Despite a a seventh straight month of industrywide negative margins, “hospitals and health systems must think strategically and make investments to strengthen performance toward long-term institutional goals despite the day-to-day financial challenges they experience,” Kaufman Hall’s Erik Swanson said.

Months of inching performance gains were upended in July as the nation’s hospitals logged “some of the worst margins since the beginning of the COVID-19 pandemic,” Kaufman Hall wrote in its latest industry report.

Decreasing outpatient revenues paired with pricier inpatient stays were chief among the culprits and outpaced minor improvements in expenses, the group wrote in its monthly sector update for July.

What’s more, seven straight months of negative margins “reversed any gains hospitals saw this year” and has the advisory group forecasting a brutal year for the industry.

“July was a disappointing month for hospitals and put 2022 on pace to be the worst financial year hospitals have experienced in a long time,” Erik Swanson, senior vice president of data and analytics with Kaufman Hall, said in a statement. “Over the past few years, hospitals and health systems have been able to offset some financial hardship with federal support, but those funding sources have dried up, and hospitals’ bottom lines remain in the red.”

Kaufman Hall placed its median year-to-date operating margin index at -0.98% through July, compared to the -0.09% from January to June the group had reported during last month’s report. Hospitals’ median percent change in operating margin from June to July was -63.9%, according to the report, and -73.6% from July 2021.

The month’s volume trends hinted at the larger shift toward scheduling procedures for ambulatory settings, Kaufman Hall wrote. For instance, operating room minutes declined 10.3% from June to July and 7.7% year over year, according to the report.

Patients who did come into the hospital tended to be sicker, the firm continued. Average length of stay increased 2% from last month and 3.4% year over year. Patient days increased 2.8% from the previous month but were down 2.6% from the prior year, while adjusted discharges dipped 2.8% from June and 4.2% from July 2021.

These trends came together as a brake check on 2022’s to-date revenue gains. Gross operating revenue fell 3.6% from June but remains up 5.5% year to date. Outpatient revenue was down 4.8% from June and maintains a 7.1% year-to-date increase. Inpatient revenue declined 0.7% from June but is still up 3.6% year to date.

The silver lining in Kaufman Hall’s report were total expenses that, although up 7.6% from July 2021, saw a modest 0.4% decline since June. Those savings came squarely among supply and drug expenses as total labor costs and labor expense per adjusted discharge still grew 0.8% and 3.5%, respectively, since June. Increases in full-time employees per adjusted occupied bed “possibly” suggest increased hiring, the group wrote in the report.

Kaufman Hall acknowledged the “urgency of day-to-day pressures” driving the month’s sudden performance dips but urged hospital leaders to prioritize long-term operational improvements as they work to keep the organization afloat.

“2022 has been, and will likely continue to be, a challenging year for hospitals and health systems, but it would not be prudent to focus on short-term solutions at the expense of long-term planning,” Swanson said. “Hospitals and health systems must think strategically and make investments to strengthen performance toward long-term institutional goals despite the day-to-day financial challenges they experience.”

Kaufman Hall’s monthly reports are based on a sample of more than 900 nationally representative hospitals.

The group isn’t alone in its doom-and-gloom warnings for providers. Fitch Ratings recently wrote that high expenses, jilted volume gains and other challenges are unlikely to resolve before the end of the year. As such, the agency downgraded its outlook for the nonprofit hospital industry from “neutral” to “deteriorating.”

Nonprofit hospitals’ median financial metrics showed improvement last year, but Fitch Ratings is projecting declines for next year and beyond.

The credit rating agency analyzed 2021 audited data and reported that “AA” rated hospital medians showed a 20 percent increase in cash to adjusted debt. “BBB” rated health systems had an 8 percent increase.

“The deceptively strong numerical improvements over prior years’ medians are less a sign of sector resiliency and more a cautionary calm before the storm,” Fitch Ratings senior director Kevin Holloran said in the Aug. 18 report. “Additional expenses, primarily labor, have become part of the permanent fabric of hospital operations, that when combined with ongoing incremental challenges will exert tremendous pressure on providers through calendar 2022 and beyond.”

Fitch predicts hospital medians will flip this time next year due to inflationary pressures, a challenging operational start to 2022 and additional omicron sub-variants.

Fitch also highlighted staffing as a concern for hospital medians.

“We are likely two years before some level of ‘normal’ returns to the sector,” Mr. Holloran said in the report. “For many hospitals, their ‘value journey’ will be on temporary hold until expenses stabilize and become more predictable.”

Here are eight health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings and Moody’s Investors Service.

1. Advocate Aurora Health has an “AA” rating and stable outlook with Fitch. The health system, dually headquartered in Milwaukee and Downers Grove, Ill., has a strong financial profile and a leading market position over a broad service area in Illinois and Wisconsin, Fitch said. The health system’s fundamental operating platform is strong, the credit rating agency said.

2. Banner Health has an “AA-” rating and stable outlook with Fitch. The Phoenix-based health system’s core hospital delivery system and growth of its insurance division combine to make it a successful highly integrated delivery system, Fitch said. The credit rating agency said it expects Banner to maintain operating EBITDA margins of about 8 percent on an annual basis, reflecting the growing revenues from the system’s insurance division and large employed physician base.

3. Lincoln, Neb.-based Bryan Health has an “AA-” rating and stable outlook with Fitch. The health system has a leading and growing market position, very strong cash flow and a strong financial position, Fitch said. The credit rating agency said Bryan Health has been resilient through the COVID-19 pandemic and is well-positioned to accommodate additional strategic investments.

