Cartoon – My Goals for the Upcoming Year

In an effort to rein in healthcare costs for its employees, Walmart sends them directly to health systems that demonstrate high-quality care outcomes, otherwise known as Centers of Excellence.

Through the COE program, Walmart will cover the travel and treatment costs for employees seeking a range of services, but only with providers the company is contracted with. Walmart then reimburses with bundled payments negotiated with the providers.

To determine which providers get access to its 1.6 million employees, Walmart starts by examining health systems. Lisa Woods, vice president of physical and emotional well-being at Walmart, and her team analyze public data, distribute requests for information and conduct detailed on-site visits.

Below are the 18 health systems or campuses to which Walmart will refer patients for defined episodes of care in 2022. (See how COE participants have evolved since 2019 or 2021.)

Cardiac

Cleveland Clinic

Geisinger Medical Center (Danville, Pa.)

Virginia Mason Medical Center (Seattle)

Weight loss surgery

Emory University Hospital (Atlanta)

Geisinger Medical Center (Danville, Pa.)

Intermountain Healthcare (Salt Lake City)

Northeast Baptist Hospital (San Antonio)

Northwest Medical Center (Springdale, Ark.)

Ochsner Medical Center (New Orleans)

Scripps Mercy Hospital (San Diego)

University Hospital (Cleveland)

Spine surgery

Emory University Hospital (Atlanta)

Geisinger Medical Center (Danville, Pa.)

Carolina NeuroSurgery & Spine Associates (Charlotte, N.C.)

Mercy Hospital Springfield (Mo.)

Mayo Clinic Arizona (Phoenix)

Mayo Clinic Florida (Jacksonville)

Mayo Clinic Minnesota (Rochester)

Memorial Hermann-Texas Medical Center (Houston)

Ochsner Medical Center (New Orleans)

Virginia Mason Medical Center (Seattle)

Breast, lung, colorectal, prostate

or blood cancer

Mayo Clinic Arizona (Phoenix)

Mayo Clinic Florida (Jacksonville)

Mayo Clinic Minnesota (Rochester)

Hip and knee replacements

Emory University Hospital (Atlanta)

Geisinger Medical Center (Danville, Pa.)

Johns Hopkins Bayview Medical Center (Baltimore)

Kaiser Permanente Irvine (Calif.) Medical Center

Mayo Clinic Florida (Jacksonville)

Mayo Clinic Minnesota (Rochester)

Mercy Hospital Springfield (Mo.)

Northeast Baptist Hospital (San Antonio)

Ochsner Medical Center (New Orleans)

Scripps Mercy Hospital (San Diego)

University Hospital (Cleveland)

Virginia Mason Medical Center (Seattle)

Organ and tissue transplants

(except cornea and intestinal)

Mayo Clinic Arizona (Phoenix)

Mayo Clinic Florida (Jacksonville)

Mayo Clinic Minnesota (Rochester)

The Massachusetts Health and Hospital Association is planning to release its semiannual health plan performance report next month and will focus on payers’ finances and enrollment in 2021.

In a May 23 newsletter, the association highlights the 22 percent increase in payers’ net worth during the COVID-19 pandemic, which totals $6.1 billion for all plans in the state. The newsletter also points to the combined $1.2 billion profit made in 2020 and 2021, which exceeds the previous five years combined.

The newsletter does point to the important role insurers played during the pandemic, including providing coverage of medical care, new therapies, vaccinations and COVID-19 testing. Under federal law, payers also provided rebates to premium payers as healthcare utilization decreased significantly. Some payers independently provided financial support to stabilize providers and used their resources to support the pandemic response.

“Despite these new expenses and efforts related to the COVID-19 emergency, health insurance company profits were substantially higher than at any point in recent history given the overwhelming effect of decreased medical utilization,” the newsletter said.

The association also criticized the decrease in claims payouts during the pandemic, arguing surplus revenue should have been used to increase payouts and not increase profits.

