Tuesday marked the start of the tenth season of open enrollment in the ACA’s health insurance exchanges. Last year, a record 14.5M Americans obtained coverage through the exchanges, and this year’s total is expected to surpass that. That’s thanks to the extended subsidies included in the Inflation Reduction Act, a fix to the “family glitch” that prevented up to 1M low-income families from accessing premium assistance, and expanded offerings by most major insurers, who have been enticed by the exchanges’ recent stability. The average unsubsidized premium for benchmark silver plans in 2023 is expected to rise by about four percent, but the enhanced financial assistance will lower net premiums for most enrollees.

The Gist: ACA marketplace enrollment has grown nearly 80 percent since opening in 2014, and exchange plans now cover 4.5 percent of Americans. After enrollment lagged during the Trump administration,the combination of policy fixes and improved risk pools are attracting insurers back into the exchanges, where enrollees are finding more affordable plans than ever before.

We consider this a commendable first decade, but the success of the exchanges over the next ten years remains subject to political winds. Congress must revisit the extended subsidies by 2025, and a different administration might deprioritize marketplace advertising and navigation support, policies have which proven crucial to the exchanges’ recent growth.

Hospitals in the United States are on track for their worst financial year in decades. According to a recent report, median hospital operating margins were cumulatively negative through the first eight months of 2022. For context, in 2020, despite unprecedented losses during the initial months of COVID-19, hospitals still reported median eight-month operating margins of 2 percent—although these were in large part buoyed by federal aid from the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

The recent, historically poor financial performance is the result of significant pressures on multiple fronts. Labor shortages and supply-chain disruptions have fueled a dramatic rise in expenses, which, due to the annually fixed nature of payment rates, hospitals have thus far been unable to pass through to payers. At the same time, diminished patient volumes—especially in more profitable service lines—have constrained revenues, and declining markets have generated substantial investment losses.

While it’s tempting to view these challenges as transient shocks, a rapid recovery seems unlikely for a number of reasons. Thus, hospitals will be forced to take aggressive cost-cutting measures to stabilize balance sheets. For some, this will include department or service line closures; for others, closing altogether. As these scenarios unfold, ultimately, the costs will be borne by patients, in one form or another.

Hospitals Face A Difficult Road To Financial Recovery

There are several factors that suggest hospital margins will face continued headwinds in the coming years. First, the primary driver of rising hospital expenses is a shortage of labor—in particular, nursing labor—which will likely worsen in the future. Since the start of the pandemic, hospitals have lost a total of 105,000 employees, and nursing vacancieshave more than doubled. In response, hospitals have relied on expensive contract nurses and extended overtime hours, resulting in surging wage costs. While this issue was exacerbated by the pandemic, the national nursing shortage is a decades-old problem that—with a substantial portion of the labor force approaching retirement and an insufficient supply of new nurses to replace them—is projected to reach 450,000 by 2025.

Second, while payment rates will eventually adjust to rising costs, this is likely to occur slowly and unevenly. Medicare rates, which are adjusted annually based on an inflation projection, are already set to undershoot hospital costs. Given that Medicare doesn’t issue retrospective corrections, this underadjustment will become baked into Medicare prices for the foreseeable future, widening the gap between costs and payments.

This leaves commercial payers to make up the difference. Commercial rates are typically negotiated in three- to five-year contract cycles, so hospitals on the early side of a new contract may be forced to wait until renegotiation for more substantial pricing adjustments. “Negotiation” is also the operative term here, as payers are under no obligation to offset rising costs. Instead, it is likely that the speed and degree of price adjustments will be dictated by provider market share, leaving smaller hospitals at a further disadvantage. This trend was exemplified during the 2008 financial crisis, in which only the most prestigious hospitals were able to significantly adjust pricing in response to historic investment losses.