4. Gundersen Health System has an “AA-” rating and stable outlook with Fitch. The La Crosse, Wis.-based health system has strong balance sheet metrics and a leading market position and expanding operating platform in its service area, Fitch said. The credit rating agency expects the health system to return to strong operating performance as it emerges from disruption related to the COVID-19 pandemic.

5. Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based health system has shown consistent year-over-year increases in market share and has a solid liquidity position, Fitch said.

6. Falls Church, Va.-based Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The health system has a consistently strong operating cash flow margin and ample balance sheet resources, Moody’s said. Inova’s financial excellence will remain undergirded by its favorable regulatory and economic environment, the credit rating agency said.

7. Salt Lake City-based Intermountain Healthcare has an “Aa1” rating and stable outlook with Moody’s. The health system has exceptional credit quality, which will continue to benefit from its leading market position in Utah, Moody’s said. The credit rating agency said the health system’s merger with Broomfield, Colo.-based SCL Health will give Intermountain greater geographic reach.

8. UnityPoint Health has an “AA-” rating and stable outlook with Fitch. The Des Moines, Iowa-based health system has strong leverage metrics and cash position, Fitch said. The credit rating agency expects the health system’s balance sheet and debt service coverage metrics to remain robust.

Hospitals are forced to absorb inflationary expenses, particularly related to supporting their workforce, AHA says.

The Centers for Medicare and Medicaid Services’ increase in the inpatient payment rate for 2023 is welcome but not enough to offset expenses, according to the American Hospital Association.

CMS set a 4.1% market basket update for 2023 in its final rule released Monday, calling it the highest in the last 25 years. The increase was due to the higher cost in compensation for hospital workers.

The final rule gave inpatient hospitals a 4.3% increase for 2023, as opposed to the 3.2% increase in April’s proposed rule.

WHY THIS MATTERS

CMS used more recent data to calculate the market basket and disproportionate share hospital payments, a move that better reflects inflation and labor and supply cost pressures on hospitals, the AHA said.

“That said, this update still falls short of what hospitals and health systems need to continue to overcome the many challenges that threaten their ability to care for patients and provide essential services for their communities,” said AHA Executive Vice President Stacey Hughes. “This includes the extraordinary inflationary expenses in the cost of caring hospitals are being forced to absorb, particularly related to supporting their workforce while experiencing severe staff shortages.”

The AHA would continue to urge Congress to take action to support the hospital field, including by extending the low-volume adjustment and Medicare-dependent hospital programs, Hughes said.

In late July, Senate and House members urged CMS to increase the inpatient hospital payment.

Premier, which works with hospitals, also said the 4.3% payment update falls short of reflecting the rising labor costs that hospitals have experienced since the onset of the pandemic.

“Coupled with record high inflation, this inadequate payment bump will only exacerbate the intense financial pressure on American hospitals,” said Soumi Saha, senior vice president of Government Affairs for Premier.

THE LARGER TREND

Recent studies show hospitals remain financially challenged since the COVID-19 pandemic’s effect on revenue and supply chain and labor expenses. Piled onto that has been inflation that has added to soaring expenses.

Hospital margins were up slightly from May to June, but are still significantly lower than pre-pandemic levels, according to a Flash Report from Kaufman Hall.

The effects of the pandemic on the healthcare industry have been profound, resulting in the creation of new business models, according to a report from McKinsey.

Transformational change is necessary as hospitals have been hit hard by eroding margins due to cost inflation and expenses, Fitch found.

Here are 10 health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings and Moody’s Investors Service.

1. AnMed Health has an “AA-” rating and stable outlook with Fitch. The Anderson, S.C.-based system has a leading market share in most service lines, strong operating performance and very solid EBITDA margins, Fitch said.

2. Banner Health has an “AA-” rating and stable outlook with Fitch. The Phoenix-based health system’s core hospital delivery system and growth of its insurance division combine to make it a successful highly integrated delivery system, Fitch said. The credit rating agency said it expects Banner to maintain operating EBITDA margins of about 8 percent on an annual basis, reflecting the growing revenues from the system’s insurance division and large employed physician base.

3. Franciscan Alliance has an “AA” rating and stable outlook with Fitch. The Mishawaka, Ind.-based health system has a very strong cash position and maintains leading market shares in seven of its nine defined primary service areas, Fitch said. The health system benefits from a good payer mix, the credit rating agency said.

4. Gundersen Health System has an “AA-” rating and stable outlook with Fitch. The La Crosse, Wis.-based health system has strong balance sheet metrics and a leading market position and expanding operating platform in its service area, Fitch said. The credit rating agency expects the health system to return to strong operating performance as it emerges from disruption related to the COVID-19 pandemic.

5. Hackensack Meridian Health has an “AA-” rating and stable outlook with Fitch. The Edison, N.J.-based health system has shown consistent year-over-year increases in market share and has a solid liquidity position, Fitch said.

6. Falls Church, Va.-based Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The health system has a consistently strong operating cash flow margin and ample balance sheet resources, Moody’s said. Inova’s financial excellence will remain undergirded by its favorable regulatory and economic environment, the credit rating agency said.

7. Salt Lake City-based Intermountain Healthcare has an “Aa1” rating and stable outlook with Moody’s. The health system has exceptional credit quality, which will continue to benefit from its leading market position in Utah, Moody’s said. The credit rating agency said the health system’s merger with Broomfield, Colo.-based SCL Health will give Intermountain greater geographic reach.

8. Fort Wayne, Ind.-based Parkview Health has an “Aa3” rating and stable outlook with Moody’s. The health system has a leading market position with expansive tertiary and quaternary clinical services in northeastern Indiana and northwestern Ohio, Moody’s said. The credit rating agency said the stable outlook reflects management’s ability to generate strong operating performance during the pandement and with less favorable reimbursement rates.

