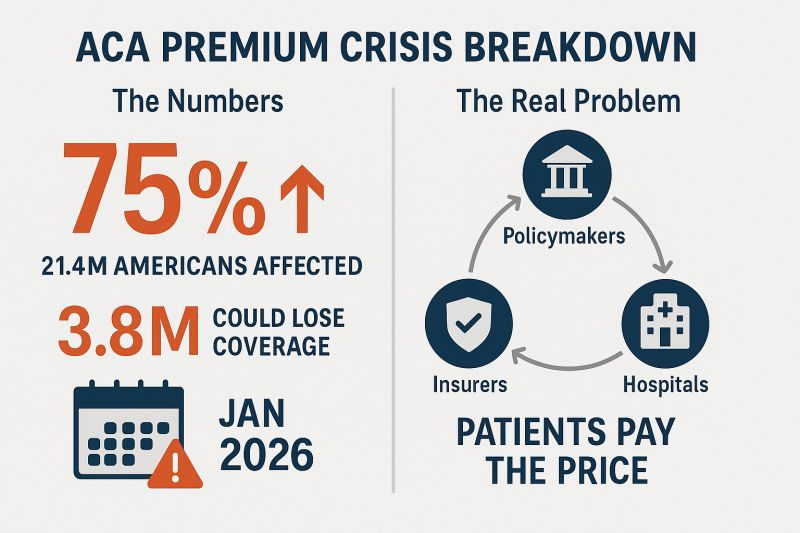

People who buy health insurance through the Affordable Care Act (ACA) are set to see a median premium increase of 18 percent, more than double last year’s 7 percent median proposed increase, according to an analysis of preliminary filings by KFF.

The proposed rates are preliminary and could change before being finalized in late summer. The analysis includes proposed rate changes from 312 insurers in all 50 states and DC.

It’s the largest rate change insurers have requested since 2018, the last time that policy uncertainty contributed to sharp premium increases. On average, ACA marketplace insurers are raising premiums by about 20 percent in 2026, KFF found.

Insurers said they wanted higher premiums to cover rising health care costs, like hospitalizations and physician care, as well as prescription drug costs. Tariffs on imported goods could play a role in rising medical costs, but insurers said there was a lot of uncertainty around implementation, and not many insurers were citing tariffs as a reason for higher rates.

But they are adding in higher increases due to changes being made by the Trump administration and Republicans in Congress. For instance, the majority of insurers said they are taking into account the potential expiration of enhanced premium tax credits.

Those subsidies, put in place during the COVID-19 pandemic, are set to expire at the end of the year, and there are few signs that Republicans are interested in tackling the issue at all.

If Congress takes no action, premiums for subsidized enrollees are projected to increase by over 75 percent starting in January 2026, according to KFF.

But some states are pushing back.

Arkansas Gov. Sarah Huckabee Sanders (R) on Wednesday called on the state’s insurance commissioner to disapprove the proposed increases from Centene and Blue Cross Blue Shield. The companies filed increases of up to 54 percent and 25.5 percent, respectively, she said.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both,” Huckabee Sanders said in a statement.

“I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

The healthcare industry is still licking its wounds from $1 trillion in federal funding cuts included in the One Big Beautiful Bill Act (OBBBA) signed into law July 4.

Adding insult to injury, the Center for Medicare and Medicaid services issued a 913-page proposed rule last Tuesday that includes unwelcome changes especially troublesome for hospitals i.e. adoption of site neutral payments, expansion of hospital price transparency requirements, reduction of inpatient-only services, acceleration of hospital 340B discount repayment obligations and more.

The combination of the two is bad news for healthcare overall and hospitals especially: the timing is precarious:

Economic uncertainty: Economists believe a recession is less likely but uncertainty about tariffs, fear about rising inflation, labor market volatility a housing market slowdown and speculation about interest rates have capital markets anxious. Healthcare is capital intense: the impact of the two in tandem with economic uncertainty is unsettling.

