Franklin, Tenn.-based CHS, which reported a net loss of $20 million in the first quarter on revenues of $3.1 billion, is on the hunt for new acquisitions just as it is also in discussions to sell off more assets.

“We are considering further opportunities to expand our portfolio,” CEO Tim Hingtgen said in a webcast discussing first-quarter results.

Selling off certain assets would also help balance the system and further reduce some of its debt, President and CFO Kevin Hammons confirmed on the call.

“Moreover, we may give consideration to divesting certain additional hospitals and non-hospital businesses,” CHS said in an SEC filing. “Generally, these hospitals and non-hospital businesses are not in one of our strategically beneficial services areas, are less complementary to our business strategy and/or have lower operating margins. In addition, we continue to receive interest from potential acquirers for certain of our hospitals and non-hospital businesses.”

The health system, which operates 79 hospitals in 15 states, has agreed to sell four more hospitals effective Jan. 1, the filing stated.

CHS recently completed the $92 million sale of Oak Hill, W.Va.-base Plateau Medical Center to Charleston, W.Va.-based Vandalia Health. It also finalized on Jan. 3 an $85 million sale of its former 122-bed facility in Ronceverte, W.Va, also to Vandalia Health.

CHS shares were trading at $6.24 before its results were released. It is currently trading at approximately $3.70.

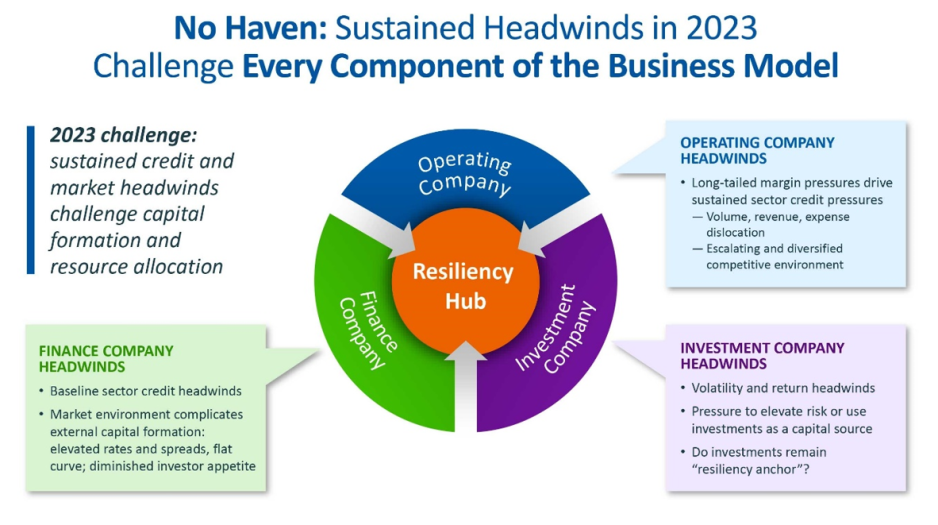

For the first time in recent history, we saw all three functions of the not-for-profit healthcare system’s financial structure suffer significant and sustained dislocation over the course of the year 2022 (Figure above).

The headwinds disrupting these functions are carrying over into 2023, and it is uncertain how long they will continue to erode the operating and financial performance of not-for-profit hospitals and health systems.

The Operating Function is challenged by elevated expenses, uncertain recovery of service volumes, and an escalating and diversified competitive environment.

The Finance Function is challenged by a more difficult credit environment (all three rating agencies

now have a negative perspective on the not-forprofit healthcare sector), rising rates for debt, and a diminished investor appetite for new healthcare debt issuance. Total healthcare debt issuance in 2022 was $28 billion, down sharply from a trailing two-year average of $46 billion.

The Investment Function is challenged by volatility and heightened risk in markets concerned with the Federal Reserve’s tightening of monetary policy and the prospect of a recession. The S&P 500—a major stock index—was down almost 20% in 2022. Investments had served as a “resiliency anchor” during the first two years of the pandemic; their ability to continue to serve that function is now in question.

A significant factor in Operating Function challenges is labor: both increases in the cost of labor and staffing shortages that are forcing many organizations to run at less than full capacity. In Kaufman Hall’s 2022 State of Healthcare Performance Improvement Survey, for example, 67% of respondents had seen year-over-year increases of more than 10% for clinical staff wages, and 66% reported that they had run their facilities at less-than-full capacity because of staffing shortages.