Finally, economic uncertainty and the threat of recession will create continued disruptions in patient volumes, particularly with elective procedures. Although health care has historically been referred to as “recession-proof,” the growing prevalence of high-deductible health plans (HDHPs) and more aggressive cost-sharing mechanisms have left patients more exposed to health care costs and more likely to weigh these costs against other household expenditures when budgets get tight. While this consumerist response is not new—research on previous recessions has identified direct correlations between economic strength and surgical volumes—the degree of cost exposure for patients is historically high. Since 2008, enrollment in HDHPs has increased nearly four-fold, now representing 28 percent of all employer-sponsored enrollments. There’s evidence that this exposure is already impacting patient decisions. Recently, one in five adults reported delaying or forgoing treatment in response to general inflation.

Taken together, these factors suggest that the current financial pressures are unlikely to resolve in the short term. As losses mount and cash reserves dwindle, hospitals will ultimately need to cut costs to stem the bleeding—which presents both challenges and opportunities.

Direct And Indirect Consequences For Cost, Quality, And Access To Care

Inevitably, as rising costs become baked into commercial pricing, patients will face dramatic premium hikes. As discussed above, this process is likely to occur slowly over the next few years. In the meantime, the current challenges and the manner in which hospitals respond will have lasting implications on quality and access to care, particularly among the most vulnerable populations.

Likely Effects On Patient Experience And Quality Of Care

Insufficient staffing has already created substantial bottlenecks in outpatient and acute-care facilities, resulting in increased wait times, delayed procedures, and, in extreme cases, hospitals diverting patients altogether. During the Omicron surge, 52 of 62 hospitals in Los Angeles, California, were reportedly diverting patients due to insufficient beds and staffing.

The challenges with nursing labor will have direct consequences for clinical quality. Persistent nursing shortages will force hospitals to increase patient loads and expand overtime hours, measures that have been repeatedly linked to longer hospital stays, more clinical errors, and worse patient outcomes. Additionally, the wave of experienced nurses exiting the workforce will accelerate an already growing divide between average nursing experience and the complexity of care they are asked to provide. This trend, referred to as the “Experience-Complexity Gap,” will only worsen in the coming years as a significant portion of the nursing workforce reaches retirement age. In addition to the clinical quality implications, the exodus of experienced nurses—many of whom serve in crucial nurse educator and mentorship roles—also has feedback effects on the training and supply of new nurses.

Staffing impacts on quality of care are not limited to clinical staff. During the initial months of the pandemic, hospitals laid off or furloughed hundreds of thousands of nonclinical staff, a common target for short-term payroll reductions. While these staff do not directly impact patient care (or billed charges), they can have a significant impact on patient experience and satisfaction. Additionally, downsizing support staff can negatively impact physician productivity and time spent with patients, which can have downstream effects on cost and quality of care.

Disproportionate Impacts On Underserved Communities

Reduced access to care will be felt most acutely in rural regions. A recent report found that more than 30 percent of rural hospitals were at risk of closure within the next six years, placing the affected communities—statistically older, sicker, and poorer than average—at higher risk for adverse health outcomes. When rural hospitals close, local residents are forced to travel more than 20 miles further to access inpatient or emergency care. For patients with life-threatening conditions, this increased travel has been linked to a 5–10 percent increase in risk of mortality.

Rural closures also have downstream effects that further deteriorate patient use and access to care. Rural hospitals often employ the majority of local physicians, many of whom leave the community when these facilities close. Access to complex specialty care and diagnostic testing is also diminished, as many of these services are provided by vendors or provider groups within hospital facilities. Thus, when rural hospitals close, the surrounding communities lose access to the entire care continuum. As a result, individuals within these communities are more likely to forgo treatment, testing, or routine preventive services, further exacerbating existing health disparities.

In areas not affected by hospital closures, access will be more selectively impacted. After the 2008 financial crisis, the most common cost-shifting response from hospitals was to reduce unprofitable service offerings. Historically, these measures have disproportionately impacted minority and low-income patients, as they tend to include services with high Medicaid populations (for example, psychiatric and addiction care) and crucial services such as obstetrics and trauma care, which are already underprovided in these communities. Since 2020, dozens of hospitals, both urban and rural, have closed or suspended maternity care. Similar to closure of rural hospitals, these closures have downstream effects on local access to physicians or other health services.