Consumer spending fragility: Consumer spending is holding steady for the time being but housing equity values are dropping, rents are increasing, student loan obligations suspended during Covid are now re-activated, prices for hospital and physicians are increasing faster than other necessities and inflation ticked up slightly last month. Consumer out-of-pocket spending for healthcare products and services is directly impacted by purchases in every category.

Heightened payer pressures: Insurers and employers are expecting double-digit increases for premiums and health benefits next year blaming their higher costs on hospitals and drugs, OBBBA-induced insurance coverage lapses and systemic lack of cost-accountability. For insurers, already reeling from 2023-2024 financial reversals, forecasts are dire. Payers will heighten pressure on healthcare providers—especially hospitals and specialists—as a result.

Why healthcare appears to have borne the brunt of the funding cuts in the OBBBA is speculative:

Might a case have been made for cuts in other departments? Might healthcare programs other than Medicaid have been ripe for “waste, fraud and abuse” driven cuts? Might technology-driven administrative costs reductions across the expanse of federal and state government been more effective than DOGE- blunt experimentation?

Healthcare is 18% of the GDP and 28% of total federal spending: that leaves room for cuts in other industries.

Why hospitals, along with nursing homes and public health programs, are likely to bear the lion’s share of OBBBA’ cut fallout and CMS’ proposed rule disruptions is equally vexing. Might the high-profile successes of some not-for-profit hospital operators have drawn attention? Might Congress have been attentive to IRS Form 990 filings for NFP operators and quarterly earnings of investor-owned systems and assume hospital finances are OK? Might advocacy efforts to maintain the status quo with facility fees, 340B drug discounts, executive compensation et al been overshadowed by concerns about consolidation-induced cost increases and disregard for affordability? Hospital emergency rooms in rural and urban communities, nursing homes, public health programs and many physicians will be adversely impacted by the OBBBA cuts: the impact will vary by state. What’s not clear is how much.

My take:

Having read both the OBBBA and CMS proposed rules and observed reactions from industry, two things are clear to me:

The antipathy toward the healthcare industry among the public and in Congress played a key role in passage of the OBBBA and regulatory changes likely to follow.

Polls show three-fourths of likely voters want to see transformational change to healthcare and two-thirds think the industry is more concerned with its profit over their care: these views lend to hostile regulatory changes. The public and the majority of elected officials think the industry prioritizes protection of the status quo over obligations to serve communities and the greater good.

The result: winners and losers in each sector, lack of continuity and interoperability, runaway costs and poor outcomes.

No sector in healthcare stands as the surrogate for the health and wellbeing of the population. There are well-intended players in each sector who seek the moral high ground for healthcare, but their boards and leaders put short-term sustainability above long-term systemness and purpose. That void needs to be filled.

The timing of these changes is predictably political.

Most of the lower-cost initiatives in both the OBBBA changes and CMS proposals carry obligations to commence in 2026—in time for the November 2026 mid-term campaigns. Most of the results, including costs and savings, will not be known before 2028 or after. They’re geared toward voters inclined to think healthcare is systemically fraudulent, wasteful and self-serving.

And they’re just the start: officials across the Departments of Health and Human Services, Justice, Commerce, Labor and Veterans Affairs will add to the lists.

Medicaid serves as a vital source of health insurance coverage for Americans living in rural areas, including children, parents, seniors, individuals with disabilities, and pregnant women. Congressional lawmakers are currently considering more than $800 billion in cuts to the Medicaid program, which would reduce Medicaid funding and terminate coverage for vulnerable Americans.

The proposed changes would also result in a significant reduction in Medicaid reimbursement that could result in rural hospital closures.

The National Rural Health Association recently partnered with experts from Manatt Health to shed light on the potential impacts of those cuts on rural residents and the hospitals that care for them over the next decade.

NRHA held a press conference on June 24 that can be accessed with passcode MBTZf4$H. NRHA chief policy officer Carrie Cochran-McClain discussed the findings with Manatt Health partner and former deputy administrator at CMS Cindy Mann and the real world implications of the details of this report with three NRHA member hospital and health system leaders

Report findings provide insight into the impact on rural America at a critical moment in the Congressional debate over the future of the reconciliation package.

