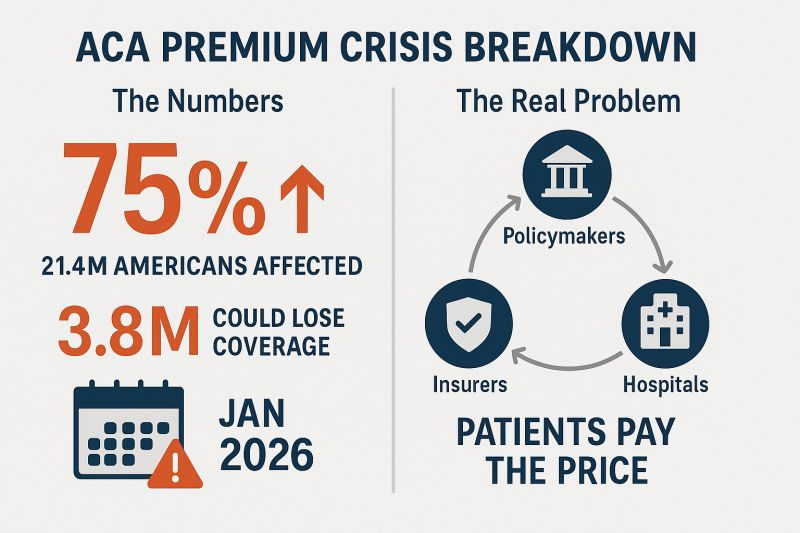

People who buy health insurance through the Affordable Care Act (ACA) are set to see a median premium increase of 18 percent, more than double last year’s 7 percent median proposed increase, according to an analysis of preliminary filings by KFF.

The proposed rates are preliminary and could change before being finalized in late summer. The analysis includes proposed rate changes from 312 insurers in all 50 states and DC.

It’s the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA marketplace insurers are raising premiums by about 20 percent in 2026, KFF found.

Insurers said they wanted higher premiums to cover rising health care costs, like hospitalizations and physician care, as well as prescription drug costs. Tariffs on imported goods could play a role in rising medical costs, but insurers said there was a lot of uncertainty around implementation, and not many insurers were citing tariffs as a reason for higher rates.

But they are adding in higher increases due to changes being made by the Trump administration and Republicans in Congress. For instance, the majority of insurers said they are taking into account the potential expiration of enhanced premium tax credits.

Those subsidies, put in place during the COVID-19 pandemic, are set to expire at the end of the year, and there are few signs that Republicans are interested in tackling the issue at all.

If Congress takes no action, premiums for subsidized enrollees are projected to increase by over 75 percent starting in January 2026, according to KFF.

But some states are pushing back.

Arkansas Gov. Sarah Huckabee Sanders (R) on Wednesday called on the state’s insurance commissioner to disapprove the proposed increases from Centene and Blue Cross Blue Shield. The companies filed increases of up to 54 percent and 25.5 percent, respectively, she said.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both,” Huckabee Sanders said in a statement.

“I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

Ahead of my Congressional testimony last week before the Senate HELP committee, I compiled data on the profits, revenues and CEO compensations of big health insurers in 2024. The curiosity from senators on both sides of the aisle signaled, to me, that lawmakers are as interested as I’ve ever seen in the industry’s rampant profiteering.

What I found was that the seven biggest publicly traded health insurance companies collectively made $71.3 billion in profits, up more than half a billion dollars from 2023. All while millions of Americans continued to skip their medications, rationed insulin and delayed care due to insurers’ out-of-pocket demands.

Let’s break it down.

You won’t be surprised to learn that shareholders are not the only ones benefiting from the care-restricting barriers insurers have erected to boost profits. The CEOs of those seven companies took home a combined $146.1 million in 2024 compensation. That’s enough to cover annual premiums for thousands of American families.

Here’s what the top brass made:

Meanwhile, patients across the country report increasing out-of-pocket costs, more aggressive prior authorizations and narrower provider networks. But for these executives, the real measure of success is how high they can push their stock prices and not how many people can afford to see a doctor.

So, What’s Driving the Revenue Surge?

One word: Gouging.

