If a picture is worth a thousand words, a video, if done well, can be worth thousands more.

Regular readers of HEALTH CARE un-covered know we have published lots of words about the barriers health insurance companies have erected that make it harder and harder for patients to get the care their doctors know they need.

It’s a perfect example of how something that was designed to protect patients from inappropriate and unnecessary care has been weaponized by health insurers to pad their bottom lines.

Prior authorization in today’s world all too often serves as a bureaucratic barrier, requiring patients and their doctors to obtain approval in advance from insurers before certain treatments, medications, or procedures will be covered.

While insurance companies argue that prior authorization helps control costs and ensure appropriate care, the reality is far grimmer.

Both patients and their health care providers suffer the consequences. Patients frequently face delays in receiving necessary treatments or medications, exacerbating their health conditions and causing unnecessary stress and anxiety. Many forgo needed care altogether due to the complexities and frustrations of navigating the prior authorization process. This practice not only undermines patients’ trust in their health care providers but also compromises their health, often leading to worsened conditions and, tragically, sometimes irreversible harm.

The burden of prior authorization falls heavily on clinicians and their office staff who must spend valuable time and resources navigating the bureaucratic red tape imposed by insurers. This administrative burden not only detracts from patient care but also contributes to physician burnout, dissatisfaction and moral crisis, according to many doctors.

Ultimately, the health insurance industry’s prioritization of profit over patient well-being is evident in its insistence on maintaining these barriers to care, perpetuating a system that defaults to financial gain at the expense of human lives.

The New York Times video cuts to the chase. Prior authorization, as practiced today by insurance companies, is “medical injustice disguised as paperwork.”

If Congress in the next year or two succeeds in transforming Medicare into something that looks like a run-of-the mill Medicare Advantage plan for everyone – not just for those who now have the plans – it will mark the culmination of a 30-year project funded by the Heritage Foundation.

A conservative think tank, the Heritage Foundation grew to prominence in the 1970s and ’80s with a well-funded mission to remake or eliminate progressive governmental programs Americans had come to rely on, like Medicare, Social Security and Workers’ Compensation.

Some 30 million people already have been lured into private Medicare Advantage plans, eager to grab such sales enticements as groceries, gym memberships and a sprinkling of dental coverage while apparently oblivious to the restrictions on care they may encounter when they get seriously ill and need expensive treatment. That’s the time when you really need good insurance to pay the bills.

Congress may soon pass legislation that authorizes a study commission pushed by Heritage and some Republican members aimed at placing recommendations on the legislative table that would end Medicare and Social Security, replacing those programs with new ones offering lesser benefits for fewer people.

In other words, they would no longer be available to everyone in a particular group. Instead they would morph into something like welfare, where only the neediest could receive benefits.

How did these popular programs, now affecting 67.4 million Americans on Social Security and nearly 67 million on Medicare, become imperiled?

As I wrote in my book, Slanting the Story: The Forces That Shape the News, Heritage had embarked on a campaign to turn Medicare into a totally privatized arrangement. It’s instructive to look at the 30-year campaign by right-wing think tanks, particularly the Heritage Foundation, to turn these programs into something more akin to health insurance sold by profit-making companies like Aetna and UnitedHealthcare than social insurance, where everyone who pays into the system is entitled to a benefit when they become eligible.

The proverbial handwriting was on the wall as early as 1997 when a group of American and Japanese health journalists gathered at an apartment in Manhattan to hear a program about services for the elderly. The featured speaker was Dr. Robyn Stone who had just left her position as assistant secretary for the Department of Health and Human Services in the Clinton administration.

Stone chastised the American reporters in the audience, telling them: “What is amazing to me is that you have not picked up on probably the most significant story in aging since the 1960s, and that is passage of the Balanced Budget Act of 1997, which creates Medicare Plus Choice” – a forerunner of today’s Advantage plans.

“This is the beginning of the end of entitlements for the Medicare program,” Stone said, explaining that the changes signaled a move toward a “defined contribution” program rather than a “defined benefit” plan with a predetermined set of benefits for everyone. “The legislation was so gently passed that nobody looked at the details.”

Robert Rosenblatt, who covered the aging beat for the Los Angeles Times, immediately challenged her. “It’s not the beginning of the end of Medicare as we know it,” he shot back. “It expands consumer choice.”

Consumer choice had become the watchword of the so-called “consumer movement,” ostensibly empowering shoppers – but without always identifying the conditions under which their choices must be made.

When consumers lured by TV pitchmen sign up for Medicare Advantage, how many of the sellers disclose that once those consumers leave traditional Medicare for an Advantage plan, they may be trapped. In most states, they will not be able to buy a Medicare supplement policy if they don’t like their new plan unless they are in super-good health.

In other words, most seniors are stuck. That can leave beneficiaries medically stranded when they have a serious, costly illness at a time in life when many are using up or have already exhausted their resources. I once asked a Medicare counselor what beneficiaries with little income would do if they became seriously ill and their Advantage plan refused to pay many of the bills, an increasingly common predicament. The cavalier answer I got was: “They could just go on Medicaid.”

The push to privatize Medicare began in February 1995 when Heritage issued a six-page committee brief titled “A Special Report to the House Ways and Means Committee”, which was sent to members of Congress, editorial writers, columnists, talk show hosts and other media. Heritage then spent months promoting its slant on the story. Along with other right-wing groups dedicated to transforming Medicare from social insurance to a private arrangement like car insurance, Heritage clobbered reporters who produced stories that didn’t fit the conservative narrative.

The right-wing Media Research Center singled out journalists who didn’t use the prescribed vocabulary to describe Heritage plans. Its newsletter criticized CBS reporter Linda Douglas when she reported that the senior citizens lobby had warned that the Republican budget would gut Medicare. The group reprimanded another CBS reporter, Connie Chung, for reporting that the House and Senate GOP plans “call for deep cuts in Medicare and other programs.” Haley Barbour, then Republican National Committee chairman, vowed to raise “unshirted hell” with the news media whenever they used the word “cut.” He wined and dined reporters, “educating” them on the “difference” between cuts and slowing Medicare’s growth. Former Republican U.S. Rep. John Kasich of Ohio, who chaired the House budget committee, called reporters warning them not to use the word “cut,” later admitting he “worked them over.”

As I wrote at the time, by fall of that year reporters had fallen in line. Douglas, who had been criticized all summer, got the words right and reported that the Republican bill contained a number of provisions “all adding up to a savings of $270 billion in the growth of Medicare spending.”

Fast forward to now. The Heritage Foundation’s Budget Blueprint for fiscal year 2023 offered ominous recommendations for Medicare, some of which might be enacted in a Republican administration. The think tank yet again called for a “premium support system” for Medicare, claiming that if its implementation was assumed in 2025, it “would reduce outlays by $1 trillion during the FY 2023-2032 period.” Heritage argues that the controversial approach would foster “intense competition among health plans and providers,” “expand beneficiaries’ choices,” “control costs,” “slow the growth of Medicare spending,” and “stimulate innovation.”

The potential beneficiaries would be given a sum of money, often called a premium support, to shop in the new marketplace, which could resemble today’s sales bazaar for Medicare Advantage plans, setting up the possibility for more hype and more sellers hoping to cash in on the revamped Medicare program. Many experts fear that such a program ultimately could destroy what is left of traditional Medicare, which about half of the Medicare population still prefers.

In other words, most seniors are stuck.

That can leave beneficiaries medically stranded when they have a serious, costly illness at a time in life when many are using up or have already exhausted their resources. I once asked a Medicare counselor what beneficiaries with little income would do if they became seriously ill and their Advantage plan refused to pay many of the bills, an increasingly common predicament. The cavalier answer I got was: “They could just go on Medicaid.”

The push to privatize Medicare began in February 1995 when Heritage issued a six-page committee brief titled “A Special Report to the House Ways and Means Committee”, which was sent to members of Congress, editorial writers, columnists, talk show hosts and other media. Heritage then spent months promoting its slant on the story. Along with other right-wing groups dedicated to transforming Medicare from social insurance to a private arrangement like car insurance, Heritage clobbered reporters who produced stories that didn’t fit the conservative narrative.