The report shows the significant impact from coverage losses that rural communities will face given:

Medicaid plays an outsized role in rural America, covering a larger share of children and adults in rural communities than in urban ones.

Nearly half of all children and one in five adults in small towns and rural areas rely on Medicaid or CHIP for their health insurance.

Medicaid covers nearly one-quarter of women of childbearing age and finances half of all births in these communities.

According to Manatt’s estimates, rural hospitals will lose 21 cents out of every dollar they receive in Medicaid funding due to the One Big Beautiful Bill Act. Total cuts in Medicaid reimbursement for rural hospitals—including both federal and state funds—over the ten-year period outlined in the bill would reach almost $70 billion for hospitals in rural areas.

Reductions in Medicaid funding of this magnitude would likely accelerate rural hospital closures and reduce access to care for rural residents, exacerbating economic hardship in communities where hospitals are major employers.

As a key insurer in rural communities, Medicaid provides a financial lifeline for rural health care providers — including hospitals, rural health clinics, community health centers, and nursing homes—that are already facing significant financial distress. These cuts may lead to more hospitals and other rural facility closures, and for those rural hospitals that remain open, lead to the elimination or curtailment of critical services, such as obstetrics.

“Medicaid is a substantial source of federal funds in rural communities across the country. The proposed changes to Medicaid will result in significant coverage losses, reduce access to care for rural patients, and threaten the viability of rural facilities,” said Alan Morgan, CEO of the National Rural Health Association.

“It’s very clear that Medicaid cuts will result in rural hospital closures resulting in loss of access to care for those living in rural America.”

A media briefing will be held on Tuesday, June 24, from noon to 1:00 PMEST to provide more information about the analysis. This event will feature representatives from NRHA, Manatt Health, and rural hospital leaders across the country. Questions may be submitted in advance, as well as during the press conference. To register for and join the media briefing, click on the Zoom link here.

NRHA is a non-profit membership organization that provides leadership on rural health issues with tens of thousands of members nationwide. Our membership includes nearly every component of rural America’s health care, including rural community hospitals, critical access hospitals, doctors, nurses, and patients. We work to improve rural America’s health needs through government advocacy, communications, education, and research. Learn more about the association at RuralHealth.US.

About Manatt Health

Manatt Health is a leading professional services firm specializing in health policy, health care transformation, and Medicaid redesign. Their modeling draws upon publicly available state data including Medicaid financial management report data from the Centers for Medicare and Medicaid Services, enrollment and expenditure data from the Medicaid Budget and Expenditure System, and data from the Medicaid and CHIP Payment and Access Commission. The Manatt Health Model is tailored specifically to rural health and has been reviewed in consultation with states and other key stakeholders.

Nearly 12 million people would lose their health insurance under President Trump’s “big, beautiful bill,” an erosion of the social safety net that would lead to more unmanaged chronic illnesses, higher medical debt and overcrowding of hospital emergency departments.

Why it matters:

The changes in the Senate version of the bill could wipe out most of the health coverage gains made under the Affordable Care Act and slash state support for Medicaid and SNAP.

“We are going back to a place of a lot of uncompensated care and a lot of patchwork systems for people to get care,” said Ellen Montz, a managing director at Manatt Health who oversaw the ACA federal marketplace during the Biden administration.

The big picture:

The stakes are huge for low-income and working-class Americans who depend on Medicaid and subsidized ACA coverage.

Without health coverage, more people with diabetes, heart disease, asthma and other chronic conditions will likely go without checkups and medication to keep their ailments in check.

Those who try to keep up with care after losing insurance will pay more out of pocket, driving up medical debt and increasing the risk of eviction, food insecurity and depleted savings.

Uninsured patients have worse cancer survival outcomes and are less likely to get prenatal care. Medicaid also is a major payer of behavioral health counseling and crisis intervention.