These are long-term challenges,

dependent in part on increasing the pipeline of new talent entering healthcare professions, and they will not be quickly resolved. Recovery of returns from the Investment Function is similarly uncertain. Ideally, not-for-profit health systems can maintain a one-way flow of funds into the Investment Function, continuing to build the basis that generates returns. Organizations must now contemplate flows in the other direction to access

funds needed to cover operating losses, which in many cases would involve selling invested assets at a loss in a down market and reducing the basis available to generate returns when markets recover.

The current situation demonstrates why financial reserves are so important:

many not-for-profit hospitals and health systems will have to rely on them to cover losses until they can reach a point where operations and markets have stabilized, or they have been able to adjust their business to a new, lower margin environment. As noted above, relief funding and the MAAP program helped bolster financial reserves after the initial shock of the pandemic. As the impact of relief funding wanes and organizations repay remaining balances under the MAAP program, Days Cash on Hand has begun to shrink, and the need to cover operating losses is hastening this decline. From its highest

point in 2021, Days Cash on Hand had decreased, as of September 2022, by:

29% at the 75th percentile, declining from 302 to 216 DCOH (a drop of 86 days)

28% at the 50th percentile, declining from 202 to 147 DCOH (a drop of 55 days)

49% at the 25th percentile, declining from 67 to 34 DCOH (a drop of 33 days)

Financial reserves are playing the role for which they were intended; the only question is whether enough not-for-profit hospitals and health systems have built sufficient reserves to carry them through what is likely to be a protracted period of recovery from the pandemic.

KEY TAKEAWAYS

All three functions of the not-for-profit healthcare system’s financial structure—operations, finance, and investments—suffered significant and sustained dislocation over the course of 2022.

These headwinds will continue to challenge not-forprofit

hospitals and health systems well into 2023.

Days Cash on Hand is showing a steady decline, as the impact of relief funding recedes and the need to cover operating losses persists.

Financial reserves are playing a critical role in covering operating losses as hospitals and health systems struggle to stabilize their operational and financial performance.

Conclusion

Not-for-profit hospitals and health systems serve many community needs. They provide patients access to healthcare when and where they need it. They invest in new technologies and treatments that offer patients and their families lifesaving advances in care. They offer career opportunities to a broad range of highly skilled professionals, supporting the economic health of the communities they serve.

These services and investments are expensive and cannot be covered solely by the revenue received from providing care to patients.

Strong financial reserves are the foundation of good financial stewardship for not-for-profit hospitals and health systems.

Financial reserves help fund needed investments in facilities and technology, improve an organization’s debt capacity, enable better access to capital at more affordable interest rates, and provide a critical resource to meet expenses when organizations need to bridge periods of operational disruption or financial distress. Many hospitals and health systems today are relying on the strength of their reserves to navigate a difficult

environment; without these reserves, they would not be able to meet their expenses and would be at risk of closure.

Financial reserves, in other words, are serving the very purpose for which they are intended—ensuring that hospitals and health systems can continue to serve their communities in the face of challenging operational and financial headwinds.

When these headwinds have subsided, rebuilding these reserves should be a top priority to ensure that our not-for-profit hospitals and health systems can remain a vital resource for the communities they serve.

Hospital margins continued to stabilize in March with a slight improvement over February, according to data from Kaufman Hall’s National Hospital Flash Report. However, margins remain below pre-pandemic levels, leaving hospitals in a vulnerable position should a recession or a new public health emergency materialize.

For provider practices, physician productivity increased but the increased revenues could not keep pace expenses, according to the quarterly Physician Flash Report.

While things appear relatively calm at the moment, there remain significant challenges—specifically labor shortages and diminished margins—that could quickly reach the surface if hospitals and health systems are faced with another crisis.

Kaufman Hall experts are seeing increased reliance on advanced practice providers (APPs)—e.g. Nurse Practitioners and Physician Associates—and note that those that hire, retain and deploy this critical workforce most effectively will see more success in the long term.

Here is a summary of recent credit downgrades and outlook revisions for hospitals and health systems going back to the most recent major roundup March 16.

The various downgrades reflect continued operating challenges many nonprofit systems are facing and will likely continue to deal with for some years to come. The most recent downgrades and revisions, which have not been included in any more recent roundups, are listed first.

Baptist Health Care (Pensacola, Fla.):

BHC had the rating downgraded on a series of its bonds as a reflection of “pressured operating performance and cash flow,” S&P Global said April 19.

As well as typical industry pressures of inflation and labor expenses, the three-hospital system may face further challenge because of a replacement project for its flagship Baptist Hospital that is due to be completed in late 2023.

Beacon Health (South Bend, Ind.):

Beacon Health System had its outlook revised to negative from stable on “AA-” rated bonds it holds, S&P Global said April 14.

The move reflects weaker operating results and an expectation of increased debt over the near term.