Insurers continued to jack up premiums for their commercial customers and overcharge the government. Despite watchdog warnings, Uncle Sam continues to pour money into private Medicare Advantage plans even as audits and investigations uncover widespread fraud and upcoding. And Medicaid managed care is a gold mine, too. These insurers now dominate state Medicaid contracts and can quietly extract billions through behind-the-scenes ownership of pharmacies, PBMs and providers.

It’s not just health insurance anymore — it’s a monopolized empire.

All that said, to the dismay of shareholders, the big seven insurers have had to admit that so far in 2025, they’ve paid more medical claims than they had expected, which means their profits were down somewhat during the first months of the year. I’ll shed more light on that in a future post. No need for you to shed any tears for them, though, because we’re still talking billions and billions in profits.

So if you’re wondering why your premiums, deductibles and costs at the pharmacy counter keep going up — just look at those 2024 numbers. We all paid more for health insurance and got less for the hard-earned money we had to shovel out for our “coverage.”

And expect even more financial pain (and difficulty getting the care you need) as these companies do all they can to get their profit margins back to where Wall Street wants them.

President Donald Trump has made big promises about fixing American healthcare. Now comes the moment that separates talk from action.

With the 2026 midterms fast approaching and congressional attention soon shifting to electoral strategy, the window for legislative results is closing quickly. This summer will determine whether the administration turns promises into policy or lets the opportunity slip away.

Trump and his handpicked healthcare leaders — HHS Secretary Robert F. Kennedy Jr. and FDA Commissioner Dr. Marty Makary — have identified three major priorities: lowering drug prices, reversing chronic disease and unleashing generative AI. Each one, if achieved, would save tens of thousands of lives and reduce costs.

But promises are easy. Real change requires political will and congressional action. Here are three tests that Americans can use to gauge whether the Trump administration succeeds or fails in delivering on its healthcare agenda.

Test No. 1: Have Drug Prices Come Down?

Americans pay two to four times more for prescription drugs than citizens in other wealthy nations. This price gap has persisted for more than 20 years and continues to widen as pharmaceutical companies launch new medications with average list prices exceeding $370,000 per year.

One key reason for the disparity is a 2003 law that prohibits Medicare from negotiating prices directly with drug manufacturers. Although the Inflation Reduction Act of 2022 granted limited negotiation rights, the initial round of price reductions did little to close the gap with other high-income nations.

President Trump has repeatedly promised to change that. In his first term, and again in May 2025, he condemned foreign “free riders,” promising, “The United States will no longer subsidize the healthcare of foreign countries and will no longer tolerate profiteering and price gouging.”

To support these commitments, the president signed an executive order titled “Delivering Most-Favored-Nation (MFN) Prescription Drug Pricing to American Patients.” The order directs HHS to develop and communicate MFN price targets to pharmaceutical manufacturers, with the hope that they will voluntarily align U.S. drug prices with those in other developed nations. Should manufacturers fail to make significant progress toward these targets, the administration said it plans to pursue additional measures, such as facilitating drug importation and imposing tariffs. However, implementing these measures will most likely require congressional legislation and will encounter substantial legal and political challenges.

The pharmaceutical industry knows that without congressional action, there is no way for the president to force them to lower prices. And they are likely to continue to appeal to Americans by arguing that lower prices will restrict innovation and lifesaving drug development.

But the truth about drug “innovation” is in the numbers: According to a study by America’s Health Insurance Plans, seven out of 10 of the largest pharmaceutical companies spend more on sales and marketing than on research and development. And if drugmakers want to invest more in R&D, they can start by requiring peer nations to pay their fair share — rather than depending so heavily on U.S. patients to foot the bill.

If Congress fails to act, the president has other tools at his disposal. One effective step would be for the FDA to redefine “drug shortages” to include medications priced beyond the reach of most Americans. That change would enable compounding pharmacies to produce lower-cost alternatives just as they did recently with GLP-1 weight-loss injections.

If no action is taken, however, and Americans continue paying more than twice as much as citizens in other wealthy nations, the administration will fail this crucial test.

Test No. 2: Did Food Health, Quality Improve?

Obesity has become a leading health threat in the United States, surpassing smoking and opioid addiction as a cause of death.

Since 1980, adult obesity rates have surged from 15% to over 40%, contributing significantly to chronic diseases, including type 2 diabetes, heart disease and multiple types of cancers.