Much of the coverage losses from the bill will come from new Medicaid work reporting requirements, congressional scorekeepers predict. Work rules generally will have to be implemented for coverage starting in 2027, but could be earlier or later depending on the state.

Past experiments with Medicaid work rules show that many eligible people fall through the cracks verifying they’ve met the requirements or navigating new state bureaucracies.

Often, people don’t find out they’ve lost coverage until they try to fill a prescription or see their doctor. States typically provide written notices, but contacts can be out of date.

Nearly 1 in 3 adults who were disenrolled from Medicaid after the COVID pandemic found out they no longer had health insurance only when they tried to access care, per a KFF survey.

Zoom out:

The Medicaid and ACA changes will also affect people who keep their coverage.

The anticipated drop-off in preventive care means the uninsured will be more likely to go to the emergency room when they get sick. That could further crowd already bursting ERs, resulting in even longer wait times.

Changes to ACA markets in the bill, along with the impending expiration of enhanced premium subsidies, may drive healthier people to drop out, Montz said, skewing the risk pool and driving up premiums for remaining enrollees.

States will likely have to make further cuts to their safety-net programs if the bill passes in order to keep state budgets functioning with less federal Medicaid funding.

The other side:

The White House and GOP proponents of the bill say the health care changes will fight fraud, waste and abuse, and argue that coverage loss projections are overblown.

Conservative health care thinkers also posit that there isn’t strong enough evidence that public health insurance improves health.

Reality check:

Not all insurance is created equally, and many people with health coverage still struggle to access care. But the bill’s impact would take the focus off ways to improve the health system, Montz said.

“This is taking us catastrophically backward, where we don’t get to think about the things that we should be thinking about how to best keep people healthy,” she said.

The bottom line:

The changes will unfold against a backdrop of Health Secretary Robert F. Kennedy Jr.’s purported focus on preventive care and ending chronic illness in the U.S.

But American health care is an insurance-based system, said Manatt Health’s Patricia Boozang. Coverage is what unlocks access.

Scrapping millions of people’s health coverage “seems inconsistent with the goal of making America healthier,” she said.

The CBO projects that 10.9 million more people would be uninsured under President Trump’s sweeping budget bill — mostly from the way it would overhaul Medicaid, including new work requirements.

Why it matters:

That would amount to major coverage losses that are certain to fuel Democratic attacks on the measure, and put new pressure on vulnerable Republicans heading into the midterm election cycle, Peter Sullivan wrote first on Pro.

By the numbers:

The CBO on Wednesday projected that 7.8 million more people would be uninsured due to the Medicaid changes, with the rest likely due to Affordable Care Act marketplace changes, including new barriers to signing up that are aimed at fighting fraud.

The estimate includes 1.4 million people without verified citizenship “or satisfactory immigration status,” a reference to undocumented immigrants that some states opt to cover with non-federal dollars in their Medicaid programs.

The CBO was responding to a request from congressional Democrats about the number of uninsured people stemming from the package the House passed last month.

Republicans say the changes would ensure that Medicaid is targeted at beneficiaries deserving of coverage, and that taxpayer money should not be spent on healthy adults who are choosing not to work.

Opponents say people who are working will be caught up in the red tape from the changes and could still lose coverage.

The CBO also said another 5.1 million would become uninsured if Congress opts to let Affordable Care Act premium tax credit subsidies expire next year.

If a picture is worth a thousand words, a video, if done well, can be worth thousands more.

Regular readers of HEALTH CARE un-covered know we have published lots of words about the barriers health insurance companies have erected that make it harder and harder for patients to get the care their doctors know they need.

It’s a perfect example of how something that was designed to protect patients from inappropriate and unnecessary care has been weaponized by health insurers to pad their bottom lines.

Prior authorization in today’s world all too often serves as a bureaucratic barrier, requiring patients and their doctors to obtain approval in advance from insurers before certain treatments, medications, or procedures will be covered.

While insurance companies argue that prior authorization helps control costs and ensure appropriate care, the reality is far grimmer.