The right-wing Media Research Center singled out journalists who didn’t use the prescribed vocabulary to describe Heritage plans. Its newsletter criticized CBS reporter Linda Douglas when she reported that the senior citizens lobby had warned that the Republican budget would gut Medicare. The group reprimanded another CBS reporter, Connie Chung, for reporting that the House and Senate GOP plans “call for deep cuts in Medicare and other programs.” Haley Barbour, then Republican National Committee chairman, vowed to raise “unshirted hell” with the news media whenever they used the word “cut.” He wined and dined reporters, “educating” them on the “difference” between cuts and slowing Medicare’s growth. Former Republican U.S. Rep. John Kasich of Ohio, who chaired the House budget committee, called reporters warning them not to use the word “cut,” later admitting he “worked them over.”

As I wrote at the time, by fall of that year reporters had fallen in line. Douglas, who had been criticized all summer, got the words right and reported that the Republican bill contained a number of provisions “all adding up to a savings of $270 billion in the growth of Medicare spending.”

Fast forward to now. The Heritage Foundation’s Budget Blueprint for fiscal year 2023 offered ominous recommendations for Medicare, some of which might be enacted in a Republican administration. The think tank yet again called for a “premium support system” for Medicare, claiming that if its implementation was assumed in 2025, it “would reduce outlays by $1 trillion during the FY 2023-2032 period.” Heritage argues that the controversial approach would foster “intense competition among health plans and providers,” “expand beneficiaries’ choices,” “control costs,” “slow the growth of Medicare spending,” and “stimulate innovation.”

The potential beneficiaries would be given a sum of money, often called a premium support, to shop in the new marketplace, which could resemble today’s sales bazaar for Medicare Advantage plans, setting up the possibility for more hype and more sellers hoping to cash in on the revamped Medicare program. Many experts fear that such a program ultimately could destroy what is left of traditional Medicare, which about half of the Medicare population still prefers.

In a Republican administration with a GOP Congress, some of the recommendations, or parts of them, might well become law. The last 30 years have shown that the Heritage Foundation and other organizations driven by ideological or financial reasons want to transform Medicare, and they are committed for the long haul. They have the resources to promote their cause year after year, resulting in the continual erosion of traditional Medicare by Advantage Plans, many of which are of questionable value when serious illness strikes.

The seeds of Medicare’s destruction are in the air.

The program as it was set out in 1965 has kept millions of older Americans out of medical poverty for over 50 years, but it may well become something else – a privatized health care system for the oldest citizens whose medical care will depend on the profit goals of a handful of private insurers. It’s a future that STAT’s Bob Herman, whose reporting has explored the inevitable clash between health care and an insurer’s profit goals, has shown us.

In the long term, the gym memberships, the groceries, the bit of dental and vision care so alluring today may well disappear, and millions of seniors will be left once again to the vagaries of America’s private insurance marketplace.

Wall Street has fallen out of love with big insurers that depend heavily on the federal government’s overpayments to the private Medicare replacement plans they market, deceptively, under the name, “Medicare Advantage.”

I’ll explain below. But first, thank you if you reached out to your members of Congress and the Biden administration last week as I suggested to demand an end to the ongoing looting by those companies of the Medicare Trust Fund.

As I wrote on March 26, the Center for Medicare and Medicaid Services was scheduled to announce this week how much more taxpayer dollars it would send to Medicare Advantage companies next year. On January 31, CMS said it planned to increase the amount slightly to account for the increased cost of health care, based on how much more the government likely would spend to cover people enrolled in the traditional Medicare program. It uses traditional Medicare as a benchmark.

Big insurers like UnitedHealthcare, Humana and Aetna, owned by CVS, howled when CMS released its preliminary 2025 rate notice that day. They claimed they wouldn’t be getting enough of taxpayers’ dollars. So they launched a high-pressure campaign to get CMS to give them more money. They demanded extra billions because, they said, their Medicare Advantage enrollees had used more prescription drugs and went to the doctor more often in 2023 and January of this year than the companies had expected.

CMS announced after the market closed Monday that it was sticking to its plan to increase payments to Medicare Advantage plans by 3.7% – more than $16 billion –from 2024 to 2025. That would mean that it would pay companies that operate MA plans between $500 and $600 billion next year, considerably less than insurers wanted.

Shocked investors began running for the exits right away. When the New York Stock Exchange closed at 4 p.m. ET on Tuesday, more than 52 million shares of the companies’ stock had been traded–many millions more than average–driving the share prices of all of them way down. And the carnage has continued throughout this week.

By the end of trading yesterday, UnitedHealth, Humana and CVS/Aetna had lost nearly $95 billion in market capitalization. To put that in perspective, that’s more than the entire market cap of CVS, which fell to $93 billion yesterday.

All seven of the big for-profit companies with Medicare Advantage enrollment had a bad week, although Cigna, where I used to work and which announced recently it is getting out of the Medicare Advantage business next year, suffered the least. Its shares were down a little more than 1% as of yesterday afternoon.

Humana, the second largest MA company, which last year said it was getting out of the commercial insurance business to focus more fully on Medicare Advantage, by contrast, was the biggest loser of the bunch–and one of the biggest losers on the NYSE. Its shares fell more than 13% on Tuesday. As of yesterday, they were still down nearly 12%.

Noting that Humana’s stock has fallen 40% this year, he wrote:

Last fall, the insurer Humana was on top of the world. The stock was trading above $520 per share, as the company’s major bet on Medicare Advantage—the privately-run, publicly-funded insurance program for U.S. seniors—seemed to be paying off.

Long a darling of Wall Street’s analyst class, the stock had returned nearly 290% since the start of 2015, handily outperforming the S&P 500 over the same period.

Over the past five months, that position has crumbled. Humana shares were down to $308 Tuesday morning, as the outlook for Medicare Advantage and, by extension, for Humana’s business, has grown dimmer and dimmer.

Humana shares dived 12.3% early Tuesday, after the latest blow to the future prospects for the profitability of the Medicare Advantage business. Late Monday, the Centers for Medicare and Medicaid Services announced Medicare Advantage payment rates for 2025 that fell short of investor expectations.

The other companies also had a disastrous week. Shares of UnitedHealth, the biggest of the group in terms of Medicare Advantage enrollment (and overall revenues and profits), had fallen by 7% by the end of the day yesterday. CVS/Aetna’s shares were down 7.1%; Elevance’s were down 3.37%; Molina’s were down 7.15%; and Centene’s were down 7.33%.

When I was at Cigna, one of my responsibilities was to handle media questions when the company announced quarterly earnings, mergers and acquisitions, and whenever there was a major event like the CMS rate notice. The worst days of my 20-year career in the industry were when some kind of news triggered a stock selloff. I had to try to put the best spin possible on the situation. But my job was relatively easy compared to what the CEO, CFO and the company’s investor relations team had to do.

You can be certain they have been on the phone and in Zooms all week with Wall Street financial analysts, big institutional investors and even the company’s big employer customers in attempts to persuade them that the sky has not fallen.

You can also be certain that the companies will now shift their focus to the political arena. To keep this from happening again, they will begin pouring enormous sums of your premium dollars into campaigns to help elect industry-friendly candidates for Congress and the presidency this November. We provided a glimpse of where they’re already sending those donations in a story last November. We will continue to monitor this in the months ahead.

Of late, private equity investors in healthcare services have faced intense criticism that their business practices have compromised patient safety and raised costs for consumers. March 5, the FTC, DOJ and HHS announced the launch of an investigation into the inner workings of PE in healthcare. It comes on the heels of U.S. Senate investigations in their Finance, HELP and Budget Committees to explore legislative levers they might pull to address their growing concerns about affordability, competition and accountability in the industry.

PE funds don’t welcome the spotlight.

Their business model lends to misinformation and disinformation: company takeovers by new owners are rarely treated as good news unless the circumstance under prior ownership was dire. Even then, attention shifts quickly to the fairness of the PE business model playbook: acquire the asset on favorable terms, replace management, reduce operating costs, grow and the sell in 5-7 years at a profit using debt to finance the deal along the way. In exchange, the PE fund’s General Partner gets an annual management fee of 2% plus 20% of the value they create when they sell the company or take it public, and favorable tax treatment (carried interest) on their gain.