The hospital group stated that four specific payers, Harvard Pilgrim Health Care, UnitedHealthcare of New England, Tufts Associated HMO and HMO Blue from BCBS Massachusetts have risk-based capital ratios that approach or exceed 600 percent.

While healthcare is delivered locally, the business of healthcare

is regional, and the regions are only getting bigger. Hospital

and health system mergers alike have continued to shift from

local to regional, and the recently announced merger between Advocate Aurora

Health and Atrium Health clearly highlights that the regions are only getting

bigger.

Advocate Aurora, with a presence in Illinois and Wisconsin, and Atrium Health,

with a presence in North Carolina, South Carolina, Georgia, and Alabama, will

combine to create a $27 billion health system that will span six states and make it

one of the leading healthcare delivery systems in the country. The combined

organization, which will transition to a new brand, Advocate Health, will operate

67 hospitals and over 1,000 sites of care, employ nearly 150,000 teammates, and

serve 5.5 million patients. Together, Advocate Health will become the 6th largest

system in the country behind Kaiser Permanente, HCA Healthcare, CommonSpirit

Health, Ascension, and Providence.

We have seen a number of large health systems come together recently,

including Intermountain Healthcare + SCL Health to create a $15 billion revenue

system, Spectrum Health + Beaumont ($14 billion), NorthShore University Health

System + Edward-Elmhurst Healthcare ($5 billion), LifePoint Health + Kindred

Healthcare ($14 billion), and Jefferson Health + Einstein Healthcare Network ($8

billion).

The exact reasoning for each merger differs slightly, but one of the common

threads across all is scale. But not scale in the traditional M&A sense. Rather,

scale in covered lives; scale in physician infrastructure and alignment; scale in

clinical and operational capabilities; scale in technology, innovation, and

partnerships with non-traditional players; scale for capital access; and scale for

insurance risk to compete in a value-based world. It is no longer the strong

acquiring the weak. Rather, strong players are coming together to gain scale to

face the headwinds in a unified manner.

For Advocate Aurora and Atrium, coming together is about leveraging their combined clinical excellence,

advancing data analytics capabilities and digital consumer infrastructure, improving affordability, driving health equity, creating a next-generation workforce, research, and environmental sustainability. Together, they have pledged $2 billion to disrupt the root causes of health inequities across underserved communities and create more than 20,000 new jobs.

Both Advocate Aurora and Atrium are no strangers to mergers. Advocate and Aurora came together in 2018, and prior to that Advocate was intending to merge with NorthShore before being blocked due to anti-trust. Atrium has grown over the years, merging with systems such as Navicent Health in Georgia in 2018, Wake Forest Baptist Health in North Carolina 2020, and Floyd Health System in Georgia in 2021. In the newly proposed merger, Advocate Aurora and Atrium are coming together via a joint operating arrangement where each entity will be responsible for their own liabilities and maintain ownership of their respective assets but operate together under the new parent entity and board. This may allow the combined entity more flexibility in local decision-making. The current CEOs, Jim Skogsbergh and Eugene Woods will serve as co-CEOs for the first 18 months, at which point Skogsbergh will retire, and Woods will take over as the sole CEO.

Mergers can come in various shapes and structures, but the driving forces behind consolidation are not unique. With the need to compete in value-based care, adequately manage risk, gain scale across covered lives, physicians, and points of access, successfully deliver affordable high-quality care, and the need to deal with the vertical and horizontal consolidation of the large-scale payers, the markets that health systems operate in must be large enough to be effective and relevant. We fully expect to see more of these larger scale health system mergers in the near term.

The physical delivery of healthcare is local, but, again, the business of healthcare is not; it is regional, and the regions are only getting bigger.

Everyone agrees that the US healthcare system is not working so great. Compared to the rest of the world, our healthcare is extremely expensive and yet we suffer worse health by many measures. And we can’t seem to agree on what’s to blame, or what we should do about it. Do we have too much, or not enough, competition? Should the government intervene in health care markets more or less?

Basic economics can help us better understand what’s happening.