Both patients and their health care providers suffer the consequences. Patients frequently face delays in receiving necessary treatments or medications, exacerbating their health conditions and causing unnecessary stress and anxiety. Many forgo needed care altogether due to the complexities and frustrations of navigating the prior authorization process. This practice not only undermines patients’ trust in their health care providers but also compromises their health, often leading to worsened conditions and, tragically, sometimes irreversible harm.

The burden of prior authorization falls heavily on clinicians and their office staff who must spend valuable time and resources navigating the bureaucratic red tape imposed by insurers. This administrative burden not only detracts from patient care but also contributes to physician burnout, dissatisfaction and moral crisis, according to many doctors.

Ultimately, the health insurance industry’s prioritization of profit over patient well-being is evident in its insistence on maintaining these barriers to care, perpetuating a system that defaults to financial gain at the expense of human lives.

The New York Times video cuts to the chase. Prior authorization, as practiced today by insurance companies, is “medical injustice disguised as paperwork.”

Last week, the nation’s two largest Medicare Advantage insurers revealed that second quarter outpatient volumes were higher than anticipated, prompting a selloff of insurance stocks.

Minnetonka, MN-based UnitedHealth Group (UHG) executives said at a Goldman Sachs investor conference that increased outpatient utilization was driving up its medical loss ratio (MLR) to the high end of its annual target, surmising that a new wave of seniors were finally accessing elective procedures like joint replacements postponed throughout COVID.

Then, in an investor filling, Louisville, KY-based Humana noted that both outpatient and inpatient utilization levels were elevated, though it did not point to any specific causes. But not all insurers have experienced higher-than-expected utilization: Indianapolis, IN-based Elevance Health reported that its medical spending this year so far was in line with expectations, and it did not expect a surge in procedure demand.

The Gist: Health systems will find this news, especially Humana’s reports of elevated inpatient and emergency department volumes, as encouraging as the insurers consider it alarming. But the bulk of this outpatient volume isn’t necessarily returning to health systems, as the proliferation of insurer- and investor-backed ambulatory surgery centers has resulted in not only more, but also lower-cost, competition.

Health systems with significant ambulatory surgery center footprints, including Tenet and HCA, should be well-positioned to capture the volume return.

A majority of Americans with health insurance said they had encountered obstacles to coverage, including denied medical care, higher bills and a dearth of doctors in their plans, according to a new survey from KFF, a nonprofit health research group. As a result, some people delayed or skipped treatment.

Those who were most likely to need medical care — people who described themselves as in fair or poor health — reported more trouble; three-fourths of those receiving mental health treatment experienced problems.

“The consequences of care delayed and missed altogether because of the sheer complexity of the system are significant, especially for people who are sick,” said Drew Altman, the CEO of KFF, formerly known as the Kaiser Family Foundation.

The survey also underscored the persistent problem of affordability as people struggled to pay their share of health care costs. About 40% of those surveyed said they had delayed or gone without care in the last year because of the expense. People in fair or poor health were more than twice as likely to report problems with paying medical bills than those in better health, and Black adults were more likely than white adults to indicate they had trouble.

Why It Matters: Delayed care can endanger health.

Nearly half of those who encountered a problem with their insurance said they could not satisfactorily resolve it. Some could not obtain the care they had sought, while others said they paid more than expected. Among the nearly 60% who reported difficulty with their insurance coverage, 15% said their health had declined.

“This survey shows it’s not enough to just get a card in your pocket — the insurance has to work or it’s not exactly coverage,” said Karen Pollitz, the co-director for KFF’s patient and consumer protections program.

People have a hard time understanding their coverage and benefits, with 30% or more reporting difficulty figuring out what they will be required to pay for care or what exactly their insurance will cover.

“Insurances are way more complicated than they should be,” said Amanda Parente, a 19-year-old college student in Nashville, Tennessee, who is covered under her mother’s employer plan. She was surprised to find that her out-of-pocket costs spiked recently when she sought treatment for strep throat. While she realized her copayments would be higher, “I guess we didn’t know how drastic it was going to be,” she said.