Concern about PE in healthcare services comes at a particularly delicate time: hospitals. nursing homes, outpatient care, medical practices, clinics et al) are still feeling the after-effects of the pandemic, proposed reimbursement bumps by Medicare for hospitals and physicians do not offset medical inflation and the Change Healthcare cybersecurity breach February 21 has created cash flow issues for all.

Concern about PE ownership was high already.

Innovations funded through PE-backed organizations have been drowned out by the steady drip of peer reviewed and industry-sponsored studies a causal relationship between PE ownership decreased quality and patient safety and increased prices and worker discontent. Nonetheless, PE-owns 4% of hospitals (among 36% that are investor-owned, 13% of medical practices and 6% of nursing homes today and they’re increasing in all cohorts of health services.

Here are the facts:

Private equity enjoys significant influence in public policy including healthcare. Direct lobbying activity by PE funds in Congress and state legislatures is well-funded and effective, especially by the It is increasingly 20 global fund sponsors that control 46% of assets under management. Cash on hand and fund-raising by PE are strong and healthcare remains an important but non-exclusive target of PE investing.

2023 was a down year for PE, 2024 will be strong: the IPO market and sponsor- to sponsor transactions dipped, and deal values shrank. Even with interest rates remaining high, returns exceeded overall growth in the stock market for deals consummated. At the same time, PE raised $1.2 trillion last year and has $2.6 trillion of dry powder to invest. Healthcare services will be a target as PE deal activity increases in 2024.

In U.S. healthcare, PE investments are significant and increasing. Technology-enabled services that lower unit costs and AI-based solutions that enable standardization and workforce efficiency will garner higher valuations and greater PE interest than traditional services. Valuations will recover from record 2023 lows and dry powder will be deployed for roll-ups despite antitrust concerns and government investigations. Congress will investigate the impact on PE on patient safety, prices and competition and, in tandem with FTC and DOJ issue guidance: compliance will be mandated and financial penalties added. But displacement of PE in health services is unlikely.

Some notable data:

Private equity funds have $2.49 trillion of cash on hand to invest—up 7% from 2022. They raised $1.2 trillion globally in 2023. 26% of its global dry powder is more than 4 years old—undeployed.

Private equity groups globally are sitting on a record 28,000 unsold companies worth more than $3tn. 40% of the companies waiting to be sold are at least four years old. Last year, the combined value of companies that the industry sold privately or on public markets fell 44% and the value of companies sold to other buyout groups fell 47%.

Private equity investments in almost every sector in healthcare are significant, and until lately, increasing. Last year, deals were down 16.2% (from 940 to 788) cutting across every sector. In some sectors, like physician services, PE deals were tuck-in’s to their previous platform investments increasing from 75 deals in 2012 to 484 deals in 2021.

PE investments in US healthcare exceeded $1 trillion in the last 10 years. Investments in healthcare services i.e. acute, long-term, ambulatory and physician services– have been less profitable to investors than PE investments in technology, devices and therapeutics (based on the ratio of Enterprise Value to EBITDA) but exceed equity-market returns overall.

Peer reviewed studies have shown causal relationships between private equity ownership of hospitals, nursing homes and medical practices with lower operating costs, higher staff turnover, high prices and higher profits.

My take:

Like it or not, private equity investment in healthcare is here to stay. The likelihood of higher taxes paid by employers and individuals to fund the health system is nil. The majority (69%) of the public think it wasteful and inefficient (See Polling below). The majority believe it puts its profits above all else. The majority think it needs major change. That’s not new, but it’s felt more intensely and more widely than ever.

That means accommodation for private capital, including private equity, is not a major concern to voters: the prices they pay matters more than who owns the organization.

Tighter regulation of private equity, including more rights given to the Limited Partners who invest in the PE funds and limitations on public officials who become fund advisors, are likely. Bad actors will be vilified by regulators and elected officials. Media scrutiny of specific PE funds and their GPs will intensify as PE public reporting regulations commence. And investments made by not-for-profit multi-hospital systems and independent hospitals will be critical elements in upcoming Congressional and regulatory policy setting about their community benefit accountability and tax exemptions.

The public’s major concern about its healthcare industry is affordability. To the extent PE-backed solutions offer lower-cost, higher-value alternatives on a playing field that’s level with respect to equitable access and demand-management, they will be at the table.

To the extent PE-backed solutions cherry-pick the system’s low-hanging fruit at the expense of patient safety and affordability sans any regulatory restriction, they’ll breed public discontent from those they choose to ignore.

So, the reality is this: PE’s focus is generating profits for its GP and their LPs. Doing business in a socially responsible way is a fund’s prerogative. Some do it better than others.

PE is part of healthcare’s solution to its poorly structured, perpetually inadequate and mal-distributed funding. But creating a level playing field through meaningful regulatory reform is necessary first.

PS Among the stickier issues facing hospitals is site-neutral payments. Hospitals oppose the proposal reasoning the overhead structure for their outpatient services (HOPD) include indirect & direct costs for services provided those unable to pay i.e. emergency services. Proponents of the change argue that what’s done is the key, not where it’s done, and uniform pricing is common sense. Leavitt Partners has advanced a compromise: a Unified Ambulatory Payment System for HOPDs, ASCs and physician clinics that would be applied to 66 services starting

Tuesday, the, FTC, and DOJ announced creation of a task force focused on tackling “unfair and illegal pricing” in healthcare. The same day, HHS joined FTC and DOJ regulators in launching an investigation with the DOJ and FTC probing private equity’ investments in healthcare expressing concern these deals may generate profits for corporate investors at the expense of patients’ health, workers’ safety and affordable care.

Thursday’s State of the Union address by President Biden (SOTU) and the Republican response by Alabama Senator Katey Britt put the spotlight on women’s reproductive health, drug prices and healthcare affordability.

Friday, the Senate passed a $468 billion spending bill (75-22) that had passed in the House Wednesday (339-85) averting a government shutdown. The bill postpones an $8 billion reduction in Medicaid disproportionate share hospital payments for a year, allocates $4.27 billion to federally qualified health centers through the end of the year and rolls back a significant portion of a Medicare physician pay cut that kicked in on Jan. 1. Next, Congress must pass appropriations for HHS and other agencies before the March 22 shutdown.

And all week, the cyberattack on Optum’s Change Healthcare discovered February 21 hovered as hospitals, clinics, pharmacies and others scrambled to manage gaps in transaction processing. Notably, the American Hospital Association and others have amplified criticism of UnitedHealth Group’s handling of the disruption, having, bought Change for $13 billion in October, 2022 after a lengthy Department of Justice anti-trust review. This week, UHG indicates partial service of CH support will be restored. Stay tuned.

Just another week for healthcare: Congressional infighting about healthcare spending. Regulator announcements of new rules to stimulate competition and protect consumers in the healthcare market. Lobbying by leading trade groups to protect funding and disable threats from rivals. And so on.

At the macro level, it’s understandable: healthcare is an attractive market, especially in its services sectors. Since the pandemic, prices for services (i.e. physicians, hospitals et al) have steadily increased and remain elevated despite the pressures of transparency mandates and insurer pushback. By contrast, prices for most products (drugs, disposables, technologies et al) have followed the broader market pricing trends where prices for some escalated fast and then dipped.

While some branded prescription medicines are exceptions, it is health services that have driven the majority of health cost inflation since the pandemic.

UnitedHealth Group’s financial success is illustrative:

it’s big, high profile and vertically integrated across all major services sectors. In its year end 2023 financial report (January 12, 2024) it reported revenues of $371.6 Billion (up 15% Year-Over-Year), earnings from operations up 14%, cash flows from operations of $29.1 Billion (1.3x Net Income), medical care ratio at 83.2% up from 82% last year, net earnings of $23.86/share and adjusted net earnings of $25.12/share and guidance its 2024 revenues of $400-403 billion. They buy products using their scale and scope leverage to pay less for services they don’t own less and products needed to support them. It’s a big business in a buyer’s market and that’s unsettling to many.

Big business is not new to healthcare:

it’s been dominant in every sector but of late more a focus of unflattering regulator and media attention. Coupled with growing public discontent about the system’s effectiveness and affordability, it seems it’s near a tipping point.