9. UnityPoint Health has an “AA-” rating and stable outlook with Fitch. The Des Moines, Iowa-based health system has strong leverage metrics and cash position, Fitch said. The credit rating agency expects the health system’s balance sheet and debt service coverage metrics to remain robust.

10. Yale New Haven (Conn.) Health has an “AA-” rating and stable outlook with Fitch. The health system’s turnaround efforts, brand recognition and market presence will help it return to strong operating

Here are 11 health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. Morristown, N.J.-based Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The health system has strong operating performance and liquidity metrics, Moody’s said. The credit rating agency expects Atlantic Health System to sustain strong performance to support capital spending.

2. Greensboro, N.C.-based Cone Health has an “AA” rating and stable outlook with Fitch. The health system has a leading market share and a favorable payer mix, Fitch said. The health system’s broad operating platform and strategic capital investments should enable it to return to stronger operating results, the credit rating agency said.

3. Falls Church, Va.-based Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The health system has a consistently strong operating cash flow margin and ample balance sheet resources, Moody’s said. Inova’s financial excellence will remain undergirded by its favorable regulatory and economic environment, the credit rating agency said.

4. Vineland, N.J.-based Inspira Health Network has an “AA-” rating and stable outlook with Fitch. The health system has strong operating performance, a leading market position in a stable service area and a growing residency program, Fitch said. The credit rating agency expects the system’s growing outpatient footprint and an increase in patient volumes to support its operating stability.

5. Oakland, Calif.-based Kaiser Permanente has an “AA-” rating and stable outlook with Fitch. The health system has a strong financial profile, and the system’s operating platform is “arguably the most emulated model” for nonprofit healthcare delivery in the U.S., Fitch said. By revenue base, Kaiser is the largest nonprofit health system in the U.S., and it is the most fully integrated healthcare delivery system in the country, according to the credit rating agency.

6. Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s and an “AA-” rating and stable outlook with S&P. The Boston-based health system has an excellent clinical reputation, good financial performance and strong balance sheet metrics, Moody’s said. The credit rating agency said it expects Mass General Brigham to maintain a strong market position and stable financial performance.

7. Rochester, Minn.-based Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The credit rating agency said Mayo Clinic’s strong market position and patient demand will drive favorable financial results. The health system “will continue to leverage its excellent reputation and patient demand to continue generating favorable operating performance while maintaining strong balance sheet ratios,” Moody’s said.

8. Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. The Dallas-based system has strong operating performance, and investments in facilities have allowed it to continue to capture more market share in the fast-growing Dallas-Fort Worth, Texas, area, Moody’s said. The credit rating agency said it expects Methodist Health System’s strong operating performance and favorable liquidity to continue.

9. Traverse City, Mich.-based Munson Healthcare has an “AA” rating and stable outlook with Fitch. The health system has a strong market position, a good payer mix and robust cash-to-adjusted debt levels, Fitch said. The credit rating agency expects the system to weather an expected period of weakened operating cash flow margins.

10. Albuquerque, N.M.-based Presbyterian Healthcare Services has an “Aa3” rating and stable outlook with Moody’s and an “AA” rating and stable outlook with Fitch. Presbyterian Healthcare Services is the largest health system in New Mexico, and it has strong revenue growth and a healthy balance sheet, Moody’s said. The credit rating agency said it expects the health system’s balance sheet and debt metrics to remain strong.

11. University of Iowa Hospitals and Clinics has an “Aa2” rating and stable outlook with Moody’s. The Iowa City-based health system, the only academic medical center in Iowa, has strong patient demand and excellent financial management, Moody’s said. The credit rating agency said it expects the health system to continue to manage the pandemic with improved operating cash flow margins.

Hospitals are experiencing significant increases in expenses for workforce, drugs and medical supplies

Introduction

For over two years since the outset of the COVID-19 pandemic, America’s hospitals and health systems have been on the front lines caring for patients, comforting families and protecting communities.

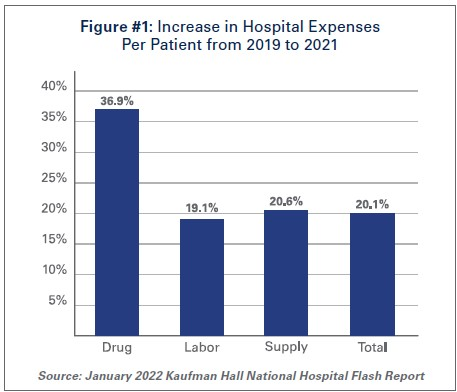

With over 80 million cases1, nearly 1 million deaths2, and over 4.6 million hospitalizations3, the pandemic has taken a significant toll on hospitals and health systems and placed enormous strain on the nation’s health care workforce. During this unprecedented public health crisis, hospitals and health systems have confronted many challenges, including historic volume and revenue losses, as well as skyrocketing expenses (See Figure #1).

Hospitals and health systems have been nimble in responding to surges in COVID-19 cases throughout the pandemic by expanding treatment capacity, hiring staff to meet demand, acquiring and maintaining adequate supplies and personal protective equipment (PPE) to protect patients and staff and ensuring that critical services and programs remain available to the patients and communities they serve. However, these and other factors have led to billions of dollars in losses over the last two years for hospitals, and over 33% of hospitals are operating on negative margins.