Kuakini Health System (Honolulu):

Kuakini Health System, which has a “CCC” long-term rating, has been placed on CreditWatch with negative implications, S&P Global said April 14.

The move reflects the system’s sustained operating challenges with no foreseeable major changes and questions about its long-term viability, the agency said, describing the system’s “precarious financial position.”

Baystate Health (Springfield, Mass.):

Baystate Health had ratings downgraded on specific bonds related to its flagship medical center, S&P Global said April 12.

While ratings were affirmed on other debt, those on others specific to the 780-bed Baystate Medical Center were downgraded to “A” from “A+” as the system’s operating challenges continue into 2023, the agency said.

Penn State Health (Hershey, Pa.):

Higher-than-expected operating losses have led to Penn State Health being downgraded on a series of bonds from “A+” to “A,” S&P Global said April 6.

Original budgets for the first part of fiscal 2023 targeted a slightly positive full-year operating margin, but data shows a $75 million lower-than-forecasted figure, S&P Global said. Operating income showed a loss of $154.5 million for the six months ending Dec. 31 compared with a $48.8 million loss in all of fiscal 2022.

Legacy Health(Portland, Ore.):

Legacy Health had its outlook revised to negative from stable amid expectations the eight-hospital system will continue to experience difficult operating conditions and concern it will continue to fail to meet debt obligations, Moody’s said April 5.

The rating on its revenue bonds was affirmed at “A1.” Total debt stands at $738 million.

Providence (Renton, Wash.):

The 51-hospital system recorded the first of three downgrades in the space of a few weeks March 17 when Fitch Ratings attached an “A” grade to both the system’s default rating and a series of bonds worth approximately $7.4 billion. The outlook for the system is negative due to its higher-than-average debt loads, Fitch said.

S&P Global then downgraded Providence to the same notch from “A+” March 21 amid higher expenses and an expectation of only a multiyear process of recovery. The outlook for the system was also negative given the steep operating losses that need to be dealt with, S&P said.

Finally, Providence was downgraded by Moody’s on a series of bonds from “A1” to “A2.

Thomas Jefferson (Philadelphia):

Thomas Jefferson University has undergone a credit downgrade with cash flow margins expected to stay low for “several years,” Moody’s said March 30.

The 18-hospital system, which also operates 10 colleges located primarily on two campuses in Philadelphia, is expected to stabilize its days of cash on hand to about 140, but debt will remain high, Moody’s said. The outlook is stable.

Oaklawn Hospital (Marshall, Mich.):

The 68-bed community hospital was downgraded to “BBB-” from “BBB” as it reported operating losses due to higher expenses and length of patient stay, Fitch Ratings said March 29.

The downgrade refers both to its default rating and on bonds worth $63.5 million. The outlook is negative.

DCH Health (Tuscaloosa, Ala.):

The three-hospital system saw its rating on a series of bonds lowered to “A-” from “A” as it continues to suffer operating losses, S&P Global said March 29.

The system’s “deeply negative underlying operations” are unlikely to lead to any substantial improvement in the near future, the agency said.

DCH Health operates a total of 510 staffed beds.

AU Health System (Augusta, Ga.):

The system, which is being pursued by Marietta, Ga.-based Wellstar Health, was downgraded March 23 amid concern over negative cash flow and that it may breach covenant agreements later this year, Moody’s said.

The downgrade to “B2” from “Ba3” applies to revenue bonds the system holds. The outlook is negative.

PeaceHealth (Vancouver, Wash.):

“Considerable operating stress” was the driver behind Fitch Ratings downgrading the 10-hospital system March 21.

The downgrade to “A+” from “AA-” applied to both the system’s default rating and on a series of bonds. The outlook is stable.

Management is targeting a return to profitability by fiscal 2026, Fitch noted.

Mercy Iowa CityHospital:

The hospital, part of Des Moines, Iowa-based MercyOne, was downgraded March 16 to “Caa1” from “B1” because of what Moody’s called “severe cash flow deterioration.” The “Caa1” categorization is seen as “substantial risk.”

According to a new report from the American Hospital Association (AHA), hospitals and health systems are facing significant financial pressures from rising expenses, including for labor, drugs, medical supplies and more. And without increased government support, the organization warns that patients’ access to care could be at risk.

Hospitals continue to see expenses grow, negative margins

In the report, AHA writes that several factors, including historic inflation and critical workforce shortages leading to a reliance on contract labor, led to “2022 being the most financially challenging year for hospitals since the pandemic began.”