Potential For Productive Cost Reduction And The Need For A Measured Policy Response

Despite the doom-and-gloom scenario presented above, the focus on hospital costs is not entirely negative. Cost-cutting measures will inevitably yield efficiencies in a notoriously inefficient industry. Additionally, not all facility closures negatively impact care. While rural facility closures can have dire consequences in health emergencies, studies have found that outcomes for non-urgent conditions remained similar or actually improved.

Historically, attempts to rein in health care spending have focused on the demand side (that is, use) or on negotiated prices. These measures ignore the impact of hospital costs, which have historically outpaced inflation and contributed directly to rising prices. Thus, the current situation presents a brief window of opportunity in which hospital incentives are aligned with the broader policy goals of lowering costs. Capitalizing on this opportunity will require a careful balancing act from policy makers.

In response to the current challenges, the American Hospital Association has already appealed to Congress to extend federal aid programs created in the CARES Act. While this would help to mitigate losses in the short term, it would also undermine any positive gains in cost efficiency. Instead of a broad-spectrum bailout, policy makers should consider a more targeted approach that supports crucial community and rural services without continuing to fund broader health system inefficiencies.

The establishment of Rural Emergency Hospitals beginning in 2023 represents one such approach to eliminating excess costs while preventing negative patient consequences. This rule provides financial incentives for struggling critical access and rural hospitals to convert to standalone emergency departments instead of outright closing. If effective, this policy would ensure that affected communities maintain crucial access to emergency care while reducing overall costs attributed to low-volume, financially unviable services.

Policies can also help promote efficiencies by improving coverage for digital and telehealth services—long touted as potential solutions to rural health care deserts—or easing regulations to encourage more effective use of mid-level providers.

Conclusion

The financial challenges facing hospitals are substantial and likely to persist in the coming years. As a result, health systems will be forced to take drastic measures to reduce costs and stabilize profit margins. The existing challenges and the manner in which hospitals respond will have long-term implications for cost, quality, and access to care, especially within historically underserved communities. As with any crisis, though, they also present an opportunity to address industrywide inefficiencies. By relying on targeted, evidence-based policies, policy makers can mitigate the negative consequences and allow for a more efficient and effective system to emerge.

Drawing on a report published by the North Carolina State Health Plan for Teachers and State Employees, a recent Kaiser Health News article shines a light on the lack of transparency in financial reporting of not-for-profit hospitals’ community benefit obligations.

The report claims many North Carolina hospitals—including the state’s largest system, Atrium Health—show profits on Medicare patients in their cost report filings, while at the same time claiming sizable unrecouped losses on Medicare patients as a part of their overall community benefit analyses.

The Gist: These kind of reporting discrepancies draw attention to the controversial issue of whether not-for-profit hospitals provide sufficient community benefit to compensate for their tax-exempt status, which was worth nearly $2 billion in 2020 for North Carolina hospitals alone.

Greater transparency around charity care, community benefit, and losses sustained from public payerscould go a long way toward shoring up stakeholder support for not-for-profit institutions at a time when their political goodwill has deteriorated. Hospitals should be proactive on this front, as political leaders increasingly train their sites on high hospital spending in the current tight economic environment.

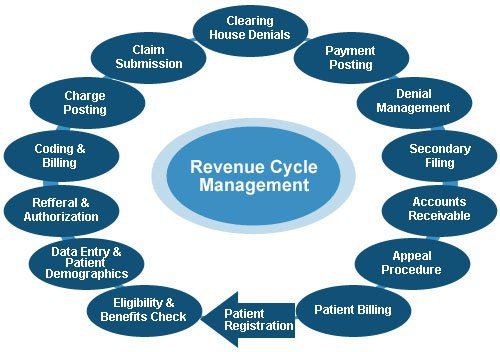

Revenue cycle challenges “seem to have intensified over the past year,” according to Kaufman Hall’s “2022 State of Healthcare Performance Improvement” report, released Oct. 18.

The consulting firm said that in 2021, 25 percent of survey respondents said they had not seen any pandemic-related effects on their respective revenue cycles. This year, only 7 percent said they saw no effects.