The most recent surges triggered by the delta and omicron variants have added even more pressure to hospitals. During these surges, hospitals saw the number of COVID-19 infected patients rise while other patient volumes fell, and patient acuity increased. This drove up expenses and added significant financial pressure for hospitals. Moreover, hospitals did not receive any government assistance through the COVID-19 Provider Relief Fund (PRF) to help mitigate rising expenses and lost revenues during the delta and omicron surges. This is despite the fact that more than half of COVID-19 hospitalizations have occurred since July 1, 2021, during these two most recent COVID-19 surges.

At the same time, patient acuity has increased, as measured by how long patients need to stay in the hospital. The increase in acuity is a result of the complexity of COVID-19 care, as well as treatment for patients who may have put off care during the pandemic. The average length of a patient stay increased 9.9% by the end of 2021 compared to pre-pandemic levels in 2019.4

As hospitals treat sicker patients requiring more intensive treatment, they also must ensure that sufficient staffing levels are available to care for these patients, and must acquire the necessary expensive drugs and medical supplies to provide high-quality care. As a result, overall hospital expenses have experienced considerable growth.

Data from Kaufman Hall, a consulting firm that tracks hospital financial metrics, shows that by the end of 2021, total hospital expenses were up 11% compared to pre-pandemic levels in 2019. Even after accounting for changes in volume that occurred during the pandemic, hospital expenses per patient increased significantly from pre-pandemic levels across every category. (See Figure #1)

The pandemic has strained hospitals’ and health systems’ finances. Many hospitals operate on razorthin margins, so even slight increases in expenses can have dramatic negative effects on operating margins, which can jeopardize their ability to care for patients. These expense increases have been more challenging to withstand in light of rising inflation and growth in input prices. In fact, despite modest growth in revenues compared to pre-pandemic levels, median hospital operating margins were down 3.8% by the end of 2021 compared to pre-pandemic levels, according to Kaufman Hall. Further exacerbating the problem for hospitals are Medicare sequestration cuts and payment increases that are well below increases in costs. For example, an analysis by PINC found that for fiscal year 2022, hospitals received a 2.4% increase in their Medicare inpatient payment rate, while hospital labor rates increased 6.5%.5

These levels of increased expenses and declines in operating margins are not sustainable. This report highlights key pressures currently facing hospitals and health systems, including:

Each of these issues separately presents significant challenges to the hospital field. Taken together, they represent conditions that would be potentially catastrophic for most organizations, institutions and industries. However, the fact that the nation’s hospitals and health systems continue to serve on the front lines of the ongoing pandemic is a testament to their resiliency and steadfast commitment to their mission to serve patients and communities around the country.

Hospitals and health systems are the cornerstones of their communities. Their patients depend on them for access to care 24 hours a day, seven days a week. Hospitals are often the largest employers in their community, and large purchasers of local services and goods. Additional support is needed to help ensure hospitals have the adequate resources to care for their communities.

I. Workforce and Contract Labor Expenses

The hospital workforce is central to the care process and often the largest expense for hospitals. It is no surprise then that even before the pandemic, labor costs — which include costs associated with recruiting and retaining employed staff, benefits and incentives — accounted for more than 50% of hospitals’ total expenses. Therefore, even a slight increase in these costs can have significant impacts on a hospital’s total expenses and operating margins.

As the pandemic has persisted for over two years, the toll on the health care workforce has been immense. A recent survey of health care workers found that approximately half of respondents felt “burned out” and nearly a quarter of respondents said they anticipated leaving the health care field.6

This has been mirrored by a significant and sustained decline in hospital employment, down approximately 100,000 employees from pre-pandemic levels.7 At the height of the omicron surge, approximately 1,400 hospitals or 30% of all U.S. hospitals reporting data to the government, indicated that they anticipated a critical staffing shortage within the week.8This high percentage of hospitals reporting a critical staffing shortage stayed relatively consistent throughout the delta and omicron surges.

The combination of employee burnout, fewer available staff, increased patient acuity and higher demand for care especially during the delta and omicron surges, has forced hospitals to turn to contract staffing firms to help address staffing shortages.

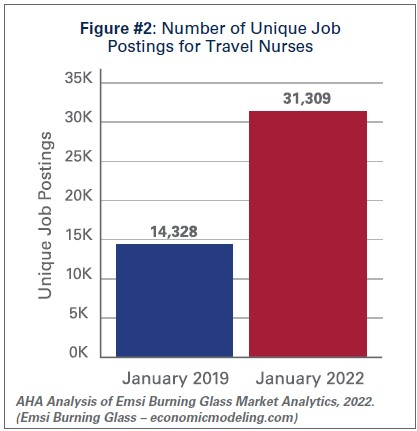

Though hospitals have long worked with contract staffing firms to bridge temporary gaps in staffing, the pandemic-driven-staffing-shortage has created an expanded reliance on contract staff, especially contract or travel registered nurses. Travel nurses are in particularly high demand because they serve a critical role in delivering care for both COVID-19 and non-COVID-19 patients and allow the hospital to meet the demand for care, especially during pandemic surges.