David Johnson, one of the most thoughtful analysts of the health industry, reminded his readers last week that the current state of affairs in U.S. healthcare is not new citing the January 1970 Fortune cover story “Our Ailing Medical System”

“American medicine, the pride of the nation for many years, stands now on the brink of chaos. To be sure, our medical practitioners have their great moments of drama and triumph. But much of U.S. medical care, particularly the everyday business of preventing and treating routine illnesses, is inferior in quality, wastefully dispensed, and inequitably financed…

Whether poor or not, most Americans are badly served by the obsolete, overstrained medical system that has grown up around them helter-skelter. … The time has come for radical change.”

Johnson added: “The healthcare industry, however, cannot fight gravity forever. Consumerism, technological advances and pro-market regulatory reforms are so powerful and coming so fast that status-quo healthcare cannot forestall their ascendance. Properly harnessed, these disruptive forces have the collective power necessary for U.S. healthcare to finally achieve the 1970 Fortune magazine goal of delivering “good care to every American with little increase in cost.”

He’s right.

I believe the U.S. health system as we know it has reached its tipping point. The big-name organizations in every sector see it and have nominal contingency plans in place; the smaller players are buying time until the shoe drops. But I am worried.

I am worried the system’s future is in the hands of hyper-partisanship by both parties seeking political advantage in election cycles over meaningful creation of a health system that functions for the greater good.

I am worried that the industry’s aversion toprice transparency, meaningful discussion about affordability and consistency in defining quality, safety and value will precipitate short-term gamesmanship for reputational advantage and nullify systemness and interoperability requisite to its transformation.

I am worried that understandably frustrated employers will drop employee health benefits to force the system to needed accountability.

I am worried that the growing armies of under-served and dissatisfied populations will revolt.

I am worried that its workforce is ill-prepared for a future that’s technology-enabled and consumer centric.

I am worried that the industry’s most prominent trade groups are concentrating more on “warfare” against their rivals and less about the long-term future of the system.

I am worried that transformational change is all talk.

It’s time to start an adult conversation about the future of the system. The starting point: acknowledging that it’s not about bad people; it’s about systemic flaws in its design and functioning. Fixing it requires balancing lag indicators about its use, costs and demand with assumptions about innovations that hold promise to shift its trajectory long-term. It requires employers to actively participate: in 2009-2010, Big Business mistakenly chose to sit out deliberations about the Affordable Care Act. And it requires independent, visionary facilitation free from bias and input beyond the DC talking heads that have dominated reform thought leadership for 6 decades.

Or, collectively, we can watch events like last week’s roll by and witness the emergence of a large public utility serving most and a smaller private option for those that afford it. Or something worse.

P.S. Today, thousands will make the pilgrimage to Orlando for HIMSS24 kicking off with a keynote by Robert Garrett, CEO of Hackensack Meridian Health tomorrow about ‘transformational change’ and closing Friday with a keynote by Nick Saban, legendary Alabama football coach on leadership. In between, the meeting’s 24 premier supporters and hundreds of exhibitors will push their latest solutions to prospects and customers keenly aware healthcare’s future is not a repeat of its past primarily due to technology. Information-driven healthcare is dependent on technologies that enable cost-effective, customized evidence-based care that’s readily accessible to individuals where and when they want it and with whom.

And many will be anticipating HCA Mission Health’s (Asheville NC) Plan of Action response due to CMS this Wednesday addressing deficiencies in 6 areas including CMS Deficiency 482.12 “which ensures that hospitals have a responsible governing body overseeing critical aspects of patient care and medical staff appointments.” Interest is high outside the region as the nation’s largest investor-owned system was put in “immediate jeopardy” of losing its Medicare participation status last year at Mission. FYI: HCA reported operating income of $7.7 billion (11.8% operating margin) on revenues of $65 billion in 2023.

Last week, Congress avoided a partial federal shutdown by passing a stop-gap spending bill and now faces March 8 and March 22 deadlines for authorizations including key healthcare programs.

This week, lawmakers’ political antenna will be directed at Super Tuesday GOP Presidential Primary results which prognosticators predict sets the stage for the Biden-Trump re-match in November. And President Biden will deliver his 3rd State of the Union Address Thursday in which he is certain to tout the economy’s post-pandemic strength and recovery.

The common denominator of these activities in Congress is their short-term focus: a longer-term view about the direction of the country, its priorities and its funding is not on its radar anytime soon.

The healthcare system, which is nation’s biggest employer and 17.3% of its GDP, suffers from neglect as a result of chronic near-sightedness by its elected officials. A retrospective about its funding should prompt Congress to prepare otherwise.

U.S. Healthcare Spending 2000-2022

Year-over-year changes in U.S. healthcare spending reflect shifting demand for services and their underlying costs, changes in the healthiness of the population and the regulatory framework in which the U.S. health system operates to receive payments. Fluctuations are apparent year-to-year, but a multiyear retrospective on health spending is necessary to a longer-term view of its future.

The period from 2000 to 2022 (the last year for which U.S. spending data is available) spans two economic downturns (2008–2010 and 2020–2021); four presidencies; shifts in the composition of Congress, the Supreme Court, state legislatures and governors’ offices; and the passage of two major healthcare laws (the Medicare Modernization Act of 2003 and the Affordable Care Act of 2010).

During this span of time, there were notable changes in healthcare spending:

In 2000, national health expenditures were $1.4 trillion (13.3% of gross domestic product); in 2022, they were $4.5 trillion (17.3% of the GDP)—a 4.1% increase overall, a 321% increase in nominal spending and a 30% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 333 million, per capita healthcare spending increased 178% from $4,845 to $13,493 due primarily to inflation-impacted higher unit costs for , facilities, technologies and specialty provider costs and increased utilization by consumers due to escalating chronic diseases.

There were notable changes where dollars were spent: Hospitals remained relatively unchanged (from $415 billion/30.4% of total spending to $1.355 trillion/31.4%), physician services shrank (from $288.2 billion/21.1% to $884.8/19.6%) and prescription drugs were unchanged (from $122.3 billion/8.95% to $405.9 billion/9.0%).

And significant changes in funding Out-of-pocket shrank from 14.2% ($193.6 billion in 2020) to (10.5% ($471 billion) in 2020, private insurance shrank from $441 billion/32.3% to $1.289 trillion/29%, Medicare spending grew from $224.8 billion/16.5% to $944.3billion/21%; Medicaid and the Children’s Health Insurance Program spending grew from $203.4 billion/14.9% to $7805.7billion/18%; and Department of Veterans Affairs healthcare spending grew from $19.1 billion/1.4% to $98 billion/2.2%.

Looking ahead (2022-2031), CMS forecasts average National Health Expenditures (NHE) will grow at 5.4% per year outpacing average GDP growth (4.6%) and resulting in an increase in the health spending share of Gross Domestic Product (GDP) from 17.3% in 2021 to 19.6% in 2031.

The agency’s actuaries assume

“The insured share of the population is projected to reach a historic high of 92.3% in 2022… Medicaid enrollment will decline from its 2022 peak of 90.4M to 81.1M by 2025 as states disenroll beneficiaries no longer eligible for coverage. By 2031, the insured share of the population is projected to be 90.5 percent. The Inflation Reduction Act (IRA) is projected to result in lower out-of-pocket spending on prescription drugs for 2024 and beyond as Medicare beneficiaries incur savings associated with several provisions from the legislation including the $2,000 annual out-of-pocket spending cap and lower gross prices resulting from negotiations with manufacturers.”

My take:

The reality is this: no one knows for sure what the U.S. health economy will be in 2025 much less 2035 and beyond. There are too many moving parts, too much invested capital seeking near-term profits, too many compensation packages tied to near-term profits, too many unknowns like the impact of artificial intelligence and court decisions about consolidation and too much political risk for state and federal politicians to change anything.

One trend stands out in the data from 2000-2022: The healthcare economy is increasingly dependent on indirect funding by taxpayers and less dependent on direct payments by users.

In the last 22 years, local, state and federal government programs like Medicare, Medicaid and others have become the major sources of funding to the system while direct payments by consumers and employers, vis-à-vis premium out-of-pocket costs, increased nominally but not at the same rate as government programs. And total spending has increased more than the overall economy (GDP), household wages and costs of living almost every year.

Thus, given the trends, five questions must be addressed in the context of the system’s long-term solvency and effectiveness looking to 2031 and beyond:

Should its total spending and public funding be capped?