A major driver of this epidemic is the widespread consumption of ultra-processed foods: products high in added sugar, unhealthy fats and artificial additives. These foods are engineered to be hyper-palatable and calorie-dense, promoting overconsumption and, in some cases, addictive eating behaviors.

RFK Jr. has publicly condemned artificial additives as “poison” and spotlighted their impact on children’s health. In May 2025, he led the release of the White House’s Make America Healthy Again (MAHA) report, which identifies ultra-processed foods, chemical exposures, lack of exercise and excessive prescription drug use as primary contributors to America’s chronic disease epidemic.

But while the report raises valid concerns, it has yet to produce concrete reforms.

To move from rhetoric to results, the administration will need to implement tangible policies.

Here are three approaches (from least difficult to most) that, if enacted, would signify meaningful progress:

Front-of-package labeling. Implement clear and aggressive labeling to inform consumers about the nutritional content of food products, using symbols to indicate healthy versus unhealthy options.

Taxation and subsidization. Impose taxes on unhealthy food items and use the revenue to subsidize healthier food options, especially for socio-economically disadvantaged populations.

Regulation of food composition. Restrict the use of harmful additives and limit the total amount of fat and sugar included, particularly for foods aimed at kids.

These measures will doubtlessly face fierce opposition from the food and agriculture industries. But if the Trump administration and Congress manage to enact even one of these options — or an equivalent reform — they can claim success.

If, instead, they preserve the status quo, leaving Americans to decipher nutritional fine print on the back of the box, obesity will continue to rise, and the administration will have failed.

Test No. 3: Are Patients Using Generative AI To Improve Health?

The Trump administration has signaled a strong commitment to using generative AI across various industries, including healthcare. At the AI Action Summit in Paris, Vice President JD Vance made the administration’s agenda clear: “I’m not here this morning to talk about AI safety … I’m here to talk about AI opportunity.”

FDA Commissioner Dr. Marty Makary has echoed that message with internal action. After an AI-assisted scientific review pilot program, he announced plans to integrate generative AI across all FDA centers by June 30.

But internal efficiency alone won’t improve the nation’s health. The real test is whether the administration will help develop and approve GenAI tools that expand clinical access, improve outcomes and reduce costs.

To these ends, generative AI holds enormous promise:

Managing chronic disease: By analyzing real-time data from wearables, GenAI can empower patients to better control their blood pressure, blood sugar and heart failure. Instead of waiting months between doctor visits for a checkup, patients could receive personalized analyzes of their data, recommendations for medication adjustments and warnings about potential risk in real time.

Improving diagnoses: AI can identify clinical patterns missed by humans, reducing the 400,000 deaths each year caused by misdiagnoses.

Personalizing treatment: Using patient history and genetics, GenAI can help physicians tailor care to individual needs, improving outcomes and reducing side effects.

These breakthroughs aren’t theoretical. They’re achievable. But they won’t happen unless federal leaders facilitate broad adoption.

That will require investing in innovation. The NIH must provide funding for next-generation GenAI tools designed for patient empowerment, and the FDA will need to facilitate approval for broad implementation. That will require modernizing current regulations. The FDA’s approval process wasn’t built for probabilistic AI models that rely on continuous application training and include patient-provided prompts. Americans need a new, fit-for-purpose framework that protects patients without paralyzing progress.

Most important, federal leaders must abandon the illusion of zero risk. If American healthcare were delivering superior clinical outcomes, managing chronic disease effectively and keeping patients safe, that would be one thing. But medical care in the United States is far from that reality. Hundreds of thousands of Americans die annually from poorly controlled chronic diseases, medical errors and misdiagnoses.

If generative AI technology remains confined to billing support and back-office automation, the opportunity to transform American healthcare will be lost. And the administration will have failed to deliver on this promise.

When I teach strategy at Stanford’s Graduate School of Business, I tell students that the best leaders focus on a few high-priority goals with clear definitions of success — and a refusal to accept failure. Based on the administration’s own words, grading the administration on these three healthcare tests will fulfill those criteria.

However, with Labor Day just months away, the window for action will soon close. The time for presidential action is now.