According to a survey by AMN Healthcare, one of the nation’s largest health care staffing agencies, 95% of health care facilities reported hiring nurse staff from contract labor firms during the pandemic.9Staffing firms have increased their recruitment of contract or travel nurses, illustrating the significant growth in their demand. According to data from EMSI/Burning Glass, there has been a nearly 120% increase in job postings for contract or travel nurses from pre-pandemic levels in January 2019 to January 2022. (See Figure #2)

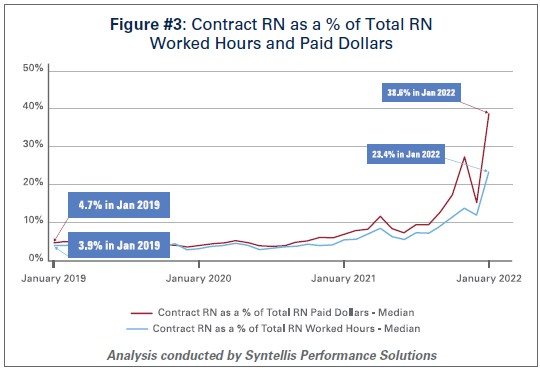

Similarly, the hours worked by contract or travel nurses as a percentage of total hours worked by nurses in hospitals has grown from 3.9% in January 2019 to 23.4% in January 2022, according to data from Syntellis Performance Solutions. (See Figure #3) In fact, a quarter of hospitals have experienced nearly a third of their total nurse hours accounted for by contract or travel nurses.

As the share of contract travel nurse hours has grown significantly compared to before the pandemic, so too have the costs of employing travel nurses compared to pre-pandemic levels. In 2019, hospitals spent a median of 4.7% of their total nurse labor expenses for contract travel nurses, which skyrocketed to a median of 38.6% in January 2022. (See Figure #3) A quarter of hospitals — those who have had to rely disproportionately on contract travel nurses — saw their costs for contract travel nurses account for over 50% of their total nurse labor expenses. In fact, while contract travel nurses accounted for 23.4% of total nurse hours in January 2022, they accounted for nearly 40% of the labor expenses for nurses. (See Figure #3) This difference has grown considerably compared to pre-pandemic levels in 2019, suggesting that the exorbitant prices charged by staffing companies are a primary driver of higher labor expenses for hospitals.

Data from Syntellis Performance Solutions show a 213% increase in hourly rates charged to hospitals by staffing companies for travel nurses in January 2022 compared to pre-pandemic levels in January 2019. This is because staffing agencies have exploited the situation by increasing the hourly rates billed to hospitals for contract travel nurses more than the hourly rates they pay to travel nurses. This is effectively the “margin” retained by the staffing agencies. During pre-pandemic levels in 2019, the average “margin” retained by staffing agencies for travel nurses was about 15%. As of January 2022, the average “margin” has grown to an astounding 62%. (See Figure #4)

These high “margins” have fueled massive growth in the revenues and profits of health care staffing companies. Several staffing firms have reported significant growth in their revenues to as high as $1.1 billion in just the fourth quarter of 202110, tripling their revenues and net income compared to 2020 levels.11

The data indicate that the growth in labor expenses for hospitals and health systems was in large part due to the exorbitant rates charged by contract staffing firms. By the end of 2021, hospital labor expenses per patient were 36.9% higher than pre-pandemic levels, and increased to 57% at the height of the omicron surge in January 2022.12 A study looking at hospitals in New Jersey found that the increased labor expenses for contract staff amounted to $670 million in 2021 alone, which was more than triple what their hospitals spent in 2020.13High reliance on contract or travel staff prevents hospitals and health systems from investing those costs into their existing employees, leading to low morale and high turnover, which further exacerbates the challenges hospitals and health systems have been facing.

II. Drug Expenses

Prescription drug spending in the U.S. has grown significantly since the pandemic. In 2021, drug spending (including spending in both retail and non-retail settings) increased 7.7%14, which was on top of an increase of 4.9%15 in 2020. While some of this growth can be attributed to increased utilization as patient acuity increased during the pandemic, a significant driver has been the continued increase in prices of existing drugs as well as the introduction of new products at very high prices. A study by GoodRx found that in January 2022 alone, drug companies increased the price of about 810 brand and generic drugs that they reviewed by an average of 5.1%.16 These price increases followed massive price hikes for certain drugs often used in the hospital such as Hydromorphone (107%), Mitomycin (99%), and Vasopressin (97%).17 For another example, the drug manufacturer of Humira, one of the most popular brand drugs used to treat rheumatoid arthritis, increased the price of the drug by 21% between 2019 and 2021.18 A study by the Kaiser Family Foundation found that in Medicare Part B and D markets, half of all drugs in each market experienced price increases above the rate of inflation between 2019 and 2020 – in fact, a third of these drugs experienced price increases of greater than 7.5%.19 At the same time, according to a report by the Institute for Clinical and Economic Review (ICER), eight drugs with unsupported U.S. drug price increases between 2019 and 2020 alone accounted for an additional $1.67 billion in drug spending, further illustrating that drug companies’ decisions to raise the prices of their drugs are simply an unsustainable practice.20

As hospitals have worked to treat sicker patients during the pandemic, they have been forced to contend with sky-high prices for drugs, many of which are critical and lifesaving for their patients. For example, in 2020, 16 of the top 25 drugs by spending in Medicare Part B (hospital outpatient settings) had price increases greater than inflation — two of the top three drugs, Keytruda and Prolia — experienced price increases of 3.3% and 4.1%, respectively.21

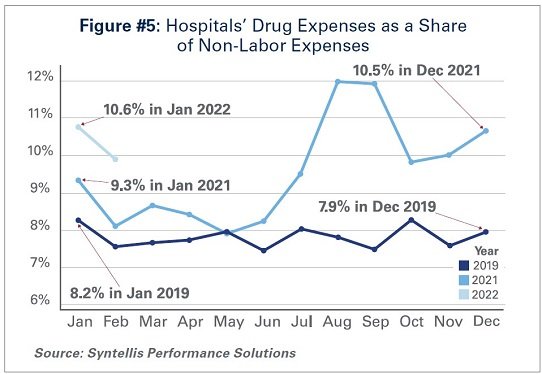

As a result of these price increases, hospital drug expenses have skyrocketed. By the end of 2021, total drug expenses were 28.2% higher than pre-pandemic levels.22 When taken as a share of all non-labor expenses, drug expenses have grown from approximately 8.2% in January 2019, to 9.3% in January 2021, and to 10.6% in January 2022. (See Figure #5) Even when considering changes in volume during the pandemic, drug expenses per patient compared to pre-pandemic levels in 2019 saw significant increases, with a 36.9% increase through 2021.