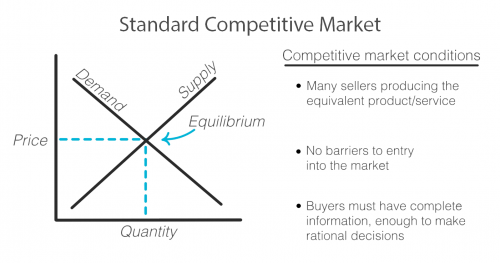

As with any exchange of goods and services, the standard competitive market model has the familiar upward sloping supply curve and downward sloping demand curve, illustrating that when prices are higher, demand decreases and supply increases as sellers are incentivized to produce more of that good or service at its higher price. Sellers and buyers arrive at what quantity to produce and consume and at what price based on where these two lines intersect, called the equilibrium. Both buyer and seller are happy with the deal they’ve struck!

But not every market works this way. There are actually standards that need to be met in order for a market to fit this model and for it to work efficiently for both the buyer and seller.

First, there must exist multiple sellers competing to sell the same goods or services and new sellers must be able to easily enter the market.

There must be a sufficient open exchange of information between buyer and seller about price, availability, and value of a service or good.

And buyers must make, or be in a position to make, rational decisions using the information they possess about the market.

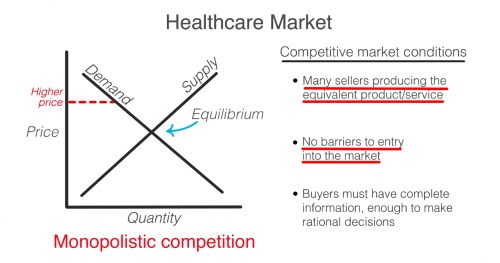

Healthcare does not meet these standards and when these standards are not met, the equilibrium cannot be reached or accurately known. Any price and quantity that falls outside of the equilibrium is considered a market failure. Using only this model, we can see how healthcare’s market failures contribute to high prices.

To start, it’s true that healthcare is failing the market standards when it comes to competition. The number of sellers in the market is decreasing due to both an increase in barriers to entry and due to consolidation, including hospital mergers. This causes an imbalance in power of the seller over the buyer that can begin to reflect what economists call monopolistic competition where sellers can charge a price above the perfect competition equilibrium. In the extreme, when there is only one seller, the market is a monopoly.

So then, don’t we just need more competition? Unfortunately, a lack of competition isn’t the only reason that healthcare fails the market standards.

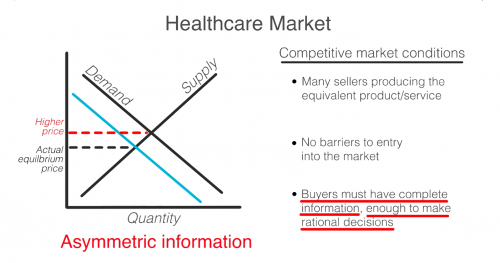

Another failure is that consumers in healthcare, patients, do not have all the information that providers, like doctors and hospitals, do. This is known as asymmetric information. Patients often have no idea before getting care how much it will cost, what the prices available to them elsewhere are, or what the quality will be. When consumers are in the dark about these basic features, the true demand and supply will be different than the model. The true demand may be lower if patients knew ahead of time how much it cost or how much less valuable the service is compared to how it is promoted. This means prices can be set higher than they likely would be if the true demand was known.

Even if patients had full information, they are not always in a position to act as rational consumers. A patient’s decision may be influenced by their concern for their health, or their ability to think rationally may itself be affected by their condition.

So, as you can see, the problem is that a lack of competition only accounts for part of the reason why healthcare doesn’t meet the market standards. No matter how much the government either steps back to allow for more competition or invests to foster competition, the market will never fix ALL of these failures on its own. Healthcare is not and can never be a free market. It simply does not fit this model.

In 1963, economist and later Nobel prize winner, Kenneth Arrow, warned us about this looming healthcare crisis. He explains that “If the actual market differs significantly from the competitive model […] coordination of purchases and sales must take place”

That coordination he is referring to is government intervention.