July 2025 will be the month U.S. healthcare leaders recognize as the industry’s modern turning point. Consider…

On July 4, the One Big Beautiful Bill Act was signed into law setting in motion $960 billion in Medicaid cuts over the decade and massive uncertainty among those most adversely impacted—low income and under-served populations dependent on public programs, 8 to 11 million who used now-suspended marketplace subsidies to buy insurance coverage, and hundreds of state and local health agencies left in funding limbo.

On July 15, the Bureau of Labor Statistics reported the June Consumer Price Index rose .3% bumping the LTM to 2.7% (lower than LTM of 3.4% for medical services). Prices have edged up.

On July 31, President Trump issued an Executive Order to 17 drug companies ordering them to reduce prices on their drugs by September 29 or else. And CMS issued final rules for FY2026 Medicare payments to hospitals, rehab and other providers reflecting increases ranging from 2.5-3.3% effective October 1.

And on the same day, the Bureau of Labor issued its July 2025 jobs report that showed a disappointing net gain of 73,000 jobs plus downward revisions for May and June of 258,000 sparking Wall Street anxiety and President Trump to call the results “rigged” before firing BLS head Erika McEntarfer. Note: healthcare added 55,000 in July—the biggest of any sector and more than its 42,000 average monthly increase.

Collectively, these actions reflect rejection of the health industry by the GOP-led Congress.

It follows 15 years of support vis a vis the Affordable Care Act (2010) and pandemic recovery emergency funding (2020-2021). In that 15-year period, the bigger players got bigger in each sector, investment of private equity in each sector became more prevalent, costs increased, affordability for consumers and employers decreased, and the public’s overall satisfaction with the health system declined precipitously.

For the four major players in the system, the passage of the “big, beautiful bill” was a disappointment. Their primary concerns were not addressed:

Physicians wanted relieffrom annual payment cuts by Medicare preferring reimbursement tied directly to medical inflation. And insurer’ prior authorization and provider reimbursement was a top issue. Status: Not much has changed though adjustments are promised.

Hospitals wanted continuation of federal Medicaid funding, protection of the 340B drug purchasing program, rejection of site-neutral payment policies, higher Medicare reimbursement and relief from insurer prior authorization frustrations. Status: Medicaid funding is being cut forcing the issue for states. CMS payment increases for 2026 are lower than operating cost increases. Insurers have promised prior-auth relief but details about how and when are unknown. And Congress posture toward hospitals seems harsh: price transparency compliance, safety event reporting, and cost concerns are bipartisan issues.

Insurers wanted sustained funding for state Medicaid and Medicare Advantage programs and federal pushback against drug prices and hospital consolidation. Status: Congress appears sympathetic to enrollee complaints and anxious to address insurer “waste, fraud and abuse” including overpayments in Medicare Advantage.

Drug companies oppose “Most Favored Nation” pricing and want protections of their patents and limits on how much insurers, pharmacy benefits managers, wholesalers, online distributors and other “middlemen” earn at their expense. Status: to date, little action despite sympathetic rhetoric by lawmakers. Status: to date, Congress has taken nominal action beyond the Inflation Reduction Act (2022) though 23 states have passed legislation requiring PBMs, insurers and manufacturers to disclose drug prices and 12 states have established Prescription Drug Affordability Boards to monitor prices.

My take:

The landscape for U.S. healthcare is fundamentally changed as a result of the July actions noted above. It is compounded by public anxiety about the economy at home and global tensions abroad.

These July actions were a turning point for the industry: responding appropriately will require fresh ideas and statesmanship. Transparency about prices, costs, incentives and performance is table stakes. Leaders dedicated to the greater good will be the difference.

The recently passed One Big Beautiful Bill Act, which makes deep cuts to the Medicaid program, also puts the food assistance that 41 million low-income Americans rely on in jeopardy. Many of the families currently getting food provided by the Supplemental Nutrition Assistance Program (SNAP) stand to lose that support.

SNAP may well disappear for some families as the federal government moves to trim it. “The cuts are massive and extremely cruel when families need more support, not less,” says Signe Anderson, senior director of nutrition advocacy, at the Tennessee Justice Center in Nashville.