Should the allocation of funds be better adapted to innovations in technology and clinical evidence?

Should the financing and delivery of health services be integrated to enhance the effectiveness and efficiency of the system?

Should its structure be a dual public-private system akin to public-private designations in education?

Should consumers play a more direct role in its oversight and funding?

Answers will not be forthcoming in Campaign 2024 despite the growing significance of healthcare in the minds of voters. But they require attention now despite political neglect.

PS: The month of February might be remembered as the month two stalwarts in the industry faced troubles:

United HealthGroup, the biggest health insurer, saw fallout from a cyberattack against its recently acquired (2/22) insurance transaction processor by ALPHV/Blackcat, creating havoc for the 6000 hospitals, 1 million physicians, and 39,000 pharmacies seeking payments and/or authorizations. Then, news circulated about the DOJ’s investigation about its anti-competitive behavior with respect to the 90,000 physicians it employs. Its stock price ended the week at 489.53, down from 507.14 February 1.

And HCA, the biggest hospital operator, faced continued fallout from lawsuits for its handling of Mission Health (Asheville) where last Tuesday, a North Carolina federal court refused to dismiss a lawsuit accusing it of scheming to restrict competition and artificially drive-up costs for health plans. closed at 311.59 last week, down from 314.66 February 1.

With the South Carolina Republican primary results in over the weekend, it seems a Biden-Trump re-match is inevitable. Given the legacies associated with Presidencies of the two and the healthcare platforms espoused by their political parties, the landscape for healthcare politics seems clear:

Healthcare Issue

Biden Policy

Trump Policy

Access to Abortion

‘It’s a basic right for women protected by the Federal Government’

‘It’s up to the states and should be safe and rare. A 16-week ban should be the national standard.’

Ageism

‘President Biden is alert and capable. It’s a non-issue.’

‘President Biden is senile and unlikely to finish a second term is elected. President Trump is active and prepared.’

Access to IVF Treatments

‘It’s a basic right and should be universally accessible in every state and protected’

‘It’s a complex issue that should be considered in every state.’

Affordability

‘The system is unaffordable because it’s dominated by profit-focused corporations. It needs increased regulation including price controls.’

‘The system is unaffordable to some because it’s overly regulated and lacks competition and price transparency.’

Access to Health Insurance Coverage

‘It’s necessary for access to needed services & should be universally accessible and affordable.’

‘It’s a personal choice. Government should play a limited role.’

Public health

‘Underfunded and increasingly important.’

‘Fragmented and suboptimal. States should take the lead.’

Drug prices

‘Drug companies take advantage of the system to keep prices high. Price controls are necessary to lower costs.’

‘Drug prices are too high. Allowing importation and increased price transparency are keys to reducing costs.’

Medicare

‘It’s foundational to seniors’ wellbeing & should be protected. But demand is growing requiring modernization (aka the value agenda) and additional revenues (taxes + appropriations).’

‘It’s foundational to senior health & in need of modernization thru privatization. Waste and fraud are problematic to its future.’

Medicaid

‘Medicaid Managed Care is its future with increased enrollment and standardization of eligibility & benefits across states.’

‘Medicaid is a state program allowing modernization & innovation. The federal role should be subordinate to the states.’

Competition

‘The federal government (FTC, DOJ) should enhance protections against vertical and horizontal consolidation that reduce choices and increase prices in every sector of healthcare.’

‘Current anti-trust and consumer protections are adequate to address consolidation in healthcare.’

Price Transparency

‘Necessary and essential to protect consumers. Needs expansion.’

‘Necessary to drive competition in markets. Needs more attention.’

The Affordable Care Act

‘A necessary foundation for health system modernization that appropriately balances public and private responsibilities. Fix and Repair’

‘An unnecessary government takeover of the health system that’s harmful and wasteful. Repeal and Replace.’

Role of federal government

‘The federal government should enable equitable access and affordability. The private sector is focused more on profit than the public good.’

‘Market forces will drive better value. States should play a bigger role’

My take:

Polls indicate Campaign 2024 will be decided based on economic conditions in the fall 2024 as voters zero in on their choice. Per KFF’s latest poll, 74% of adults say an unexpected healthcare bill is their number-one financial concern—above their fears about food, energy and housing. So, if you’re handicapping healthcare in Campaign 2024, bet on its emergence as an economic issue, especially in the swing states (Michigan, Florida, North Carolina, Georgia and Arizona) where there are sharp health policy differences and the healthcare systems in these states are dominated by consolidated hospitals and national insurers.

Three issues will be the primary focus of both campaigns: women’s health and access to abortion, affordability and competition. On women’s health, there are sharp differences; on affordability and competition, the distinctions between the campaigns will be less clear to voters. Both will opine support for policy changes without offering details on what, when and how.

The Affordable Care Act will surface in rhetoric contrasting a ‘government run system’ to a ‘market driven system.’ In reality, both campaigns will favor changes to the ACA rather than repeal.

Both campaigns will voice support for state leadership in resolving abortion, drug pricing and consolidation. State cost containment laws and actions taken by state attorneys general to limit hospital consolidation and private equity ownership will get support from both campaigns.

Neither campaign will propose transformative policy changes: they’re too risky. integrating health & social services, capping total spending, reforms of drug patient laws, restricting tax exemptions for ‘not for profit’ hospitals, federalizing Medicaid, and others will not be on the table. There’s safety in promoting populist themes (price transparency, competition) and steering away from anything more.

As the primary season wears on (in Michigan tomorrow and 23 others on/before March 5), how the health system is positioned in the court of public opinion will come into focus.

Abortion rights will garner votes; affordability, price transparency, Medicare solvency and system consolidation will emerge as wedge issues alongside.

PS: Re: federal budgeting for key healthcare agencies, two deadlines are eminent: March 1 for funding for the FDA and the VA and March 8 for HHS funding.

It’s no secret I feel strongly that “Medicare Advantage for All” is not a healthy end goal for universal health care coverage in our country. But I also recognize there are many folks, across the political spectrum, who see the program as one that has some merit. And it’s not going away anytime soon. To say the insurance industry has clout in Washington is an understatement.

As politicians in both parties increase their scrutiny of Medicare Advantage, and the Biden administration reviews proposed reforms to the program, I think it’s important to highlight common-sense, achievable changes with broad appeal that would address the many problems with MA and begin leveling the playing field with the traditional Medicare program.

1. Align prior authorization MA standards with traditional Medicare

Since my mother entered into an MA plan more than a decade ago, I’ve watched how health insurers have applied practices from traditional employer-based plans to MA beneficiaries. For many years, insurers have made doctors submit a proposed course of treatment for a patient to the insurance company for payment pre-approval — widely known as “prior authorization.”

While most prior authorization requests are approved, and most of those denied are approved if they are appealed, prior authorization accomplishes two things that increase insurers’ margins.

The practice adds a hurdle between diagnosis and treatment and increases the likelihood that a patient or doctor won’t follow through, which decreases the odds that the insurer will ultimately have to pay a claim. In addition, prior authorization increases the length of time insurers can hold on to premium dollars, which they invest to drive higher earnings. (A considerable percentage of insurers’ profits come from the investments they make using the premiums you pay.)

Last year, the Kaiser Family Foundation found the level of prior authorization requests in MA plans increased significantly in recent years, which is partially the result of the share of services subject to prior authorization increasing dramatically. While most requests were ultimately approved (as they were with employer-based insurance plans), the process delayed care and kept dollars in insurers’ coffers longer.

The outrage generated by older Americans in MA plans waiting for prior authorization approvals has moved the Biden administration to action.

Beginning in 2024, MA plans may be no more restrictive with prior authorization requirements than traditional Medicare.

That’s a significant change and one for which Health and Human Services Secretary Xavier Becerra should be lauded.

But as large provider groups like the American Hospital Association have pointed out, the federal government must remain vigilant in its enforcement of this rule. As I wrote about recently with the implementation of the No Surprises Act, well-intentioned legislation and implementation rules put in place by regulators can have little real-world impact if insurers are not held accountable. It’s important to note, though, that federal regulatory agencies must be adequately staffed and resourced to be able to police the industry and address insurers’ relentless efforts to find loopholes in federal policy to maximize profits. Congress needs to provide the Department of Health and Human Services with additional funding for enforcement activities, for HHS to require transparency and reporting by insurers on their practices, and for stakeholders, especially providers and patients, to have an avenue to raise concerns with insurers’ practices as they become apparent.