Background: Insurance coverage is confusing to everyone.

Navigating the intricacies of coverage and benefits were similar regardless of what kind of insurance people had. At least half of those surveyed with private coverage, through an employer, those with an “Obamacare” plan, or a government program like Medicare or Medicaid, said they experienced difficulties.

People might be unhappy with their coverage because they were already concerned about higher inflation and potential layoffs, said Christopher Lis, the managing director of global health care intelligence at J.D. Power, which found that consumer satisfaction with insurers had declined in a recent study. “We’ve got economic conditions that set the stage for concern around coverage and benefits,” he said.

Insurers say people generally report being happy with their plan, and 81% of those surveyed by KFF gave their insurance high ratings. “Health insurance providers are committed to improving access, affordability and convenience for all Americans and will continue to find innovative solutions to work toward this common goal,” said David Allen, a spokesperson for AHIP, a trade group that represents insurers.

What’s Next: How to haggle with insurers or appeal?

Also striking among the survey’s findings was how unaware people were about pursuing appeals of denied coverage and how to go about doing so.

“Most people don’t know who to call,” Pollitz said. Sixty percent of insured adults surveyed did not know they had a legal right to appeal, and about three-fourths said they did not know which government agency to contact for help, particularly respondents with private insurance.

State insurance regulators oversee fully insured policies sold to individuals and small businesses, and the federal Department of Labor has jurisdiction over employer-sponsored insurance.

Many of the problems people have with their insurance could be solved by enforcing existing rules, like federal regulations requiring private insurers to issue understandable explanations of benefits and to maintain accurate, current lists of doctors and hospitals within their networks.

Pent-up demand for delayed healthcare during the COVID-19 pandemic is pressuring medical costs for health insurers that had a financial windfall during the pandemic amid low utilization.

UnitedHealth, the parent company of the largest private payer in the U.S., expects its medical loss ratio — the share of premiums spent on member’s healthcare costs — to be higher than previously expected in the second quarter of 2023, due to a surge in outpatient care utilization among seniors, CFO John Rex said Tuesday during Goldman Sachs’ investor conference.

The news sent UnitedHealth’s stock down 7% in morning trade Wednesday, and affected other Medicare-focused health insurers as well. Humana, CVS and Centene — the three largest MA insurers by enrollee after UnitedHealth — dropped 13%, 6% and 8%, respectively.

Dive Insight:

The early days of COVID saw widespread halts in nonessential services, causing visits to plunge with an estimated one-third of U.S. adults delaying or foregoing medical care in the pandemic’s first year. By 2022, the sizable rebound in deferred care that many predicted had yet to materialize.

Now, early signs suggest utilization may again be increasing, with the cost of rebounding care coming around to hit payers. UnitedHealth now expects its MLR for the second quarter to reach or exceed its full-year target of 82.1% to 83.1%.

“As you look at a Q2, you would expect Q2 medical care ratio to be somewhere in the zone of probably the upper bound or moderately above the upper bound of our full-year outlook,” Rex said. “I would expect at this distance that the full year would probably settle in in the upper half of the existing range we set up.”

In comparison, the insurer reported an MLR of 82.2% in the first quarter of 2023. UnitedHealth’s MLR was 82% in 2022.

UnitedHealth said the MLR increase is because medical activity is normalizing after COVID kept seniors away from non-essential care.

“We’re seeing as behaviors kind of normalize across the country in a lot of different ways and mask mandates are dropped, especially in physician offices, we’re seeing that more seniors are just more comfortable accessing services for things that they might have pushed off a bit like knees and hips,” said Tim Noel, UnitedHealth’s chief executive for Medicare and retirement.

The Minnetonka, Minnesota-based insurer has seen strong outpatient demand through April, May and June, particularly in hips and knees with high volumes at its owned ambulatory surgical centers and within its Medicare business, executives said.