Government food assistance was established during the Great Depression, but it wasn’t until 1977 that the program became more accessible when the requirement that recipients had to pay for a portion of their food stamps was ended. Throughout its history, foes of the program have tried to dismantle it and may have succeeded as a result of provisions in the bill President Trump signed on July 4.

The new legislation calls for cutting spending for food stamps by $186 billion through 2034. “Everyone on food stamps will be affected in some way, and many will lose benefits,” Anderson says. “I don’t think the Congress understands the level of necessity in the community for food, health care and mental health treatment, some for the rest of their lives.”

One major change is being made to work requirements that have historically been part of the Medicaid program, which is administered and partially funded by the states. Anderson points out that under the new arrangements, participants may find the task of enrolling and staying enrolled more onerous. “We see a lot of people cut off already because too many life circumstances make it difficult for them to meet work requirements.”

Indeed when you look at the changes to SNAP, the first word that might come to mind is ‘draconian.’

To receive benefits those new to the program, and those already on it who are between 55 and 64 and do not have dependent children or who have children 14 and older, will have to prove they work. Or they will have to volunteer at least 20 hours a week or enroll in training programs. Parents of school-aged children will now be required to work.

Some five million people, including about 800,000 children and about a half million adults who are 65 and older, could lose their food benefits.

The programs the new law targets have been a lifeline for some. Nikole Ralls, a 43-year-old woman in Nashville, who was once a drug addict but now counsels others who need help, says, “I got my life turned around because of Medicaid and SNAP.”

In a recent memo to state agencies administering the SNAP program, Agriculture Secretary Brooke Rollins said she was concerned about what was described as abuse of the waiver system by states, noting that the new approach for the SNAP program would prioritize work, education and volunteering over what the department characterized as “idleness and excessive spending.”

Anderson said, “The public doesn’t understand what hunger looks like and are misinformed about how well-run and streamlined the SNAP program is.”

“Most of the people who can, do work. We have parents working two and three jobs,” Anderson said. For families in this predicament food banks, which have become default grocery stores, may be of little help. They, too, are stretched thin. The Wall Street Journal reported food banks across the country are already straining under rising demand, and some worry there won’t be enough food to meet demand.

Imagine you’re facing your midyear performance review with your boss. You dread it, even though you’ve done all you thought possible and legal to help the company meet Wall Street’s profit expectations, because shareholders haven’t been pleased with your employer’s performance lately.

Now let’s imagine your employer is a health insurance conglomerate like, say, UnitedHealth Group. You’ve watched as the stock price has been sliding, sometimes a little and on some days crashing through lows not seen in years, like last Friday (down almost 5% in a single day, to $237.77, which is down a stunning 62% since a mid-November high of $630 and change).

You know what your boss is going to say. We all have to do more to meet the Street’s expectations. Something has changed from the days when the government and employers were overly generous, not questioning our value proposition, always willing to pick up the tab and pay many hidden tips, and we could pull our many levers to make it harder for people to get the care they need.

Despite government and media reports for years that the federal government has been overpaying Medicare Advantage plans like UnitedHealth’s – at least $84 billion this year alone – Congress has pretended not to notice. There is evidence that might be changing, with Republicans and Democrats alike making noises about cracking down on MA plans.

Employers have complained for ages about constantly rising premiums, but they’ve sucked it up, knowing they could pass much of the increase onto their workers – and make them pay thousands of dollars out of their own pockets before their coverage kicks in. Now, at least some of them are realizing they don’t have to work with the giant conglomerates anymore.

Doctors and hospitals have complained, too, about burdensome paperwork and not getting paid right and on time, but they’ve largely been ignored as the big conglomerates get bigger and are now even competing with them.

UnitedHealth is the biggest employer of doctors in the country. But doctors and hospitals are beginning to push back, too.

Since last fall, UnitedHealth and its smaller but still enormous competitors have found that “headwinds” are making it harder for them to maintain the profit margins investors demand. That is mainly because, despite the many barriers patients have to overcome to get the care they need, many of them are nevertheless using health care, often in the most expensive setting – the emergency room. They put off seeing a doctor so long because of insurers’ penny-wise-pound-foolishness that they had some kind of event that scared them enough to head straight to the ER.