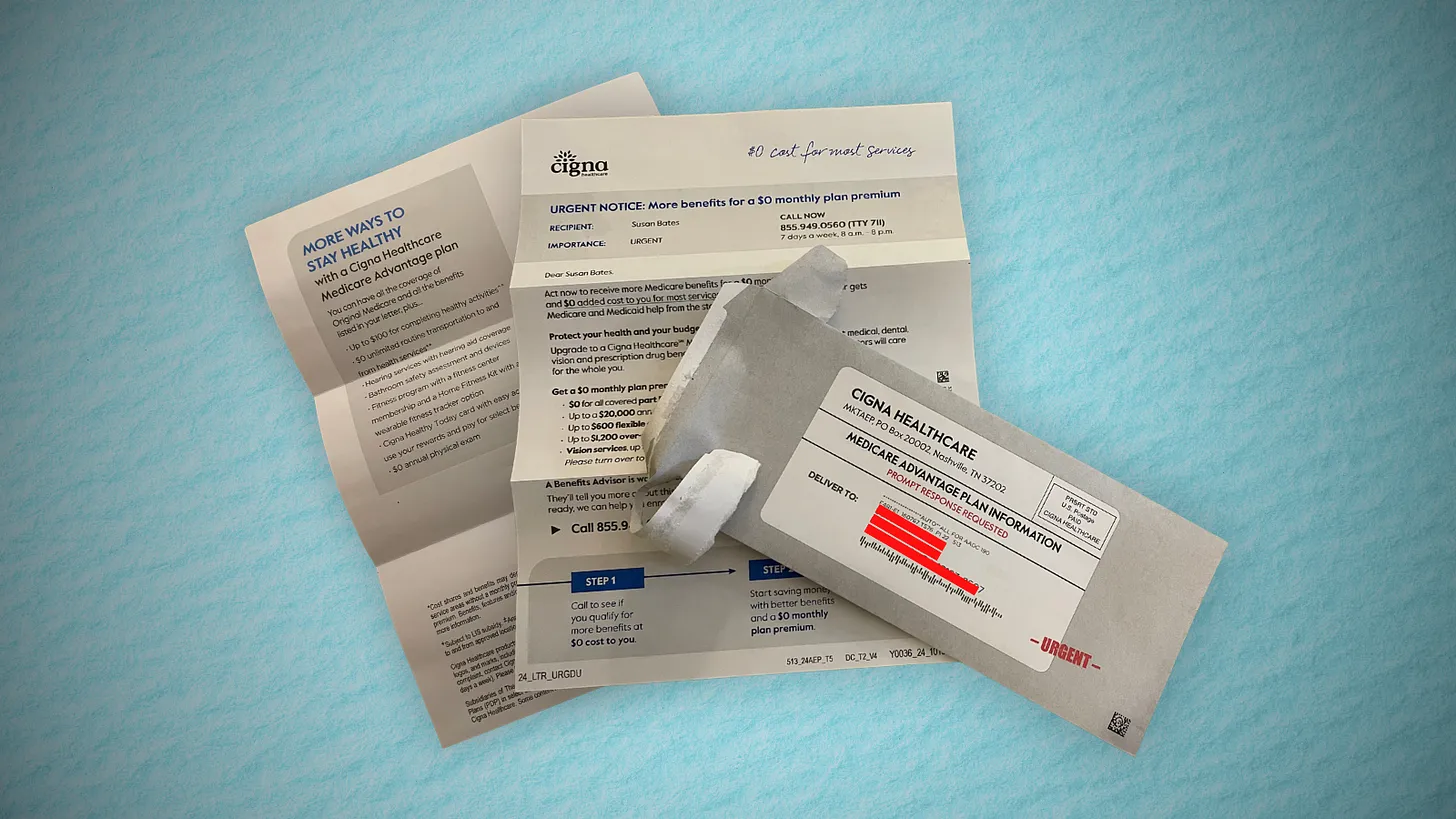

2. Protect seniors from marketing scams

If it’s fall, it’s football season. And that means it’s time for former NFL quarterback Joe Namath’s annual call to action on the airwaves for MA enrollment.

As Congresswoman Jan Schakowsky and I wrote about more than a year ago, these innocent-appearing advertisements are misleading at their best and fraudulent at their worst. Thankfully, this is another area the Biden administration has also been watching over the past year.

CMS now prohibits the use of ads that do not mention a specific plan name or that use the Medicare name and logos in a misleading way, the marketing of benefits in a service area where they are not available, and the use of superlatives (e.g., “best” or “most”) in marketing when not substantiated by data from the current or prior year.

As part of its efforts to enforce the new marketing restrictions, the Center for Medicare and Medicaid Services for the first time evaluated more than 3,000 MA ads before they ran in advance of 2024 open enrollment. It rejected more than 1,000 for being misleading, confusing, or otherwise non-compliant with the new requirements. These types of reviews will, I hope, continue.

CMS has proposed a fixed payment to brokers of MA plans that, if implemented, would significantly improve the problem of steering seniors to the highest-paying plan — with the highest compensation for the insurance broker. I think we can all agree brokers should be required to direct their clients to the best product, not the one that pays the broker the most. (That has been established practice for financial advisors for many years.) CMS should see this rule through, and send MA brokers profiteering off seniors packing.

A bonus regulation in this space to consider: banning MA plan brokers from selling the contact information of MA beneficiaries. Ever wonder why grandma and grandpa get so many spam calls targeting their health conditions? This practice has a lot to do with it. And there’s bipartisan support in Congress for banning sales of beneficiary contact information.

In addition, just as drug companies have to mention the potential side effects of their medications, MA plans should also be required to be forthcoming about their restrictions, including prior authorization requirements, limited networks, and potentially high out-of-pocket costs, in their ads and marketing materials.

3. Be real about supplemental benefits

Tell me if this one sounds familiar. The federal government introduced flexibility to MA plans to offer seniors benefits beyond what they can receive in traditional Medicare funded primarily through taxpayer dollars.

Those “supplemental” benefits were intended to keep seniors active and healthy. Instead, insurers have manipulated the program to offer benefits seniors are less likely to use, so more of the dollars CMS doles out to pay for those benefits stay with payers.

Many seniors in MA plans will see options to enroll in wellness plans, access gym memberships, acquire food vouchers, pick out new sneakers, and even help pay for pet care, believe it or not — all included under their MA plan. Those benefits are paid for by a pot of “rebate” dollars that CMS passes through to plans, with the presumed goal of improving health outcomes through innovative uses.

There is a growing sense, though, that insurers have figured out how to game this system. While some of these offerings seem appealing and are certainly a focus of marketing by insurers, how heavily are they being used? How heavily do insurers communicate to seniors that they have these benefits, once seniors have signed up for them? Are insurers offering things people are actually using? Or are insurers strategically offering benefits that are rarely used?

Those answers are important because MA plans do not have to pay unused rebate dollars back to the federal government.

CMS in 2024 is requiring insurers to submit detailed data for the first time on how seniors are using these benefits. The agency should lean into this effort and ensure plan compliance with the reporting. And as this year rolls on, CMS should be prepared to make the case to Congress that we expect the data to show that plans are pocketing many of these dollars, and they are not significantly improving health outcomes of older Americans.

4. Addressing coding intensity

If you’re a regular reader, you probably know one of my core views on traditional Medicare vs. Medicare Advantage plans. Traditional Medicare has straightforward, transparent payment, while Medicare Advantage presents more avenues for insurers to arbitrarily raise what they charge the government. A good example of this is in higher coding per patient found in MA plans relative to Traditional Medicare.

An older patient goes in to see their doctor. They are diagnosed, and prescribed a course of treatment. Under Traditional Medicare, that service performed by the doctor is coded and reimbursed. The payment is generally the same no matter what conditions or health history that patient brought into the exam room. Straightforward.

MA plans, however, pay more when more codes are added to a diagnosis.

Plans have advertised this to doctors, incentivizing the providers to add every possible code to a submission for reimbursement. So, if that same patient described above has diabetes, but they’re being treated for an unrelated flu diagnosis, the doctor is incentivized by MA to add a code for diabetes treatment. MA plans, in turn, get paid more by the government based on their enrollee’s health status, as determined based on the diagnoses associated with that individual.