The findings in Kaufman Hall’s report are based on survey responses from 86 hospital and health system leaders across the U.S.

Here are the top five ways leaders said the pandemic affected the revenue cycle in 2022:

1. Increased rate claim denials — 67 percent

2. Change in payer mix: Lower percentage of commercially insured patients — 51 percent

3. Increase in bad debt/uncompensated care — 41 percent

4. Change in payer mix: Higher percentage of Medicaid patients — 35 percent

5. Change in payer mix: Higher percentage of self-pay or uninsured patients — 31 percent

Earlier this month, the Biden administration officially extended the federal public health emergency (PHE) declaration it had set in place for COVID-19. That means the PHE provisions will stay in effect for another 90 days — until mid-January at least.

When the PHE does end, a number of rules developed in response to the pandemic will sunset. One of those is a provision that temporarily requires states to let all Medicaid beneficiaries remain enrolled in the program — even if they have become ineligible during the pandemic.

Estimates suggest that millions could lose Medicaid coverage when this emergency provision ends. Among those who would lose coverage because they are no longer eligible for the program, about one-third are expected to qualify for subsidized coverage on the Affordable Care Act (ACA) marketplaces. Most others are expected to get coverage through an employer. It remains an open question, though, how many people will successfully transition to these other plans.

A recent paper by health economics researcher Laura Dague and colleagues in the Journal of Health Politics, Policy, and Law sheds light on these dynamics. The authors used a prior change in eligibility in Wisconsin’s Medicaid program to estimate how many people successfully transitioned to a private plan when their Medicaid eligibility ended.

Wisconsin’s Medicaid program is unique. Back in 2008 — before the ACA passed — Wisconsin broadly expanded Medicaid eligibility for non-elderly adults. After the ACA came into effect, Wisconsin reworked its Medicaid program in a way that made about 44,000 adults (mostly parents) with incomes above the federal poverty line ineligible for the program. To remain insured, they would have to switch to private coverage (via Obamacare or an employer).

Only about one-third of those 44,000 people had definitely enrolled in private coverage within two months of exiting the Medicaid program.

The remaining two-thirds of people were uninsured or their insurance status couldn’t be determined.

Even using the most optimistic assumptions to fill in that missing insurance status data, the authors estimated only up to 42% of people might have had private coverage within three months.

Nearly 1 in 10 enrollees had re-entered Medicaid coverage within six months, possibly due to fluctuations in household income.

This paper has several limitations. Health insurers are not required to participate in Wisconsin’s APCD, so the authors may not be capturing all successful transitions from Medicaid to private insurance. The paper also does not distinguish between different types of private insurance: Some coverage gains may have resulted from employer-based insurance rather than the ACA marketplace.

Still, the findings suggest that when a large number of Wisconsin residents lost Medicaid eligibility in 2014, many were not able to transition from Medicaid to private coverage. Wisconsin’s experience can help us understand what might happen when the national public health emergency ends and Medicaid programs resume removing people from their rolls.

A spokesperson for RWJBarnabas Health said the case is “yet another in a series of baseless complaints filed by … an organization whose leadership apparently prefers to assign blame to others rather than accept responsibility for the unsatisfactory results of their own poor business decisions and actions over the years.”

A lawsuit filed last week accuses RWJBarnabas Health of “a years-long systemic effort” to hamper competition and monopolize acute care hospital services in northern New Jersey.

The case brought by CarePoint Health to a U.S. District Court accuses the state’s largest integrated healthcare delivery system of “aiming to destroy the three hospitals operated by CarePoint as independent competitors” with the support of healthcare real estate investors and Horizon Blue Cross Blue Shield, the state’s largest health insurer.

CarePoint Health includes the 349-bed Christ Hospital, 224-bed Bayonne Medical and 348-bed Hoboken University Medical Center (HUMC).

The group said RWJBarnabas intended to force the first two hospitals to shut down but acquire the third due to its more profitable payer mix.

“RWJBarnabas Health’s] goal explicitly disregarded the needs of the poor, underinsured and charity care patients which CarePoint serves in its role as the safety net hospital system in Jersey City and surrounding areas,” CarePoint wrote in the lawsuit.