It’s not just you who is dreading your midyear review. Everybody, regardless of their position on the corporate ladder, and even the poorly paid folks in customer service, are in the same boat. And so is your boss. Nobody will put the details of what has to be done in writing. They don’t have to. Your boss will remind you that you have to do your part to help the company achieve the “profitable growth” Wall Street demands, quarter after quarter after quarter. It never, ever ends. You know this because you and most other employees watch what happens after the company releases quarterly financials. You also watch your 401K balance and you see the financial consequences of a company that Wall Street isn’t happy with. And Wall Street is especially unhappy with UnitedHealth these days.

And when things are as bad as they are now at UnitedHealth’s headquarters in Minnesota, you know that a big consulting firm like McKinsey & Company has been called in, and that those suits will recommend some kind of “restructuring” and changes in leadership to get the ship back on course. You know the drill. Everybody already is subject to forced ranking, meaning that at the end of the year, some of your colleagues, regardless of job title, will fall below a line that means automatic termination. You pedal as fast as you can to stay above that line, often doing things you worry are not in the best interest of millions of people and might not even be lawful. But you know that if you have any chance of staying employed, much less getting a raise or bonus, you have to convince your superiors you are motivated and “engaged to win.” No one is safe. Look what happened to Sir Andrew Witty, whose departure as CEO to spend more time with his family (in London) was announced days after shareholders turned thumbs down on the company’s promises to return to an acceptable level of profitability.

If you are at UnitedHealth, you listened to what the once and again CEO, Stephen Hemsley, and CFO John Rex, who got shuffled to a lesser role of “advisor” to the CEO last week, laid out a new action plan to their bosses – big institutional investors who have been losing their shirts for months now. You know that what the C-Suite promised on their July 29 call will mean that you will have to “execute” to enable the company to deliver on those promises. And you know that you and your colleagues will have to inflict a lot more pain on everybody who is not a big shareholder – patients, taxpayers, employers, doctors, hospital administrators. That is your job. And you will try to do it because you have a mortgage, kids in college and maxed-out credit cards.

Here’s what Hemsley and his leadership team said, out loud in a public forum, although admittedly one that few people know about or can take an hour-and-a-half to listen to:

Even though UnitedHealth took in billions more in revenue, its margins shrank a little because it had to pay more medical claims than expected.

Still, the company made $14.3 billion in profits during the second quarter. That’s a lot but not as much as the $15.8 billion in 2Q 2024, and that made shareholders unhappy.

Enrollment in its commercial (individual and employer) plans increased just 1%, but enrollment in its Medicare Advantage plans increased nearly 8%. That’s normally just fine, but something happened that the company’s beancounters couldn’t stop.

Those seniors figured out how to get at least some care despite the company’s high barriers to care (aggressive use of prior authorization, “narrow” networks of providers, etc.)

To fix all of this, Hemsley and team promised:

To dump 600,000 or so enrollees who might need care next year

To raise premiums “in the double digits” – way above the “medical trend” that PriceWaterhouseCoopers predicts to be 8.5% (high but not double-digit high)

Boot more providers it doesn’t already own out of network

Reduce benefits

Throughout the call with investors (actually with a couple dozen Wall Street financial analysts, the only people who can ask questions), Hemsley and team went on and on about the “value-based care” the company theoretically delivers, without providing specifics. But here is what you need to know: If you are enrolled in a UnitedHealth plan of any nature – commercial, Medicare or Medicaid or VA (yes, VA, too) – expect the value of your coverage to diminish, just as it has year after year after year.

The term for this in industry jargon is “benefit buydown.”

That means that even as your premiums go up by double digits, you will soon have fewer providers to choose from, you likely will spend more out-of-pocket before your coverage kicks in, you might have to switch to a medication made by a drug company UnitedHealth will get bigger kickbacks from, and you might even be among the 600,000 policyholders who will get “purged” (another industry term) at the end of the year.

Why do we and our employers and Uncle Sam keep putting up with this?

Yes, we pay more for new cars and iPhones, but we at least can count on some improvements in gas mileage and battery life and maybe even better-placed cup holders. You can now buy a massive high-def TV for a fraction of what it cost a couple of years ago. Health insurance? Just the opposite.