While continued drug price increases by drug companies have been a major driver of the growth in overall hospital drug expenses, there also are other important driving factors to consider:

Drug Treatments for COVID-19 Patients:Remdesivir, one of the primary drugs used to treat COVID-19 patients in the hospital, has become the top spend drug for most hospitals since the pandemic. This drug alone accounted for over $1 billion in sales in the fourth quarter of 2021.23 Priced at an average of $3,12024, Remdesivir’s cost was initially covered by the federal government. However, hospitals must now purchase the drug directly.

Limitation of 340B Contract Pharmacies: The 340B program allows eligible providers, including hospitals that treat many low-income patients or treat certain patient populations like children and cancer patients, to buy certain outpatient drugs at discounted prices and use those savings to provide more comprehensive services to the patients and communities they serve. Since July 2020, several of the largest drug manufacturers have denied 340B pricing to eligible hospitals through pharmacies with whom they contract, despite calls from the Department of Health and Human Services that such actions are illegal. Because of these actions, many 340B hospitals, especially rural hospitals who disproportionately rely on contract pharmacies to ensure access to drugs for their patients, have lost millions in 340B drug savings.25 In addition, these manufacturers have required claim-level data submissions as a condition of receiving 340B discounts, which has increased costs to deliver the data as well as staff time and expense to manage that process. The loss of 340B savings coupled with increased burden of providing detailed data to drug companies have contributed to increasing drug expenses.

Health Plans’/Pharmacy Benefit Managers’ (PBMs’) “White Bagging” Policies: Health plans and PBMs have engaged in a tactic that steers hospital patients to third-party specialty pharmacies to acquire medication necessary for clinician-administered treatments, known as “white-bagging.” This practice disallows the hospital from procuring and managing the handling of a drug — typically drugs that are infused or injected requiring a clinician to administer in a hospital or clinic setting — used in patient care. These policies not only create serious patient safety concerns, but create delays and risks in patient care; add to administration, storage and handling costs; and create important liability issues for hospitals.

Taken together, these factors increase both drug expenses and overall hospital expenses.

III. Medical Supply and PPE Expenses

The U.S., like most countries in the world, relies on global supply chains for goods and services. This is especially true for medical supplies used at hospitals and other health care settings. Everything from the masks and gloves worn by staff to medical devices used in patient care come from a large network of global suppliers. Prior to the global pandemic, hospitals had established relationships with distributors and other vendors in the global health care supply chain to deliver goods as necessitated by demand. After the pandemic hit, many factories, distributors and other vendors shut down their operations, leaving hospitals, which were on the front lines facing surging demand, to fend for themselves. In fact, supply chain disruptions across industries, including health care, increased by 67% in 2020 alone.26

As a result, hospitals turned to local suppliers and non-traditional suppliers, often paying significantly higher rates than they did prior to the pandemic. Between fall 2020 and early 2022 costs for energy, resins, cotton and most metals surged in excess of 30%; these all are critical elements in the manufacturing of medical supplies and devices used every day in hospitals.27 As COVID-19 cases surged, demand for hospital PPE, such as N95 masks, gloves, eye protection and surgical gowns, increased dramatically causing hospitals to invest in acquiring and maintaining reserves of these supplies. Further, downstream effects from other global events such as the war in Ukraine and the energy crisis in China, as well as domestic issues, such as labor shortages and rising fuel and transportation costs, have all contributed to drive up even higher overall medical supply expenses for hospitals in the U.S.28 For instance, according to the Health Industry Distributors Association, transportation times for medical supplies are 440% longer than pre-pandemic times resulting in massive delays.29

Compared to 2019 levels, supply expenses for hospitals were up 15.9%30 through the end of 2021. When focusing on hospital departments involved most directly in care for COVID-19 patients − primarily hospital intensive care units (ICUs) and respiratory care departments − the increase in expenses is significantly higher. Medical supply expenses in ICUs and respiratory care departments increased 31.5% and 22.3%, respectively. Further, accounting for changes in volume during surge and non-surge periods of the pandemic, medical supply expenses per patient in ICUs and respiratory care departments were 31.8% and 25.9% higher, respectively. (See Figure #6) These numbers help illustrate the magnitude of the impact that increases in supply costs have had on hospital finances during the pandemic.

IV. Impact of Rising Inflation

Higher economy-wide costs have serious implications for hospitals and health systems, increasing the pressures of higher labor, supply, and acquisition costs; and potentially lower consumer demand. Inflation is defined as the general increase in prices and the decrease in purchasing power. It is measured by the Consumer Price Index (CPI-U). In April 2021, the Bureau of Labor Statistics (BLS) reported that the CPI-U had the largest 12-month increase since September 2008. The CPI-U hit 40-year highs in February 2022.31 Overall, consumer prices rose by a historic 8.5% on an annualized basis in March 2022 alone.32

As inflation measured by consumer prices is at record highs, below are key considerations on the potential impact of higher general inflation on hospital prices:

Labor Costs and Retention: Labor costs represent a significant portion of hospital costs (typically more than 50% of hospital expenses are related to labor costs). As the cost-of-living increases, employees generally demand higher wages/total compensation packages to offset those costs. This is especially true in the health care sector, where labor demands are already high, and labor supply is low.