The slew of alleged tactics listed in the lawsuit largely surround RWJBarnabas Health’s “serial acquisitions” of hospitals, providers and real estate that “has gone unchecked by the state and [New Jersey Department of Health],” CarePoint wrote.

This included an alleged bad faith proposal to acquire Christ Hospital and HUMC, the true intent of which CarePoint said was to “gain market knowledge and gather competitive intelligence, and use this newly-acquired information to freeze programmatic growth and any significant hiring or construction at Christ Hospital.” The process had a negative impact on CarePoint’s employee retention and staffing, according to the suit.

The plaintiff also alleged that RWJBarnabas used its political connections to influence whether state departments granted CarePoint Certificates of Need for multiple revenue-generating projects as well as COVID-19 relief funding.

Further, CarePoint accused RWJBarnabas of strategically adjusting its service offerings in competitive markets to drive uninsured or underinsured patients to CarePoint facilities while using its relationships with Horizon and ambulance operators to drive emergency room traffic and well-insured patients, respectively, to competing locations.

These collective actions constitute violations of the Sherman Antitrust Act as well as the New Jersey Antitrust Act, CarePoint wrote.

“The idea that [RWJBarnabas Health] would use its influence to jeopardize the health of that community and the care providers of a competing hospital not only directly contradicts its own vision, but clearly demonstrates that [RWJBarnabas Health] is far more interested in anti-competitive and predatory business activities than serving the New Jersey community,” CarePoint wrote.

RWJBarnabas Health discounted the allegations in an email statement.

“This is yet another in a series of baseless complaints filed by CarePoint, an organization whose leadership apparently prefers to assign blame to others rather than accept responsibility for the unsatisfactory results of their own poor business decisions and actions over the years,” a spokesperson for the system told Fierce Healthcare. “RWJBarnabas Health has a longstanding commitment to serve the residents of Hudson County, and is proud of the significant investments we have made in technology, facilities and clinical teams as we advance our mission.”

RWJBarnabas Health treats over 3 million patients per year and employs 37,000 people. The academic healthcare system runs 12 acute care hospitals and four specialty hospitals alongside other locations and services. It disclosed more than $6.6 billion in total operating revenues across 2021.

The system’s merger and acquisition activity placed it in the federal spotlight this past year after the Federal Trade Commission moved to block its planned integration of New Brunswick-based Saint Peter’s Healthcare System. The deal was called off in June.

Children, young adults will be impacted disproportionately, with 5.3 million children and 4.7 million adults ages 18-34 predicted to lose coverage.

Roughly 15 million people could lose Medicaid coverage when the COVID-19 public health emergency ends, and only a small percentage are likely to obtain coverage on the Affordable Care Act exchanges, according to a new report from the Department of Health and Human Services.

Using longitudinal survey data and 2021 enrollment information, HHS estimated that, based on historical patterns of coverage loss, this would translate to about 17.4% of Medicaid and Children’s Health Insurance Program (CHIP) enrollees leaving the program.

About 9.5% of Medicaid enrollees, or 8.2 million people, will leave Medicaid due to loss of eligibility and will need to transition to another source of coverage. Based on historical patterns, 7.9% (6.8 million) will lose Medicaid coverage despite still being eligible – a phenomenon known as “administrative churning” – although HHS said it’s taking steps to reduce this outcome.

Children and young adults will be impacted disproportionately, with 5.3 million children and 4.7 million adults ages 18-34 predicted to lose Medicaid/CHIP coverage. Nearly one-third of those predicted to lose coverage are Hispanic (4.6 million) and 15% (2.2 million) are Black.

Almost one-third (2.7 million) of those predicted to lose eligibility are expected to qualify for marketplace premium tax credits. Among these, more than 60% (1.7 million) are expected to be eligible for zero-premium marketplace plans under the provisions of the American Rescue Plan. Another 5 million would be expected to obtain other coverage, primarily employer-sponsored insurance.