As I will explain in a future post, all of the big for-profit insurers are facing those same headwinds UnitedHealth is facing. You will not be spared regardless of the name on your insurance card. If you still have one come January 1. Pain is on the way. Once again.

It’s no secret the brand name prescription drug costs are high. The rising costs have been blamed by health care analysts on kickbacks within the drug supply chain demanded by the federal government, drug distributors (wholesalers), health insurance companies and pharmacy benefit managers (PBMs).

How about $356 billion worth of pure glut in the prescription drug supply chain, according to the analysis by DCI. Simply put, the market price established for these drugs by manufacturers has $356 billion worth of markups that mainly accommodate the financial demands (i.e. kickbacks or rebates) of groups that profit off the prescription drug system in the United States, health insurers and their PBMs in particular.

And that’s an all-time record.

Why?

Get ready to choke on your popcorn.

In the 1990s the federal government mandated in the Medicaid program that drug manufacturers offer a minimum rebate of 23% off the purchase price of brand name drugs. The feds also mandated that if drug manufacturers offer a better rebate on those drugs to someone else, the government also gets that same rebate.

The thought was no one gets a better deal than the federal government.

Rebates expanded again as PBMs continued to gain more control over the drug supply chain. The PBMs now force drug manufacturers to offer significant concessions in order to get on the list of approved medications – known as a formulary – available to patients with health insurance.

To account for these demands, drug manufacturers set the list price for their brand name drugs with these price concessions baked into the number.

DCI’s analysis found that baking is $356 billion of goodies for health care companies paid for by the government and you.

It’s the same kind of concept as a U.S. popular clothing retailer that displays inflated retail costs on the tags of goods and then right below displaying a lower “sale” price to make the consumer think they got a deal.

Here’s another way of thinking of it: Just like Congress has a lot of “pork” in its spending bills, there’s also a lot of pork in prescription drug costs that have very little to do with anything, other than increase profits for the health care industry.

Though the federal government intended to create a better system for taxpayers back in the 1990s when it demanded rebates in the Medicaid system, it instead created a feeding frenzy for companies in the drug supply chain.

In the year 2000 just a handful of companies in the drug supply chain dotted the Fortune 100 list of most financially successful companies. Today there are four such companies in the top 10.

The Minnesota-based health care conglomerate UnitedHealth leads that pack. The company’s profits have soared in the last two decades largely due to increasing medical costs and prescription drug costs paid by Americans. It has leaped over companies like Exxon Mobile and Apple to become the third largest company in America. Only Walmart and Amazon take in more revenue.

The company employs more than 400,000, including doctors and clinicians and has its own pharmacy benefits manager called Optum Rx.

We reported last month that Americans spent $464 billion last year on prescription drugs. That was also an all-time record, which will likely be set again and again and again until reforms are enacted.

Not long ago, Dr. Richard Menger, a neurosurgeon, was ready to operate on a 16-year-old with complex scoliosis. A team of doctors had spent months preparing for the surgery, consulting orthopedists and cardiologists, even printing a 3D model of the teen’s spine.

The surgery was scheduled for a Friday when Menger got the news: the teen’s insurer, Blue Cross Blue Shield of Alabama, had denied coverage of the surgery.

It wasn’t particularly surprising to Menger, who has been practicing in Alabama since 2019. Alabama essentially has one private insurer, Blue Cross Blue Shield of Alabama, which has a whopping 94% of the market of large-group insurance plans, according to the health policy nonprofit KFF. That dominance allows the insurer to consistently deny claims, many doctors say, charge people more for coverage, and pay lower rates to doctors and hospitals than they would in other states.

“It makes the natural problems for insurance that much more magnified because there’s no market competition or choice,” says Menger, who in 2023 wrote an op-ed in 1819 News, a local news site, arguing that ending Blue Cross Blue Shield of Alabama’s health insurance monopoly would make people in the state healthier.

Blue Cross Blue Shield of Alabama also has the largest share of individual insurance plans in the state, according to data from the Centers for Medicaid & Medicare Services. Perhaps not coincidentally, Alabama also had the highest denial rates for in-network claims by insurers on the individual marketplace in 2023, according to a KFF analysis: 34%. Neighboring Mississippi, where the majority insurer has less of the market share at 81%, has an average denial rate of 15%.