Supply Chain Costs: Medical supplies account for approximately 20% of hospital expenses, on average. As input/raw good costs increase due to general inflation, hospital supplies and medical device costs increase as well. Furthermore, shortages of raw materials, including those used to manufacture drugs, could stress supply chains (i.e., medical supply shortages), which may result in changes in care patterns and add further burden on staff to implement work arounds.

Capital Investment Costs: Capital investments also may be strained, especially as hospitals have already invested heavily in expanding capacity to treat patients during the pandemic (e.g., constructing spaces for testing and isolation of COVID-19 patients). One of the areas that has seen the largest increase in prices/shortages is building materials (e.g., lumber). Additionally, a historically large increase in inflation has resulted in increases in interest rates, which may hamper borrowing options and add to overall costs.

Consumer Demand: Higher inflation also may result in decreases in demand for health care services, specifically if inflation exceeds wage growth. Specifically, higher costs for necessities (food, transportation, etc.) could push down demand for health care services and, in turn, dampen hospital volumes and revenues in the long run.

Health care and hospital prices are not driving recent overall inflation increases. The BLS has cited increases in the indices for gasoline, shelter and food as the largest contributors to the seasonally adjusted all items increase. The CPI-U increased 0.8% in February on a seasonally adjusted basis, whereas the medical care index rose 0.2% in February. The index for prescription drugs rose 0.3%, but the hospital index for hospital services declined 0.1%.33

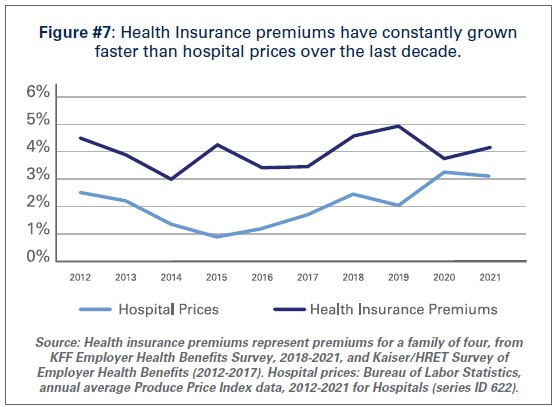

This is consistent with pre-pandemic trends. Despite persistent cost pressures, hospital prices have seen consistently modest growth in recent years. According to BLS data, hospital prices have grown an average 2.1% per year over the last decade, about half the average annual increase in health insurance premiums. (See Figure #7) More recently, hospital prices have grown much more slowly than the overall rate of inflation. In the 12 months ending in February 2022, hospital prices increased 2.1%. In fact, even when excluding the artificially low rates paid to hospitals by Medicare and Medicaid, average annual price growth has still been below 3% in recent years.34

Conclusion

While we hope that our nation is rounding the corner in the battle against COVID-19, it is clear that the pandemic is not over. During the week of April 11, there have been an average of over 33,000 cases per day35 and reports suggest that a new subvariant of the virus (Omicron BA.2) is now the dominant strain in the U.S.36As a result, the challenges hospitals and health systems are currently facing are bound to last much longer.

As COVID-19 infections and hospitalizations are decreasing in some parts of the U.S. and increasing in others, hospitals and health systems continue to care for COVID-19 and non-COVID-19 patients. With additional surges potentially on the horizon, the massive growth in expenses is unsustainable. Most of the nation’s hospitals were operating on razor thin margins prior to the pandemic; and now, many of these hospitals are in an even more precarious financial situation. Regardless of potential new surges of COVID-19, hospitals and health systems continue to face workforce retention and recruitment challenges, supply chain disruptions and exorbitant expenses as outlined in this report.

Hospitals appreciate the support and resources that Congress has provided throughout the pandemic; however, additional support is needed now to keep hospitals strong so they can continue to provide care to patients and communities.

Here are 16 hospitals and health health systems with strong operational metrics and solid financial positions, according to reports from Fitch Ratings, Moody’s Investors Service and S&P Global Ratings.

1. Morristown, N.J.-based Atlantic Health System has an “Aa3” rating and stable outlook with Moody’s. The health system has strong operating performance and liquidity metrics, Moody’s said. The credit rating agency expects Atlantic Health System to sustain strong performance to support capital spending.

2. Children’s Hospital of Akron (Ohio) has an “AA-” rating and stable outlook with Fitch. The hospital has strong operating performance and a leading market position as Akron’s only standalone pediatric hospital, Fitch said. The credit rating agency expects the organization’s strong profitability and limited capital needs to lead to liquidity growth.

3. Milwaukee-based Children’s Wisconsin has an “Aa3” rating and stable outlook with Moody’s. The health system has a leading statewide market share for children’s healthcare services, solid cash flow, strong revenue growth and a robust balance sheet, Moody’s said. The credit rating agency expects Children’s Wisconsin’s balance sheet and debt metrics to remain strong.

4. Greensboro, N.C.-based Cone Health has an “AA” rating and stable outlook with Fitch. The health system has a leading market share and a favorable payer mix, Fitch said. The health system’s broad operating platform and strategic capital investments should enable it to return to stronger operating results, the credit rating agency said.

5. El Camino Health has an “AA-” rating and stable outlook with Fitch. El Camino Health, which includes hospital campuses in Los Gatos, Calif., and Mountain View, Calif., has a solid market share in a competitive market and a stable payer mix, Fitch said. The credit rating agency said El Camino Health’s balance sheet provides moderate financial flexibility.