Dr. Mike Chernew, Health Economist and Professor of Health Policy at Harvard Medical School agrees…“an unregulated health care market is unlikely to lead to desired outcomes.”

In reality, health care always has, and always will, involve a combination of both government intervention and market forces to control prices and increase quality. The debate isn’t really whether or not the government should intervene, but by how much and in what way.

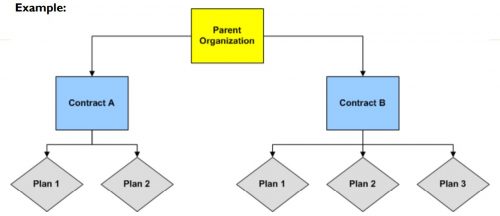

Medicare Advantage (MA) is the private insurance alternative to traditional Medicare. MA organizations contract with Centers for Medicare and Medicaid Services (CMS) to offer eligible beneficiaries residing in a defined geographic service area (a collection of counties) a selection of private plans. Insurers may offer multiple plans across different plan types under one contract. The service area is defined at the contract-level, and for most MA plans, service areas can include a single county or a collection of multiple counties. (There are other types of plans for which there are constraints on the boundaries of the service area, but these don’t account for very much of MA enrollment.)

As MA-offering insurers contract with CMS, they establish networks that govern patient liability for seeing in- and out-of-network providers. Consequently, plans will vary in their cost-sharing structures and benefit designs as they assume different levels of liability for the cost of out-of-network providers. Overall, plans will cover the cost of care (less copays and deductibles) for patients seeing providers in-network, and certain plan types may require that patients pay more for out-of-network services or receive referrals/prior authorization from primary care providers (PCP) to see specialists.

The most common plan types offered by MA insurers include the following:

The differences across plan types in access to and cost sharing for out-of-network providers leads to the important question, do MA networks vary by plan within contract? For example, in Figure 1 below, do the beneficiaries enrolled in Plan 1 or 2 under Contract A have the same set of in- and out-of-network providers (likewise for the beneficiaries in Plans 1-3 under contract B)? More specifically, what if Plan 1 is an HMO and Plan 2 is a HMO-POS plan, do they share the same network?

The simple answer seems to be: not necessarily, though more recent regulations attempt to push insurers toward having the same networks across plans within contracts.

For instance, prior to 2019, CMS only reviewed the adequacy of an MA organization’s contracted network under a “triggering event,” like if an organization were to operate a new plan, expand coverage to additional service areas, or in a response to inadequate network complaints. The scope of CMS’ review varied depending on the triggering event that occurred. In some cases, CMS could only conduct partial reviews of a contract’s network, looking at a select set of specialties or counties. A study by the US Government Accountability Office found that between 2013 and 2015, CMS had reviewed less than 1% of all networks. Without regular scrutiny by regulators, it seems likely that networks varied across plans within contracts.

Under the current MA Network Adequacy Criteria Guidance, CMS assesses network adequacy requirements both under triggering events (as explained above) and, separate from that, on a triennial-basis at the contract-level. CMS has previously commented in the 2021 Final Rule that this approach allows them to assess the adequacy of organizations’ networks across all of their plan types (HMOs, PPOs, SNPs) and consider the broadest availability of providers and facilities for an organization. Again, this suggests that insurers may vary networks across plans within contracts.

There are at least two scenarios for which we know certain plans can and likely do have different networks compared with other plans in the contract.

Future work with Vericred provider-network data could be one approach to exploring variations in networks among plans under the same contract and service area, beyond the cases listed above. If networks are varying across HMO, PPO, and HMO-POS plans within contracts, it would be interesting to explore just how different they are from one another. Moreover, as CMS reviews continues to review network adequacy requirements at the contract-level (and if networks do differ by plan), one should consider the breadth of the network that organizations are submitting for evaluation. To what extent all plans in a contract are in compliance with network adequacy rules warrants future investigation.

tradeoffs.org/2022/05/17/medicaid-physician-access/

A certain segment of the health policy world spends a lot of time trying to get more states to expand Medicaid and reduce underinsurance.

