgent care chain, adding 59 urgent care centers to its existing 170. Meanwhile Tenet’s $1.1B deal to buy SurgCenter Development cements its position as the nation’s largest ambulatory surgery center (ASC) operator, eclipsing Envision-owned AMSURG and Optum-owned Surgical Care Affiliates.

The Gist: Healthcare services are increasingly moving outpatient and even virtual—a trend only accelerated by the pandemic. With this latest acquisition, Tenet will now own or operate nearly seven times as many ASCs as hospitals. Such national, for-profit systems are looking to add more non-acute assets to their portfolios, to capitalize on a shift fueled by both consumer preference for greater convenience, and purchaser pressure to reduce care costs.

The boom in global mergers and acquisitions in 2021 will surge into 2022, fueled by abundant investment capital, historically low interest rates and a rebound in global economic growth, according to a survey of 345 corporate dealmakers in the U.S. by KPMG.

“Based on the volume of new pitches in November and December — transactions that would come to market in Q1 and Q2 of 2022 — there are no signs of a slowing deal market,” according to Philip Isom, global head of M&A at KPMG. While facing high valuations, “most investors have limited time horizons to invest in, so they may be willing to reach further on price than they have historically.”

More than 80% of the survey respondents across several industries expect total M&A valuations to rise further next year, with about one out of every three predicting at least a 10% increase, KPMG said. Dealmakers said transaction levels will remain robust because companies “need to remain on the offense with the competition” and “feel pressure from investors to raise their own valuations.”

Dive Insight:

Worldwide deal value from January until mid-November this year hit $5.1 trillion, the highest level since 2015 and a 34% gain compared with all of 2020, KPMG said. U.S. transactions rose to $2.9 trillion, or 55% more than during all of last year.

M&A has soared in 2021 as the economy recovered from a pandemic shock, record monetary and fiscal stimulus pumped up liquidity and many companies sought through acquisitions to regain their footing after months of lockdowns and persistent supply chain disruptions.

A widespread labor shortage will probably push up dealmaking next year. One-third of survey respondents said they want to use M&A to acquire talent, KPMG said.

Also, companies increasingly use acquisitions to change their business or operating models, KPMG said, noting that industrial and financial services companies buy companies that help speed their digital transformation.

“The aim is to increase efficiencies and contribute to having more agile workforces,” according to Carole Streicher, KPMG’s deal advisory and strategy service group leader in the U.S.

Private equity firms will continue to push up the volume and value of M&A next year, after increasing their involvement in transaction value by more than 55% so far in 2021, KPMG said. PE firms have pursued deals this year in part because of the prospect of an increase in corporate capital gains taxes.

Growing support for sustainability among investors, regulators and other stakeholders may prompt M&A, “as businesses look at their ecological footprint and consider purchasing, rationalizing or divesting assets,” KPMG said. Investors are likely to consider sustainable businesses more adaptable to market shifts.

Finally, concerns about the potential for rising borrowing costs may prompt dealmakers who rely on debt financing to speed up acquisition plans. Federal Reserve Chair Jerome Powell late last month said policymakers at their two-day meeting beginning Tuesday will likely consider speeding up the withdrawal of accommodation.

Dealmakers face some headwinds. Democrats in the Senate have yet to muster enough support for a roughly $2 trillion social policy bill that would help sustain economic growth. Meanwhile, the outbreak of the omicron variant of COVID-19 has highlighted the fragility of financial markets and the economy to any setbacks in curbing the pandemic.

Survey respondents identified several factors that will influence dealmaking next year, with 61% underscoring high valuations, 56% pointing to liquidity and other economic considerations, and 55% noting intense competition for a limited number of highly valued acquisition targets, KPMG said.

Still, only 7% of the survey respondents said they expect deal volumes to decline in their industries next year.

Survey respondents work at companies in industries ranging from media and financial services to energy and technology, with 194 of them CFOs, CEOs or other C-suite executives.

In 2020, a record-breaking 19 rural hospitals closed their doors due to a combination of worsening economic conditions, changing payer mix, and declining patient volumes. But many more are looking to affiliate with larger health systems to remain open and maintain access to care in their communities. The graphic above illustrates how rural hospital affiliations (including acquisitions and other contractual partnerships) have increased over time, and the resulting effects of partnerships.

Affiliation rose nearly 20 percent from 2007 to 2016; today nearly half of rural hospitals are affiliated with a larger health system.

Economic stability is a primary benefit: the average rural hospital becomes profitable post-affiliation, boosting its operating margin roughly three percent in five years. But despite improved margins, many affiliated rural hospitals cut some services, often low-volume obstetrics programs, in the years following affiliation.

Overall, the relationship likely improves quality: a recent JAMA study found that rural hospital mergers are linked to better patient mortality outcomes for certain conditions, like acute myocardial infarction. Still, the ongoing tide of rural hospital closures is concerning, leaving many rural consumers without adequate access to care. Late last month, the Department of Health and Human Services announced it would distribute another $7.5B in American Rescue Plan Act funds to rural providers.

While this cash infusion may forestall some closures, longer-term economic pressures, combined with changing consumer demands, will likely push a growing number of rural hospitals to seek closer ties with larger health systems.