According to data from Syntellis Performance Solutions, overall hospital expenses increased by 17.5% between 2019 and 2022 — more than double the increases in Medicare reimbursements during the same time. Between 2019 and 2022, Medicare reimbursement only grew by 7.5%.

With expenses significantly outpacing reimbursement, hospital margins have been consistently negative over the last year. In fact, AHA noted that “over half of hospitals ended 2022 operating at a financial loss — an unsustainable situation for any organization in any sector, let alone hospitals.”

So far, this trend has continued into 2023, with hospitals reporting negative median operating margins in both January and February.

A recent analysis also found that the first quarter of 2023 had the largest number of bond defaults among hospitals in over 10 years.

Between 2019, and 2022 hospital labor expenses increased by 20.8%, a rise that was largely driven by a growing reliance on contract labor to fill in workforce gaps during the pandemic. Even after accounting for an increase in patient acuity, labor expenses per patient increased by 24.7%.

Compared to pre-pandemic levels, hospitals saw a 56.8% increase in the rates they were charged for contract employees in 2022. Overall, hospitals’ contract labor expenses increased by a “staggering” 257.9% in 2022 compared to 2019 levels.

A sharp rise in inflation in recent months has also led to a significant increase in hospitals’ non-labor expenses, particularly for drugs and medical expenses. According to a report by Kaufman Hall, just non-labor expenses would lead to a $49 billion one-year expense increase for hospitals and health systems.

Since 2019, non-labor expenses have grown 16.6% per patient. Hospitals’ expenses for drugs and medical supplies/equipment have seen similar increases per patient at 19.7% and 18.5%, respectively. Costs of laboratory services (27.1%), emergency services (31.9%), and purchased services, including IT and food and nutrition services, (18%) have also increased significantly per patient.

Outside of labor and non-labor expenses, AHA writes that policies from health insurers have also contributed to significant burden among hospital staff and increased administrative costs. Currently, administrative costs account for up to 31% of total healthcare spending — of which, billing and insurance makes up 82%.

With the COVID-19 public health emergency ending on May 11, several important hospital waivers and flexibilities will soon end, and “[t]he downstream effects of this will be wide-ranging as hospitals will be faced with a set of additional challenges,” AHA writes.

“Rising costs for drugs, supplies, and labor coupled with sicker patients, longer hospital stays, and government reimbursement rates that do not come close to covering the costs of caring for patients have created a dire situation for hospitals and health systems,” said AHA president and CEO Rick Pollack.

“This is not just a financial problem; it is an access problem.

When healthcare providers cannot afford the tools and teams they need to care for patients, they will be forced to make hard choices and the people who will be impacted the most are patients. We can’t let that happen. Congress and others must act to preserve the care our nation needs and depend on.”

To address these financial challenges and ensure that hospitals are able to continue caring for patients, AHA has suggested several actions Congress could take to support hospitals going forward, including:

Enacting policies to support efforts to boost the healthcare workforce and ensure of future pipeline of professionals to combat longstanding labor shortages

Rejecting attempts to cut Medicare or Medicaid payments to hospitals, which could further reduce patients’ access to care

Encouraging CMS to use its “special exceptions and adjustments” to make retrospective adjustments to account for differences between what was implemented for fiscal year 2022 and what is currently projected

Creating a special statutory designation and providing additional support to hospitals that serve historically marginalized communities

“As the hospital field maintains its commitment to care in the face of significant challenges, policymakers must step up and help protect the health and well-being of our nation by ensuring America has strong hospitals and health systems,” AHA writes.

Using data from Kaufman Hall’s National Hospital Flash Report, as well as publicly available investor reports for some of the nation’s largest nonprofit health systems, the graphic above takes stock of the current state of health system margins.

The median US hospital has now maintained a negative operating margin for a full year. Some good news may be on the horizon, as the picture is slightly less gloomy than a year ago, with year-over-yearrevenues increasing seven points more than total expenses.

However, the external conditions suppressing operating margins aren’t expected to abate, and many large health systems are still struggling.

Among large national non-profits Ascension, CommonSpirit Health, Providence, and Trinity Health, operating income in FY 2022 decreased 180 percent on average, and investment returns fell by 150 percent on average, compared to the year prior.

While health systems’ drop in investment returns mirrors the overall stock market downturn, and is largely comprised of unrealized returns, systems may not be able to rely on investment income to make up for ongoing operating losses.

On today’s episode of Gist Healthcare Daily, Kaufman Hall co-founder and Chair Ken Kaufman joins the podcast to discuss his recent blog that examines Ford Motor Company’s decision to stop producing internal-combustion sedans, and talk about whether there are parallels for health system leaders to ponder about whether their traditional strategies are beginning to age out.