6. Falls Church, Va.-based Inova Health System has an “Aa2” rating and stable outlook with Moody’s. The health system has a consistently strong operating cash flow margin and ample balance sheet resources, Moody’s said. Inova’s financial excellence will remain undergirded by its favorable regulatory and economic environment, the credit rating agency said.

7. Mass General Brigham has an “Aa3” rating and stable outlook with Moody’s and an “AA-” rating and stable outlook with S&P. The Boston-based health system has an excellent clinical reputation, good financial performance and strong balance sheet metrics, Moody’s said. The credit rating agency said it expects Mass General Brigham to maintain a strong market position and stable financial performance.

8. Rochester, Minn.-based Mayo Clinic has an “Aa2” rating and stable outlook with Moody’s. The credit rating agency said Mayo Clinic’s strong market position and patient demand will drive favorable financial results. The health system “will continue to leverage its excellent reputation and patient demand to continue generating favorable operating performance while maintaining strong balance sheet ratios,” Moody’s said.

9. Memorial Sloan Kettering Cancer Center in New York City has an “AA” rating and stable outlook with Fitch and an “AA-” rating and stable outlook with S&P. Memorial Sloan Kettering Cancer Center’s national and international reputation as a premier cancer hospital will continue to support the organization’s growth, Fitch said. The hospital has a leading and growing market share for its specialty services, according to the credit rating agency.

10. Methodist Health System has an “Aa3” rating and stable outlook with Moody’s. The Dallas-based system has strong operating performance, and investments in facilities have allowed it to continue to capture more market share in the fast-growing Dallas-Fort Worth, Texas, area, Moody’s said. The credit rating agency said it expects Methodist Health System’s strong operating performance and favorable liquidity to continue.

11. Albuquerque, N.M.-based Presbyterian Healthcare Services has an “Aa3” rating and stable outlook with Moody’s and an “AA” rating and stable outlook with Fitch. The health system has a leading statewide market share, strong revenue growth and a healthy balance sheet, Moody’s said. The credit rating agency said it expects Presbyterian Healthcare Services’ operations to continue to improve and its balance sheet and debt metrics to remain strong.

12. Chicago-based Rush Health has an “AA-” rating and stable outlook with Fitch. The health system has a strong financial profile and a broad reach for high-acuity services as a leading academic medical center, Fitch said. The credit rating agency expects Rush’s services to remain profitable over time.

13. Stanford (Calif.) Health Care has an “AA” rating and stable outlook with Fitch. The health system has extensive clinical reach in a competitive market and its financial profile is improving, Fitch said. The health system’s EBITDA margins rebounded in fiscal year 2021 and are expected to remain strong going forward, the crediting rating agency said.

14. St. Clair Hospital in Pittsburgh has an “AA-” rating and stable outlook with Fitch. The hospital has a strong financial profile and a solid market position in the competitive greater Pittsburgh-area healthcare market, Fitch said. The credit rating agency expects the hospital’s margins to remain solid, driven by growth in key service lines.

15. University of Chicago Medical Center has an “AA-” rating and stable outlook with Fitch. The credit rating agency said it expects University of Chicago Medical Center’s capital-related ratios to remain strong, in part because of its broad reach of high-acuity services.

16. University of Iowa Hospitals and Clinics has an “Aa2” rating and stable outlook with Moody’s. The Iowa City-based health system, the only academic medical center in Iowa, has strong patient demand and excellent financial management, Moody’s said. The credit rating agency said it expects the health system to continue to manage the pandemic with improved operating cash flow margins.

Judging from our recent conversations with health system executives, we’d guess CEOs across the industry woke up this morning glad to see the first quarter in the rearview mirror.

Almost everyone we’ve spoken to has told us that the past three months have been miserable from an operating margin perspective—skyrocketing labor costs, rising drug and supply prices, and stubbornly long length of stay, particularly among Medicare patients.

In the words of one CFO, “I’ve never seen anything like this. For the first time, we budgeted for a negative margin, and still didn’t hit our target. I’m not sure how long our board will let us stay on this trajectory before things change.”

Yet few of the drivers of poor financial performance appear to be temporary. Perhaps the over-reliance on agency nursing staff will wane as COVID volumes bottom out (for how long remains unknown), but overall labor costs will remain high, there’s no immediate relief for supply chain issues, and COVID-related delays in care have left many patients sicker—and thus in need of more costly care. Plus, the lifeline of federal relief funds is rapidly dwindling, if not already gone.

Expect the next three quarters (and beyond) to bring a greater focus on cost cutting, especially as not-for-profit systems struggle to defend their bond ratings in the face of rising interest rates.

Due to financial struggles, West Reading, Pa.-based Tower Health is looking for other health systems to take over St. Christopher’s Hospital for Children, which it co-owns with Drexel University, rather than renew its $85 million line of credit to the hospital, The Philadelphia Inquirer reported April 8.

Tower Health’s credit line was set to expire March 31, but Drexel University renewed its line of credit to the Philadelphia hospital for the next four years.

Philadelphia-based St. Chris has been struggling financially, but has recently improved. Its projected loss was $23.6 million for the year ended June 30, compared to $97.6 million in fiscal year 2021, Drexel University President John Fry told the Inquirer.

“We will stand behind this hospital and we will find a solution. We just need more help than the help that Drexel and Tower can provide,” Mr. Fry told the paper.

The hospital was part of the American Academic Health System bankruptcy in 2019. It was previously owned by Dallas-based Tenet Healthcare.

Tower Health has also been dealing with financial problems, with operating losses of more than $900 million in the last four and a half fiscal years, according to the paper.

Temple University Health System confirmed to the Inquirer that it is in discussions to help support the hospital.