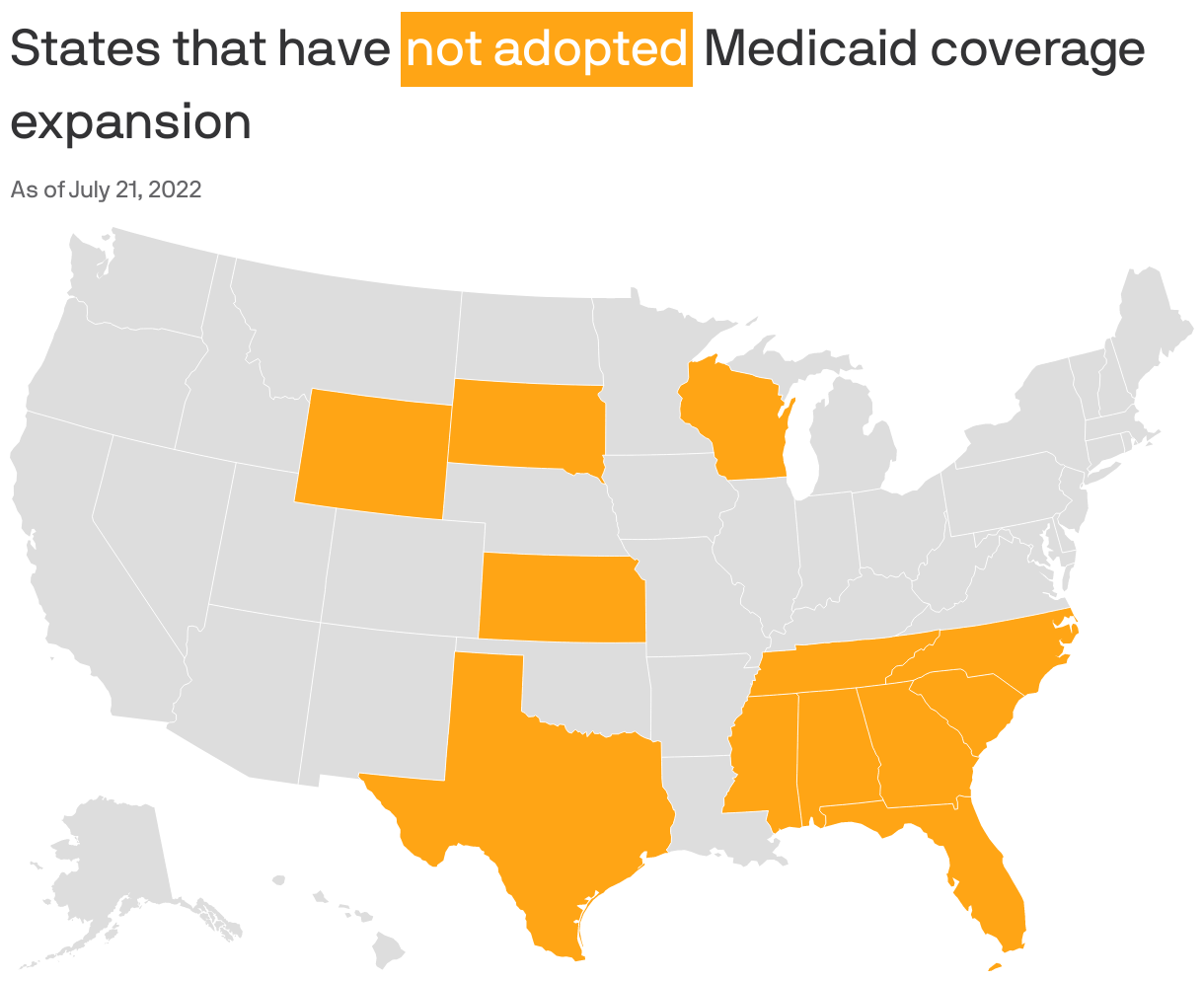

An estimated 383,000 people projected to lose eligibility for Medicaid would fall in the coverage gap in the remaining 12 non-expansion states – with incomes too high for Medicaid, but too low to receive Marketplace tax credits. State adoption of Medicaid expansion in these states is a key tool to mitigate potential coverage loss at the end of the PHE, said HHS.