Inpatient volumes have remained consistent, and while outpatient utilization has increased, patient acuity has remained the same. Optum Health’s behavioral businesses are also seeing higher utilization in the second quarter, said Patrick Conway, CEO of Care Solutions at Optum, UnitedHealth’s health services division.

UnitedHealth doesn’t expect this higher activity to let up anytime soon. As a result, the payer incorporated higher outpatient utilization into its Medicare Advantage plan bids for 2024, which were placed in early June. The move attests to the longer duration of the trend, SVB Securities analyst Whit Mayo wrote in a note.

“Assuming it is going to end quickly wouldn’t be prudent on our part,” Rex said. “We’ll see how this progresses here.”

The film “American Hospitals: Healing a Broken System” premiered in Washington, D.C., on March 29. This documentary exposes the inconvenient truths embedded within the U.S. healthcare system. Here is a dirty dozen of them:

Hospitals are largely unaccountable for poor clinical outcomes.

The cost of commercially insured care is multiples higher than the cost of government-insured care for identical procedures.

Customer service at hospitals is dreadful.

Frontline clinicians are overburdened and leaving the profession in droves.

Healthcare still operates the same way it has for the last one hundred years — delivering hierarchical, fragmented, hospital-centric, disease-centric, physician-centric “sick” care. Accordingly, healthcare business models optimize revenue generation and profitability rather than health outcomes. These factors explain, in part, why U.S. life expectancy has declined four of the five years and maternal deaths are higher today than a generation ago.

It’s hard to imagine that the devil itself could create a more inhumane, ineffective, costly and change-resistant system. Hospitals consume more and more societal resources to maintain an inadequate status quo. They’re a major part of America’s healthcare problem, certainly not its solution. Even so, hospitals have largely avoided scrutiny and the public’s wrath. Until now.

“American Hospitals” is now playing in theaters throughout the nation. It chronicles the pervasive and chronic dysfunction plaguing America’s hospitals. It portrays the devastating emotional, financial and physical toll that hospitals impose on both consumers and caregivers.

Despite its critical lens, “American Hospitals” is not a diatribe against hospitals. Its contributors include some of healthcare’s most prominent and respected industry leaders, including Donald Berwick, Elizabeth Rosenthal, Shannon Brownlee and Stephen Klasko. The film explores payment and regulatory reforms that would deliver higher-value care. It profiles Maryland’s all-payer system as an example of how constructive reforms can constrain healthcare spending and direct resources into more effective, community-based care.

The United States already spends more than enough on healthcare. It doesn’t need to spend more. It needs to spend more wisely. The system must downsize its acute and specialty care footprint and invest more in primary care, behavioral health, chronic disease management and health promotion. It’s really that simple.

My only critique of “American Hospitals” is many of its contributors expect too much from hospitals. They want them to simultaneously improve their care delivery and advance the health of their communities. This is wishful thinking. Health and healthcare are fundamentally different businesses. Rather than pivoting to population health, hospitals must focus all their efforts on delivering the right care at the right time, place and price.

If hospitals can deliver appropriate care more affordably, this will free up enormous resources for society to invest in health promotion and aligned social-care services. In this brave new world, right-sized hospitals deliver only necessary care within healthier, happier and more productive communities.

All Americans deserve access to affordable health insurance that covers necessary healthcare services without bankrupting them and/or the country. Let me restate the obvious. This requires less healthcare spending and more investments in health-creating activities. Less healthcare and more health is the type of transformative reform that the country could rally behind.

At issue is whether America’s hospitals will constructively participate in downsizing and reconfiguring the nation’s healthcare system. If they do so, they can reinvent themselves from the inside out and control their destinies.

Historically, hospitals have preferred to use their political and financial leverage to protect their privileged position rather than advance the nation’s well-being. Like Satan in Milton’s “Paradise Lost,” they have preferred to reign in hell rather than serve in heaven.

Pride comes before the fall. Woe to those hospitals that fight the nation’s natural evolution toward value-based care and healthier communities. They will experience a customer-led revolution from outside in and lose market relevance. Only by admitting and addressing their structural flaws can hospitals truly serve the American people.