Extrapolate that out across tens of millions of seniors with MA plans, and it’s clear MA plans are significantly overcharging the federal government because of over-coding.

One solution I find appealing: similar to fee-for-service, create a new baseline for payments in MA plans to remove the incentive to add more codes to submissions. Proposals I’ve seen would pay providers more than traditional Medicare but without creating the plan-driven incentive for doctors to over-code.

5. Focusing in on Medicare Advantage network cuts in rural areas

Rural America is older and unhealthier than the national average. This should be the area where MA plans should experience the highest utilization.

Instead, we’re seeing that the aggressive practices insurers use to maximize profits force many rural hospitals to cancel their contracts with MA plans. As we wrote about at length in December, MA is becoming a ghost benefit for seniors living in rural communities. The reimbursement rates these plans pay hospitals in rural communities are significantly lower than traditional Medicare. That has further stressed the low margins rural hospitals face.

As Congressional focus on MA grows, I predict more bipartisan recommendations to come forth that address the growing gap between MA plan payments and what hospitals need to be paid in rural areas.

If MA is not accepted by providers in older, rural America, then truly, what purpose does it serve?

If you’re a U.S. health industry watcher, it would appear the $4.5 trillion system is under fire at every corner.

Pressures to lower costs, increase accessibility and affordability to all populations, disclose prices and demonstrate value are hitting every sector. Complicating matters, state and federal legislators are challenging ‘business as usual’ seeking ways to spend tax dollars more wisely with surprisingly strong bipartisan support on many issues. No sector faces these challenges more intensely than hospitals.

In 2022 (the latest year for NHE data from CMS), hospitals accounted for 30.4% of total spending ($1.35 trillion. While total healthcare spending increased 4.1% that year, hospital spending was up 2.2%–less than physician services (+2.7%), prescription drugs (+8.4%), private insurance (+5.9%) and the overall inflation rate (+6.5%) and only slightly less than the overall economy (GDP +1.9%). Operating margins were negative (-.3%) because operating costs increased more than revenues (+7.7% vs. 6.5%) creating deficits for most. Hardest hit: the safety net, rural hospitals and those that operate in markets with challenging economic conditions.

In 2023, the hospital outlook improved. Pre-Covid utilization levels were restored. Workforce tensions eased somewhat. And many not-for-profits and investor-owned operators who had invested their cash flows in equities saw their non-operating income hit record levels as the S&P 500 gained 26.29% for the year.

In 2024, the S&P is up 5.15% YTD but most hospital operators are uncertain about the future, even some that appear to have weathered the pandemic storm better than others. A sense of frustration and despair is felt widely across the sector, especially in critical access, rural, safety net, public and small community hospitals where long-term survival is in question.

The cynicism felt by hospitals is rooted in four conflicts in which many believe hospitals are losing ground:

Hospitals vs. Insurers:

Insurers believe hospitals are inefficient and wasteful, and their business models afford them the role of deciding how much they’ll pay hospitals and when based on data they keep private. They change their rules annually to meet their financial needs. Longer-term contracts are out of the question. They have the upper hand on hospitals.

Hospitals take financial risks for facilities, technologies, workforce and therapies necessary to care. Their direct costs are driven by inflationary pressures in their wage and supply chains outside their control and indirect costs from regulatory compliance and administrative overhead, Demand is soaring. Hospital balance sheets are eroding while insurers are doubling down on hospital reimbursement cuts to offset shortfalls they anticipate from Medicare Advantage. Their finances and long-term sustainability are primarily controlled by insurers. They have minimal latitude to modify workforces, technology and clinical practices annually in response to insurer requirements.

Hospitals vs. the Drug Procurement Establishment:

Drug manufacturers enjoy patent protections and regulatory apparatus that discourage competition and enable near-total price elasticity. They operate thru a labyrinth of manufacturers, wholesalers, distributors and dispensers in which their therapies gain market access through monopolies created to fend-off competition. They protect themselves in the U.S. market through well-funded advocacy and tight relationships with middlemen (GPOs, PBMs) and it’s understandable: the global market for prescription drugs is worth $1.6 trillion, the US represents 27% but only 4% of the world population.

And ownership of the 3 major PBMs that control 80% of drug benefits by insurers assures the drug establishment will be protected.

Prescription drugs are the third biggest expense in hospitals after payroll and med/surg supplies. They’re a major source of unexpected out-of-pocket cost to patients and unanticipated costs to hospitals, especially cancer therapies. And hospitals (other than academic hospitals that do applied research) are relegated to customers though every patient uses their products.

Prescription drug cost escalation is a threat to the solvency and affordability of hospital care in every community.

Hospitals vs. the FTC, DOJ and State Officials:

Hospital consolidation has been a staple in hospital sustainability and growth strategies. It’s a major focus of regulator attention. Horizontal consolidation has enabled hospitals to share operating costs thru shared services and concentrate clinical programs for better outcomes. Vertical consolidation has enabled hospitals to diversify as a hedge against declining inpatient demand: today, 200+ sponsor health insurance plans, 60% employ physicians directly and the majority offer long-term, senior care and/or post-acute services. But regulators like the FTC think hospital consolidation has been harmful to consumers and third-party data has shown promised cost-savings to consumers are not realized.

Federal regulators are also scrutinizing the tax exemptions afforded not-for-profit hospitals, their investment strategies, the roles of private equity in hospital prices and quality and executive compensation among other concerns. And in many states, elected officials are building their statewide campaigns around reining in “out of control” hospitals and so on.

Bottom line: Hospitals are prime targets for regulators.

Hospitals vs. Congress:

Influential members in key House and Senate Committees are now investigating regulatory changes that could protect rural and safety net hospitals while cutting payments to the rest. In key Committees (Senate HELP and Finance, House Energy and Commerce, Budget), hospitals are a target. Example: The Lower Cost, More Transparency Act passed in the the House December 11, 2023. It includes price transparency requirements for hospitals and PBMs, site-neutral payments, additional funding for rural and community health among more. The American Hospital Association objected noting “The AHA supports the elimination of the Medicaid disproportionate share hospital (DSH) reductions for two years. However, hospitals and health systems strongly oppose efforts to include permanent site-neutral payment cuts in this bill. In addition, the AHA has concerns about the added regulatory burdens on hospitals and health systems from the sections to codify the Hospital Price Transparency Rule and to establish unique identifiers for off-campus hospital outpatient departments (HOPDs).” Nonetheless, hospitals appear to be fighting an uphill battle in Congress.

Hospitals have other problems:

Threats from retail health mega-companies are disruptive. The public’s trust in hospitals has been fractured. Lenders are becoming more cautious in their term sheets. And the hospital workforce—especially its doctors and nurses—is disgruntled. But the four conflicts above seem most important to the future for hospitals.

However, conflict resolution on these is problematic because opinions about hospitals inside and outside the sector are strongly held and remedy proposals vary widely across hospital tribes—not-for profits, investor-owned, public, safety nets, rural, specialty and others.

Nonetheless, conflict resolution on these issues must be pursued if hospitals are to be effective, affordable and accessible contributors and/or hubs for community health systems in the future. The risks of inaction for society, the communities served and the 5.48 million (NAICS Bureau of Labor 622) employed in the sector cannot be overstated. The likelihood they can be resolved without the addition of new voices and fresh solutions is unlikely.

PS: In the sections that follow, citations illustrate the gist of today’s major message: hospitals are under attack—some deserved, some not. It’s a tough business climate for all of them requiring fresh ideas from a broad set of stakeholders.

PS If you’ve been following the travails of Mission Hospital, Asheville NC—its sale to HCA Healthcare in 2019 under a cloud of suspicion and now its “immediate jeopardy” warning from CMS alleging safety and quality concerns—accountability falls squarely on its Board of Directors. I read the asset purchase agreement between HCA and Mission: it sets forth the principles of operating post-acquisition but does not specify measurable ways patient safety, outcomes, staffing levels and program quality will be defined. It does not appear HCA is in violation with the terms of the APA, but irreparable damage has been done and the community has lost confidence in the new Mission to operate in its best interest. Sadly, evidence shows the process was flawed, disclosures by key parties were incomplete and the hospital’s Board is sworn to secrecy preventing a full investigation.