States are directly responsible for eligibility redeterminations, while the Centers for Medicare and Medicaid Services provides technical assistance and oversight of compliance with Medicaid regulations. Eligibility and renewal systems, staffing capacity, and investment in end-of-PHE preparedness vary across states.

HHS said it’s working with states to facilitate enrollment in alternative sources of health coverage and minimize administrative churning. These efforts could reduce the number of eligible people losing Medicaid, the agency said.

The Inflation Reduction Act of 2022extends the ARP’s enhanced and expanded Marketplace premium tax credit provisions until 2025, providing a key source of alternative coverage for those losing Medicaid eligibility, said HHS.

WHAT’S THE IMPACT?

While the model projects that as many as 15 million people could leave Medicaid after the PHE, about 5 million are likely to obtain other coverage outside the marketplace and nearly 3 million would have a subsidized Marketplace option. And some who lose eligibility at the end of the PHE may regain it during the unwinding period, while some who lose coverage despite being eligible may re-enroll.

The findings highlight the importance of administrative and legislative actions to reduce the risk of coverage losses after the continuous enrollment provision ends, said HHS. Successful policy approaches should address the different reasons for coverage loss.

Broadly speaking, one set of strategies is needed to increase the likelihood that those losing Medicaid eligibility acquire other coverage, and a second set of strategies is needed to minimize administrative churning among those still eligible for coverage.

Importantly, some administrative churning is expected under all scenarios, though reducing the typical churning rate by half would result in the retention of 3.4 million additional enrollees.

THE LARGER TREND

CMS has released a roadmap to ending the COVID-19 public health emergency as health officials are expecting the Biden administration to extend the PHE for another 90 days after mid-October.

The end of the PHE, last continued on July 15, is not known, but HHS Secretary Xavier Becerra has promised to give providers 60 days’ notice before announcing the end of the public health emergency.

A public health emergency has existed since January 27, 2020.

Republican-led states that have resisted expanding Medicaid for more than a decade are showing new openness to the idea.

Driving the news: In the decade-plus since the landmark Affordable Care Act was enacted, 12 states with GOP-led legislatures still have not expanded Medicaid coverage to people living below 138% of the poverty line (or nearly $19,000 annually for one person in 2022).

But there’s evidence that the political winds are changing in holdout states like North Carolina, Georgia, Wyoming, Alabama and Texas, as leaders court rural voters, assess new financial incentives and confront the bipartisan popularity of extending health care coverage.

Why it matters: Medicaid expansion, a key component of the Affordable Care Act, means increasing access to federal health insurance coverage for low-income residents, in exchange for a 10% state match of the federal spending.

Experts say it expands access to care, lowers uninsured rates and improves health outcomes for low-income populations.

More than 2 million Americans would gain coverage if the 12 states expand Medicaid, according to a 2021 estimate from the Kaiser Family Foundation.

The big picture: Some Republican states have already expanded Medicaid through executive authority or — in states where it’s legal to do so — citizen-led ballot initiatives.

Referendums on the issue passed in Nebraska, Utah and Idaho in 2018 and Missouri and Oklahoma in 2020.

Medicaid expansion is on this November’s ballot in Republican-controlled South Dakota. (Voters there in June rejected a GOP proposal to make it harder to pass.)

Be smart: In most of the remaining non-expansion states, neither ballot initiatives nor executive authority are options, leaving the legislature with the authority to make the decision.

State of play: In Georgia, as first reported by Axios Atlanta, conversations about a path forward have been taking place behind the scenes in both parties. This follows the stunning support of full expansion legislation by North Carolina’s top Republican this spring, first reported by Axios Raleigh.

“If there is a person that has spoken out more against Medicaid expansion than I have, I’d like to meet that person,” Republican Senate leader Phil Berger said at a May press conference after reversing his stance. “This is the right thing for us to do.”

Brian Robinson, former spokesman for the first Georgia governor to reject Medicaid expansion, argued in June it’s time to make the change. Politically, it would “steal an issue” from Democrats, he told Axios Atlanta.