But are we doing enough to make sure care is accessible once people enroll? One issue is access to physicians, who are less likely to treat patients on Medicaid than Medicare or private insurance because Medicaid payment rates are lower.

A new paper in Health Affairs by Avital Ludomirsky and colleagues looked at how well the networks of physicians supposedly participating in Medicaid reflect access to care. The researchers used claims data and provider directories from Medicaid managed care plans (the private insurers that most states contract with to run their Medicaid programs) in Kansas, Louisiana, Michigan and Tennessee from 2015 and 2017 to assess how the delivery of care to Medicaid patients was distributed among participating doctors. Their results were striking:

The authors note that their study only covers primary care and mental health providers in four states, so it is not necessarily generalizable to other states or specialties. But these results are still concerning.

States have so-called network adequacy standards for their Medicaid managed care plans that are supposed to make sure there are enough providers. These standards typically rely on either a radius (a certain number of providers for a geographic area) or ratio (number of providers per enrollee), but the authors’ findings show these methods fall short if they are based on directories alone.

The authors specifically recommend states use claims-based assessments like the ones in the study and “secret shopper” programs — like this recently published one from Maryland by Abigail Burman and Simon Haeder — to better evaluate whether plans are offering adequate access to physicians. We absolutely need people to have coverage, but it needs to be more than just a card in their wallet.

The American Hospital Association, on behalf of its nearly 5,000 healthcare organizations, is urging the Justice Department to probe routine denials from commercial health insurance companies.

Specifically, the AHA is asking the Justice Department to establish a task force to conduct False Claims Act investigations into the insurers that routinely deny payments to providers, according to a May 19 letter to the department.

The request from the AHA comes after HHS’ Office of Inspector General released a report April 27 that found Medicare Advantage Organizations sometimes delayed or denied enrollees’ access to services although the provider’s prior authorization request met Medicare coverage rules.

“It is time for the Department of Justice to exercise its False Claims Act authority to both punish those MAOs that have denied Medicare beneficiaries and their providers their rightful coverage and to deter future misdeeds,” the AHA said in a letter to the Justice Department. “This problem has grown so large — and has lasted for so long — that only the prospect of civil and criminal penalties can adequately prevent the widespread fraud certain MAOs are perpetrating against sick and elderly patients across the country.”

Read the full letter here.

Boston-based Mass General Brigham submitted a cost-reduction plan to Massachusetts regulators May 16, which includes a promise to cut healthcare spending by $70 million a year.

The health system was ordered by the Massachusetts Health Policy Commission in January to develop a plan to reduce costs after the watchdog determined it had pushed healthcare spending above acceptable levels in the last few years. Specifically, the commission found that Mass General Brigham had substantially higher-than-average commercial spending from 2014 to 2019. The health system spent $293 million those years, more than any other provider in the state.

To achieve its spending reduction goal, Mass General Brigham said it would focus on four items: cutting prices, reducing utilization, shifting care to lower-cost sites and expanding value-based care.

A key savings driver in Mass General Brigham’s plan is to lower outpatient and ConnectorCare rates to improve affordability. ConnectorCare is a program of subsidized private health insurance plans for patients whose family income doesn’t exceed 300 percent of the federal poverty level and who are not eligible for MassHealth, Medicare or other affordable health coverage. The health system expects to save about $53.8 million in spending a year through reducing these rates.

“Mass General Brigham is committed to expanding access to consumers, particularly in ambulatory care. To achieve improved access, we are focused on decreasing the price variation between Mass General Brigham pricing and the marketplace,” Mass General Brigham said in the performance improvement plan.

The health system said it expects to save $10.8 million in spending a year by reducing unnecessary hospitalizations, emergency room visits and post-acute care and reducing use of high-cost outpatient imaging.

The health system said it expects to save $5.3 million in spending a year by shifting care to lower-cost settings, such as moving to “hospital at home,” expanding telehealth or using other ambulatory sites.

In addition to reducing utilization, shifting care to lower-cost sites and reducing price, Mass General Brigham said it is committed to expanding value-based care.