The lessons are 2 for every hospital:

Boards must be prepared vis a vis education, objective data and independent counsel to carry out their fiduciary responsibility to their communities and key stakeholders. And the business of running hospitals is complex, easily prone to over-simplification and misinformation but highly important and visible in communities where they operate.

Business relationships, price transparency, board performance, executive compensation et al can no longer to treated as private arrangements.

Jayne Kleinman is bombarded with Medicare Advantage promotions every open enrollment period — even though she has no interest in leaving traditional Medicare, which allows seniors to choose their doctors and get the care they want without interference from multi-billion-dollar insurance companies.

“My biggest problem with being barraged is that so many of the ads were inaccurate,” Kleinman, a retired social services professional in New Haven County, Connecticut, told HEALTH CARE un-covered.

“They neglect to say that the amount of coverage you get is limited. They don’t talk about what you are losing by leaving traditional Medicare. It feels like insurance companies are manipulating us to get Medicare Advantage plans sold so that they can control the system, as opposed to treating us like human beings.”

Seniors face a torrent of Medicare Advantage advertising: an analysis by KFF found 9,500 daily TV ads during open enrollment in 2022. A recent survey by the Commonwealth Fund found that 30% of seniors received seven or more phone calls weekly from Medicare Advantage marketers during the most recent open enrollment (Oct. 15 to Dec. 7) for 2024 coverage.

In 2023, a critical milestone was passed: over half of seniors are now enrolled in privatized Medicare Advantage plans. The marketing for these plans nearly always fails to mention how hard it is to return to traditional Medicare once you are in Medicare Advantage, and that the MA plans have closed provider networks and require prior authorization for medical procedures. Instead, the marketing emphasizes the fringe benefits offered by Medicare Advantage plans like gym memberships.

U.S. Sen. Ron Wyden (D-Ore.), chairman of the Senate Finance Committee, criticized the widespread and predatory marketing of Medicare Advantage in a report in November 2022 and has continued to pressure the Biden administration to do more to address the problem.

The report said that consumer complaints about Medicare Advantage marketing more than doubled from 2020 to 2021 to 41,000. It cites cases such as that of an Oregon man whose switch to Medicare Advantage meant he could no longer afford his prescription drugs, as well as a 94-year-old woman with dementia in a rural area who bought a Medicare Advantage plan that required her to obtain care miles further from her residence than she had to travel before.

When open enrollment began last fall, it was “the start of a marketing barrage as marketing middlemen look to collect seniors’ information in order to bombard them with direct mail, emails, and phone calls to get them to enroll,” Wyden stated in a letter to the Centers for Medicare and Medicaid Services (CMS), which was signed by the other Democrats on the Senate Finance Committee.

Just three weeks after Wyden sent the letter, CMS released a proposed rule reforming Medicare Advantage practices that the main lobby group for Medicare Advantage plans, the Better Medicare Alliance, endorsed.

But key recommendations by Wyden were missing, including a ban on list acquisition by Medicare Advantage third-party marketing organizations, which includes brokers, and banning brokers that call beneficiaries multiple times a day for days in a row.

Among the prominent third-party marketing organizations is TogetherHealth, a subsidiary of Benefytt Technologies, which runs ads featuring former football star Joe Namath.

In August 2022, the Federal Trade Commission forced Benefytt to repay $100 million for fraudulent activities. The month before, the Securities and Exchange Commission levied more than $12 million in fines against Benefytt.

But CMS continues to allow Benefytt to work as a broker. Benefytt is owned by Madison Dearborn Partners, a Chicago-based private equity firm with ties to former Chicago mayor and current Ambassador to Japan Rahm Emanuel. Benefytt collects leads on potential customers, which they then sell to brokers and insurers to aggressively target seniors. CMS did not provide comment as to why they had not blocked Benefytt’s continuing work as a third-party marketing organization for Medicare.

Two different rounds of rule-making on Medicare Advantage marketing in 2023 instead focused on such reforms as reining in exaggerated claims and excessive broker compensation.

The enormous profits generated by Medicare Advantage plans — costing the federal government as much as $140 billion annually in overpayments to private companies — explains what drives the aggressive and often unethical marketing practices, said David Lipschutz, an associate director at the Center for Medicare Advocacy.

“The fact is, there is an increasingly imbalanced playing field between Medicare Advantage and traditional Medicare,” he said. “Medicare Advantage is being favored in many ways. Medicare Advantage plans are paid more than what traditional Medicare spends on a given beneficiary.

Those factors combined with the fact that they generate such profits for insurance companies, leads to those companies doing everything they can to maximize enrollment.”

Adding to the problem, Lipschutz argued, was the enormous influence of the health insurance industry in Washington. Health insurers spent more than $33 million lobbying Washington in just the first three quarters of 2023 alone.

“There is no real organized lobby for traditional Medicare, or organized advertising efforts,” he said. “During open enrollment, 80% of Medicare-related ads have to do with Medicare Advantage. We regularly encounter very well-educated and savvy folks who are tripped up by advertising and lured in by the bells and whistles. The deck is stacked against the consumer.”

Private equity firms have made a large investment in the Medicare Advantage brokerage and marketing sector, in addition to Madison Dearborn’s acquisition of Benefytt. Bain Capital, which Sen. Mitt Romney (R-Utah) co-founded, invested $150 million in Enhance Health, a Medicare Advantage broker, in 2021.

The CEO of EasyHealth, another private equity-backed brokerage, toldModern Healthcare in 2021 that “Insurance distribution is our Trojan horse into healthcare services.”

As federal law requires truth in advertising, a group of advocacy organizations–led by the Center for Medicare Advocacy, Disability Rights Connecticut, and the National Health Law Project–cited what they considered blatantly deceptive marketing by UnitedHealthcare to people who are eligible for both Medicare and Medicaid, in a complaint to CMS.

UnitedHealthcare had purchased ads in the Hartford Courant asking seniors in large bold-faced type: “Eligible for Medicare and Medicaid? You could get more with UnitedHealthcare.”

People who are eligible for both Medicare and Medicaid due to their income level are better off in traditional Medicare than Medicare Advantage given that Medicaid covers their out-of-pocket costs, meaning that they have wide latitude to choose their doctors, hospitals and medical procedures.

Sheldon Toubman, an attorney with Disability Rights Connecticut who worked to draft the complaint, framed the ad in the broader context of poor marketing practices by the Medicare Advantage industry.

“I have been aware for a long time of basically fraudulent advertising in the MA insurance industry,” Toubman told HEALTH CARE un-covered. “There’s an overriding misrepresentation — they tell you how great Medicare Advantage is, and never the downsides.

“There are two big downsides of going out of traditional Medicare:

They don’t tell you that you give up the broad Medicare provider network, which has nearly every doctor. And should you need expensive medical care in Medicare Advantage, you will learn there are prior authorization requirements. Traditional Medicare does almost no prior authorization, so you don’t have that obstacle. They don’t ever tell you any of that,” he said.

But it is marketing to dual-eligible individuals that is arguably the most problematic, Toubman argued. “They have Medicare and they are also low income. Because they are low-income, they also have Medicaid.

“Medicaid is a broader program — it covers a lot of things that Medicare doesn’t cover.

In Connecticut, 92,000 dual-eligible seniors have been ‘persuaded’ to sign up for Medicare Advantage. What’s outrageous about the marketing is they get you to sign up by offering extra services. … If you look at the ad in the Hartford Courant, it says you could get more, with the only real benefit being $130 per month toward food. But you now have this problem of a more limited provider network and prior authorization. UnitedHealth is doing false advertising.”

It’s a nationwide problem, Toubman said. “All insurers are doing this everywhere. We’re asking CMS and the Federal Trade Commission to conduct a nationwide investigation of this kind of problem. The failure to tell people that they give up their broader Medicare network — they don’t tell anybody that.”

For Jayne Kleinman, the unending ads are about one thing only: insurance industry profits. “Medicare Advantage has been strictly based on the people who make millions of dollars at the top of the company making more,” she said. “It’s all about money, not about you as an individual. Every time I saw an ad I’d get angry every single time — because I felt they were misleading people. The Medicare Advantage insurers are trying to scam people out of an interest of making money.”