Policy-wise, “this isn’t what we would do,” Robinson said of Medicaid’s much-criticized structure. “But Republicans can’t agree on what we would do. This is the policy and the law, and it’s not going away. It would bring home hundreds of millions from a program we’re paying into already.”

What they’re saying: “There is real momentum on Medicaid expansion in these conservative states that have been holding out,” said Melissa Burroughs of Families USA, a health care advocacy group working with partners in non-expansion states to push the policy.

Burroughs told Axios there are Republicans championing or discussing expansion in every non-expansion state, but often “political dynamics and leadership” stand in the way.

Former Alabama Gov. Robert Bentley,who had refused to expand Medicaid himself, is now urging his fellow Republicans to pass it for the benefit of rural parts of the state.

The bipartisan legislative movement on expansion this year has given advocates in Wyoming hope.

In Texas, the state with the highest percentage of uninsured residents per capita, some Republicans have co-sponsored Medicaid expansion bills. That indicates “cracks” in Republican opposition, Luis Figueroa, legislative and policy director at progressive think tank Every Texan, told Axios Austin’s Nicole Cobler and Asher Price.

Tennessee’s Republican lieutenant governorsuggested possible openness to the policy last year, though there’s been no meaningful legislative movement.

Details: The winds are shifting for several reasons, experts told Axios.

Money: The 2021 federal pandemic relief law sweetened the deal for non-expansion states, with a provision designed to offset states’ costs entirely for the first two years. Plus, Republicans’ initial fears that the federal government would pull its 90% matching funds haven’t come to pass.

COVID-19: Under the federal state of a public health emergency, Medicaid access was automatically extended. But those temporary allowances could lift next year and millions could lose coverage, putting additional pressure on leaders.

Politics: Medicaid expansion continues to be broadly popular, and the Republican campaign to “repeal and replace” the Affordable Care Act has failed in the courts and Congress — neutralizing what was once a key argument against expansion.

Health care access: As hospitals across the country close, deepening the rural health care crisis, the benefit of getting more reimbursement from additional Medicaid recipients is difficult to ignore for rural hospital revenues — though the policy is not a silver bullet to end the crisis.

The intrigue: Democrats in these states, including gubernatorial candidates like Georgia’s Stacey Abrams and Texas’ Beto O’Rourke, continue to campaign heavily on Medicaid expansion — banking on polling showing the policy to be consistently popular among the public.

“I think a lot of Republican members would like to extend Medicaid even more than they will say it,” Texas Democratic State Sen. Nathan Johnson, who has led the push for expansion there, told Axios Austin’s Cobler and Price.

He said Republicans “are handcuffed by the ideological and political constraints. They will try to do some things to help people, but they need to get over the reflexive opposition to Medicaid expansion.”

Between the lines: Even in non-expansion states, partial expansion proposals have gained traction.

Kaiser Health News found that nine of the 12 states have sought or plan to seek an extension of postpartum Medicaid coverage, including for up to one year in North Carolina, Tennessee, South Carolina and Georgia.

What we’re watching: Even in holdout states showing signs of momentum, the issue remains politically fraught.

North Carolina’s most powerful politicians say the state’s negotiations this year were torpedoed by hospitals, though Democrats and Republicans alike are optimistic about its chances next session.

The national uninsured rate reached an all-time low of 8 percent in the first quarter of 2022, according to an HHS report released Aug. 2.

The report analyzed data from the National Health Interview Survey and the American Community Survey, according to an Aug. 2 HHS news release.

Three things to know:

1. The previous record low uninsured rate was 9 percent, set in 2016.

2. The uninsured rate among adults ages 18-64 was 11.8 percent in the first quarter of 2022. The uninsured rate for children ages 0-17 was 3.7 percent.

3. About 5.2 million people have gained health coverage since 2020. Gains in coverage are concurrent with the implementation of the American Rescue Plan’s enhanced ACA Marketplace subsidies, the continuous enrollment provision in Medicaid, several state Medicaid expansions and enrollment outreach efforts.