Alabama is an extreme case, but people in many other states face health insurance monopolies, too. One insurer, Premera Blue Cross Group, has a 94% share of the large-group market in Alaska, and Blue Cross Blue Shield of Wyoming has a 91% market share in that state. In 18 states, one insurer has 75% or more of the large-group health insurance marketplace, according to KFF data.

These monopolies drive up costs, says Leemore Dafny, a professor at Harvard Business School and Harvard Kennedy School who has long studied competition among health insurance companies and providers.

“More competitors tend to drive lower premiums and more generous benefits for consumers,” she says. “There’s a lot of concern from analysts like myself about concentration in a range of sectors, including health insurance.”

Bruce A. Scott, the immediate past president of the American Medical Association, has said that when the dominant insurer in his state of Kentucky was renegotiating its contract with his medical group, it offered lower rates than it had paid six years before. “This same type of financial squeeze play is found nationwide, and its frequency has been exacerbated by health insurance industry consolidation,” he wrote in The Hill in 2023.

What happened to competition? There used to be a lot more regional health insurers, Dafny says. But as costs started to rise, they didn’t have enough leverage to negotiate prices down with providers and stay profitable. As a result, many were happy to be acquired by larger companies. Then hospitals and doctor’s offices merged to get more leverage against the bigger insurers. Now, there’s a lot of concentration among both provider groups and insurers.

“None of this had anything to do with taking better care of patients,” she says. “It had to do with trying to get the upper hand.”

In a statement to TIME, Blue Cross Blue Shield of Alabama said that it was working to make the prior authorization process more transparent and reverse the requirement of prior authorization for certain in-network medical services. It will attempt to answer at least 80% of requests for prior authorization in near real-time by 2027, it says. (A coalition of major health insurers recently vowed to fix their prior authorization processes under pressure from the federal government.)

The insurer also says it welcomes competition. “We know Alabamians have a choice when it comes to choosing their health insurance carrier and we don’t take that for granted,” a spokesperson said in the statement. In the commercial and underwritten market—which represents the bulk of its business—Blue Cross Blue Shield Alabama competes with four other companies that sell individual, family, and group plans, the company says, and it competes with 68 companies who sell Medicare plans in Alabama. Its success in the state is partly because it sells policies in every county in Alabama, the insurer says, while others do not.

Other casualties of such a concentrated health-insurance marketplace are rural hospitals and providers. Small rural hospitals are often independent and have not merged with other systems like many of their large urban counterparts, so they have an even harder time negotiating with the one big insurer in the state, says Harold Miller, president and CEO of the Center for Healthcare Quality and Payment Reform, a national policy center that studies health-care costs. That means big insurers will often refuse to cover procedures or pay lower prices for services.

“I’ve had rural hospitals tell me they can’t even get the health plan on the phone,” Miller says.

In the past decade, the Department of Justice has stopped some mergers, but has not been very aggressive at stopping consolidation in the health-care industry, Dafny says. That may be in part because the courts require a high standard of evidence to block a transaction, and the government might have been worried it would have lost whatever cases it brought.

A few factors prevent insurers with a monopoly from driving costs too high, says Benjamin Handel, an economics professor at the University of California, Berkeley who studies health care. One is a regulation called minimum loss ratio that essentially requires insurers to spend a certain share of what they earn from premiums on medical care. Another is that an insurer with a monopoly that angers consumers might attract attention from regulators, he says.

Of course, there’s not a whole lot regulators can do to make a marketplace more competitive. A state could try to incentivize more insurers to enter their states with tax breaks or other sweeteners, but it’s very hard to enter a market and offer low rates right away. The establishment of the health-care marketplaces in the Affordable Care Act allowed new entrants, Dafny says, but many of them did not survive.

Menger, the Alabama doctor, says that he and his colleagues—and therefore their patients—are basically stuck. His staff has to spend 10-15 hours a week negotiating with the insurer to get prior authorizations that sometimes don’t come, even while patients pay higher premiums.

The teenage boy eventually got approved for the scoliosis surgery, but not after the family went through a lot of stress with postponements and uncertainty. “I think it’s pretty clear that the more competition, the better things are,” Menger says. “This prior authorization nonsense is really hurting patients.”